Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

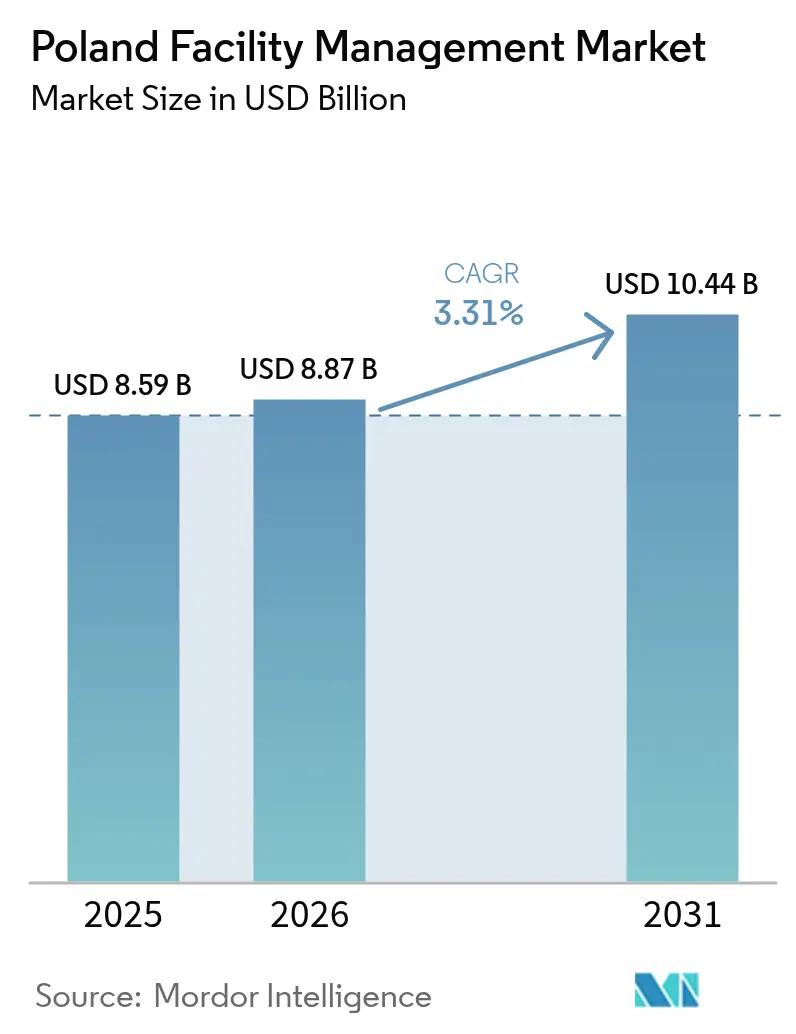

| Base Year Market Size (2025) | USD 8.59 Billion |

| Market Size (2026) | USD 8.87 Billion |

| Market Size (2031) | USD 10.44 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

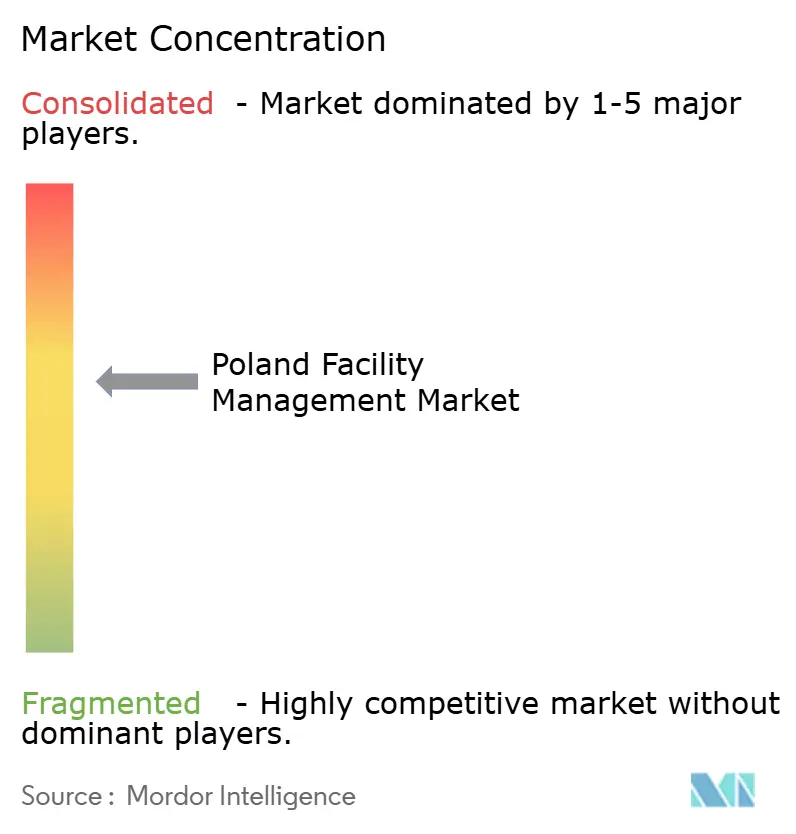

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Facility Management Market Analysis by Mordor Intelligence

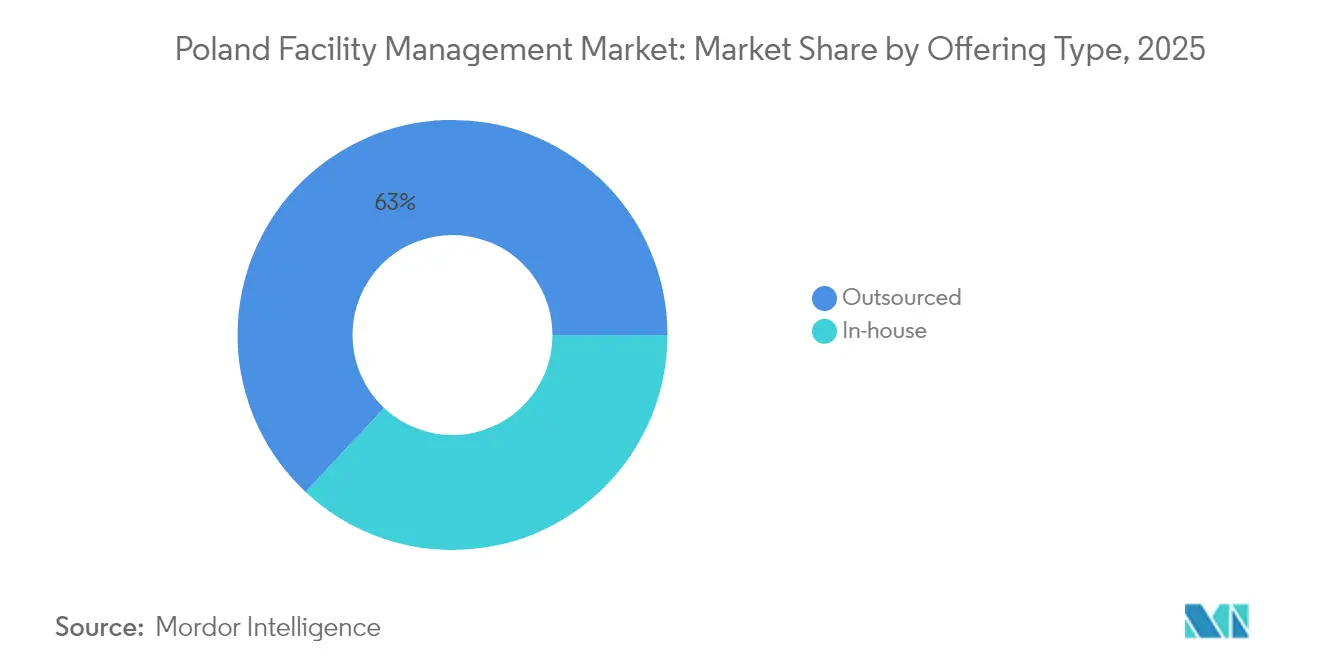

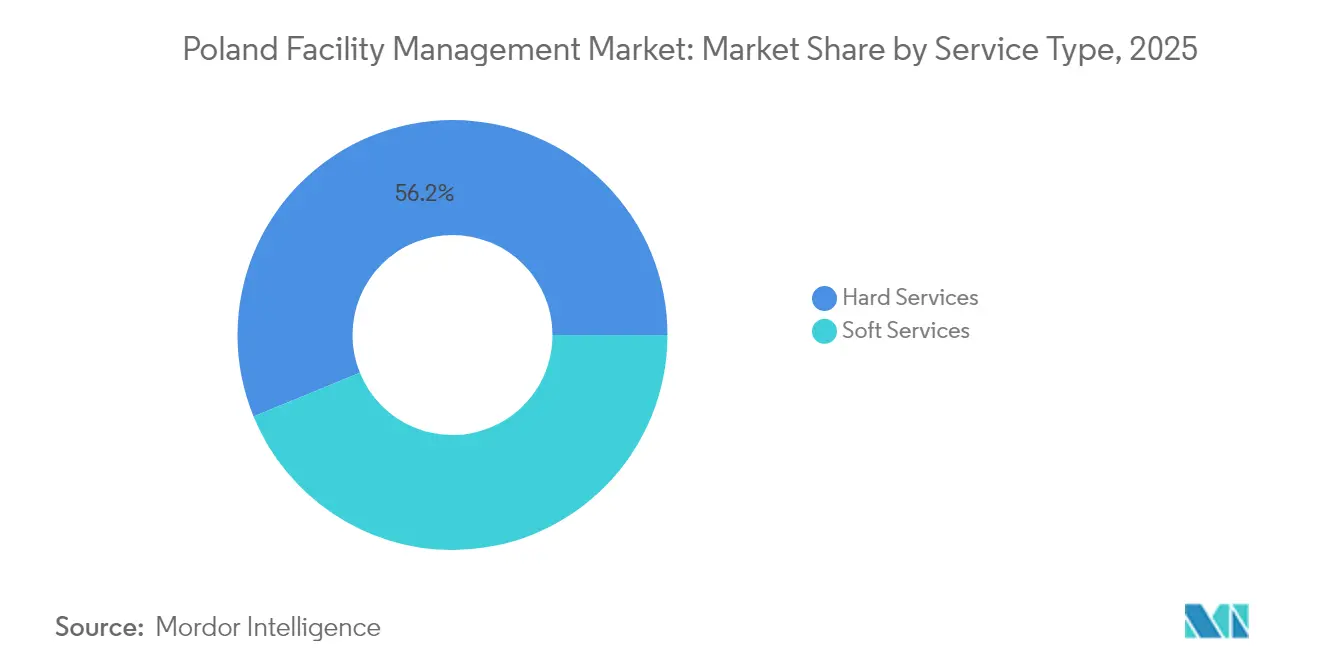

Poland facility management market size in 2026 is estimated at USD 8.87 billion, growing from 2025 value of USD 8.59 billion with 2031 projections showing USD 10.44 billion, growing at 3.31% CAGR over 2026-2031. This expansion has been anchored by a PLN 700 billion national investment pipeline, a decisive corporate pivot toward outsourcing, and persistent infrastructure modernization. Outsourced services commanded 63.7% of the Poland facility management market in 2024, indicating a structurally entrenched client preference for professional operators that can navigate tightening labor and safety rules. Hard services led with a 56.9% revenue share, yet soft services expanded more vigorously at 4.9% CAGR, aided by hybrid-office adoption and workplace-experience upgrades. Commercial real-estate demand, particularly Grade-A offices in Warsaw, Kraków, and Wrocław, bolstered service volume, while the institutional and public-infrastructure segment emerged as the fastest-growing end user on the back of EU-funded energy retrofit programs. Provider margins, however, continued to compress as wage inflation outpaced contract indexation, prompting accelerated technology investment in IoT-enabled monitoring and digital-twin solutions.

Key Report Takeaways

- By service type, hard services held 56.18% of the Poland facility management market share in 2025, whereas soft services are projected to grow at a 4.72% CAGR through 2031.

- By offering type, outsourced models accounted for 63.02% of the Poland facility management market size in 2025 and are forecast to expand at a 4.32% CAGR to 2031.

- By end-user industry, the commercial segment led with 37.34% revenue share in 2025, while institutional and public infrastructure are advancing at a 4.74% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate shift toward outsourcing non-core building operations | +1.2% | Global, with early gains in Warsaw, Kraków, Wrocław | Medium term (2-4 years) |

| Expansion of Grade-A commercial real estate stock and occupancy in major Polish metros | +0.8% | Warsaw, Kraków, Łódź, Wrocław, Poznań | Short term (≤ 2 years) |

| National infrastructure pipeline boosting long-term O&M requirements | +1.0% | National, with a concentration in transport corridors | Long term (≥ 4 years) |

| Tightening labour and safety-standard regulations mandating professional FM compliance | +0.6% | National, with stricter enforcement in major metros | Medium term (2-4 years) |

| EU-funded public-building energy-retrofit programs driving integrated FM demand | +0.9% | National, with priority in public sector facilities | Medium term (2-4 years) |

| Investor pushes for ESG-aligned FM services linked to EU Taxonomy disclosure | +0.7% | APAC core, spill-over to major commercial hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate shift toward outsourcing non-core building operations

By 2025, many large enterprises had bundled cleaning, security, and maintenance into integrated contracts that delivered 15-20% cost savings versus in-house teams.[1]ABSL Poland, “HR Market Trends in the SSC Sector,” ABSL.PL Outsourcing proved particularly attractive to shared-services centres employing more than 400,000 professionals, where salary inflation of 7-8% per year forced executives to contain non-personnel spending. Certified FM partners also mitigated compliance risk under Poland’s occupational health regime, which mandates periodic safety training for every job class. As hybrid work patterns stabilised, demand rose for flexible service scopes that could scale with fluctuating occupancy.

Expansion of Grade-A commercial real-estate stock and occupancy in major Polish metros

Warsaw alone recorded 286,700 sqm of net absorption in 2022, almost triple the 2021 levels. A 140% rebound in commercial-property investments to EUR 5 billion (USD 5.81 billion) in 2024 signalled renewed landlord confidence. Developers prioritised energy-efficient buildings to satisfy tenant ESG mandates, prompting FM providers to deploy sensor-driven HVAC optimisation that cut energy bills by up to 35%. Higher specification assets require continuous MEP oversight, reinforcing hard-services demand across the Poland facility management market.

National infrastructure pipeline boosting long-term O&M requirements

The PLN 700 billion (USD 190.84 billion) public-investment agenda unveiled for 2025 earmarked PLN 180 billion for railway upgrades and PLN 65 billion (USD 17.72 billion) for energy-grid modernisation. The Central Communication Port project alone involves PLN 44.7 billion (USD 12.19 billion) for Europe’s largest intermodal hub, slated to handle 34 million passengers annually by 2032. These assets demand multi-decade O&M contracts that favour FM firms with nationwide technical capacity and transport-sector know-how.

Tightening labour- and safety-standard regulations mandating professional FM compliance

Minimum-wage rises to PLN 4,242 gross in January 2024, and stricter building-code updates in August 2024 elevated compliance complexity for owners. State Labour Inspection spot-checks expanded, exposing companies without certified FM support to penalties. Consequently, organisations increasingly relied on external providers accredited in OHS, fire safety, and accessibility standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid wage inflation is eroding FM provider profit margins | -0.9% | National, with acute pressure in major metros | Short term (≤ 2 years) |

| Highly fragmented subcontractor base causing service-quality variability | -0.6% | National, with a concentration in construction-heavy regions | Medium term (2-4 years) |

| Slow digital-tool adoption among legacy public-sector facilities | -0.4% | National, with particular challenges in smaller municipalities | Long term (≥ 4 years) |

| Out-migration of certified technical staff, creating hard-services skill gaps | -0.8% | National, with a severe impact in border regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid wage inflation eroding FM provider profit margins

Construction firms offered 20% pay hikes and referral bonuses in 2024 to fill a 100,000-worker gap, pushing labour costs well above contract indexation. Labour typically forms 60-70% of service expenditure in the Poland facility management market, so providers faced sharp margin compression when annual price escalators remained tied to headline inflation rather than wage trends. In metropolitan areas, intense competition for licensed technicians further lifted salaries, compelling FM firms to accelerate automation and renegotiate multi-year agreements.

Highly fragmented subcontractor base causing service-quality variability

The European Labour Authority flagged Poland’s construction sector for widespread use of small subcontractors and inconsistent labour standards that complicated oversight.[2]European Labour Authority, “Construction-Sector Report 2023,” ELA.EUROPA.EU FM primes spent more on vetting and training to assure uniform quality across mechanical, electrical, and fire-safety works. Fragmentation also limited scalability, hampering consistent delivery for clients with nationwide footprints and tempering growth potential in the Poland facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering Type: outsourced leadership, integrated FM acceleration

Outsourcing captured 63.02% revenue share in 2025 and is on track for a 4.32% CAGR through 2031 as corporates shifted non-core functions to external specialists. Shared-services centres reported cost efficiencies of up to 20% after transitioning to multi-service contracts. In-house delivery persisted in high-security environments such as defence plants and select public assets but remained cost-intensive. Within outsourcing, integrated FM rose fastest; single-provider models reduced interface risk and enabled consistent ESG reporting, a key investor demand under the EU taxonomy. Bundled FM solutions appealed to mid-sized firms seeking economies of scope without full contract complexity, while single-service deals continued where niche expertise or liability concerns prevailed.

Providers scaled through technology: IoT tags tracked asset utilisation, and digital twins simulated building behaviour to optimise preventive schedules. Kraków-based Kontakt.io secured EUR 12 million (USD 13.92 million) from the European Investment Bank in 2024 to deploy such solutions, delivering up to 35% power savings in pilot facilities. Automation’s promise to ease labour pressure further entrenched the outsourced share in the Poland facility management market.

By End-user Industry: commercial scale, public-sector velocity

Commercial real estate, led by offices, retail, and logistics, contributed 37.34% of 2025 revenue. Warsaw’s Grade-A absorption and EUR 5 billion (USD 5.81 billion) investment turnaround in 2024 underpinned FM volumes, while warehouse stock surpassed 31.5 million m² as e-commerce matured. Corporate occupiers demanded sophisticated energy dashboards and occupancy analytics, elevating the technical content of service contracts. Hotels and mixed-use complexes emphasised brand-consistent guest experiences, blending hard and soft services in outcome-based frameworks.

Institutional and public-infrastructure facilities are projected to grow 4.74% CAGR, lifted by EUR 15.51 billion (USD 18.03 billion) for green-energy projects under Poland’s Recovery and Resilience. Energy-retrofit grants spurred demand for integrated FM that could document carbon reductions. Healthcare settings require infection-control protocols and medical-equipment maintenance, commanding premium pricing for certified operators. Industrial and process plants invested in Industry 4.0 and required continuous uptime support, maintaining stable demand for hard-skills capacity in the Poland facility management industry.

By Service Type: hard-services dominance, soft-services momentum

Hard services accounted for 56.18% of revenue in 2025, underpinned by large-scale rail and energy projects that required specialised MEP maintenance, asset management, and fire-protection systems. The segment’s scale places it at the core of the Poland facility management market, especially as infrastructure assets age and require lifecycle support. Soft services grew faster, at a 4.72% CAGR by 2031, thanks to employers' focus on health, cleanliness, and occupant experience in flexible office environments. Integrated workplace programmes bundled cleaning, reception, catering, and minor technical tasks into single-invoice solutions, supporting user experience while managing cost volatility. As environmental standards tightened, cleaning protocols increasingly specified microfibre technologies and eco-label chemicals, elevating skill levels and documentation requirements.

A growing share of hard-services contracts incorporated performance-based clauses that tied provider remuneration to energy-consumption targets. Case studies in public-school retrofits recorded 35-46% utility savings after HVAC and envelope upgrades. These outcomes validated data-driven maintenance strategies and strengthened demand for predictive analytics platforms across the Poland facility management market at the sub-segment level. Soft-services providers likewise adopted real-time occupancy sensors to align cleaning frequency with actual footfall, securing labour savings that partly offset wage inflation.

Geography Analysis

Warsaw generated a significant share of national revenue in 2024, drawing on its 400,000-strong business-services workforce and high-grade office stock. Net absorption growth and sustained occupancy above 90% in prime zones underpinned service volumes, while major multinationals signed long-term integrated FM contracts covering multi-tower campuses. Kraków followed as the second-largest hub, benefitting from sizable technology tenants and a 4.2% historical CAGR in FM services from 2019-2024. Wrocław, Gdańsk, and Poznań collectively accounted for roughly 40% of demand, each supported by logistics corridors and university clusters that attracted foreign direct investments.

Eastern Poland advanced at a prominent CAGR to 2030, stimulated by PLN 2.4 billion (USD 0.66 billion) in EU-funded road projects that opened new industrial parks. Łódź emerged as an investment alternative to capital-city costs, leveraging improved rail links and lower office rents. The Silesian region sustained steady contracts from heavy industry and mining, while coastal markets such as Gdańsk and Szczecin expanded through port modernisation. Smaller municipalities faced legacy-building migration issues and slower digital adoption, inviting FM providers to roll out scalable, cloud-based platforms capable of remote diagnostics.

Inter-regional portfolios became more common as domestic investors entered multiple voivodeships. Clients demanded consistent service-level metrics, pushing FM companies to standardise procedures and centralise help-desk operations across the Poland facility management market. Automated asset registers and mobile workflows supported field teams dispersed over wide territories, reducing travel time and ensuring compliance uniformity.

Competitive Landscape

The ten largest players controlled the majority of revenue in 2024, indicating moderate concentration. Global brands such as ISS Facility Services Polska, Sodexo Polska, and Compass Group Poland leveraged international best practices, technology suites, and multi-country client relationships to secure large contracts. Local champions Impel Group and OKIN Facility Poland competed on price flexibility and regional familiarity. All tiers invested in digital solutions: smart sensors, machine-learning-based maintenance scheduling, and centralised energy-management dashboards. The skilled-labour deficit intensified automation economics; contactless cleaning robots and AI-guided workforce-management tools entered pilot operations, trimming low-value manual tasks.

ESG capability became a key differentiator. Providers with demonstrable carbon-saving metrics won public-sector tenders tied to EU taxonomy disclosures. For instance, ISS appointed a Group Head of ESG in July 2024 to embed sustainability across service lines.[4]ISS A/S, “ISS Appoints Signe Adamsen as New Group Head of ESG,” ISSWORLD.COM Meanwhile, Sescom attracted new investors in May 2024 to finance European expansion and strengthen energy-performance contracts abroad. M&A discussions intensified around specialist technical firms, as integrated FM suppliers sought to deepen hard-services competencies and reduce reliance on volatile subcontractors.

Pressure on margins steered the market toward outcome-based pricing. Contracts increasingly tie payments to uptime, energy, or satisfaction metrics instead of labour hours, aligning incentives and rewarding technology innovation. Investors valued providers capable of scaling these models, supporting continued consolidation and reinforcing the ascendancy of integrated solutions within the Poland facility management market.

Poland Facility Management Industry Leaders

ISS Facility Services Polska

Sodexo Polska Sp. z o.o.

Impel Group

Compass Group Poland

Engie Services FM Poland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Dec 2024: CPK and Polish Airports agreed on PLN 44.7 billion for a central airport capable of 34 million passengers per year.

- July 2024: ISS A/S named Signe Adamsen Group Head of ESG to embed sustainability across global operations.

- May 2024: Sescom secured new equity to extend its European service footprint, following its entry into the UK market.

- March 2024: Poland’s commercial-property transactions hit EUR 5 billion, signalling renewed investor appetite that lifted FM service demand.

Poland Facility Management Market Report Scope

Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. While hard services include physical and structural services like fire alarm system lifts, among others, soft services include cleaning, landscaping, security, and similar human-sourced services, providing a solution to end-users such as commercial buildings, retail, and government, public entities, etc.

The Poland facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehousing) |

| Hospitality (Hotels, Eateries and Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehousing) | |

| Hospitality (Hotels, Eateries and Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

Key Questions Answered in the Report

What is the current value of the Poland facility management market?

The market was valued at USD 8.87 billion in 2026 and is projected to reach USD 10.44 billion by 2031.

Which service type dominates Poland’s facility management contracts?

Hard services led with 56.18% revenue share in 2025, driven by intensive infrastructure and technical maintenance needs.

Why are outsourced models preferred in Poland?

Outsourced services delivered cost reductions of 15-20% versus in-house teams and simplified compliance with labour and safety regulations.

Which end-user segment is expanding fastest?

Institutional and public-infrastructure facilities are forecast to grow at a 4.74% CAGR on the back of EU-funded energy retrofits and green-building mandates.

How is technology altering service delivery?

IoT sensors, digital twins, and AI-driven maintenance have reduced energy bills by up to 35% and mitigated labour shortages.

What labour challenges affect FM providers?

Wage inflation of up to 20% and migration of certified technicians compress margins and spur automation investments.

Page last updated on: