Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

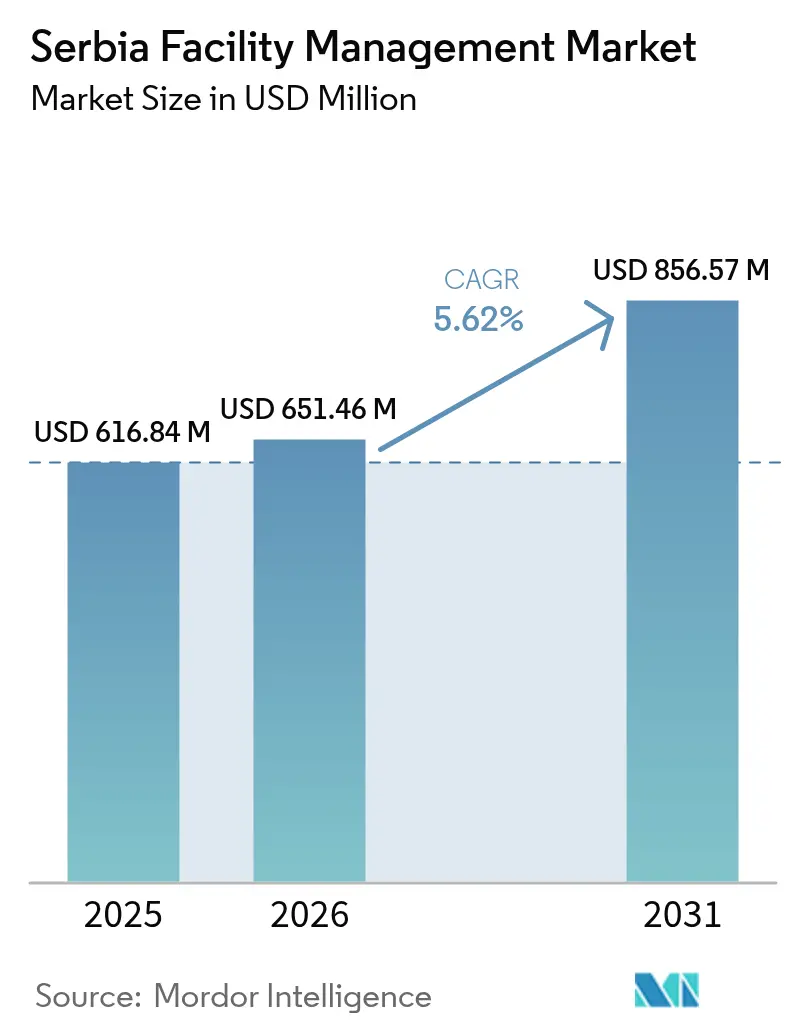

| Base Year Market Size (2025) | USD 616.84 Million |

| Market Size (2026) | USD 651.46 Million |

| Market Size (2031) | USD 856.57 Million |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

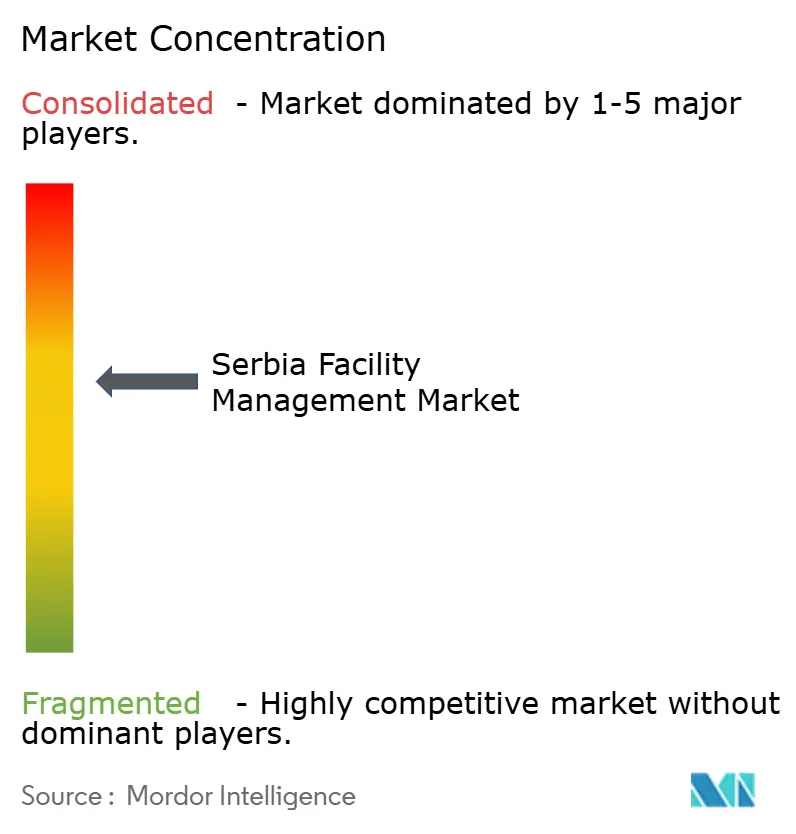

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Serbia Facility Management Market Analysis by Mordor Intelligence

The Serbia facility management market size was valued at USD 616.84 million in 2025 and estimated to grow from USD 651.46 million in 2026 to reach USD 856.57 million by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). Serbia’s investment-grade credit rating in late 2024 triggered EUR 5.2 billion in foreign direct investment that is feeding sustained demand for Grade A offices, logistics hubs and related integrated services.[1]Jorgovanka Tabaković, “Serbia 2027 – striving towards a high-income economy,” Bank for International Settlements, bis.org The EU Economic and Investment Plan is channeling EUR 9 billion into transport, energy and environmental projects, anchoring a long pipeline of public-sector assets that now require professionally managed operations. Large multinationals nearshoring shared-service and IT centers to Belgrade and Novi Sad are deepening the shift from cost-based cleaning or security contracts to outcome-based, tech-enabled facility bundles. At the same time, Serbia’s Integrated National Energy and Climate Plan is accelerating retrofits toward nearly zero-energy buildings, forcing owners to embed energy-optimization clauses in new facility contracts.

Key Report Takeaways

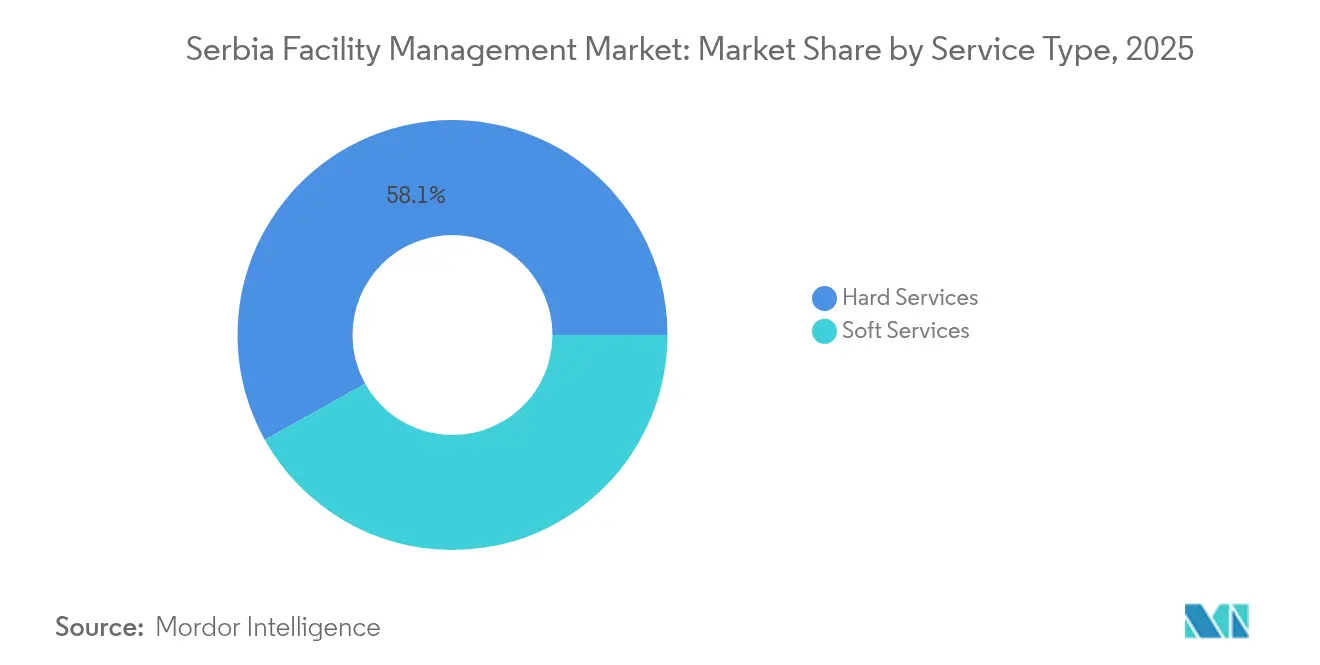

- By service type, Hard Services captured 58.10% of Serbia facility management market share in 2025, while Soft Services are advancing at a 5.85% CAGR through 2031.

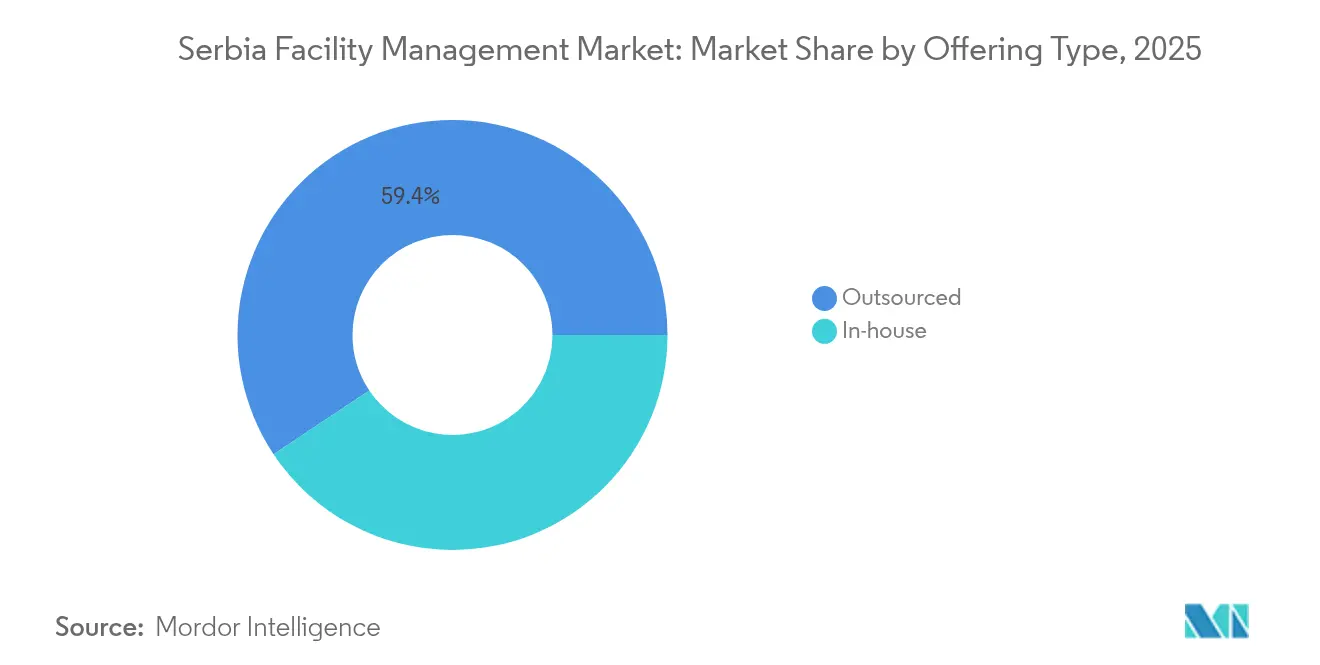

- By offering type, the Outsourced model accounted for 59.35% share of the Serbia facility management market size in 2025 and is expanding at a 6.05% CAGR over 2026-2031.

- By end-user industry, Commercial facilities led with 35.70% revenue share in 2025; Institutional & Public Infrastructure is forecast to post the fastest 6.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Serbia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing preference among corporates | +1.2% | National (Belgrade, Novi Sad) | Medium term (2-4 years) |

| Expansion of Grade-A office & logistics stock | +1.5% | Belgrade and secondary cities | Short term (≤2 years) |

| EU-backed infrastructure modernization | +1.0% | National urban centers | Long term (≥4 years) |

| Demand for certified green buildings | +0.8% | Belgrade, Novi Sad, Niš | Medium term (2-4 years) |

| Nearshoring influx of shared-service & IT hubs | +1.1% | Belgrade, Novi Sad, Kragujevac | Short term (≤2 years) |

| Government digitalization driving smart FM | +0.6% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing outsourcing preference among Serbian corporates

Firms are reallocating scarce talent toward core, high-margin tasks and handing non-core activities to external specialists that can guarantee compliance with EU standards.[1]World Bank Group, “Green, Livable, Resilient Cities in Serbia Program,” worldbank.orgForeign-owned plants inside free economic zones now insist on globally harmonized facility protocols, accelerating bundled contracts for cleaning, security and energy management. Rising administrative-burden reforms and a shortage of credentialed facility engineers further tilt the cost-benefit equation toward outsourcing.

Expansion of Grade-A office and logistics real estate stock

Belgrade exceeds 1.1 million m² of modern offices, with Airport City alone set to hit 230,000 m², each building demanding 24/7 MEP, HVAC and smart-system oversight. Active-office designs featuring flexible zones and 40% lower energy use make predictive maintenance and occupant-wellness metrics standard service-level items.

EU-backed public infrastructure modernization pipeline

Projects such as the EUR 730 million PPF8 transport and environment program expand the asset base needing lifecycle maintenance plans, asset-register digitization and warranty tracking. [3]Ministry of European Integration, “Project Preparation Facilities,” mei.gov.rs Digital-governance reforms funded by a USD 50 million World Bank loan embed IoT devices in public buildings, compelling authorities to procure integrated facility platforms.

Rising demand for certified green & energy-efficient buildings

Serbia’s roadmap toward nearly zero-energy public buildings mandates real-time energy dashboards, fault detection and carbon reporting protocols that most owners source from specialist FM providers. [4]United Nations Development Programme, “Roadmap: Nearly Zero-Energy Pathway,” undp.orgThe Integrated National Energy and Climate Plan pushes 3.5 GW of renewables by 2030, sharpening scrutiny on building-level energy intensity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-based tendering squeezing margins | -0.9% | National public procurement | Short term (≤2 years) |

| Persistent informal labor | -0.7% | Smaller cities | Medium term (2-4 years) |

| Aging building stock outside Belgrade | -0.5% | Regional areas | Long term (≥4 years) |

| Volatile utility tariffs | -0.4% | National (industrial) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-based tendering squeezing provider margins

Lowest-bid public tenders still dominate, encouraging race-to-the-bottom pricing that dilutes investment in training and smart tools. Limited FM literacy among procurers further commoditizes complex, multiyear service packages, delaying Serbia’s convergence with EU value-based models.

Persistent informal labor limiting compliance

Shadow-economy labor, equal to 30.1% of GDP, enables unregistered contractors to undercut compliant firms but exposes owners to safety and tax liabilities. Inconsistent enforcement outside Belgrade restricts skills-development pipelines and undermines professionalization targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard services underpin current revenue, soft services accelerate

Hard Services generated 58.10% of 2025 revenue within the Serbia facility management market, led by MEP & HVAC packages needed to overhaul aging industrial stock to EU efficiency codes. Fire-safety upgrades are expanding fastest inside factories and logistics nodes aligning with harmonized EU directives, pushing asset-integrity contracts longer than five years.

Soft Services are projected to outpace at a 5.85% CAGR thanks to the rise of IT parks and shared-service centers that embed workplace-experience KPIs such as hygiene, catering variety and reception analytics. Cleaning contracts now bundle indoor-air-quality monitoring, a standard adopted in post-pandemic active-office formats.

By Offering Type: Outsourced partnerships dominate growth

The Outsourced model commands 59.35% of 2025 spending and is widening through 2026-2031 at a 6.05% CAGR as foreign investors in free zones require single governance dashboards across multitenant sites. Single-service cleaning or security contracts remain the usual entry but quickly graduate to bundled or integrated FM arrangements once owners measure downtime savings.

Integrated FM is the fastest-growing slice, driven by flagship assets like the Smart Manufacturing Innovation Center in Novi Sad, where OT-IT convergence dictates 24/7 digital-infrastructure stewardship. In-house teams persist mainly in government bodies yet lose ground as institutional investment rules now score bidders on energy and ESG competencies.

By End-User Industry: Commercial leads today while institutional assets gain speed

Commercial portfolios—office, retail and warehousing—held 35.70% of 2025 demand, reflecting Belgrade’s technology-sector influx and EUR 125 million of retail-logistics spend by multinational brands. Data-center fit-outs linked to 5G deployment further enlarge requirement lists to include critical-environment maintenance and redundant power testing.

Institutional & Public Infrastructure is forecast to rise at a 6.02% CAGR to 2031, fueled by EU-funded rail, solid-waste and e-government undertakings that mandate performance-based FM contracts for new assets. Hospitals and schools pursuing NZEB targets create long-term energy-service agreements blending O&M with guaranteed consumption reductions

Geography Analysis

Belgrade dominates the Serbia facility management market with the bulk of Grade A offices, government ministries and cultural flagships such as the planned Philharmonic Concert Hall that will require acoustics-specific maintenance protocols. Competition is intense among ISS, Sodexo and CBRE alongside local Atrium Property Services, each layering IoT sensors and real-time dashboards into bids to win five-year integrated contracts.

Novi Sad is the second growth pole thanks to its Smart Manufacturing Innovation Center and thriving ag-tech cluster, prompting demand for facility partners skilled in OT network resilience and ISO 50001 energy-management routines. City authorities additionally deploy EU green-city funds to retrofit public buildings, raising outsourced opportunities for mid-cap providers.

Secondary cities—Niš, Kragujevac and Subotica—are emerging as nearshoring spillovers where data centers, logistics depots and Expo 2027 venues expand the outsourced serviceable area. Government balanced-development policy and World Bank resilient-cities grants are formalizing procurement frameworks that favor compliant FM vendors over informal crews.

Competitive Landscape

Serbia’s facility management arena is moderately fragmented: global incumbents such as ISS, Sodexo and Johnson Controls compete with regional names like Atrium Property Services and CBRE, while digital disruptors like Hauzmajstor leverage app-based booking and dynamic pricing. Multinationals rely on global frameworks to lock in energy-performance clauses and ESG reporting; regional firms counter with localized regulatory know-how and 24-hour dispatch hubs.

Consolidation prospects rise as Serbia tightens labor, VAT and waste-handling statutes, shrinking room for under-the-radar operators. Providers able to finance BMS upgrades and predictive-maintenance analytics will likely accumulate share when shadow-economy participants exit. Technology partnerships—e.g., HBIS and Siemens’ digital green-steel facility—signal a new frontier where FM contractors manage not only buildings but embedded production tech.

Outcome-based contracts are gaining currency in logistics and healthcare, rewarding vendors on uptime and energy-cost savings rather than fixed task lists. This model favors firms with balance-sheet strength to underwrite sensors, software platforms and staff reskilling, leaving niche cleaners or security-only players to either merge or focus on specialized segments like heritage-site conservation.

Serbia Facility Management Industry Leaders

Sauter AG

Atrium Property Services

Atalian Global Services

REIWAG Facility Services

Diversey Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Eviden secured a EUR 50 million deal to build Serbia’s National AI Factory, opening sizeable smart-infrastructure FM scopes.

- March 2025: ISS A/S launched a DKK 2.5 billion share-buyback, underlining capital depth for Balkan expansions.

- November 2024: EBRD approved EUR 75 million for Serbia’s Solid Waste Programme, boosting environmental-services demand.

- May 2024: HBIS and Siemens agreed to construct a digital green steel plant requiring advanced facility energy-control protocols.

Serbia Facility Management Market Report Scope

Facilities management helps clinch the comfort, efficiency, safety, functionality, and sustainability of buildings and grounds, real estate, and infrastructure. There are two basic areas in facility management, i.e., In-house Facility Management and Outsourced Facility Management.

The Serbia facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehousing) |

| Hospitality (Hotels, Eateries and Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehousing) | |

| Hospitality (Hotels, Eateries and Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Serbia facility management market?

The Serbia facility management market size equals USD 651.46 million in 2026 and is projected to grow steadily through 2031.

Which service category generates the most revenue?

Hard Services—primarily MEP, HVAC, and fire-safety maintenance—held 58.10% market share in 2025, making it the dominant revenue engine.

Why is outsourcing gaining traction in Serbia?

Scarce technical labor, rising compliance complexity, and foreign investors’ demand for harmonized service standards are pushing Serbian occupiers toward outsourced facility-management partnerships.

Which end-user segment will expand fastest by 2031?

The Institutional & Public Infrastructure segment is expected to deliver a 6.02% CAGR, boosted by EU-funded modernization programs and smart-city investments.

How fragmented is market competition?

With the top five providers controlling slightly more than 60% of spending, the market is moderately concentrated; consolidation is anticipated as shadow-economy operators exit and digital-capable firms gain ground.

What technologies are shaping future contracts?

IoT sensors, AI-driven predictive maintenance, BIM-integrated CMMS platforms, and energy-analytics dashboards are becoming standard requirements in new integrated facility-management agreements.

Page last updated on: