Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

The Lithuania Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-House, Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

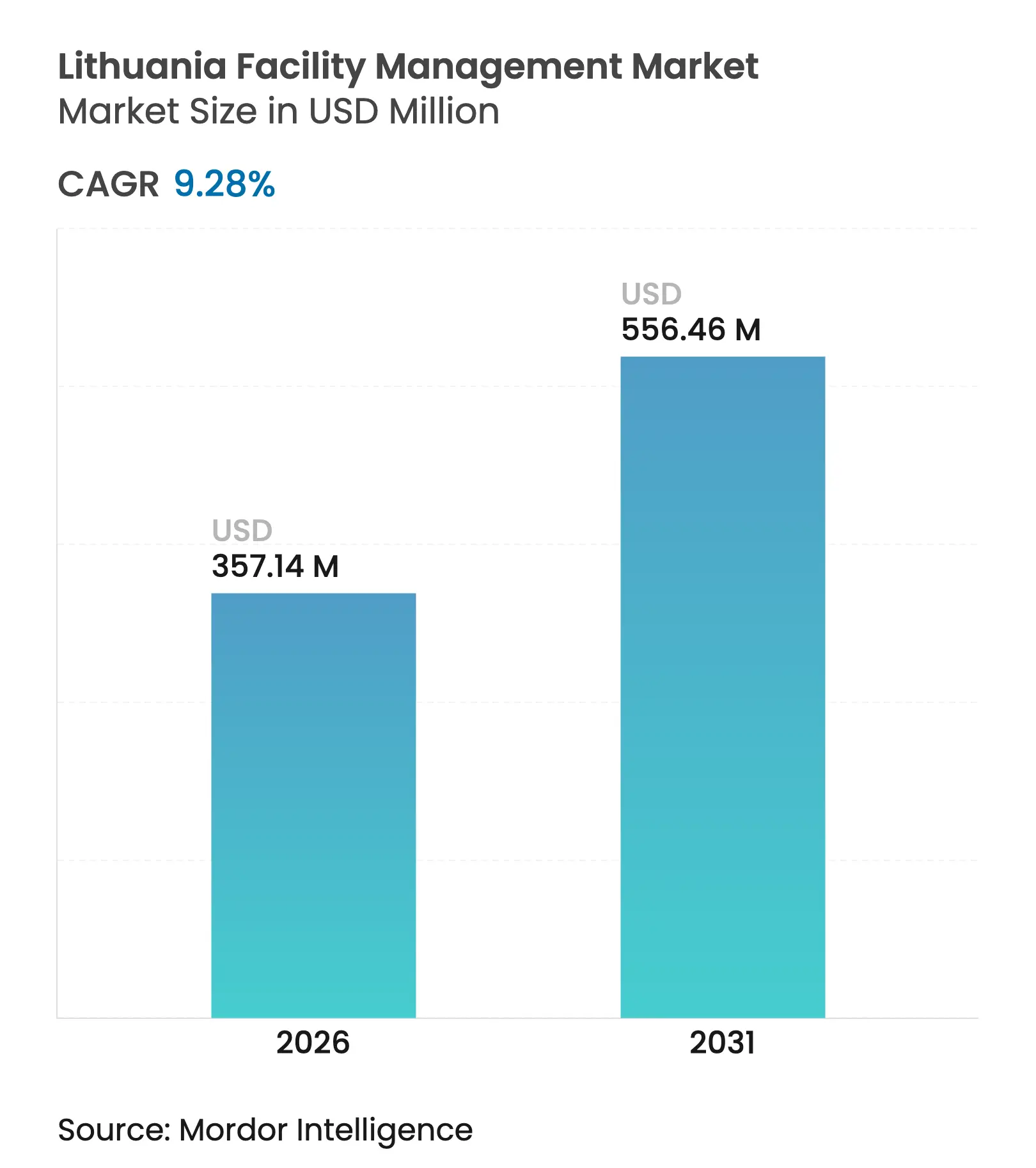

| Market Size (2026) | USD 357.14 Million |

| Market Size (2031) | USD 556.46 Million |

| Growth Rate (2026 - 2031) | 9.28 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Lithuania facility management market size in 2026 is estimated at USD 357.14 million, growing from 2025 value of USD 326.8 million with 2031 projections showing USD 556.46 million, growing at 9.28% CAGR over 2026-2031. Investments from the EU Recovery and Resilience Plan, continued GDP growth of 2.7% in 2025, and an expanding commercial real estate pipeline keep demand for facility services elevated. [1]OECD, “OECD Economic Outlook 2025: Lithuania,” oecd.orgGovernment reforms accelerate outsourcing, while energy-efficient building retrofits and integrated service contracts support recurring revenues. Digital tools such as IoT sensors, predictive maintenance, and AI-driven building controls sharpen competitive advantages for providers that adopt them early. Wage inflation linked to a shrinking labour pool and a fragmented supplier base remain the key cost headwinds shaping short-term pricing.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growth in Outsourced FM Contracts from Public Sector Reforms Growth in Outsourced FM Contracts from Public Sector Reforms | +2.1% | National, concentrated in Vilnius, Kaunas, Klaipėda | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:National, concentrated in Vilnius, Kaunas, Klaipėda | Impact Timeline:Medium term (2-4 years) |

Expansion of Commercial Real Estate & Logistics Hubs Post-EU Funding Expansion of Commercial Real Estate & Logistics Hubs Post-EU Funding | +1.8% | National, with early gains in Vilnius, Kaunas, Šiauliai | Long term (≥ 4 years) | |||

Rising Demand for Energy-Efficient Building Retrofits Rising Demand for Energy-Efficient Building Retrofits | +1.5% | National, prioritizing major metros | Medium term (2-4 years) | |||

Increasing Adoption of Integrated FM Service Models Increasing Adoption of Integrated FM Service Models | +1.2% | National, spill-over to regional centers | Long term (≥ 4 years) | |||

Lithuania's Green Public Procurement Quotas Favoring ESG-Aligned FM Vendors Lithuania's Green Public Procurement Quotas Favoring ESG-Aligned FM Vendors | +0.9% | National, government facilities focus | Short term (≤ 2 years) | |||

Nearshoring of Nordic Shared Service Centers Boosting 24/7 Facility Uptime Needs Nearshoring of Nordic Shared Service Centers Boosting 24/7 Facility Uptime Needs | +0.8% | Concentrated in Vilnius and Kaunas | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Growth in Outsourced FM Contracts from Public Sector Reforms

Higher public investment drives ministries and municipalities to externalise technical tasks. The 2025 state budget channels EUR 3.6 billion into infrastructure, which lifts competitive tenders for maintenance, cleaning, and energy management. State property agency Turto bankas posted 25% revenue growth to EUR 42.9 million in 2024 after completing more than 50 renovation projects, showing how outsourced contracts raise asset quality.[2]Verslo Žinios, “Turto Bankas 2024 Results,” vz.lt As central authorities sign outcome-based agreements, vendors that can guarantee measurable savings dominate renewal cycles.

Expansion of Commercial Real Estate & Logistics Hubs Post-EU Funding

EU grants worth EUR 2.22 billion funnel into landmark schemes such as Tech Zity and Bio City in Vilnius, with the latter alone representing EUR 7 billion in long-term capital. Šiauliai industrial park valuations near EUR 100 million and a 6,435-strong workforce attract logistics FM contracts that cover security, cleaning, and on-site maintenance. The sale of a 60,000 square-metre distribution centre near Kaunas for EUR 60 million underscores international appetite for Lithuanian warehousing and the corresponding rise in service hours per asset.

Rising Demand for Energy-Efficient Building Retrofits

National targets call for a 30% emissions reduction by 2030, which pushes public and private owners to retrofit HVAC and lighting. The European Investment Bank allocated EUR 35 million to modernise the Kaunas district heating grid, benefiting 400,000 residents and creating steady workloads for technical FM teams.[3]European Investment Bank, “Kaunas Heating Upgrade,” eib.orgWind generation reached 1.5 TWh while solar output rose 79.4% to 342.2 million kWh in 2022, each requiring specialist maintenance schedules. AI-driven ventilation can cut office energy use by 12.5%, so providers that integrate such analytics gain procurement advantages.

Increasing Adoption of Integrated FM Service Models

Clients prefer single contracts covering hard and soft tasks. Everfield’s purchase of Lithuanian field-service platform Frontu followed a 400% revenue climb, illustrating investor belief in integrated, tech-enabled workflows. Globally, CBRE merged flexible workspace and facilities under its Building Operations & Experience unit, underscoring the scale merits at stake. Such bundled models reduce administration for occupiers and open paths for performance-linked fees.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shrinking Low-Skilled Labor Pool Driving Wage Inflation Shrinking Low-Skilled Labor Pool Driving Wage Inflation | -1.4% | National, acute in major metros | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:National, acute in major metros | Impact Timeline:Short term (≤ 2 years) |

Fragmented Supplier Base Limiting Service Standardization Fragmented Supplier Base Limiting Service Standardization | -0.8% | National, regional variations | Medium term (2-4 years) | |||

Volatile District Heating Tariffs Complicating Long-Term Hard FM Budgeting Volatile District Heating Tariffs Complicating Long-Term Hard FM Budgeting | -0.6% | National, concentrated in urban centers | Medium term (2-4 years) | |||

Cyber-security Compliance Costs for Smart-Building FM Platforms Cyber-security Compliance Costs for Smart-Building FM Platforms | -0.4% | National, technology-adopting facilities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Shrinking Low-Skilled Labour Pool Driving Wage Inflation

Lithuania’s population has fallen by more than 800,000 since independence, leaving only 2.8 million residents and fewer young workers. Cleaning and guarding roles face acute vacancies, while registered unemployment of 9% hides skills mismatches. Proposed limits on third-country nationals may tighten supply further and lift hourly wages by double-digit rates, squeezing gross margins for small FM firms.

Fragmented Supplier Base Limiting Service Standardisation

Dozens of SMEs compete with global brands such as ISS, Sodexo, and CBRE. A lack of shared service benchmarks complicates multisite contracts and raises transaction costs for buyers. Providers in Vilnius offer advanced digital dashboards, while firms in smaller cities rely on manual logs, creating uneven service quality. Consolidation remains slow because regional clients value flexible pricing and local ties, so market uniformity progresses gradually.

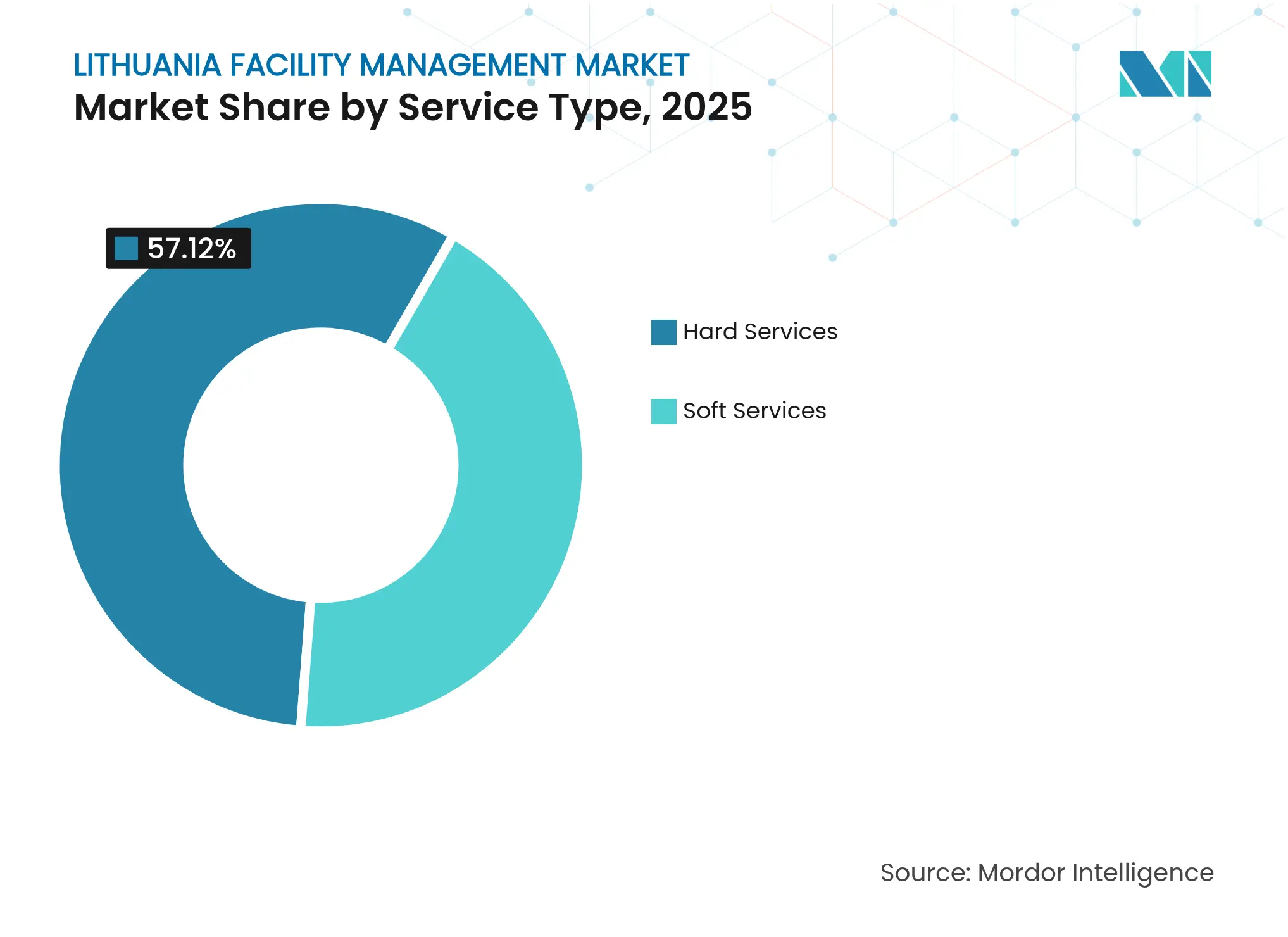

By Service Type: Hard Services Lead Despite Soft Services Growth

Hard services controlled 57.12% of Lithuania facility management market in 2025 as aging assets demanded mechanical, electrical, and HVAC expertise. Demand for smart metering and building automation widens barriers to entry, favouring providers with licensed engineers and IoT skills. Energy modernisation funds, including EUR 35 million for Kaunas heating, boost workload visibility and extend contract tenors.

Soft services record the fastest trajectory with a 9.78% forecast CAGR, propelled by shared service centres and new life-science campuses. Cleaning, reception, and catering volumes expand in tandem with headcount in modern offices, while overnight security gains relevance for logistics hubs. Labour shortages push operators towards robotics and sensor-enabled quality audits. Strong pipeline activity gives the Lithuania facility management market additional volume, yet wage inflation compresses margins in labour-intensive sub-segments.

Note: Segment shares of all individual segments available upon report purchase

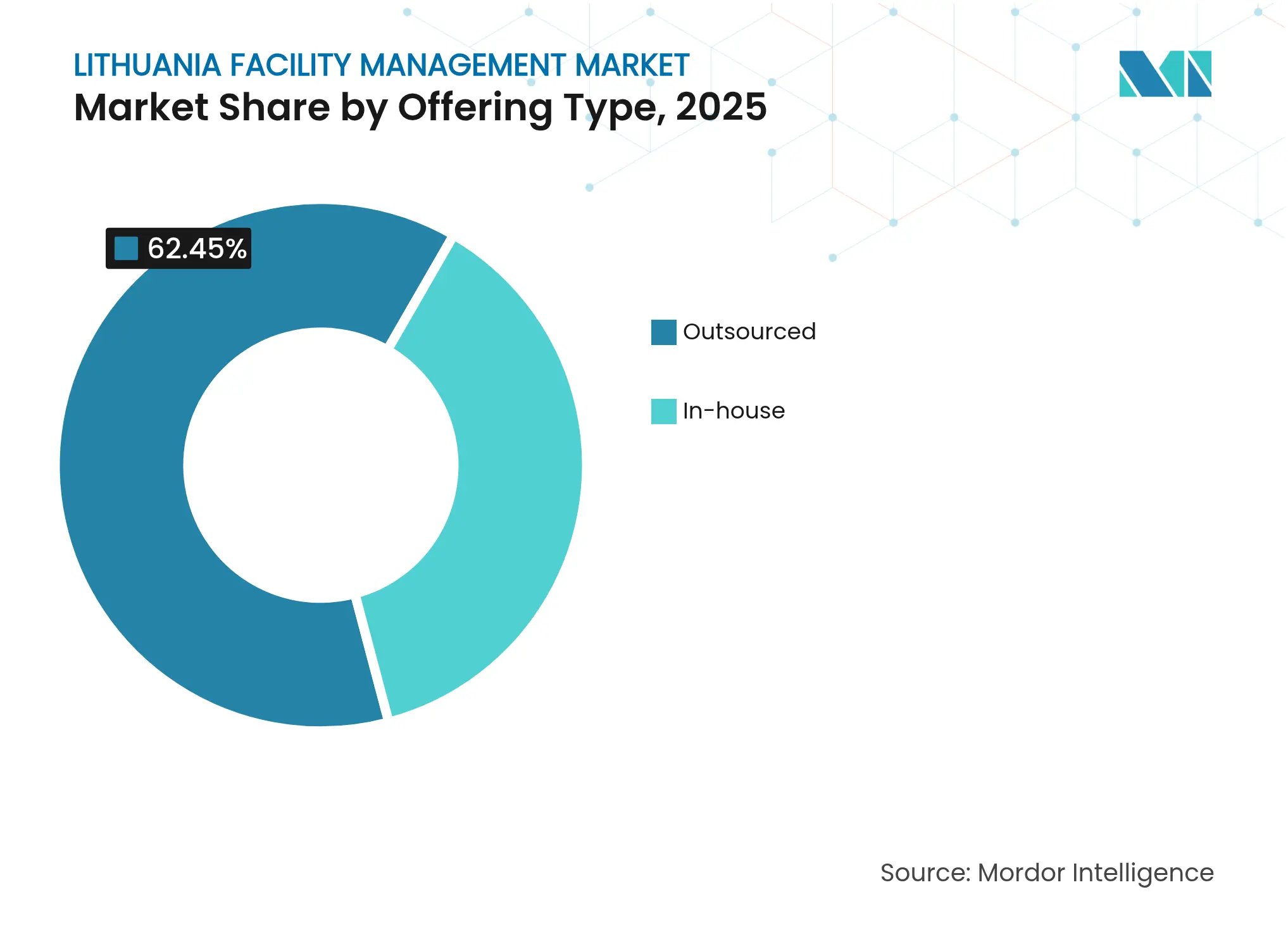

By Offering Type: Outsourced Models Accelerate Market Growth

Outsourced contracts held 62.45% of Lithuania facility management market size in 2025 and are on a 9.55% CAGR path as public bodies convert in-house teams to framework agreements. Integrated FM garners the quickest uptake because bundled scopes reduce duplicate supervision and align KPIs across cleaning, maintenance, and energy domains.

In-house models remain relevant in heavy industry and healthcare where process know-how is critical. Yet rising compliance demands favour specialists that carry professional indemnity, cyber-security protocols, and sustainability reporting. Hybrid structures, where clients retain strategic oversight and outsource execution, help organisations manage risk while accessing the innovation pace of the Lithuania facility management industry.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Commercial Dominance Amid Public Sector Growth

Commercial premises accounted for 37.65% of Lithuania facility management market in 2025, led by IT, retail, and warehousing projects tied to EU funds and nearshoring flows. Multinational tenants demand SLA-driven uptime, which raises spend on predictive maintenance and analytics.

Institutional and public infrastructure posts the fastest 9.63% CAGR to 2031 as ministries and municipalities retrofit schools, courts, and transport hubs. Green public procurement clauses move cost evaluation away from low-bid scoring toward total lifecycle savings, opening margins for ESG-aligned vendors. Industrial clients in free economic zones maintain steady but smaller volumes, while hospitality recovers gradually. Together, these shifts widen scope for technology-rich propositions within the broader Lithuania facility management industry.

Vilnius remains the epicentre for the Lithuania facility management market because it hosts central government, the largest share of modern offices, and flagship developments such as Tech Zity and Bio City that together exceed EUR 7 billion in pipeline value. The city captures the majority of integrated FM tenders and sets service benchmarks adopted nationwide.

Kaunas follows as a growth node anchored by logistics and engineering heritage. The EUR 35 million EIB injection into its district heating grid elevates demand for energy-focused hard services, while the EUR 60 million logistics centre sale confirms sustained investor commitment. Klaipėda requires specialised marine-related maintenance for port facilities and hospitality sites linked to cruise traffic.

Secondary cities such as Šiauliai and Panevėžys show emerging potential thanks to free economic zones and industrial parks valued near EUR 100 million. Providers that can offer modular service packages and competitive travel rates win contracts in these lower-density areas. Although unit pricing differs by region, knowledge transfer from Vilnius and Kaunas gradually lifts service quality norms across the entire Lithuania facility management market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

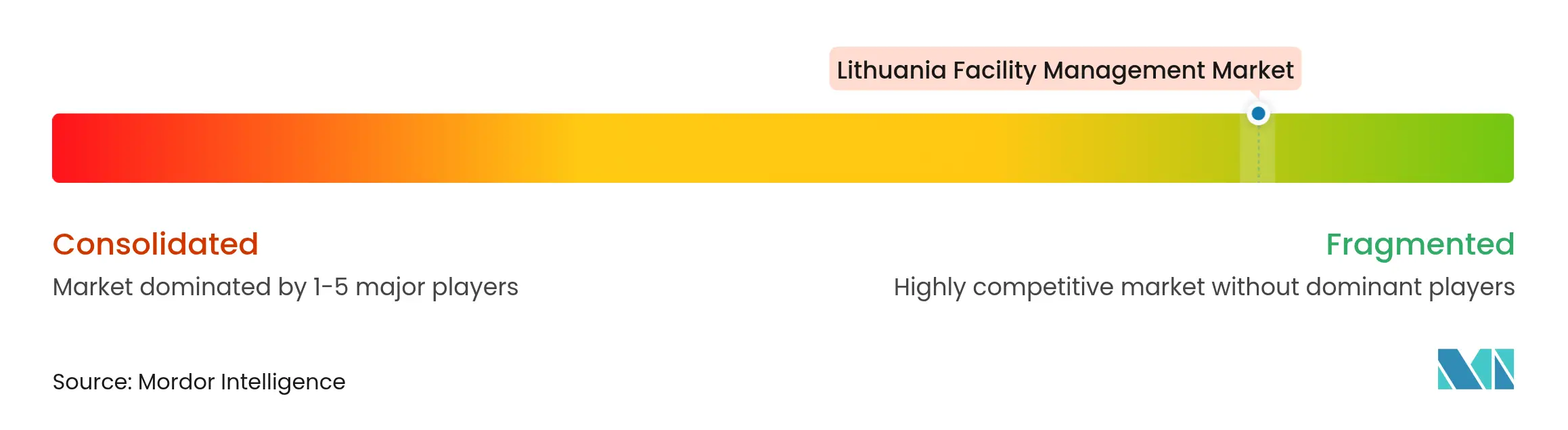

Market Concentration

The supplier field remains moderately fragmented, with global groups such as ISS, Sodexo, and CBRE competing against strong locals like City Service SE, Civinity, and Mano Būstas. No single company controls more than a tenth of national revenue, which leaves ample room for niche specialists and regional champions.

Technology is the main differentiator. EIB’s EUR 50 million financing for Teltonika IoT highlights the merger of FM and digital building analytics. Providers that deploy sensor networks and AI diagnostics document faster fault resolution, which supports outcome-based pricing. Frontu’s acquisition by Everfield shows investor appetite for software that coordinates multi-site field technicians.

Consolidation prospects revolve around integrated FM capabilities and ESG reporting skills. Multinational asset owners prefer single partners that can guarantee consistency and audit-ready data. Local firms that embrace certification and remote-monitoring tools can scale, while those that resist digital change risk margin erosion in the Lithuania facility management market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Facility management services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres. The adoption of facility management solutions and services is likely to be driven by a number of factors, including an increase in demand for cloud-based facility management solutions and a rise in demand for facility management systems linked with intelligent software.

The Lithuania facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

Mapping Real Estate Opportunities in Bali

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.