Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

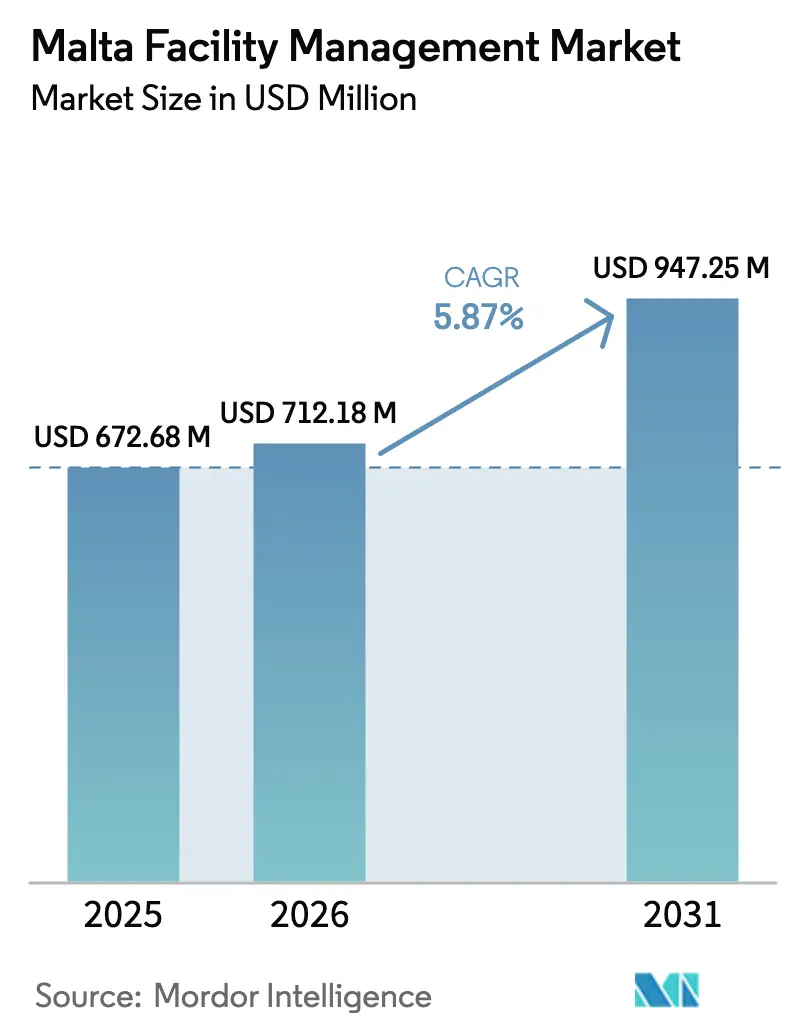

| Base Year Market Size (2025) | USD 672.68 Million |

| Market Size (2026) | USD 712.18 Million |

| Market Size (2031) | USD 947.25 Million |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

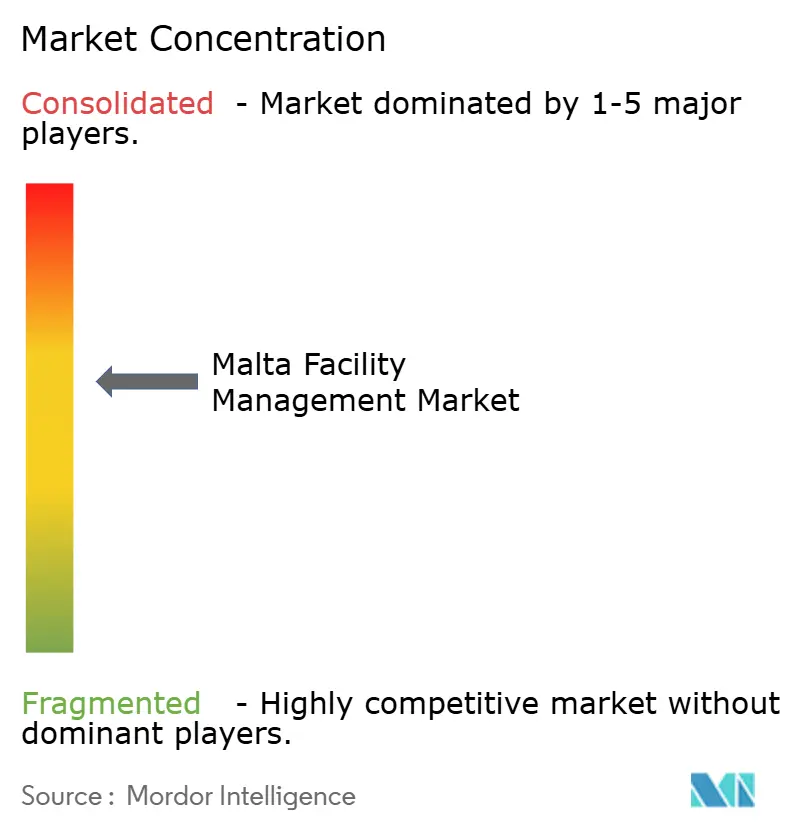

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malta Facility Management Market Analysis by Mordor Intelligence

The Malta Facility Management Market size is expected to grow from USD 672.68 million in 2025 to USD 712.18 million in 2026 and is forecast to reach USD 947.25 million by 2031 at 5.87% CAGR over 2026-2031. Growth is underpinned by infrastructure modernization, steady tourism recovery, and the island’s National Investment Plan, all of which intensify demand for integrated building services, digital maintenance platforms, and heritage-compliant solutions. Commercial real-estate expansion across Valletta, Sliema, and St. Julian’s keeps hard services in high demand, while public-sector projects enlarge the addressable pool for outsourced contracts. Labor regulation upgrades and rising occupancy rates encourage organizations to outsource for cost control and compliance assurance. Technology adoption—particularly AI-driven predictive maintenance and IoT-enabled building management—has become the pivotal differentiator, as Malta positions itself as the “Ultimate AI Launchpad” by 2030.

Key Report Takeaways

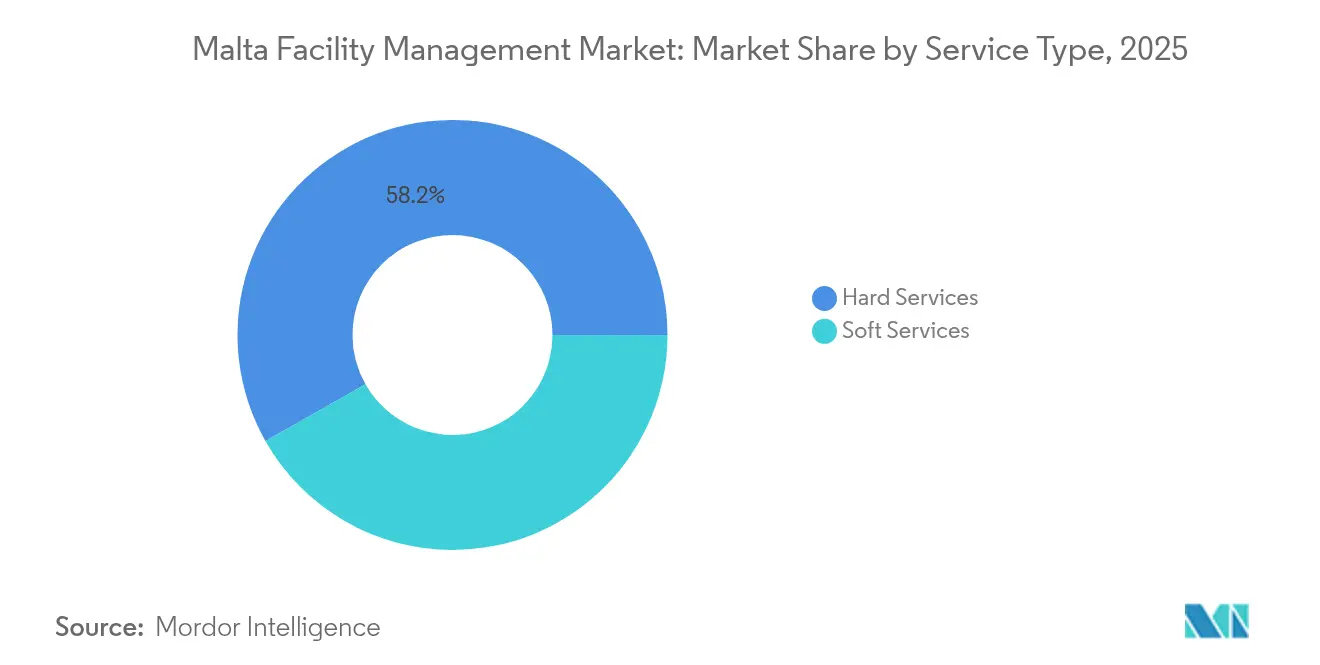

- By service type, hard services led with 58.20% Malta facility management market share in 2025; soft services are expanding at an 8.02% CAGR through 2031.

- By offering, outsourced services commanded 64.70% of the Malta facility management market size in 2025 and is projected to rise at a 7.39% CAGR; in-house services retained a 35.30% share of the Malta facility management market size in 2025.

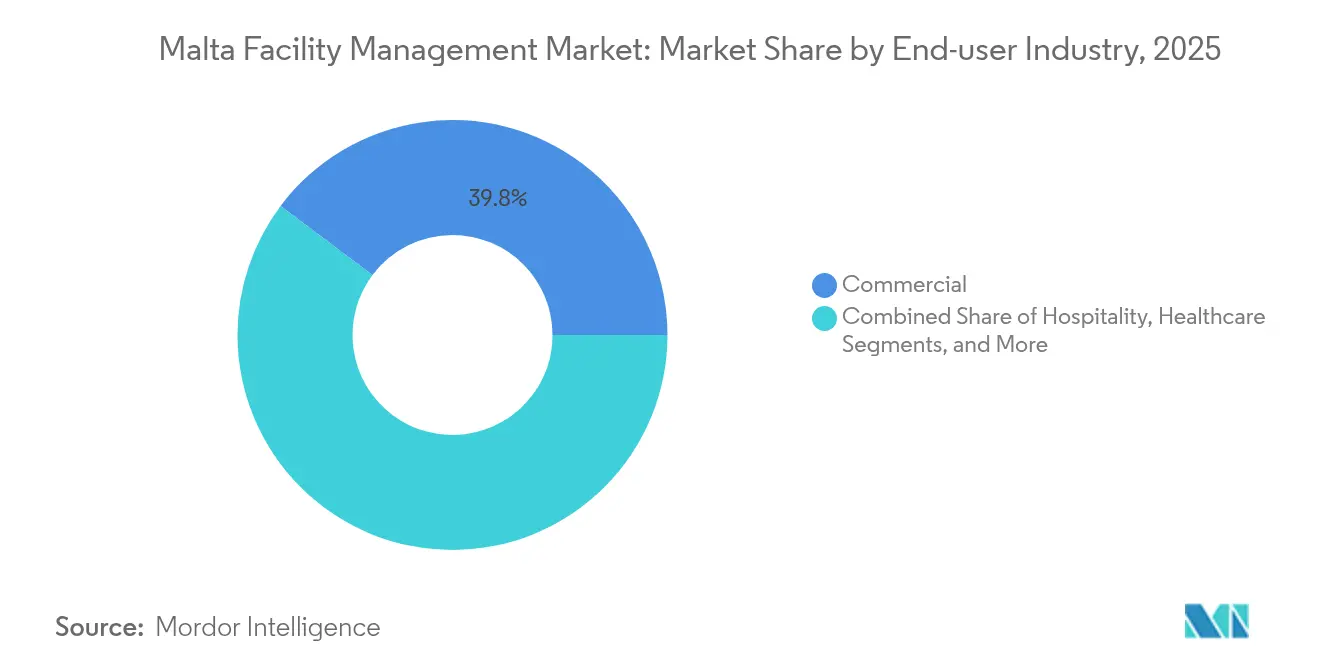

- By end-user industry, commercial facilities held 39.75% of the Malta facility management market share in 2025, while institutional and public infrastructure is advancing at a 7.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malta Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and population growth | +1.2% | National, concentrated in Valletta, Sliema, St. Julian's | Medium term (2-4 years) |

| Labor and safety regulation upgrade | +0.8% | National, with stricter enforcement in heritage zones | Short term (≤ 2 years) |

| Infrastructure investment pipeline | +1.5% | National, with focus on transport and utilities | Long term (≥ 4 years) |

| Rising occupancy rates | +0.9% | Commercial districts, hospitality zones | Medium term (2-4 years) |

| Digitalization and smart building adoption | +1.1% | Commercial and institutional sectors | Medium term (2-4 years) |

| Tourism-led revival in the hospitality sector | +0.7% | Hospitality zones, coastal areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization and Population Growth

The population density of 1,649 people per km² stresses Malta’s limited built environment and generates unprecedented service demand across residential, commercial, and public facilities. [1]International Monetary Fund, “Malta: Selected Issues,” imf.org The 25% population increase since 2014 has redirected many Valletta residences toward short-stay rentals, creating hybrid property portfolios that need adaptive maintenance schedules. Investment in social housing, exemplified by the EUR 22 million EIB-backed Luqa project, amplifies the need for modern MEP and life-safety systems. Urban crowding drives integrated waste, energy, and water solutions, encouraging IoT deployment for space-efficient asset management. A growing cohort of tech-savvy residents expects mobile service portals and real-time building analytics, prompting facility managers to digitize work-order flows.

Labor and Safety Regulation Upgrade

Statutory 40-hour work weeks and minimum wages of EUR 192.73 per week elevate cost bases, pushing firms toward outsourced, technology-augmented models. [2]Department for Industrial and Employment Relations, “Employment Conditions,” dier.gov.mt Safety directives in confined heritage structures require certified technicians, advantaging larger providers with compliance training capacity. Mandatory certifications spur predictive maintenance adoption to limit technician exposure to hazardous environments. These regulations raise entry barriers for smaller vendors yet enhance service quality, aligning Malta's facility management market standards with broader EU norms.

Infrastructure Investment Pipeline

Projects such as the EUR 34.7 million Msida Creek development embed 10-year operations-and-maintenance clauses, creating long-tail revenue for integrated service providers. The Water Services Corporation’s EUR 310.5 million program targets network efficiency gains from 52% in 2011 to 72% in 2023 and integrates AI modeling to predict system failures, widening the technology services segment. EU co-financing channels stable capital flows, encouraging suppliers to invest in advanced asset-management platforms that can be replicated across future concessions.

Rising Occupancy Rates

DoubleTree by Hilton’s new 485-room property reflects surging hospitality demand and introduces over 2,000 m² of event space that requires event-driven cleaning, security, and HVAC loads. Commercial offices are revisiting space allocations for hybrid work, requiring dynamic service scaling and sensor-based people-counting solutions. Higher utilization accelerates wear on MEP systems, pushing clients toward outcome-based maintenance contracts with uptime guarantees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortage and skill gaps | -1.3% | National, acute in specialized trades | Medium term (2-4 years) |

| Budget constraints and cost inflation | -0.9% | National, affecting all sectors | Short term (≤ 2 years) |

| Complex compliance for heritage and historical buildings | -0.6% | Heritage zones, Valletta, Mdina | Long term (≥ 4 years) |

| Limited economies of scale in a small domestic market | -0.4% | National, affecting service pricing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortage and Skill Gaps

Construction cost inflation between 30% and 40% reflects the scarcity of certified tradespeople, increasing wage bills for MEP and fire-safety works. Heritage conservation demands rare craftsmanship, compelling providers to source foreign artisans or invest in vocational training alliances with local institutes. Rising labor premiums incentivize robotics for façade cleaning and drone-based inspections, partially offsetting personnel constraints. Yet, small domestic scale limits the pool of apprenticeships, extending the skills gap beyond 2028. [3]Ministry for Finance and Employment, “Annual Report 2022,” finanzi.gov.mt

Budget Constraints and Cost Inflation

Producer-price inflation of 7.15% since 2021 squeezes FM budgets, encouraging life-cycle cost optimization over capex-heavy retrofits. Supply-chain frictions elevate spare-parts lead times, forcing stockpiling strategies that strain working capital for smaller vendors. Public authorities pursue value-based procurement to shield against overruns, demanding performance-linked fee structures. These fiscal pressures impel the adoption of open-protocol systems to avoid vendor lock-in and facilitate competitive tendering for upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Infrastructure Modernization

Hard Services held 58.20% of the Malta facility management market size in 2025, driven by the island’s aging building stock and the stringent regulatory framework that mandates professional upkeep of MEP, HVAC, and fire-protection assets. The Msida Creek flyover and Water Services upgrades lock in multi-year maintenance contracts that sustain revenue visibility. Heritage restoration norms oblige specialized stonework, elevating the technical barrier to entry. Demand for building resilience against salt-air corrosion further supports predictive asset-management platforms.

Soft Services, expanding at an 8.02% CAGR, rides on the back of workplace-experience programs and tourism revival. Digitally scheduled cleaning, security robots, and ESG-aligned waste minimization broaden the outsourced menu. Integration between soft and hard services via IoT dashboards allows single-pane visibility, encouraging bundled procurement. The Malta facility management market thus sees suppliers positioning themselves as total-lifecycle partners rather than stand-alone janitorial or MEP vendors.

By Offering Type: Outsourcing Dominates, Integrated FM Accelerates

Outsourced contracts commanded 64.70% of the Malta facility management market size in 2025 as enterprises and public bodies entrusted specialists with compliance and cost control. The model’s 7.39% CAGR through 2031 reflects labor-shortage mitigation and the need for capex-sharing in technology rollouts. Integrated FM, combining multi-vertical services under one SLA, delivers data-driven reporting coveted by ESG-focused investors.

In-house management persists among large campuses and critical infrastructure, where institutional knowledge and security sensitivities prevail. Nevertheless, hybrid models emerge—core teams oversee strategy while niche tasks, such as heritage façade upkeep or AI-based energy analytics, are subcontracted. The Malta facility management market’s small geographic footprint supports shared mobile teams, reducing response times and bolstering service-level compliance.

By End-user Industry: Commercial Stronghold Encounters Institutional Momentum

Commercial facilities held 39.75% Malta facility management market share in 2025, anchored by the financial and tech clusters lining the northern harbor. Grade-A offices, data centers, and mixed-use retail demand 24/7 uptime and cybersecurity-integrated BMS platforms. Space re-configurability for hybrid work elevates change-management requirements, fueling spend on sensor-driven occupancy analytics.

Institutional and Public Infrastructure is projected to grow at 7.68% CAGR, propelled by EU-funded water, transport, and educational programs. Hospitals operated under public-private partnerships require stringent environmental controls and continuous accreditation audits, providing steady income streams for specialized FM providers. Government ESG targets catalyze energy retrofits in schools and municipal buildings, magnifying the role of smart meters and AI-enabled efficiency dashboards. As a result, the Malta facility management market tilts toward K-12 campuses, water utilities, and transportation nodes as the next demand hotspots.

Geography Analysis

Malta’s compact 316 km² geography concentrates service demand, enabling rapid dispatch of technicians and cost-effective resource pooling. The Valletta-Sliema-St. Julian’s corridor hosts the lion’s share of premium offices and high-end hotels, translating into the highest revenue density per square kilometer. These assets call for heritage-sensitive HVAC retrofits and premium concierge-level soft services, contributing more than half of the Malta facility management market size within a 10-km radius.

Central and southern districts house industrial complexes such as the 29,000 m² De La Rue facility and STMicroelectronics’ semiconductor plant, both requiring clean-room maintenance, vibration-controlled flooring, and 24/7 utility oversight. Proximity to the freeport and airport streamlines spare-parts logistics. Gozo’s budding tourism and educational investments signal a nascent cluster that values eco-certified FM practices, supported by government incentives for renewable-ready buildings.

Coastal exposure demands anti-corrosion protocols, frequent façade inspections, and salt-resistant materials, differentiating Malta from inland European markets. Water scarcity shapes stringent leak-detection and wastewater reuse standards, broadening the scope for IoT sensor deployments. Alignment with the national carbon-neutrality roadmap drives island-wide retrocommissioning of HVAC systems and rooftop solar maintenance, positioning geography as both constraint and catalyst in the Malta facility management market.

Competitive Landscape

The Malta facility management market is moderately concentrated, blending global multinationals with agile local champions. CBRE, JLL, and Cushman & Wakefield secure multinational clients by leveraging international best practices and deep capital resources. Local specialists—FMcore Limited, Clentec Malta, and Shine Management—edge ahead in heritage compliance and rapid site mobilization, aided by intimate knowledge of planning regulations. Mid-sized integrators fill the service gap for bundled contracts below the threshold of global firms, often subcontracting niche technical tasks to certified artisans.

Technology leadership is the key competitive lever. Johnson Controls and Schneider Electric supply AI-ready BMS hardware, while regional integrators layer analytics and user dashboards. Contract models evolve toward outcome-based SLAs guaranteeing energy savings or uptime, favoring vendors with robust data-science capabilities. Market entrants focusing on ESG consulting and digital platform integration exploit the white-space left by volume-oriented maintenance houses.

M&A activity remains selective; multinationals prefer strategic alliances over outright acquisitions to mitigate concentrated-market risk. However, rising compliance burdens and the lure of AI pilot projects could prompt consolidation as smaller firms struggle with capex demands for technology upgrades. The Malta facility management market, therefore, rewards scale balanced with local agility and technology prowess.

Malta Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

Cushman & Wakefield plc

Sodexo SA

ISS A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Hertz Malta obtained ESG certification, signalling rising sustainability metrics in service contracts.

- September 2024: Water Services Corporation detailed its EUR 310.5 million National Investment Plan featuring AI-based infrastructure management.

- August 2024: RS2 p.l.c. reported EUR 19.1 million revenue, highlighting FM needs for expanding fintech campuses.

- July 2024: Infrastructure Malta announced Triq tal-Barrani road works, underscoring continuous civil works FM demand.

- June 2024: Mekanika intensified its focus on sustainable building technology, expanding the pool of green FM solutions.

Malta Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through their responsibility for often maintaining an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The integrated facility management service (IFM) market, along with single and bundled services, is included in the outsourced FM services segment.

The Malta facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Malta facility management market?

The Malta facility management market size is USD 712.18 million in 2026.

How fast is the Malta facility management market expected to grow?

It is projected to reach USD 947.25 million by 2031, registering a 5.87% CAGR over 2026-2031.

Which service type holds the largest share?

Hard Services command 58.20% market share, reflecting the need for specialized MEP and asset-management expertise.

Why are outsourced contracts increasing in Malta?

Labor shortages, complex compliance rules, and advanced technology requirements push organizations to rely on providers offering scale and integrated digital platforms.

Which end-user segment is growing the fastest?

Institutional and Public Infrastructure facilities are forecast to expand at a 7.68% CAGR as EU-funded projects and modernization efforts accelerate demand.

Page last updated on: