Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

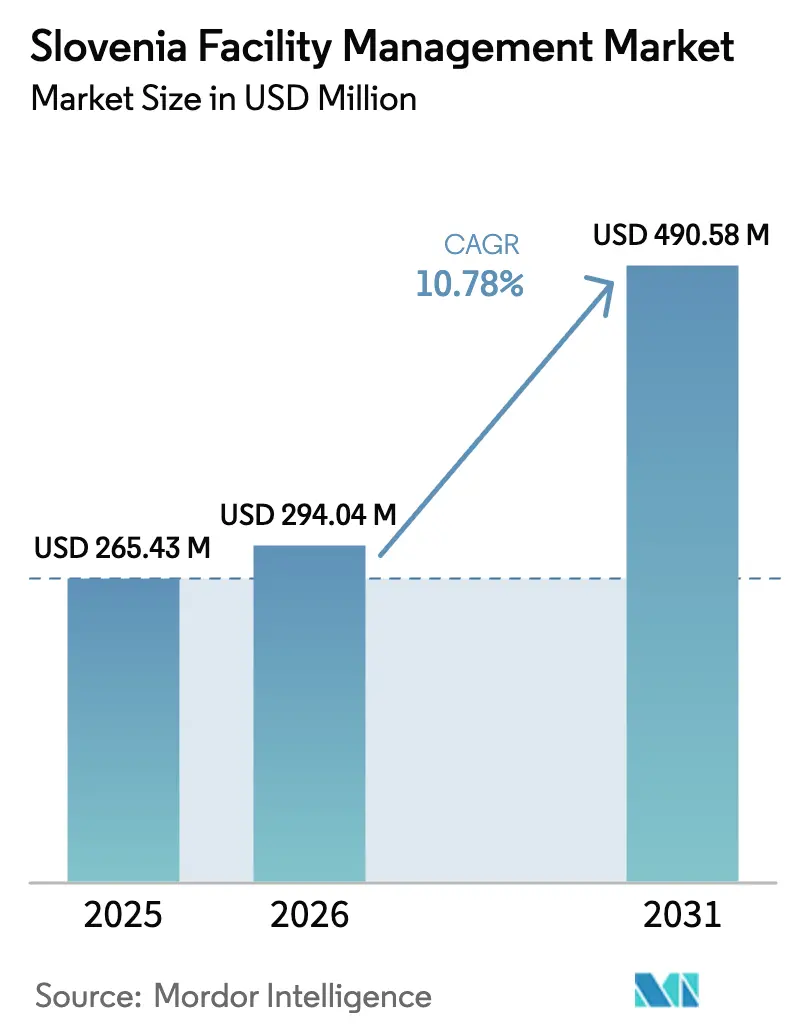

| Base Year Market Size (2025) | USD 265.43 Million |

| Market Size (2026) | USD 294.04 Million |

| Market Size (2031) | USD 490.58 Million |

| Growth Rate (2026 - 2031) | 10.78% CAGR |

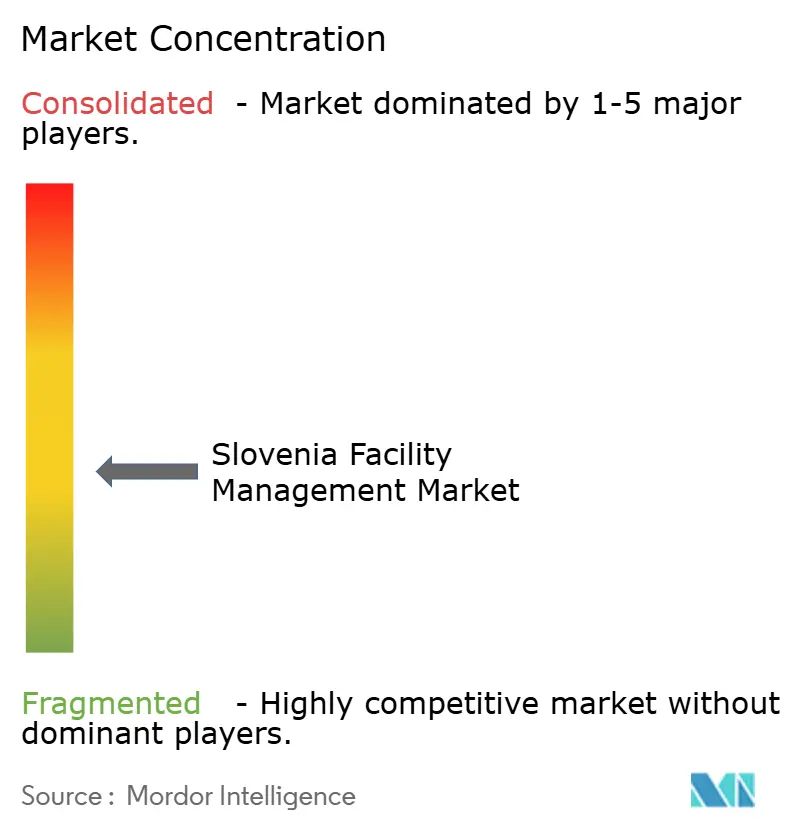

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovenia Facility Management Market Analysis by Mordor Intelligence

The Slovenia Facility Management Market size was valued at USD 265.43 million in 2025 and estimated to grow from USD 294.04 million in 2026 to reach USD 490.58 million by 2031, at a CAGR of 10.78% during the forecast period (2026-2031). Robust public investment under the EUR 2.7 billion Recovery and Resilience Plan, rising wage pressure in a 4.4% unemployment environment, and growing recognition of facility services as productivity enablers rather than cost centers are driving this expansion. [1]European Commission, “Slovenia's Recovery and Resilience Plan,” commission.europa.eu The Slovenia facility management market benefits from EU-aligned sustainability rules that push clients toward outsourced technical expertise for compliance. Demand is further catalyzed by digitalization incentives that encourage data-driven maintenance, while tight labor supply and inflationary construction costs make outsourcing a hedge against unpredictable in-house expense. [2]Statistical Office of the Republic of Slovenia, “Cene storitev v gradbeništvu ponovno navzgor,” stat.si Competitive intensity is increasing as both international majors and local specialists invest in IoT-enabled building management systems and predictive analytics.

Key Report Takeaways

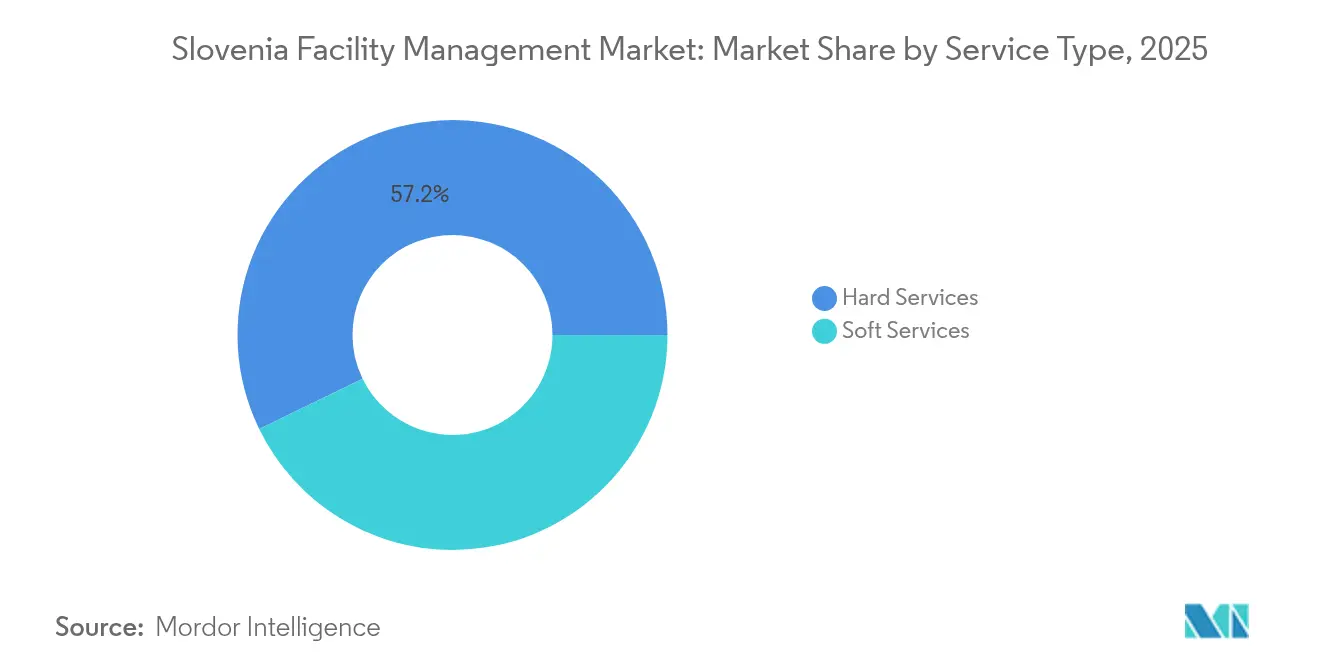

- By service type, hard services led with a 57.21% Slovenia facility management market share in 2025, while soft services are projected to advance at a 13.78% CAGR through 2031.

- By offering type, the outsourced delivery models accounted for 65.85% of the Slovenia facility management market share in 2025, with integrated outsourcing forecast to grow at 12.88% CAGR to 2031.

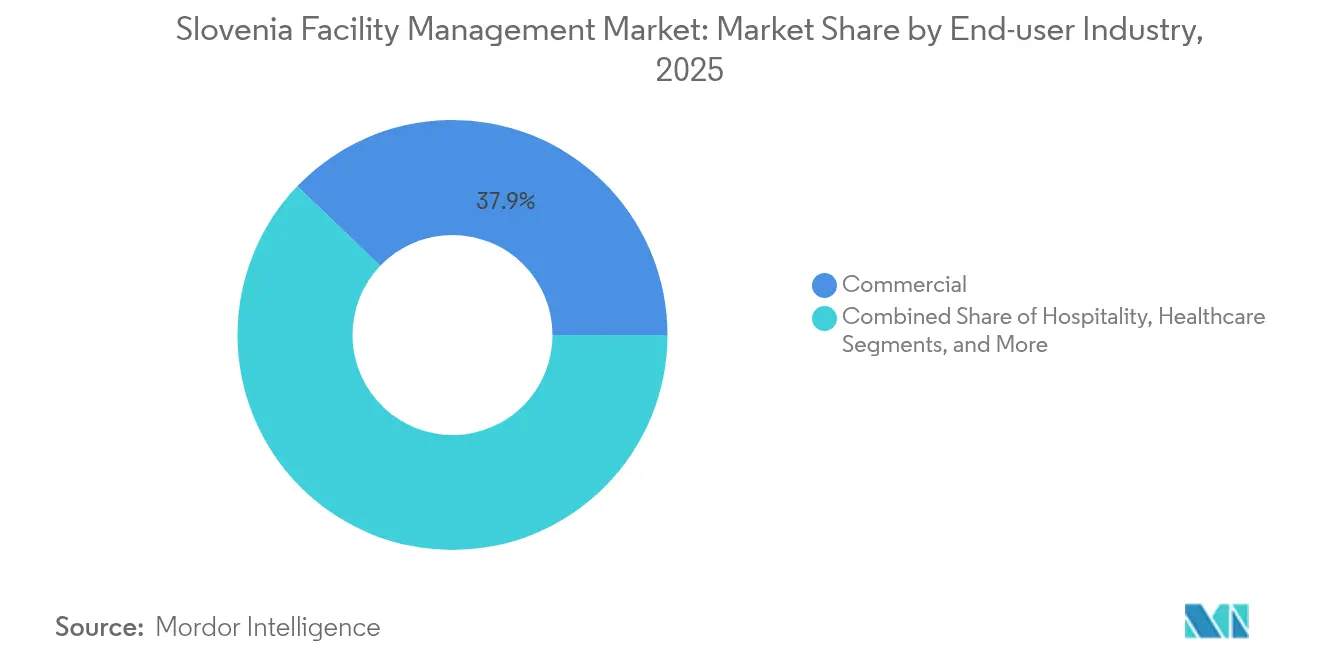

- By end-user industry, the commercial segment captured 37.85% of the Slovenia facility management market in 2025; institutional and public infrastructure is on track for a 13.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovenia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing outsourcing of non-core business functions | +2.1% | Slovenia, with spillover to Central Europe | Medium term (2-4 years) |

| Growing demand for integrated facility management solutions | +1.8% | National, with early gains in Ljubljana, Maribor, Celje | Medium term (2-4 years) |

| Rising focus on workplace experience and employee productivity | +1.5% | Commercial hubs in Ljubljana and coastal regions | Short term (≤ 2 years) |

| Technological advancements in building management systems | +1.3% | Urban centers and industrial zones | Long term (≥ 4 years) |

| Growing emphasis on green building certifications and sustainability compliance | +1.7% | EU-aligned markets with regulatory pressure | Long term (≥ 4 years) |

| Expansion of public-private partnerships in infrastructure and facilities maintenance | +1.4% | National infrastructure projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Outsourcing of Non-Core Business Functions

Organizations are reallocating resources toward strategic priorities as GDP growth rebounds to a 2.5% outlook for 2025. Outsourcing addresses talent shortages, evidenced by seven successive quarterly declines in job vacancies to 17,900 in Q4 2024, and gives companies access to specialized digital and ESG skills absent internally. [3]Statistical Office of the Republic of Slovenia, “The number of job vacancies down for the seventh time,” stat.si The Slovenia facility management market, therefore, records rising multi-year service contracts within ICT and construction, where 3,200 open roles underscore capacity gaps. Preferred-partner models prevail, mirroring broader European trends in which a single vendor assumes R&D-like responsibilities. Clients cite predictable cost structures and compliance assurance as primary motivations. This momentum lifts the Slovenia facility management market toward greater consolidation as large providers leverage economies of scale.

Growing Demand for Integrated Facility Management Solutions

Clients seek one-stop accountability that merges technical maintenance with hospitality-style services. Healthcare exemplifies this shift: AI-driven building platforms cut HVAC energy use by up to 37%, supporting patient comfort and sustainability mandates. Slovenia dedicates 20% of its EU recovery funds to digital transition, fostering environments where physical asset care and digital infrastructure monitoring coexist. New spatial-planning laws in 2025 make integrated compliance management essential. Commercial landlords echo this need, aligning facility services with workplace-experience goals to attract tenants in competitive urban markets.

Rising Focus on Workplace Experience and Employee Productivity

Inflation at 2.2% in June 2025 shrinks discretionary income and places pressure on employers to deliver engaging work environments. With 40% of new residences embedding smart-home features, employees expect comparable office amenities. Facility providers deploy indoor-air sensors, ergonomic layouts, and wellness programs that boost retention. Hybrid work increases the complexity of space planning; IoT analytics now guide real-time desk and climate optimization. Immigration-screening simplification for EU investors intensifies competition for knowledge workers, reinforcing the link between facility quality and talent attraction.

Technological Advancements in Building Management Systems

Cloud expenditure rose 35% in 2021, underpinning rapid adoption of IoT sensors and edge computing for energy and security oversight. Global smart-building stock is set to exceed 115 million by 2026, and Slovenia aligns with this trajectory through state-funded pilots. AI analytics enable predictive maintenance that halves unplanned downtime and yields double-digit energy savings. Demonstrations in Ireland and Greece recorded 61% commercial-building energy reductions via IoT retrofits, reinforcing ROI arguments. Carbon-neutrality goals further encourage the rollout of such platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled facility management professionals | -1.9% | National, with acute impact in Ljubljana and industrial regions | Short term (≤ 2 years) |

| Regulatory complexities and compliance challenges | -1.2% | EU-aligned markets with evolving legislation | Medium term (2-4 years) |

| Price sensitivity amid economic uncertainty and cost-cutting pressures | -0.8% | SME-dominated sectors and budget-constrained organizations | Short term (≤ 2 years) |

| Fragmented supplier landscape leading to inconsistent service quality | -0.6% | Regional markets with limited provider consolidation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Facility Management Professionals

The vacancy rate dipped to 2.2% in Q4 2024, yet construction and manufacturing each carried more than 3,000 unfilled roles. Digital fluency and ESG reporting skills remain scarce, and 60% of facility leaders cite talent as a top strategic risk. Immigration reforms cut permit wait times, but sector attractiveness still lags, especially among younger cohorts. Providers respond with upskilling programs and technology tools that reduce manual tasks, but short-term wage pressure persists. Labor constraints, therefore, cap the growth ceiling for the Slovenia facility management market.

Regulatory Complexities and Compliance Challenges

Overlapping amendments to environmental, spatial-planning, and construction laws in 2025 force providers to navigate more documentation and audits. EU climate disclosures add building-level emissions and energy-use reporting to lease contracts. Smaller suppliers struggle with the cost of specialized legal and technical staff, nudging clients toward larger, integrated vendors. New tax rules affecting small firms (normiranci) alter margin structures from January 2025, introducing additional uncertainty. These factors combine to slow procurement cycles and raise compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Form the Operational Core

Hard services contributed 57.21% of Slovenia's facility management market share in 2025, buoyed by aging hospitals where 70% exceed optimal lifespan. Mechanical, electrical, and plumbing upkeep anchors predictable revenue streams, while IoT-enabled asset monitoring now reduces equipment downtime by 30%. The Slovenia facility management market size for hard services is forecast to scale alongside public-sector retrofits aimed at cutting energy use. Soft services, however, post the quickest trajectory with a 13.78% CAGR as employers link workplace ambience to productivity. Cleaning, security, catering, and concierge offerings increasingly integrate wellness and sustainability metrics to meet tenant expectations.

Soft-service providers deploy sensor-based occupancy analytics to right-size staffing, yielding cost reductions that offset wage inflation. Technology convergence is blurring service lines: in hospitals, integrated hard- and soft-service contracts tie HVAC optimization to patient-experience indicators. The ensuing performance-based models encourage providers to invest in AI and robotics, elevating differentiation within the Slovenia facility management market.

By Offering Type: Outsourcing Dominates Strategic Choices

Outsourced arrangements commanded 65.85% Slovenia facility management market share in 2025 and are poised for a 12.88% CAGR to 2031. Clients view external partners as a hedge against wage volatility and regulatory risk, intensifying demand for single-invoice integrated solutions. The Slovenia facility management market size for outsourced delivery should expand as ICT firms prioritize core R&D over property logistics. Integrated contracts that bundle technical, workplace, and digital services now outpace single-service deals, supported by performance-linked KPIs.

In-house models remain in defense and heavy industry, where security protocols require tighter control; nevertheless, these organizations experiment with hybrid setups such as externally managed predictive maintenance overlays. Wage pressure from a 4.4% unemployment rate keeps the cost advantage firmly on the side of outsourcing. Vendor consolidation continues as clients trim supplier rosters to improve accountability and leverage data insights.

By End-user Industry: Commercial Leads, Institutional Accelerates

Commercial accounts—covering IT, telecom, retail, and warehousing—held 37.85% share of the Slovenia facility management market in 2025, reflecting the country’s 3,000-strong ICT company base and 35% annual cloud-adoption growth. Retail and logistics tenants demand energy-efficient warehouses and omnichannel fulfillment hubs, prompting widespread installation of smart lighting and automated cleaning solutions. The Slovenia facility management market size within institutional and public infrastructure is expanding at a 13.45% CAGR due to PPP-funded hospitals, schools, and transport projects.

Healthcare facilities present intense opportunities, as utility charges represent 77.45% of total management costs, encouraging investment in building analytics that yield rapid payback. Industrial users implement ESG-aligned retrofits to satisfy supply-chain audits, integrating real-time carbon monitoring into facility dashboards. Hospitality rebounds alongside tourism, and multi-housing developments with smart-home features push providers to deliver 24/7 remote monitoring services.

Geography Analysis

Urban hubs drive the Slovenia facility management market, with Ljubljana, Maribor, and Celje capturing the bulk of service contracts as commercial tenancy rates climb. The western coastal corridor, anchored by Koper port, records rising demand tied to tourism and logistics. Institutional spending under EU recovery funds is evenly spread, fostering facility modernization in secondary towns and rural municipalities.

Infrastructure upgrades such as the Divaca–Koper railway expand opportunity corridors, requiring technical maintenance for stations, signaling systems, and ancillary real estate. Residential building permits rose 18% since 2023, supporting geographic dispersion of soft-service requirements for new multi-housing complexes. Border regions hosting logistics depots benefit from Slovenia’s favorable trading-across-borders ranking, stimulating integrated facility contracts that blend security, warehousing, MEP upkeep, and ESG monitoring.

Demographic shifts add nuance: aging populations cluster in eastern regions, prompting specialized healthcare and senior-housing facility needs. Conversely, tech start-ups congregate in Ljubljana’s innovation districts, demanding high-spec smart-office services. These patterns ensure that the Slovenia facility management market maintains balanced growth across the country.

Competitive Landscape

Slovenia’s facility management arena remains fragmented, with international groups such as Sodexo, CBRE, and JLL competing alongside domestic specialists MG Facility Management, First Facility, and Iskra Facility Management. No single vendor dominates across all service lines, though global players leverage standardized processes to secure large multisite deals. Local firms sustain an advantage through regulatory fluency and agile service customization, particularly for smaller municipalities and niche industries.

Technology is the principal battleground. Providers integrate AI-powered work-order platforms, digital twins, and occupancy analytics to deliver outcome-based contracts. Case studies show energy cost cuts of up to 36.8 kW after implementing predictive maintenance protocols. Partnerships between facility managers and ICT firms accelerate solution rollouts; alliances such as JLL–Microsoft indoor mapping exemplify this convergence.

Consolidation intensifies as firms seek regional scale. Allied Universal’s multicountry acquisitions and Johnson Controls’ building-automation buys signal a pivot toward portfolio extension into adjacent security and energy domains. White-space remains in ESG compliance consulting and data-driven healthcare facilities, where demand outstrips current capacity within the Slovenia facility management market.

Slovenia Facility Management Industry Leaders

Sodexo Slovenia

CBRE GWS

MG Facility Management d.o.o.

First Facility d.o.o.

Diversey Slovenia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: JLL and Microsoft integrated indoor mapping technology to advance workplace digitalization.

- March 2025: Sodexo launched the “One & All” dining experience program targeting university campuses.

- March 2025: Allied Universal completed six acquisitions worth USD 240 million in annual revenue to broaden its security technology reach.

- January 2025: United Rentals acquired H&E Rentals for USD 4.8 billion, expanding equipment services linked to facility upkeep.

- January 2025: Johnson Controls continued building-automation acquisitions to deepen sustainability capabilities.

- November 2024: Sodexo won a five-year integrated workplace contract with HMRC covering 24 sites.

Slovenia Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through their responsibility for often maintaining an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation.

Facility management services involve building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further divided into hard facility management services and soft facility management services spheres.

Both in-house facility management and outsourced FM services are considered in the scope. The integrated facility management service (IFM) market, along with single and bundled services, is included in the outsourced FM services segment.

The Slovenia facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current size of the Slovenia facility management market?

The Slovenia facility management market size is USD 294.04 million in 2026 and is projected to reach USD 490.58 million by 2031.

Which service type leads the market?

Hard services lead with 57.21% market share in 2025, driven by demand for technical maintenance of aging infrastructure.

How fast is outsourced facility management growing?

Outsourced models are forecast to expand at a 12.88% CAGR between 2026 and 2031 as organizations seek specialized expertise and cost predictability.

What end-user segment is expanding the quickest?

Institutional and public infrastructure facilities are expected to grow at a 13.45% CAGR, buoyed by EU-funded modernization projects.

Why is technology investment critical for providers?

IoT and AI platforms enable predictive maintenance and energy savings that improve contract performance and differentiate service offerings.

How does Slovenia’s regulatory environment affect facility management?

New environmental and construction laws effective 2025 increase compliance complexity, favoring providers with integrated ESG and legal expertise.

Page last updated on: