Malaysia Semiconductor Foundry Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

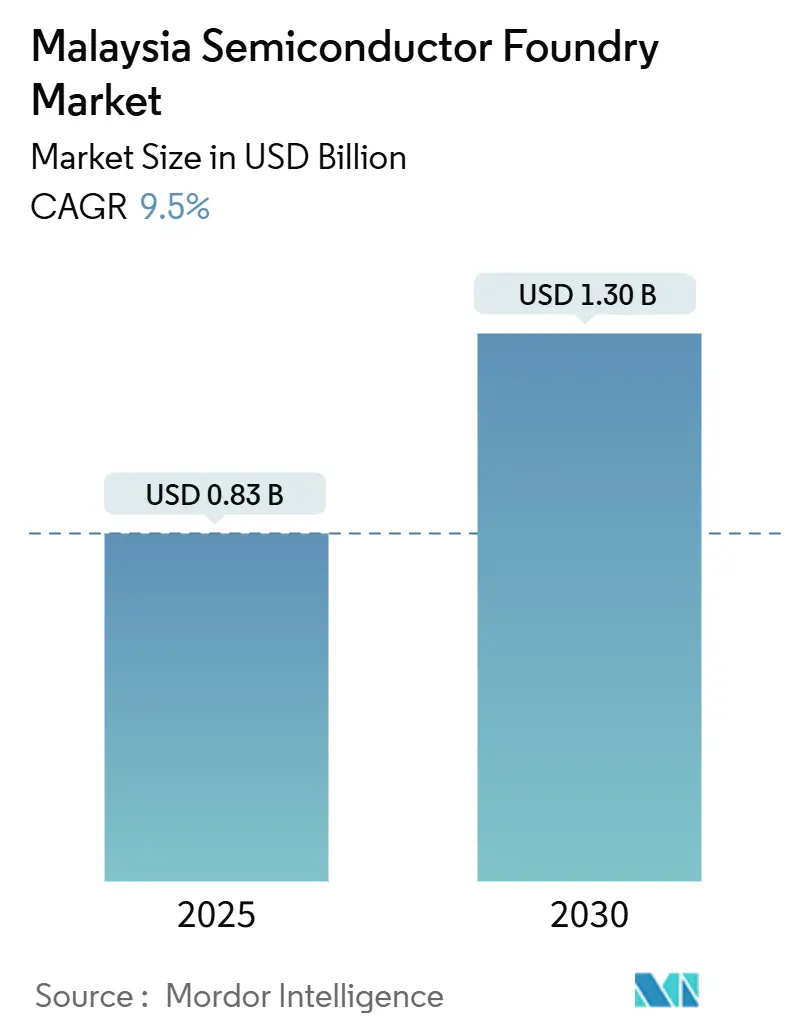

| Market Size (2025) | USD 0.83 Billion |

| Market Size (2030) | USD 1.30 Billion |

| Growth Rate (2025 - 2030) | 9.50% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malaysia Semiconductor Foundry Market Analysis by Mordor Intelligence

The Malaysia semiconductor foundry market size is valued at USD 0.83 billion in 2025 and is forecast to reach USD 1.3 billion by 2030, expanding at a 9.5% CAGR. Sustained inflows linked to “China-plus-one” diversification, a decade-long RM 25 billion (USD 5.33 billion) National Semiconductor Strategy, and over USD 25 billion of data-center and chip investments announced between 2021 and 2023 underpin the growth path for the Malaysia semiconductor foundry market.[1]South-China-Morning-Post, “Silicon rally: can Malaysia reclaim its semiconductor glory,” scmp.com Mature-node reliability for automotive electronics, accelerated demand for AI-focused high-performance computing, and expanding renewable-energy capacity that lowers fab utility costs further reinforce positive momentum. Global supply-chain realignment continues to steer advanced packaging and final test work toward Penang and Kulim, keeping average fab utilization above 85% in 2025. Meanwhile, new partnerships with ARM and other IP owners aim to close Malaysia’s design-engineering talent gap and pivot the Malaysia semiconductor foundry market toward higher-value front-end activity.

Key Report Takeaways

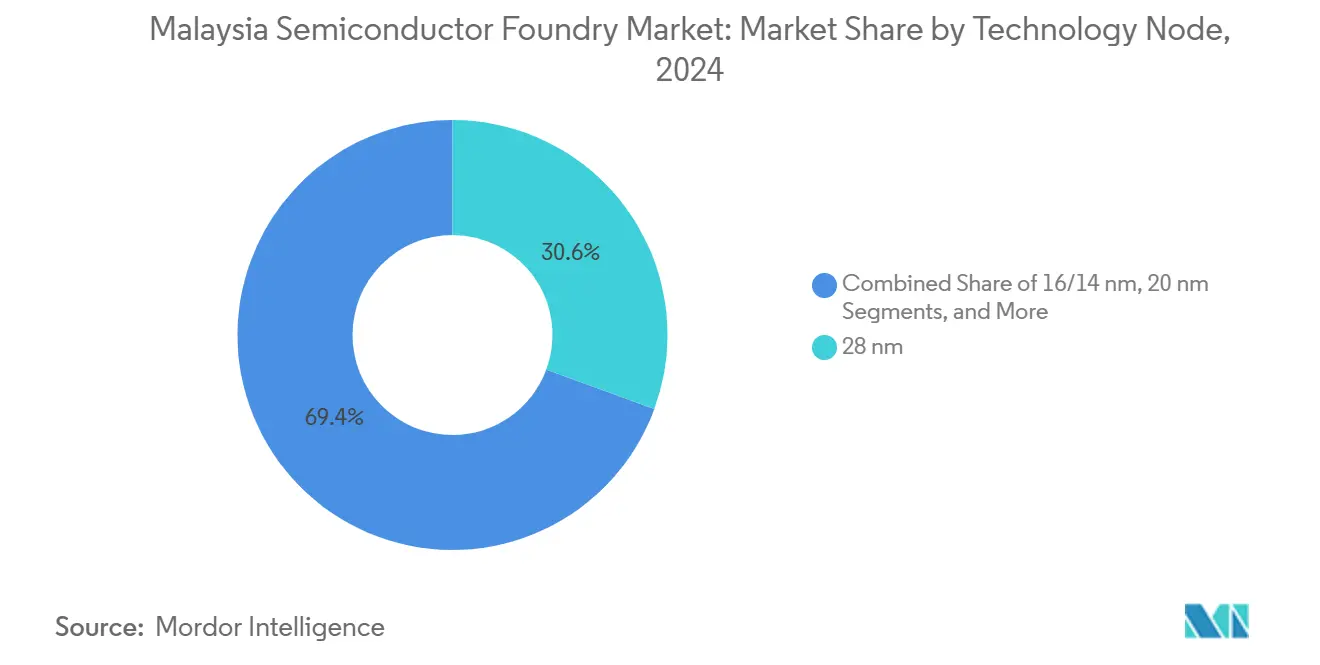

- By technology node, 28 nm processes led with 30.6% of Malaysia semiconductor foundry market share in 2024, while 10/7/5 nm nodes are projected to post a 15.2% CAGR to 2030.

- By wafer size, 300 mm production accounted for 60.4% of the Malaysia semiconductor foundry market size in 2024 and is anticipated to expand at a 12.4% CAGR through 2030.

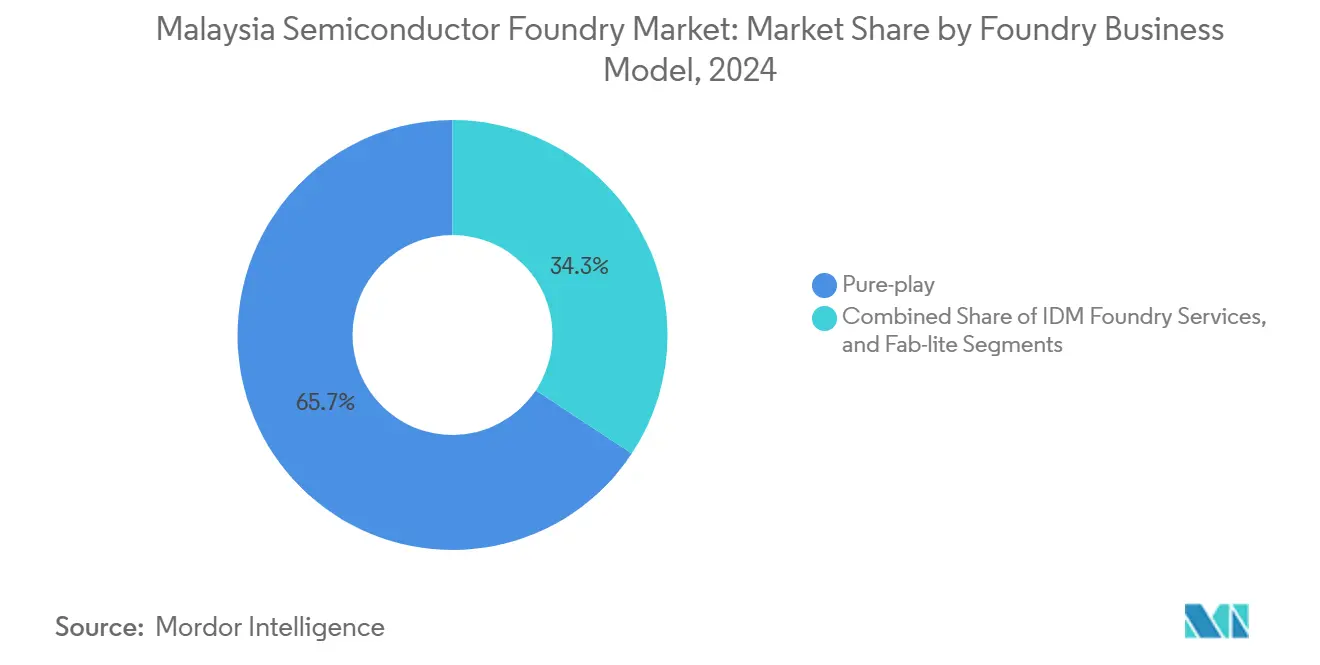

- By the foundry model, pure-play operators held a 65.7% revenue share in 2024, and their segment is forecast to grow at a 13.2% CAGR through 2030.

- By application, consumer electronics and communication commanded 40.2% of the Malaysia semiconductor foundry market size in 2024, while high-performance computing is advancing at a 15.1% CAGR to 2030.

National developments in Malaysia connect differently with activity unfolding across other parts of the world. In the global semiconductor foundry market coverage, Mordor Intelligence integrates these into a single analytical framework.

Malaysia Semiconductor Foundry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in global demand for mature-node automotive chips | +2.1% | Global, with concentration in Penang and Kulim industrial zones | Medium term (2-4 years) |

| Government incentives under Malaysia's National Investment Aspirations (NIA) | +1.8% | National, with a focus on Selangor, Penang, and Johor states | Long term (≥ 4 years) |

| Expansion of global supply-chain diversification away from mainland China | +2.3% | Global, with spillover effects across Southeast Asia | Short term (≤ 2 years) |

| Growing domestic electronics manufacturing ecosystem (EMS, OSAT, design houses) | +1.5% | National, with early gains in Penang, Kulim, and Selangor | Medium term (2-4 years) |

| Rapid adoption of silicon-photonics lines in Penang | +0.9% | Regional, concentrated in Penang, with expansion to Kulim | Long term (≥ 4 years) |

| Build-out of renewable energy sources, lowering fab operating costs | +0.7% | National, with priority in industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in global demand for mature-node automotive chips

Automotive electrification lifts demand for proven 45 nm-to-28 nm nodes that underpin battery control, power management, and sensor fusion functions. STMicroelectronics projects electric-vehicle penetration to rise from 15% of global car sales in 2023 to 40% by 2030, heightening the need for highly reliable chips that tolerate harsh thermal cycles.[2]STMicroelectronics, “Company Presentation,” st.com Malaysia hosts multiple 200 mm and 300 mm fabs qualified for automotive AEC-Q100 standards, enabling suppliers to diversify away from capacity-constrained Taiwanese and mainland Chinese plants. The automotive semiconductor shortage of 2021-2022 reinforced the strategic premium that customers place on diversified mature-node sourcing, and foundries in Penang continued to operate above 85% loading during that period. Long design cycles in automotive ensure sticky multi-year wafer orders that stabilize the Malaysia semiconductor foundry market.

Government incentives under Malaysia’s National Investment Aspirations (NIA)

The 10-year RM 25 billion (USD 5.33 billion) allocation supports grants, training, and infrastructure upgrades that move local players up the value chain from back-end assembly toward front-end design and fabrication. Targets include 60,000 engineers and 100 semiconductor-related startups, directly addressing the annual shortfall of 45,000 engineers versus industry needs. Structured partnerships such as the USD 250 million ARM agreement provide IP access alongside talent-development pipelines, ensuring that fiscal incentives translate to sustainable know-how. Combined tax holidays, streamlined permit procedures, and green-energy subsidies lower operating costs and accelerate time-to-market for new fabs in Selangor and Johor.

Expansion of global supply-chain diversification away from mainland China

Escalating U.S. export controls on advanced chips intensify “China-plus-one” realignment, and the Malaysia semiconductor foundry market sees immediate upstream pull-through. Malaysia became the single largest source of U.S. chip assembly imports in 2023, with export value to the United States climbing 12.1% in early 2024. Multinationals' route design, advanced test, and wafer-level RDL lines through Penang to leverage Malaysia’s neutral trade position. Accelerated infrastructure approvals—averaging six months compared with 18 months in neighboring economies—shorten ramp timelines and lock in commitments from cloud and AI chipset vendors.

Growing domestic EMS, OSAT, design-house ecosystem

Vertical clustering unlocks proximity benefits. Local OSAT players sit within a 30-km radius of pure-play foundries, cutting wafer transit time and enabling same-shift failure analysis. Selangor’s integrated-circuit design hub, opened in 2024, accommodates more than 400 engineers and attracts anchor tenants such as Phison. Knowledge spillovers accelerate learning cycles, while shared clean-room logistics yield double-digit savings on specialty gases and photoresist materials. The ecosystem effect drives incremental capacity reservations that support the Malaysia semiconductor foundry market through cyclical demand swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity and long pay-back period | -1.4% | Global, with a particular impact on local Malaysian companies | Long term (≥ 4 years) |

| Talent shortage in advanced-node process engineering | -1.1% | National, with acute shortages in Penang and Kulim | Medium term (2-4 years) |

| Limited local supply of ultra-pure chemicals | -0.8% | National, affecting all semiconductor manufacturing sites | Medium term (2-4 years) |

| Rising water-stress risks in Kulim and Penang industrial zones | -0.6% | Regional, concentrated in major industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital intensity and long pay-back period

Leading-edge fabs demand USD 10-20 billion outlays, and returns stretch 7-10 years. Intel’s decision in February 2025 to put its USD 9 billion Penang wafer-fab plan on hold illustrates how corporate capital budgets can pivot rapidly toward higher-margin U.S. expansions. Malaysian mid-tier firms lack domestic debt markets deep enough to finance such scale, forcing joint ventures or foreign majority ownership. Silterra’s RM 273 million (USD 61.6 million) sale to DNeX and CGP Fund in 2024 highlighted the need for external equity injections even for 200 mm specialty lines. While advanced packaging offers lower capital thresholds, the strategic aim of moving into front-end lithography remains constrained by financing hurdles.

Talent shortage in advanced-node process engineering

Universities graduate 5,000 engineers annually against industry demand for 50,000, and 15% of fresh talent migrates to higher-paying Singapore roles within one year. Extreme-ultraviolet lithography experts are particularly scarce, slowing qualification of 10 nm-class processes. ViTrox launched an internal college in 2023, but the first cohort only entered production lines in late 2026.[3]InvestPenang, “ViTrox Sets Up College to Address Talent Shortage,” investpenang.gov.my The ARM knowledge-transfer program helps, but scales gradually, making talent the rate-limiting factor that caps the top-end growth trajectory for the Malaysia semiconductor foundry market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Node: Mature nodes anchor volume while advanced nodes unlock premium pricing

The 28 nm class captured 30.6% revenue in 2024 within the Malaysia semiconductor foundry market, driven by automotive and industrial control units requiring validated reliability at extended temperature ranges. Meanwhile, 10/7/5 nm processes, though lower in immediate volume, log a 15.2% forecast CAGR on rising AI accelerator and data-center ASIC demand routed through Malaysian backend hubs. Foundry operators balance capex by dedicating greenfield space in Kulim to advanced lithography while retaining high-margin 45 nm nodes for power-management integrated circuits. The Malaysia semiconductor foundry industry, therefore, captures value across both ends of the node spectrum, reducing cyclicality associated with single-node dependency.

Malaysia semiconductor foundry market size growth at the 28 nm node is further supported by specialty embedded non-volatile memory modules that command premium pricing relative to planar SLC NAND, underscoring why mature nodes remain integral to overall profitability. Local fabs align tooling roadmaps so that older immersion steppers continue to run full shifts, ensuring equipment depreciation syncs with cash-flow generation. Advanced-node engagements often involve collaborative R&D with foreign IDMs that supply the process flow, allowing Malaysian partners to leapfrog several interim nodes without incurring excessive internal development cost.

By Wafer Size: 300 mm scale economics strengthen cost leadership

The 300 mm segment held 60.4% share of the Malaysia semiconductor foundry market size in 2024 as economies of scale lower die cost and raise gross-margin headroom. Cost per good die falls by nearly 40% when migrating from 200 mm to 300 mm at 28 nm, attracting volume orders in consumer and automotive microcontrollers. Accelerated 300 mm tool deliveries scheduled for 2025-2026 accommodate advanced copper metallization upgrades, aligning Malaysia with evolving international automotive quality audits.

Conversely, 200 mm lines remain indispensable for silicon-carbide and gallium-nitride power devices where equipment compatibility favors smaller diameters. Infineon’s Kulim investment illustrates the strategy: EUR 2 billion (USD 2.26 billion) committed to 200 mm SiC capacity in 2024, followed by a potential EUR 5 billion (USD 5.65 billion) phase-two slot to 2030. This dual-wafer strategy allows the Malaysia semiconductor foundry market to monetize both high-volume and high-value niches without stranding capital.

By Foundry Business Model: Pure-play expertise deepens design-service integration

Pure-play operators controlled 65.7% of 2024 revenue and are projected to advance 13.2% yearly through 2030 on robust customer diversification. Fabless customers value the absence of internal device divisions, which mitigates competitive risk and accelerates IP exchange. The Malaysia semiconductor foundry market benefits because pure-play plants in Penang can simultaneously fabricate automotive MCUs and data-center PHYs within adjacent clean rooms, optimizing operator learning curves.

IDM Foundry Services, while smaller, remains strategically important for clients needing traceability into vertically integrated backend analytics. Nonetheless, pure-play players attract ecosystem partners like OSAT firms and mask-set vendors, reinforcing network effects and lowering input-material freight costs. Malaysia's semiconductor foundry industry growth in the pure-play segment also stimulates local EDA tool support businesses, creating multiplier effects across the domestic supply chain.

By Application: Broad consumer base supports high-performance computing acceleration

Consumer electronics and communication represented 40.2% revenue in 2024, providing volume stability for mature nodes. High-performance computing wafer demand, however, is catching up quickly with a 15.1% CAGR projection through 2030, spurred by hyperscale data-center expansion, particularly from U.S. cloud majors committing multi-billion-dollar buildouts in Johor and Selangor. Automotive remains a sustained engine for 28 nm and 45 nm nodes thanks to electrification mandates across ASEAN capitals.

Malaysia's semiconductor foundry market size is linked to industrial and IoT applications benefit from government smart-factory incentives, keeping demand for low-power microcontrollers resilient even during handset slowdowns. As design houses co-locate with fabs, time-to-prototype shrinks from six weeks to nine days, positioning Malaysia as a rapid-turn prototyping base serving Southeast Asian OEMs. The Malaysia semiconductor foundry industry thus secures multiple demand pillars that buffer against single-application volatility.

Geography Analysis

Penang anchors approximately half of the existing installed capacity and delivers 13% of global outsourced assembly and test revenue, providing a mature vendor base that lowers procurement lead times for chemicals and photomasks. Parallel expansions in Kulim Hi-Tech Park, backed by RM 65.5 billion (USD 14.8 billion) approved investments, will double the land area to 12,000 acres under the KHTP 2 blueprint. Proximity to Bayan Lepas Free Industrial Zone enables just-in-time delivery between wafer-fab and OSAT sites, trimming logistics cycles to under 24 hours.

Selangor’s Puchong Financial Corporate Centre houses Malaysia’s first integrated circuit design hub, accommodating 400 engineers across analog, digital, and verification disciplines.[4]Asia-Nikkei, “Malaysia moves up value chain with first semiconductor park,” asia.nikkei.com The state leverages its port infrastructure at Klang to shorten equipment import clearance, adding a logistics edge for the Malaysia semiconductor foundry market. Johor’s planned special economic zone with Singapore offers fiscal incentives paired with cross-border R&D collaboration, creating a complementary manufacturing-finance cluster for advanced packaging and board-level system integration.

Sarawak enters the frame as a nascent design-services node through state-backed joint ventures aimed at indigenous CPU IP blocks. Its hydro-electric surplus could draw power-intensive wafer-bumping operations beyond 2027, adding geographic redundancy for the Malaysia semiconductor foundry market. Long-term water-stress risks in Penang and Kulim, cited by the National Water Services Commission, prompt multi-state footprint planning that diversifies operational risk and aligns with investor ESG mandates.

For the semiconductor foundry market, country-specific intelligence is available for Japan, Singapore, Taiwan, South Korea, Germany, China, United States, and Israel, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Malaysia semiconductor foundry market hosts a balanced mix of global multinationals and specialized domestic players. Infineon, STMicroelectronics, and Intel collectively control significant mature-node and power-device capacity; Infineon’s Kulim SiC line alone booked EUR 5 billion (USD 5.65 billion) in secured design wins by 2024. Pure-play domestic champion Silterra focuses on analog and embedded-flash niches, and post-acquisition plans include an RM 200 million (USD 45.1 million) capex program to lift utilization beyond 90%.

Strategic tie-ups extend competitive reach. ASE Technology Holdings leverages Penang automation labs to strengthen its IC test offerings for European automotive clients, deepening service integration. Optical-engine producer POET Technologies expanded assembly volume through Malaysian contract manufacturers in 2024 to support the targeted output of 1 million SiPh modules annually by 2026. Competitive advantage, therefore, stems from coupling specialty process expertise with packaging and test synergies rather than cost alone.

Regulatory alignment with ISO 26262 and renewable-energy procurement agreements, like STMicroelectronics’ 50 GWh solar PPA signed in Kedah, embed sustainability benchmarks that buyers increasingly treat as prerequisite supplier qualifications. Compliance differentiates incumbents and raises barriers for potential greenfield entrants, supporting moderate concentration while leaving space for niche innovators in compound-semiconductor and silicon-photonics lines.

Malaysia Semiconductor Foundry Industry Leaders

-

Silterra Malaysia Sdn. Bhd.

-

X-FAB Silicon Foundries SE (Sarawak Fab)

-

Infineon Technologies AG

-

Nexperia Malaysia Sdn. Bhd.

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Malaysia inked a USD 250 million strategic partnership with ARM Holdings to establish the company’s first ASEAN office and train 10,000 engineers.

- February 2025: Intel indefinitely postponed its USD 9 billion Penang wafer-fab project, reallocating trained engineers to U.S. sites and signaling capital-spending caution.

- August 2024: Infineon Technologies opened phase one of its 200 mm silicon-carbide power-semiconductor fab at Kulim 3 with EUR 2 billion (USD 2.26 billion) investment, creating 900 jobs and planning an additional EUR 5 billion (USD 5.65 billion) phase-two expansion.

- June 2024: Khazanah Nasional completed the divestment of Silterra to DNeX (60%) and CGP Fund (40%) for RM 273 million (USD 61.6 million), with new owners earmarking RM 200 million (USD 45.1 million) for capacity upgrades.

Malaysia Semiconductor Foundry Market Report Scope

| 10/7/5 nm and below |

| 16/14 nm |

| 20 nm |

| 28 nm |

| 45/40 nm |

| 65 nm and above |

| 300 mm |

| 200 mm |

| <150 mm |

| Pure-play |

| IDM Foundry Services |

| Fab-lite |

| Consumer Electronics and Communication |

| Automotive |

| Industrial and IoT |

| High-Performance Computing (HPC) |

| Other Applications |

| By Technology Node | 10/7/5 nm and below |

| 16/14 nm | |

| 20 nm | |

| 28 nm | |

| 45/40 nm | |

| 65 nm and above | |

| By Wafer Size | 300 mm |

| 200 mm | |

| <150 mm | |

| By Foundry Business Model | Pure-play |

| IDM Foundry Services | |

| Fab-lite | |

| By Application | Consumer Electronics and Communication |

| Automotive | |

| Industrial and IoT | |

| High-Performance Computing (HPC) | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the Malaysia semiconductor foundry market and its expected growth by 2030?

The market stands at USD 0.83 billion in 2025 and is projected to reach USD 1.3 billion by 2030, reflecting a 9.5% CAGR.

How does Malaysia benefit from “China-plus-one” supply-chain moves?

Diversification strategies redirect wafer testing, packaging, and now select front-end work to Malaysia’s established Penang and Kulim hubs, lifting capacity utilization above 85% in 2025.

Which wafer size is most widely used in Malaysian fabs?

300 mm accounts for 60.4% of 2024 output, expanding at a 12.4% CAGR as fabs pursue lower die cost and higher gross margins.

Why are mature nodes still important despite the shift toward advanced processes?

Automotive and industrial applications require proven reliability, keeping 45 nm-to-28 nm demand strong and ensuring balanced revenue streams for local foundries.

What government initiatives support Malaysia’s semiconductor ambitions?

The National Semiconductor Strategy allocates RM 25 billion (USD 5.33 billion) over 10 years for incentives, talent development, and infrastructure upgrades aimed at elevating design and fabrication capabilities.

Which recent foreign partnership focuses on chip-design talent in Malaysia?

A USD 250 million agreement with ARM Holdings launched in March 2025 to establish ARM’s first ASEAN office and train 10,000 engineers.

Page last updated on: