Malaysia Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

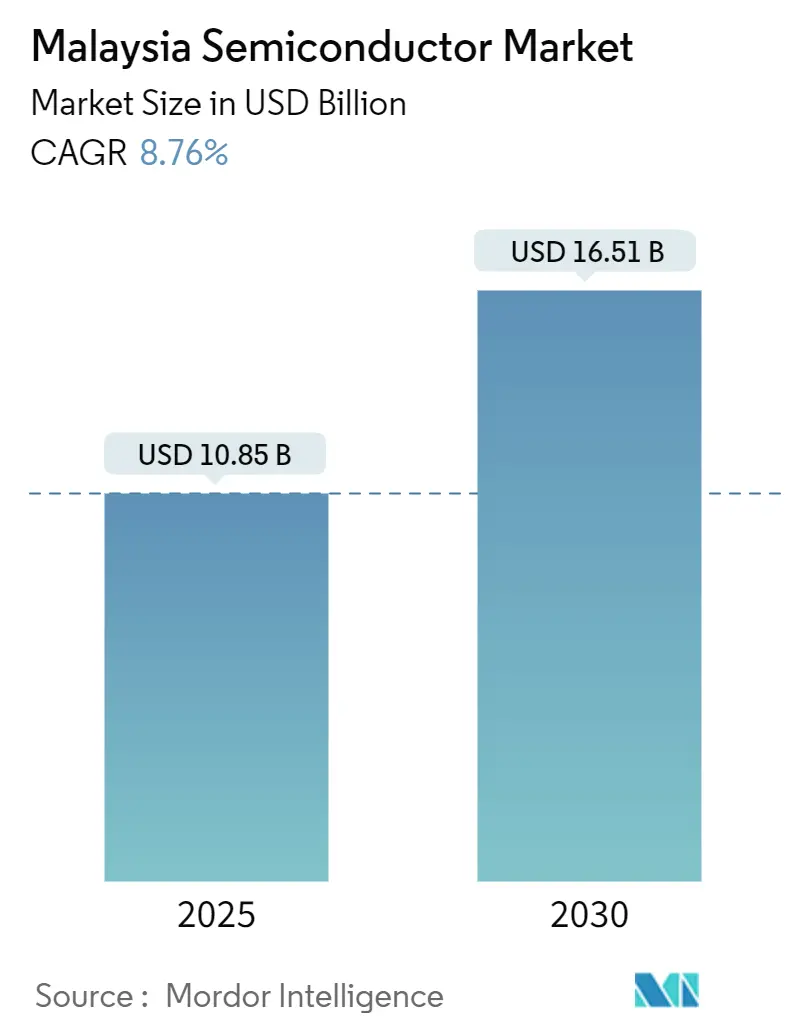

| Market Size (2025) | USD 10.85 Billion |

| Market Size (2030) | USD 16.51 Billion |

| Growth Rate (2025 - 2030) | 8.76% CAGR |

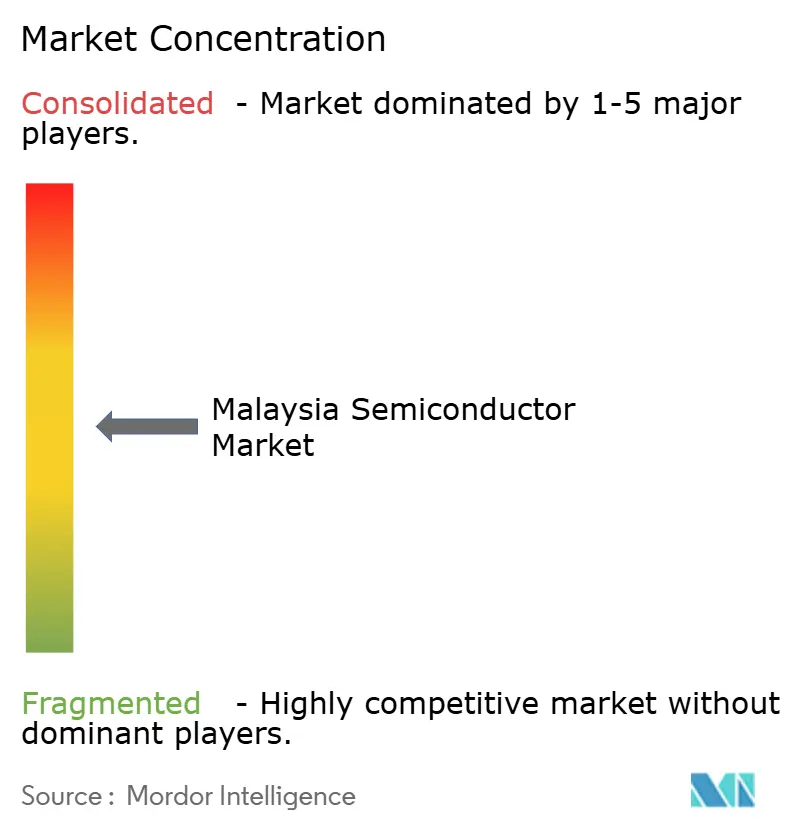

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Semiconductor Market Analysis by Mordor Intelligence

The Malaysia semiconductor market size reached USD 10.85 billion in 2025 and is projected to climb to USD 16.51 billion by 2030, translating into a 8.76% CAGR during the forecast window. A half-century production track record, more than USD 100 billion in announced capital commitments, and a government-funded RM 25 billion National Semiconductor Strategy anchor that upward path.[1]Malaysian Investment Development Authority, “National Semiconductor Strategy to guide industry up value chain,” mida.gov.my Geopolitical supply-chain rebalancing away from China directs high-value assembly and advanced packaging mandates to Malaysian sites, while an export base worth RM 575 billion (USD 130 billion) in 2024 confirms global relevance. Integrated circuits dominate factory output, but surging sensor and MEMS demand, robust incentives, and fast uptake of electric-vehicle power devices expand the opportunity set. Intensifying competition for skilled labour and reliable utilities pose headwinds that companies offset through automation, green-energy procurement, and targeted upskilling programs.

Key Report Takeaways

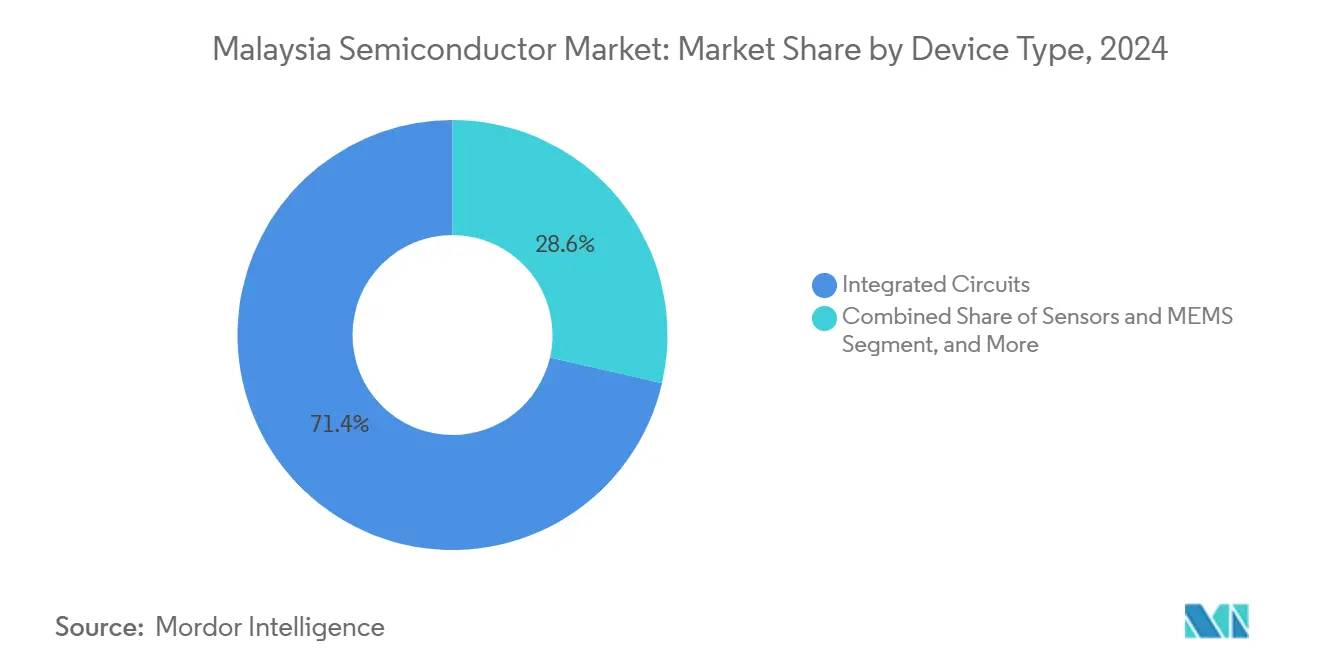

- By device type, integrated circuits led with 71.40% of Malaysia semiconductor market share in 2024. Sensors and MEMS are advancing at a 10.56% CAGR through 2030, the fastest among device categories.

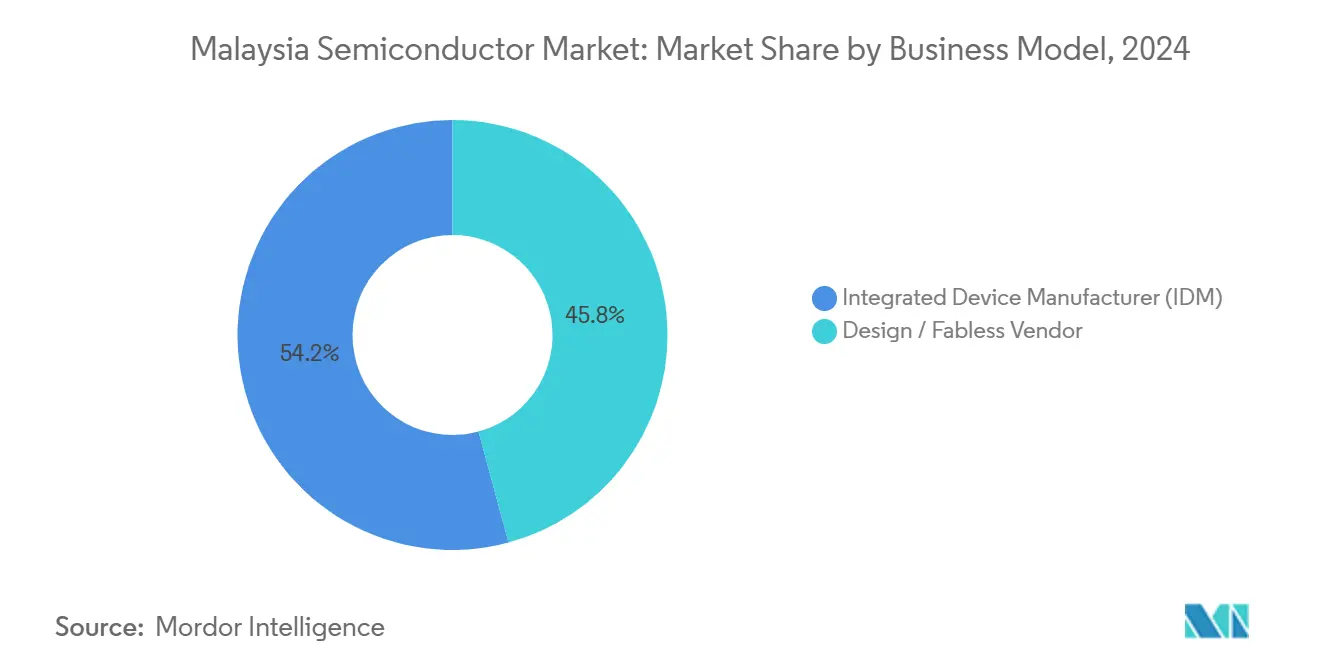

- By business model, the IDM segment held 54.20% share of the Malaysia semiconductor market size in 2024. Design and fabless vendors are projected to expand at a 9.88% CAGR to 2030.

- By end-user industry, communication applications accounted for 27.60% revenue share in 2024. AI applications record the highest forecast growth at an 11.21% CAGR through 2030.

Malaysia Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust government incentives and tax holidays | +1.80% | National, with concentration in Penang, Kedah, Selangor | Medium term (2-4 years) |

| Growing domestic demand for automotive electrification | +1.20% | National, with spillover to ASEAN automotive hubs | Long term (≥ 4 years) |

| Surge in global 5G handset outsourcing to Malaysian OSATs | +1.50% | Penang, Selangor, with regional ASEAN impact | Short term (≤ 2 years) |

| Emergence of Penang as a regional chip-testing hub | +1.00% | Penang-centric, extending to northern Malaysia | Medium term (2-4 years) |

| Green-energy PPAs lowering fab operating costs | +0.80% | National, particularly Kedah and Penang industrial zones | Long term (≥ 4 years) |

| Early adoption of advanced chiplet-based packaging | +0.70% | Penang, Cyberjaya, with technology transfer to other states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Government Incentives and Tax Holidays

The National Semiconductor Strategy allocates RM 25 billion in fiscal sweeteners that include pioneer tax status, investment allowances, and fast-track licensing. Those terms spurred over RM 1 trillion (USD 232.2 billion) in committed spending from 2021 to mid-2024, highlighted by Infineon’s EUR 7 billion silicon-carbide fab and AT&S’s EUR 1.7 billion substrate plant. Preferential corporate rates inside the Johor-Singapore Special Economic Zone widen the incentive envelope for AI and quantum startups. The predictable policy stack reduces entry risk for multinationals and speeds scale-up for local suppliers, adding positive momentum to the Malaysia semiconductor market.

Growing Domestic Demand for Automotive Electrification

Electric vehicles pack triple the semiconductor content of internal-combustion cars. Infineon’s Kulim facility, designed to serve 30% of the global silicon-carbide power market by decade-end, validates that pull factor. Malaysia’s position as an ASEAN vehicle assembly base means rising EV programs translate directly into local chip orders. Power semiconductors, battery-management ICs, and advanced driver-assistance sensors therefore underpin an incremental growth stream for the Malaysia semiconductor market.

Surge in Global 5G Handset Outsourcing to Malaysian OSATs

Leading OSATs including ASE Technology and Unisem added clean-room real estate and advanced RF testing gear to accommodate 5G handset complexity. ASE’s fifth Penang plant raised total floor space to 3.4 million sq ft.[3]ASE Holdings, “ASE expands its chip packaging and testing facility,” aseglobal.com Paired with Malaysia’s domestic 5G adoption target of 84% mobile penetration by 2029, outsourcing flows consolidate Penang’s role in global smartphone supply chains.

Emergence of Penang as a Regional Chip-Testing Hub

Over 350 foreign enterprises and 4,000 SMEs operate inside Penang’s “Silicon Island.” Decades of cumulative know-how now extend into system-in-package formats and 3D integration for automotive, AI, and industrial devices. Local equipment makers co-locate to shorten upgrade cycles, while state grants subsidize Industry 4.0 automation. These network effects keep assembly and test lead-times tight and attract future chiplet programs, supporting sustained value capture in the Malaysia semiconductor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-talent shortage in advanced IC design | -1.50% | National, acute in Penang and Cyberjaya | Short term (≤ 2 years) |

| Rising utility-rate volatility (water and power) | -0.80% | National, particularly affecting energy-intensive fabs | Medium term (2-4 years) |

| Geopolitical over-dependence on China-centric supply chain | -1.20% | National, with export-oriented facilities most exposed | Long term (≥ 4 years) |

| Limited local wafer-grade raw-material ecosystem | -0.90% | National, affecting upstream integration ambitions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Talent Shortage in Advanced IC Design

Universities deliver only 5,000 engineering graduates each year against a sector need of about 50,000, creating bottlenecks in analog layout, verification, and advanced packaging. Salary gaps with Singapore accelerate brain drain. Although the Arm-Malaysia alliance will train 10,000 engineers over a decade, near-term project ramps still rely on expatriate specialists. The talent gap restrains the speed at which the Malaysia semiconductor market can migrate upstream into IP-rich activities.

Rising Utility-Rate Volatility (Water and Power)

Power can represent up to 20% of fabrication cost, and tariff revisions tied to fuel prices inject forecasting risk. Seasonal water constraints in Kedah and Penang have already prompted fabs to invest in recycling plants and reserve ponds. Renewable-energy procurement meets ESG targets but adds balancing costs, especially for round-the-clock loads. These variables weigh on margin planning and influence site-selection decisions inside the Malaysia semiconductor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated circuits anchor revenue while sensors surge

Integrated circuits held 71.40% of Malaysia semiconductor market share in 2024, a testament to deep process expertise that spans microcontrollers, power management, and high-performance logic. Sub-segments such as analog and RF devices benefit from long-standing ties to global telecom suppliers. Memory assembly provides volume stability despite pricing swings. The shift to chiplet architecture invites higher value-added advanced packaging, helping local OSATs widen margins.

Sensors and MEMS record the fastest 10.56% CAGR through 2030, propelled by automotive safety mandates, factory automation, and wearables adoption. Malaysian lines already produce pressure, magnetic, and inertial sensors for global Tier-1 car brands. Optical and discrete power devices continue to support LED lighting and EV charger rollouts. This diversified device mix shields the Malaysia semiconductor market from mono-segment demand shocks.

By Business Model: IDM scale meets fabless agility

IDMs captured 54.20% of the Malaysia semiconductor market size in 2024, leveraging end-to-end control to protect know-how and assure supply quality. Intel, Infineon, and STMicroelectronics embed R&D, wafer processing, and test within Malaysian campuses, streamlining feedback loops. Rising labour cost and talent scarcity, however, nudge IDMs toward higher factory automation.

Design and fabless players, while smaller today, are expanding at a 9.88% CAGR as policy pushes IP creation. Newly formed IC design parks in Selangor and Penang offer subsidized EDA tools, while the USD 250 million Arm partnership lowers entry barriers to advanced processor cores. Successful IPOs of local design houses such as Oppstar underscore investor appetite. Collaboration between fabless startups and local OSATs enhances ecosystem stickiness and advances Malaysia semiconductor market sophistication.

By End-user Industry: Communications lead and AI accelerates

Communications equipment consumed 27.60% of 2024 output as global OEMs rerouted 5G radio assembly to Malaysian sites that offer neutrality and mature RF competence. Ongoing 5G base-station rollouts across ASEAN sustain RF power-amplifier demand, ensuring baseline utilization for OSATs.

Artificial intelligence workloads deliver the strongest 11.21% CAGR forecast. USD 10 billion in hyperscale data-center pledges around Johor and Cyberjaya drive orders for AI accelerators, high-bandwidth memory, and advanced substrates. Automotive, consumer, and industrial segments add balanced growth as EV penetration, smart-home gadgets, and Industry 4.0 retrofits accelerate. This diversified customer portfolio reinforces revenue stability for the Malaysia semiconductor market.

Geography Analysis

Penang anchors the Malaysia semiconductor market, hosting more than 350 multinational factories and 4,000 supporting SMEs that together account for roughly 80% of national assembly and test capacity. The island’s cluster effect shortens supply lines, integrates equipment services, and fosters rapid knowledge spillover.

Kedah’s Kulim High Tech Park rises as the advanced-fab node. Infineon’s EUR 7 billion silicon-carbide plant and AT&S’s EUR 1.7 billion substrate facility have turned Kedah into a power-device and substrate focal point. Selangor, near Kuala Lumpur, concentrates IC design houses, regional headquarters, and venture finance, leveraging airport and digital-infrastructure access to accelerate time-to-market.

Regionally, Malaysia eclipsed China in 2024 FDI inflows aimed at semiconductor supply-chain diversification, capturing USD 235 billion and reinforcing strategic neutrality.[4]Mark Kennedy et al., “How Southeast Asia can attract more FDI in chips and AI,” Wilson Center, wilsoncenter.org Competition from Vietnam and Thailand persists on cost grounds, whereas Singapore contests high-end design mandates. The Johor-Singapore Special Economic Zone intends to merge Malaysia’s manufacturing depth with Singaporean capital agility, potentially creating a cross-border innovation corridor.

Logistics strength rests on deepwater ports at Penang and Port Klang plus well-developed air-cargo links that provide 48-hour delivery windows to major Asian hubs. Vulnerabilities include dependence on imported wafers and specialty gases, which the government aims to mitigate through upstream incentive packages. Overall, geographic dispersion aligns with a climb up the value chain and underpins resilience across the Malaysia semiconductor market.

Competitive Landscape

The Malaysia semiconductor market exhibits mid-level concentration. Top global players and their local subsidiaries combine to hold near-60% of total output, while indigenous champions cover niche test, inspection, and precision-machining roles. Intel’s assembly and test mega-site, Infineon’s power-device fab, and ASE’s expanded packaging complex anchor multinational presence. Local leaders such as Inari Amertron and ViTrox specialize in RF module testing and automated optical inspection respectively, supplying multiple tier-one customers.

Strategic moves during 2024-2025 centered on capacity expansion and technology migration. ASE tripled Penang floor space to target AI and automotive demand, while Intel paused its USD 7 billion advanced-packaging investment pending global market clarity. AT&S delivered Southeast Asia’s first high-end substrate line, positioning Malaysia to capture motherboard and AI accelerator demand spikes. Collaboration agreements, such as the Arm partnership, signal transition toward IP generation and design services inside the Malaysia semiconductor market.

Competition intensity accelerates talent poaching and pushes wages upward. Firms deploy scholarships, dual-degree programs, and foreign recruitment to close gaps. Automation adoption and green-energy power purchase agreements lower cost per wafer pass and satisfy ESG mandates sought by global customers. M&A is limited but niche acquisitions in imaging-sensor test and power-module assembly are anticipated as local specialists broaden portfolios.

Malaysia Semiconductor Industry Leaders

Infineon Technologies (Malaysia) Sdn. Bhd.

Intel Technology Sdn. Bhd.

STMicroelectronics Sdn. Bhd.

Osram Opto Semiconductors (Malaysia) Sdn. Bhd.

Silterra Malaysia Sdn. Bhd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Malaysia signed a USD 250 million agreement with Arm Holdings to build local chip-design proficiency and train 10,000 engineers.

- February 2025: ASE Technology inaugurated its fifth Penang plant, expanding to 3.4 million sq ft and focusing on AI and automotive packaging.

- January 2025: AT&S opened its EUR 1.7 billion substrate facility in Kulim to supply AI systems.

- December 2024: Weeroc committed RM 20 million for a Selangor specialty-chip plant commencing early 2025.

Malaysia Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microcontrollers (MCU) | ||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microcontrollers (MCU) | |||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

What is the value of the Malaysia semiconductor market in 2025?

It is valued at USD 10.85 billion, with expansion toward USD 16.51 billion expected by 2030.

How fast is the market growing?

The market posts a 8.76% CAGR for 2025-2030, supported by incentive-driven investment inflows.

Which device category dominates Malaysian output?

Integrated circuits lead with 71.40% share, reflecting long-standing assembly and advanced packaging strength.

Why is talent availability a top challenge?

Universities supply only 5,000 engineers yearly, far short of the 50,000 professionals industry needs for IC design and advanced packaging roles.

How will electric vehicles affect semiconductor demand?

EV production triples semiconductor content per car, boosting power-device and sensor shipments from Malaysian fabs.

Where are new high-tech fabs located?

Kedah’s Kulim High Tech Park hosts silicon-carbide and substrate megaprojects, while Penang remains the center for assembly and test expansions.

Page last updated on: