Sickle Cell Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

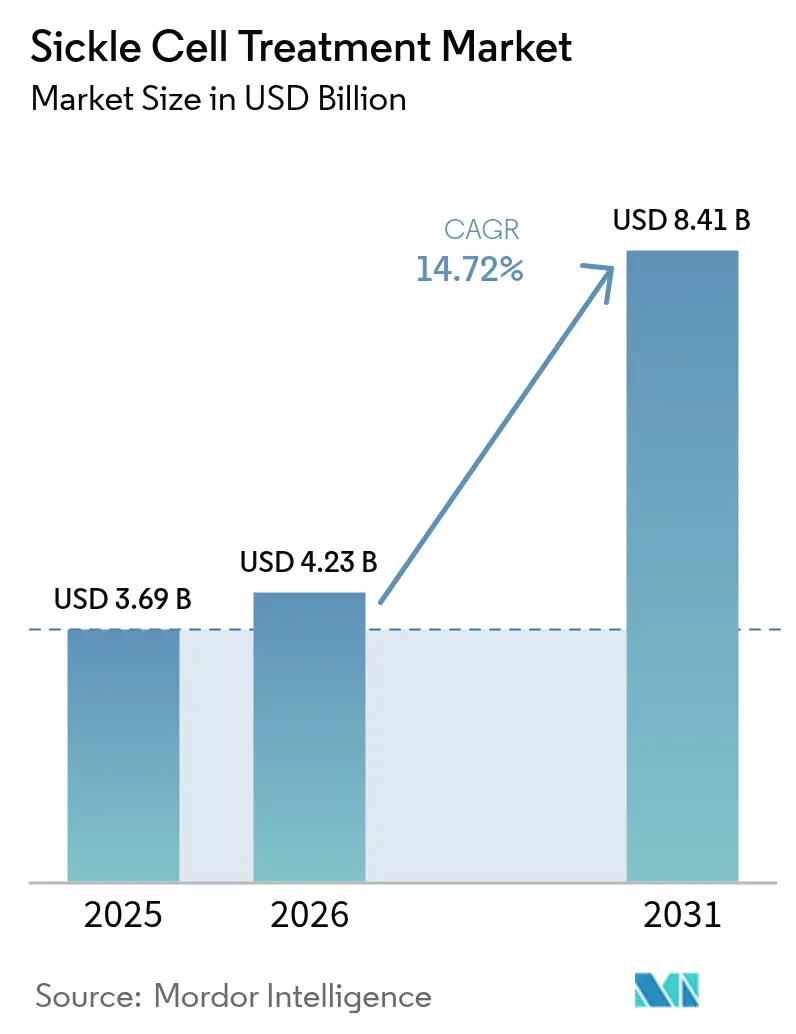

| Market Size (2026) | USD 4.23 Billion |

| Market Size (2031) | USD 8.41 Billion |

| Growth Rate (2026 - 2031) | 14.72% CAGR |

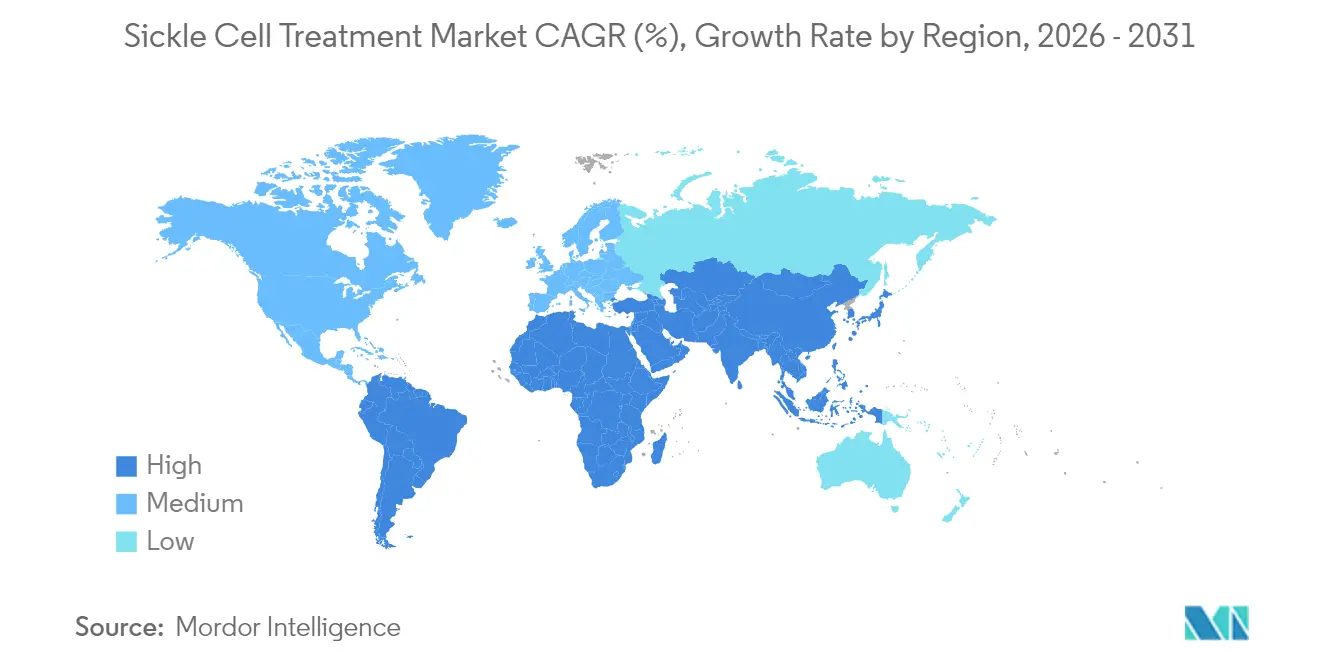

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sickle Cell Treatment Market Analysis by Mordor Intelligence

The global sickle cell treatment market size was valued at USD 3.69 billion in 2025 and estimated to grow from USD 4.23 billion in 2026 to reach USD 8.41 billion by 2031, at a CAGR of 14.72% during the forecast period (2026-2031). Accelerated growth reflects headline drivers such as gene-editing approvals, wider newborn screening, and evolving value-based payment models. Pharmacotherapy maintains the largest revenue pool, while curative gene therapies create a premium-priced, high-growth niche that redefines long-term disease management. Reimbursement experiments in North America, infrastructure rollouts in Asia-Pacific, and orphan-drug incentives across major agencies collectively reinforce demand signals. Headwinds persist in low-income regions where supply chain gaps, limited insurance coverage, and workforce shortages slow adoption of advanced therapies.

Key Report Takeaways

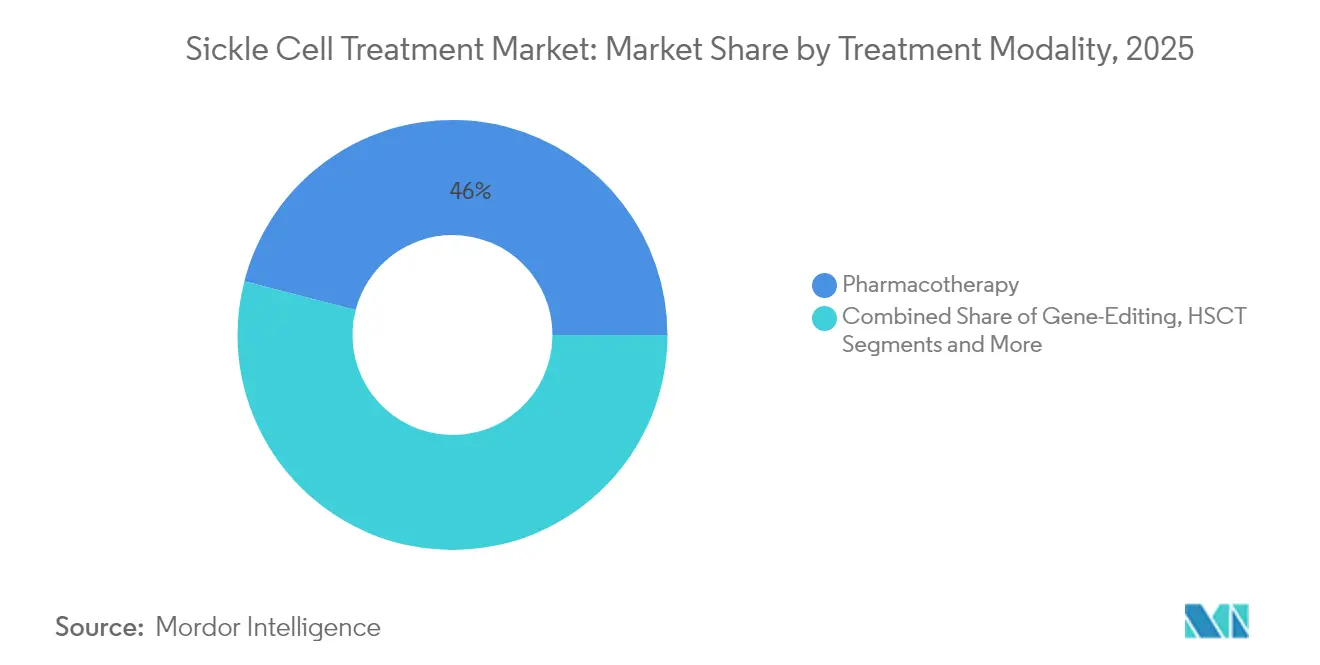

- By treatment modality, pharmacotherapy led with 45.97% of the sickle cell treatment market share in 2025, while gene-editing therapies are forecast to expand at a 17.05% CAGR through 2031.

- By patient age group, the pediatric segment accounted for 50.12% of the sickle cell treatment market size in 2025, whereas the adult segment is projected to rise at a 15.76% CAGR to 2031.

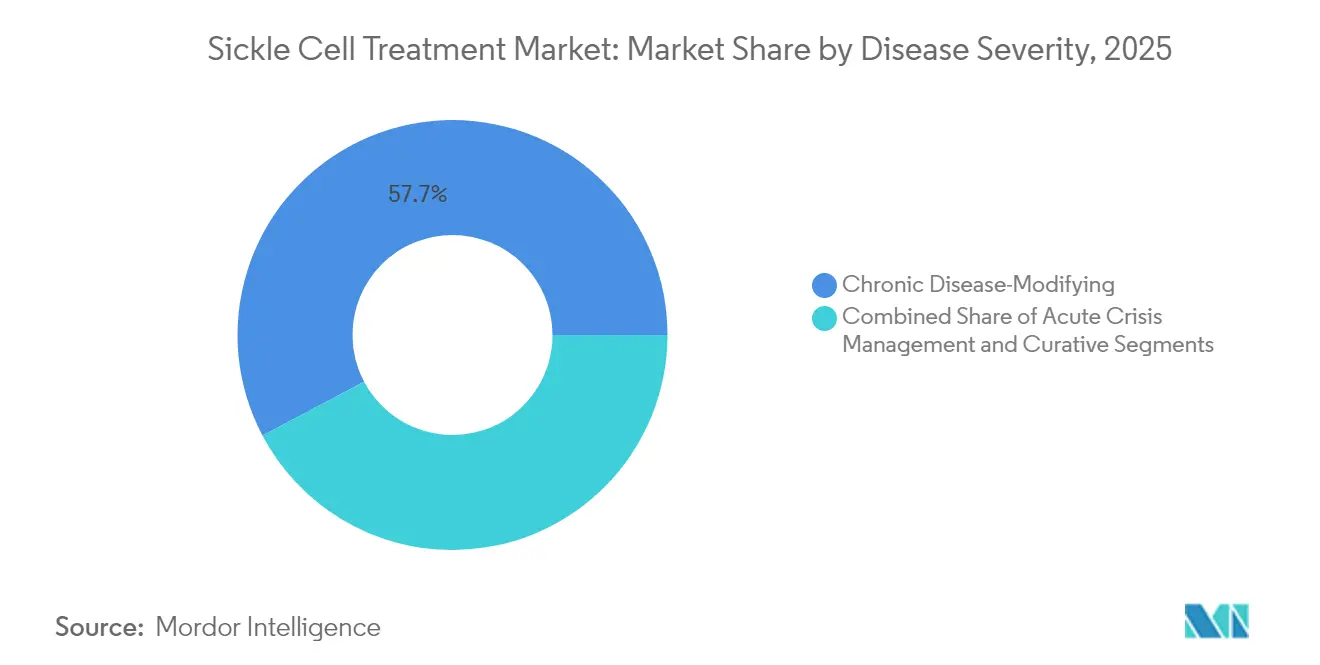

- By disease severity, chronic disease-modifying treatments held 57.74% share of the sickle cell treatment market size in 2025, while curative approaches are advancing at an 18.12% CAGR over the same period.

- By end-user, hospitals dominated with 59.05% revenue share in 2025, while ambulatory surgical centers are expected to grow at a 15.44% CAGR through 2031.

- By geography, North America led with 35.92% of sickle cell treatment market share in 2025, yet Asia-Pacific is poised for the fastest expansion at a 15.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sickle Cell Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of sickle-cell mutations | +2.1% | Global with focus on Sub-Saharan Africa and Middle East | Long term (≥ 4 years) |

| Robust late-stage R&D pipeline | +3.2% | North America and Europe with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Regulatory fast-track and orphan-drug incentives | +2.8% | Global led by FDA and EMA | Short term (≤ 2 years) |

| Commercial rollout of disease-modifying drugs | +2.4% | North America expanding to Europe and Middle East | Medium term (2-4 years) |

| Expansion of newborn screening in Sub-Saharan Africa | +1.9% | Sub-Saharan Africa with pilot programs in Asia | Long term (≥ 4 years) |

| Value-based reimbursement for curative gene editing therapies | +1.8% | North America with early adoption in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Sickle-Cell Mutations

Global births affected by sickle cell disease reached 515,000 in 2021, and annual mortality remains high at 376,000 deaths, sustaining multi-regional demand for therapeutic interventions. Nigeria drives one-third of the global patient pool, while migration elevates case numbers in Europe and the Gulf. National registries in Saudi Arabia track 22,956 patients across state facilities, enabling care coordination and real-world data capture.[1]Hoda Ezzat, “Revealing the Power of Disease Registries in Real-World Patient Care and Research – The Saudi National Sickle Cell Disease Registry Success Story,” HemaSphere, journals.lww.com Longevity gains in high-income countries create a second surge of adult patients who require long-term disease-modifying or curative options.

Robust Late-Stage R&D Pipeline

Clinical momentum remains strong as gene editors, metabolic modulators, and epigenetic regulators advance through Phase 2 and Phase 3 programs. Etavopivat shows reduction in vaso-occlusive crises, mitapivat targets red cell metabolism, and next-generation agents such as Novartis dWIZ-1 and Fulcrum’s epigenetic candidates broaden mechanisms of action.[2]Evelyn Harlow, “Make Gene Therapies More Available by Manufacturing Them in Lower-Income Nations,” Nature, nature.com Trial designs integrate patient-reported outcomes and real-world evidence, streamlining approval packages and lowering commercialization risk.

Regulatory Fast-Track & Orphan-Drug Incentives

The US FDA cleared exagamglogene autotemcel (Casgevy) and lovotibeglogene autotemcel (Lyfgenia) within a year of each other, demonstrating unprecedented acceleration under breakthrough therapy status and priority review. EMA alignment shortens European access timelines and provides unified reference pricing for payers.[3]Edward R. Scheffer-Cliff, “High Prices for Gene Therapies in Sickle Cell Disease,” JAMA, jamanetwork.com Tax credits and seven-to-ten-year exclusivity windows enhance return-on-investment for developers targeting small populations.

Commercial Rollout of Disease-Modifying Drugs

Voxelotor, crizanlizumab, and L-glutamine expanded treatment beyond hydroxyurea monotherapy, underscoring appetite for combination regimens that better control vaso-occlusive crises. Pfizer’s 2024 withdrawal of voxelotor due to safety issues highlights post-marketing surveillance importance, yet sustained real-world efficacy of crizanlizumab preserves confidence in disease-modifying pathways fiercepharma.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of care and single-use gene editing prices | -2.9% | Global with greatest strain in emerging markets | Long term (≥ 4 years) |

| Limited matched-donor availability for HSCT | -1.4% | Worldwide with higher deficit in genetically diverse regions | Long term (≥ 4 years) |

| Cold-chain and infusion-centre infrastructure gaps in LMICs | -2.1% | Sub-Saharan Africa plus parts of Asia and Latin America | Medium term (2-4 years) |

| Uneven insurance coverage and benefit-design exclusions | -1.8% | Global with variability by payer model | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Care & Single-Use Gene-Editing Prices

Commercial list prices of USD 2.2 million for Casgevy and USD 3.1 million for Lyfgenia create affordability stress despite projected lifetime savings from reduced hospitalizations. Bluebird Bio established more than 70 treatment centers, yet uptake stalled as payers negotiated outcome-linked payment schedules. Additional costs for conditioning, hospitalization, and monitoring inflate total spending envelopes, delaying widespread access.

Cold-Chain & Infusion-Centre Infrastructure Gaps in LMICs

Many high-burden African countries lack reliable electricity, advanced laboratories, and trained infusion teams required for ex-vivo gene therapy. WHO’s 2024 guidelines outline staged capacity building and financing pathways but execution remains slow. Logistics barriers persist despite philanthropic support for technology transfer and workforce training.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Gene Editing Drives Premium Growth

Gene editing commanded the fastest trajectory with a 17.05% CAGR between 2026 and 2031, reflecting strong payer interest in one-time curative interventions. Pharmacotherapy retained 45.97% of revenue in 2025, underscoring entrenched demand for hydroxyurea and recently introduced disease-modifying drugs. The sickle cell treatment market size for pharmacotherapy reached USD 1.7 billion in 2025, while gene-editing’s share was smaller but accelerating following Casgevy and Lyfgenia approvals. Stem cell transplantation continues to face donor limitations and conditioning-related morbidity that restrict procedural volumes.

Bluebird Bio and Vertex selected divergent roll-out strategies. Bluebird prioritized broad treatment-site certification, whereas Vertex focused on streamlined patient funneling through 35 hubs to improve throughput. Tessera Therapeutics explores in-vivo gene writers that could bypass harvesting and reinfusion steps, potentially lowering cost-to-serve and expanding the sickle cell treatment market in resource-limited settings.

By Patient Age Group: Adult Segment Accelerates

Adult patients aged 18-49 posted a 15.76% CAGR, supported by survival gains and inclusion in gene-therapy eligibility criteria. The pediatric segment held a 50.12% sickle cell treatment market share in 2025, backed by mandatory screening and early intervention programs. Saudi registry averages indicate a patient age of 28 years, reflecting successful transition to adult care.

Higher age groups bring cumulative organ complications, driving combination therapy regimens and multidisciplinary follow-up. Adult uptake of gene therapy is rising where financing and clinical capacity align, enlarging the sickle cell treatment market size for advanced modalities.

By Disease Severity: Curative Approaches Transform Care

Curative and potentially curative options grew at 18.12% CAGR and captured early adopters who experience severe, recurrent crises. Chronic disease-modifying agents held 57.74% of 2025 revenue, driven by hydroxyurea, crizanlizumab, and L-glutamine. Acute crisis interventions remain critical to all severity bands and anchor hospital spending. Lyfgenia resolved severe vaso-occlusive events in 94% of treated patients, while Casgevy sustained freedom from severe crises in 97% over one year.

Demonstrated durability of benefit is refocusing payer calculus from repetitive chronic expenditures to single-event cures. This pivot is expected to broaden the sickle cell treatment industry’s investment-case diversity, attracting capital to both disruptive and complementary platforms.

By End-User: Ambulatory Centers Gain Traction

Hospitals retained 59.05% of sales in 2025 given their role in emergency management and conditioning regimens, yet ambulatory surgical centers advanced at 15.44% CAGR as outpatient gene-therapy protocols gained regulatory acceptance. Network certification programs underpin reliable service quality.

Bluebird’s 70-strong site roster and Vertex’s 35-hub model underscore the on-going shift toward specialized, high-throughput centers of excellence. Academic institutes sustain trials and translational research, fuelling next-wave technology validation and education pipelines.

Geography Analysis

North America commanded 35.92% revenue in 2025 due to early approvals, high insurance coverage, and dense specialist networks. The United States remains the policy trendsetter, designing value-based payment models through CMS that influence global reimbursement debate. Canada and Mexico leverage provincial and social security frameworks to subsidize costly therapies, although adoption rates vary by province and funding cycle. Cross-border collaborations allow Mexican patients to access US centers, expanding treatment choices.

Asia-Pacific carries the highest growth momentum at a 15.93% CAGR. India’s National Sickle Cell Anaemia Elimination Mission implements universal screening across 17 states, integrating patient education and subsidized pharmacotherapy. The initiative enlarges the diagnosed pool and creates procurement scale for generics. Malaysia, Thailand, and Indonesia report that 78% of providers highlight treatment affordability as a primary barrier, reinforcing demand for cost-effective innovation. Regional governments negotiate tiered pricing to balance public budgets and patient outcomes, paving the way for eventual curative therapy roll-out once infrastructure matures.

Europe exhibits steady adoption anchored by strong social insurance systems and EMA regulatory synchrony. Germany and France reimburse gene editing under risk-sharing deals, while the United Kingdom pilots annuity payment structures to spread cost across budget cycles. Middle East and Africa are bifurcated. Gulf states, led by Bahrain’s first CRISPR treatment outside the United States, invest heavily in precision medicine. Sub-Saharan Africa, despite highest prevalence, confronts infrastructure limits that dull near-term adoption of advanced products. WHO’s 2024 guideline package directs donor funding toward lab capacity, workforce training, and supply-chain resilience.

Competitive Landscape

Market concentration is moderate. Vertex Pharmaceuticals and CRISPR Therapeutics enjoy first-mover advantage in gene editing through Casgevy, securing premium positioning and brand recognition. Bluebird Bio offers the sole alternative autologous gene therapy but wrestles with slower enrollment tied to financing complexity. Novartis spans both conventional and next-generation segments with hydroxyurea generics, crizanlizumab, and a pipeline of targeted agents. Pfizer’s exit from voxelotor underscores volatility in post-launch safety surveillance.

Emergent technology differentiators include in-vivo gene writers, lipid nanoparticle delivery, and oral modulators aimed at hemoglobin polymerization. Tessera Therapeutics, backed by the Gates Foundation, pursues single-dose intravenous administration that could disrupt resource-intensive ex-vivo protocols. Generic manufacturers hold volume leadership in hydroxyurea, preserving cost-effective options for public programs in Africa and South Asia. Competitive battlegrounds now extend beyond molecules to integrated care models, site certification, and real-world data partnerships that demonstrate durability and health-economic value.

Sickle Cell Treatment Industry Leaders

Novartis AG

Sanofi SA

Pfizer

Vertex Pharmaceuticals Inc.

CRISPR Therapeutics AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vascarta Inc. received FDA Orphan Drug Designation for VAS-101 to treat sickle cell disease.

- February 2025: Bahrain Oncology Centre completed the first CRISPR-based Casgevy treatment outside the United States, positioning Bahrain as a precision-medicine hub.

- December 2024: Tessera Therapeutics secured USD 50 million from the Gates Foundation for in-vivo gene-editing development.

- September 2024: Pfizer voluntarily withdrew all lots of Oxbryta (voxelotor) from global markets.

Global Sickle Cell Treatment Market Report Scope

As per the scope of the report, sickle cell is a group of disorders that cause red blood cells to become misshapen and break down. With sickle cell disease, an inherited group of disorders, red blood cells contort into a sickle shape. The cells die early, leaving a shortage of healthy red blood cells (sickle cell anemia), and can block blood flow, causing pain (sickle cell crisis).

The sickle cell treatment market is segmented by treatment modality, end-user, and geography. By treatment modality, the market is segmented into bone marrow transplant, blood transfusion, and pharmacotherapy. By end user, the market is segmented into hospitals, specialty clinics, and other end users. Other end-users include research laboratories and academic institutes, blood banks and transfusion centers, among others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.

| Blood Transfusion | |

| Hematopoietic Stem-Cell Transplant (HSCT) | |

| Pharmacotherapy | Hydroxyurea |

| L-Glutamine | |

| Voxelotor | |

| Crizanlizumab | |

| Others (incl. Pain-management, Folic Acid) | |

| Gene-Editing / Gene-Addition Therapies |

| Paediatric (0–17 yrs) |

| Adult (18–49 yrs) |

| Older Adult (50 yrs +) |

| Acute Crisis Management |

| Chronic Disease-Modifying |

| Curative / Potentially Curative |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Modality | Blood Transfusion | |

| Hematopoietic Stem-Cell Transplant (HSCT) | ||

| Pharmacotherapy | Hydroxyurea | |

| L-Glutamine | ||

| Voxelotor | ||

| Crizanlizumab | ||

| Others (incl. Pain-management, Folic Acid) | ||

| Gene-Editing / Gene-Addition Therapies | ||

| By Patient Age Group | Paediatric (0–17 yrs) | |

| Adult (18–49 yrs) | ||

| Older Adult (50 yrs +) | ||

| By Disease Severity / Clinical Objective | Acute Crisis Management | |

| Chronic Disease-Modifying | ||

| Curative / Potentially Curative | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centres | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the sickle cell treatment market?

The sickle cell treatment market size is valued at USD 4.23 billion in 2026 with a projected USD 8.41 billion value by 2031.

Which treatment modality is growing the fastest?

Gene-editing therapies are expanding at a 17.05% CAGR, reflecting early adoption of curative options such as Casgevy and Lyfgenia.

Why is Asia-Pacific expected to grow rapidly?

Government initiatives like India’s National Sickle Cell Anaemia Elimination Mission, improved screening, and rising healthcare investment propel a 15.93% CAGR in the region.

How do high therapy prices affect market growth?

List prices above USD 2 million limit access, reduce uptake speed, and subtract up to 2.9% from the forecast CAGR where financing mechanisms are weak.

What reimbursement models are emerging for curative therapies?

Value-based agreements such as CMS’s Cell and Gene Therapy Access Model tie payments to long-term patient outcomes to mitigate high upfront costs.

What years does this Sickle Cell Treatment Market cover, and what was the market size in 2025?

In 2025, the Sickle Cell Treatment Market size was estimated at USD 4.23 billion. The report covers the Sickle Cell Treatment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Sickle Cell Treatment Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: