Mesenchymal Stem Cells Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

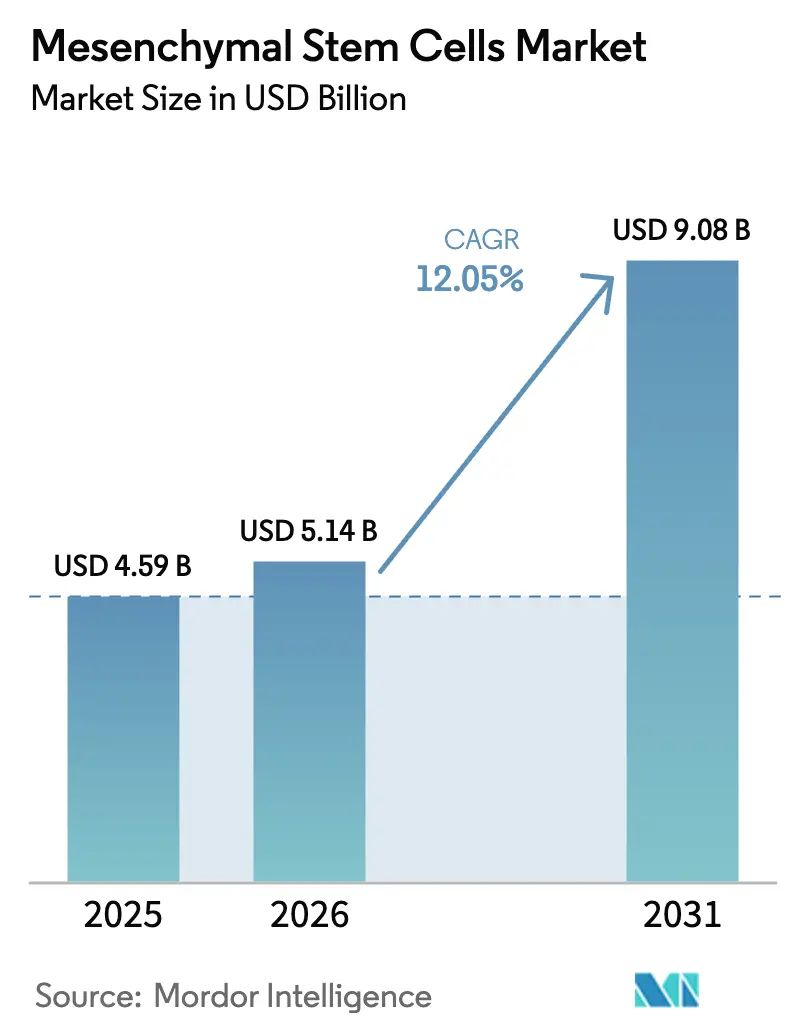

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 9.08 Billion |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

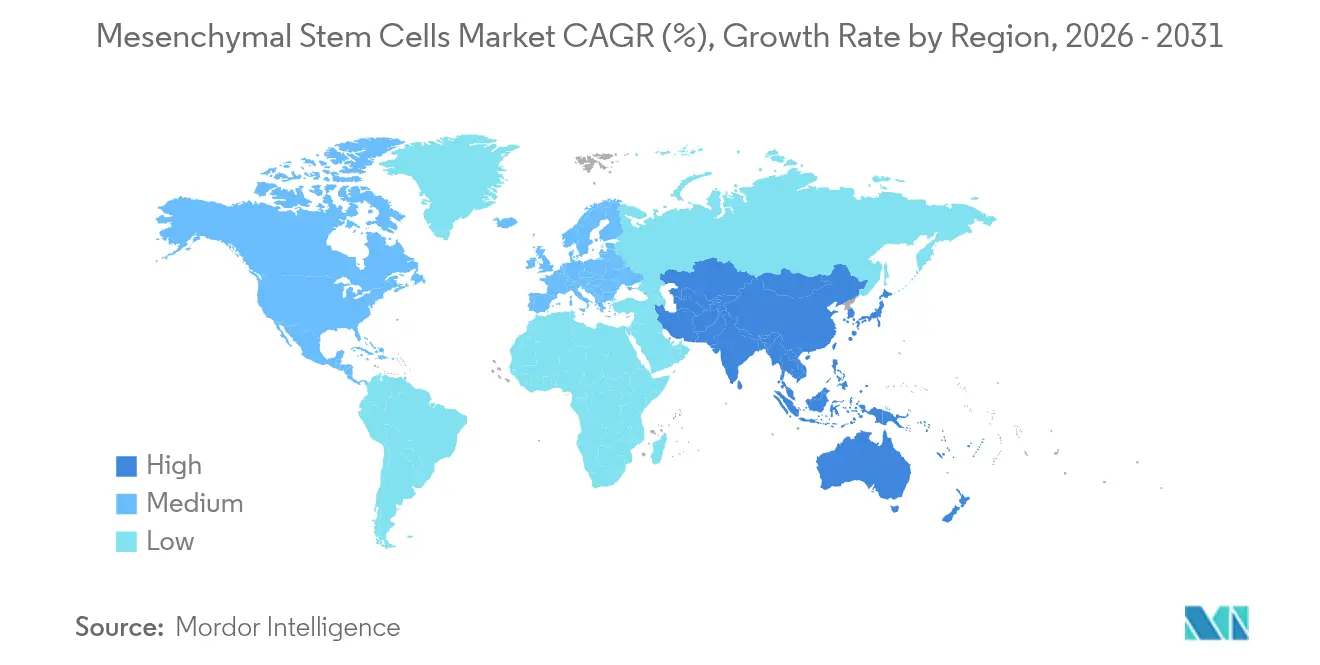

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mesenchymal Stem Cells Market Analysis by Mordor Intelligence

The Mesenchymal Stem Cells market size is expected to grow from USD 4.59 billion in 2025 to USD 5.14 billion in 2026 and is forecast to reach USD 9.08 billion by 2031 at 12.05% CAGR over 2026-2031.

This steady rise reflects a transition from bench-side experimentation to commercial therapies as regulatory bodies accelerate approvals and companies scale manufacturing. Ryoncil’s 2024 clearance as the first allogeneic mesenchymal stromal cell product validated the therapeutic class and set a precedent for subsequent filings, while North American insurers, venture investors, and hospital systems are synchronizing reimbursement, funding, and clinical infrastructure. In parallel, Asian regulators are fast-tracking reviews, creating a dual-speed expansion in which established economies focus on manufacturing scale and emerging economies build regulatory capacity. Competitive momentum is tilting toward firms that combine proprietary cell lines with end-to-end bioprocessing platforms, and diversified pharmaceutical groups are purchasing or partnering with contract manufacturers to secure supply resilience. As a result, the mesenchymal stem cells market is expected to crystallize around providers that can deliver consistent potency, transparent analytics, and compelling health-economic evidence.

Key Report Takeaways

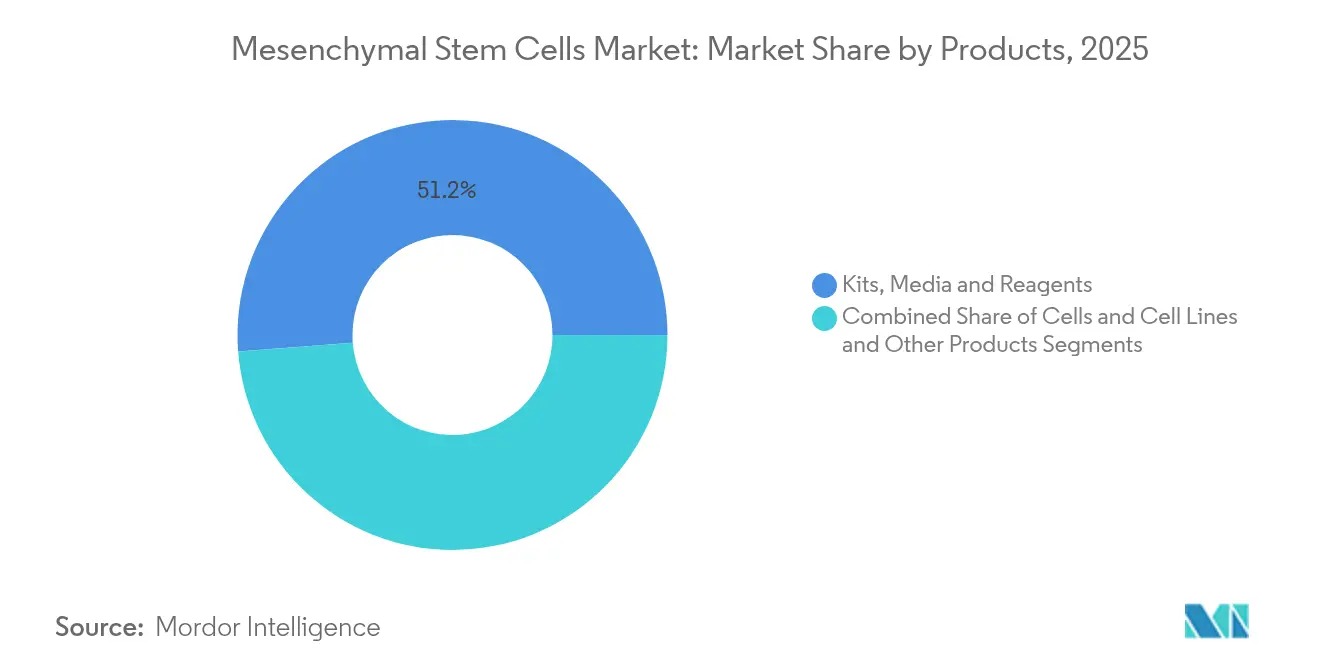

- By products, kits, media and reagents led with 51.23% revenue share in 2025, while cells and cell lines are forecast to expand at a 13.28% CAGR to 2031.

- By type, the allogeneic segment held 58.66% of the mesenchymal stem cells market share in 2025, whereas autologous approaches are projected to grow at a 13.31% CAGR through 2031.

- By source, bone marrow accounted for 33.74% of the mesenchymal stem cells market size in 2025; adipose tissue–derived cells are advancing at a 13.86% CAGR over the same horizon.

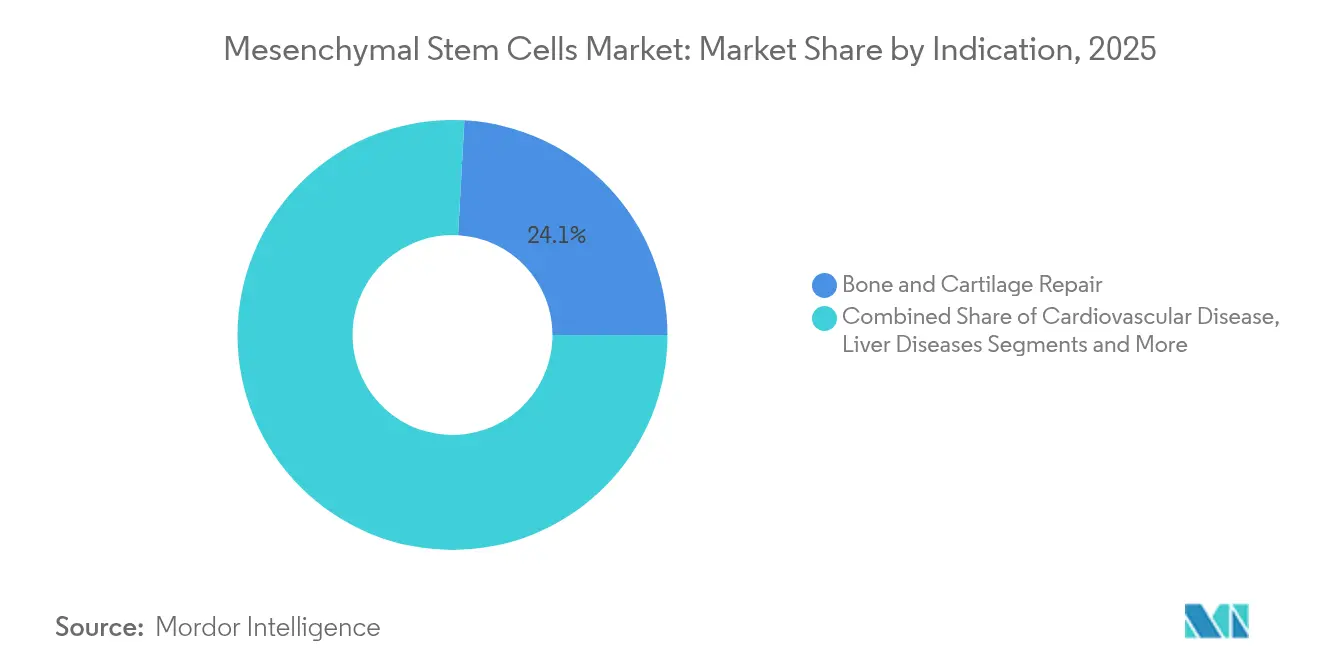

- By indication, bone and cartilage repair captured 24.12% revenue share in 2025, whereas cardiovascular applications are expected to accelerate at a 14.01% CAGR between 2026-2031.

- By geography, North America led with 40.78% market share in 2025, while Asia-Pacific is set to post the fastest 14.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Mesenchymal Stem Cells Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Degenerative and Autoimmune Disorders | +2.1% | Global, with concentration in aging populations of North America and Europe | Long term (≥ 4 years) |

| Expanding Global Pipeline of MSC Clinical Trials and IND Filings | +1.8% | North America and Europe leading, Asia-Pacific accelerating | Medium term (2-4 years) |

| Scaling cGMP Manufacturing Capacity and Contract Development Services | +1.6% | North America and Europe, with emerging capabilities in Asia-Pacific | Medium term (2-4 years) |

| Advances in off-the-shelf Allogeneic MSC Products | +1.4% | Global, with regulatory leadership in US and EU | Medium term (2-4 years) |

| Accelerated Regulatory Pathways for MSC-Derived Exosome Therapeutics | +1.2% | US and EU leading, gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of Point-of-Care Closed-Loop Bioreactors in Orthopaedic Clinics | +0.9% | North America and Europe, limited penetration in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Degenerative and Autoimmune Disorders

Cardiovascular use cases are the fastest-growing indication at a 14.29% CAGR, underscoring how clinicians are extending MSC therapy beyond orthopaedics toward systemic inflammatory diseases. Optimized licensing regimens that prime cells with interferon-gamma and tumor necrosis factor-alpha enhance immunomodulation, fueling demand in heart failure, stroke, and chronic inflammatory conditions.[1]Source: Y. Wu et al., “Fine-Tuning Licensing Strategies to Boost MSC-Based Immunomodulatory Secretome,” Stem Cell Research & Therapy, stemcellres.biomedcentral.com Persistent demographic aging in the United States, Japan, and Western Europe sustains long-term procedure volumes, while emerging economies confront lifestyle-driven degenerative burdens. The wide disease spectrum broadens revenue streams and mitigates single-indication risk, yet compels manufacturers to maintain indication-specific analytics and potency assays. Payers are beginning to evaluate cost offsets from reduced hospitalizations, improving reimbursement prospects in high-burden chronic diseases.

Expanding Global Pipeline of MSC Clinical Trials and IND Filings

More than 1,200 interventional studies were active worldwide in 2025, with Phase III programs targeting back pain, acute myocardial infarction, and diabetic foot ulcers. The FDA’s 2024 draft guidance on allogeneic cell safety testing harmonized potency assays and contamination screens, lowering regulatory ambiguity. Sponsors are shifting trials to multi-regional platforms that blend US, EU, and Asia-Pacific sites to accelerate enrollment and build country-specific pricing dossiers. Increased clarity around master cell bank characterization and release specifications is drawing institutional investors, bridging historic funding gaps and pushing the mesenchymal stem cells market deeper into phase-driven value inflections.

Scaling cGMP Manufacturing Capacity and Contract Development Services

Contract development and manufacturing organizations (CDMOs) such as Thermo Fisher are commissioning dedicated cleanrooms, analytics suites, and cryogenic logistics to handle autologous and allogeneic batches. Automation via closed-loop bioreactors is cutting labor costs while minimizing batch-to-batch variability, a pivotal hurdle for commercial scale. Capital-intensive expansions in British Columbia and Texas illustrate how regional governments now view cell-therapy factories as strategic assets that attract life-science clusters. Early-stage developers increasingly outsource process development to CDMOs, compressing time-to-clinic and allowing leaner operating models. These dynamics are transforming the mesenchymal stem cells market into an ecosystem where manufacturing know-how equals therapeutic IP.

Advances in Off-the-Shelf Allogeneic MSC Products

Allogeneic candidates leverage established master cell banks to meet population-scale demand without donor matching, lowering per-patient cost relative to autologous regimens. Ryoncil’s USD 194,000 list price signals premium reimbursement headroom in high-mortality pediatric graft-versus-host disease. Uniform formulation and centralized filling reduce cold-chain nodes and simplify hospital pharmacy workflows. Nevertheless, innate immune activation remains a residual risk, motivating post-market surveillance and biomarker-guided patient selection. Most pipeline developers are pairing allogeneic cells with exosome co-the rapies to reinforce anti-inflammatory durability, solidifying the mesenchymal stem cells market’s shift toward ready-to-infuse biologics.

Restraints Impact Analysis of Mesenchymal Stem Cells Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Harmonised Global GMP and Potency Standards | -1.9% | Global, with particular challenges in cross-border product registration | Long term (≥ 4 years) |

| High Treatment Cost and Uncertain Reimbursement Landscape | -1.6% | North America and Europe primarily, emerging impact in Asia-Pacific | Medium term (2-4 years) |

| Donor-to-donor Biological Variability Influencing Batch Consistency | -1.2% | Global manufacturing challenge, more pronounced in autologous approaches | Medium term (2-4 years) |

| Competition from iPSC-derived cell Therapies | -0.8% | Advanced markets with strong R&D capabilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Harmonised Global GMP and Potency Standards

Divergent FDA and EMA quality criteria force developers to prepare region-specific submission packages, stretching regulatory budgets for mid-cap innovators.[2]Source: European Medicines Agency, “Guideline on Quality Requirements for Investigational Advanced Therapy Medicinal Products,” ema.europa.eu Varied potency assays across jurisdictions impair cross-trial comparison and complicate meta-analyses, delaying payer confidence in class efficacy. Industry consortia such as the International Society for Cell & Gene Therapy seek convergence, but philosophical divides over donor-source traceability and viral safety persist. Until harmonization advances, global launches will remain staggered, tempering the revenue ramp of the mesenchymal stem cells market.

High Treatment Cost and Uncertain Reimbursement Landscape

Insurers label many musculoskeletal uses as investigational, limiting coverage to compassionate-use cases and shifting costs to patients. US payers now demand real-world evidence that total knee replacements decline after intra-articular MSC injections before approving broad coverage. European health technology assessment bodies require comparative cost-utility studies against standard care, extending market-access timelines. These reimbursement obstacles restrain volume expansion even as clinical efficacy strengthens, slowing the mesenchymal stem cells market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Mesenchymal Stem Cells Market Segment Analysis

By Products:

Reagents Sustain Manufacturing MomentumKits, media, and reagents commanded 51.23% revenue in 2025, underscoring how consumables dominate day-to-day production budgets across Good Manufacturing Practice suites. This category feeds recurring demand as every cell expansion run requires lineage-specific cytokine blends, serum-free media, and lot-validated reagents. Elevated bioprocess runs triggered by Ryoncil’s launch and expanding clinical pipelines will likely preserve the mesenchymal stem cells market size leadership of reagents.

The cells and cell lines subdivision is projected to climb at a 13.28% CAGR as standardized master banks become critical for multinational submissions and tech-transfer initiatives. CDMOs increasingly bundle cell-bank licensing with analytics, shrinking early-stage development timelines. Service revenues—covering contract manufacturing, assay development, and regulatory consulting—are also gaining share as lean virtual biotechs outsource heavy infrastructure. Collectively, these trends broaden the products stack and inject resilience into the mesenchymal stem cells market.

By Type:

Allogeneic Scale Versus Autologous PersonalizationAllogeneic therapies held 58.66% revenue share in 2025, supported by economies of scale, ease of storage, and single-donor master banks that drive cost efficiency. Centralized manufacturing and stock-on-shelf distribution resonate with hospital logistics teams, reinforcing the mesenchymal stem cells market share for this segment.

Autologous approaches, however, are expanding at 13.31% CAGR because point-of-care bioreactors slash turnaround time and bypass graft-versus-host risk. Same-day harvest reinfusion suits elite sports injuries and personalized orthopaedic cases. While per-patient cost remains higher, hospitals value customized cell phenotype alignment with individual biology, preserving a technology pathway that diversifies the mesenchymal stem cells market.

By Source:

Bone Marrow’s Tradition Meets Adipose ConvenienceBone marrow-derived cells maintained 33.74% share in 2025, reflecting a decades-long safety and efficacy dossier that reassures regulators and clinicians alike. These cells possess well-documented differentiation pathways for skeletal and haematopoietic repair, anchoring their status inside the mesenchymal stem cells market size hierarchy.

Adipose tissue sources are growing fastest at 13.86% CAGR because minimally invasive liposuction yields high cell numbers with superior expansion kinetics. Cord-blood-derived cells deliver elevated proliferation and telomerase activity, while emerging placental and dental pulp lines cater to niche regenerative applications. As sourcing diversifies, supply resilience strengthens across the mesenchymal stem cells market.

By Indication:

Orthopaedic Foundation Expands to Cardiovascular FrontierBone and cartilage repair represented 24.12% of 2025 revenue owing to surgeon familiarity and supportive clinical evidence. Spinal fusion, knee cartilage resurfacing, and non-union fracture repair remain anchor procedures that stabilize commercial forecasts for the mesenchymal stem cells market.

Cardiovascular therapy is slated for a 14.01% CAGR, propelled by early signals of improved left-ventricular ejection fraction in ischemic heart failure cohorts. Parallel momentum in inflammatory bowel disease, liver cirrhosis, and graft-versus-host disease broadens indication spread. Collectively, diversified pipelines reduce dependency on a single therapeutic area and promote balanced revenue stacking across the mesenchymal stem cells market.

By Application:

Disease Modeling Strengthens Research RevenueDisease modeling held 33.85% share in 2025 as pharmaceutical sponsors invested in human-relevant assays to de-risk small-molecule pipelines. The pairing of 3D biomaterial scaffolds with MSCs speeds target validation, cementing application demand within the mesenchymal stem cells market.

Tissue engineering is forecast to climb at 13.79% CAGR as scaffold innovations enhance cell viability and engraftment. Banking services and discovery platforms add ancillary income streams, while toxicology screens augment safety datasets for regulatory filings. Together, these pursuits weave MSCs deeper into translational research cycles, lengthening the value chain of the mesenchymal stem cells market.

Geography Analysis

North America Mesenchymal Stem Cells Market

North America delivered 40.78% revenue in 2025 owing to FDA leadership, deep venture pools, and hospital networks capable of integrating GMP suites. Early reimbursement pilots for graft-versus-host disease procedures encourage hospital uptake, yet orthopaedic coverage remains patchy, capping short-term volume gains. Canada’s public-private partnerships, exemplified by STEMCELL Technologies’ new facility, illustrate policy-led manufacturing clusters that bolster the mesenchymal stem cells market across the continent.

Europe Mesenchymal Stem Cells Market

Europe ranks second by value, supported by the EMA’s Advanced Therapy Medicinal Products pathway and strong academic-industry ties. Germany and the United Kingdom drive trial volumes, while Italy and Spain expand commercial treatment centers. Divergent health-technology-assessment outcomes, however, fragment reimbursement, compelling developers to craft country-specific dossiers, which lengthens uptake timelines in the mesenchymal stem cells market.

APAC Mesenchymal Stem Cells Market

Asia-Pacific is the fastest-growing region at a 14.66% CAGR as China authorizes its first MSC therapy and invests in provincial GMP hubs. Japan leverages the Pharmaceuticals and Medical Devices Act’s conditional approval clause to speed launches, and Australian regulators streamline clinical-trial notification. India and South Korea ramp contract manufacturing, positioning the region as a cost-advantaged production base that reinforces global supply security for the mesenchymal stem cells market. Nevertheless, reimbursement ambiguity and heterogeneous hospital infrastructure remain headwinds to widespread adoption.

Competitive Landscape

The mesenchymal stem cells market is moderately fragmented, yet consolidation is accelerating as pharmaceutical conglomerates acquire specialized cell-therapy units to secure process know-how. Lonza’s 2024 reorganization into Cell & Gene Technologies sharpened focus on modality-specific services and signaled further capacity infusions. Thermo Fisher’s CDMO expansion underscores how diversified suppliers anchor the manufacturing backbone for small biotechs lacking infrastructure.

Process automation, digital twins, and inline analytics now serve as decisive competitive levers. Companies that integrate single-use bioreactors, real-time potency assays, and AI-driven release-testing shorten turnaround and lower cost of goods, differentiating their offerings. Intellectual property around cell sourcing, cryopreservation, and exosome characterization fortifies positioning, with Mesoblast’s broad US and EU patent estate providing defense against generic entrants.

Regional players exploit white-space opportunities by forming consortia with hospital systems and equipment makers to develop localized manufacturing ecosystems. Nikon’s 2025 licensing pact with RoosterBio equips Japanese clients with turnkey MSC production platforms, illustrating partnership-driven market entry strategies that amplify reach without costly acquisitions. This evolving competitive chessboard indicates the mesenchymal stem cells market will reward firms that couple specialized platforms with flexible manufacturing networks.

Mesenchymal Stem Cells Industry Leaders

Cell Applications, Inc

Axol Bioscience Ltd.

STEMCELL Technologies Inc.

Thermo Fisher Scientific Inc.

Cyagen Biosciences Inc.

- *Disclaimer: Major Players sorted in no particular order

Mesenchymal Stem Cells Market Companies Covered in this Report

- Axol Bioscience Ltd

- Cell Applications Inc.

- Cellcolabs Clinical Ltd

- Celprogen Inc.

- Cyagen Biosciences Inc.

- Lonza Group

- Merck

- PromoCell

- ScienCell Research Laboratories Inc.

- Stem Cell Technologies

- Thermo Fisher Scientific

- Mesoblast

- Pluri Inc.

- Athersys

- Cynata Therapeutics

- Orgenesis Inc.

- Stempeutics Research

- BioRestorative Therapies

Recent Industry Developments in Mesenchymal Stem Cells Market

- April 2025: Nikon CeLL innovation and RoosterBio signed a licensing agreement that offers Japanese drug developers an integrated development-to-manufacturing solution for human MSC and extracellular-vesicle therapeutics.

- April 2024: Memel Biotech, a contract development and manufacturing organization based in Lithuania, unveiled a comprehensive, advanced therapy development and manufacturing service at its Klaipeda facility to cater to markets within the European Union (EU). Through this initiative, Memel Biotech seeks to forge partnerships with emerging and established biotech firms aiming to venture into advanced therapy medicinal products (ATMPs). The company's manufacturing capabilities span a diverse range, including mesenchymal stem cells and chimeric antigen receptor T cells.

- February 2024: The University of Liverpool launched a new spin-out company, TrophiCell, that developed an approach to harness the therapeutic potential of adult mesenchymal stem cells (MSCs).

Global Mesenchymal Stem Cells Market Report Scope

As per the scope of the report, mesenchymal stem cells (MSCs) are a type of multipotent stem cell that can differentiate into a variety of cell types, such as cartilage cells (chondrocytes), bone cells (osteoblasts), muscle cells (myocytes), and fat cells (adipocytes).

The mesenchymal stem cells market is segmented into products and services, type, source, indication, application, and geography. The products and services segment is further divided into products and services. The products segment is subdivided into kits, media and reagents, cells and cell lines, and other products. By type, the market is segmented into autologous and allogeneic. The source segment is further divided into adipose tissue, bone marrow, cord blood, fetal liver, and others. The indication segment is further divided into bone and cartilage repair, cardiovascular diseases, inflammatory and immunological diseases, liver diseases, cancer, graft vs host diseases, and others. The application segment is divided into disease modeling, drug development and discovery, stem cell banking, tissue engineering, toxicology studies, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for all the above segments.

Segmentation Overview

| Products | Kits, Media and Reagents |

| Cells and Cell Lines | |

| Other Products | |

| Services |

| Autologous |

| Allogeneic |

| Adipose Tissue |

| Bone Marrow |

| Cord Blood |

| Fetal Liver |

| Others |

| Bone and Cartilage Repair |

| Cardiovascular Disease |

| Inflammatory and Immunological Disease |

| Liver Diseases |

| Cancer |

| Graft-versus-Host Disease |

| Others |

| Disease Modelling |

| Drug Development and Discovery |

| Stem Cell Banking |

| Tissue Engineering |

| Toxicology Studies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products & Services | Products | Kits, Media and Reagents |

| Cells and Cell Lines | ||

| Other Products | ||

| Services | ||

| By Type | Autologous | |

| Allogeneic | ||

| By Source | Adipose Tissue | |

| Bone Marrow | ||

| Cord Blood | ||

| Fetal Liver | ||

| Others | ||

| By Indication | Bone and Cartilage Repair | |

| Cardiovascular Disease | ||

| Inflammatory and Immunological Disease | ||

| Liver Diseases | ||

| Cancer | ||

| Graft-versus-Host Disease | ||

| Others | ||

| By Application | Disease Modelling | |

| Drug Development and Discovery | ||

| Stem Cell Banking | ||

| Tissue Engineering | ||

| Toxicology Studies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 valuation of the mesenchymal stem cells market?

The mesenchymal stem cells market size is valued at USD 5.14 billion in 2026.

How fast will the market grow through 2031?

The market is projected to expand at a 12.05% CAGR, reaching USD 9.08 billion by 2031.

Which region grows fastest over the forecast period?

Asia-Pacific records the highest 14.66% CAGR due to supportive regulation and manufacturing investments.

What segment holds the largest revenue share in 2025?

Kits, media, and reagents lead with 51.23% of revenue thanks to recurring consumable demand.

Why are allogeneic therapies dominant?

Allogeneic products offer scalable master cell banks, streamlined logistics, and cost advantages, holding 58.66% of 2025 revenue.

What major regulatory milestone impacted the market in 2024?

The FDA approved Ryoncil, the first allogeneic MSC therapy, establishing a regulatory precedent for future products.

Page last updated on: