Acute Myeloid Leukemia Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

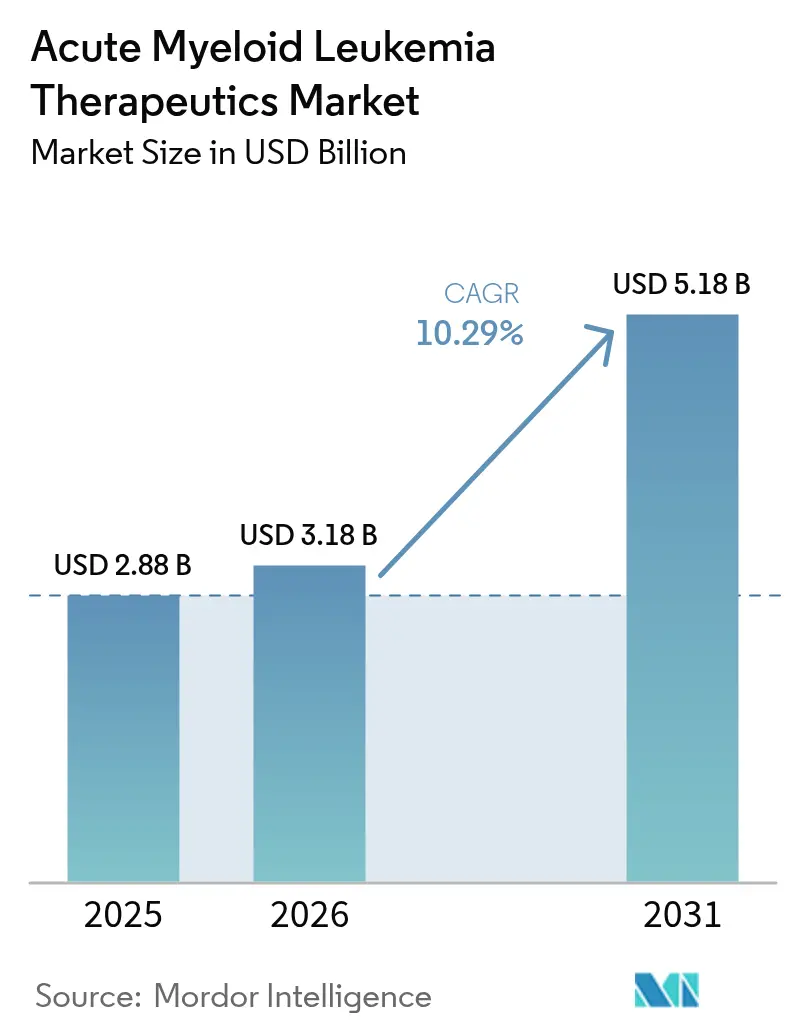

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 5.18 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

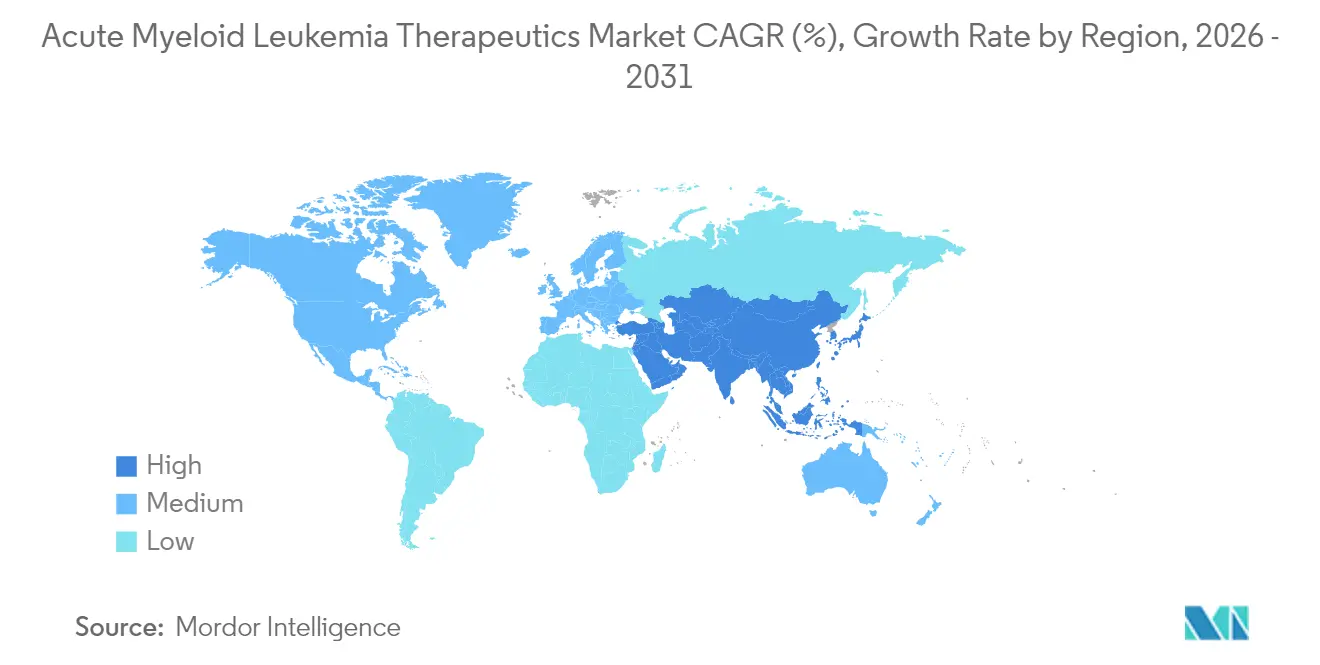

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Myeloid Leukemia Therapeutics Market Analysis by Mordor Intelligence

The acute myeloid leukemia therapeutics market size was valued at USD 2.88 billion in 2025 and estimated to grow from USD 3.18 billion in 2026 to reach USD 5.18 billion by 2031, at a CAGR of 10.29% during the forecast period (2026-2031). Therapeutic innovation is shifting clinical practice away from broad-spectrum chemotherapy toward targeted therapies that exploit precise molecular weaknesses, such as FLT3, IDH1/2, BCL-2, and menin. Regulatory agencies have quickened review timelines, resulting in several first-in-class approvals that immediately translated into commercial uptake. Venture investment and large-cap licensing deals channel fresh capital into discovery programs, while next-generation sequencing (NGS) diagnostics expand the treatable population by identifying actionable mutations. Although chemotherapy still dominates treatment volume, the commercial spotlight now falls on oral targeted combinations that lower hospitalization needs, increase adherence, and improve survival, especially among frail seniors. Supply-chain vulnerabilities and rising genetic-testing costs temper the outlook but do not derail the long-term growth trajectory.

Key Report Takeaways

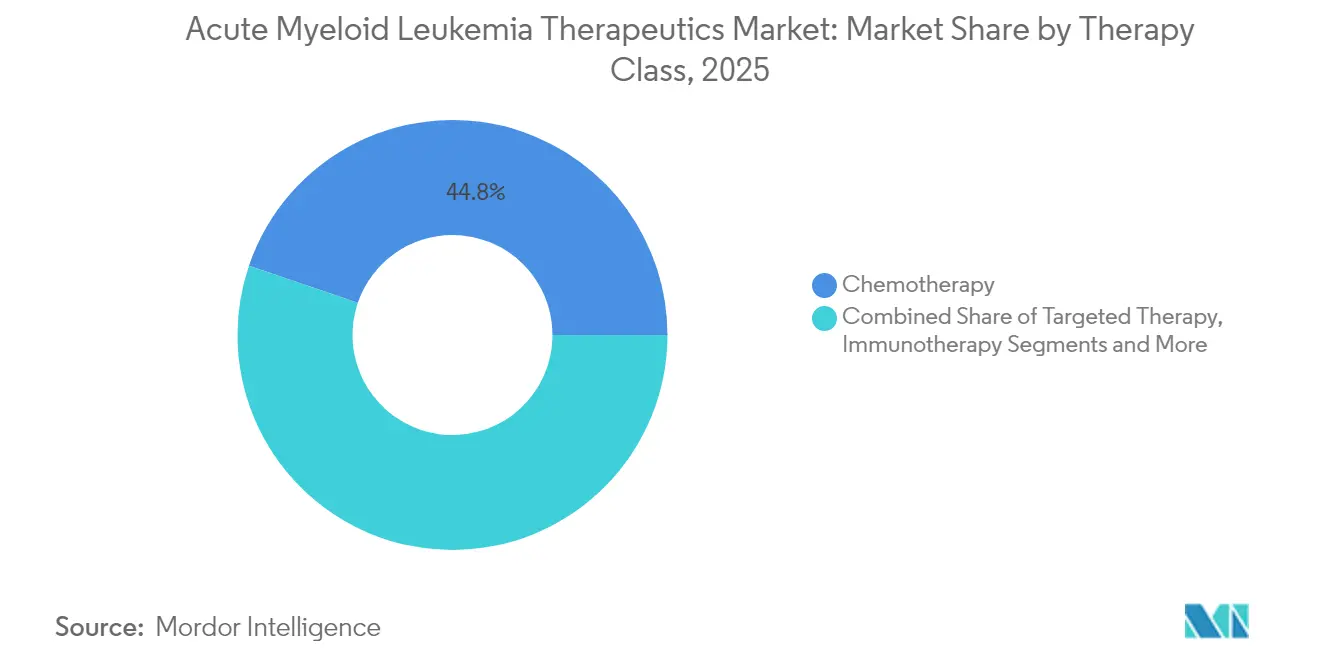

- By therapy class – Chemotherapy retained 44.78% of the acute myeloid leukemia therapeutics market share in 2025, whereas immunotherapy is projected to log the fastest 12.14% CAGR through 2031.

- By mechanism/molecular target, FLT3 inhibitors led with a 23.21% revenue share in 2025; BCL-2 inhibitors are expected to expand at a 13.22% CAGR, the highest among all molecular targets.

- By patient age group, adults aged 18-64 years accounted for a 50.86% share in 2025, while the ≥65-year cohort is set to grow at a 12.06% CAGR, driven by better-tolerated oral regimens.

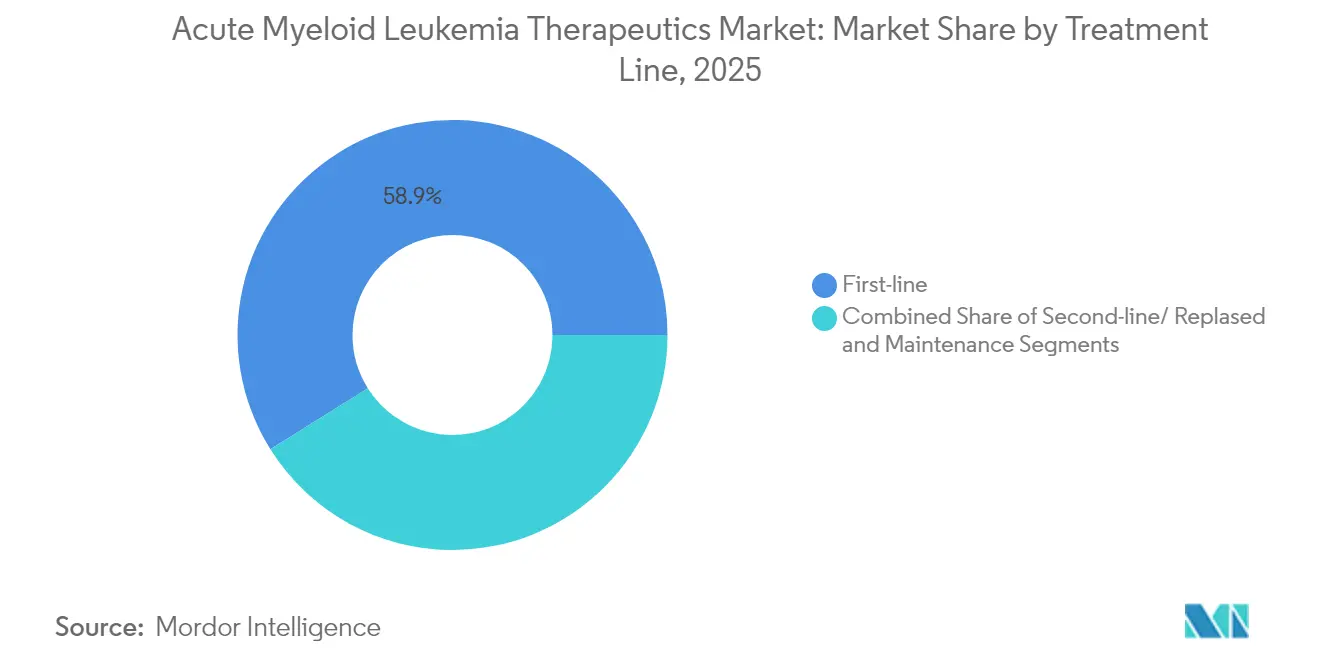

- By treatment line, First-line therapies commanded a 58.92% share in 2025; however, second-line / relapsed treatments are forecast to rise at a 13.07% CAGR, as survival improvements enable multiple lines of care.

- By end user, hospitals captured a 58.12% share in 2025; home and outpatient settings represent the fastest-growing channel, with a 13.34% CAGR, supported by reimbursement for at-home infusions.

- By geography, North America led with a 43.12% market share in 2025, while the Asia-Pacific region is expected to advance at a 11.95% CAGR, the steepest regional growth rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acute Myeloid Leukemia Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of AML among ageing populations | +1.8% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| Precision-medicine approvals for FLT3/IDH/BCL-2 inhibitors | +2.3% | North America & EU; spreading to APAC | Medium term (2-4 years) |

| Escalating global R&D investments & venture financing | +1.2% | US & EU innovation hubs | Medium term (2-4 years) |

| Expedited FDA/EMA pathways & orphan-drug incentives | +1.5% | North America & EU | Short term (≤ 2 years) |

| Outpatient venetoclax-based regimens expanding treatable pool | +1.9% | Global; high impact in LMICs | Short term (≤ 2 years) |

| Wider adoption of NGS companion diagnostics in emerging markets | +1.1% | Core APAC; spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of AML Among Ageing Populations

Global life expectancy gains widen the pool of patients over 65 years who are most susceptible to AML. The incidence in this cohort accelerates demand for gentler yet potent regimens, a niche currently filled by venetoclax-based oral combinations that report an overall response rate of 73% in real-world frail cohorts.[1]Priyanka Chauhan, “Venetoclax and hypomethylating agent based outpatient AML induction,” journals.lww.com Outpatient-enabled dosing reduces hospital burden and widens geographic reach, driving a 12.42% CAGR among geriatric patients. National screening policies that encourage baseline bloodwork in seniors further enlarge the diagnosed population.

Precision-Medicine Approvals For FLT3/IDH/BCL-2 Inhibitors

Mutation-specific drugs are rewriting first-line standards. Revumenib became the first menin inhibitor approved for KMT2A-rearranged leukemia, while quizartinib nearly doubled median overall survival in FLT3-ITD-positive disease when paired with backbone chemotherapy. Regulatory confidence in these data spurs companies to broaden label indications and bundle companion diagnostics, resulting in a multiplier effect across therapeutic and testing revenues.

Escalating Global R&D Investments & Venture Financing

Large-cap firms are pouring capital into differentiated modalities. Gilead earmarked USD 1.5 billion for trispecific T-cell engagers, underscoring its confidence in next-generation immunotherapies. Grant support, such as NIH-backed protein therapeutics, extends the innovative runway for smaller biotechs. Deepening pipelines shortens cycle times between discovery and first-in-human studies, sustaining the growth engine of the acute myeloid leukemia therapeutics market.

Expedited FDA/EMA Pathways & Orphan-Drug Incentives

Breakthrough, fast-track, and orphan designations truncate review cycles and add exclusivity benefits. Ziftomenib secured breakthrough status for NPM1-mutant AML, granting rolling submissions and frequent FDA guidance. Comparable EMA mechanisms ensure synchronized European launches, reinforcing global revenue prospects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-phase clinical-trial attrition | -1.4% | Global; highest where trial infrastructure is weak | Long term (≥ 4 years) |

| Severe chemo-toxicity & treatment-related mortality | -1.1% | Global; acute among elderly | Medium term (2-4 years) |

| Cold-chain/IP barriers limiting novel-drug access in LMICs | -0.9% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Rising cost burden of genomics-driven care | -1.2% | Varies with reimbursement stringency | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Phase Clinical-Trial Attrition

AML’s biological diversity demands large, stratified trials that encounter enrollment bottlenecks and soaring costs. Moleculin’s MIRACLE study highlights the challenge of recruiting mutation-matched subjects across multiple continents, a hurdle that prolongs timelines and increases costs. Investors price this risk into financing terms, potentially slowing pipeline expansion.

Severe Chemo-Toxicity & Treatment-Related Mortality

Legacy induction regimens still carry high mortality, especially in patients over 70 years, prompting clinicians to favor lower-intensity options or hospice care. Although targeted drugs mitigate toxicity, they often serve as add-ons rather than substitutes, leaving cumulative side effects unresolved and curbing overall adoption.[2]Hagop M. Kantarjian, “Acute Myeloid Leukemia Management and Research in 2025,” PubMed, pubmed.ncbi.nlm.nih.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Class: Immunotherapy Drives Innovation Wave

Chemotherapy controlled 44.78% of the acute myeloid leukemia therapeutics market in 2025, yet immunotherapy’s 12.14% CAGR defines the future revenue slope. Early clinical data on CD371-directed CAR-T cells and CD33-GSPT1 antibody-drug conjugates demonstrate durable remissions in relapsed populations where cytotoxic therapies fail. Stem-cell transplant conditioning also entered the precision era with FDA approval of treosulfan plus fludarabine, a regimen that produces superior long-term survival compared with older busulfan protocols.

Investment inflows sustain this momentum. Bristol Myers Squibb aligns its cell-therapy franchise with antibody conjugates to capture multiple immune pathways, and academic consortia explore dual-antigen CAR designs to bypass antigen-loss relapse. Supportive-care innovations now focus on mitigating cytokine release, thereby broadening eligibility for outpatient administration. The therapy-class mix will therefore shift steadily toward immune-modulating agents that integrate seamlessly with targeted small molecules, expanding the acute myeloid leukemia therapeutics market.

By Mechanism/Molecular Target: BCL-2 Inhibitors Lead Growth

FLT3 inhibitors held 23.21% mechanism-level share in 2025, yet the BCL-2 subclass posts the sharpest 13.22% CAGR, propelled by venetoclax’s robust complete-remission depth when combined with hypomethylating agents. Menin inhibition inaugurates a new mechanistic era after revumenib’s approval, broadening therapeutic geometry beyond kinase or epigenetic targets.

Pipeline synergies multiply as developers pair BCL-2 blockade with FLT3 or IDH inhibition to forestall clonal escape. Hedgehog and CD33 pathways retain strategic relevance in combination cocktails aimed at minimal residual disease. Consequently, sponsors with diversified target portfolios, rather than single-asset bets, are positioned to capitalize on the projected gains in the acute myeloid leukemia therapeutics market size for the period.

By Patient Age Group: Geriatric Segment Transforms Treatment

The ≥65-year cohort drives a 12.06% CAGR even though adults aged 18-64 years still generate the largest revenue slice. Venetoclax-based low-intensity regimens achieve a 73% composite remission rate in octo- and nonagenarians, shifting therapeutic decision-making from palliation to disease eradication in seniors. Reduced transfusion and hospitalization requirements enable decentralized care, improving quality of life.

Pediatric incidence remains low, but benefits from dedicated centers that employ genomic-guided risk stratification and early transplant referral. Intravenous delivery innovations, including smaller-volume CAR-T products, may eventually bridge the age divide. Overall, a fine-grained, age-aware model replaces the historical one-size-fits-all paradigm, expanding the acute myeloid leukemia therapeutics market.

By Treatment Line: Second-Line Therapies Gain Momentum

First-line settings capture 58.92% of revenue, but second-line and relapsed therapy areas accelerate at a 13.07% CAGR, as survival gains allow for multiple treatment sequences. Venetoclax, combined with cytidine analogs, dominates salvage regimens, while emergent cell therapies anchor bridge-to-transplant strategies. Maintenance therapy gains commercial focus, utilizing low-dose targeted agents to sustain remission and generate annuity-like revenue streams, thereby increasing the size of the acute myeloid leukemia therapeutics market.

Sequential therapy design now guides clinical-trial architecture, with sponsors developing drug portfolios explicitly staged for first, second, and maintenance lines to maximize lifetime value per patient. The trend reinforces the demand for molecular monitoring tools that detect early relapse, thereby connecting diagnostic and therapeutic revenue streams.

By End User: Home Care Revolution Accelerates

Hospitals represented 58.12% of the acute myeloid leukemia therapeutics market in 2025, whereas home/outpatient venues are projected to set the fastest 13.34% CAGR through 2031. Medicare’s 2025 reimbursement update authorizes higher payment for home infusions, removing a key financial barrier. Portable infusion pumps and digital adherence tools make daily oral care feasible outside inpatient wards, further decentralizing care.

Academic centers remain indispensable for complex cellular therapies; however, they are increasingly partnering with community clinics for post-infusion follow-up. Ambulatory centers navigate the intricacies of coverage but benefit from patients' preference for shorter stays. Taken together, shifting care delivery patterns expand the acute myeloid leukemia therapeutics market while easing capacity constraints at tertiary hospitals.

Geography Analysis

North America captured 43.12% of the acute myeloid leukemia therapeutics market in 2025. The United States drives this dominance through robust private and public reimbursement, widespread mandatory testing, and rapid FDA pathways that reduce the time from submission to bedside. Academic networks such as the Alliance for Clinical Trials link smaller hospitals into nationwide studies, accelerating trial recruitment and broadening early access. Cellular-therapy centers of excellence anchor a thriving referral ecosystem, ensuring continued uptake of high-value interventions. Canada mirrors practice patterns but faces occasional formulary lags. At the same time, Mexico improves access through participation in cross-border clinical trials. Collectively, the region is expected to maintain momentum through 2030, as payer policies increasingly endorse precision approaches that demonstrate superior value.

Europe ranks second by revenue, leveraging centralized EMA approvals to harmonize drug availability. Markets such as Germany and the United Kingdom rapidly integrate newly authorized therapies after rigorous health technology appraisals validate their cost-effectiveness. Recent EMA endorsements of Rytelo and the CRISPR-derived Casgevy illustrate a willingness to back transformative modalities. National genomic strategies fund NGS panels, ensuring that mutation-matched therapies reach eligible patients. Southern European countries adopt at a measured pace due to budget constraints, yet benefit from EU joint procurement initiatives that negotiate volume-based discounts. Overall, Europe’s evidence-driven environment sustains stable growth and drives clinical trial diversity, which is essential for mechanistic validation.

Asia-Pacific logs the highest 11.95% CAGR as healthcare infrastructure modernizes and diagnostic capacity expands. Japan’s universal coverage rapidly reimburses approved agents, while local studies adapt global regimens to Asian metabolic profiles. China’s domestic innovators are leveraging government funding to enter Phase 3 international trials, aiming to match or exceed Western benchmarks in survival rates. India proves the cost-effectiveness of outpatient venetoclax protocols, making precision care viable even in lower-resource settings. Australia and South Korea serve as gateways for clinical trials for multinationals targeting regional approval. The Middle East and Africa remain nascent but show incremental progress through public–private partnerships that build diagnostic labs and negotiate tiered pricing. Together, these trends propel theacute myeloid leukemia therapeutics market into new high-growth territories.

Competitive Landscape

The acute myeloid leukemia therapeutics market remains moderately fragmented. AbbVie and Genentech's venetoclax franchise generates blockbuster revenue, driven by a compelling survival benefit and flexible oral dosing. Bristol Myers Squibb expands its hematology footprint through CAR-T platforms and a CD33-GSPT1 conjugate that seeks to outrun antigen escape. Gilead's USD 1.5 billion collaboration with Merus underscores the industry's appetite for multispecific T-cell engagers that promise off-the-shelf convenience and deep remissions. Pfizer strengthens its position via quizartinib, creating a dual-FLT3 offering alongside gilteritinib, while Astellas co-develops maintenance regimens to extend the patient journey and lifetime value.

Emerging players carve niches with differentiated science. Actinium Pharmaceuticals' Actimab-A couples alpha particle payloads to a CD33 antibody, showing activity across mutational backgrounds and synergy with FLT3 and menin inhibitors. Academic spin-outs are piloting protein-degradation technologies aimed at transcription factors that have been historically deemed undruggable. Venture-backed startups target epitranscriptomic pathways, aiming to leapfrog crowded kinase spaces. Partnership models prevail, pairing biotech creativity with big-pharma capital and commercialization muscle. Competitive intensity will therefore continue to rise, with combination-ready portfolios emerging as the winning formula in the acute myeloid leukemia therapeutics market.

Acute Myeloid Leukemia Therapeutics Industry Leaders

Pfizer Inc.

Novartis AG

Bristol Myers Squibb

Astellas Pharma

AbbVie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Actinium Pharmaceuticals and Memorial Sloan Kettering Cancer Center expanded a collaboration on Actimab-A combinations with FLT3 and menin inhibitors to address a multi-billion-dollar opportunity.

- March 2025: Johnson & Johnson launched the Camelot-2 phase 3 trial of bleximenib plus venetoclax and azacitidine in frontline AML patients ineligible for intensive chemotherapy, positioning against Syndax’s revumenib program.

- January 2025: FDA approved treosulfan with fludarabine as a preparative regimen for allogeneic stem-cell transplant in AML or MDS, reporting superior overall survival versus busulfan-based conditioning.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the acute myeloid leukemia (AML) therapeutics market as all branded, generic, and pipeline drugs, including chemotherapies, FLT3/IDH/BCL-2/menin inhibitors, antibody-drug conjugates, immunotherapies, and stem-cell-conditioning regimens, used to treat de novo or secondary AML in inpatient or outpatient care.

Scope exclusion: supportive medicines such as anti-emetics, hematopoietic growth factors, and antibiotic prophylaxis are outside this valuation.

Segmentation Overview

- By Therapy Class

- Chemotherapy

- Targeted Therapy

- Immunotherapy (incl. CAR-T, bispecifics)

- Stem-cell Transplant

- Supportive / Others

- By Mechanism / Molecular Target

- FLT3 Inhibitors

- IDH1/2 Inhibitors

- BCL-2 Inhibitors

- Hedgehog Pathway Inhibitors

- CD33-Directed Antibody–Drug Conjugates

- By Patient Age Group

- Paediatric (<18 yrs)

- Adults (18-64 yrs)

- Geriatric (≥65 yrs)

- By Treatment Line

- First-line

- Second-line/Relapsed

- Maintenance

- By End User

- Hospitals

- Specialty Oncology Centres

- Academic & Research Institutes

- Home/Out-patient Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hematologists, transplant coordinators, and reimbursement specialists across North America, Europe, and Asia Pacific to validate dosing shifts, inpatient-outpatient split, and price erosion paths. We also ran concise online surveys with AML survivors that clarified adherence and refill behavior.

Desk Research

We began with trusted public datasets like SEER, GLOBOCAN, the American Cancer Society, EMA and FDA drug approval logs, and WHO ATC/DDD files. Company 10-Ks, investor decks, and hospital procurement portals established launch timing, average selling prices, and uptake speed.

Real-world utilization curves were further refined through shipment records in Volza, adverse event signals captured via Dow Jones Factiva, and revenue splits verified in D&B Hoovers. These layers let us align incidence, line of therapy mix, and course length. The sources cited here are illustrative; many additional publications informed data checks and clarifications.

Market-Sizing & Forecasting

A top-down epidemiology to treatment model converts incident and prevalent patient pools into demand by applying diagnosis rates, therapy penetration, average cycles, and dosage. Sampled supplier roll ups and channel checks provide a bottom-up reasonableness test. Key variables include mutation testing uptake, first-line venetoclax penetration, transplant eligibility share, wholesale acquisition cost drift, and survival linked treatment duration. Multivariate regression on these drivers produces the baseline and a total for the forecast period, with scenario analysis for pivotal trial readouts.

Data Validation & Update Cycle

Outputs pass variance checks against national drug sales monitors and hospital charge data before senior review. We refresh the model each year and release interim updates after major approvals, withdrawals, or reimbursement shifts.

Why Our Acute Myeloid Leukemia Baseline Commands Reliability

Published estimates often diverge because studies select different drug baskets, patient cohorts, and refresh cadences. According to Mordor Intelligence, disciplined scope alignment and annually recalibrated drivers narrow those gaps.

Key gap drivers include the merging of AML revenue with broader leukemia spend, omission of new immunotherapies, and spot rate currency conversions that distort totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.88 B (2025) | Mordor Intelligence | - |

| USD 3.47 B (2024) | Global Consultancy A | Includes supportive care drugs and mixed ALL/AML pools |

| USD 1.74 B (2025) | Regional Consultancy B | Excludes novel immunotherapies and outpatient spend |

The comparison shows that our balanced, transparent baseline, grounded in epidemiology and verified spend, gives decision makers a dependable starting point.

Key Questions Answered in the Report

What is the current size of the acute myeloid leukemia therapeutics market?

The acute myeloid leukemia therapeutics market stands at USD 3.18 billion in 2026 and is projected to reach USD 5.18 billion by 2031 at a 10.29% CAGR.

Which therapy class is growing fastest in acute myeloid leukemia treatment?

Immunotherapy, including CAR-T cells and antibody-drug conjugates, is expanding at a 12.14% CAGR, outpacing other classes.

Why is Asia-Pacific considered the high-growth region for AML drugs?

Improved healthcare infrastructure, broader NGS access, and rising investment propel a 11.95% CAGR in Asia-Pacific.

How are outpatient regimens shaping AML care?

Oral venetoclax-based combinations enable home administration, cut hospital costs, and expand the treatable patient pool, especially among seniors.

What recent FDA approval significantly impacts transplant conditioning?

In January 2025, the FDA cleared treosulfan with fludarabine, offering better survival than busulfan-based regimens for allogeneic transplant candidates.

How concentrated is the AML treatment market?

A market concentration score of 5 signals moderate competition, with the top five firms controlling about half of total revenue.

Page last updated on: