Shock Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

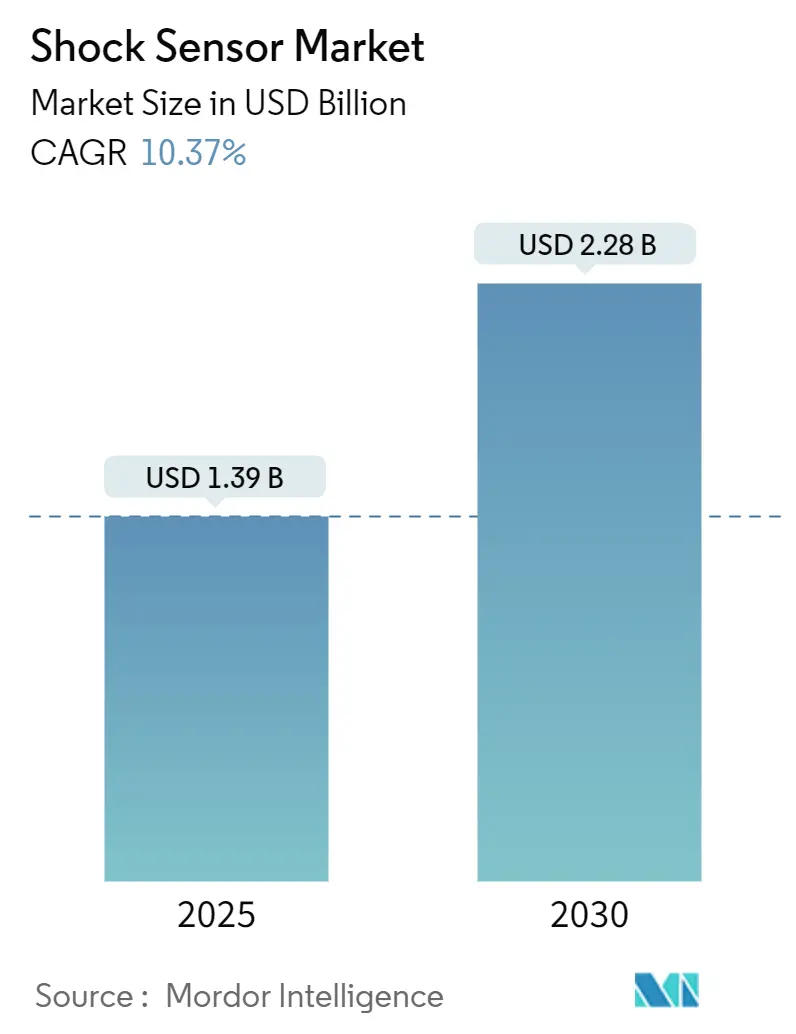

| Market Size (2025) | USD 1.39 Billion |

| Market Size (2030) | USD 2.28 Billion |

| Growth Rate (2025 - 2030) | 10.37% CAGR |

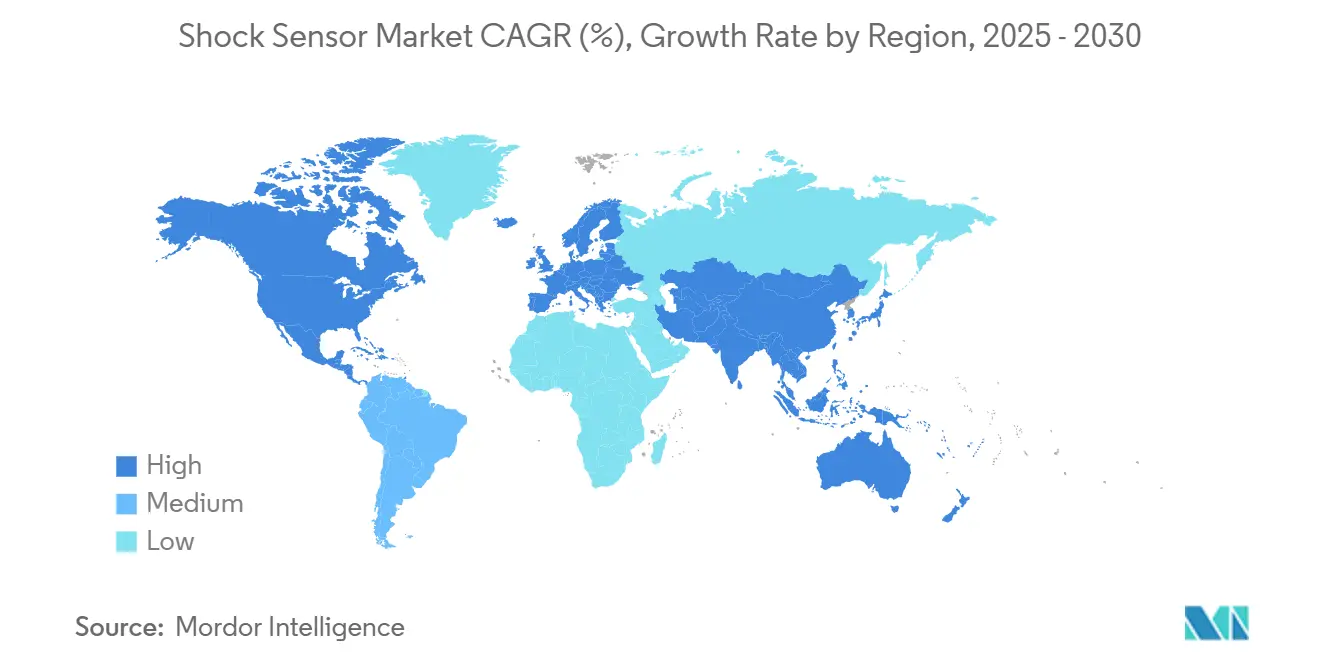

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shock Sensor Market Analysis by Mordor Intelligence

The shock sensor market size is estimated at USD 1.39 billion in 2025, and is expected to reach USD 2.28 billion by 2030, at a CAGR of 10.37% during the forcast period (2025-2030). Rapid adoption of predictive maintenance, tighter automotive safety mandates, and miniaturization of consumer electronics collectively widen the addressable base for precision impact-monitoring devices. Piezoelectric designs dominate value creation because they convert mechanical stress to electrical charge without external power, enabling long-life deployment in remote settings. Parallel material science progress improves sensitivity, while edge AI allows sensors to diagnose anomalies locally, trimming cloud latency and bandwidth costs. Industries that once reacted to machinery failures now design maintenance programs on real-time vibration data, shrinking unplanned downtime and extending asset life. Heightened focus on cybersecurity, however, reshapes procurement specifications, pushing vendors to embed encryption and intrusion-detection functions at the sensor level.

Key Report Takeaways

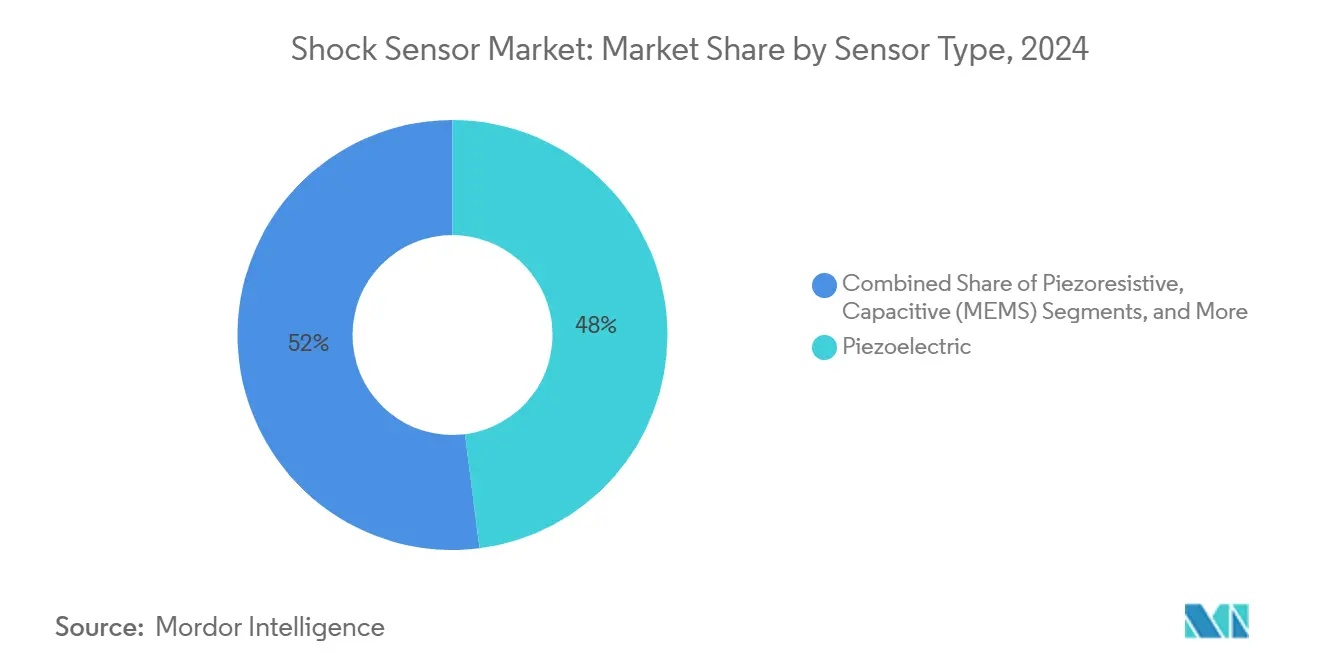

- By sensor type, piezoelectric devices held 48% of the shock sensor market share in 2024; capacitive MEMS posted the highest growth at a 10.7% CAGR to 2030.

- By material, lead zirconate titanate commanded 57% of the shock sensor market size in 2024, while PVDF is projected to grow at a 10.9% CAGR through 2030.

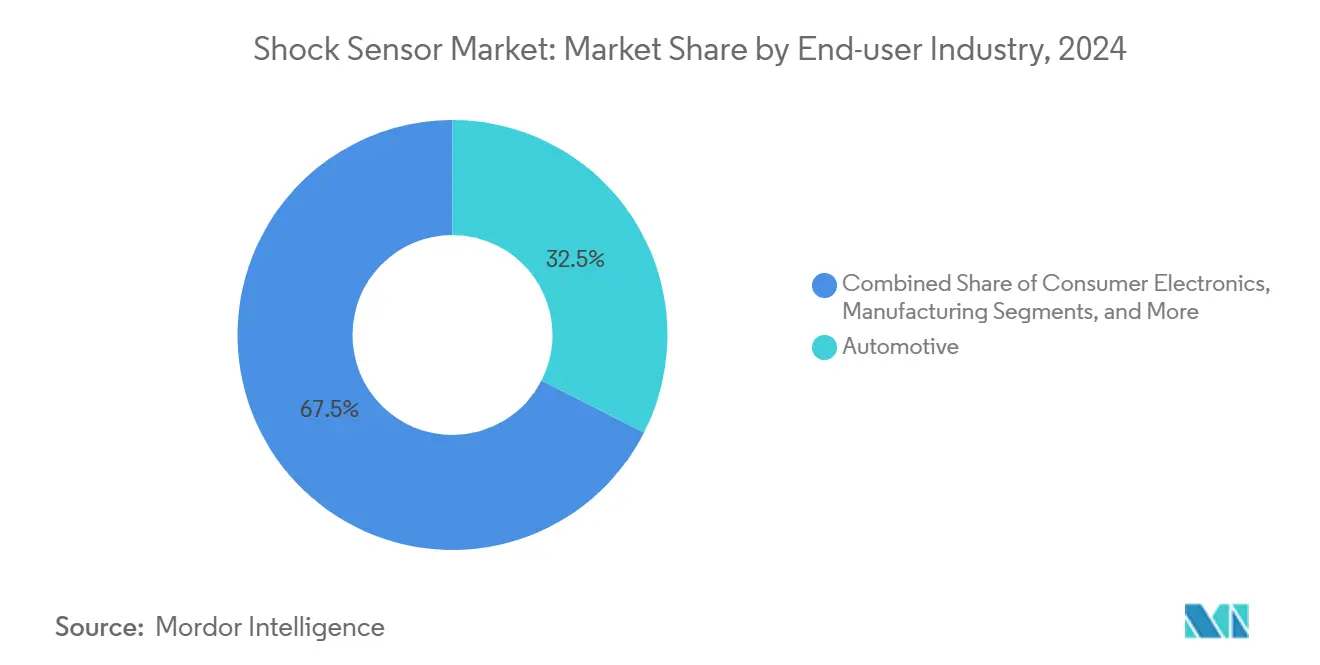

- By end-user industry, automotive applications accounted for 32.5% of 2024 revenue; consumer electronics is forecast to rise at an 11.5% CAGR between 2025-2030.

- By geography, Asia-Pacific captured 44% of 2024 revenue and Africa is set to expand at an 11% CAGR from 2025 onward.

Global Shock Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated SME automation demand | +2.1% | Global with APAC focus | Medium term (2-4 years) |

| Cost and footprint advantage of compact PLCs | +1.8% | North America and EU | Short term (≤2 years) |

| Convergence of PLC with IIoT and edge analytics | +2.3% | Global; early in Germany, Japan, South Korea | Long term (≥4 years) |

| Transition toward open, software-defined control | +1.6% | North America and EU; gradual APAC | Long term (≥4 years) |

| Explosion-proof micro PLC upgrades in hazardous plants | +1.4% | Oil and gas hubs worldwide | Medium term (2-4 years) |

| Mobile-robot OEM shift to battery-optimized nano PLCs | +1.5% | APAC manufacturing, NA logistics | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerated SME Automation Demand

Small and medium manufacturers now equip assets with low-cost wireless vibration nodes, opening a USD 250 billion sensor opportunity where shock detection claims roughly 15%. [1]Corporate Communications, “2024 Universal Registration Document,” Schneider Electric, 2025, se.com Edge analytics let factory managers spot imbalance events early, delivering documented 55% drops in expected failures and 40% longer machine life, as shown by Regal Rexnord deployments. [2]Staff Writer, “Regal Rexnord Unveils Next Generation of Perceptiv Intelligent Solutions,” Regal Rexnord, 2025, regalrexnord.com Wireless form factors bypass cabling expenses, broadening coverage across distributed plants. ISO 10816-3 vibration thresholds reinforce compliance needs, turning predictive maintenance from a discretionary upgrade into a line-item budget priority. As cloud fees fall, subscription-based dashboards further reduce entry barriers for SMEs.

Cost and Footprint Advantage of Compact PLCs

MEMS miniaturization trims sensor footprint by 60% versus legacy piezoelectric units while boosting high-frequency response. [3]Research Group, “Development of Leadless SiC Pressure Sensors,” Nature Microsystems & Nanoengineering, 2025, nature.com Leadless packages withstand harsh chemicals and vibration, cutting installation labor and ensuring stable output even under elevated temperatures. Integrating multiple sensing modalities in one die halves bill-of-materials cost, which widens adoption in price-sensitive applications. WirelessHART or similar protocols deliver interoperability, streamlining commissioning and ongoing upgrades without specialized gateways. Lower power draw means field-replaceable batteries last multi-year cycles, lowering total cost of ownership.

Convergence of PLC with IIoT and Edge Analytics

Low-power microcontrollers now host anomaly-detection models that previously demanded cloud GPUs, shrinking latency and preserving bandwidth. TinyML lets high-resolution time-series data remain on-device, mitigating cybersecurity exposure because raw data never exits the local network. Qualcomm’s collaboration with Honeywell illustrates these hybrid architectures that pair cellular or Wi-Fi backhaul with stacked inference engines, extending battery life and reducing server calls. [4]Editors, “Qualcomm and Honeywell Partner on AI-Powered Energy Solutions,” StockTitan, 2024, stocktitan.com Combined accelerometer, gyroscope, and temperature arrays feed fused algorithms, creating self-calibrating nodes that learn baseline patterns over time. Vendors differentiate on on-chip DSP libraries, enabling domain-specific models through over-the-air updates.

Transition Toward Open, Software-Defined Control

Containerized runtimes decouple application code from hardware, so shock sensor firmware gains new functions via remote refresh rather than physical swap-outs. Open APIs curb vendor lock-in, letting operators mix best-of-breed analytics with preferred dashboards. Firmware-level encryption and signed updates satisfy regulators that demand traceable change records in safety-critical lines. Multi-tenant management portals orchestrate hundreds of distributed nodes while preserving real-time edge decisions; this architecture lengthens product lifecycles and cuts capex associated with hardware refreshes.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity vulnerabilities | -1.8% | Global critical infrastructure | Short term (≤2 years) |

| Functional limits vs. mid-range PLCs | -1.2% | North America and EU automation | Medium term (2-4 years) |

| Substitution by SBCs and industrial MCUs | -1.4% | APAC manufacturing | Long term (≥4 years) |

| Semiconductor-grade component shortages | -2.1% | Global supply chain; acute automotive | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity Vulnerabilities

Wireless nodes introduce fresh attack surfaces that adversaries can weaponize to manipulate safety thresholds in real-time. Successful exploits could spoof vibration signatures, prompting false shutdowns or masking genuine hazards, undermining operator trust and slowing procurement cycles. Legacy control systems lack layered authentication, so retrofits demand parallel investment in secure gateways and encrypted firmware. Evolving standards, including IEC 62443, impose compliance costs and allocate budget away from sensor rollout.

Semiconductor-Grade Component Shortages

MEMS shock sensor production hinges on analog amplifiers and high-precision ADCs that share fabs with EV powertrains and infotainment chipsets. Vehicle electrification spikes demand and lengthens lead times beyond 40 weeks for some SKUs. Geopolitical risk concentrates advanced packaging in a handful of Asian hubs, so localized surges strain capacity. Cost overhangs cascade through bill-of-materials, prompting end users to defer upgrades or pick less-granular monitoring solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Piezoelectric Dominance Drives Innovation

In 2024, piezoelectric devices held 48% of revenue, setting the benchmark for sensitivity across broad frequency bands. Capacitive MEMS designs, while younger, advance at a 10.7% CAGR as smartphone makers prize integration with existing silicon processes. The shock sensor market size for piezoelectric solutions is projected to widen steadily through 2030, aided by energy-harvesting capability that minimizes external power wiring. Piezoresistive silicon-carbide variants remain the go-to choice for engines operating near 600 °C, particularly within aerospace turbines where redundancy and long service intervals matter. Emerging magnetoelectric composites in the “Others” category multiply voltage output by two orders of magnitude, holding promise for next-level sensitivity in defense and medical imaging.

Advanced fabrication, such as synchronized floating-potential HiPIMS, yields uniform thin films on insulating substrates, which unlocks integration of piezo layers directly atop ASICs. These gains point toward single-package vibration nodes that blend detection, amplification, digitization, and edge processing. Vendors who secure IP around cross-domain integration will likely capture premium margins even as unit prices trend lower.

By Material: PZT Ceramics Lead While PVDF Polymers Accelerate

Lead zirconate titanate sustained 57% share in 2024, favored for high piezo coefficients and temperature resilience. Yet PVDF rises fastest at a 10.9% CAGR, driven by wearables that need light, flexible substrates. The shock sensor market share for PVDF-based devices is expected to widen appreciably in remote health-monitoring patches. Hybrid composites marry ceramic filler with polymer matrices, aiming to blend stiffness-driven sensitivity with bendable form factors. Research on lead-free bismuth-based alternatives responds to global RoHS directives, positioning compliant suppliers for early-mover advantage.

Continuous casting lines and roll-to-roll processing reduce PVDF sheet costs, lowering barriers for consumer device makers. Meanwhile, gallium orthophosphate targets the ultra-high-temperature niche, retaining piezoelectric properties well past 900 °C, crucial for deep-well drilling and re-entry vehicles.

By End-User Industry: Automotive Leadership Meets Consumer Electronics Growth

Automotive plants absorbed 32.5% of 2024 shipments as ADAS mandates escalated. EU General Safety Regulation II now obliges event data recorders that rely on millisecond-grade impact detection. Battery electric vehicles add further sensors to watch thermal runaway. Consumer electronics, with an 11.5% CAGR, widens the revenue pool through drop-detection routines that safeguard displays and internal storage. The shock sensor market size for handheld devices is projected to expand sharply as foldable phones and AR headsets demand rapid inertial feedback.

Aerospace retains steady volume because airlines field roughly 100 structural-health nodes per jet, each validating airframe integrity every flight cycle. Manufacturing industries quantify ROI easily: wireless vibration suites cut unplanned stoppages by more than half, freeing labor and spare-parts budgets to fund digital expansion. Healthcare wearables, still nascent, illustrate upside: piezo-based fall-detection patches trigger alerts within 30 ms, crucial for geriatric care.

Geography Analysis

Asia-Pacific captured 44% of 2024 value, benefiting from dense electronics supply chains, automotive final assembly capacity, and state support for Industry 4.0 upgrades. China anchors both demand and supply, while Japan contributes materials innovation and South Korea scales wafer-level MEMS processes. India’s production-linked incentive schemes lure new fabs and spur local sensor sourcing.

North America relies on aerospace, defense, and oil-field services for steady sensor offtake. FAA programs encourage fleetwide deployment of structural-health kits, and both U.S. and Canadian miners retrofit heavy machinery to monitor haul-truck frame fatigue. Venture capital favors edge-AI startups, catalyzing regional growth in analytical firmware.

Europe combines regulatory pull and engineering talent. The EU safety law effective July 2024 cements shock sensors inside brake-assist modules and black-box recorders, ensuring baseline volume for Tier-1 suppliers. Germany’s machine-tool builders adopt smart maintenance to protect export competitiveness. Nordic wind operators apply extreme-weather-proof nodes to turbine blades, curbing ice-induced vibration.

Africa, while starting from a small base, posts an 11% CAGR thanks to mining expansion across Zambia, South Africa, and Ghana. Localized energy projects and port modernizations require ruggedized monitoring, inviting partnerships between global OEMs and regional integrators.

Competitive Landscape

The field remains moderately fragmented. TE Connectivity, Murata, and Honeywell leverage vertically integrated ceramics, ASICs, and packaging to deliver broad catalogs across automotive, industrial, and aerospace channels. Scale lets them absorb raw-material inflation and secure long-term silicon allocations.

Mid-tier specialists differentiate through application focus. TDK’s ultracompact module co-packages tri-axis accelerometers with on-die neural networks, reducing board space for predictive maintenance kits. Start-ups commercialize magnetoelectric composites or flexible PVDF printheads aimed at biomedical wearables.

Patent filings show rivalry around hybrid material stacks, advanced flip-chip assemblies, and AI-enabled signal chains. Suppliers that fuse hardware with subscription analytics monetize recurring revenue streams and deepen switching costs. Hardware-only vendors face margin compression unless they lock in design wins through automotive qualification or aerospace certification.

Government subsidies for domestic semiconductor plants and edge-AI initiatives shape merger pipelines. STMicroelectronics’ planned purchase of NXP’s sensor unit for up to USD 950 million illustrates consolidation aimed at securing MEMS capacity and diversifying customer mix.

Shock Sensor Industry Leaders

TE Connectivity Ltd.

Murata Manufacturing Co., Ltd.

Honeywell International Inc.

PCB Piezotronics, Inc.

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: STMicroelectronics announced acquisition of NXP Semiconductors' sensor business unit for up to USD 950 million, significantly expanding their MEMS and sensor portfolio to strengthen position in automotive and industrial markets.

- April 2025: TE Connectivity reported 17% sales growth in Industrial segment for Q2 FY2025, driven by strong demand in AI, aerospace, and energy applications, with net sales reaching USD 4.1 billion; the company's acquisition of Richards Manufacturing Co. aims to capitalize on growth opportunities in North American utility markets.

- January 2025: Honeywell introduced Battery Safety Electrolyte Sensor for electric vehicle applications, capable of detecting potential battery fires 5-20 minutes before occurrence.

- June 2024: Regal Rexnord launched next-generation Perceptiv Intelligent Reliability platform, integrating wireless vibration and temperature sensors with universal gateway capabilities for industrial manufacturing applications.

- September 2024: Transense Technologies selected for GBP 11 million UK electric vehicle R&D project, contributing SAWsense technology to enhance in-wheel motor systems for next-generation EVs.

Global Shock Sensor Market Report Scope

| Piezoelectric |

| Piezoresistive |

| Capacitive (MEMS) |

| Others |

| Quartz |

| Lead Zirconate Titanate (PZT) |

| Polyvinylidene Fluoride (PVDF) |

| Gallium Orthophosphate |

| Others |

| Automotive |

| Aerospace |

| Manufacturing |

| Consumer Electronics |

| Healthcare and Medical Devices |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Sensor Type | Piezoelectric | ||

| Piezoresistive | |||

| Capacitive (MEMS) | |||

| Others | |||

| By Material | Quartz | ||

| Lead Zirconate Titanate (PZT) | |||

| Polyvinylidene Fluoride (PVDF) | |||

| Gallium Orthophosphate | |||

| Others | |||

| By End-User Industry | Automotive | ||

| Aerospace | |||

| Manufacturing | |||

| Consumer Electronics | |||

| Healthcare and Medical Devices | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the global shock sensor market by 2030?

The market is forecast to reach USD 2.28 billion by 2030.

Which sensor type leads current revenue?

Piezoelectric devices held 48% of 2024 revenue.

Which end-user segment is expected to grow fastest through 2030?

Consumer electronics is projected to register an 11.5% CAGR.

Why is PVDF gaining traction as a material?

Its flexibility and biocompatibility support wearables and harsh-environment devices, driving a 10.9% CAGR.

Which region currently dominates sales?

Asia-Pacific captured 44% of 2024 revenue due to dense electronics and automotive ecosystems.

Page last updated on: