Tactile Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.01 Billion |

| Market Size (2030) | USD 8.37 Billion |

| Growth Rate (2025 - 2030) | 15.86% CAGR |

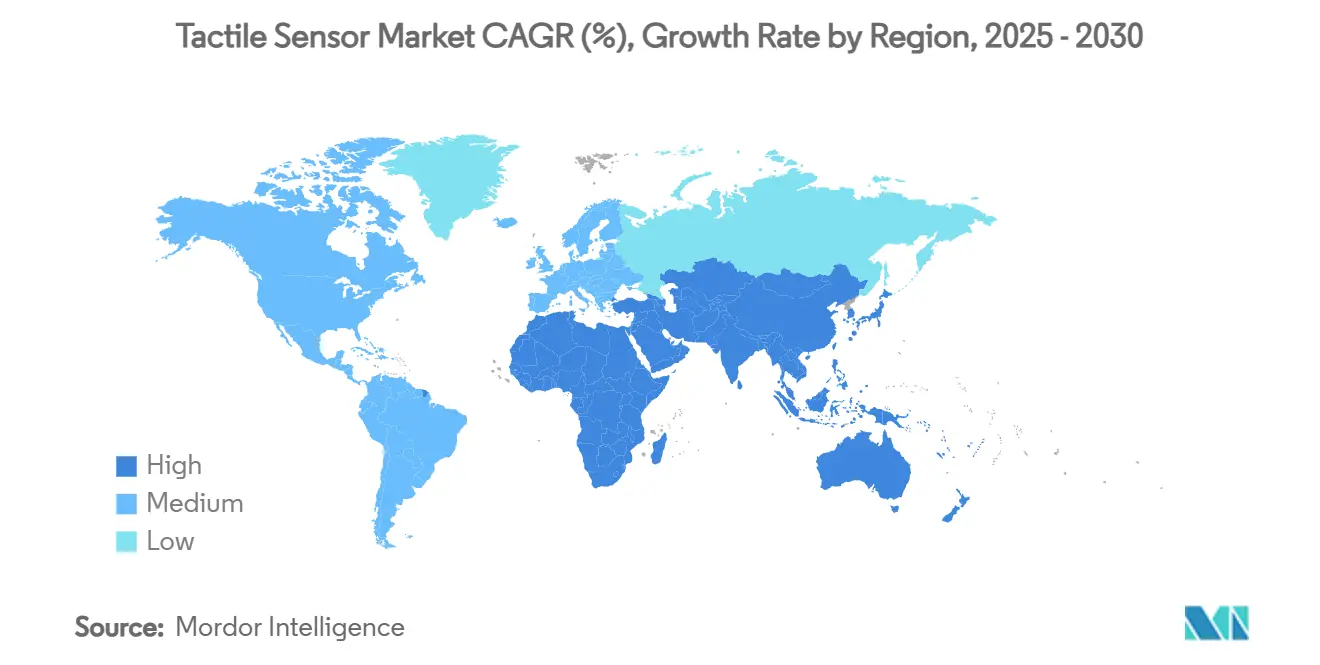

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

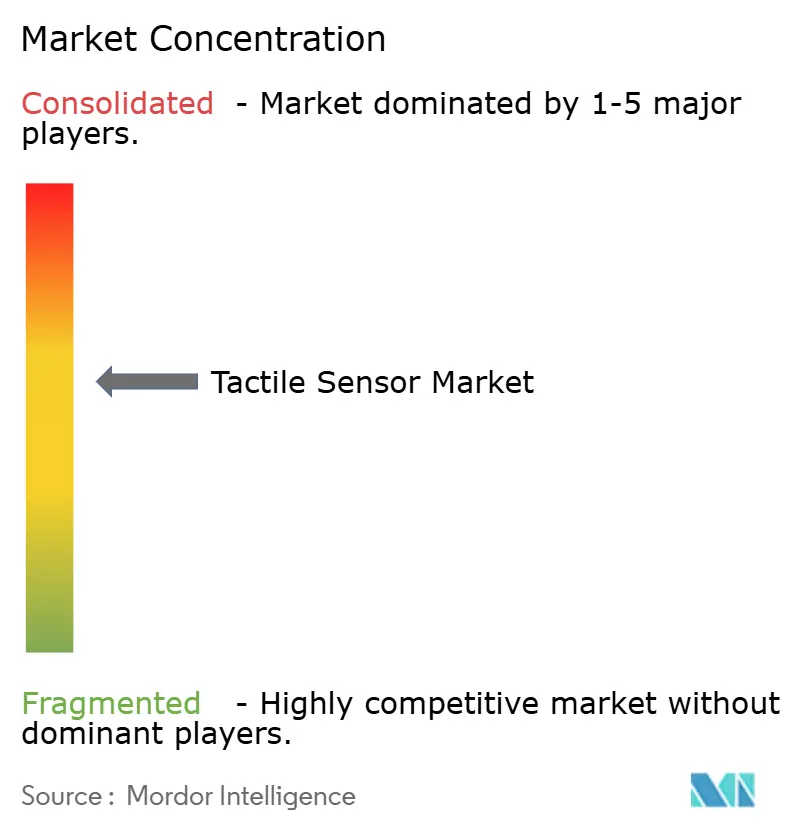

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tactile Sensor Market Analysis by Mordor Intelligence

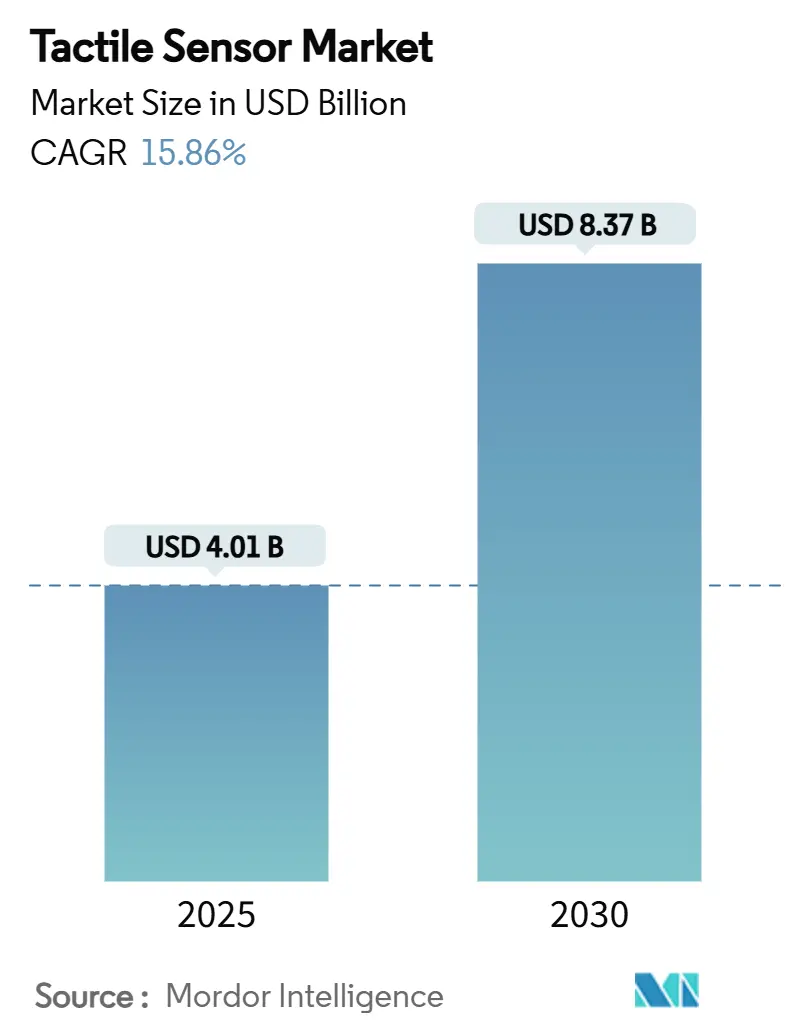

The tactile sensor market size reached USD 4.01 billion in 2025 and is forecast to attain USD 8.37 billion by 2030, reflecting a 15.86% CAGR over the period. Momentum is anchored in precision manufacturing, surgical robotics and humanoid automation, which push tactile sensing from optional add-on to foundational infrastructure. Manufacturers now recognize that visual systems alone cannot manage the sub-millimeter tolerances of high-mix assembly lines, so demand for real-time pressure mapping and force feedback is soaring. Humanoid projects, meanwhile, treat artificial skin as core architecture, allocating sizable funding for biomimetic sensing platforms. Policy support such as the EU’s IPCEI microelectronics grants and complementary US incentives further accelerates adoption, yet also introduces dependency on shifting public priorities. Supply-chain fragility in specialty elastomers and nanomaterials remains the chief cost risk, especially for sensors built for harsh chemical or temperature extremes.

Key Report Takeaways

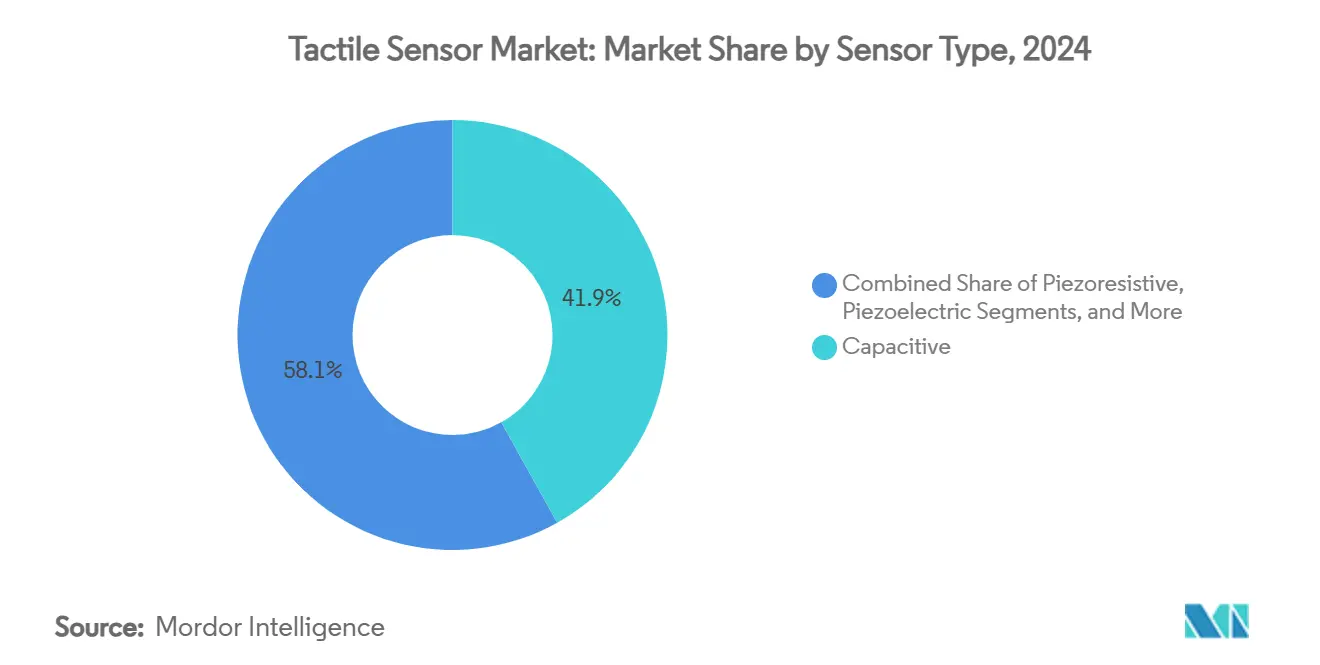

- By sensor type, capacitive solutions captured 41.91% of tactile sensor market share in 2024, while flexible printed electronics are projected to expand at a 15.91% CAGR to 2030.

- By transduction mechanism, MEMS devices held 37.53% of the tactile sensor market size in 2024; flexible printed electronics record the fastest rise at 15.91% CAGR through 2030.

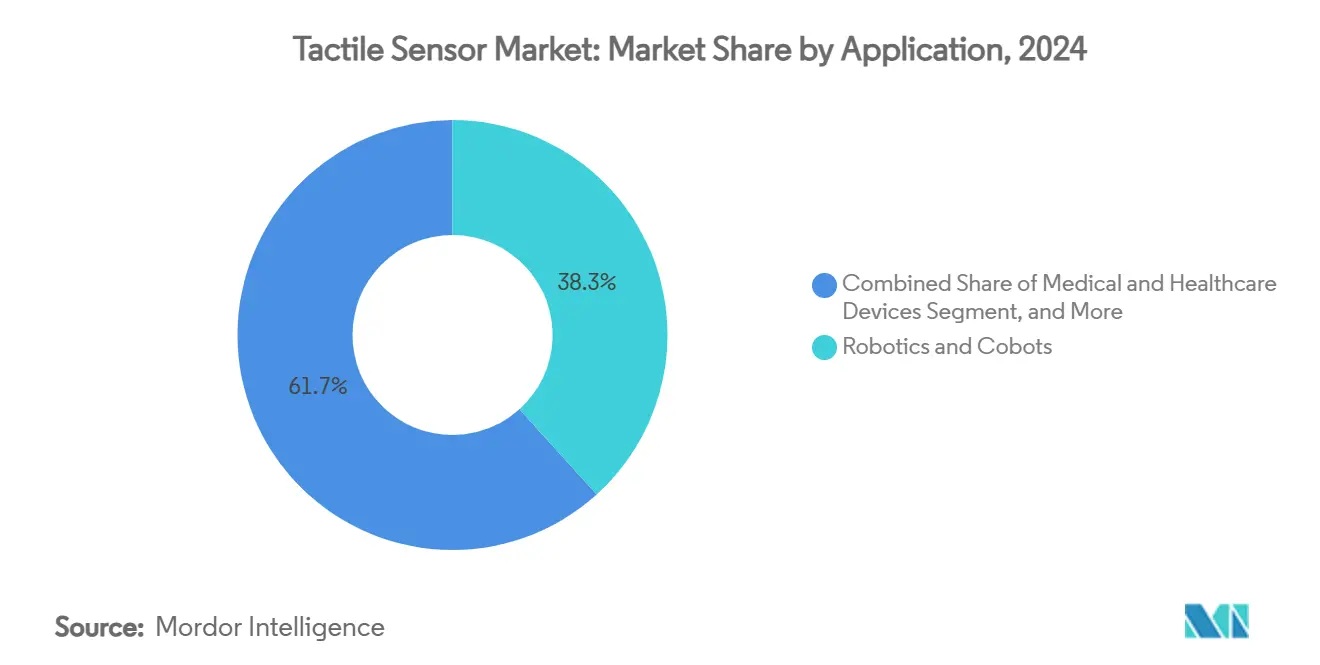

- By application, robotics and cobots commanded 38.29% of the tactile sensor market size in 2024, whereas medical and healthcare devices advance at a 16.16% CAGR between 2025-2030.

- By End-user, Advanced manufacturing held 32.47% share in 2024; whereas Healthcare providers segment emerge as the fastest-growing buyers at 16.11% CAGR between 2025-2030.

- By geography, Asia-Pacific led with a 46.19% revenue share in 2024; Middle East and Africa posts the quickest climb at 16.26% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Tactile Sensor Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid robotics adoption in precision manufacturing | +4.2% | Global, with Asia-Pacific core concentration | Medium term (2-4 years) |

| Proliferation of minimally-invasive surgical tools | +3.8% | North America and EU leading | Short term (≤ 2 years) |

| Surge in humanoid and service robot funding post-2025 | +3.1% | Global, with early gains in US, China, Japan | Long term (≥ 4 years) |

| Integration with soft-robotic grippers in agri-food automation | +2.7% | Global, with concentration in agricultural regions | Medium term (2-4 years) |

| Advances in stretchable electronic skin platforms | +2.9% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Government incentives for resilient automation | +2.1% | EU and US primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Robotics Adoption in Precision Manufacturing

High-mix, low-volume production lines now treat tactile sensing as an enabler of throughput rather than an experimental feature. Sennheiser boosted PCB test output by 33% across 115 component variants after embedding tactile-enabled cobots that quickly adapt to shape deviations without reprogramming.[1]Robotiq, “Increase Quality Testing Numbers—Robotiq,” robotiq.com Automotive suppliers are mapping gasket sealing pressures and press-fit forces to detect defects invisible to optical systems, unlocking real-time quality control. Industry 4.0 frameworks are therefore re-architected around sensor fusion nodes that ingest tactile, vision and force data simultaneously, shortening deployment time when vendors ship pre-calibrated plug-and-play arrays.

Proliferation of Minimally-Invasive Surgical Tools

Haptic-enabled surgical robots now rely on ultra-thin FlexiForce sheets, allowing clinicians to feel force gradients that differentiate healthy from diseased tissue during delicate laparoscopic maneuver.[2]Tekscan, “Tactile Feedback Robotic Surgery,” tekscan.com In rehabilitation, pressure sensors modulate exoskeleton support based on patient progression, a capability tied to the USD 500 million North American rehabilitation robotics segment in 2024. The FDA’s breakthrough pathway is fast-tracking devices that prove measurable clinical benefit, giving established medical OEMs with mature quality systems a head start in commercialization.

Surge in Humanoid and Service Robot Funding Post-2025

Funding rounds exceeding USD 300 million for humanoid projects explicitly earmark tactile skin as critical to human-like dexterity. Investors back curved, high-density sensor arrays capable of millisecond-level response times, betting that early technical dominance will yield patent shields and manufacturing scale. Hospitality and elder-care robots require compliant touch to operate safely around people, setting performance bars higher than legacy industrial sensors.

Integration with Soft-Robotic Grippers in Agri-Food Automation

Soft grippers harvesting strawberries now deploy Acoustic Soft Tactile (AST) layers that maintain gentle forces across fruit sizes, preventing bruising and allowing selective picking by firmness.[3]Vishnu Rajendran et al., “Enabling Tactile Feedback for Robotic Strawberry Handling Using AST Skin,” arxiv.orgWash-down designs rated IP67 enable food-grade sanitation, while energy-harvesting triboelectric skins run for 10-hour field shifts on battery power. Developers favor self-powered arrays that adapt to temperature and humidity swings typical of outdoor farming.

Restraints Impact Analysis of Tactile Sensor Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High calibration and drift-correction costs for large-area arrays | -2.8% | Global, particularly affecting industrial applications | Short term (≤ 2 years) |

| Supply-chain fragility of specialty elastomers and nanomaterials | -2.1% | Global, with concentration in Asia-Pacific supply chains | Medium term (2-4 years) |

| Lack of global test-standards for multimodal tactile metrics | -1.7% | Global, with regulatory focus in EU and US | Long term (≥ 4 years) |

| Cyber-security liability for tactile-data hacks in collaborative robots | -1.4% | Global, with emphasis on manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Calibration and Drift-Correction Costs for Large-Area Arrays

Arrays topping 1,000 taxels demand calibration routines whose labor rises quadratically, making manual methods cost-prohibitive for factory deployment. Temperature swings of 40 °C shift baselines enough to require frequent recalibration, halting production. Flexible substrates exacerbate drift as mechanical strain adds sensor offset, pushing vendors toward embedded intelligence that self-corrects in real time.

Supply-Chain Fragility of Specialty Elastomers and Nanomaterials

Graphene inks and conductive elastomers originate from a handful of Asia-Pacific foundries; pandemic shutdowns revealed shipment delays stretching to months. Biocompatible grades for surgical probes face even narrower supply pools due to regulatory qualification hurdles. Unable to pass volatile input costs to price-sensitive buyers, mid-tier suppliers pursue backward integration or long-term volume contracts to shield margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Tactile Sensor Market Segment Analysis

By Sensor Type:

Capacitive Solutions Extend Industrial LeadCapacitive devices held 41.91% of tactile sensor market share in 2024 and are forecast to clock a 15.88% CAGR, underpinned by immunity to electromagnetic interference around drives and welders. The ability to detect both proximity and pressure lets a single element perform dual roles in collaborative robot safety, streamlining system design. Piezoresistive sheets capture demand for sub-gram force sensing in medical staplers and micro-assembly tooling, while piezoelectric stacks address fast transient events such as impact detection. Optical arrays, prized for isolation from electrical noise, stay confined to research settings due to cost.

Second-generation capacitive skins now embed in automotive dashboards through Injection-Molded Structural Electronics (IMSE), replacing mechanical buttons with seamless touch surfaces that also relay haptic cues. Hybrid stacks combining capacitive proximity layers with piezoresistive force pixels promise single-sensor solutions for dexterous grippers, widening addressable use cases across the tactile sensor market.

By Transduction Mechanism:

MEMS Reliability Versus Flexible InnovationMEMS processes contributed 37.53% of tactile sensor market size in 2024 thanks to semiconductor fabs delivering consistent tolerances. Their ceramic packages survive humidity cycles that would delaminate printed films, satisfying automotive AEC-Q100 benchmarks. Flexible printed electronics, however, chart the fastest 15.91% CAGR as roll-to-roll lines cut per-square-meter cost and enable conformance to curved or stretchable surfaces.

Fiber-optic taxels carve a niche in nuclear or MRI environments where electromagnetic immunity is non-negotiable, whereas triboelectric skins gather the spotlight for battery-free operation in field robots. Pioneering academics demonstrated air-channel pneumatic touchpads devoid of electronics for magnetically hostile zones. Technology roadmaps converge toward hybrid assemblies that sandwich MEMS islands onto stretchable interposers, aiming to merge reliability with form-factor flexibility across the tactile sensor market.

By Application:

Robotics Lead While Healthcare RisesRobotics and cobots took 38.29% of the tactile sensor market size in 2024, cemented by safety regulations that mandate force-limited interaction. Suppliers now bundle tactile skins as default on new robot arms, slashing integrator workload. Medical and healthcare devices will outpace other segments at 16.16% CAGR as minimally invasive surgery and rehabilitation exosuits require force feedback for efficacy. Consumer electronics continue embedding localized haptics in foldable phones and next-gen game controllers, but growth moderates as base penetration climbs.

Automotive interiors adopt touch-responsive surfaces to declutter cockpits and meet distraction guidelines, while industrial logistics robots leverage pressure sensors on grippers to prevent box crushing. The interplay of diverse use cases fuels healthy competition, preventing any single vertical from monopolizing the tactile sensor market.

By End-User Industry:

Manufacturing Maturity Meets Healthcare InnovationAdvanced manufacturing held 32.47% share in 2024; years of Six Sigma initiatives prove that real-time pressure mapping cuts scrap and rework. Return-on-investment models often show payback in under 12 months for gasket or press-fit inspection, sustaining capital budgets even during macro softness. Healthcare providers emerge as the fastest-growing buyers at 16.11% CAGR, catalyzed by evidence that haptic feedback improves surgical precision and accelerates patient rehabilitation.

Consumer electronics OEMs exploit micro-tactile motors and force sensors under flexible OLED screens to deliver richer UX, while automakers shift to touch-first human-machine interfaces that reallocate physical knobs to software-defined surfaces. Agriculture cooperatives begin outfitting picking robots with compliant skins to avoid produce damage, nudging tactile sensing beyond the factory floor and diversifying revenue across the tactile sensor market.

Geography Analysis

APAC Tactile Sensor Market

Asia-Pacific led with 46.19% revenue in 2024, powered by China’s industrial robot boom and Japan’s meticulous machining traditions. The local ecosystem spans chip fabrication, sensor packaging and robot assembly, cutting lead times and cost. Chinese analysts expect the domestic sensor sector to surpass CNY 179.55 billion (USD 24.9 billion) by 2025 after producers like Keli Sensor scaled six-axis force modules for collaborative arms. South Korea invests in humanoid research that integrates full-body skins, while India’s PLI schemes coax SMEs toward automation.

MEA Tactile Sensor Market

Middle East and Africa, though embryonic, is on track for a 16.26% CAGR as Saudi and Emirati diversification agendas bankroll green-field factories and smart hospitals that specify tactile skins from the outset. Mining houses in South Africa pilot ruggedized pressure arrays on autonomous drills where dust and vibration defeat optical probes. Partnerships with European OEMs transfer know-how while uplifting local integration capacity.

North America and Europe Tactile Sensor Market

North America and Europe form the mature tier. The EU funnels EUR 21 billion into microelectronics, including tactile innovations, and already awarded ams OSRAM EUR 227 million for sensor line expansion. US robotics startups benefit from tax credits aimed at supply-chain reshoring, pairing domestic fabs with global software teams. Tight regulatory frameworks reward suppliers that document every millinewton of accuracy, supporting premium price points across the tactile sensor market.

Competitive Landscape

Market fragmentation persists as no single technology dominates every use case. Tekscan sustains a lead on thin-film pressure mapping for medical and tire testing, while XELA Robotics concentrates on compact tactile modules for cobot fingertips. New entrants such as Touchence tap stretchable conductive polymers to serve soft-robotics. Moderate concentration stems from diverse performance envelopes—industrial lines crave durability, surgeons prioritize sterility, and field robots require self-powered skins.

Strategy now tilts toward vertical integration. Vendors bundle ASICs, calibration software and API layers, selling subsystems rather than bare sensors. White-space opportunities sit in self-healing elastomers and AI-on-edge processors that classify contact patterns locally, trimming cloud bandwidth. Patent filings cluster around multi-modal stacks that co-locate pressure, temperature and proximity sensing. Meta showcased a robotic hand with an integrated capacitive-piezoresistive mesh that mimics human fingertip acuity. Apple's moisture-tolerant optical touch layers promise to disrupt wet-environment interfaces.

Acquisition likelihood grows as integrators chase turnkey capabilities. Should a leading humanoid platform lock exclusive rights to a high-resolution skin, rivals may need to buy the underlying supplier, driving eventual consolidation within the tactile sensor market.

Tactile Sensor Industry Leaders

Tekscan, Inc.

Pressure Profile Systems, Inc.

XELA Robotics, Inc.

Tacterion GmbH

SingleTact (TTP Ventures Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Tactile Sensor Market Companies Covered in this Report

- Tekscan, Inc.

- Pressure Profile Systems, Inc.

- XELA Robotics, Inc.

- Tacterion GmbH

- Touchence Inc.

- SingleTact (TTP Ventures Ltd.)

- Syntouch LLC

- OptoForce (Now OnRobot A/S)

- Weiss Robotics GmbH & Co. KG

- NanoTouch Materials, Inc.

- Zhejiang Runteck Electronics Co., Ltd.

- PiezoSensor Co., Ltd.

- TouchNetix Ltd.

- Hap2U SAS

- Nitta Corp. (Feel-MG)

- Commercial Sensors & Engineering, Inc.

- Innovative Sensor Technology IST AG

- Peratech Holdco Ltd.

- SensingTex SL

- NextInput, Inc. (A TDK Group Company)

Recent Industry Developments in Tactile Sensor Market

- March 2025: Meta revealed an advanced robotic hand featuring high-density tactile sensors aimed at mixed-reality research.

- February 2025: Apple secured a patent for a moisture-insensitive optical touch display that could redefine waterproof user interfaces.

- January 2025: MDPI Technologies published a review noting the USD 500 million North American rehabilitation robotics segment and underscoring growth avenues in Asia and Europe.

- October 2024: Tampere University introduced a non-electric pneumatic touchpad suited for MRI and explosive settings.

Global Tactile Sensor Market Report Scope

Segmentation Overview

| Capacitive |

| Piezoresistive |

| Piezoelectric |

| Optical |

| Magnetic / Hall-Effect |

| MEMS |

| Flexible Printed Electronics |

| Fiber-Optic |

| Triboelectric |

| Robotics and Cobots |

| Medical and Healthcare Devices |

| Consumer Electronics and Haptics |

| Automotive Safety and Interiors |

| Industrial and Logistics Automation |

| Advanced Manufacturing |

| Healthcare Providers |

| Consumer Electronics OEMs |

| Automotive OEMs |

| Agriculture and Food Processing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Sensor Type | Capacitive | ||

| Piezoresistive | |||

| Piezoelectric | |||

| Optical | |||

| Magnetic / Hall-Effect | |||

| By Transduction Mechanism | MEMS | ||

| Flexible Printed Electronics | |||

| Fiber-Optic | |||

| Triboelectric | |||

| By Application | Robotics and Cobots | ||

| Medical and Healthcare Devices | |||

| Consumer Electronics and Haptics | |||

| Automotive Safety and Interiors | |||

| Industrial and Logistics Automation | |||

| By End-User Industry | Advanced Manufacturing | ||

| Healthcare Providers | |||

| Consumer Electronics OEMs | |||

| Automotive OEMs | |||

| Agriculture and Food Processing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the tactile sensor market in 2025?

The tactile sensor market size reached USD 4.01 billion in 2025 and is projected to double by 2030.

What CAGR is expected for tactile sensors through 2030?

The market is forecast to grow at 15.86% CAGR during 2025-2030.

Which region leads demand for tactile sensors?

Asia-Pacific held 46.19% revenue share in 2024, propelled by China’s industrial automation boom.

Which application is growing fastest?

Medical and healthcare devices are expanding at 16.16% CAGR thanks to minimally invasive surgery and rehabilitation robotics.

What is the main restraint to widescale deployment?

High calibration and drift-correction costs for large-area arrays currently subtract 2.8 percentage points from forecast CAGR.

Who are the key players?

Tekscan dominates thin-film pressure mapping, while innovators like XELA Robotics, Touchence and GelSight address niche robotics and metrology needs.

Page last updated on: