Sensor Patch Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.20 Billion |

| Market Size (2030) | USD 19.30 Billion |

| Growth Rate (2025 - 2030) | 29.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensor Patch Market Analysis by Mordor Intelligence

The global sensor patch market size reached USD 5.20 billion in 2025 and is forecast to grow to USD 19.30 billion by 2030, posting a robust 29.99% CAGR, driven by the convergence of flexible electronics miniaturization, healthcare digitization mandates, and streamlined regulatory pathways. Continuous home-based care models now complement clinical monitoring, enabling multi-parameter tracking, real-time biomarker analysis, and drug delivery integration within a single device. North America remains the largest regional hub, while Asia-Pacific accelerates in expanding telehealth access and domestic manufacturing capacity.[1] Center for Devices and Radiological Health, “Simplera System – P160007/S047,” U.S. FDA, Nov 15, 2024, fda.gov Payer reimbursement expansion, edge-computing integration that safeguards privacy, and self-healing substrates further reinforce adoption across chronic care, sports science, and military applications. At the same time, cybersecurity vulnerabilities, adhesive-related skin irritation, and substrate-material supply risks test suppliers’ resilience, prompting investment in local processing and biocompatible adhesives.

Key Report Takeaways

- By product type, blood glucose patches led with 31.2% of sensor patch market share in 2024, while blood oxygen patches are advancing at a 31.3% CAGR through 2030.

- By application, medical monitoring accounted for a 42.3% share of the sensor patch market size in 2024, whereas drug-delivery and therapeutics are expanding at a 32.0% CAGR to 2030.

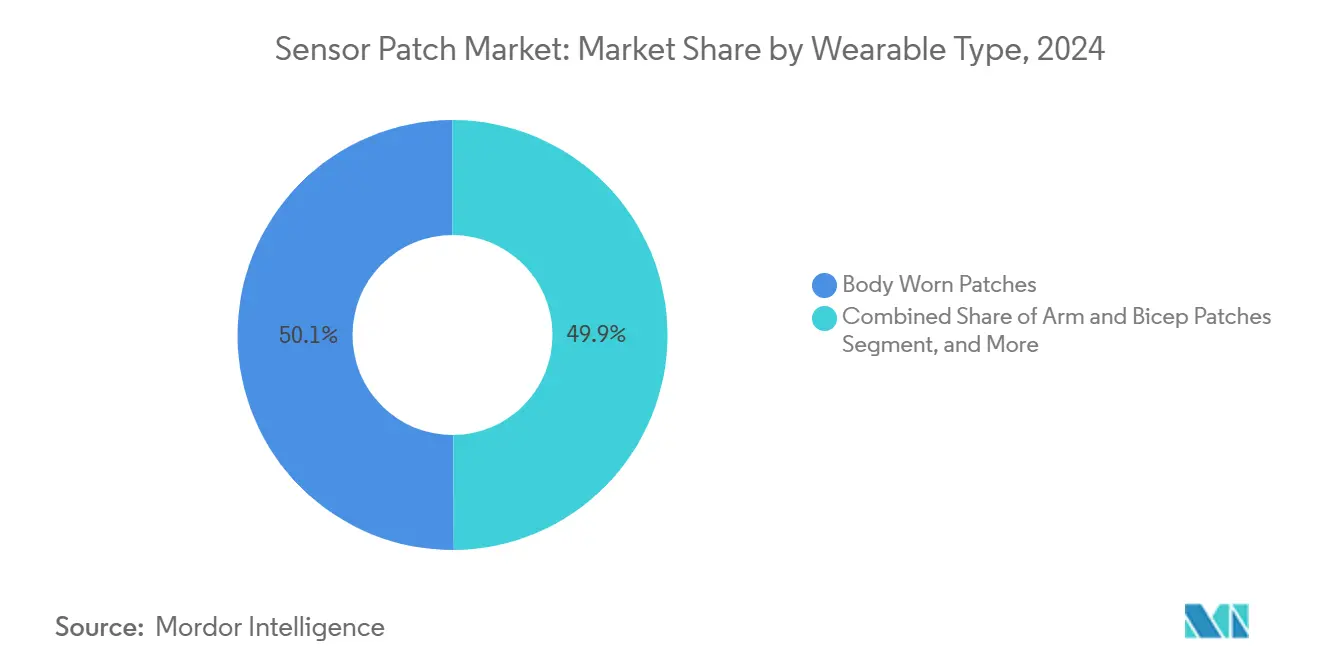

- By wearable type, body-worn patches captured 50.1% revenue share in 2024, and chest-and-torso formats are forecast to post a 31.6% CAGR during 2025-2030.

- By geography, North America commanded 35.60% of the sensor patch market in 2024; Asia-Pacific records the highest projected CAGR at 32.50% through 2030.

Global Sensor Patch Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases (Diabetes, CVD) | +8.2% | North America, Europe | Long term (≥ 4 years) |

| Expansion of Telehealth and Remote Patient-Monitoring Programs | +7.5% | Asia-Pacific, Middle East and Africa, Global | Medium term (2-4 years) |

| Miniaturization and Cost Reduction in Flexible Electronics | +6.8% | Asia-Pacific hubs | Medium term (2-4 years) |

| Growing Acceptance of Sensor Patches in Home Healthcare | +4.9% | North America, Europe | Short term (≤ 2 years) |

| Digital-Therapeutics Reimbursement Pathways Opening | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Apparel/OEM Partnerships for “Invisible” Smart Garments | +1.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Disease Drives Continuous Monitoring Demand

The global burden of diabetes and cardiovascular conditions prompts health systems to favor continuous glucose monitoring and related sensor-based interventions that lower readmission rates by up to 41%. Multi-analyte patches now consolidate glucose, lactate, and electrolytes, helping clinicians fine-tune therapy without repeated finger-stick tests. Device makers cite higher medication-adherence scores when RPM data feed directly into electronic medical records, reinforcing payer support for reimbursement. Sustained cost pressure favors sensor patches because they deliver longitudinal insight at a fraction of hospital-based monitoring expense, a trend most pronounced within value-based-care contracts. As a result, sensor patch market adoption is extending beyond diabetes toward chronic heart failure, COPD, and oncology treatment monitoring.

Expansion of Telehealth Programs Accelerates Sensor Integration

Telehealth utilization remains nearly three times above pre-2020 levels, and approximately 50 million U.S. residents actively transmit physiologic data via remote patient-monitoring platforms.[2]Anthony L. Komaroff, “What’s the Future of Remote Patient Monitoring?” Harvard Health, Dec 01, 2022, health.harvard.eduPatches that embed 5G modems support low-latency alerts, letting clinicians intervene before deterioration escalates into hospitalization. Asia-Pacific ministries of health are replicating similar fee schedules, which is propelling sensor patch market penetration in Japan, Australia, and South Korea. As AI analytics mature, telehealth platforms are increasingly prioritizing device data quality, rewarding patches that provide validated, lab-grade accuracy, thereby shifting the competitive advantage toward clinically proven vendors.

Miniaturization Advances Enable New Form Factors and Applications

Roll-to-roll printing, heterogeneous wafer stacking, and 3D micro-strain gauge architectures now let manufacturers embed AI coprocessors and power-management circuits within patches thinner than 50 µm while preserving skin conformability.[3]Tech Xplore Staff, “3D Micro Strain Gauges Promote Sensing Capabilities of Electronic Skins,” TechXplore, Sep 03, 2024, techxplore.com DNA-inspired fiber matrices withstand 1,000+ stretch cycles without electrical failure, addressing past durability complaints. Production cost curves continue to drop as factories share common substrates across multiple medical and consumer product lines. Integrated edge-processing now filters raw signals locally, transmitting only clinically relevant events, lowering bandwidth use, and improving cybersecurity posture by minimizing cloud exposure. These innovations unlock new use cases such as emotion-detection patches and underwater functions for diver safety.

Home Healthcare Acceptance Transforms Patient Engagement Models

Patients gravitate toward painless microneedle arrays that sample interstitial fluid without lancets, boosting compliance for multi-week wear cycles. Wireless-charging substrates eliminate battery swaps, and 88.2% of trial participants described 50-day monitoring as comfortable. Real-time smartphone dashboards shift responsibility toward proactive self-management, with clinicians acting as remote coaches rather than episodic troubleshooters. Consumer satisfaction feedback loops foster rapid product iteration, tightening the innovation cycle in the sensor patch market. Coupled with social determinants-of-health programs, remote monitoring reduces transport burdens for elderly or rural patients, broadening equitable access to specialist care.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent and Fragmented Regulatory Approval Processes | -4.3% | Global | Medium term (2-4 years) |

| Data-Privacy and Cybersecurity Risks in Connected Devices | -3.8% | Europe, North America | Short term (≤ 2 years) |

| High Material and Manufacturing Costs for Advanced Substrates | -3.2% | Asia-Pacific supply chain | Medium term (2-4 years) |

| Adhesive-Related Skin Irritation Lowering Long-Wear Compliance | -2.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity Delays Market Entry for Innovative Technologies

Manufacturers must juggle U.S. FDA 510(k) submissions for class II patches and EU MDR joint clinical assessments, a dual burden that can double time-to-market for breakthrough formats lacking predicate comparators. Smaller innovators without in-house regulatory teams often license technology to established firms, slowing competitive diversity. Post-market surveillance adds cost through algorithm-drift validation-essential when on-device AI learns from additional patient data. Harmonization initiatives remain years away, encouraging U.S.-centric launches first, then staged rollouts to Europe and Asia-Pacific.

Cybersecurity Vulnerabilities Threaten Patient Data and Device Integrity

Each Bluetooth or Wi-Fi patch represents an entry node for malicious actors targeting personal health information or manipulating vital-sign data, jeopardizing treatment decisions. GDPR and HIPAA fines create a material risk for providers deploying unpatched firmware, leading some hospitals to restrict device connectivity to private networks only. Edge-processing mitigates cloud exposure but shifts complexity to field-device updates, where missed patches open latent vulnerabilities. Industry working groups now draft security-by-design guidelines that will likely become de facto standards, increasing development costs in the near term yet reducing breach liabilities over the long term. Persistent public concerns can slow adoption among privacy-sensitive demographics, limiting the full addressable sensor patch market in certain regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Glucose Leads; Oxygen Sensing Accelerates

Blood glucose patches delivered 31.2% of 2024 revenue as continuous glucose monitoring is deeply embedded in diabetes care pathways, benefiting overall sensor patch market size leadership. Meanwhile, blood-oxygen patches grow at a 31.3% CAGR, aided by heightened awareness of respiratory wellness post global health events and the merging of pulse oximetry into integrated wellness platforms. Temperature and blood-pressure variants fulfill niche clinical needs, yet accuracy and reimbursement hurdles keep their uptake moderate. ECG patches earn traction in cardiac rehabilitation, supported by well-defined clinical protocols, although limited payer coverage inhibits broad deployment. Multi-parameter platforms, bundling glucose, lactate, and electrolytes, offer differentiation as hardware commoditizes, signaling a shift toward analytics-driven value capture within the sensor patch market.

Market entrants invest in printable photoplethysmography arrays to cut BOM cost, enabling heart-rate patches priced for consumer athletics. Hydration-monitoring patches backed by military field tests reach commercial pilots in sporting goods channels, showing cross-sector growth. As patent cliffs approach for single-analyte formats, suppliers accelerate research and development toward multiplexed chemistry detection. Overall, glucose remains the anchor, but growth curves flatten, while oxygen and multi-parameter solutions reshape product mix through 2030.

By Application: Monitoring Dominates; Therapeutic Integration Surges

Medical monitoring captured 42.3% of 2024 demand, delivering the largest slice of sensor patch market share because chronic-care protocols rely on near-continuous data feeds.[4] Alice Ravizza, “Regulatory Landscape of Accelerated Approval Pathways for Medical Devices,” Frontiers in Medical Technology, May 15, 2025, frontiersin.org Drug-delivery patches, integrating micro-reservoirs and feedback-controlled dosing, expand fastest at 32.0% CAGR, creating closed-loop therapeutic ecosystems. Diagnostics leverage minimally invasive fluid sampling to detect early disease biomarkers; however, reimbursement coding lags, slowing revenue recognition despite promising clinical outcomes. Fitness and sports segments exploit consumer desire for data-driven performance gains, commanding premium price points yet contributing smaller absolute value. Military programs deploy patches for heat stress and battlefield exposure analytics, with procurement cycles providing long-term but episodic orders. Infant-care patches, designed for fragile skin in neonatal intensive care units, demonstrate high ASPs and stringent accuracy, adding a stable albeit limited revenue stream.

By 2030, the sensor patch market size for closed-loop drug-delivery could quadruple current levels as more biologics gain approval for microneedle-enabled transdermal administration. Still, medical monitoring retains a sizeable customer base; integration with electronic health records cements its role in value-based-care models. Vendors increasingly bundle software subscriptions, shifting revenue mix toward recurring analytics fees rather than sole reliance on hardware margins.

By Wearable Type: Body-Worn Dominates; Chest Patches Gain

Body-worn patches achieved 50.1% revenue share in 2024 due to their flexible placement and compatibility with varied sensor arrays, safeguarding leadership in the sensor patch market. Chest-and-torso form factors, optimally positioned for cardiac and respiratory metrics, exhibit 31.6% CAGR, gaining favor in clinical trials for early extravasation detection where resistance shifts exceed 40% with minimal fluid escape. Wrist-worn patches capitalize on smartwatch familiarity but face competitive overlap; arm-based units remain favored for interstitial fluid sampling. Ear and neck variants support neurological interfaces yet stay pre-commercial.

Emerging textile-embedded sensors blur form-factor lines, embedding capacitive arrays directly into clothing fibers. Wireless charging mats and reusable substrate developments reduce cost per wear, reinforcing chest-patch adoption in home cardiac care. In the future, orthopedic rehabilitation and elderly-fall detection present incremental chest-patch use cases, bolstering their growth relative to other wearables within the sensor patch market.

Geography Analysis

North America retained a 35.60% share in 2024, aided by Medicare RPM codes, venture funding, and FDA breakthrough-device pathways that fast-track approvals for clinically meaningful innovations. Device makers leverage domestic pilots to collect evidence before global rollout, fostering a virtuous cycle of clinical validation and payer adoption. Regional hospitals increasingly standardize procurement around interoperable platforms, supporting multi-vendor integration.

Asia-Pacific logs the highest 32.50% CAGR through 2030 as governments push digital-health initiatives and local fabs drive cost declines. China’s tier-1 hospitals pilot AI-enabled cardiac patches, while Japan’s aging populace embraces at-home monitoring to reduce caregiver burden. India and Southeast Asia expand preventive-health programs, fostering sensor patch market penetration via low-cost, value-tier offerings. Local component sourcing mitigates exchange-rate risk, improving pricing flexibility and export potential.

Europe maintains stringent data-privacy rules yet ranks second in adoption, especially within Germany and the United Kingdom, where hospital networks pursue readmission penalties reduction. The EU MDR unifies classification rules, albeit with increased administrative load, prompting phased launches. Nordic nations showcase high per-capita usage and government subsidies for remote care, setting benchmarks for patient engagement. Brexit-induced divergence necessitates dual submissions for CE and UKCA marks, modestly extending time-to-profit for entrants, but market wallets remain attractive due to high healthcare spending.

Competitive Landscape

Market structure remains moderately fragmented. Medtronic leverages its Simplera disposable CGM to defend incumbency and cross-sell insulin-pump ecosystems. Abbott partners with Medtronic to co-develop interoperable platforms that widen sensor patch market coverage beyond glucose into cardiometabolic profiling. Biolinq secures USD 100 million to accelerate the development of intradermal sensors, signaling investor confidence in multi-analyte patches for metabolic health.

Start-ups such as iRhythm target niche markets in cardiac diagnostics, while textile innovators pursue OEM garment partnerships for invisible monitoring. Patent portfolios are shifting toward software, machine-learning IP, and biocompatible adhesive chemistry as baseline sensing products sell at lower margins. Suppliers court hospital networks with end-to-end analytics dashboards, seeking subscription revenue that smooths hardware cyclicality. Mergers and acquisitions activity centers on vertically bundling data-science talent, cloud pipelines, and user-experience design to reinforce platform stickiness and raise switching costs.

Sensor Patch Industry Leaders

Abbott Laboratories

Dexcom, Inc.

Medtronic PLC

iRhythm Technologies Inc.

Senseonics Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Biolinq raised USD 100 million Series B to scale its bio wearable platform, accelerating clinical trials for intradermal glucose sensors and integrated multi-analyte solutions.

- February 2025: Terasaki Institute unveiled self-healing electronic skin that restores 80% function within 10 seconds of damage, aiming to boost multi-year patch durability in harsh conditions.

- January 2025: Penn State introduced stretchable, rechargeable emotion-detection patches that pair physiologic sensors with facial-expression analytics, positioning for mental-health telemedicine adoption.

- November 2024: FDA cleared Medtronic’s Simplera disposable CGM featuring an all-in-one design, reducing insertion complexity and eliminating overtape needs.

Global Sensor Patch Market Report Scope

| Temperature Sensor Patches |

| Blood Glucose Sensor Patches |

| Blood Pressure Sensor Patches |

| Heart Rate Sensor Patches |

| ECG Sensor Patches |

| Blood Oxygen (SpO₂) Sensor Patches |

| Multi-parameter Sensor Patches |

| Hydration and Sweat-analyte Sensor Patches |

| Medical Monitoring |

| Diagnostics |

| Fitness and Sports |

| Drug-Delivery and Therapeutics |

| Military and Defense Monitoring |

| Infant and Neonatal Care |

| Geriatric Care |

| Wrist-worn Patches |

| Arm and Bicep Patches |

| Chest and Torso Patches |

| Ear and Neck Patches |

| Foot and Ankle Patches |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Temperature Sensor Patches | ||

| Blood Glucose Sensor Patches | |||

| Blood Pressure Sensor Patches | |||

| Heart Rate Sensor Patches | |||

| ECG Sensor Patches | |||

| Blood Oxygen (SpO₂) Sensor Patches | |||

| Multi-parameter Sensor Patches | |||

| Hydration and Sweat-analyte Sensor Patches | |||

| By Application | Medical Monitoring | ||

| Diagnostics | |||

| Fitness and Sports | |||

| Drug-Delivery and Therapeutics | |||

| Military and Defense Monitoring | |||

| Infant and Neonatal Care | |||

| Geriatric Care | |||

| By Wearable Type | Wrist-worn Patches | ||

| Arm and Bicep Patches | |||

| Chest and Torso Patches | |||

| Ear and Neck Patches | |||

| Foot and Ankle Patches | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the sensor patch market?

The sensor patch market size was USD 5.20 billion in 2025, reflecting rapid uptake in chronic-disease monitoring and telehealth programs.

How fast will the sensor patch market grow through 2030?

Global revenue is projected to rise to USD 19.30 billion by 2030, translating into a 29.99% CAGR driven by device miniaturization and telehealth reimbursement expansion.

Which product segment leads the sensor patch market?

Blood-glucose monitoring patches dominate, holding 31.2% of 2024 revenue, though blood-oxygen patches are the fastest growing at a 31.3% CAGR.

Which region is growing the quickest?

Asia-Pacific posts the highest regional CAGR at 32.50% due to expanding digital-health initiatives, aging demographics, and local manufacturing cost advantages.

Page last updated on: