Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 66.44 Billion |

| Market Size (2031) | USD 90.21 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

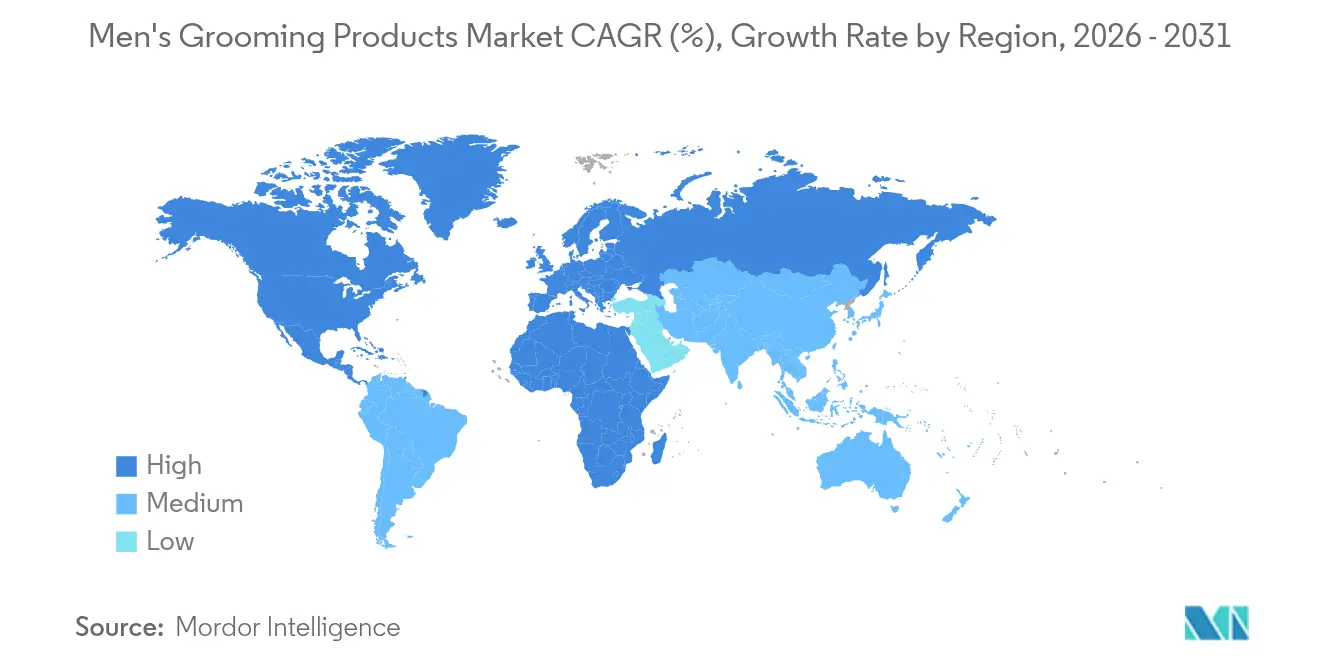

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

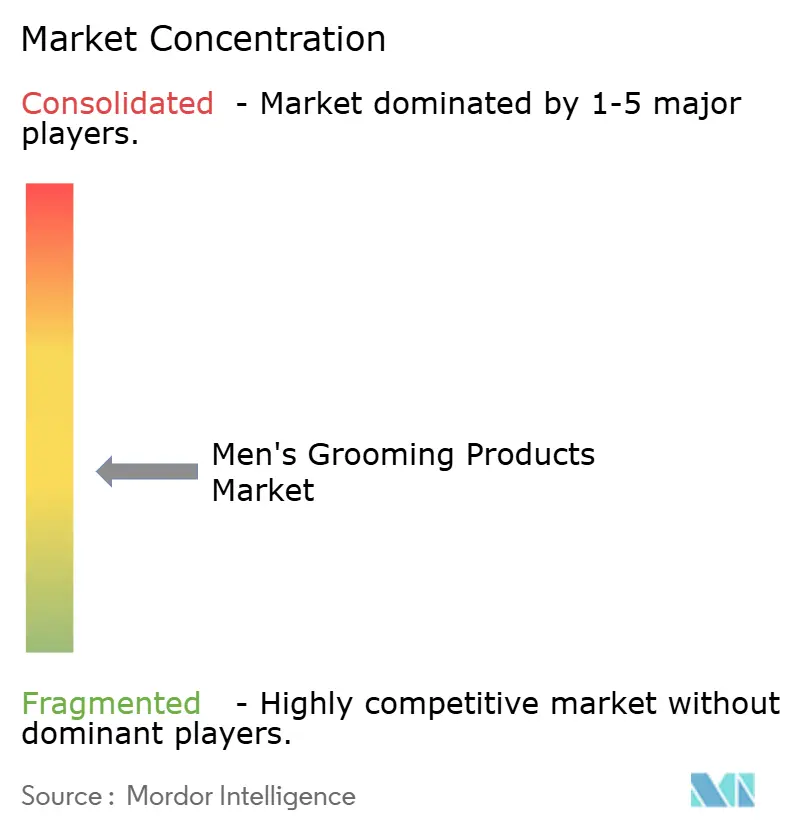

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Men's Grooming Products Market Analysis by Mordor Intelligence

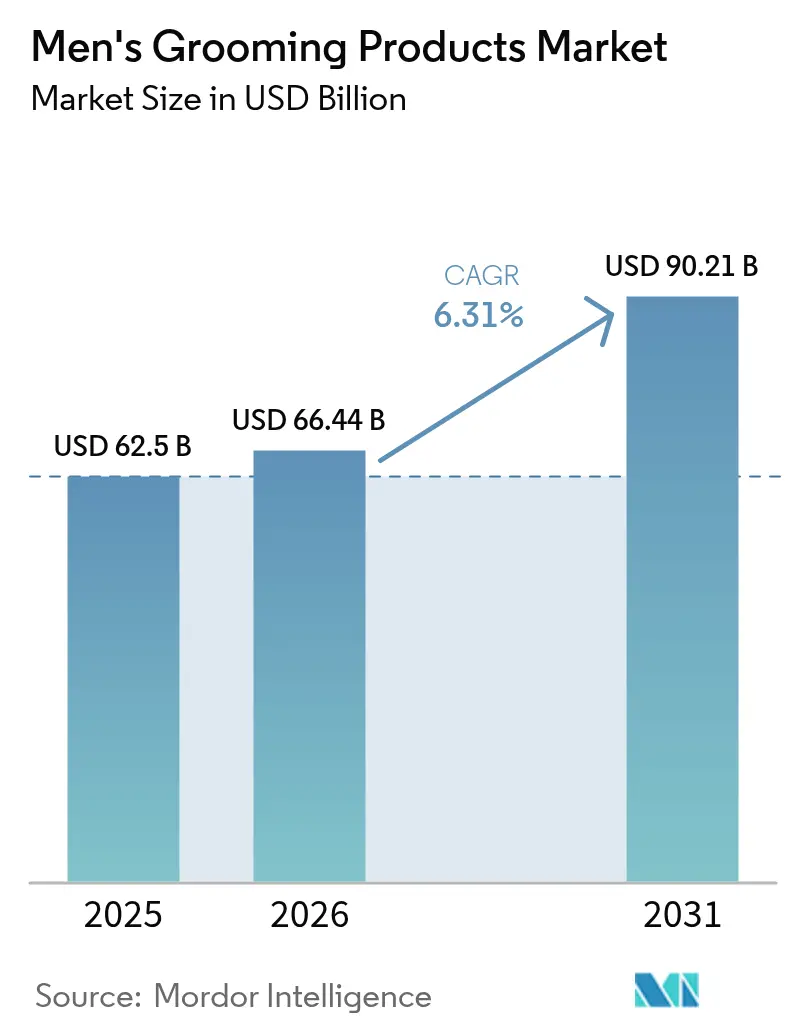

The men’s grooming products market size was valued at USD 62.50 billion in 2025 and estimated to grow from USD 66.44 billion in 2026 to reach USD 90.21 billion by 2031, at a CAGR of 6.31% during the forecast period (2026-2031). Rising disposable incomes, social media influence, and shifting cultural perceptions of masculinity are encouraging men to adopt multifaceted self-care routines that now mirror long-established female beauty behaviors. Premiumization, ingredient transparency, clean-label demand, and rapid device innovation are expanding category breadth, while sustainability concerns are reshaping packaging design and raw-material selection. This is driving the growth in the number of organic products. For instance, according to the Bundesanstalt für Landwirtschaft und Ernährung, as of December 2024, a total of 109,567 products in Germany carried organic labels[1]Source: Bundesanstalt für Landwirtschaft und Ernährung, "Quarterly redients. Th Report - Development of product advertisements for the organic seal, 4th Quarter 2024", www.oekolandbau.de. Competitive momentum is intensifying as global conglomerates acquire agile digital-native brands to secure growth niches. Meanwhile, omnichannel retail strategies are widening consumer access and fostering data-driven personalization, reinforcing the long-term expansion narrative for the men’s grooming products market.

Key Report Takeaways

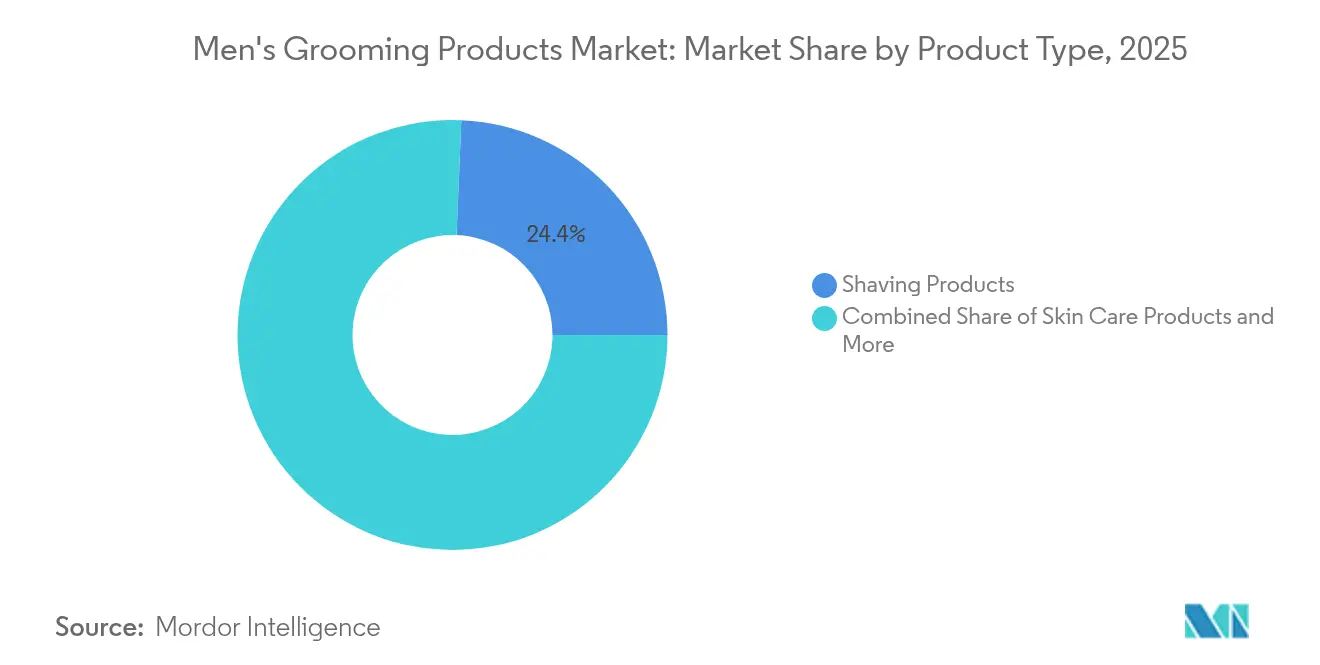

- By product type, shaving products held 24.35% of the men’s grooming products market share in 2025, whereas skincare is forecast to deliver the fastest 8.11% CAGR through 2031.

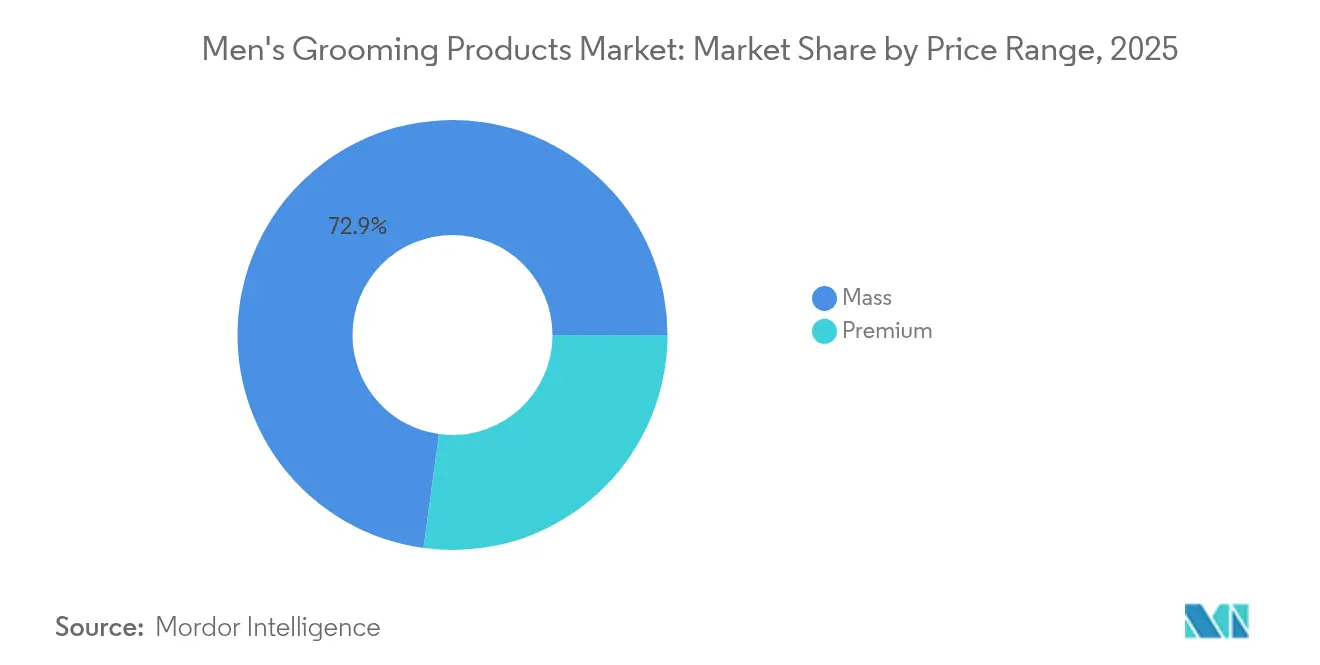

- By price range, the mass segment commanded 72.85% of revenue in 2025, yet premium lines are on track to rise at a 7.52% CAGR to 2031.

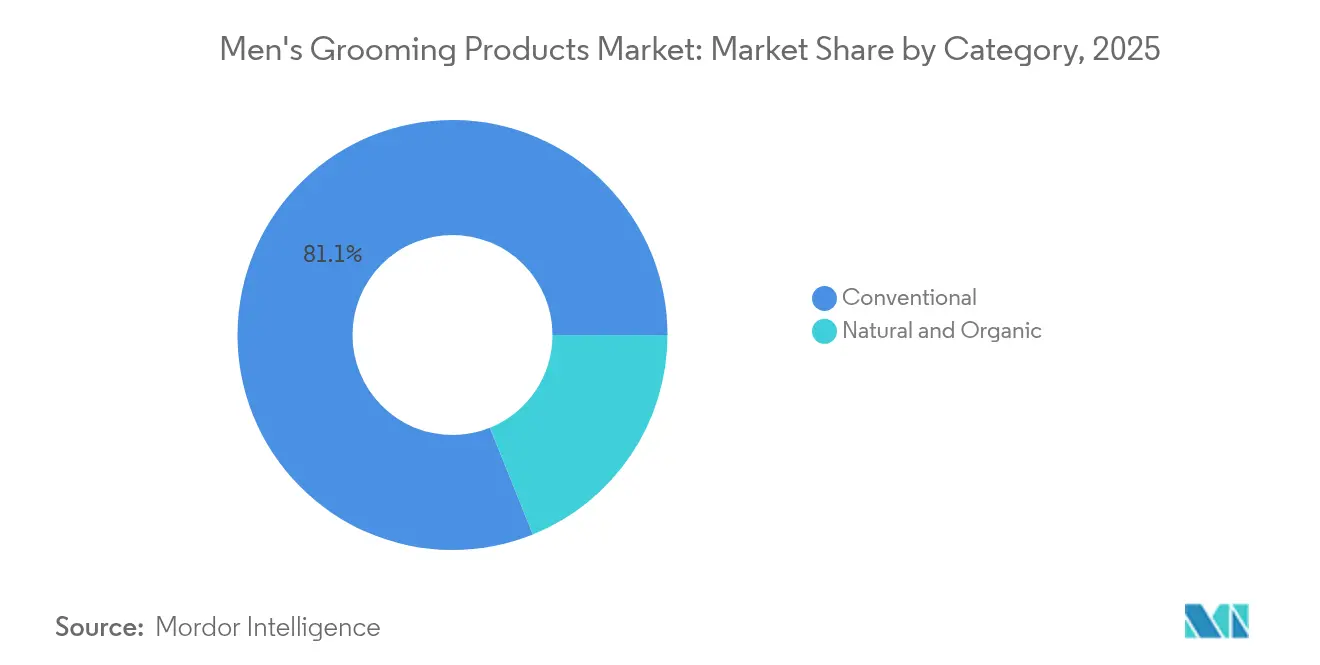

- By category, conventional formulations represented 81.10% of the men’s grooming products market size in 2025, while organic offerings are set to expand at an 8.50% CAGR over the outlook.

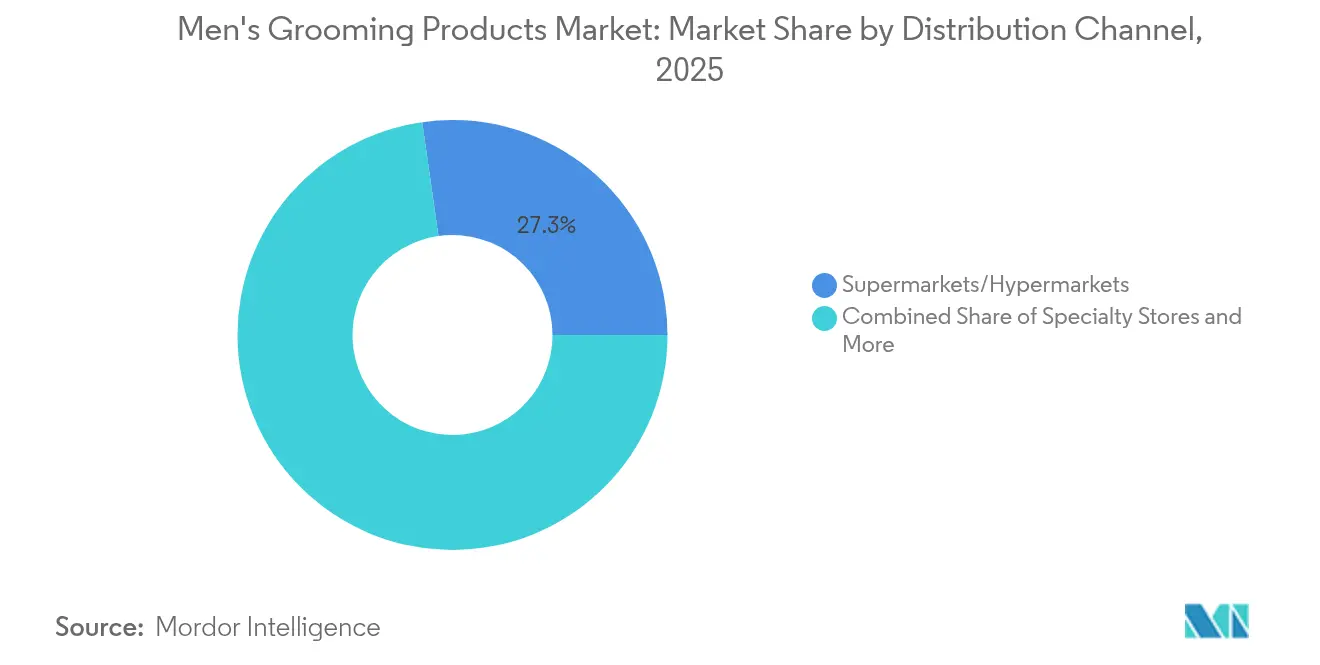

- By distribution channel, supermarkets and hypermarkets retained a 27.25% share in 2025, specialty stores, however, are advancing at a 6.84% CAGR.

- By geography, Europe led with 27.45% revenue in 2025, whereas the Middle East and Africa region is anticipated to post the strongest 8.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Men's Grooming Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of men's skincare and specialized routines | +1.2% | Global, with strong momentum in North America and Europe | Medium term (2-4 years) |

| Growing market for beard care and styling | +0.8% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Technological innovations in grooming tools | +1.0% | Global, led by developed markets | Long term (≥ 4 years) |

| Rise of natural and organic products | +0.9% | North America and EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Personalization and customization | +0.7% | Premium markets globally | Long term (≥ 4 years) |

| Premiumization trend | +0.6% | Global, strongest in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Men's Skincare and Specialized Routines

Men's skincare adoption accelerates beyond traditional aftershave applications, with specialized formulations addressing specific concerns like acne, aging, and sensitivity. According to a survey by Hot Pepper Beauty Academy in August 2023, face wash emerged as the top cosmetic choice for male consumers in Japan. The survey revealed that 49% of Japanese men purchased at least one face wash product in the past year[2]Source: Hot Pepper Beauty Academy, "Beauty Census Second Half of the Year 2023", hba.beauty.hotpepper.jp. In line with this, Dove Men+Care's Advanced Care Face + Body Cleansing collection launch in January 2025 targets dry repair, sensitive calm, and acne clear segments, reflecting 80% male consumer interest in advanced skincare solutions. Similarly, Estée Lauder's Lab Series expansion into Amazon Premium Beauty demonstrates institutional confidence in male skincare sophistication, emphasizing science-backed formulations for educated consumers. Suntory Wellness's KIZEN launch in the US market achieved 90% satisfaction rates in pre-launch testing, with 92% specifically satisfied with moisturizing properties, indicating formulation precision drives adoption. This expansion creates new revenue streams while elevating average selling prices across product portfolios. Moreover, FDA cosmetic regulations under the Modernization of Cosmetics Regulation Act of 2022 ensure safety standards that build consumer confidence in specialized formulations, driving the market's growth.

Growing Market for Beard Care and Styling

Beard care evolves from basic maintenance to sophisticated styling systems, with specialized tools and formulations creating distinct market segments. For instance, Highland's "The Wash" launch addresses hair thinning concerns among consumers under 35. Additionally, in 2023, Cosmetica Italia reported that shaving soaps and gels led to men's care product consumption in Italy, capturing a notable 58.4% share[3]Source: Cosmetica Italia, "Annual-Report-2024", cosmeticaitalia.it. Patent developments include compositions for hair loss prevention and treatment, incorporating natural extracts like shikimic acid and ursolic acid, expanding therapeutic applications. Moreover, beard styling tools integrate precision engineering with ergonomic design, creating premium price points that justify investment in specialized manufacturing capabilities. NSF/ANSI 305 standards for organic personal care products enable premium positioning for natural beard care formulations, further supporting the market's growth.

Technological Innovations in Grooming Tools

Smart grooming devices integrate sensors, artificial intelligence, and connectivity to deliver personalized experiences that traditional tools cannot match. For instance, Philips' i9000 Prestige Ultra incorporates AI-driven SenseIQ Pro technology for real-time coaching, five smart shaving modes, and a 360° Precision Flexing System. Patent activity reveals an interactive hair grooming apparatus utilizing artificial intelligence to analyze techniques and provide instructional overlays, enhancing accuracy through predictive analytics. Similarly, Gillette's sensor-enabled razors incorporate acceleration, angular velocity, and displacement sensors to provide user feedback on pressure, stroke count, and handle orientation, demonstrating IoT integration potential. These innovations command premium pricing while generating recurring revenue through app subscriptions and data analytics services. Moreover, patent protection creates competitive moats, with L'Oréal filing over 370 international applications in 2023, including smart grooming device innovations.

Rise of Natural and Organic Products

Natural and organic formulations gain traction as consumers prioritize ingredient transparency and environmental sustainability, creating premium market segments with higher margins. In line with this, players like Every Man Jack updated formulas in 2023 to enhance safety and sustainability, emphasizing naturally derived and plant-based components while avoiding parabens and phthalates. Similarly, Dr. Squatch's USD 1.5 billion valuation in June 2025 demonstrates natural grooming market potential, with Unilever's acquisition targeting international expansion of natural soap and deodorant formulations. Moreover, USDA National Organic Program regulations enable certified organic labeling for cosmetic products containing agricultural ingredients, creating differentiation opportunities for premium positioning, while Bioagricert certification standards prohibit GMOs and outline allowed substances, supporting premium price justification through verified organic claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense market competition | -0.8% | Global, particularly in mature markets | Short term (≤ 2 years) |

| Environmental concerns associated with packaging | -0.6% | Europe and North America leading, expanding globally | Medium term (2-4 years) |

| Fluctuating raw material costs | -0.7% | Global, with regional supply chain variations | Short term (≤ 2 years) |

| Allergic reactions and skin sensitivities | -0.4% | Global, with regulatory focus in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Market Competition

Market saturation in developed regions intensifies competitive pressure, compressing margins and requiring increased marketing investments to maintain share. Suave's relaunch with 34 new products priced under USD 6 in June 2025 demonstrates value positioning strategies, emphasizing competitive pricing against premium brands like Olaplex through "dupe culture" marketing. Procter & Gamble's grooming segment experienced net sales of USD 1.68 billion despite 4% unit volume increases as of June 2025, indicating pricing pressure from competitive dynamics. Moreover, private label expansion threatens branded manufacturers, with retailers developing sophisticated formulations that match branded performance at lower price points. Digital-native brands like Harry's and Dollar Shave Club disrupted traditional distribution models, forcing established players to invest heavily in direct-to-consumer capabilities and subscription services. Thus, competitive intensity accelerates consolidation, as demonstrated by major acquisitions like Unilever's Dr. Squatch purchase, creating barriers for smaller independent brands seeking market access.

Environmental Concerns Associated with Packaging

Sustainability pressures drive packaging innovation requirements that increase costs while consumers demand environmental responsibility without premium pricing. Edgewell Personal Care's razor recycling program addresses the 2 billion razors that are annually discarded, requiring infrastructure investment and logistics coordination. In line with this, players like Dove Men+Care commit to 100% recyclable packaging by 2025, with roll-on deodorants containing 60% recycled plastic and body wash bottles made from 100% recycled materials. Firsthand Supply utilizes Post Consumer Resin from recycled milk jugs, successfully recycling over 300,000 containers while maintaining product integrity and visual appeal. Leaf Shave achieved Climate Neutral Certification with 881 tCO2e emissions in 2023, implementing 25% shipping material emission reductions and greener office supply transitions. Regulatory frameworks like the EU's packaging waste directives create compliance costs that disproportionately impact smaller manufacturers lacking scale economies for sustainable packaging investments, restraining the market's growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skincare Acceleration Challenges Shaving Dominance

Shaving products maintained a 24.35% market share in 2025, reflecting established consumer habits and repeat purchase patterns, while skincare products achieved an 8.11% CAGR through 2031, indicating fundamental shifts in male grooming priorities. Traditional shaving categories, including pre-shave, post-shave, and razors and blades, benefit from technological innovations like Panasonic's Series 900s, featuring 70,000 cutting actions per minute and Responsive Beard Sensor+ Technology. Hair care products experience steady growth through specialized formulations addressing thinning concerns, with Highland's "The Wash" targeting consumers under 35 who invest in preventative care. Other product types, including fragrances and body care, expand through celebrity partnerships, exemplified by Aramis' Intuition launch with Dwyane Wade as global ambassador in May 2025.

Skincare acceleration stems from sophisticated consumer education and targeted formulations addressing specific concerns like acne, aging, and sensitivity. Dove Men+Care's Advanced Care Face + Body collection launch in March 2023 demonstrates market sophistication, with 80% of men expressing interest in advanced skincare solutions. Similarly, Lab Series expansion into Amazon Premium Beauty in August 2024 emphasizes science-backed formulations for educated consumers seeking clinical efficacy. Patent developments include compositions for treating urushiol-induced contact dermatitis using lysine, addressing skin irritation concerns that drive skincare adoption. Moreover, FDA cosmetic regulations under MoCRA ensure safety standards that build consumer confidence in specialized skincare formulations, supporting premium price positioning across the category.

By Price Range: Premium Growth Outpaces Mass Market Expansion

Mass market products command 72.85% market share in 2025, demonstrating broad consumer accessibility and established distribution networks, while premium segments achieve 7.52% CAGR through 2031, reflecting consumer willingness to invest in superior formulations and experiences. Premium positioning benefits from technological innovations like Philips' i9000 Prestige Ultra, featuring AI-driven coaching and precision engineering. Mass market strategies focus on value positioning, exemplified by Suave's relaunch with 34 products priced under USD 6 in March 2025, targeting consumers seeking premium performance at accessible price points.

Premium growth acceleration stems from consumer sophistication and willingness to invest in personalized experiences that deliver superior results. For instance, Dr. Squatch's USD 1.5 billion valuation in June 2025 demonstrates premium natural positioning effectiveness, with Unilever's acquisition targeting international expansion of high-margin formulations. Similarly, Scotch Porter's recognition as the fastest-growing US male grooming brand reflects premium positioning success, achieving over 70% growth while emphasizing community impact and holistic wellness approaches. Moreover, patent protection enables premium pricing through technological differentiation, with L'Oréal filing over 370 international applications in 2023, including smart grooming innovations. Mass market resilience stems from distribution accessibility and repeat purchase patterns, though margin pressure from private label expansion requires continuous innovation to maintain competitive positioning.

By Category: Organic Surge Challenges Conventional Dominance

In 2025, conventional products command an 81.10% market share, thanks to their established formulations and cost-effective manufacturing. Meanwhile, the organic segment is on a growth trajectory, boasting an 8.50% CAGR through 2031. This surge is fueled by rising demands for ingredient transparency and a heightened awareness of sustainability. Regulatory frameworks, such as the USDA National Organic Program certification, bolster organic growth. They allow for premium positioning by verifying agricultural ingredient standards. Additionally, NSF/ANSI 305 standards play a pivotal role, setting labeling requirements for products with a minimum of 70% organic content. This third-party verification fosters trust among consumers. Conventional formulations have a competitive edge, thanks to their proven efficacy, cost optimization, and economies of scale in manufacturing. These advantages allow them to price competitively across mass market segments.

Bioagricert certification standards further enhance this positioning. By prohibiting GMOs and outlining permissible substances, they lend credibility to organic claims, appealing to environmentally conscious consumers. The patent landscape is also evolving, with developments highlighting natural compositions for hair loss treatments. These innovations, rooted in botanical extracts, broaden therapeutic applications while adhering to organic formulation constraints. Conventional products are not standing still either. They're adopting hybrid approaches, blending natural ingredients with synthetic ones. This strategy optimizes performance and creates 'bridge products' that cater to a wide array of consumer preferences without overhauling their entire formulation.

By Distribution Channel: Specialty Stores Outpace Traditional Retail

In 2025, supermarkets and hypermarkets capture a 27.25% market share, thanks to their widespread consumer accessibility and well-established supply chains. Meanwhile, specialty stores are on track to achieve a 6.84% CAGR through 2031, underscoring a growing consumer preference for curated shopping experiences and expert guidance. Specialty retailers, benefiting from personalized consultations and a premium brand positioning, showcase the potential of digital platforms with Lab Series' recent launch on Amazon Premium Beauty. The online retail sector is witnessing a surge, particularly through direct-to-consumer strategies. A testament to this trend, Philips reveals that nearly 50% of its global Personal Health sales are now online. Convenience stores continue to thrive, driven by impulse purchases and travel-sized product offerings.

Digital-native brands, exemplified by House of Atlas, are opting for direct-to-consumer launches. This strategy not only circumvents traditional retail margins but also offers pricing flexibility and enhanced control over customer relationships. Bath & Body Works is adapting to market trends, venturing into men's grooming. By introducing face and beard care, hair care, and shaving products, they're strategically leveraging their established customer base. Ulta Beauty, recognizing the market's potential, is expanding its men's grooming category. With a robust loyalty program boasting over 43 million members, Ulta enjoys a significant edge in customer data insights. The growth of specialty stores can be attributed to their emphasis on expert consultations, curated product selections, and partnerships with premium brands. These elements collectively craft a shopping experience that justifies higher price points, setting them apart from mass retail alternatives.

Geography Analysis

Regional dynamics, shaped by cultural nuances, economic trajectories, and evolving consumer preferences, define the global men's grooming products market. Europe, with its deep-rooted appreciation for premium offerings and a well-established brand landscape, commands the largest market share. In 2025, Europe accounted for 27.45% of global revenues, bolstered by legacy luxury brands, unified EU cosmetic regulations, and a consistent cost structure. While Western Europe leans towards upscale fragrances and cutting-edge anti-aging solutions, Eastern Europe boasts cost-effective manufacturing and a burgeoning middle-class appetite. Sustainability trends from the Nordics are swiftly gaining traction, pushing for wider adoption of recyclable packaging. Countries like the U.K., Germany, and Italy lead the continent's demand for natural formulations and established grooming routines. North America, closely trailing Europe, thrives on its affluent consumer base, heightened brand awareness, and the emergence of the "metrosexual" trend, with notable investments in high-tech grooming devices and subscription services.

In the Middle East and Africa, an impressive 8.36% CAGR positions it as the fastest-growing region. Dubai's strategic logistics zones and Saudi Arabia's Vision 2030 retail initiatives are paving the way for global grooming brands. Factors like a youthful urban demographic, heightened social media influence, and a surge in tourism are propelling consumption. While South Africa serves as a pivotal distribution hub, Nigeria holds promise for future growth, contingent on stabilizing spending power.

North America stands at the forefront of tech-centric grooming solutions and rapidly expanding direct-to-consumer brands. Suntory's KIZEN moisturizer, boasting a 90% satisfaction rate in U.S. trials, underscores the market's receptiveness to scientifically formulated imports. Canadian consumers echo U.S. preferences, especially favoring clean labels, while Mexico's maquiladora system facilitates razor assembly near the border. The Asia-Pacific region presents a dual narrative: Japan and South Korea lead in innovation, while India and China drive volume, each year welcoming millions of new entrants to the men's grooming arena.

Competitive Landscape

The global men's grooming products market is fragmented, with major players like Procter & Gamble, Unilever, L'Oréal, Beiersdorf, and Edgewell Personal Care competing with numerous regional and niche digital-native brands. The competitive landscape is defined by strategies focused on product innovation, expanding into specialized categories, acquiring agile digital-first brands, and enhancing omnichannel retail presence. For example, in August 2024, MENZ launched a comprehensive line for men, focusing on sophisticated scents and effective yet gentle formulations, while Maneuver introduced a luxury grooming line in September 2024, signaling a move towards premium, high-end experiences. In March 2024, Ustraa launched charcoal face wash and beard growth oil, emphasizing natural ingredients and botanical extracts to appeal to the growing demand for natural and plant-based formulations.

While top multinationals hold significant positions, numerous indie challengers seize niche opportunities. In 2025, Unilever acquired Dr Squatch for USD 1.5 billion, highlighting incumbents' preference for tapping into the virality of natural soaps rather than starting anew. L’Oréal's 370-plus patent filings, covering innovations from smart razors to carbon-negative packaging, showcase a research and development depth that's challenging for smaller brands to rival. Philips carves out a niche with AI-driven firmware and subscription-based blades, creating ecosystem lock-ins reminiscent of electric toothbrush models. Major players are actively acquiring these successful smaller brands to secure growth niches, a trend that is intensifying competitive momentum. The market is also being shaped by sustainability efforts, with players like Dove Men+Care committing to recyclable packaging by 2025 and Edgewell Personal Care launching a razor recycling program. In terms of distribution, e-commerce is a critical channel, with digital-native brands like House of Atlas focusing on direct-to-consumer launches. At the same time, companies like Philips are witnessing a shift in global personal health sales moving online, indicating a significant change in consumer purchasing habits.

Furthermore, traditional retailers are expanding their offerings; for instance, Bath & Body Works has ventured into men's grooming by leveraging its existing customer base, and Ulta Beauty is expanding its men's category, utilizing its extensive loyalty program for customer insights. Overall, the market is driven by rising male beauty consciousness, premiumization, and the growing influence of social media influencers. The fastest growth is expected in the skincare and organic product segments, along with the Middle East and Africa region. These factors combine to create a dynamic and highly competitive market where innovation, targeted strategies, and strategic acquisitions are key to gaining market share.

Men's Grooming Products Industry Leaders

-

Beiersdorf AG

-

Procter & Gamble Co.

-

L'Oréal SA

-

Unilever PLC

-

LVMH Moet Hennessy Louis Vuitton SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Joico launched a scalp vitality collection with a skincare-inspired approach to scalp and hair health. It included a shampoo with stinging nettle and rosehip oil to hydrate and protect the scalp barrier, an exfoliating foaming scrub to clear buildup, and a replenishing essence to soothe dry, itchy scalps. These products were asserted to support optimal scalp health.

- September 2024: Maneuver launched its men's luxury grooming line, crafted to offer a premium grooming experience combining luxury with practicality. It included face washes, moisturizers, and pre- and post-shave products that cater to both bearded and clean-shaven men. The products focused on hydrating and soothing the skin while ensuring a smooth shave.

- August 2024: MENZ launched a comprehensive range of grooming essentials for men, such as hair spray, shaving foam, shampoo, face wash, and deodorant body spray. The line was characterized by sophisticated, fresh scents and formulations balancing effectiveness with gentleness. These products were asserted to be designed to suit men looking for an all-in-one grooming solution that fits seamlessly into busy lifestyles.

- March 2024: Ustraa launched charcoal face wash and beard growth oil, emphasizing natural ingredients, harnessing charcoal’s deep cleansing properties to remove impurities and excess oil without stripping the skin. The beard growth oil was asserted to be enriched with botanical extracts designed to nourish hair follicles and promote healthy, thicker beard growth. Together, these products aimed to improve skin clarity and beard vitality using plant-based formulations.

Global Men's Grooming Products Market Report Scope

Male grooming products include a wide range of personal care products especially designed for men to maintain hygiene and enhance appearance.

The scope of the study is segmented by product type, distribution channel, and geography. The market is segmented by product type into hair care, skin care, shaving products, and others. The skin care products segment is further segmented into face washes, moisturizers, face masks, and other skincare products. The hair care products segment is further segmented into shampoos and conditioners, styling products, hair colorants, and other hair care products. The shaving products segment is further classified into pre-shave, post-shave, razor and blades. The market is segmented by distribution channel into specialty stores, supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing and forecasts have been done for each segment based on value (USD).

By Product Type

| Skin Care products | Face Wash | |

| Moisturizers | ||

| Face Mask | ||

| Other Skin Care Products | ||

| Hair Care products | Shampoo and Conditioners | |

| Styling Products | ||

| Hair Colorants | ||

| Other Hair Care Products | ||

| Shaving Products | Pre-Shave | Shaving Cream |

| Pre-Shave Oil | ||

| Shaving Soap | ||

| Other Pre-Shave Products | ||

| Post-Shave | After-Shave | |

| Balms | ||

| Other Post-Shave Products | ||

| Razors and Blades | ||

| Other Product Types | ||

By Price Range

| Mass |

| Premium |

By Category

| Conventional |

| Natural and Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Retail Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Skin Care products | Face Wash | |

| Moisturizers | |||

| Face Mask | |||

| Other Skin Care Products | |||

| Hair Care products | Shampoo and Conditioners | ||

| Styling Products | |||

| Hair Colorants | |||

| Other Hair Care Products | |||

| Shaving Products | Pre-Shave | Shaving Cream | |

| Pre-Shave Oil | |||

| Shaving Soap | |||

| Other Pre-Shave Products | |||

| Post-Shave | After-Shave | ||

| Balms | |||

| Other Post-Shave Products | |||

| Razors and Blades | |||

| Other Product Types | |||

| By Price Range | Mass | ||

| Premium | |||

| By Category | Conventional | ||

| Natural and Organic | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Convenience Stores | |||

| Specialty Stores | |||

| Online Retail Stores | |||

| Other Retail Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Sweden | |||

| Belgium | |||

| Poland | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Thailand | |||

| Singapore | |||

| Indonesia | |||

| South Korea | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Saudi Arabia | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How large is the men’s grooming products market in 2026?

The men’s grooming products market size is USD 66.44 billion in 2026 and is poised to hit USD 90.21 billion by 2031.

Which product category is growing fastest?

Skincare is forecast to expand at an 8.11% CAGR, making it the quickest-growing category within men’s grooming.

Which region will post the highest growth rate?

The Middle East & Africa region is projected to record an 8.36% CAGR, outpacing all other geographies.

Why are premium products gaining share?

Advanced technology, luxurious ingredients, and lifestyle storytelling support a 7.52% CAGR for premium lines compared with the mass segment.

What role does sustainability play?

Recyclable packaging and certified organic formulations are propelling an 8.50% CAGR for the organic segment while reshaping supply-chain priorities.

Which company strategies stand out in 2026?

Acquisitions such as Unilever’s Dr Squatch deal and Philips’ AI-enabled device pipeline illustrate how incumbents secure innovation and premium pricing.

Page last updated on: