Sexual Wellness Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

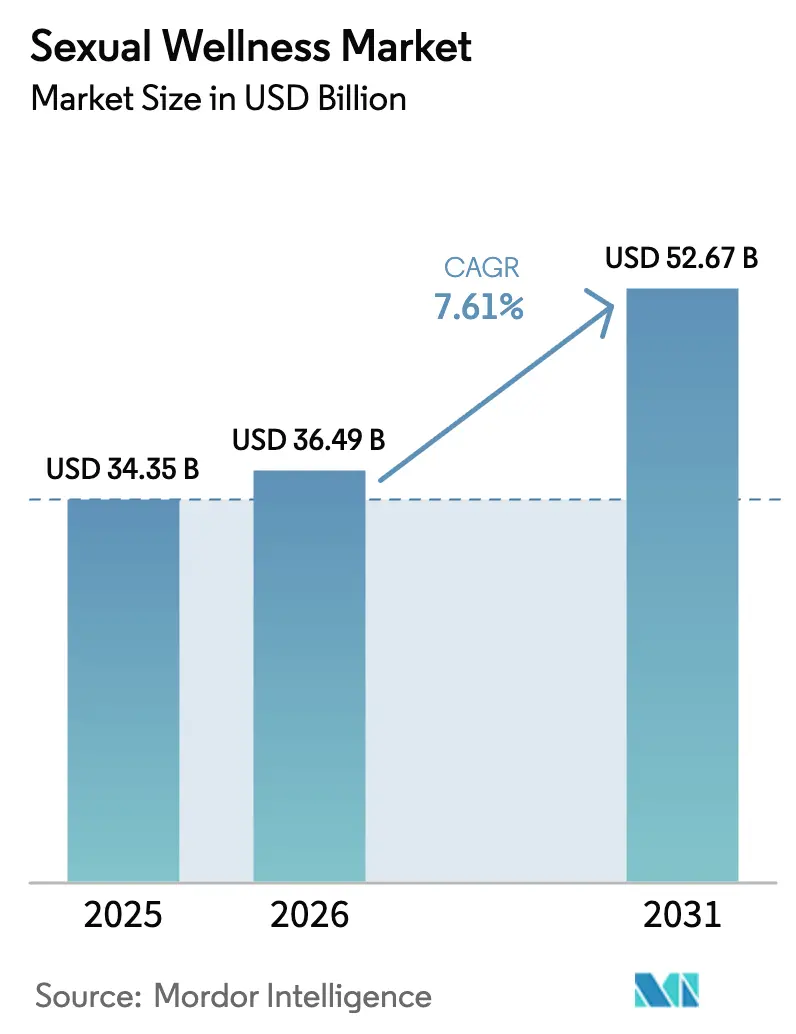

| Market Size (2026) | USD 36.49 Billion |

| Market Size (2031) | USD 52.67 Billion |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

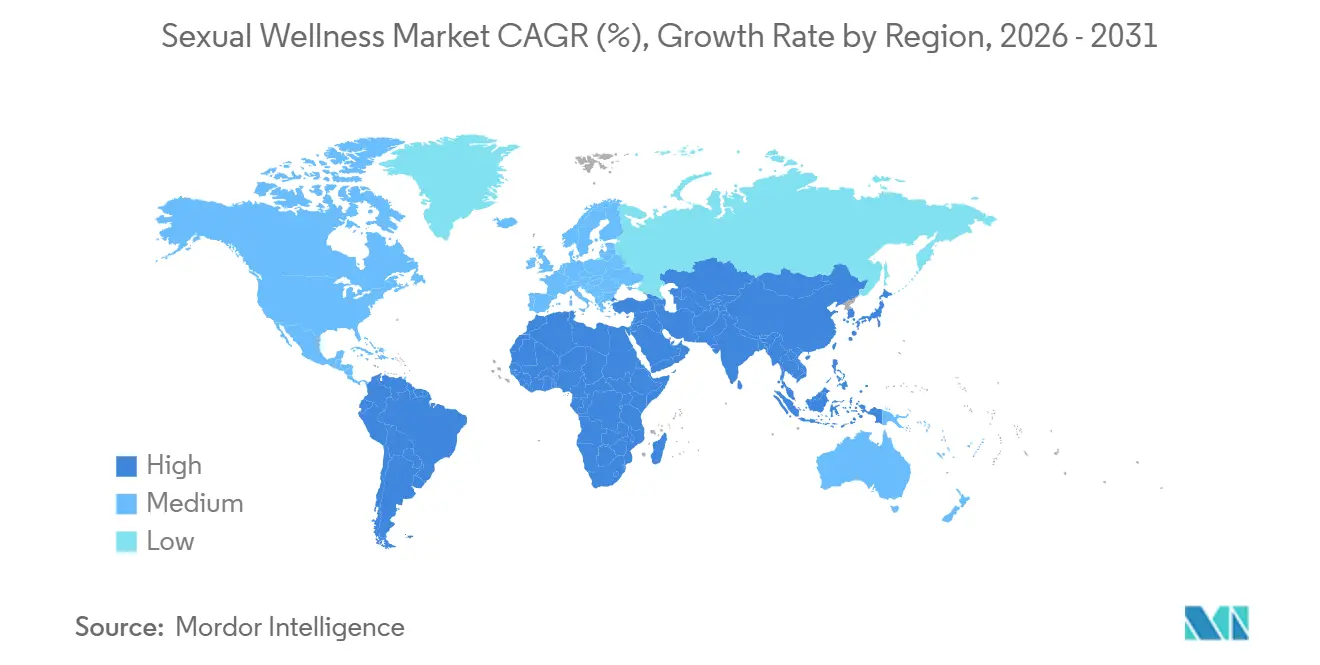

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

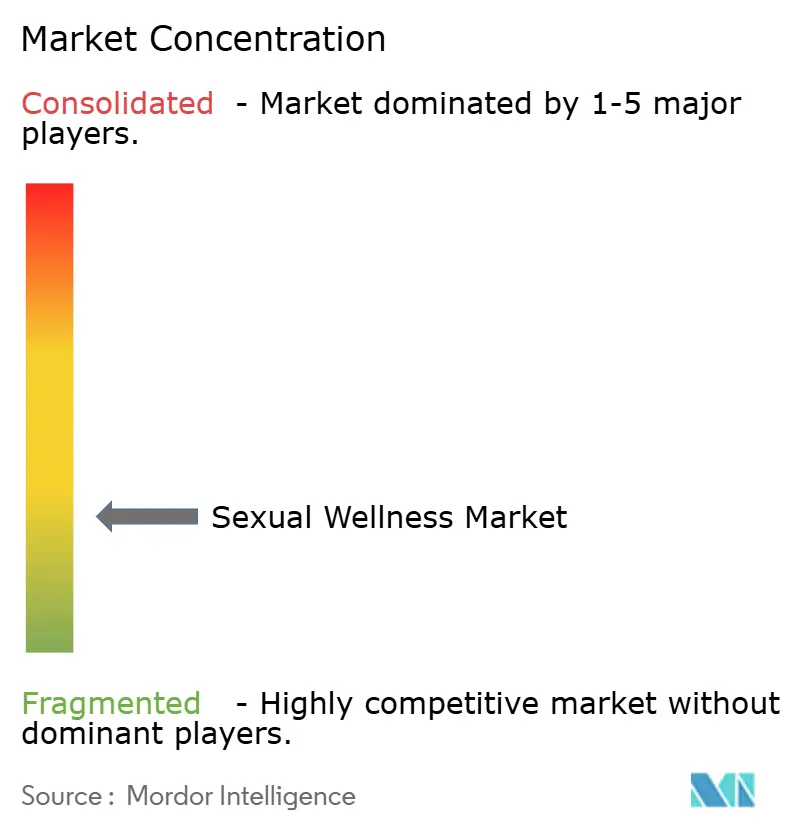

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sexual Wellness Market Analysis by Mordor Intelligence

The Sexual Wellness Market size is expected to grow from USD 34.35 billion in 2025 to USD 36.49 billion in 2026 and is forecast to reach USD 52.67 billion by 2031 at 7.61% CAGR over 2026-2031.

E-commerce platforms convert what once was a discreet, episodic purchase into a digital-first, subscription-driven habit, giving direct-to-consumer brands behavioral data that guides rapid product iteration. Regionally, the Middle East & Africa is the fastest-growing territory as smartphone adoption overcomes brick-and-mortar visibility barriers. Product innovation clusters around connected toys and premium, body-safe materials, while corporate wellness programs bundle sexual health benefits to create a new B2B2C channel. Competitive intensity remains moderate: multinational condom makers still anchor store shelves, yet digitally native specialists gain share by coupling influencer marketing with discreet fulfillment.

Key Report Takeaways

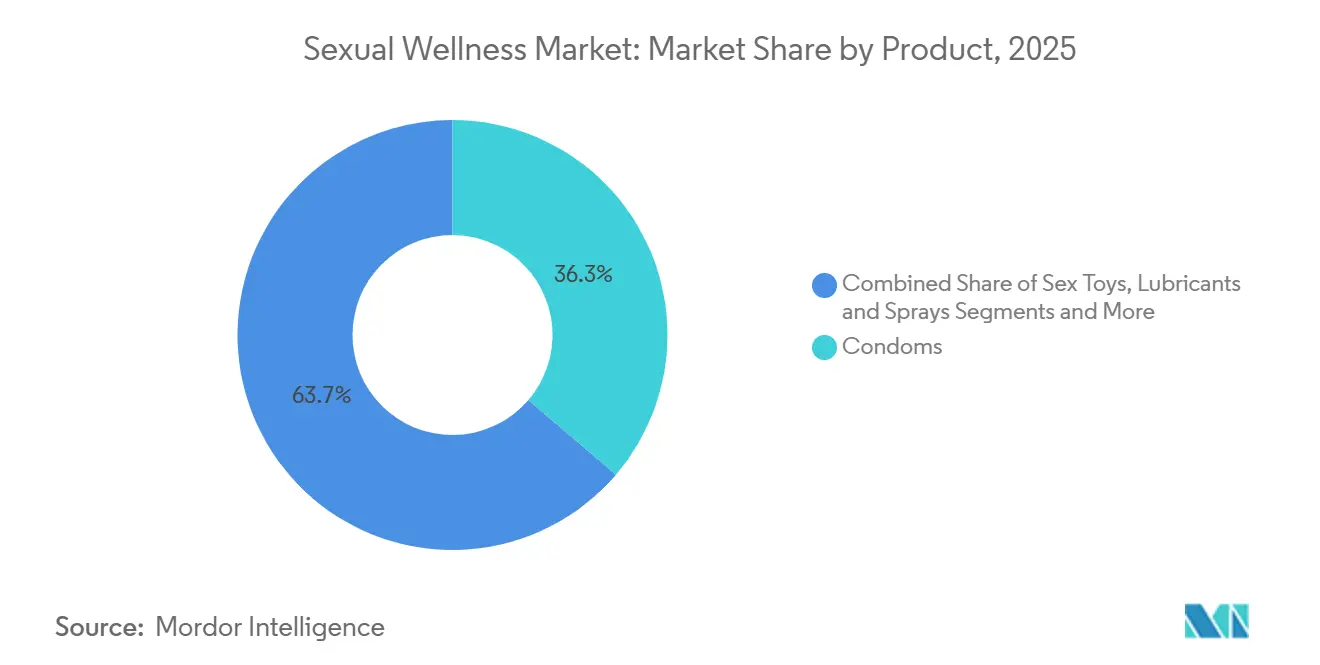

- By product category, condoms held 36.25% of the sexual wellness market share in 2025, whereas connected sex toys are advancing at an 11.66% CAGR through 2031.

- By material, latex and natural rubber commanded 54.63% of the sexual wellness market size in 2025, while medical-grade silicone is growing at a 10.84% CAGR over the same horizon.

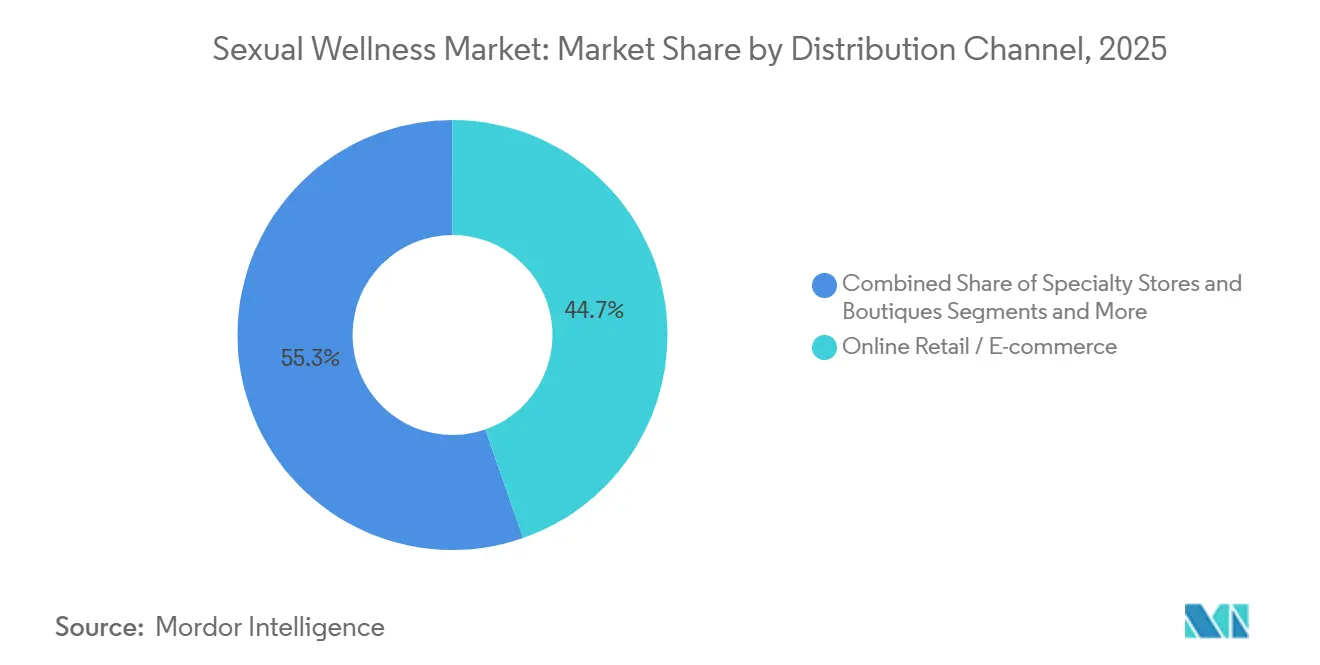

- By distribution channel, online retail captured 44.67% share of the sexual wellness market size in 2025 and leads future growth at an 11.93% CAGR.

- By end user, women accounted for 54.74% share of the sexual wellness market size in 2025; the LGBTQ+ cohort is the fastest climber at a 9.51% CAGR through 2031.

- By geography, the Asia-Pacific accounted for 36.25% of revenue share in 2025. Middle East & Africa is set to expand at a 9.13% CAGR, the quickest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sexual Wellness Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding E-commerce penetration | +1.8% | Global, stronger in APAC and MEA | Short term (≤ 2 years) |

| Rising acceptance of sexual wellness in emerging economies | +1.5% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Government HIV-prevention campaigns encouraging condom use | +1.2% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Premiumization of sex toys through tech integration | +1.4% | North America, Europe, urban APAC | Short term (≤ 2 years) |

| Growing role of femtech platforms bundling sexual-health subscriptions | +0.9% | North America & EU, expanding to urban APAC | Medium term (2-4 years) |

| Corporate well-being programs adding sexual-health benefits | +0.6% | North America, Western Europe, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding E-commerce Penetration

Digital storefronts already delivered 44.67% of sexual wellness market revenue in 2025, and recommendation engines convert first-time shoppers into subscribers at rising rates. Discreet checkout descriptors and plain packaging eliminate social friction, while direct-to-consumer routing compresses costs that brands redeploy into influencer partnerships. Rocket Health’s tele-consult plus delivery model in Uganda exemplifies platform integration that captures both product and service margin. Supply-chain data harvested from each order informs inventory planning and next-gen product design. As digital penetration deepens, the sexual wellness market gains predictability that attracts institutional capital.

Rising Acceptance of Sexual Wellness in Emerging Economies

India’s 2025 e-commerce reforms cleared regulatory bottlenecks, accelerating online contraceptive sales and sparking new product launches. Urban Chinese shoppers upgrade to premium lubricants and couples’ devices as rising incomes meet social-media-fueled aspiration, even while rural demand lags. Youthful populations in Indonesia, Egypt, and Nigeria embrace candid sexual-health conversations, pushing retailers to stock broader assortments. Still, cultural guardrails persist; marketers temper imagery and rely on neutral language to avoid backlash. This duality creates segmented opportunity inside the broader sexual wellness market.

Government HIV Prevention Campaigns Encouraging Condom Use

WHO’s 2025 guideline update embedded condoms within combination-prevention toolkits, sustaining baseline demand in public distribution channels.[1]World Health Organization, “WHO Guidelines on HIV Prevention and Condom Promotion,” World Health Organization, who.int UNAIDS reported a 12% uptick in protected acts among high-risk groups across targeted zones in 2024.[2]UNAIDS, “Condom Use Increases in High-Risk Populations,” UNAIDS, unaids.org Subsidized tenders pressure prices, so manufacturers bifurcate portfolios: basic variants for public bids and premium SKUs for retail. Campaign visibility normalizes condom usage in conservative cultures, indirectly expanding the sexual wellness market by destigmatizing adjacent categories like lubricants and toys. Public-private procurement frameworks now set volume floors that improve factory utilization rates.

Premiumization of Sex Toys Through Tech Integration

Connected devices post an 11.66% CAGR, the highest inside the sexual wellness market. Lovense’s integration with Apple Vision Pro in 2025 lets long-distance partners sync haptic feedback to shared VR scenes. Cybersecurity risk rises in parallel; FDA guidance from 2025 calls for encryption and secure firmware updates in intimate IoT products.[3]U.S. Food and Drug Administration Staff, “Guidance on Connected Intimate Devices,” U.S. Food and Drug Administration, fda.gov Brands that pre-emptively certify under ISO 27001 and publish penetration-test reports gain trust premiums. App ecosystems lock users into proprietary accessories, boosting lifetime value. As tech layers multiply, component sourcing and software maintenance become key differentiators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural and religious taboos limiting product visibility | −1.1% | MEA, South Asia, conservative pockets worldwide | Long term (≥ 4 years) |

| Counterfeit and unregulated products eroding consumer trust | −0.8% | Global, intense in APAC and MEA | Medium term (2-4 years) |

| Supply-chain chokepoints for medical-grade silicone | −0.6% | Global, premium lines most exposed | Short term (≤ 2 years) |

| Data-privacy concerns with smart/IoT sex devices | −0.5% | North America, EU (GDPR-sensitive) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural And Religious Taboos Limiting Product Visibility

Retailers in Gulf nations hide intimate products in non-prominent areas or behind pharmacy counters, suppressing spontaneous purchases. Digital advertising faces keyword blocks, forcing brands to rely on opt-in newsletters or health-education content that skirts explicit terminology. Consumer surveys reveal a 30-40% gap between purchase intent and actual sales in these zones. Framing condoms as disease-prevention tools rather than pleasure items slightly eases resistance, but that tactic constrains premium positioning. Long-term growth therefore depends on gradual social liberalization and health-based messaging that keeps the sexual wellness market advancing despite cultural headwinds.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural taboos and regulatory barriers | −1.4% | Asia-Pacific and Middle East | Long term (≥4 years) |

| Product-quality recalls and stricter compliance | −0.8% | Regulated markets worldwide | Short term (≤2 years) |

| Silicone and chip supply-chain disruptions | −0.6% | Global manufacturing hubs | Medium term (2-4 years) |

| Digital-ad censorship on major platforms | −0.9% | Global; online-first brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit And Unregulated Products Eroding Consumer Trust

Multi-country raids in 2024 seized fake Durex condoms with unsafe phthalate levels, igniting headlines that dented category credibility. Third-party sellers exploit e-commerce verification gaps to list sub-par items, and refunds rarely compensate for health risks. Blockchain authentication, as rolled out by Lelo in 2024, allows consumers to verify provenance via QR scan yet broad adoption is limited by rollout cost. Persistent counterfeiting suppresses replenishment rates and slows overall sexual wellness market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Connected Experiences Drive Category Upsell

Sex toys exhibit the fastest trajectory, growing at an 11.66% CAGR as immersive tech breaks distance barriers and reframes intimacy as a shared digital activity. Condoms still anchor demand with a 36.25% sexual wellness market share in 2025, underscoring their dual health-protection appeal. Lingerie blurs into athleisure, boosting velocity through mainstream fashion channels. Lubricants benefit from aging demographics and increased toy uptake that mandates compatible formulations. Fertility and performance aids command price premiums, signaling male willingness to invest when clinical claims exist. Over the forecast period, premiumization and connectivity shift the wallet mix toward higher-margin SKUs, enlarging the overall sexual wellness market.

Enhanced margin capture stems from health-cum-pleasure positioning. Dame Products’ 2025 pelvic-floor trainer passed FDA 510(k) review, qualifying for insurance reimbursement and illustrating how medical validation secures new funding pools. Regulatory complexity therefore protects incumbents with compliance know-how, while patent races around haptic mechanisms intensify. Subscription replenishment for toy cleaners and accessory attachments further extends customer lifetime value. As a result, toy makers influence platform standards that could shape future dynamics for the sexual wellness market size.

By Material: Body-Safe Formulations Gain Favor

Latex and natural rubber supplied 54.63% of condom value in 2025, reflecting cost advantages. Yet medical-grade silicone is expanding at a 10.84% CAGR as allergy awareness and a willingness to pay for safety converge. Polyurethane and polyisoprene address sensitivities while preserving thinness and strength. Hard materials such as stainless steel attract niche users seeking temperature play, whereas glass differentiates through aesthetics and hygiene benefits. Biodegradable alternatives remain in pilot because shelf-life trade-offs outweigh eco credentials. Strategic stockpiling and dual-supplier contracts mitigate silicone scarcity, securing production continuity and safeguarding sexual wellness market size growth.

ISO 10993 compliance imposes cytotoxicity, sensitization, and irritation testing that can extend launch cycles by up to nine months. Material innovators that pass these hurdles secure durable points of difference and patent defensibility. Karex Berhad’s 2025 biodegradable condom partnership exemplifies pre-emptive diversification to hedge raw-material risk. Over time, consumer education on body-safe ingredients strengthens the case for premium pricing, adding stability to the sexual wellness market.

By Distribution Channel: Online Platforms Widen the Funnel

E-commerce held 44.67% share of the sexual wellness market size in 2025 and races ahead at an 11.93% CAGR. Recommendation engines boost basket value, while discreet packaging addresses privacy concerns. Specialty boutiques thrive on experiential retail but absorb high fixed costs. Pharmacies lend medical legitimacy, yet limited shelf space curbs assortment breadth. Mass merchandisers push volume but expose shoppers to potential social discomfort, damping conversion. Policy changes at Amazon in 2025 nudged brands to diversify into Shopify sites and niche marketplaces, spreading traffic sources.

Direct-to-consumer brands harvest first-party data to tailor bundles and optimize lifecycle email flows. Subscription models flatten seasonality, improving cash forecasting. Lightweight, non-perishable SKUs such as condoms and sachet lubricants ship economically, whereas heavier toys justify express fees only at premium price points. Blockchain tags that guarantee authenticity enhance trust, reinforcing repeat buys and compounding the sexual wellness market’s digital momentum.

By End User: Inclusive Design Expands Reach

Women represented 54.74% of purchases in 2025, buoyed by products that destigmatize female pleasure and address physiological transitions such as menopause. The LGBTQ+ cohort is the fastest-growing at a 9.51% CAGR, reflecting design thinking that transcends heteronormative assumptions. Men remain a large but slower-moving segment focused on performance enhancement and prostate health. Younger consumers gravitate toward gender-neutral SKUs and transparent ingredient lists, aligning with broader identity inclusivity trends. Femtech ecosystems bundle sexual wellness items within broader reproductive-health plans, creating integrated offerings that raise average revenue per user and reinforce retention.

Insurance coverage remains patchy because most items are deemed elective. Brands that compile clinical evidence, as Dame Products did, strengthen the reimbursement argument, potentially enlarging the covered universe. Venture investment surpassing USD 1 billion in 2024-2025 validates the growth thesis and injects capital for product expansion that pushes the outer perimeter of the sexual wellness market.

Geography Analysis

Asia-Pacific commanded 36.14% of revenue in 2025 due to population scale and rising discretionary income. China’s urban hubs and India’s tier-one cities show appetite for premium toys and lubricants despite occasional regulatory whiplash on content standards. Southeast Asia mirrors this trajectory, with Indonesia and Thailand exhibiting digital-first purchasing habits that sidestep cultural friction.

The Middle East & Africa leads growth at 9.13% CAGR to 2031. Smartphone adoption lets consumers discreetly access online assortments, while UN and NGO HIV-prevention campaigns drive condom uptake. Yet product visibility in physical retail stays limited, so omnichannel hybrids that mix pharmacy pickup with mobile ordering gain traction. Localization of packaging and messaging around health, not pleasure, improves acceptability without inflating compliance cost.

North America and Europe represent mature yet innovation-driven territories. Premiumization through connected devices, FDA-cleared therapeutic claims, and subscription clubs sustains mid-single-digit expansion. Western Europe’s comprehensive sex-education programs normalize product discussion, supporting steady replenishment. Latin America grows unevenly: Brazil and Argentina propel demand via urban e-commerce, whereas logistical challenges in rural belts and currency volatility dampen momentum. Diverse regulatory landscapes mean go-to-market speed hinges on finding local partners who grasp tariff classifications and marketing codes.

Competitive Landscape

The top two condom franchises, Durex and Trojan, still enjoy extensive retail penetration. Meanwhile, hundreds of niche players address toys, lubricants, and enhancers, making the sexual wellness market moderately fragmented. Lovehoney leverages influencer marketing and a vertically integrated e-commerce stack to capture share from legacy retailers. Dame Products channels medical validation into higher-margin, insurance-eligible SKUs, differentiating on clinical utility.

Strategic investment tilts toward technology. Church & Dwight rolled out a connected Trojan line in 2025 to reclaim relevance among digitally native consumers. Reckitt Benckiser expanded Durex capacity in Thailand to shorten supply chains and hedge tariff risk. Patent filings proliferate around haptics, biometric feedback, and antimicrobial coatings, erecting IP moats that newcomers must navigate. Yet compliance hurdles—GDPR, ISO 10993, and country-specific labeling codes—add cost layers that favor incumbents with regulatory infrastructure.

Digital-first challengers offset scale disadvantages by owning customer data. Subscription mechanics raise lifetime value, funding aggressive social-media campaigns that feed algorithmic discovery. Blockchain authenticity programs and public security audits help these brands outflank counterfeit threats and reassure privacy-sensitive buyers. Over the forecast window, collaboration deals between heritage brands and tech specialists may accelerate to fuse manufacturing muscle with software prowess, shaping the next chapter of the sexual wellness market.

Sexual Wellness Industry Leaders

Reckitt Benckiser Group plc

Church & Dwight Co., Inc.

WOW Tech Group

Lelo AB

Wow Tech Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Sexual Wellness Group (SWG Brands, Inc.) launched a vertically integrated portfolio aimed at mainstreaming high-quality, inclusive products.

- September 2025: Manforce Condoms appointed AI avatar Myra Kapoor as brand ambassador, debuting a TV commercial built on synthetic influencers.

- July 2025: ONE Condoms commissioned a 1,001-respondent U.S. survey on orgasm frequency, spotlighting gaps in climax parity.

- July 2025: Harry Styles’s Pleasing label introduced the Pleasing Double-Sided Vibrator and an FDA-approved silicone lubricant, co-created with educator Zoe Ligon.

Global Sexual Wellness Market Report Scope

Sexual wellness refers to a state of physical, emotional, mental, and social well-being related to sexuality, beyond merely the absence of disease or dysfunction. Sexual wellness products, including contraceptives, lubricants, and sexual aids, aim to enhance sexual health, pleasure, intimacy, and overall well-being while addressing risks like STIs and unintended pregnancies.

The Sexual Wellness Market Report is segmented by Product, Material, Distribution, End User, and Geography. By Product, the market is segmented into Condoms, Sex Toys, Lubricants and Sprays, and Fertility and Performance Enhancers. By Material, the market is segmented into Latex, Polyurethane, Silicone, Hard Materials, and Biodegradable materials. By Distribution, the market is segmented into Online, Specialty Stores, Pharmacies, and Supermarkets. By End User, the market is segmented into Women, Men, and LGBTQ+. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Condoms |

| Sex Toys |

| Lubricants & Sprays |

| Fertility & Performance Enhancers |

| Latex & Natural Rubber |

| Polyurethane & Polyisoprene |

| Medical-grade Silicone |

| Hard Materials |

| Others/Biodegradable |

| Online Retail/E-commerce |

| Specialty Stores & Boutiques |

| Pharmacies & Drugstores |

| Mass Merchandisers & Supermarkets |

| Women |

| Men |

| LGBTQ+ |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Condoms | |

| Sex Toys | ||

| Lubricants & Sprays | ||

| Fertility & Performance Enhancers | ||

| By Material | Latex & Natural Rubber | |

| Polyurethane & Polyisoprene | ||

| Medical-grade Silicone | ||

| Hard Materials | ||

| Others/Biodegradable | ||

| By Distribution Channel | Online Retail/E-commerce | |

| Specialty Stores & Boutiques | ||

| Pharmacies & Drugstores | ||

| Mass Merchandisers & Supermarkets | ||

| By End User | Women | |

| Men | ||

| LGBTQ+ | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the sexual wellness market be by 2031?

It is projected to reach USD 52.67 billion by 2031, expanding at a 7.61% CAGR from 2026.

Which product category is growing fastest?

Connected sex toys lead with an 11.66% CAGR thanks to app and VR integration.

Why is the Middle East & Africa the fastest-growing region?

Smartphone-driven e-commerce and a young demographic base push the region to a 9.13% CAGR despite retail visibility limits.

What drives online channels to dominate sales?

Discreet packaging, AI-based recommendations, and subscription models lifted online share to 44.67% in 2025 and keep it rising.

How are counterfeit goods affecting category growth?

Substandard and fake products erode consumer trust and subtract 0.8 percentage points from forecast CAGR until stricter authentication systems spread.

Which materials are gaining popularity beyond latex?

Medical-grade silicone grows at a 10.84% CAGR due to allergy concerns and body-safe preferences.

Page last updated on: