Prostate Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 36.01 Billion |

| Market Size (2031) | USD 55.8 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

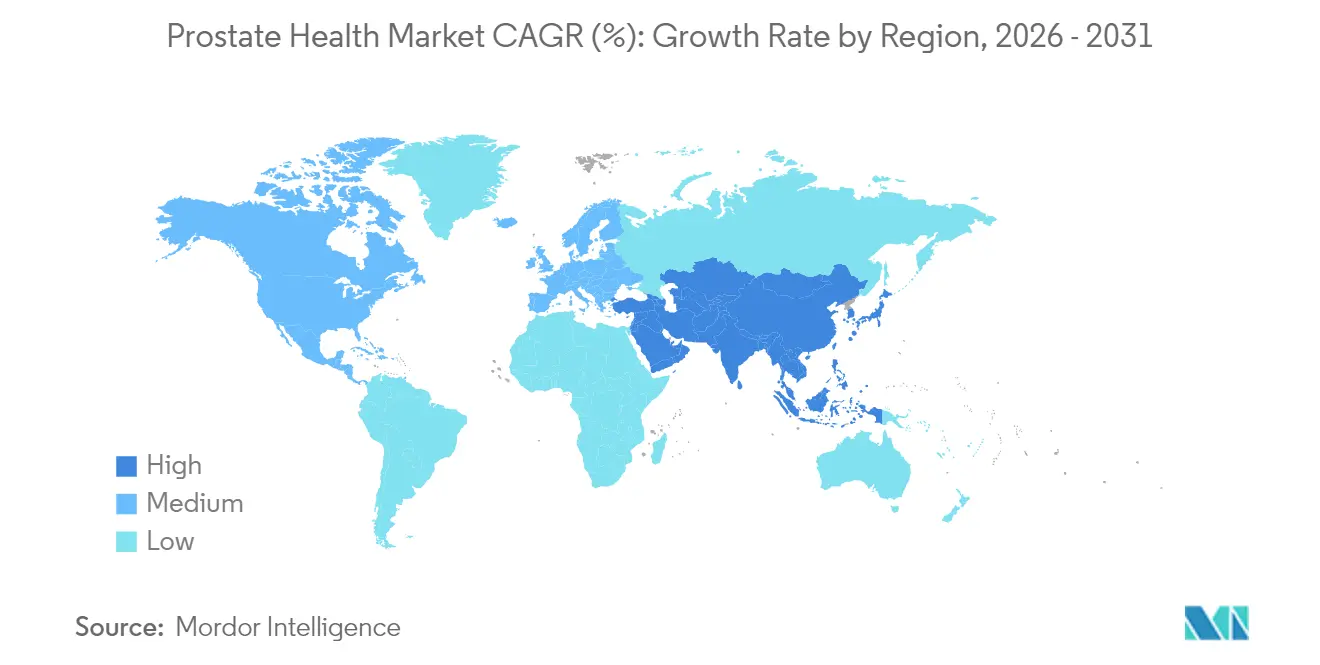

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Prostate Health Market Analysis by Mordor Intelligence

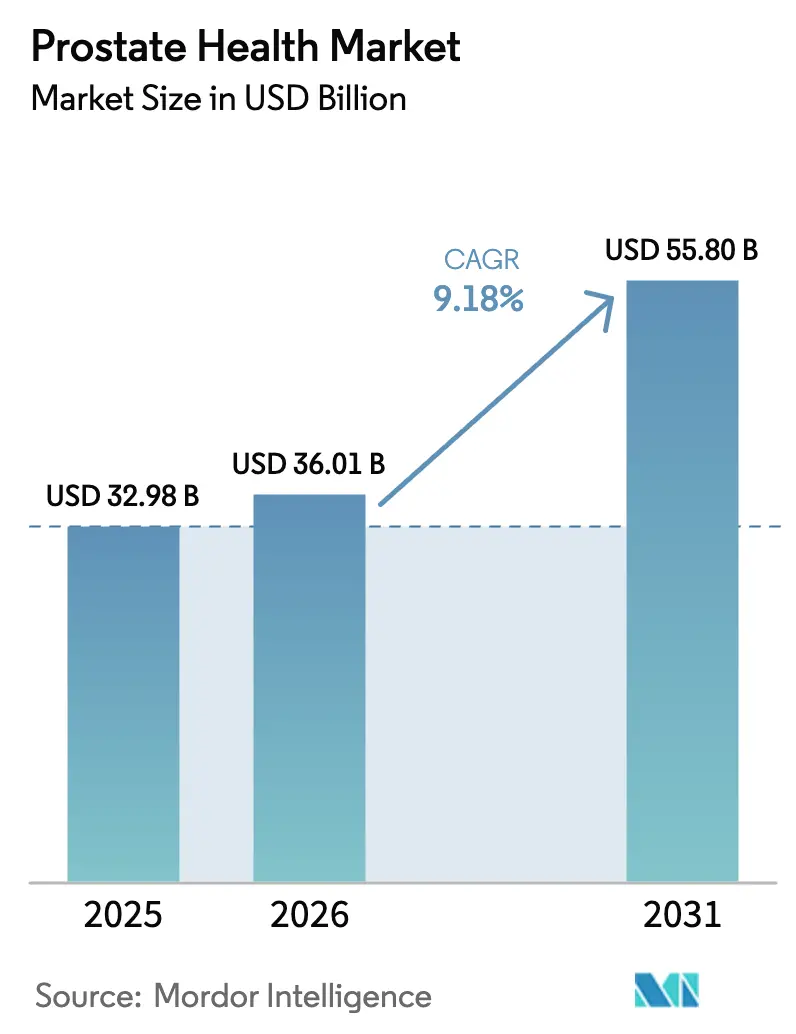

The Prostate Health Market size in 2026 is estimated at USD 36.01 billion, growing from 2025 value of USD 32.98 billion with 2031 projections showing USD 55.8 billion, growing at 9.18% CAGR over 2026-2031.

Growth derives from a swelling cohort of aging males, rapid diffusion of precision diagnostics, and digital-first delivery models that are reshaping patient engagement. Demand accelerates as benign prostatic hyperplasia (BPH) prevalence climbs with age, while falling multigene-test prices encourage earlier, risk-stratified interventions. Direct-to-consumer tele-urology platforms that combine online consultation, laboratory panels, and medicine fulfillment compress waiting times and extend outreach. Meanwhile, clearer U.S. reimbursement pathways for PSMA-PET imaging and radiopharmaceuticals drive pipeline investment, exemplified by Bristol Myers Squibb’s USD 1.3 billion buy-in to RayzeBio’s radioligand assets.

Key Report Takeaways

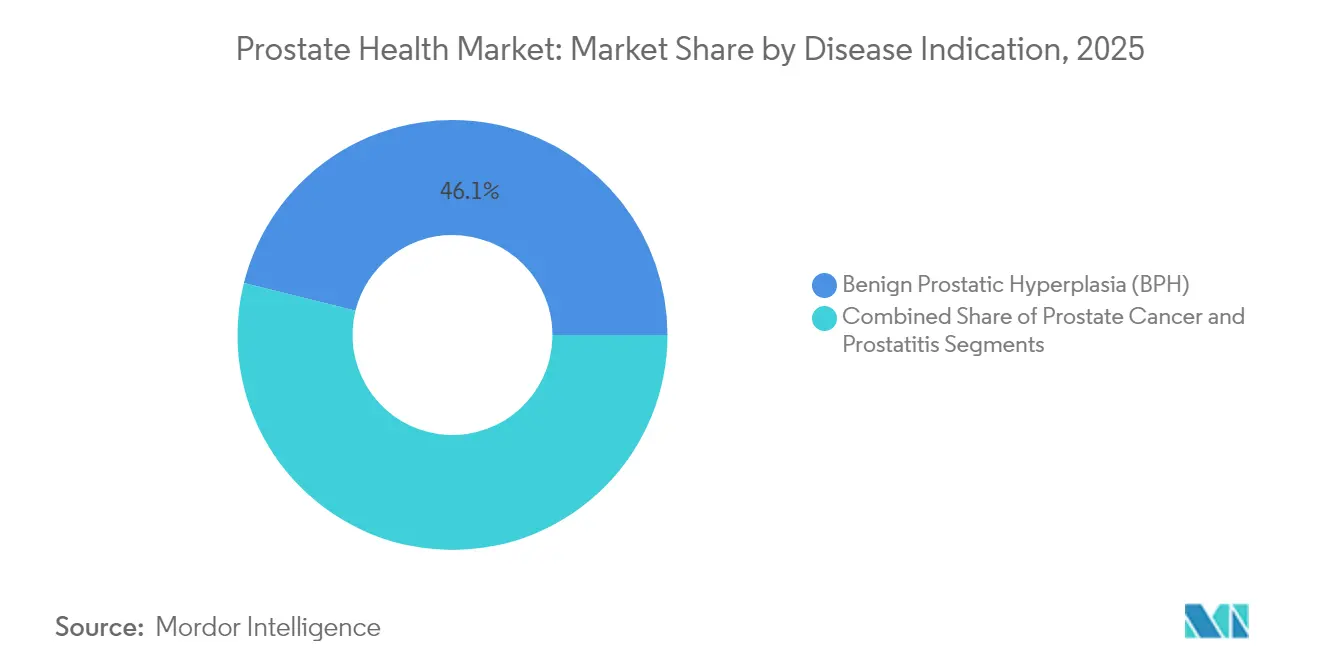

- • By disease indication, BPH commanded 46.12% of the prostate health market share in 2025; prostate cancer is projected to grow at a 9.98% CAGR through 2031.

- • By product type, prescription drugs accounted for 56.48% of the prostate health market size in 2025, while genomic diagnostics are forecast to expand at a 10.34% CAGR to 2031.

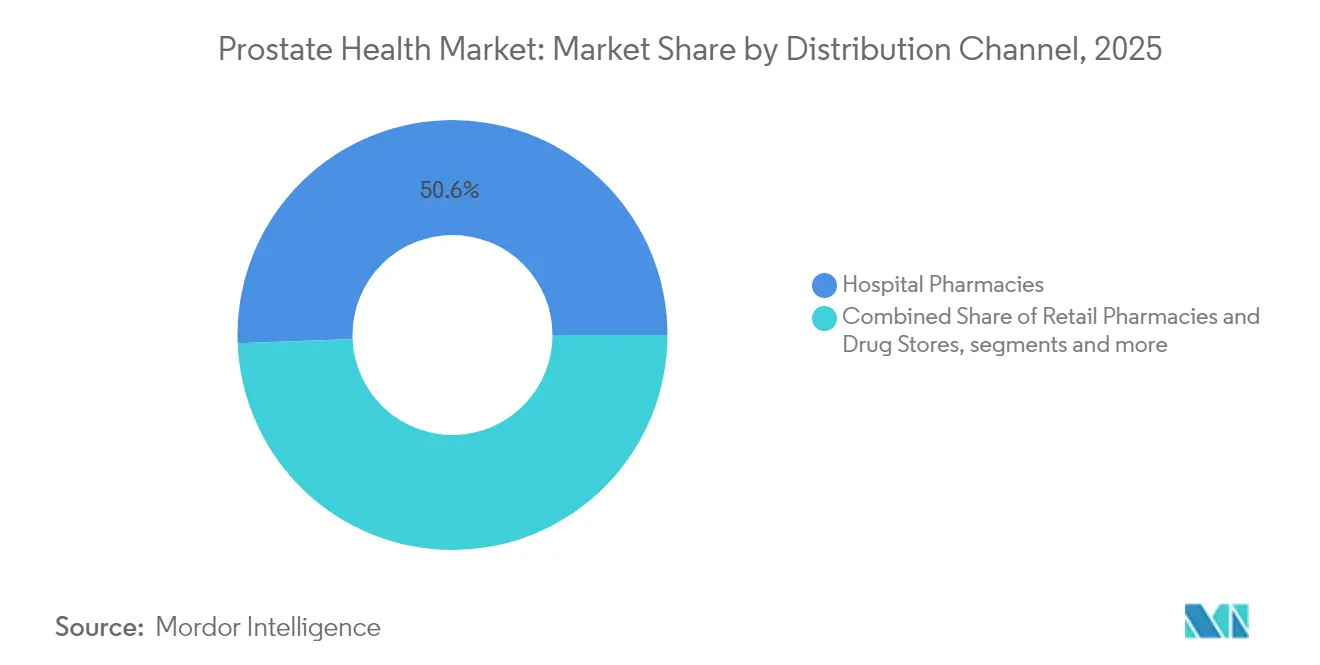

- • By distribution channel, hospital pharmacies held 50.62% of revenue in 2025; online and telemedicine platforms are advancing at an 10.86% CAGR through 2031.

- • By geography, North America secured 38.05% of the prostate health market share in 2025, whereas Asia-Pacific is set for the fastest growth at an 11.18% CAGR between 2026 and 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prostate Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-male Population Base Swells Addressable Market | +2.8% | Global, particularly North America & Europe | Long term (≥ 4 years) |

| Growing Use of PSA and mpMRI for Early Detection | +2.1% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Shift Toward Once-daily Combo Drugs for BPH Symptom Relief | +1.4% | Global, led by developed markets | Short term (≤ 2 years) |

| Radically Lower Cost of Genomic Testing Enables Risk Stratification | +1.8% | North America & EU, selective APAC adoption | Medium term (2-4 years) |

| DTC Tele-urology Platforms Bundling Meds & Labs | +1.2% | North America lead, expanding globally | Short term (≤ 2 years) |

| Corporate Men's-health Benefits Boosting Screening Uptake | +0.9% | North America & select European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-Male Population Base Swells Addressable Market

Men 65 years and older are the fastest-growing demographic worldwide and are projected to double in developed economies by 2050. BPH prevalence rises from 50% at age 60[1]Bryn M Launer, "The rising worldwide impact of benign prostatic hyperplasia," BJU International, pmc.ncbi.nlm.nih.gov to nearly 90% among men in their 90s, while prostate cancer peaks at 102.8 cases per 100,000 in the 65–74 cohort. This demographic wave heightens absolute patient numbers and per-capita utilization, ensuring structural momentum for the prostate health market.

Growing Use of PSA and mpMRI for Early Detection

MRI-first pathways enable 96% of men with negative scans to avoid biopsy without compromising detection of high-grade cancer[2]Charlie A. Hamm, "Oncological Safety of MRI-Informed Biopsy Decision-Making in Men With Suspected Prostate Cancer," JAMA Oncology, jamanetwork.com over 3 years. Combined PSA-mpMRI screening reduces unnecessary biopsies by up to 50% and is being rapidly integrated into European guideline practice. Such precision approaches strengthen patient confidence and free system resources, boosting adoption across the prostate health market.

Radically Lower Cost of Genomic Testing Enables Risk Stratification

Multigene panel costs have plunged to sub-USD 500, making population-level genetic screening feasible. MyProstateScore 2.0 eliminates 41% of unnecessary biopsies versus 11% under PSA-only criteria, underscoring the clinical and economic upside. Wider payer acceptance should accelerate penetration, adding depth to the prostate health industry’s diagnostics segment.

DTC Tele-Urology Platforms Bundling Meds & Labs

Over 90% of online sexual-health visits are deemed low-risk and safely resolved via teleconsultation. Subscription services combine hormone profiles, PSA kits, and e-prescribing, inducing sticky, recurring revenue and drawing new users into the prostate health market ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event Concerns Around Long-term 5-ARI Usage | -1.3% | Global, particularly developed markets | Long term (≥ 4 years) |

| Low Reimbursement for Precision Diagnostics Outside US/EU | -2.1% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Shortage of Fellowship-trained Uro-radiologists Limits mpMRI Utility | -1.7% | Global, acute in emerging markets | Medium term (2-4 years) |

| Social Stigma in Key Asian Markets Dampens Early Care-seeking | -1.9% | Asia-Pacific, particularly East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Concerns Around Long-Term 5-ARI Usage

Reports linking 5-ARI therapy to erectile dysfunction and mood disorders temper prescription growth. Physicians increasingly shift toward alpha-blocker combinations or device-based therapies such as UroLift, reallocating share within the prostate health market.

Low Reimbursement for Precision Diagnostics Outside US/EU

While Medicare reimburses PSMA-PET scans and gene panels, most emerging markets still rely on PSA alone, stalling adoption of advanced diagnostics. The gap limits global footprint for suppliers yet opens opportunity for lower-cost assays tailored to constrained settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Indication: BPH Dominates While Cancer Segment Accelerates

BPH captured 46.12% of the prostate health market size in 2025, propelled by lifelong symptom management and broad therapeutic choice. Pharmaceutical and device makers benefit from steady repeat sales and procedure fees. Conversely, prostate cancer posts the fastest trajectory at a 9.98% CAGR on rising genomic-screen uptake and PSMA-targeted radioligand approvals.

Prostatitis remains small but underserved. Emerging microbiota-modifying strategies and localized drug-delivery devices could expand treatment options for patients with chronic pelvic pain and create opportunities for innovators in the prostate health market.

By Product Type: Prescription Drugs Lead as Genomics Disrupts

Prescription therapies retained 56.48% of the prostate health market share in 2025, primarily due to continued reliance on alpha-blockers, next-generation androgen-receptor inhibitors, and radioligands such as Pluvicto. Darolutamide’s multiple label extensions underline the advantage of robust clinical pipelines. Label extensions for Nubeqa and Gemtesa showcase a steady flow of clinical innovation that underpins segment resilience.

Genomic diagnostics are expected to exhibit the highest growth at a 10.34% CAGR, as payers weigh the real-world savings from avoided biopsies. Minimally invasive devices, such as UroLift 2 and Rezūm, add high single-digit growth through increased procedure volume and geographic reach.

By Distribution Channel: Hospital Dominance Challenged by Digital Platforms

Hospital pharmacies generated 50.62% of revenue in 2025, as complex radiopharmaceuticals require specialist preparation. Tumor boards and same-site imaging also reinforce the channel’s centrality.

Online portals and telemedicine now form the fastest-growing route at an 10.86% CAGR, providing privacy-conscious consumers with convenient refills, home testing, and rapid escalation pathways. Retail chains maintain relevance through over-the-counter products but co-market with digital health apps to secure incremental prescriptions.

Geography Analysis

North America held a 38.05% share of the prostate health market in 2025 and is expected to sustain mid-single-digit growth through 2031. Medicare coverage for PSMA-PET imaging, gene panels, and radioligands supports premium-priced interventions while corporate wellness plans foster routine screening. United States direct-to-consumer models normalize online care seeking, boosting adherence and early detection. Canada’s single-payer system emphasizes cost-effectiveness; its approval of oral relugolix demonstrates a willingness to fund drugs that lower hospitalization and injection visits.

The Asia-Pacific region is the fastest-growing region, with a 11.18% CAGR for 2026–2031. Japan and South Korea lead in the adoption of mpMRI and guideline-based care, whereas China and India are experiencing high-volume growth but face gaps in reimbursement and awareness of screening. Governments roll out public-private campaigns, pairing hospital-based “check-up days” with tele-follow-ups to bridge access issues, drawing in multinationals and local startups to the prostate health market.

Europe follows an evidence-centric path that tempers the speed of uptake but ensures durability. Health-technology-assessment agencies tie reimbursement to real-world cost-utility, favoring scans and therapies with demonstrated survival or quality-of-life benefit. Germany and France increasingly rely on multiparametric MRI for biopsy triage, while the United Kingdom’s National Health Service pilots risk-adapted screening.

The Middle East and Africa remain nascent yet promising. Rising life expectancy, private-sector hospital build-outs, and government screening drives create incremental demand. Constraints include low urologist density and fragmented payer systems, but PSMA-PET installations in Gulf Cooperation Council states illustrate gradual capability upgrades.

Competitive Landscape

The prostate health market marries established pharmaceutical incumbents, device innovators, and digital disruptors. Bayer, Pfizer, and Merck are harnessing the multi-indication development of androgen-receptor inhibitors; darolutamide’s third U.S. approval showcases this strategy. Bristol Myers Squibb’s acquisition of RayzeBio grants immediate entry into late-stage radiopharmaceuticals and underlines investor appetite for targeted modalities

Device firms such as Boston Scientific and Teleflex expand portfolios with minimally invasive BPH tools that prioritize sexual-function preservation. The UroLift 2 platform, now cleared for all prostate anatomies, and Rezūm steam therapy deliver rapid symptom relief and shorter recovery times, enabling outpatient procedural expansion.

Digital-first platforms tackle cultural reluctance toward clinic visits. Subscription models provide on-demand testing, teleconsultation, and doorstep dispensing, capturing users who might otherwise remain untreated. Incumbents integrate virtual touchpoints or partner with e-pharmacies to avoid leakage. Competition increasingly hinges on real-world outcome evidence and payer alignment, with market access teams weighing cost-per-QALY metrics.

Prostate Health Industry Leaders

-

Teleflex

-

Novartis AG

-

Elekta

-

Siemens Healthcare GmbH

-

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA approved Telix’s Gozellix, an extended-shelf-life PSMA-PET tracer offering wider geographic distribution

- March 2025: FDA broadened Pluvicto use into earlier metastatic castration-resistant prostate cancer lines after PSMAfore trial gains

- March 2025: Mallinckrodt and Endo agreed to merge, forming a scaled pharmaceuticals entity with an enlarged prostate-care footprint

- January 2025: Sanofi’s Opella unit gained FDA clearance for an actual-use trial aimed at converting Cialis to over-the-counter status

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the prostate health market as the aggregate global revenue derived from prescription therapeutics, over-the-counter supplements, in-vitro diagnostics (for example, PSA and genomic assays), and minimally invasive BPH devices that prevent, detect, or treat benign prostatic hyperplasia, prostatitis, and prostate cancer across hospitals, retail pharmacies, and emerging e-commerce channels. According to Mordor Intelligence, the measurable universe excludes charitable services, behavioral counseling, and general urology consumables that do not directly address prostate pathology.

Scope exclusion: screening campaigns funded wholly by governments without a product or service transaction are outside the market boundary.

Segmentation Overview

-

By Disease Indication (Value)

- Benign Prostatic Hyperplasia (BPH)

- Prostate Cancer

- Prostatitis

-

By Product Type (Value)

- Prescription Drugs

- Over-the-Counter Supplements

- Diagnostics (PSA kits, mpMRI, genomic assays)

- Minimally-Invasive Devices (laser, RF, prostatic urethral lift)

-

By Distribution Channel (Value)

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Platforms & Tele-urology

-

By Geography (Value)

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with urologists, hospital pharmacy buyers, diagnostics distributors, and health-insurance actuaries across North America, Europe, Asia-Pacific, and the Gulf region helped us verify treatment patterns, average selling prices, and pipeline adoption timelines that secondary data alone cannot reveal.

Desk Research

We began with population-weighted disease incidence data published by organizations such as WHO's GLOBOCAN, the Centers for Disease Control and Prevention, and Eurostat, which provide a dependable starting point for estimating patient pools. These statistics were paired with reimbursement schedules and procedure volumes released by national health ministries, the American Urological Association, and the European Association of Urology to size paid service uptake. Our analysts next captured price and revenue markers from public company 10-Ks, U.S. FDA drug labels, and device import logs available through UN Comtrade. D&B Hoovers and Dow Jones Factiva assisted us in validating corporate splits for leading suppliers. The sources cited here are illustrative; many additional public and subscription references supported data collection and cross-checks.

Market-Sizing & Forecasting

We reconstructed global demand top-down by multiplying country-level treated patient cohorts (derived from prevalence studies and therapy penetration ratios) with validated average spending per patient. Selective bottom-up roll-ups, such as sampled PSA kit shipments and leading drug revenues, served as guardrails and revealed under-reported pockets in Japan and Brazil. Key variables that feed our model include: 1) age-stratified male population growth, 2) BPH and prostate cancer incidence trends, 3) guideline-driven therapy mix shifts toward next-generation androgen-receptor inhibitors, 4) median ASP movement after generic entry, 5) procedure capacity expansion in ambulatory surgery centers, and 6) reimbursement inclusion dates for MRI-fusion biopsies. Forecasts use a multivariate regression blended with scenario analysis, allowing us to stress-test outcomes under pricing reform or accelerated diagnostic adoption. Data gaps in supplier roll-ups are bridged through region-specific ASP proxies discussed with interviewees.

Data Validation & Update Cycle

Before sign-off, Mordor analysts triangulate model outputs against historical spend trends, currency fluctuations, and abnormal unit swings flagged by automated variance scripts. A senior reviewer signs off once anomalies are resolved. Reports refresh annually, with interim updates triggered by major approvals, reimbursement shifts, or material M&A.

Why Our Prostate Health Baseline Earns Decision Makers' Trust

Published estimates often diverge because firms slice the market differently, convert currencies on separate calendars, or refresh their models at uneven intervals.

Key gap drivers we observe include some publishers limiting scope to pharmaceuticals, others omitting diagnostics and OTC supplements, and several applying straight-line growth to outdated incidence curves, whereas we rebuild patient pools each cycle and adjust for guideline changes and ASP erosion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.93 B (2025) | Mordor Intelligence | - |

| USD 41.34 B (2024) | Regional Consultancy A | Drugs and devices only; excludes supplements and diagnostics; relies on supplier revenue extrapolation |

| USD 36.50 B (2024) | Global Consultancy B | Combines BPH and cancer drugs yet omits device procedures; uses single-year currency averages, unpublished exchange rates |

The comparison shows that Mordor's consistently refreshed, scope-complete approach delivers a balanced, transparent baseline that executives can trace back to clear variables and repeatable steps, giving them greater confidence for strategy and investment decisions.

Key Questions Answered in the Report

What is the current Global Prostate Health Market size?

The prostate health market size reached USD 36.01 billion in 2026 and is projected to climb to USD 55.8 billion by 2031.

Which condition generates the largest revenue within the market?

BPH leads, capturing 46.12% of the prostate health market share in 2025 due to its high prevalence among aging men.

Which region will witness the fastest growth?

Asia-Pacific is forecast to advance at an 11.18% CAGR between 2026 and 2031, driven by demographic aging, rising incomes, and expanding screening programs.

Why are genomic diagnostics gaining traction?

Multigene panel costs have fallen below USD 500, and tests such as MyProstateScore 2.0 eliminate 41% of unnecessary biopsies, improving care efficiency.

Page last updated on: