SexTech Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

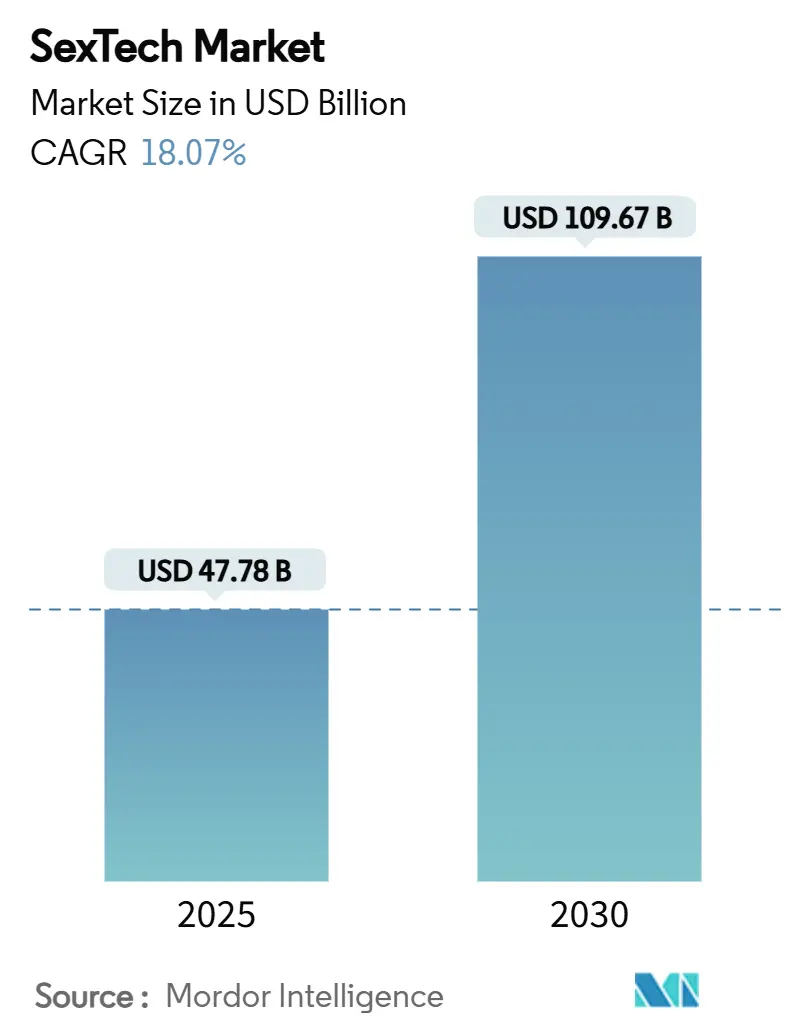

| Market Size (2025) | USD 47.78 Billion |

| Market Size (2030) | USD 109.67 Billion |

| Growth Rate (2025 - 2030) | 18.07% CAGR |

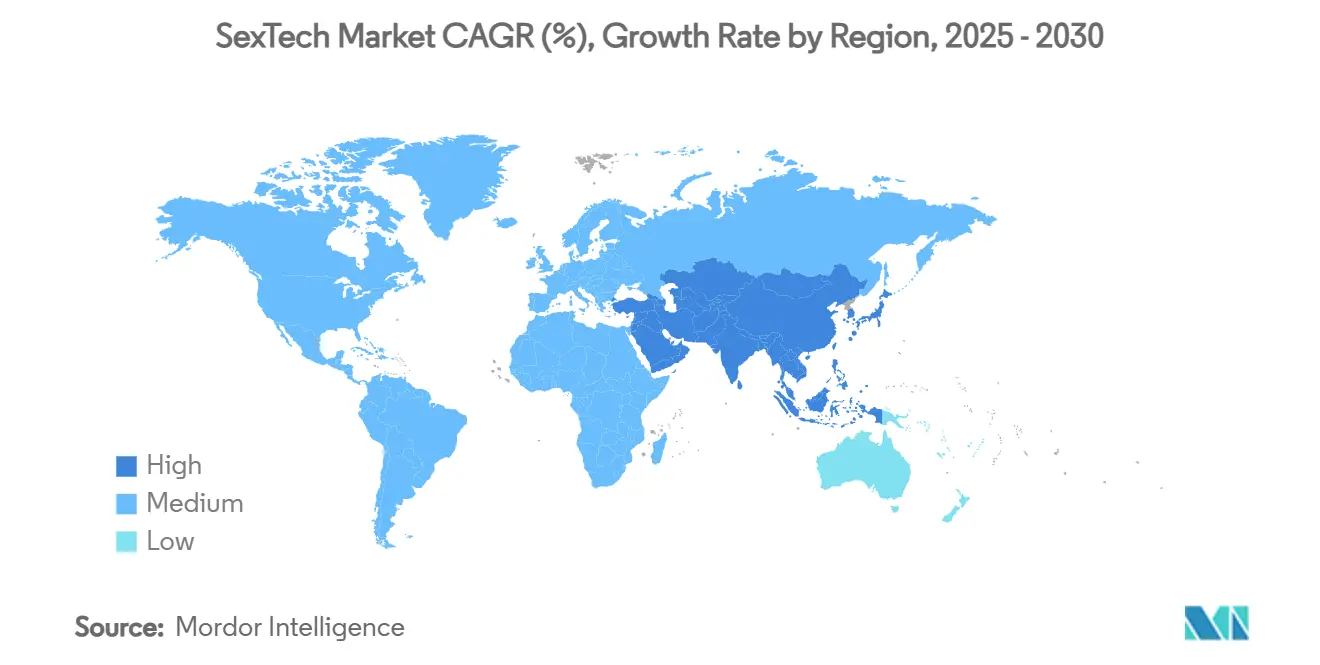

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

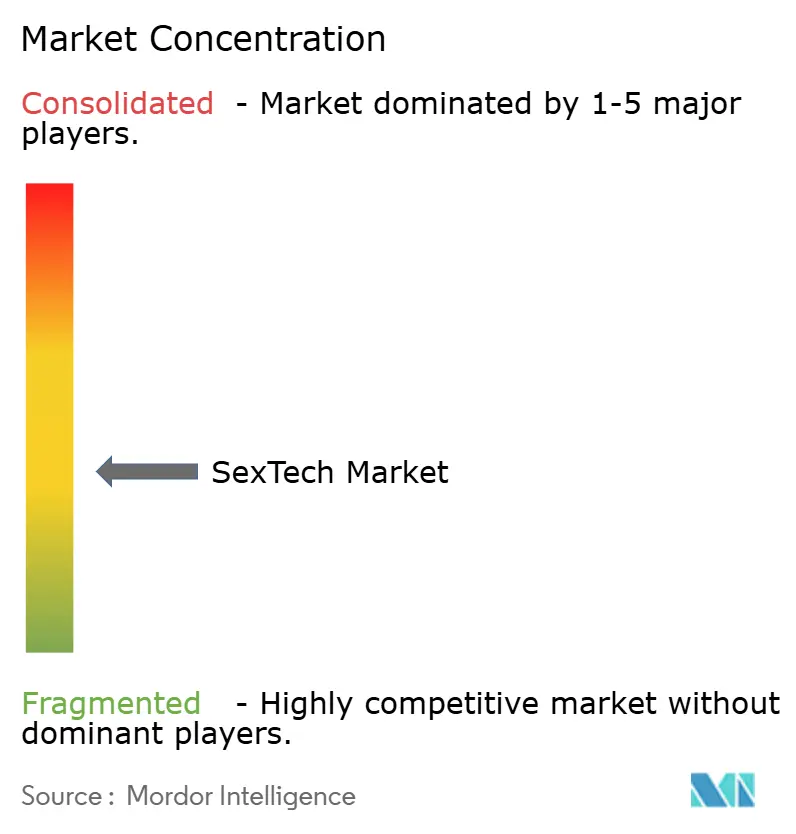

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SexTech Market Analysis by Mordor Intelligence

The sextech market size is valued at USD 47.78 billion in 2025 and is forecast to climb to USD 109.67 billion by 2030, advancing at an 18.07% CAGR; this growth underscores the rapid conversion of sexual-wellness technology from a niche to a mainstream wellness pillar. A surge in AI-enabled personalization, stable consumer acceptance among millennials and Generation Z, and the validation of connected wellness products by mass retailers are reinforcing demand. Geographic momentum is mixed: North America still contributes the largest revenue share while Asia-Pacific delivers the fastest absolute gains, signaling that cultural liberalization can expand faster than legacy regulatory reform. Connectivity and data science are now core value propositions, turning basic stimulators into multifunctional devices that double as wellness trackers. Competitive intensity remains high because low entry barriers coexist with expensive regulatory and payments compliance; firms that master both technology integration and governance progressively capture premium consumer segments.

Key Report Takeaways

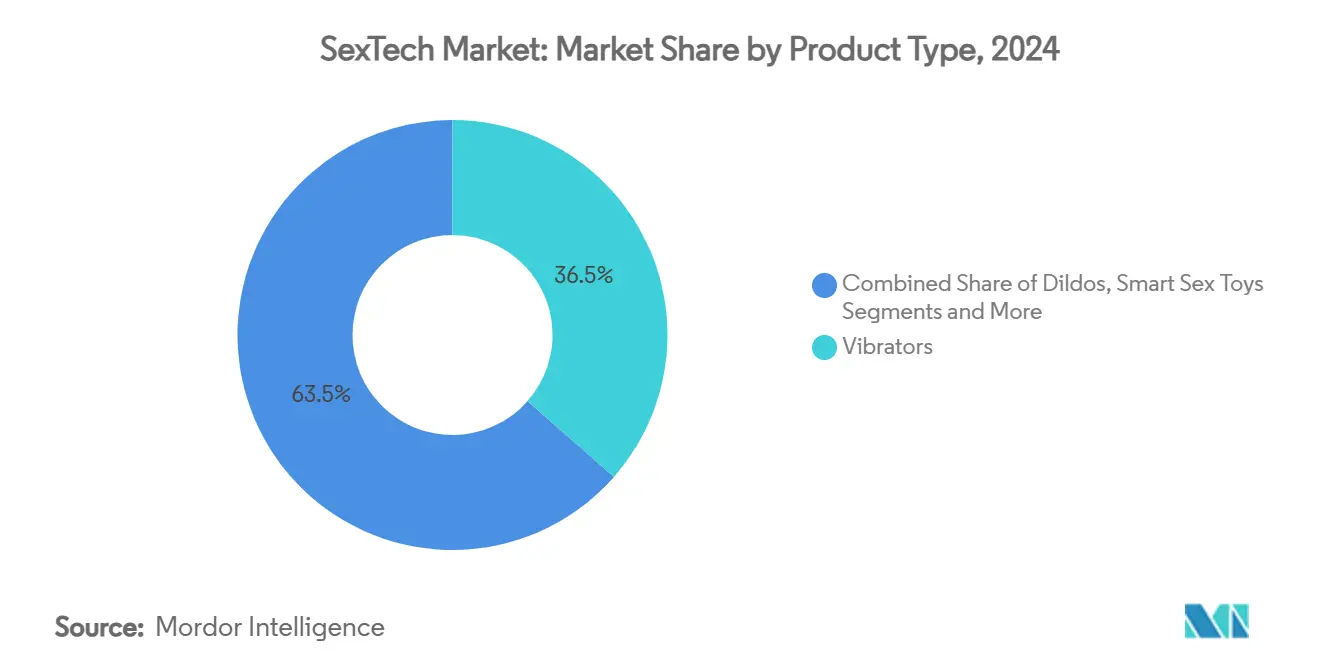

- By product type, vibrators led with 36.48% of sextech market share in 2024, while smart sex toys are projected to record a 22.34% CAGR through 2030.

- By technology, Bluetooth-enabled devices accounted for 44.64% of the sextech market size in 2024; artificial-intelligence-based devices are poised to expand at a 12.78% CAGR during 2025–2030.

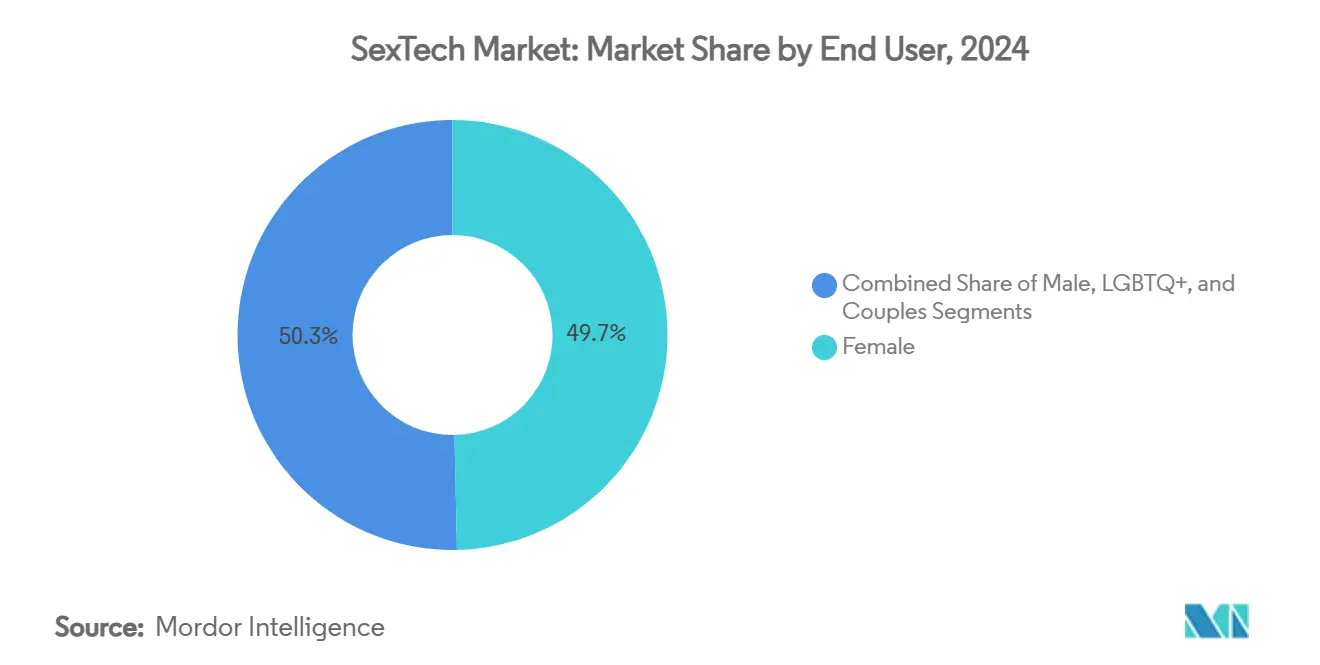

- By end-user, female consumers held 49.67% of the sextech market size in 2024, and the LGBTQ+ segment is forecast to grow at 20.53% CAGR to 2030.

- By distribution channel, online retail controlled 59.86% of the sextech market share in 2024, the same channel is expected to rise at 22.76% CAGR through 2030.

- By geography, North America retained 33.73% of global revenue in 2024, and Asia-Pacific is anticipated to post a 20.43% CAGR until 2030.

Global SexTech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Social Acceptance & Destigmatization | + 3.2% | Global, with early gains in North America & Europe | Medium term (2-4 years) |

| Expansion Of E-Commerce & D2C Platforms | + 2.8% | Global, particularly strong in Asia-Pacific | Short term (≤ 2 years) |

| Advancements In Haptic & AI-Enabled Devices | + 4.1% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Remote Sexual-Health Tele-Therapy Integration | + 2.3% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Employer-Funded Sexual-Wellness Benefits | + 1.9% | North America & EU, limited APAC adoption | Long term (≥ 4 years) |

| Rising Female Purchasing Power & Self-Care Spending | + 2.7% | Global, strongest in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Social Acceptance & Destigmatization

Mainstream beauty and pharmacy chains now stock sexual-wellness devices, granting shoppers the same impartial shelf experience they expect from skincare items. Visibility inside trusted venues is eroding stigma among younger adults, who already classify sexual health as part of holistic self-care. Active discussion on social platforms and in digital healthcare forums further normalizes purchase decisions, forming a reciprocal loop with retail presence. China’s allowance of boutique sex-toy outlets in high-footfall malls offers tangible evidence that conservative norms can soften rapidly when economic potential becomes visible. Improved academic evidence around AI-guided sex education additionally bolsters public confidence, giving schools and therapists validated content for conversations that were formerly taboo.[1]Nicola Döring et al., “The Impact of Artificial Intelligence on Human Sexuality,” Current Sexual Health Reports, link.springer.com

Expansion of E-Commerce & D2C Platforms

Private browsing, discreet packaging, and custom learning modules position online stores as the preferred channel for modern consumers, explaining why the channel already delivers 59.86% of 2024 revenue. Restrictive product policies on large marketplaces encourage brands to invest in direct-to-consumer storefronts, adding subscription replenishment and AI-based sizing recommender engines that deepen loyalty. In Asia-Pacific, where youthful demographics intersect sustained mobile-commerce adoption, pure-play e-commerce firms generate viral adoption through influencer marketing. Ethical-data frameworks proposed by founders and academics promise to reduce privacy anxieties and set voluntary standards ahead of regulation.[2]Jenny Kennedy, “Sex Tech Entrepreneurs: Governing Intimate Data in Start-Up Culture,” New Media & Society, journals.sagepub.com Supply-chain integration with last-mile providers in urban centers drastically cuts delivery times, reinforcing repeat purchases among heavy users of connected devices.

Advancements in Haptic & AI-Enabled Devices

Machine learning algorithms in flagship products customise vibration profiles and intensity curves in real time, turning one device into many experiences for multiple body anatomies. University labs now fabricate electro-hydraulic actuators that deliver broader frequency spectrums than legacy motors, paving the way for truly multisensory stimulation.[3]Max Planck Institute, “Electrohydraulic wearable devices create unprecedented haptic sensations,” ScienceDaily, sciencedaily.com Early adoption by long-distance couples validates willingness to pay premiums for telepresence intimacy. Mixed-reality headsets such as Apple Vision Pro synchronise motion and feedback, bridging haptic devices and immersive worlds. Over time, onboard AI may integrate biometric indicators such as heart-rate variability, presaging wellness dashboards analogous to sleep-tracking.

Remote Sexual-Health Tele-Therapy Integration

Retailers and medical platforms are converging: one UK-based merchant has embedded NHS-funded contraception services directly in its checkout flow, reclassifying the site as both marketplace and care provider. Remote therapists prescribe connected devices that supply usage telemetry, creating outcome-oriented reimbursement stories for insurers. AI chatbots trained on validated cognitive-behavioural protocols can triage common dysfunction queries, freeing clinical time for complex cases. Pandemic-era acceptance of telemedicine has remained stable, giving start-ups aligned with sexual medicine credible off-ramps into regulated device status. Interoperability with patient-record systems is improving, allowing therapists to cross-reference device data with hormonal or cardiovascular information, reinforcing claims of therapeutic benefit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory & Legal Uncertainty | -2.1% | Global, particularly restrictive in MEA & parts of APAC | Long term (≥ 4 years) |

| Data-Privacy & Cybersecurity Risks | -1.8% | Global, with stricter enforcement in EU & North America | Medium term (2-4 years) |

| Payment-Processing Discrimination | -2.4% | Global, most severe in North America & EU | Short term (≤ 2 years) |

| Sustainable Body-Safe Material Shortages | -1.3% | Global, with supply chain impacts in APAC manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory & Legal Uncertainty

Fragmented rules create patchwork compliance obligations for both hardware and digital services; for example, connected devices must satisfy radio-frequency, consumer-safety, and intimate-data statutes that differ among trade blocs. Financial regulators have chastised banks for “de-risking” sex-related accounts, yet enforcement clarity remains inconsistent. Trade-show organisers continue to filter entries under ambiguous “family-friendly” clauses, depriving innovators of mainstream B2B exposure. Marketing on social networks is complicated by algorithmic flagging systems that conflate sex-positive content with explicit pornography, constraining paid visibility and raising customer-acquisition costs. The lack of a harmonised smart-device safety standard also delays time to market because each jurisdiction may require separate penetration-testing certificates.

Payment-Processing Discrimination

Mainstream gateways routinely label erotic merchants as “high-risk,” charging elevated fees or cutting services with minimal notice; research shows that nearly two-thirds of sector actors experienced banking suspension during 2024–2025. High-cost alternatives drain working capital and deter venture investors seeking smooth, scalable infrastructure. The choke-point extends to personal finances, with executives at legitimate firms encountering personal account closures that blur professional and private lines, reinforcing social stigma. Disintermediation via cryptocurrency offers partial relief but adds volatility and regulatory scrutiny. Smaller brands divert design resources to payment reconciliation rather than product innovation, indirectly capping the sextech market’s attainable growth trajectory within conservative financial systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Integration Drives Premium Migration

Smart sex toys trail-blaze growth with a 22.34% CAGR, indicating that buyers now expect sensor arrays, app orchestration, and AI coaching straight out of the box. Vibrators keep 36.48% of sextech market share because brands refresh materials and ergonomic forms faster than substitution cycles, ensuring familiarity does not equal stagnation. Within the sextech market size hierarchy, dildos remain stable—commanding loyalty among price-sensitive shoppers while still receiving material upgrades such as platinum silicone. Wearables attract couples seeking discreet external use in public social settings, blending fashion and function. Sound-synchronised devices like the internal music player showcased on Kickstarter illustrate sensory crossovers previously unseen in intimate hardware. Two-way video integration between stimulators and VR content libraries is in beta, foreshadowing subscription bundles that marry consumable media and hardware leasing.

Ongoing diversification within the sextech market raises barriers for generic manufacturers, because copyrighted software environments, firmware over-the-air upgrades, and proprietary accessories lock buyers into ecosystems. Premium placements in lifestyle stores further reframe certain models as collectibles rather than purely functional aids. Cross-licensing between sexual-wellness labels and luxury fashion houses introduces influencer-led limited editions, expanding margins despite higher materials costs. Finally, academic collaborations promise medically certified variants addressing issues like postpartum recovery, carving out reimbursement pathways in private insurance.

By Technology: AI Emerges as Premium Differentiator

Bluetooth retains 44.64% of the installed base because consumers appreciate auto-pairing with smartphones; still, cybersecurity audits reveal man-in-the-middle vulnerabilities that could leak intimate data, pushing innovators toward encrypted Wi-Fi stacks. Wi-Fi modules allow cloud analytics, firmware patches, and deep-learning routines that improve device performance without user intervention, though higher battery requirements can limit form-factor miniaturisation. The AI layer grows 12.78% annually by harnessing pattern recognition to recommend session length, lubrication type, or after-care routines.

Haptic-feedback suites move beyond vibration to include pneumatic pulses and micro-fluidic membranes, delivering more nuanced pressure waves. The result is a platform effect: hardware sales feed data into algorithms that in turn create new content, renewing user engagement. Within the sextech market, early adopters are already paying subscription fees for adaptive soundscapes that respond to sensor data in real time, positioning AI as a recurring-revenue engine rather than a one-off feature.

By End-User: Inclusive Design Accelerates Adoption

Female consumers command 49.67% of global value due to decades of under-served demand that now meets destigmatised purchasing channels. LGBTQ+ segments will outpace total sextech market growth at 20.53% CAGR, making inclusivity a profit imperative rather than a CSR footnote. Designs that eliminate gendered color palettes or assume binary anatomies succeed because younger buyers value representation.

Male adoption rises as discourse around mental health, body positivity, and sexual performance opens new product subcategories for erection health and pelvic-floor training. Couples adopt app-linked devices to co-author experiences, whether co-located or remote; these jointly-controlled units help sustain intimacy in long-distance situations and offer built-in consent logging, which may become a legal asset if regulators demand proof-of-consent logs. High-net-worth older demographics are being courted with premium materials, gold-plated finishes, and concierge-level onboarding, translating inclusivity into tiered price ladders that span entry to luxury.

By Distribution Channel: Online Dominance Accelerates

Digital storefronts maintain a 59.86% grip on the sextech market share by removing embarrassment friction and enabling algorithmic curation of catalogues that often exceed brick-and-mortar shelf space by an order of magnitude. Mobile first design and one-click checkout support impulse buying during peak late-night browsing hours. Brand-owned sites handle explicit merchandising better than general marketplaces constrained by broad community-guideline algorithms; the result is resilient growth even when big-tech channels impose keyword bans.

Specialty boutiques still matter by staging in-person product demos, and they now augment retail with experiential events such as workshops on consent or sexual-position yoga classes that drive foot traffic. Hypermarkets and supermarkets begin experimenting with discreetly packaged wellness endcaps, piloting category expansion where demographic fit is proven. Pharmacy chains add over-the-counter contraceptives and lubricants that also signpost premium electronics, converging consumer health with lifestyle retail.

Geography Analysis

Asia-Pacific is the principal expansion engine, posting a 20.43% CAGR, thanks to rising middle-class income, relaxed social norms, and high smartphone penetration. Mainland China lifts visibility by allowing boutique stores in urban malls, which boosts tourist-oriented sales and demonstrates government tolerance for products formerly relegated to online channels. Japan’s ageing demographic turns to companion robots and AI-enabled strokers that promise wellness benefits beyond pleasure, aligning with healthcare incentives to maintain senior quality of life.

North America holds 33.73% of total sales in 2024, leveraging affluent consumers and robust direct-to-consumer logistics. However, payment blacklisting continues to cap small-brand scalability, meaning multinationals secure inventory priority with processors that reliably underwrite adult verticals. Public-private dialogues about intimate-data privacy gain momentum, potentially setting federal guardrails by 2027 that could harmonise device certification for remote-data capture.

Europe balances progressive attitudes with stringent data-protection frameworks; the combination encourages high compliance standards that later diffuse worldwide. Strong vendor networks in Germany, France, and the Nordic countries channel med-tech know-how into ergonomic designs with recyclable silicone, meeting growing demand for sustainable options. Latin America and the Middle East & Africa trail in dollars but present upside clusters around metropolitan hubs where youthful populations and rising connectivity rates converge, indicating emerging-market headroom once local regulatory clarity materialises.

Competitive Landscape

No single participant controls more than 10% of annual revenue; the structure yields a market concentration score of 4 on a 10-point scale, signalling moderately fragmented dynamics. Legacy leaders Lovehoney and LELO protect share through multi-brand portfolios priced from entry to luxury, commanding shelf space both online and in pharmacies. Lovense competes on first-mover status in teledildonics, recently pairing hardware with Apple Vision Pro to lock in high-income technophiles.

Start-ups leverage crowdfunding to prototype AI-driven novelties, circumventing venture-capital unease about adult themes; once demand is validated, they often license firmware IP to established OEMs, capturing royalties without building full supply chains. A clustering of femtech and sextech propositions produces acquisition deals such as Perelel’s purchase of LOOM, illustrating how broader women’s health platforms fold sexual wellness into holistic care pathways.

Strategic roadmaps highlight ecosystem lock-in: devices, educational content, AI coaches, and tele-therapy services integrate through unified log-ins and cross-compatible accessories. Intellectual-property protection shifts from hardware patents to software and algorithm libraries, complicating imitation by low-cost rivals. ESG imperatives push brands to adopt recyclable packaging and body-safe materials, brand attributes that younger shoppers increasingly require as table stakes.

SexTech Industry Leaders

LELO

Lovehoney Group

WOW Tech Group

Satisfyer

Lovense

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Fantasia unveiled an AI-powered emotional-interaction suite named Echo at AVN Expo 2025, combining a narrative app with a haptic device that synchronises tactile, auditory, and textual cues.

- October 2024: Femtech company Perelel agreed to acquire sexual-health start-up LOOM to integrate reproductive wellness and pleasure-product ideation.

- February 2024: Dame purchased design-forward brand Emojibator to broaden product aesthetics while keeping both labels operationally distinct.

Global SexTech Market Report Scope

| Vibrators |

| Dildos |

| Smart Sex Toys |

| Wearables |

| VR Pornography Platforms |

| Remote-controlled Devices |

| Other Sextech Products |

| Bluetooth |

| Wi-Fi |

| Haptic / Teledildonics |

| Virtual Reality |

| Artificial Intelligence |

| Female |

| Male |

| LGBTQ+ |

| Couples |

| Online Retail |

| Specialty Stores |

| Hypermarkets / Supermarkets |

| Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vibrators | |

| Dildos | ||

| Smart Sex Toys | ||

| Wearables | ||

| VR Pornography Platforms | ||

| Remote-controlled Devices | ||

| Other Sextech Products | ||

| By Technology | Bluetooth | |

| Wi-Fi | ||

| Haptic / Teledildonics | ||

| Virtual Reality | ||

| Artificial Intelligence | ||

| By End-User | Female | |

| Male | ||

| LGBTQ+ | ||

| Couples | ||

| By Distribution Channel | Online Retail | |

| Specialty Stores | ||

| Hypermarkets / Supermarkets | ||

| Pharmacies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the sextech market and its expected CAGR?

The sextech market size is USD 47.78 billion in 2025, and it is forecast to rise at an 18.07% CAGR to reach USD 109.67 billion by 2030.

2. Which product category leads global revenue?

Vibrators dominate with 36.48% of sextech market share in 2024, supported by continuous innovations in design and materials.

3. Which region is growing the fastest?

Asia-Pacific records a 20.43% CAGR through 2030, propelled by loosening cultural taboos and higher disposable income.

4. Why do online channels command the largest share?

Online retail offers privacy, wide assortments, and AI-based personalization, enabling it to capture 59.86% of 2024 revenue and expand at 22.76% CAGR.

5. What is the biggest barrier to growth?

Payment-processing discrimination removes banking services from legitimate firms, reducing profitability and deterring new entrants.

6. How does artificial intelligence influence product innovation?

AI personalizes stimulation patterns, offers coaching, and connects devices to tele-therapy platforms, driving the fastest technology growth segment at 12.78% CAGR.

Page last updated on: