Corporate Wellness Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

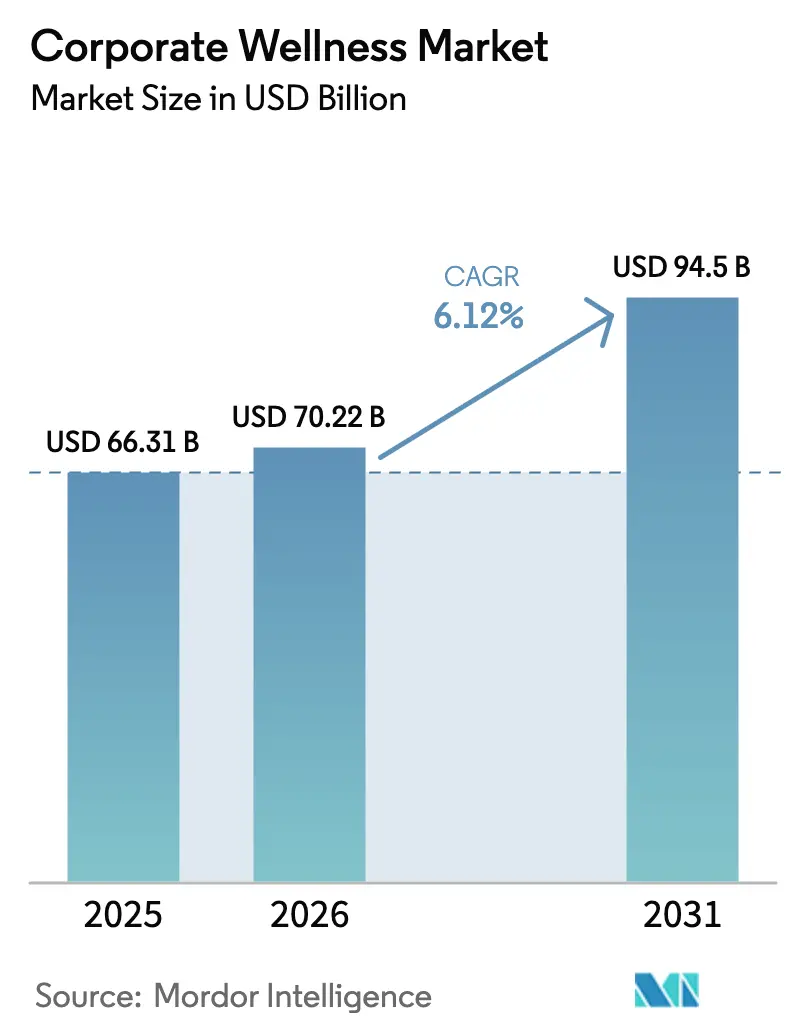

| Market Size (2026) | USD 70.22 Billion |

| Market Size (2031) | USD 94.5 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

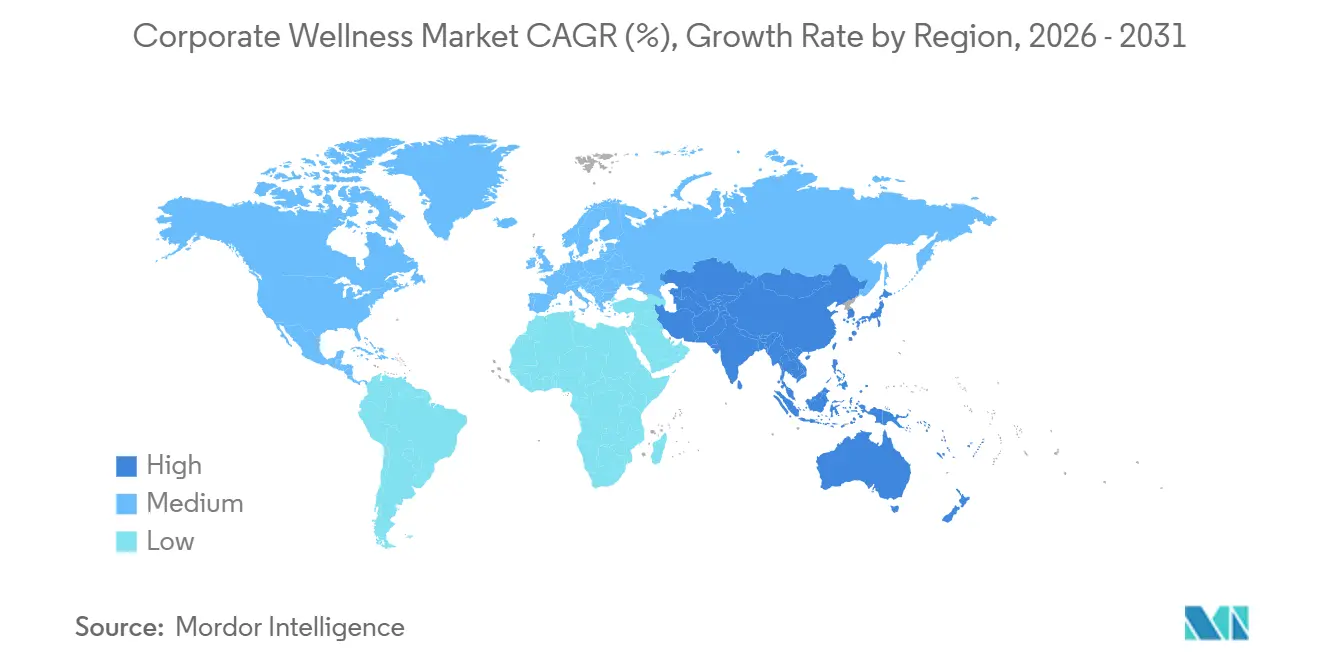

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corporate Wellness Market Analysis by Mordor Intelligence

The Corporate Wellness Market size is expected to increase from USD 66.31 billion in 2025 to USD 70.22 billion in 2026 and reach USD 94.5 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

That trajectory reflects employers' increasing focus on preventive health, productivity optimization, and talent retention as healthcare costs continue to escalate. Uptake is powered by biometric screenings, stress-management modules, and digital coaching that promise to bend the long-term expense curve. Regulatory clarity from the U.S. Department of Labor and the Department of Health and Human Services in 2024 strengthened confidence in compliant program design, while the Equal Employment Opportunity Commission’s guidance on wearable incentives closed privacy loopholes. North America continues to anchor spending, but the Asia-Pacific region is setting the pace as statutory requirements broaden in India and occupational health regulations tighten in China. Competitive intensity is moderate; insurers, point-solution startups, and integrated platforms are jockeying for a share as employers press for unified, data-rich ecosystems.

Key Report Takeaways

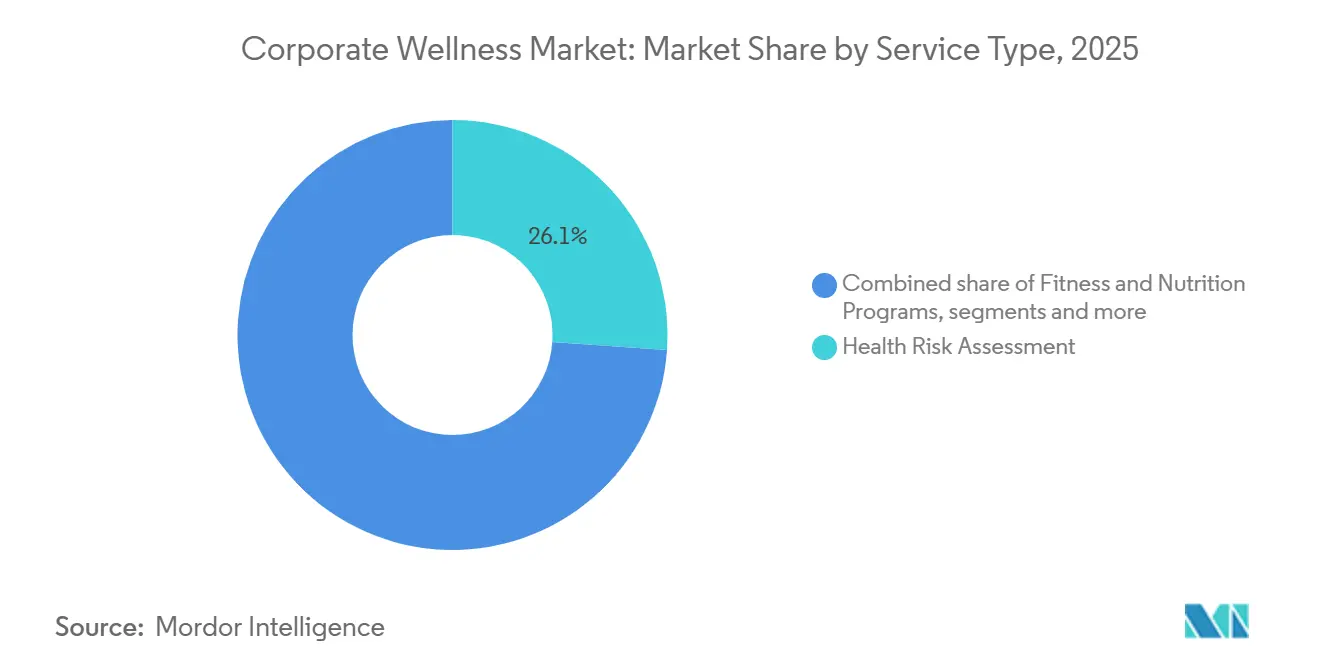

- By service type, health risk assessment led with 26.12% revenue share in 2025; stress management is projected to expand at a 7.20% CAGR to 2031.

- By delivery model, on-site programs accounted for 55.43% of the corporate wellness market share in 2025, while off-site or virtual offerings are projected to advance at an 8.23% CAGR through 2031.

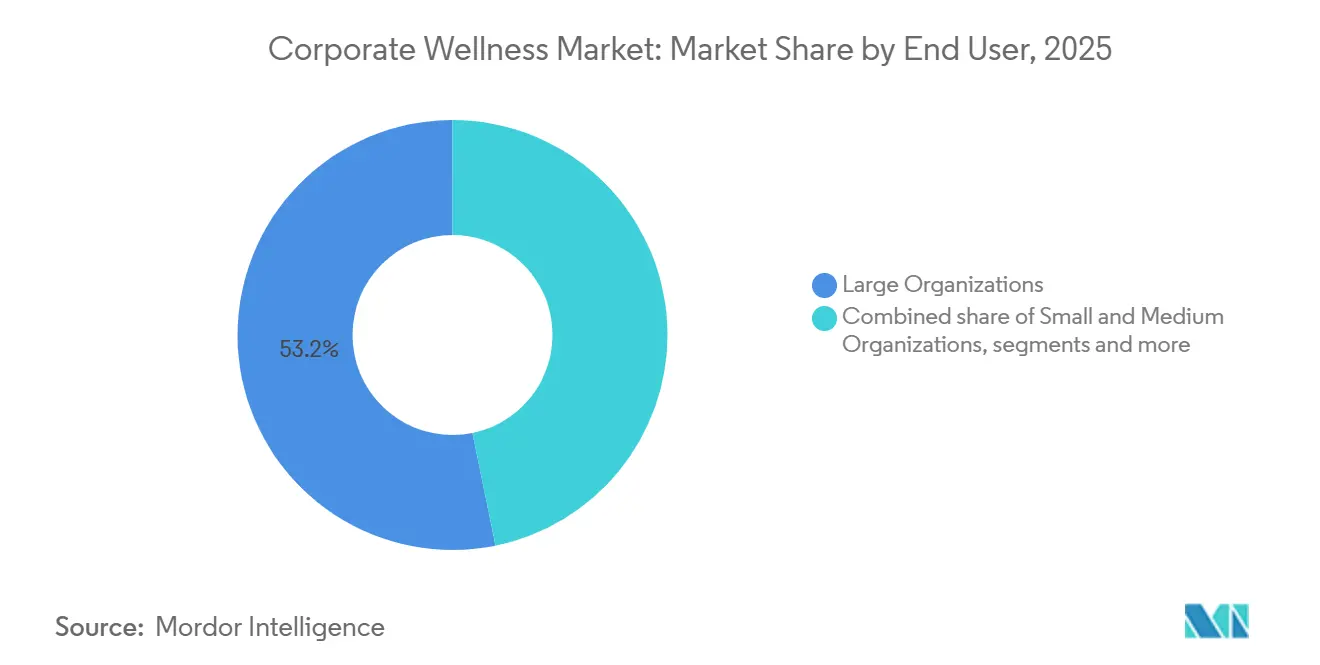

- By end user, large organizations held 53.21% of the corporate wellness market size in 2025, whereas small and medium organizations are set to grow at a 6.43% CAGR through 2031.

- By ownership model, in-house managed programs captured a 55.67% share in 2025; outsourced vendor-managed programs are expected to expand at a 6.89% CAGR through 2031.

- By geography, North America retained a 39.40% share in 2025; however, the Asia-Pacific region is the fastest-growing, with a 7.54% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corporate Wellness Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating employer healthcare expenditure | +1.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Growing burden of lifestyle-related chronic diseases | +1.5% | Global, pronounced in urban Asia-Pacific and North America | Long term (≥ 4 years) |

| Demonstrated ROI & talent retention benefits | +1.2% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption of digital health technologies | +1.4% | Global, led by North America and Asia-Pacific tech hubs | Short term (≤ 2 years) |

| Shift toward holistic well-being | +0.9% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Integration of wearable data with HR analytics | +1.0% | North America, Europe, select Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Employer Healthcare Expenditure

Family premiums for employer-sponsored insurance reached USD 25,572 in 2024, a 7% increase, and Mercer’s outlook predicted another 5.8% rise for 2025[1]Kaiser Family Foundation, “2024 Employer Health Benefits Survey,” kff.org. Finance leaders, therefore, treat wellness as a hedge, emphasizing screenings that flag pre-diabetic employees and trigger early coaching. The U.S. Surgeon General linked mental-health investment to lower absenteeism, prompting self-insured firms to accelerate premium-differential incentives. Compliance guardrails still apply; outcome-based programs must offer reasonable alternatives to avoid discriminatory penalties, a complexity that tilts adoption toward vendors with actuarial expertise.

Growing Burden of Lifestyle-Related Chronic Diseases

Chronic conditions account for approximately 90% of the annual U.S. healthcare expenditure[2]Centers for Disease Control and Prevention, “Chronic Disease Overview,” cdc.gov. Employers now view sedentary work, stress, and poor diet as controllable factors contributing to these costs. Asia-Pacific markets echo that trend as rapid urbanization replicates Western disease patterns, yet lacks matching infrastructure. Programs that pair activity tracking with nutrition coaching demonstrate measurable biometric improvements within 18 months. Coverage of GLP-1 obesity drugs by 67% of large U.S. employers in 2024 highlights the significant financial implications.

Demonstrated ROI & Talent Retention Benefits

A 2024 RAND review showed disease-management modules deliver the bulk of cost savings, while lifestyle-management boosts retention. Early-career turnover fell 10-15% at U.S. federal agencies with comprehensive wellness programs, reinforcing talent-centric justifications. Employer brand metrics improve when mental-health resources are publicized on job boards, resulting in reduced recruiting costs and a shorter time-to-fill.

Rapid Adoption of Digital Health Technologies

Express Scripts’ Digital Health Formulary treats validated apps like covered drugs, signaling payer-level endorsement for digital therapeutics. EEOC guidance requires wearable-based incentives to remain voluntary and data-segregated, limiting privacy backlash. Optum’s AI-driven coaching nudges illustrate how incumbents fine-tune engagement with real-time analytics. Scale advantages make virtual channels attractive for dispersed hybrid workforces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Low sustained employee engagement levels | -1.3% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data-privacy and cyber-security risks | -0.9% | Global, strict in Europe and North America | Medium term (2-4 years) |

| Fragmented vendor ecosystem & integration issues | -0.7% | North America and Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Limited wellness budgets in SMEs | -0.6% | Global, pronounced in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Sustained Employee Engagement Levels

Participation often drops below 30% in quarter 2, undermining ROI. Generic messaging often overlooks the diverse needs of workers, yet leadership role-modeling doubles the retention rate in programs. Gamified challenges offer short-term boosts but need intrinsic motivators to sustain change. The Surgeon General recommends embedding wellness into daily workflows, such as walking meetings, to facilitate adoption.

Data-Privacy and Cyber-Security Risks

Wellness portals handle protected health information that must be ring-fenced from personnel files. The EEOC clarifies that wellness data cannot be used to influence employment decisions. GDPR heightens compliance costs in Europe. A single breach can lead to class-action suits and reputational harm, steering large employers toward vendors with SOC 2 and ISO 27001 certifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Preventive Screening Dominates as Stress Management Accelerates

Health risk assessment held 26.12% of the corporate wellness market share in 2025, reflecting widespread employer reliance on baseline biometrics to stratify risk. Stress Management is forecast to outpace the corporate wellness market at a 7.20% CAGR through 2031, as burnout remains a top claims driver. Combined fitness and nutrition modules round out employer playbooks but face margin compression as commoditized offerings.

The corporate wellness market size tied to Health Risk Assessment remains large because HRAs drive engagement in downstream coaching and disease-management streams. Stress-management vendors now bundle cognitive-behavioral therapy and mindfulness into a single license, offering buyers an integrated option that reduces procurement friction. Smoking-cessation programs shrink in mature economies but retain relevance where tobacco use stays high.

By Delivery Model: Virtual Platforms Gain Momentum Alongside On-Site Legacy

On-site programs accounted for 55.43% of the corporate wellness market in 2025, thanks to fitness centers and face-to-face screenings that reinforce company culture. Off-site or Virtual deployments are expected to grow at an annual rate of 8.23%, making them the fastest-growing delivery mode through 2031. Hybrid models blend both, appealing to multiregional employers balancing remote and office workers.

Corporate wellness market size gains for virtual channels stem from lower marginal costs and real-time analytics. Engagement differences narrow as AI nudges personalize content. Yet, onsite fitness classes still outperform apps in terms of social reinforcement, so vendors pitch omnichannel experiences that seamlessly shift between physical and digital spaces without friction.

By End User: Enterprise Scale Powers Spend While SME Adoption Rises

Large organizations delivered 53.21% of 2025 spending, leveraging volume contracts and dedicated benefits teams. SMEs grow at 6.43% CAGR through 2031 as turnkey apps reduce administrative hurdles. Public-sector entities adopt programs more slowly but retain long contracts once funded.

The corporate wellness market size for SMEs should lift as platform costs fall and case studies prove retention ROI. Data-light offerings, such as step challenges with minimal PHI capture, mitigate privacy concerns that deter smaller firms. Enterprises continue to pursue end-to-end integrations with HR and EHR systems, thereby amplifying data-driven precision.

By Ownership Model: In-House Control Prevails but Outsourcing Ramps

In-house managed programs captured a 55.67% share in 2025, favored by self-insured employers seeking direct access to claims and biometric data. Outsourced vendor-managed programs are expected to grow at a 6.89% CAGR through 2031 as expertise demands and integration complexity increase.

Many enterprises adopt hybrid structures, retaining strategic oversight while outsourcing platform hosting. Outsourcing appeals to fully insured firms that prioritize speed and compliance certifications. The corporate wellness market size under outsourced models expands as vendors like Personify Health pitch modular ecosystems that bundle benefits administration with engagement tools.

Geography Analysis

North America held 39.40% of the corporate wellness market in 2025, anchored by high premium costs, sophisticated analytics, and clear regulatory frameworks. ACA provisions allow premium discounts for compliant programs, reinforcing adoption incentives. GLP-1 drug coverage underscored employers’ willingness to fund costly interventions when clinical evidence supports outcomes.

The Asia-Pacific region is set to register a 7.54% CAGR from 2026 to 2031, the fastest growth rate worldwide. Statutory wellness clauses in India and tightening occupational regulations in China drive uptake, while Japanese employers address aging workforce productivity gaps with resilience programs[3]. Mobile-first delivery thrives in Southeast Asia, where smartphone penetration is high; however, cultural preferences for in-person interaction in Japan and Korea temper pure virtual models.

Europe, the Middle East, Africa, and South America comprise the remainder. Europe’s GDPR raises compliance costs but also builds employee trust, aiding adoption. The Middle East experiences steady, incremental uptake, led by government mandates in the Gulf. Africa remains nascent due to limited employer-sponsored coverage. South America experiences tempered growth amid economic volatility, though Brazil and Mexico lead with large-enterprise pilots. Across regions, the corporate wellness market continues to benefit from labor market competition that prizes healthy and engaged workforces.

Regulatory Landscape

Corporate wellness programs operate at the intersection of employee benefits and employment law, and program design is shaped by the United States Department of Labor (DOL) and Department of Health and Human Services (HHS) interpretations of ACA and HIPAA nondiscrimination requirements. Under ACA Section 2705 and the implementing wellness program rules (including 45 CFR 146.121), health-contingent incentives are capped at 30% of the cost of coverage (and up to 50% for tobacco-related programs), and outcome-based designs must provide reasonable alternatives to reduce discrimination risk.

Beyond incentive mechanics, privacy, voluntariness, and safe handling of health information remain central compliance themes under the ADA/GINA framework and employer group health plan administration expectations. In February 2025, the CDC updated its Worksite Health ScoreCard manual, and employers frequently use CDC and NIOSH Total Worker Health frameworks as structured, non-mandatory reference points for program governance. In early 2026, OSHA updated its Low-Hazard Industries Table (effective for inspections on or after January 22, 2026) and issued an internal mental health and wellness awareness chapter for its safety and health manual (effective March 6, 2026), reinforcing the broader institutional focus on workplace well-being alongside traditional safety oversight.

Value Chain Analysis

The corporate wellness value chain typically starts with program design inputs, including screening protocols, coaching content, and measurement frameworks, and then moves into technology enablement and service delivery. Screening and assessment inputs are often supported by diagnostic and testing providers (for example, Quest Diagnostics Health & Wellness and Labcorp), while content and assessment tool providers support health risk assessments and baseline program engagement. The next layer is platform development and integration, where vendors consolidate mobile apps, analytics, and wearable connectivity into employer-ready dashboards and workflows, a requirement as employers seek unified experiences across on-site and virtual delivery models.

Downstream delivery includes on-site screenings, fitness and nutrition programs, and behavioral health services delivered by EAP and coaching networks (for example, ComPsych and EXOS), along with insurer and benefits administrators that embed wellness into broader health benefit management. Distribution and contracting are led by employers and benefits brokers/consultants, with procurement increasingly emphasizing single-sign-on, data governance, and interoperability with HR and health benefit systems. Common bottlenecks include data standardization across multiple point solutions, integration gaps between HR systems and health platforms, and cybersecurity assurance, which increases the premium for mature vendors that can demonstrate compliance and audit readiness.

Competitive Landscape

The corporate wellness market is moderately fragmented; no single vendor tops 10% share. Consolidation is accelerating as employers demand unified platforms. Personify Health emerged in 2024 from the merger of Virgin Pulse and HealthComp, combining benefits administration, care navigation, and engagement into a single platform. Insurers such as Cigna and Optum leverage claims data to tie biometric outcomes to premium discounts.

Express Scripts’ Digital Health Formulary positions payers as curators of quality digital therapeutics, challenging point-solution vendors that lack clinical validation. Wearable makers, including Oura, skip intermediaries by offering employer dashboards that correlate readiness scores with productivity. Vendors win deals by demonstrating AI-based personalization, single-sign-on integration, and proven compliance with HIPAA and GDPR.

SME white-space persists, inviting low-touch vendors with simplified pricing. Public-sector prospects appeal to players who are patient enough for lengthy procurement processes. Regulatory rigor remains a differentiator; EEOC privacy guidance favors mature data-governance frameworks over lightly funded startups. The market is therefore likely to coalesce around a cadre of full-stack platforms, with niche specialists serving targeted verticals or geographies.

Corporate Wellness Industry Leaders

ComPsych Corporation

Virgin Pulse

EXOS

Optum, Inc.

Quest Diagnostics Health & Wellness

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is compliance-led modernization of mental and behavioral health benefits embedded in wellness ecosystems, particularly for employers that sponsor group health plans and must document parity compliance. In March 2026, the U.S. Departments of Labor, HHS, and Treasury released the fourth annual MHPAEA enforcement report, sustaining pressure on plan sponsors to produce comparative analyses and address nonquantitative treatment limitation (NQTL) documentation requirements. This compliance load supports demand for corporate wellness platforms that combine stress management, care navigation, and behavioral health access with auditable reporting, rather than standalone engagement apps.

Another opportunity is the shift from wellness as a benefits add-on to an integrated, data-driven operating model across distributed workforces, which aligns with the move toward off-site/virtual and hybrid delivery. Employer buyers are asking for AI-augmented personalization and improved engagement retention without expanding sensitive data exposure, favoring vendors that can operationalize ethical data practices and segregate wellness data from employment decisions. In practice, this creates whitespace for platforms delivering measurable outcomes across stress management and chronic condition programs while maintaining security assurances (such as SOC 2 and ISO 27001) that reduce procurement friction for larger organizations and highly regulated industries.

Recent Industry Developments

- April 2026: ComPsych shared findings from an Integrated Benefits Institute analysis of its behavioral health services using 2024 and 2025 data, reporting a projected annual ROI figure. The use of an external evaluation framework supports more outcomes-based selling to large employers and benefits decision-makers. It also raises the bar for competing vendors that rely on engagement metrics without independently supported economic impact evidence.

- October 2025: Exos acquired sports technology company Infinite Athlete and its subsidiary Biocore to deepen its AI-driven data and biomechanics capabilities. The deal broadens Exos offerings across performance analytics and recovery, which can translate into more differentiated corporate wellness and human performance programming for employers seeking measurable outcomes. It also signals continued convergence between high-performance science and workplace well-being services.

- June 2024: Virgin Pulse and HealthComp completed their merger and rebranded the combined entity as Personify Health, unifying engagement, care navigation, and benefits administration capabilities under one platform. The integration supports employers that want fewer point solutions and tighter connections between wellness engagement and health plan operations. It added scale in platform-based corporate wellness and increased competitive pressure on standalone wellness app providers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers employer sponsored wellness offerings that are designed to improve employee health and work readiness through programs, services, and supporting platforms delivered onsite, virtual, or in hybrid formats.

Scope exclusions: Standalone health insurance premiums and direct to consumer wellness apps that are not purchased as workforce programs are excluded.

Segmentation Overview

- By Service Type

- Health Risk Assessment

- Fitness & Nutrition Programs

- Stress Management

- Smoking Cessation

- Mental & Behavioral Health Management

- Other Service Types

- By Delivery Model

- On-Site

- Off-Site / Virtual

- Hybrid

- By End User

- Large Organizations

- Small & Medium Organizations

- Public Sector & Others

- By Ownership

- In-House Managed Programs

- Outsourced Vendor-Managed Programs

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to pin down the demand context and the rules that shape employer wellness spend across regions. We referenced public sources such as the World Health Organization for NCD and mental health indicators, the International Labour Organization for workforce structure, and the OECD for employer health spending signals and productivity context.

To keep assumptions practical, the desk phase also used sources such as the US CDC workplace health content, US Bureau of Labor Statistics series on employment and compensation, and peer reviewed public health journals for program effectiveness markers (screening, activity, stress, and chronic condition support). Company filings, investor presentations, and reputable press were also checked to understand typical service bundles and delivery modes, and a paid subscription for company financials and news helped cross check scale and geographic exposure. These examples are not exhaustive, and many other sources were reviewed to collect data points, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure test the model inputs that are not consistently visible in public sources, especially adoption levels, pricing direction, and how employers bundle wellness services. We spoke with program operators, benefits and HR decision makers, and channel partners across major regions so the assumptions could be adjusted when the on the ground picture did not match desk signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 20% | APAC: 38% |

| Mid tier: 46% | Functional/Unit leaders: 25% | EMEA: 36% |

| Smaller Players: 21% | Managers: 55% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where workforce counts, employer benefit intensity, and expected wellness participation are used to reconstruct the spending pool by region, and then it is split into the program types that employers typically buy. To keep the outputs grounded, we also run selective bottom-up approximations using sampled provider revenues, channel checks, and an ASP times volume lens for common modules, and then totals are tuned when the two views do not line up.

Key inputs used in the model include employed population by region, white collar versus onsite workforce mix, wellness program penetration by organization size, typical per employee per month pricing bands, and the share of spend going to onsite versus virtual delivery. Where data is thin, gaps are handled by using proxy indicators (such as employer healthcare cost pressure and reported wellbeing initiatives) and then narrowing the range through interview feedback. For forecasting, scenario analysis is used to reflect the different adoption speeds employers show after major policy changes and benefit cycle resets, with assumptions refreshed on participation and pricing rather than only extending a CAGR.

Data Validation & Update Cycle

Outputs are validated through repeated checks that compare the modeled spending pool with independent signals such as workforce growth, employer benefit budgets, and observed pricing movement for common wellness modules. If a region or program line shows a sharp jump that is not supported by the input drivers, the assumptions are reviewed, outliers are documented, and the model is rerun before sign off.

Reports are refreshed annually, and interim updates are made when material events shift demand, pricing, or delivery models. Before delivery, we do a final pass to confirm the latest public indicators and interview feedback are reflected so the numbers align with the current market reality.

Mordor Intelligence's Corporate Wellness Market Size Compared With Other Published Estimates

It is normal to see different market values for corporate wellness because sources do not always count the same program boundaries, and they also vary in how they treat virtual delivery, pricing changes, and employer adoption speed.

By tracking participation by organization size, refreshing pricing bands by delivery mode, and validating scope boundaries, Mordor Intelligence keeps the corporate wellness total tied to employer purchased programs rather than adjacent spend that sits outside workforce wellness.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 66.31 B (2025) | |

| Global Consultancy A | USD 68.41 B (2025) | A slightly wider service bundle is implied in its scope language, which can pull in adjacent employer health services that are not always delivered as structured wellness programs, thereby lifting the total for the same year. |

| Industry Publisher B | USD 63.00 B (2024) | Uses a different base year and a longer horizon, and its 2024 value can reflect earlier pricing and adoption levels before more recent expansion of virtual and hybrid program purchasing. |

Looking across the table, most of the spread can be explained by what is counted as a wellness program versus nearby benefits spend, plus the base year used when pricing and uptake were different. Our approach stays repeatable because the total is built from clear demand drivers, and each adjustment is tied back to a documented assumption that can be rechecked at the next update.

Key Questions Answered in the Report

How large is the corporate wellness market in 2026?

It reached USD 70.22 billion in 2026 and is on track for USD 94.50 billion by 2031.

Which region leads spending on corporate wellness programs?

North America held 39.40% share in 2025 thanks to high healthcare costs and mature vendor ecosystems.

What service type is growing fastest in wellness programs?

Stress Management is advancing at a 7.20% CAGR through 2031 as employers address burnout and mental-health claims.

Why are SMEs adopting wellness solutions more quickly now?

Turnkey, low-touch platforms priced at USD 5-10 per employee per month lower administrative and cost barriers.

What is the main privacy challenge in corporate wellness initiatives?

Safeguarding biometric and health data to comply with HIPAA, GDPR, and EEOC guidance on voluntary participation.

Page last updated on: