Hormonal Contraceptives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

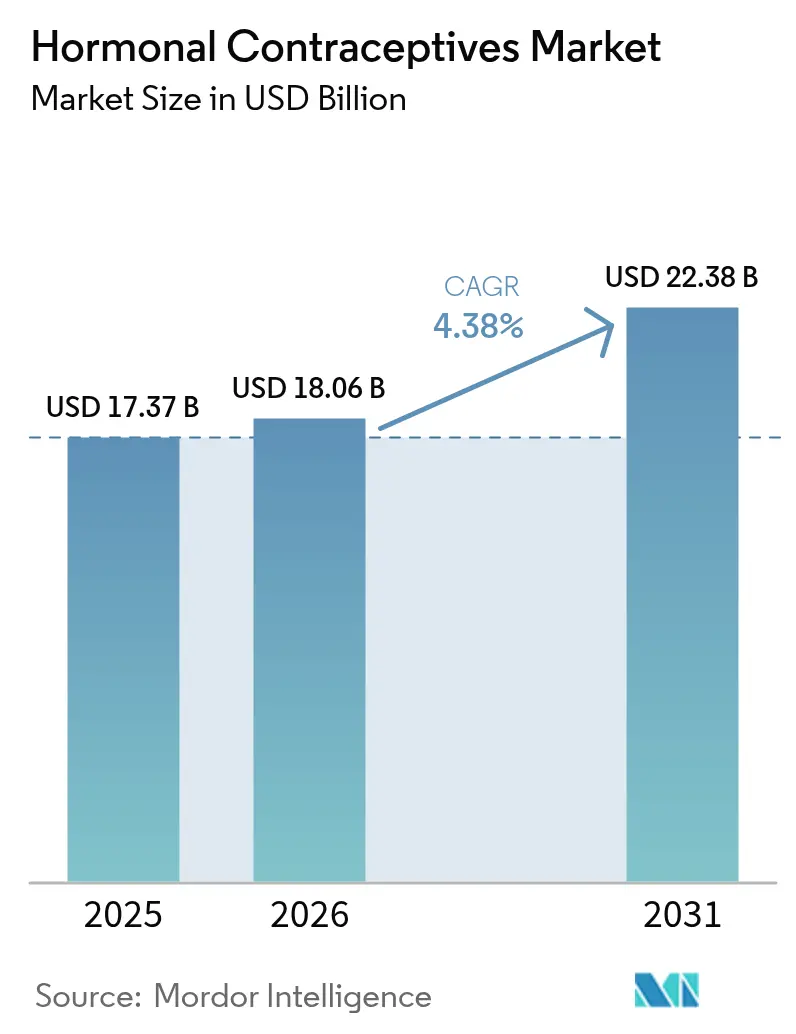

| Market Size (2026) | USD 18.06 Billion |

| Market Size (2031) | USD 22.38 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

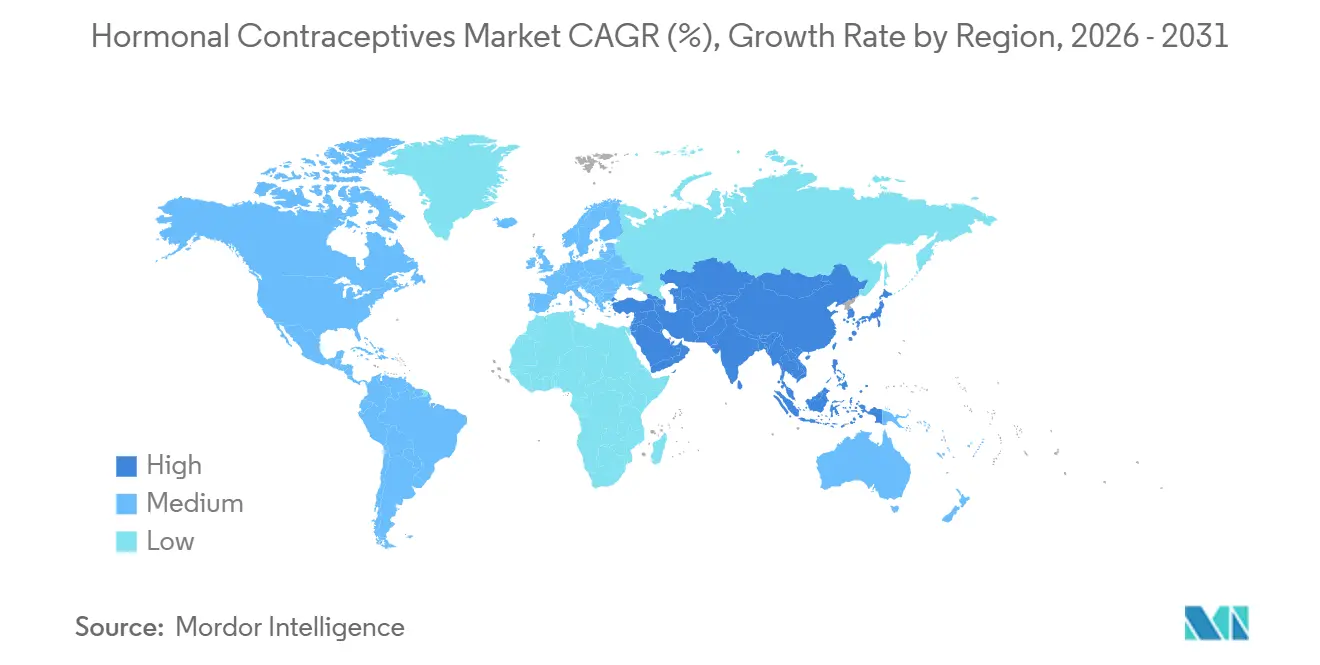

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

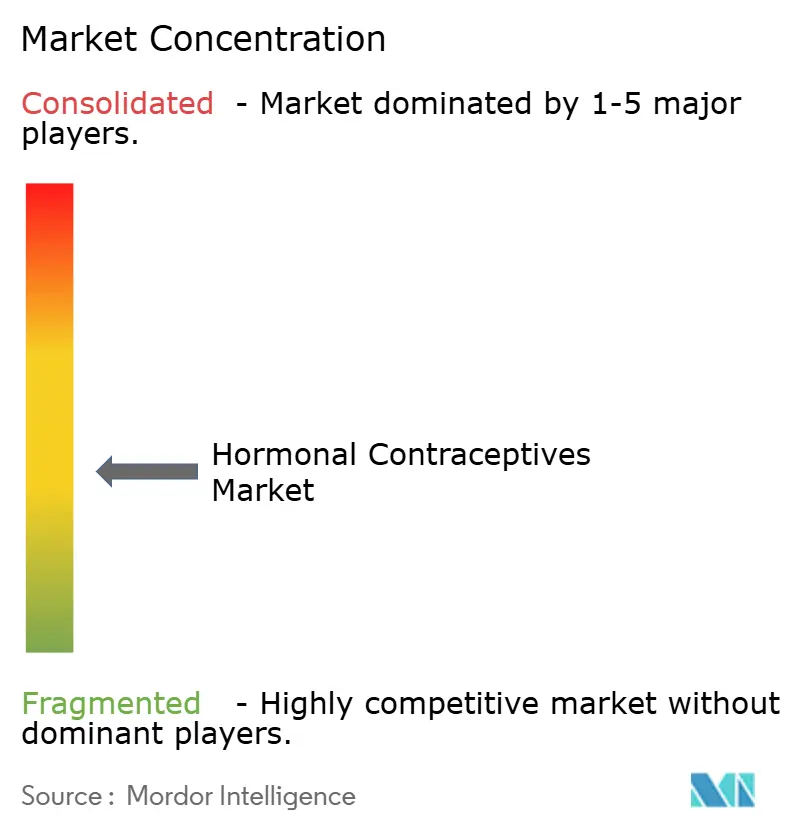

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hormonal Contraceptives Market Analysis by Mordor Intelligence

The Hormonal Contraceptives Market size was valued at USD 17.37 billion in 2025 and is estimated to grow from USD 18.06 billion in 2026 to reach USD 22.38 billion by 2031, at a CAGR of 4.38% during the forecast period (2026-2031).

Continued growth in the hormonal contraceptives market stems less from rising unit volumes and more from structural shifts in how users obtain products. Non-prescription approvals are shortening the path from consideration to purchase, while telehealth prescribing is drawing volume away from in-clinic visits that historically funneled demand through brick-and-mortar pharmacies. Lawsuits over progestin injectables are raising compliance costs and eroding injectable margins, tilting share toward long-acting reversible contraceptives (LARCs). Asia-Pacific’s rapid uptake of employer-funded benefits and school-based distribution pilots is re-allocating investment away from mature North American channels, and content moderation struggles on social media continue to shape consumer sentiment at an unprecedented speed.

Key Report Takeaways

- By product type, oral contraceptives led with 41.02% of the hormonal contraceptives market share in 2025, while implants are projected to expand at a 5.96% CAGR through 2031.

- By hormone type, progestin-only formulations captured 47.17% share of the hormonal contraceptives market size in 2025 and are forecast to grow at 6.13% from 2026-2031.

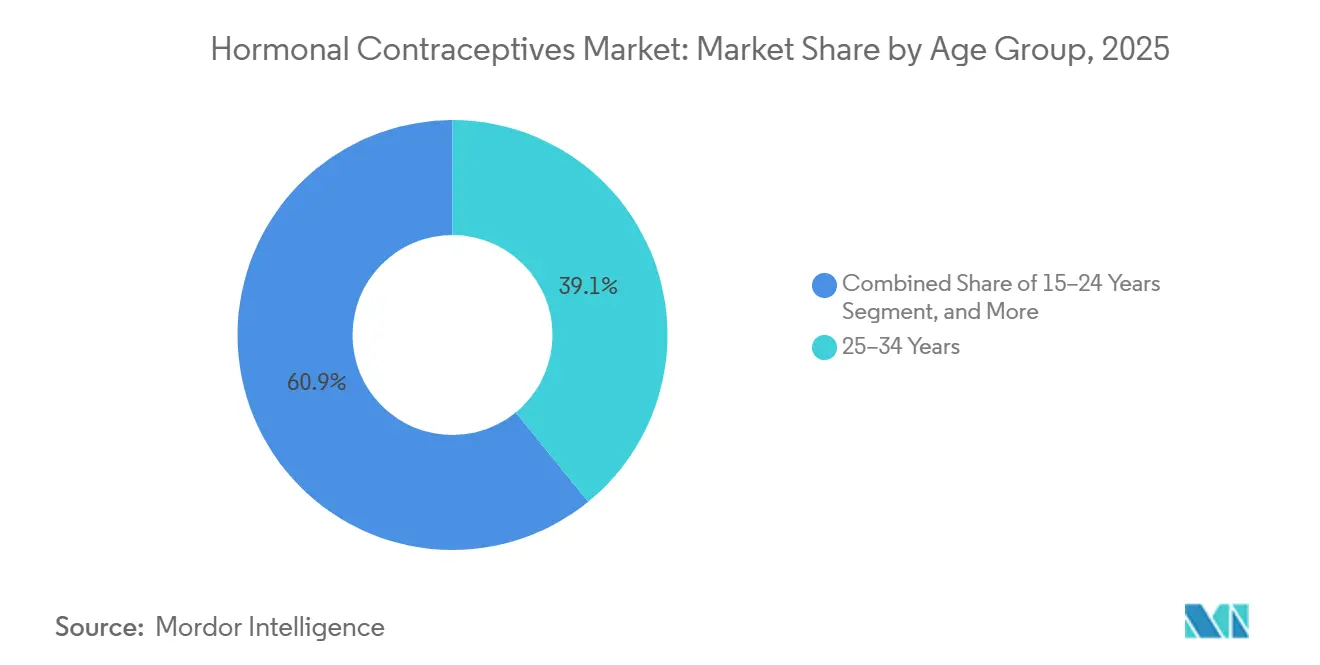

- By age group, 25–34 years led with 39.12% of the hormonal contraceptives market share in 2025; the 15-24 cohort is positioned to grow at 6.91% annually through 2031, outpacing every other bracket.

- By distribution channel, retail pharmacies led with 52.08% of the hormonal contraceptives market share in 2025; online pharmacies are advancing at a 7.11% CAGR, the fastest rate among all outlets.

- By geography, North America led with 34.78% of the hormonal contraceptives market share in 2025; and Asia Pacific is set to post an 8.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hormonal Contraceptives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising OTC Approval of Oral Contraceptive Pills | +0.8% | North America, lagging Europe | Short term (≤ 2 years) |

| Rising Prevalence of Unintended Pregnancies | +0.6% | Sub-Saharan Africa, South Asia, global spillover | Medium term (2-4 years) |

| Favorable Government Family-Planning Initiatives | +0.7% | North America, Asia-Pacific, Latin America | Medium term (2-4 years) |

| Advancements in Long-Acting Reversible Contraceptives | +0.9% | Global, early adoption in Australia and Scandinavia | Long term (≥ 4 years) |

| Expansion of Telehealth-Based Prescribing | +0.7% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Employer-Funded Benefits in Emerging Markets | +0.5% | Asia-Pacific, Latin America, Gulf Cooperation Council | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising OTC Approval of Oral Contraceptive Pills

The FDA’s 2023 decision to move the norgestrel-based Opill to over-the-counter status, followed by its March 2024 retail debut, condensed the prescription journey into a same-day retail interaction.[1]U.S. Food and Drug Administration, “Telemedicine Guidance for Prescribing Contraceptives,” fda.gov Manufacturers are now racing to replicate this model for combined formulations, with Cadence OTC aiming for clearance in late 2026. U.S. consumers gain near-instant access, but Europe remains tethered to physician gatekeeping as the EMA weighs cardiovascular-screening concerns, preserving a trans-Atlantic revenue gap. Brands active in the hormonal contraceptives market are leveraging direct-to-consumer advertising to build loyalty before European competitors secure comparable OTC pathways.

Rising Prevalence of Unintended Pregnancies

Half of all global pregnancies were unintended in 2024, and unmet contraceptive need stood at 8% among women of reproductive age.[2]World Health Organization, “Family Planning/Contraception Fact Sheet,” who.int Rural clinic shortages in Sub-Saharan Africa and South Asia magnify demand for self-administered methods such as pills and injectables. The burden falls disproportionately on 15-24-year-olds, where unintended pregnancy rates exceed 60% in several low-income countries, prompting partnerships between suppliers and NGOs to roll out school-based programs. While product availability rises, elasticity hinges on education campaigns that reframe contraception as life planning rather than family limitation.

Favorable Government Family-Planning Initiatives

U.S. Title X allocations grew 36% to USD 390 million for fiscal 2025, lighting a long-term procurement beacon for LARCs and subsidized pills. Australia’s 2024 Medicare code additions cut out-of-pocket costs for 5-year implants by 70%, generating a 15% utilization spike within six months. While these programs lift volume, mandated price ceilings challenge manufacturers to derive margin from adherence apps, telehealth bundling, and extended-cycle innovations in the hormonal contraceptives market.

Advancements in Long-Acting Reversible Contraceptives (LARC)

Five-year efficacy confirmation for Nexplanon and an eight-year label for Mirena reduce annualized cost per user and the logistical burden of repeat insertions. Phase 1 trials of biodegradable implants hold promise for removal-free solutions, addressing provider shortages in low-resource settings. These innovations tilt preference away from short-acting pills toward set-and-forget devices, a recomposition that will reshape the hormonal contraceptives market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social-Media Backlash on Hormonal Side Effects | −0.6% | North America, Western Europe, global spillover | Short term (≤ 2 years) |

| Side-Effect Concerns & Litigation | −0.9% | North America, spillover to Europe | Medium term (2-4 years) |

| Cultural & Religious Opposition | −0.4% | Middle East, Sub-Saharan Africa, parts of Latin America | Long term (≥ 4 years) |

| Fertility-Tracking Apps Cannibalizing Demand | −0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Social-Media Backlash on Hormone-Related Side Effects

A 2024 TikTok review showed 54.4% of posts on contraception skew negative, and 78.8% highlight side effects, overshadowing efficacy data. Exposure to such content increases reported mood disturbances by 40% through a documented nocebo effect. Regulatory limits on drug promotion leave brands with muted response options, pushing them to cultivate medical-influencer partnerships to restore risk-benefit balance.

Side-Effect Concerns & Litigation

More than 2,100 lawsuits in MDL 3140 allege meningioma risk from long-term Depo-Provera use, and a 2024 BMJ study reported a 5.55-fold risk elevation.[3]Christina Munk et al., “Medroxyprogesterone Acetate and Risk of Intracranial Meningioma,” bmj.com Pfizer’s December 2025 label revision and halted advertising are shifting payer preference toward implants and IUDs. The ripple effect threatens confidence in the broader progestin category, potentially slowing uptake of newly approved progestin-only pills in the hormonal contraceptives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Implants Gain as Litigation Clouds Injectables

Oral contraceptive pills accounted for 41.02% of 2025 sales and will outpace the hormonal contraceptives market average with a 5.96% CAGR as the extended five-year efficacy lowers the total cost of care. Injectable margins are being compressed by ongoing litigation, prompting national formularies to elevate implants and hormonal IUDs. Oral pills still dominate the hormonal contraceptives market size in absolute dollars, yet growth is slowing as users migrate to set-and-forget solutions preferred by payers. The incremental shift indicates a gradual recomposition rather than abrupt displacement, preserving multichannel relevance for all product types.

Mounting safety scrutiny on depot injectables is accelerating implant penetration in Asia-Pacific public tenders, where the cost per protected year is now below USD 7 following generic launches. Transdermal patches and vaginal rings remain niche but may find a foothold among environmentally conscious consumers drawn to Annovera’s reusable design. Emergency contraceptives retain episodic demand spikes in jurisdictions with restricted abortion access, but they contribute less than 3% of overall revenue, limiting their strategic weight in the hormonal contraceptives market.

By Hormone Type: Progestin-Only Formulations Capture Estrogen-Averse Users

Combined estrogen-progestin retained 47.17% of 2025 revenue. Progestin-only products are projected to 6.13% CAGR by 2031 as cardiovascular-risk messaging narrows candidate pools for combined pills. The hormonal contraceptives market share reallocation favors brands that can differentiate bleeding profiles and cycle regularity. Low-dose estrogen options remain relevant for first-time users, but rising awareness of clotting risk in smokers and perimenopausal women is ceding ground to progestin-only SKUs.

European regulators now advise combined pills mainly for women under 35 with no risk factors, restricting the potential fan-out. U.S. uptake of OTC norgestrel pills shows that convenience can outweigh brand loyalty, and mini-pill competitors are fast-following with amenorrhea-mitigating tweaks. Extended-cycle regimens have yet to achieve breakout scale, hindered by provider unfamiliarity and limited marketing budgets, yet they represent a latent lever for lifecycle innovation in the hormonal contraceptives market.

By Age Group: Younger Cohorts Drive Growth as Employer Benefits Expand

25–34 years retained 39.12% of 2025 revenue, the 15-24 cohort will contribute the largest incremental CAGR of 6.91% through 2031, aided by zero-copay coverage in corporate benefits and school-based distribution programs. Telehealth engagement rates among this group exceed 60%, underscoring digital natives’ preference for asynchronous care. The 25-34 bracket remains the single largest revenue pool today, but growth is plateauing as family-completion accelerates in high-income markets. Users aged 35-44 pivot toward hormonal IUDs for menorrhagia relief, sustaining volume but lowering refill frequency.

Uncertain legislative efforts in several U.S. states to mandate parental notification for minors could chill growth if enacted. Conversely, established state programs in California and New York increased contraceptive prevalence by 18% without parental consent, reinforcing access policy as a determinant of demand elasticity within the hormonal contraceptives market.

By Distribution Channel: Online Pharmacies Disrupt Retail Dominance

Retail chains retained 52.08% of 2025 revenue, yet online platforms are scaling faster, with a 7.11% CAGR, by sidestepping pharmacist-refusal clauses and offering doorstep delivery within 48 hours. Hospital and clinic outlets mirror public‐funding cycles, supporting volume but capping profitability through tender pricing. Direct-to-employer distribution is nascent yet expanding, where corporate wellness platforms reimburse LARCs, particularly in urban India and the Gulf.

Regulatory scrutiny over cross-state telemedicine and fulfillment licensure remains the primary friction point. Traditional retailers have responded with click-and-collect features rather than full telehealth ecosystems, inadvertently gifting first-mover advantage to digital-native pharmacies entrenched in the hormonal contraceptives market.

Geography Analysis

North America held 34.78% of the revenue share in 2025, while the Asia Pacific region had an 8.52% CAGR growth by 2030, masking heterogeneity: India’s contraceptive prevalence climbed to 67% but still lags demand in rural districts, while China’s shift from restriction to spacing boosts uptake of longer-acting methods. Japan’s subsidy plan reflects demographic urgency, yet cultural reservations weigh on hormonal adoption. North America will maintain high per-capita spending, but growth moderates as OTC switchovers flatten clinic visits and as fertility-tracking apps cannibalize a share of new starts.

Europe’s growth stalls amid regulatory delays for OTC combined pills, and the Middle East and Africa region remains constrained by cultural norms, except in GCC expatriate hubs, where employer coverage is broadening. Latin America sees steady tender-driven volume, and generic IUD launches are compressing price points. Collectively, these trends reconfirm Asia-Pacific as the primary driver of incremental revenue in the hormonal contraceptives market.

Competitive Landscape

Bayer, Organon, Viatris, Pfizer, and AbbVie capture roughly significant global revenue, positioning the hormonal contraceptives market at moderate concentration. Patent cliffs for levonorgestrel and etonogestrel between 2024-2026 triggered a wave of generics and biosimilar IUDs, especially in Europe and Latin America, pressuring branded oral pills while insulating LARCs through provider-training moats. Small entrants leverage direct-to-consumer channels, illustrated by Cadence OTC’s pursuit of a combined OTC pill and Agile Therapeutics’ patch reformulation, both prioritizing digital engagement over field sales.

Strategic moves now cluster around LARC innovation, notably biodegradable implants that negate removal procedures and extend efficacy to five years. FDA telemedicine guidance further empowers digital-native brands by reducing clinical screening overhead. Incumbents counter with bundled adherence apps, telehealth partnerships, and co-marketing with fertility-tracking platforms to preserve stickiness. As pricing competition intensifies in commodity pills, differentiation is shifting to convenience, digital ecosystems, and ancillary health services, crystallizing a bifurcated field in which value is shifting toward integrated care packages in the hormonal contraceptives market.

Hormonal Contraceptives Industry Leaders

Merck & Co., Inc.

Pfizer Inc.

Bayer AG

Teva Pharmaceutical Industries Ltd

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Daré Bioscience confirmed 15 active Phase 3 sites for Ovaprene, expecting full enrollment by mid-2025

- March 2025: Evofem Biosciences signed a license and supply deal with Windtree Therapeutics, cutting Phexxi manufacturing costs by up to 60%, broadening affordability.

- December 2024: Organon filed with the FDA to extend Nexplanon use to five years, fortifying its implant franchise.

- October 2024: GoodRx opened a dedicated Opill e-commerce portal, reaching women lacking local healthcare services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hormonal contraceptives market as prescription or over-the-counter pharmaceutical preparations and implantable or intrauterine devices that release synthetic estrogen, progestin, or their combination to suppress ovulation, thicken cervical mucus, or thin the endometrium, thereby preventing pregnancy across reproductive-age women. Coverage spans pills, injectables, patches, rings, hormonal IUDs, implants, and emergency pills sold through physical or digital pharmacy channels in more than 25 countries.

Scope Exclusion: We deliberately leave out barrier methods, fertility-tracking apps, and permanent sterilization procedures.

Segmentation Overview

- By Product Type

- Oral Contraceptive Pills

- Injectable Contraceptives

- Transdermal Patches

- Vaginal Rings

- Implantable Contraceptives

- Hormonal IUDs

- Emergency Contraceptives

- By Hormone Type

- Combined Estrogen-Progestin

- Progestin-only

- Low-dose Formulations

- Extended-cycle Regimens

- By Age Group

- 15–24 Years

- 25–34 Years

- 35–44 Years

- 45+ Years

- By Distribution Channel

- Hospital & Clinic Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

During interviews, we validate uptake assumptions with obstetricians, reproductive-health NGOs, wholesale distributors, and payers across North America, Europe, Asia-Pacific, and Africa. User surveys in four key economies clarify brand switching, course adherence, and out-of-pocket trends that filings rarely reveal.

Desk Research

Mordor analysts first map the universe of hormonal products with publicly available information drawn from regulators such as the US FDA, European Medicines Agency, and India's CDSCO. We rely on demographic and health surveys issued by UN DESA, WHO, and national statistics bodies, plus trade intelligence from UN Comtrade and clinical evidence indexed on PubMed. Company 10-Ks, investor decks, and quarterly calls retrieved through D&B Hoovers and Dow Jones Factiva add pricing and pipeline clues, while procurement portals and tender databases anchor real-world transaction values. This list is illustrative; many additional open sources inform the dataset.

A second pass compiles shipment and formulation-approval data from bodies such as IFPMA and regional gynecology societies, and we pull patent analytics via Questel, ensuring regulatory filings and market availability align before we lock the numbers.

Market-Sizing & Forecasting

We build a top-down demand pool from child-bearing-age female populations, modern-method prevalence, and average annual consumption per user. We then corroborate totals with sampled ASP × volume roll-ups for high-penetration brands. Variables such as adolescent fertility rate, OTC pill launches, reimbursement coverage, and long-acting reversible contraceptive adoption feed a multivariate regression layered on scenario analysis. Where bottom-up checks diverge beyond eight percent, we adjust transparently.

Data Validation & Update Cycle

Analysts run variance tests against historical sales and macro indicators, reconciling anomalies before sign-off. Reports refresh annually, with interim updates if regulatory or macro shocks require.

Why Mordor's Hormonal Contraceptives Baseline Commands Reliability

Published estimates often diverge because firms pick different product baskets, price points, base years, and refresh cadences.

Our disciplined scope, dual-track modeling, and yearly update rhythm help decision-makers compare apples with apples.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.31 B (2025) | Mordor Intelligence | |

| USD 19.90 B (2024) | Global Consultancy A | Bundles non-hormonal devices and applies uniform global ASP, inflating value |

| USD 16.75 B (2024) | Industry Association B | Counts prescription sales only and omits online-pharmacy revenue |

| USD 14.28 B (2024) | Trade Journal C | Uses older hospital-only sample and minimal emerging-market coverage |

The comparison shows that once scope mismatches and pricing shortcuts are stripped away, Mordor's balanced, transparent baseline remains the most dependable starting point for strategic planning.

Key Questions Answered in the Report

How large will spending on hormonal contraception be by 2031?

The hormonal contraceptives market size is forecast to reach USD 22.38 billion by 2031, reflecting a 4.38% CAGR over 2026-2031.

Which product type is set to grow the fastest?

Subdermal implants are projected to expand at 5.96% annually through 2031 as extended efficacy and lower maintenance drive payer preference.

Why are progestin-only pills gaining share?

Broader suitability for smokers, breastfeeding women, and users with cardiovascular risks, combined with recent OTC approval of Opill, is pushing progestin-only uptake at a 6.13% CAGR.

What role does telehealth play in contraceptive access?

FDA guidance in 2024 enabled remote prescribing without in-person vitals for low-risk women, letting platforms like Nurx ship products within 48 hours and accelerate growth of online channels.

Which region will add the most new revenue?

Asia-Pacific, led by India and China, is poised to grow at 8.52% per year and contribute the largest share of incremental global sales through 2031.

Page last updated on: