Male Infertility Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.25 Billion |

| Market Size (2031) | USD 5.08 Billion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Male Infertility Market Analysis by Mordor Intelligence

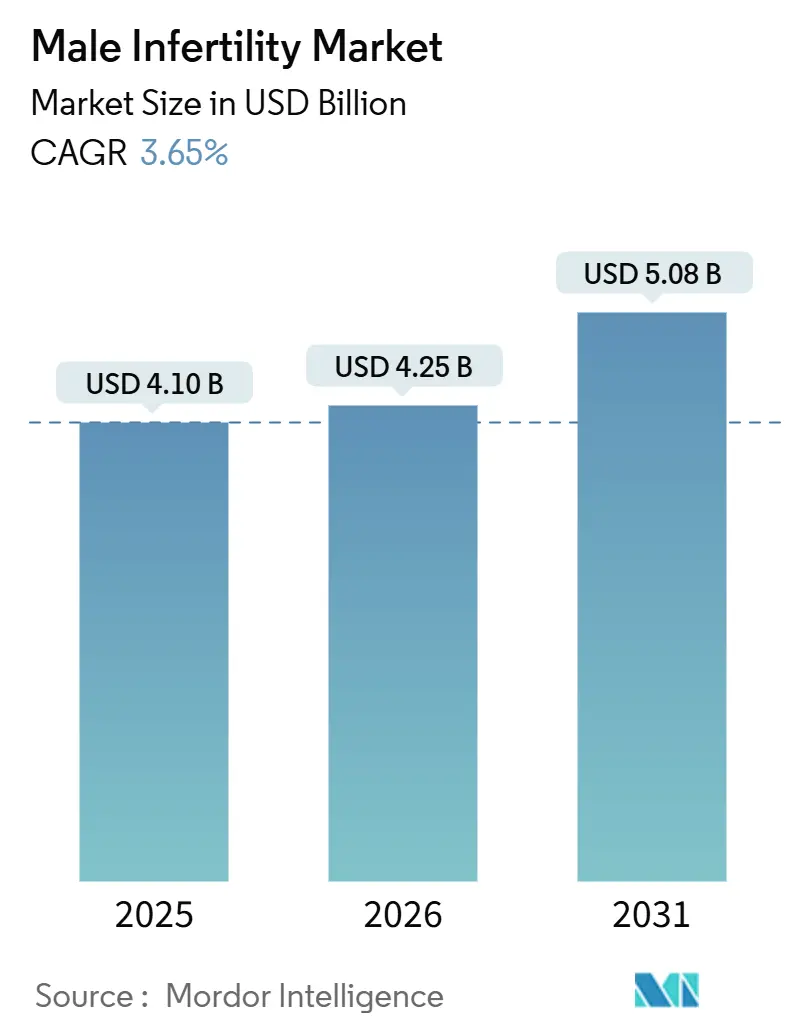

The Male Infertility Market size is expected to grow from USD 4.10 billion in 2025 to USD 4.25 billion in 2026 and is forecast to reach USD 5.08 billion by 2031 at 3.65% CAGR over 2026-2031.

Growing prevalence, documented by the World Health Organization at 17.5% of adults ever experiencing infertility with a male contribution in roughly half of cases, enlarges the prospective treatment pool. Employer health plans that now cover fertility services for one quarter of large-company workers in the United States are widening access but still concentrate benefits on in-vitro fertilization instead of male diagnostics. At-home semen tests with recent United States Food and Drug Administration 510(k) clearances are moving diagnostics outside hospital laboratories and shortening time to first result. Meanwhile, social stigma and uneven reimbursement restrict uptake in many lower-income and patriarchal settings, muting growth relative to the female fertility segment yet leaving significant latent demand.

Key Report Takeaways

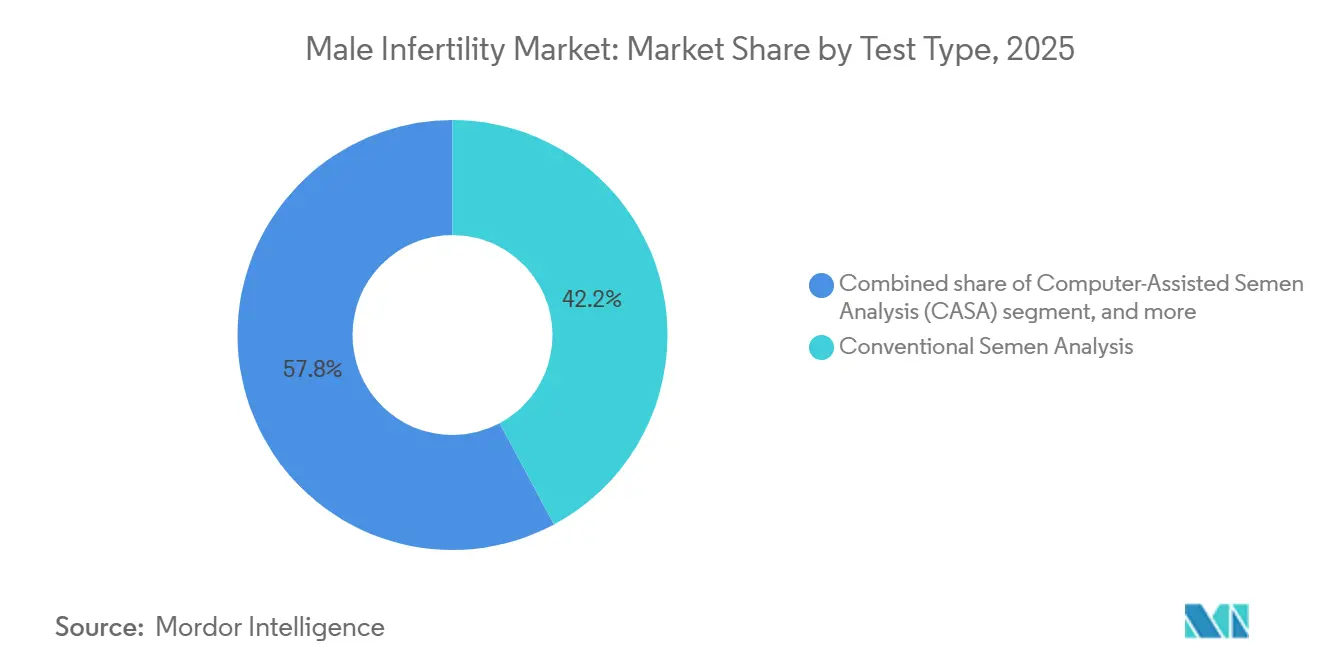

- By test type, conventional semen analysis led with 42.18% of male infertility market share in 2025, while genetic and epigenetic panels are advancing at a 5.22% CAGR through 2031.

- By treatment, medication and hormone therapy is the fastest growing segment at a 4.65% CAGR, compared with assisted reproductive technology’s 55.21% revenue share in 2025.

- By product, therapeutic drugs commanded 5.12% CAGR to 2031, whereas diagnostic kits and devices held 35.32% share of the male infertility market size in 2025.

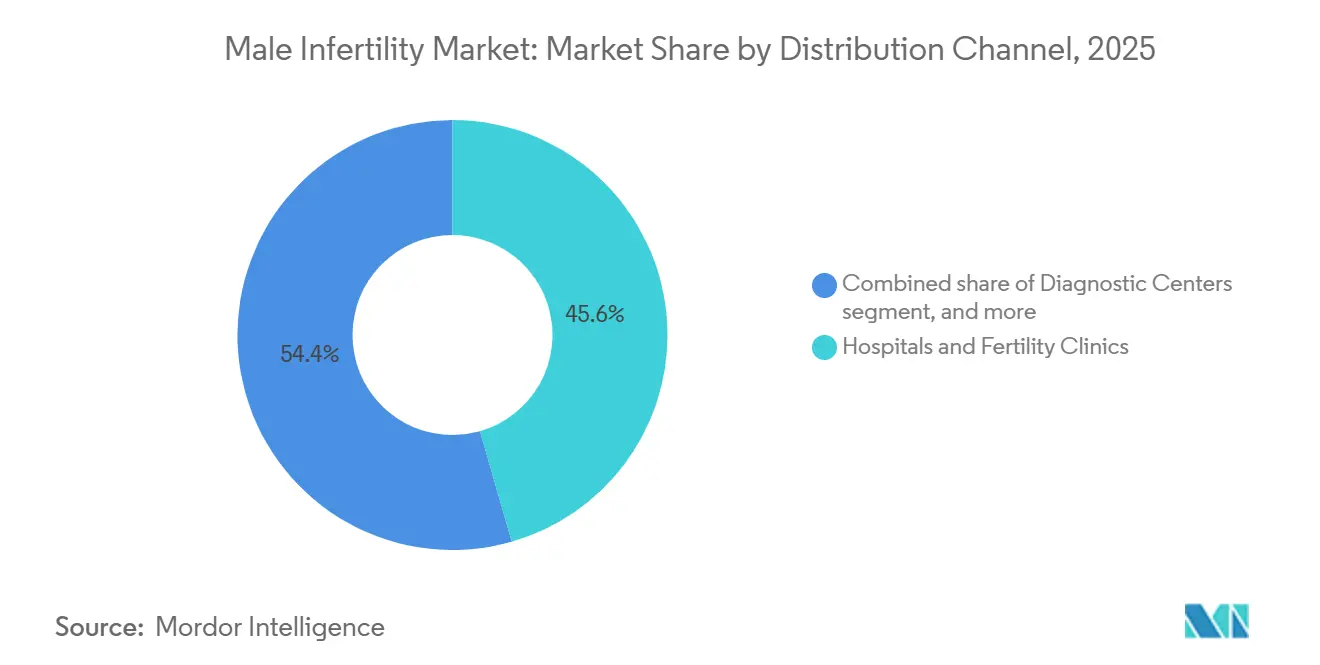

- By distribution channel, at-home testing and direct-to-consumer platforms are expanding at a 6.98% CAGR, outpacing the 45.56% share captured by hospitals and fertility clinics in 2025.

- By end-user, fertility clinics held 52.15% of 2025 revenue, whereas home-care users are forecast to post a 6.88% CAGR to 2031.

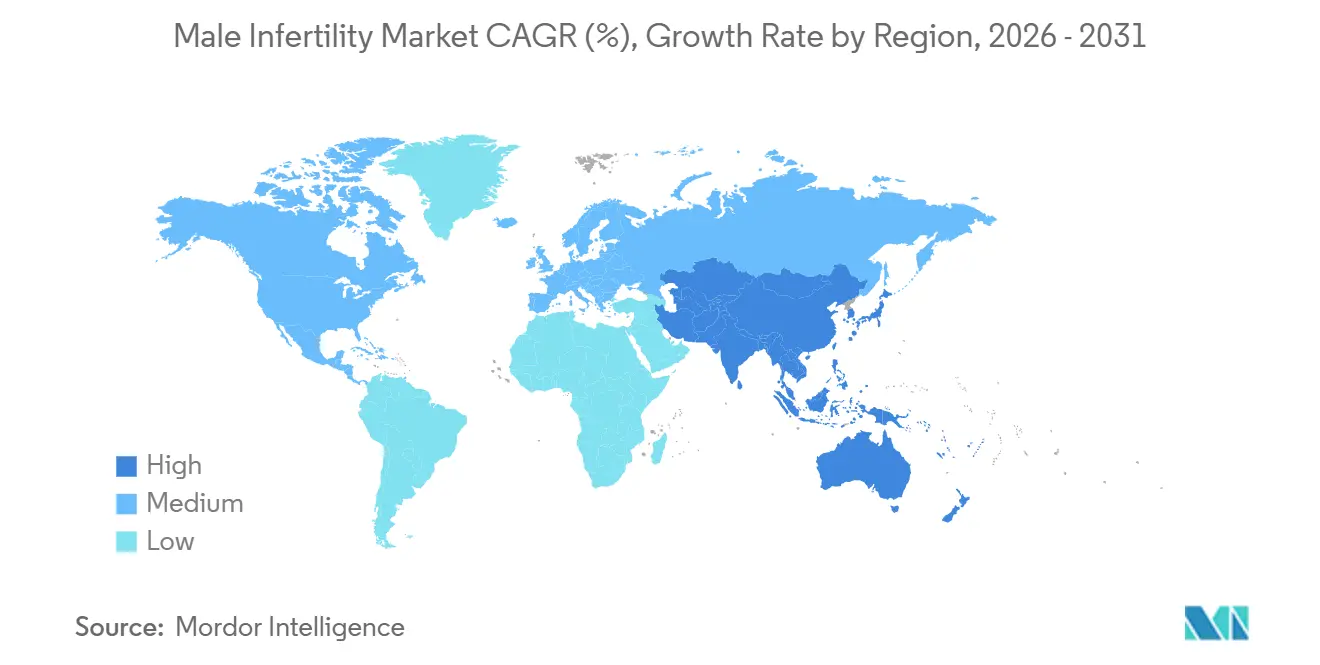

- By geography, Asia-Pacific is projected to post the quickest regional CAGR at 5.68% through 2031, surpassing North America’s 38.25% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Male Infertility Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global infertility prevalence in men | +0.8% | Global, with higher burden in South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Growth of employer-funded fertility benefits | +0.6% | North America and Western Europe | Medium term (2-4 years) |

| Rapid adoption of at-home digital semen testing | +0.5% | North America and urban Asia-Pacific | Short term (≤ 2 years) |

| AI-enabled sperm selection improving ART success | +0.4% | High-volume IVF centers worldwide | Medium term (2-4 years) |

| Government infertility-insurance mandates in new geographies | +0.5% | China, India and select European markets | Medium term (2-4 years) |

| Pipeline gene- and cell-based therapies for spermatogenic failure | +0.3% | Clinical trial hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Infertility Prevalence in Men

Meta-analysis confirms sperm concentration has fallen 1.2% yearly since 1973 and the decline accelerated after 2000 across Africa, Asia and South America. Environmental endocrine disruptors and lifestyle factors such as obesity are linked to poorer motility and DNA integrity, while the median paternal age now exceeds 32 years in most OECD nations. The wider age window for first-time fatherhood overlaps cumulative toxicant exposure, enlarging the male infertility market. Diagnosis still trails prevalence because stigma delays testing by three to five years in many countries.

Growth of Employer-Funded Fertility Benefits

A quarter of large United States employers paid for in-vitro fertilization by late 2024 and federal guidance issued in 2025 clarified that certain diagnostics are excepted benefits under the Affordable Care Act, removing regulatory ambiguity[1]U.S. Department of Labor, “Fertility Benefits as Excepted Benefits,” dol.gov. Plans usually cap lifetime benefits between USD 15,000 and USD 25,000, insufficient for multiple cycles, and often exclude advanced male diagnostics, pushing out-of-pocket spending. European companies are following Germany’s model of partial reimbursement, encouraging platform providers to negotiate bundled laboratory services, which realigns referral patterns and raises the profile of male factor testing.

Rapid Adoption of At-Home Digital Semen Testing

The FDA cleared the YO Home Sperm Test in 2024 with 97% correlation to computer-assisted laboratory systems and approved the LensHooke X12 PRO in 2025, enabling AI-based morphology scoring in under ten minutes. At-home kits lower embarrassment barriers; studies in South Asia show 68% of men cite shame as the main deterrent to clinic-based collection. Cash pricing of USD 50–150 makes the product affordable to younger urban users, though insurance coverage remains scarce. The European Union’s In Vitro Diagnostic Regulation imposes stricter validation, delaying several United States devices from entering that market until 2027.

AI-Enabled Sperm Selection Improving ART Success

Machine-learning algorithms trained on morphology, motility and fragmentation datasets outperformed embryologist assessment by 14 percentage points in a 2024 multicenter study. Systems such as Hamilton Thorne SiD cut intracytoplasmic sperm injection preparation time by 30% and early clinic audits suggest 8-12% gains in live birth rates. Adoption is highest in clinics running more than 1,000 cycles per year because the equipment costs USD 80,000–150,000. Reimbursement remains blended into cycle fees, but demonstrable pregnancy gains support premium pricing by 2028.

Restraints Impact Analysis of Male Infertility Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket costs and uneven reimbursement | -0.7% | United States and lower-middle-income countries | Medium term (2-4 years) |

| Limited specialist workforce and laboratory infrastructure | -0.5% | Sub-Saharan Africa, South Asia and Latin America | Long term (≥ 4 years) |

| Social stigma deterring male testing | -0.4% | Middle East, South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Absence of globally standardized advanced diagnostic protocols | -0.3% | Worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Costs and Uneven Reimbursement

In the United States a single intracytoplasmic sperm injection cycle costs USD 15,000–30,000, and fewer than 20% of commercial plans pay the full amount[2]American Society for Reproductive Medicine, “IVF Cost and Insurance Coverage Data,” asrm.org. Advanced male diagnostics add USD 1,000–2,500 and are seldom reimbursed. Public systems in France or Israel fund most ART, while India covers fewer than 10% of eligible couples. The funding gap forces 42% of couples into debt greater than USD 10,000, and 28% abandon therapy altogether.

Limited Specialist Workforce and Laboratory Infrastructure

Sub-Saharan Africa has under 200 board-certified andrologists for 1.2 billion residents. India’s 2021 regulations require every clinic to employ an embryologist, but 38% of registered centers failed ISO 15189 audits in 2025. Equipment cost compounds the problem; a computer-assisted semen analysis system runs USD 25,000–80,000, which exceeds budgets for most rural facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Male Infertility Market Segment Analysis

By Test Type:

Genetic Panels Gain Ground as Precision Diagnostics MatureConventional semen analysis held 42.18% sector revenue in 2025 yet the sub-segment of genetic and epigenetic panels is growing at 5.22% CAGR through 2031, outpacing all other tests. Falling sequencing costs now allow identification of Y-chromosome deletions or CFTR variants in under 48 hours for less than USD 1,000. Computer-assisted systems equipped with AI tracking reduce technician variability and push laboratories toward standardized protocols. DNA fragmentation assays, although unstandardized today, are adopted in clinics managing recurrent implantation failure, a pattern that hints at future reimbursement when ISO guidance arrives in 2027. Oxidative stress testing and acrosome reaction assays remain niche, limited to research settings. The male infertility market therefore continues to hinge on basic microscopy while transitioning toward molecular diagnostics that promise higher predictive power.

Laboratory-developed genetic tests now fall under the United States Food and Drug Administration’s May 2024 rule that expands pre-market review, increasing compliance costs for small stand-alone centers. National health systems diverge on coverage; France reimburses genetic workups after two failed IVF attempts, while most U.S. plans demand abnormal conventional results first, delaying access. These discrepancies influence the male infertility market size for advanced diagnostics, with Asia-Pacific labs adopting multiplex panels faster due to large urban patient pools and commercial pay models.

By Treatment:

Medication Gains as Hormonal Pathways Are RevisitedAssisted reproductive technology commanded 55.21% of segment revenue in 2025 because intracytoplasmic sperm injection is applied in more than 70% of global IVF cycles. Medication and hormone therapy, however, is expanding at 4.65% CAGR as urologists prescribe clomiphene citrate or letrozole to men with idiopathic oligospermia. A 2024 randomized trial showed clomiphene improved concentration by 8.4 million/mL and led to natural pregnancy in 32% of partners. Recombinant follicle-stimulating hormone remains limited to hypogonadotropic cases but biosimilars are reducing prices in Europe.

Microsurgical varicocelectomy retains a role for clinically palpable lesions, yet American Urological Association guidelines of 2024 limit surgery for subclinical cases. Lifestyle interventions and antioxidant supplements stay fragmented with limited high-quality evidence. Pipeline gene therapy candidates may shift the male infertility market share beyond 2030 if efficacy and safety hold, but current uptake is confined to clinical trials.

By Product:

Therapeutic Drugs Accelerate on Pipeline MomentumDiagnostic kits and devices accounted for 35.32% of 2025 revenue because semen analysis remains foundational. Therapeutic drugs are forecast to grow at 5.12% CAGR driven by expanded off-label clomiphene use and early gene-editing candidates advancing in trials. United States sales of clomiphene for male indications exceeded USD 120 million in 2024. Recombinant FSH biosimilars entering Europe in 2025 are increasing affordability.

Equipment for assisted reproduction such as micromanipulators, microfluidic sperm sorters and time-lapse incubators stays critical as cycle numbers rise. Vitrolife EmbryoScope units, which pair incubation with AI-based embryo ranking, command premiums of about USD 150,000 yet clinics justify the spend by citing higher pregnancy rates. Consumables pricing remains resilient, creating annuity-style revenue within the male infertility market.

By Distribution Channel:

DTC Platforms Disrupt Traditional Referral PathwaysHospitals and fertility clinics still generated 45.56% of 2025 channel revenue because they house operating theaters and high-complexity laboratories, but at-home testing and direct-to-consumer platforms are growing at 6.98% CAGR through 2031. Legacy, Posterity Health and similar brands combine mail-in semen kits, cryostorage and tele-andrology consults, reducing average time from concern to first test by six weeks. The YO Home Sperm Test clearance validated DTC diagnostics and triggered product launches with AI morphology scoring.

Diagnostic centers maintain relevance through physician referrals, while online pharmacies bundle supplements and hormone prescriptions. Europe’s IVDR slows DTC device entry, creating an uneven global landscape where North America leads adoption and regulatory certainty enlarges the male infertility market.

By End User:

Home-Care Users Surge as Convenience Trumps StigmaFertility clinics represented 52.15% of end-user spending in 2025, yet home-care users are advancing at 6.88% CAGR. Men under 35 accounted for two-thirds of mail-in kit purchases in 2024, responding to privacy, speed and bundled cryopreservation priced below hospital programs. At-home collection cuts appointment backlogs and mitigates embarrassment that previously delayed diagnosis by several months.

Hospitals still manage complex surgeries and high-risk cases, but public laboratories face six-to-nine-month queues in Brazil and parts of India, pushing middle-income patients into private channels. The absence of global standards governing sample collection during shipping remains a risk; however, platform investment in temperature-controlled logistics is raising confidence and enlarging the male infertility market size for home-based services.

Geography Analysis

North America Male Infertility Market

North America generated 38.25% of global revenue in 2025, supported by eleven United States states and the District of Columbia mandating infertility coverage and more than 450 Society for Assisted Reproductive Technology registered clinics. Rising employer benefits and early adoption of AI-enabled equipment sustain stable growth but reimbursement gaps restrain broader male testing.

APAC Male Infertility Market

Asia-Pacific is the fastest growing region at 5.68% CAGR through 2031. China cut review timelines for imported ART devices to nine months in 2024 and several provinces added male diagnostics to provincial insurance lists[3]National Medical Products Administration China, “Accelerated Approval Pathways for ART Devices,” nmpa.gov.cn. India’s ART Act spurred a 22% uptick in licensed centers by 2025 yet public funding remains limited, steering demand to private providers. Urban centers in South Korea, Japan and Australia add volume through aging parental demographics, helping the male infertility market outpace global averages.

EMEA and LATAM Male Infertility Market

Europe stands as the second largest region; France now funds ART for single women and same-sex couples, boosting partner screening volumes, while Germany reimburses 50% of ART cost for married couples under 40. The Middle East and Africa trail other regions due to workforce shortages; South Africa handles over 60% of Sub-Saharan cycles, and Dubai clinics draw international clients. Latin America sees growing cross-border traffic as patients bypass limited public capacity in Brazil and Argentina by traveling to the United States.

Competitive Landscape

The male infertility market remains moderately fragmented. Halotech DNA, Vitrolife, and CooperSurgical lead equipment, but none had a major global revenue. Hamilton Thorne added advanced imaging through the CODA acquisition in 2024, reducing prep times by 30% and offering decision-support features. Diagnostic chains LabCorp and Quest dominate conventional semen analysis volumes but face pressure from at-home entrants offering 30–40% cheaper bundled services.

Pharmaceutical portfolios are thin. Merck KGaA and Ferring sell recombinant hormones for hypogonadotropic hypogonadism, yet widespread off-label clomiphene use dilutes branded sales. Biosimilar follicle-stimulating hormone approval in Europe during 2025 is adding price competition. Venture-backed startups in gene therapy secured USD 80 million during 2025, aiming to commercialize curative treatments after 2030 and potentially displace chronic drug regimens.

Technology adoption differentiates clinics; facilities that implement AI sperm selection systems report 8–12% higher live birth rates, enabling premium cycle pricing and stronger patient inflow. ISO 15189 accreditation is emerging as a quality mark; accredited laboratories command 15–20% higher fees, yet fewer than 40% of centers presently meet the standard, giving early movers a commercial edge.

Male Infertility Industry Leaders

Merck KGaA

Vitrolife AB

CooperSurgical

Ferring International

Halotech DNA

- *Disclaimer: Major Players sorted in no particular order

Male Infertility Market Companies Covered in this Report

- AdvaCare

- Andrology Solutions

- Aytu BioScience

- Caerus Biotech

- CinnaGen

- The Cooper Companies

- Ferring International

- Genea Biomedx

- Halotech DNA

- Hamilton Thorne

- Intas Pharmaceuticals

- LabCorp

- Legacy

- Merck

- Microptic S.L.

- MotilityCount (SwimCount)

- Posterity Health

- Vitrolife

- Zydus Lifesciences

Recent Industry Developments in Male Infertility Market

- January 2026: Legacy launched the first at-home semen analysis that delivers a full clinical motility profile, closing a diagnostic gap that previously limited mail-in testing utility.

- August 2025: Researchers at the University of Hong Kong’s LKS Faculty of Medicine unveiled an AI model able to pinpoint sperm with fertilization potential with high accuracy, promising better embryo outcomes.

Male Infertility Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global male infertility market as every dollar earned from laboratory diagnostics, prescription medicines, microsurgical procedures, and assisted reproductive technologies that detect or treat male-factor infertility, clinically confirmed when conception fails after twelve months of regular unprotected intercourse.

Scope Exclusion: Spending on female infertility, generic obstetric tools, and broad wellness apps sits outside this study.

Segments Covered in This Report

- By Test Type

- Conventional Semen Analysis

- Computer-Assisted Semen Analysis (CASA)

- DNA Fragmentation Tests

- Oxidative Stress Analysis

- Genetic & Epigenetic Panels

- Other Test Types

- By Treatment

- Medication & Hormone Therapy

- Assisted Reproductive Technology (IVF, ICSI)

- Varicocele & Microsurgical Procedures

- Lifestyle, Supplements & Counselling

- By Product

- Diagnostic Kits & Devices

- Therapeutic Drugs

- ART Equipment & Disposables

- By Distribution Channel

- Hospitals & Fertility Clinics

- Diagnostic Centres

- At-home Testing / DTC Platforms

- Online & Retail Pharmacies

- By End User

- Fertility Clinics

- Hospitals

- Diagnostic Laboratories

- Home-care Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed reproductive endocrinologists, andrology-lab heads, payor medical officers, and at-home kit suppliers across North America, Europe, and Asia-Pacific. These talks clarified DNA-fragmentation uptake, routine sperm-retrieval tariffs, and early AI-enabled CASA adoption, tightening assumptions flagged during desk work.

Desk Research

We began by tracing prevalence, care routes, and price bands with open data from WHO, CDC, UN Population Division, and regional ART registries. Investor filings and peer-reviewed papers in Human Reproduction explained outcome trends, while customs dashboards highlighted trade flows.

Our team then reviewed Questel patent feeds, D&B Hoovers financials, and Factiva news to follow kit launches, lab automation, and company revenue splits. The sources named are illustrative; many other public records supported evidence gathering and cross-checks.

Market-Sizing & Forecasting

We start with each country's males aged twenty to forty-nine, apply validated infertility prevalence, then multiply by an average care bundle linking semen analyses, male-factor ART cycles, varicocele surgeries, hormone months, and supplement spends. Supplier roll-ups and spot tariff audits add bottom-up checks. Multivariate regression on GDP per capita, private-insurance reach, ART success rates, smoking prevalence, and median paternal age projects 2026-2031 values, while scenario analysis probes policy or technology shocks.

Data Validation & Update Cycle

Outputs clear variance screens and multi-analyst review, then refresh every year or sooner when guideline or reimbursement shifts surface, so clients receive the latest view.

How Mordor Intelligence's Male Infertility Market Size Compares to Other Published Estimates

Published estimates differ because publishers vary product lists, care stages, currencies, or refresh rates.

Our disciplined scope, balanced base year, and annual revisit curb drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.99 B (2025) | Mordor Intelligence | - |

| USD 4.21 B (2024) | Global Consultancy A | Excludes Latin America; uses list prices |

| USD 4.63 B (2025) | Boutique Advisory B | Combines male and unexplained drug revenue |

| USD 3.59 B (2024) | Trade Journal C | Small survey base; biennial refresh |

This comparison shows that our transparent variables, timely refresh, and reproducible steps give decision-makers a repeatable figure they can trust.

Key Questions Answered in the Report

How big is the male infertility market in 2026?

The male infertility market size stands at USD 4.25 billion in 2026.

What is the forecast CAGR for male infertility between 2026 and 2031?

Revenue is expected to rise at a 3.65% CAGR through 2031.

Which test type is growing fastest for male factor diagnosis?

Genetic and epigenetic panels lead with a projected 5.22% CAGR to 2031.

Why are at-home semen tests gaining popularity?

FDA-cleared smartphone assays reduce embarrassment, deliver rapid results and cost USD 50-150 per kit.

Which region is projected to grow quickest?

Asia-Pacific is forecast to post the highest regional CAGR at 5.68% through 2031.

What limits broader adoption of advanced male diagnostics?

Lack of global test standards and uneven reimbursement keep out-of-pocket costs high.

Page last updated on: