Server Storage Area Network Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

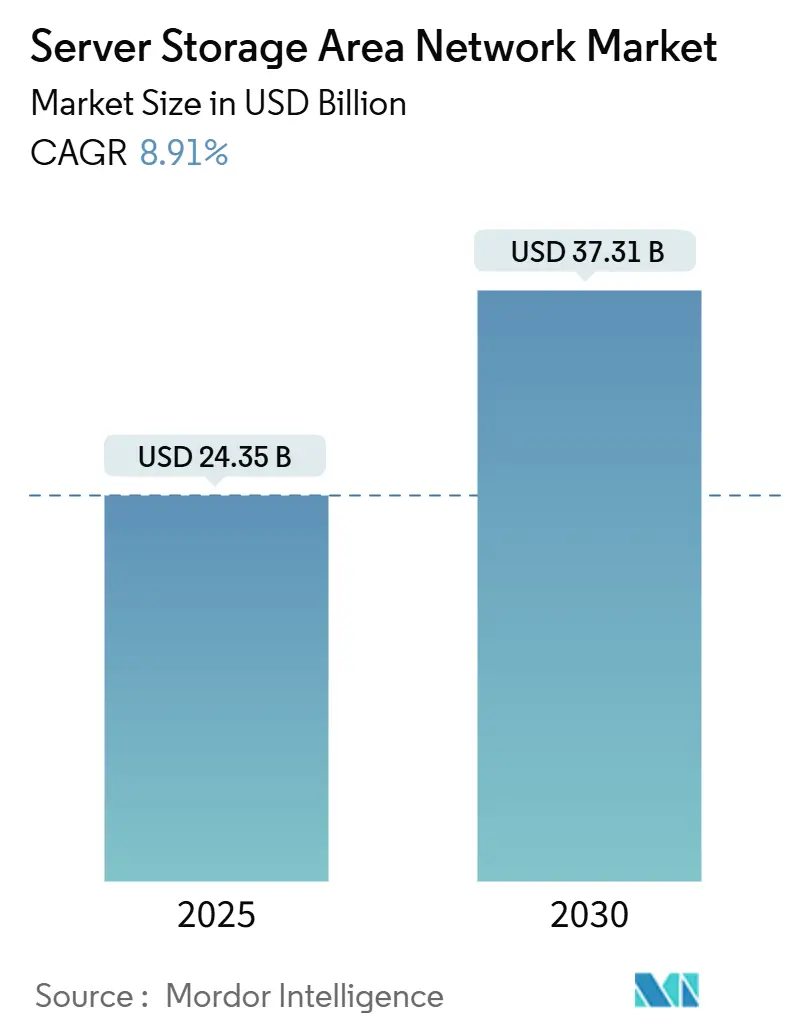

| Market Size (2025) | USD 24.35 Billion |

| Market Size (2030) | USD 37.31 Billion |

| Growth Rate (2025 - 2030) | 8.91% CAGR |

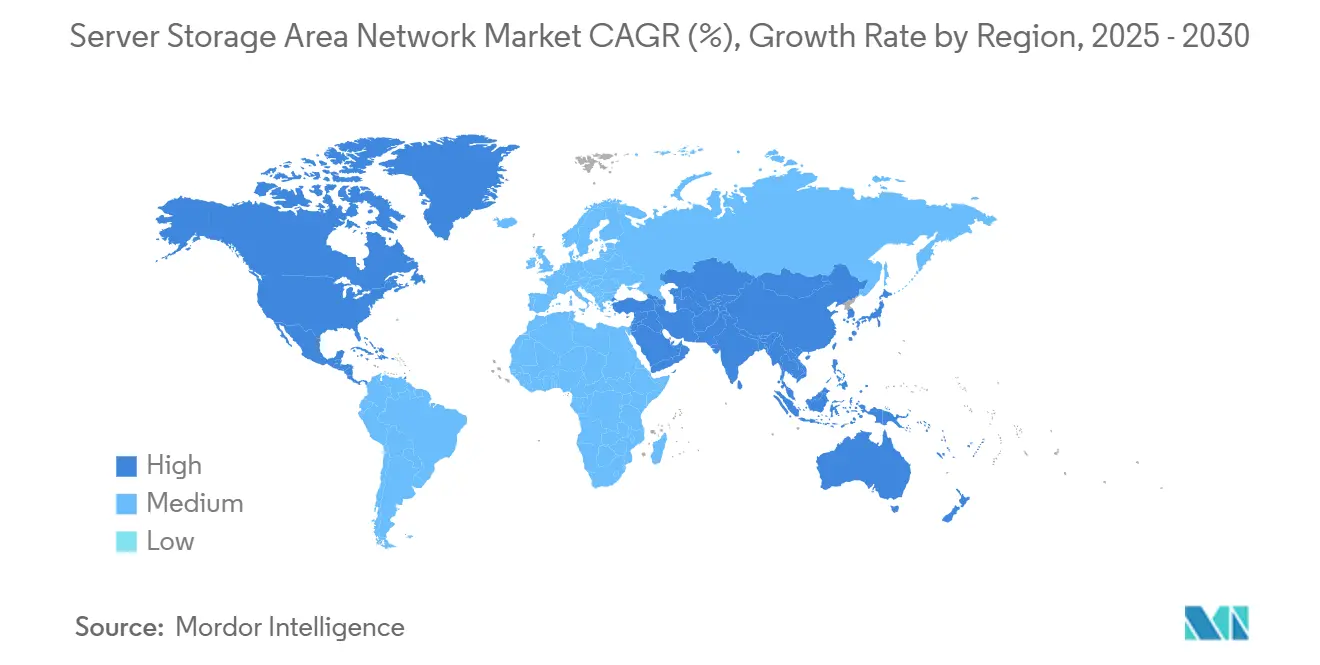

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Server Storage Area Network Market Analysis by Mordor Intelligence

The Server Storage Area Network market size stood at USD 24.35 billion in 2025 and is forecast to reach USD 37.31 billion by 2030, advancing at an 8.91% CAGR over the period. Strong hyperscale data-center investment, wider AI workload adoption and rapid transition toward software-defined, disaggregated architectures are the primary forces behind this expansion. Vendors are blending traditional block-based arrays with NVMe-over-Fabrics, computational storage and CXL-enabled memory pooling to achieve microsecond-level latency while maintaining linear throughput scaling. At the same time, enterprises are moving from monolithic purchases to consumption-based services, which transfers budget risk, shortens refresh cycles and speeds storage innovation. Pricing volatility in NAND flash and optics remains a near-term pressure, yet most buyers are absorbing the cost by extending pay-as-you-grow contracts rather than curbing deployment velocity. Strategic M&A-such as HPE-Juniper and IBM-HashiCorp-signals an industry pivot toward AI-native networking and integrated orchestration stacks that blur the line between compute and storage domains.

Key Report Takeaways

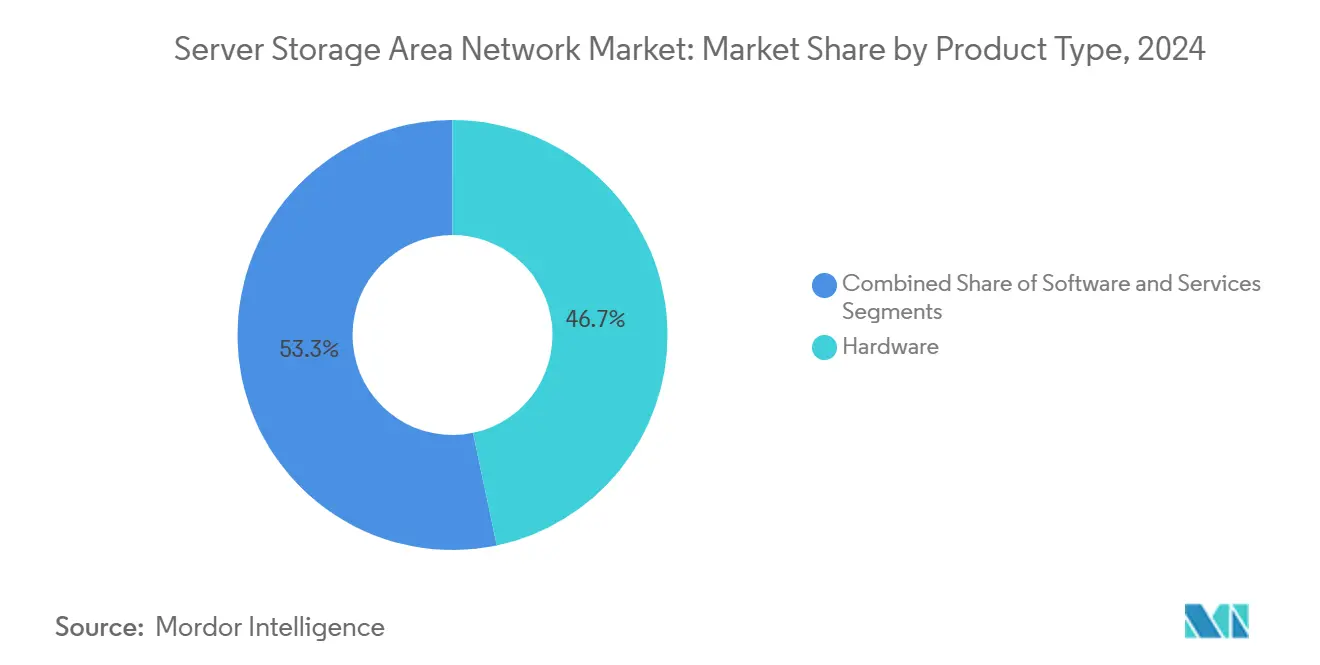

- By product type, hardware held 46.71% of Server Storage Area Network market share in 2024, while services are poised for the fastest 11.23% CAGR through 2030.

- By technology, fibre channel led with 39.87% revenue share in 2024; NVMe-over-Fabrics is projected to expand at a 10.67% CAGR to 2030.

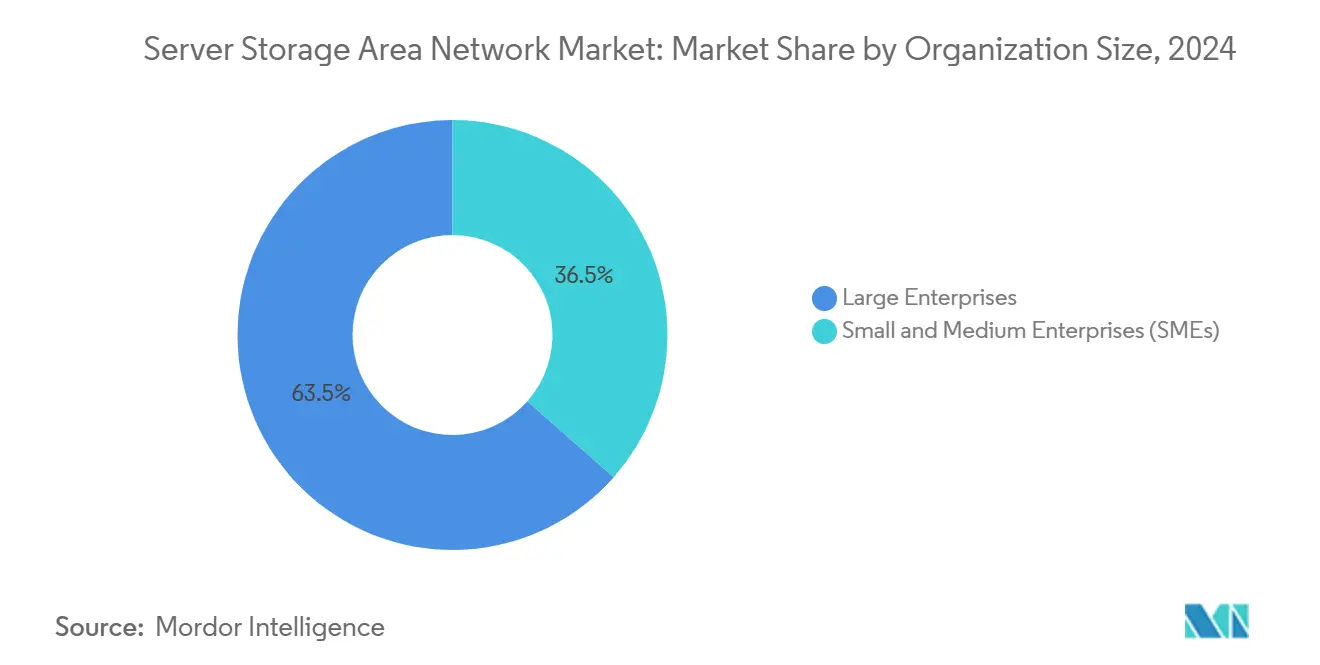

- By organization size, large enterprises commanded 63.49% of the Server Storage Area Network market size in 2024, whereas SMEs are growing the fastest at a 12.38% CAGR.

- By end-user industry, BFSI captured 21.67% revenue share in 2024; cloud service providers are forecast to record the highest 9.82% CAGR through 2030.

- By geography, North America accounted for 36.82% of the Server Storage Area Network market size in 2024, while Asia-Pacific is advancing at a 9.53% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Server Storage Area Network Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid hyperscale data-center build-outs | +2.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Shift to software-defined and hyper-converged storage | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Adoption of NVMe-over-Fabrics for ultra-low latency | +1.9% | North America and Europe | Short term (≤ 2 years) |

| Emergence of computational storage off-loads | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Edge-localized micro-SANs for sovereign data control | +0.8% | Europe and Asia-Pacific | Medium term (2-4 years) |

| CXL-based memory pooling | +0.3% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Hyperscale Data-Center Build-Outs

Cloud providers committed more than USD 676 billion to new campuses during early 2025, accelerating demand for petabyte-scale arrays capable of feeding racks that approach 1.4 exaFLOPS of GPU compute. Amazon earmarked USD 30 billion for sites in Pennsylvania and North Carolina, Google pledged USD 25 billion tied to PJM grid upgrades, and Microsoft budgeted USD 80 billion for fiscal-year builds. These projects require storage fabrics that ingest, checkpoint and stream AI data sets with sub-ten-microsecond latency at rack scale. Vendors are responding with tightly integrated compute-storage nodes that flatten tiering, pool CXL-attached memory and eliminate east-west congestion. The spending surge also shifts pricing power to buyers, pushing suppliers to bundle lifecycle management services and energy-efficient controllers to win multiyear refresh lock-ins. Collectively, the capital wave contributes a 2.8-percentage-point uplift to the Server Storage Area Network market CAGR.

Shift to Software-Defined and Hyper-Converged Storage

Enterprises facing macroeconomic uncertainty and skill shortages pivoted toward appliance-based hyper-converged infrastructure, achieving up to 40% hardware savings and shrinking backup windows from four hours to under one hour in deployments such as Saudi German Health’s Nutanix rollout. [1]Nutanix Communications, “Saudi German Health Advances Digital Healthcare Services with Nutanix,” Nutanix, nutanix.comSeventy-five percent of new rollouts now use vendor-integrated nodes that merge compute, storage and networking, allowing small IT teams to administer vast clusters through a single GUI. These systems also expose RESTful APIs, enabling policy-based automation that dynamically extends volumes for AI inference spikes. Financial models have shifted from perpetual licenses to subscription, smoothing cash flow and deepening vendor lock-in. As a result, software-first strategies are adding 2.1 percentage points to the Server Storage Area Network market CAGR.

Adoption of NVMe-over-Fabrics for Ultra-Low Latency

Financial institutions such as Toss Bank process up to 9,000 transactions per second on Pure Storage FlashArray systems running NVMe-oF, realizing 83% capacity savings through deduplication while maintaining microsecond latency. [2]Pure Storage Team, “Toss Bank Drives Financial Services with FlashArray,” Pure Storage, purestorage.com Fibre Channel continues to dominate in brownfield sites owing to proven reliability, but RDMA-over-Converged-Ethernet is the protocol of choice for greenfield AI clusters that require deterministic performance. Consistency outweighs peak bandwidth; enterprises value sub-20-microsecond tail latency more than 100 GB/s burst rates. Adoption hurdles-chiefly skills gaps in tuning RDMA congestion control-are easing as switch vendors pre-bundle lossless configurations. The performance dividend raises the market growth rate by 1.9 percentage points.

Emergence of Computational Storage Off-Loads

According to 2025 performance benchmarks, CXL-compliant drives with embedded data-plane accelerators outperform traditional PCIe expanders, achieving a 10.9 times boost in throughput and reducing latency by 5.4 times.[3]Research Contributors, “From Block to Byte: Transforming PCIe SSDs with CXL Memory Protocol,” arXiv, arxiv.org Early enterprise pilots offload preprocessing for AI inference, including filtering, compression, and tokenization, directly within SSD controllers. This architecture reduces DIMM footprint, lowers PCIe hop counts, and shrinks rack-level power draw. Regulatory bodies are beginning to codify logging and observability requirements because compute now occurs inside the storage subsystem, influencing ISO and NIST guidance. Although commercial adoption is still in its early stages, the combined visibility of roadmaps and performance gains collectively add 1.2 percentage points to long-term growth.

Restraints Impact Analysis of Server Storage Area Network Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX of all-flash arrays | –1.4% | Global, SME-heavy regions | Short term (≤ 2 years) |

| Multi-vendor interoperability and legacy lock-in | –0.9% | Global, mature markets | Medium term (2-4 years) |

| Skills gap in RDMA / NVMe-oF configuration | –0.6% | Emerging markets | Medium term (2-4 years) |

| ASIC and optical-transceiver supply-chain risks | –0.4% | Global, Asia-centric fabs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX of All-Flash Arrays

NAND vendors cut wafer starts by up to 25% during 2024, but surging AI demand reversed the glut and pushed enterprise SSD prices more than 10% higher in March 2025. A new NVMe-oF fabric with redundant 400 GbE optics can cost four to six times more than a like-for-like 16 Gb FC refresh, forcing CFOs to stage deployments or adopt storage-as-a-service. Although payback periods can drop below three months when operational savings are tallied-as in a U.S. steel manufacturer’s Celona-enabled modernization-liquidity constraints remain acute for cash-strapped SMEs. Consequently, elevated CAPEX shaves 1.4 percentage points from the Server Storage Area Network market CAGR in the near term.

Multi-Vendor Interoperability and Legacy Lock-In

Enterprises running mixed Fibre Channel, iSCSI and NVMe-oF fabrics report operational friction when layering new protocols onto legacy zoning and LUN-masking schemes. Proprietary management suites complicate orchestration across platforms, while divergent metadata handling can break snapshot consistency during migration. Europe’s 2025 Data Act further mandates workload portability, adding architecture rewrites for providers that cannot expose open APIs. These challenges restrain adoption by 0.9 percentage points until unified control planes mature and standards crystallize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Server Storage Area Network Market Segment Analysis

By Product Type:

Services Drive Subscription-Model TransformationHardware remained the largest revenue contributor in 2024, capturing 46.71% of Server Storage Area Network market share as enterprises continued rolling out high-density NVMe shelves to feed GPU farms. The services line, however, is forecast to expand at an 11.23% CAGR as buyers flock to consumption contracts that convert capex to opex and guarantee evergreen upgrades. NetApp’s Keystone more than doubled total contract value to nearly USD 150 million during fiscal 2025, while Pure Storage’s Evergreen//One helped City National Bank spin up new environments without forklift refreshes. Vendors bundle ransomware warranties, power-use dashboards and proactive component replacement to de-risk adoption, positioning services as the strategic growth lever for the Server Storage Area Network market.

The pivot reflects broader IT procurement trends favoring predictability, labor off-load and sustainability reporting. Enterprises cite 20% lower total cost of ownership versus self-managed arrays once staffing, utility and floor-space savings are counted. Smaller firms view the model as an equalizer that grants access to Tier-1 features without specialized administrators. In parallel, software revenues rise steadily on the back of AI-driven analytics that automate tiering and anomaly detection. All told, the services trajectory anchors long-run resilience of the Server Storage Area Network market.

By Technology Type:

NVMe-oF Disrupts Fibre Channel DominanceFibre Channel still delivered 39.87% of 2024 revenue thanks to entrenched mission-critical workloads, yet its growth is flattening as performance-hungry AI and analytics choose NVMe-oF fabrics posting a 10.67% CAGR. RDMA-over-Converged-Ethernet eliminates slow Serialized SCSI translation, directly accessing NVMe namespaces and slashing latency below ten microseconds. Hyperscalers further shrink path length by deploying controller-free, pooled storage blades attached via CXL switches. Hyper-converged/vSAN nodes grow in edge and departmental sites where simplicity trumps peak speed, while iSCSI lingers only in cost-sensitive archives.

The technology shift places transceiver and ASIC vendors under supply stress, lengthening lead times to up to 18 months for 800 GbE optics. Vendors hedge by qualifying multiple optic manufacturers and pre-certifying auto-negotiation firmware to avoid troubleshooting delays. As interoperability stabilizes, enterprises expect NVMe-oF pricing to drop 15-20% by 2027, further eroding Fibre Channel’s installed base. Consequently, NVMe-oF is set to emerge as the de-facto backbone of the Server Storage Area Network market.

By Organization Size:

SMEs Embrace Cloud-Native StorageLarge enterprises controlled 63.49% of the Server Storage Area Network market size in 2024 by virtue of their sprawling data estates and regulatory burdens that favor on-premises arrays. Yet the SME cohort is registering a 12.38% CAGR as turnkey hyper-converged appliances and vendor-operated services remove the need for deep storage expertise. Shimane Bank’s adoption of Lenovo ThinkSystem nodes underscores how smaller institutions can modernize core banking platforms without dedicated storage administrators.

The democratization trend accelerates as suppliers roll out five-node starter bundles bundled with 36 months of onsite support and ransomware protection. Cloud portals allow non-specialists to spin up volumes, set snapshot policies and monitor compliance from a single pane of glass. Bundled financing, zero-percent leasing and built-in capacity scaling encourage SMEs to leapfrog directly to modern fabrics. Over time, the rising SME contribution diversifies the customer base of the Server Storage Area Network market, making growth less susceptible to large-enterprise budget cycles.

By End-User Industry:

Cloud Providers Lead Infrastructure EvolutionBFSI retained the highest revenue share at 21.67% in 2024, driven by real-time settlement, fraud analytics and stringent record-retention mandates. Nonetheless, cloud service providers exhibit the strongest 9.82% CAGR thanks to relentless AI infrastructure rollouts that demand object, block and memory-class storage at hyperscale density. Providers customize controllers, deploy computational storage and pre-warm data pipelines to cut GPU idle time.

Healthcare and life sciences accelerate adoption of flash arrays to meet imaging and genomic sequencing throughput. Chang Gung Memorial Hospital achieved a seven-fold compute efficiency uplift using Pure Storage AIRI, illustrating the patient-care upside. Manufacturing embraces edge-localized micro-SANs that support predictive maintenance with sub-millisecond feedback loops. Media and entertainment firms blend NVMe-oF arrays with high-bandwidth object storage to serve real-time rendering workloads, while public bodies favor on-prem and sovereign-cloud hybrids to honor residency laws. These sectoral nuances keep the Server Storage Area Network market exposed to multiple demand vectors.

Geography Analysis

North America Server Storage Area Network Market

North America’s 36.82% revenue share mirrors hyperscale concentration, aggressive AI-native build-outs and early adoption of NVMe-oF, computational storage and CXL memory pooling. U.S. players alone invested more than USD 676 billion during early 2025, with Amazon dedicating USD 100 billion to power-dense campuses across Pennsylvania and North Carolina. Canada adds growth through provincial incentives for carbon-neutral colocation, while Mexico gains from near-shoring and automotive digitization. Government funding for edge devices in defense and public safety further widens market opportunity.

APAC Server Storage Area Network Market

Asia-Pacific’s 9.53% CAGR stems from maturing cloud ecosystems, thriving fintech hubs and strict data-residency frameworks. China’s Cybersecurity Law and Vietnam’s data-localization statutes oblige multinationals to operate in-country storage farms, boosting demand for hyper-converged vSAN clusters within sovereign clouds. Japan’s megabanks refresh Fibre Channel with NVMe-oF to meet transaction-time SLAs, whereas India’s public-sector banks migrate workloads to flash arrays to align with the Reserve Bank’s real-time settlement directives. South-east Asian telcos deploy micro-SANs at base-band hotel sites to reduce backhaul latency for video streaming and mobile gaming.

Europe Server Storage Area Network Market

Europe’s steady trajectory owes to compliance-driven refreshes and cross-border edge federations. The EU Data Act enforces interoperability, pushing providers to design open APIs and bidirectional migration toolkits. Germany and the Nordics prioritize energy-efficient arrays powered by renewable grids. France expands all-flash adoption within medical imaging repositories to meet patient data retention mandates. The United Kingdom invests in hyper-converged nodes to support AI research clusters tied to automotive and life-sciences consortia. Cumulatively, regional complexity and sovereignty concerns generate sustainable demand for the Server Storage Area Network market.

Competitive Landscape

The Server Storage Area Network market shows moderate concentration, with incumbents retaining scale advantages yet facing pressure from software-defined upstarts. Dell Technologies reported USD 12.1 billion in AI server backlog for Q1 FY 2026, pairing PowerEdge XE9785 with NVIDIA GB200 GPUs to anchor integrated compute-storage racks. Storage revenue rose 6%, lagging servers’ 16% pace, prompting heavier investment in APEX consumption models. NetApp hit USD 3.8 billion all-flash run-rate, leveraging ONTAP 9.14 and Keystone financing to grow wallet share. Pure Storage crossed USD 3.2 billion with 12% YoY growth, crediting Evergreen//One subscriptions and FlashBlade//S competitive wins.

HPE finalized a USD 14 billion Juniper acquisition, marrying Aruba’s campus portfolio with Juniper’s data-center switches to challenge Cisco and NVIDIA in AI fabrics. IBM closed a USD 6.4 billion HashiCorp deal to embed Terraform and Vault into Red Hat OpenShift, targeting hybrid orchestration. Lenovo’s planned buyout of Infinidat broadens its high-end enterprise storage, positioning to capture inflation-conscious buyers seeking premium capacity at lower TCO. Vendors also form alliances, such as Nutanix joined forces with Pure Storage to pre-validate mission-critical bundles, while NVIDIA launched an AI Data Platform reference stack with Dell, HPE and NetApp.

Differentiation themes include cyber-resilience (immutable snapshots, hardware-root-of-trust controllers), energy optimization (DPUs managing I/O off-load, liquid-cooled drive sleds) and AI workload orchestration. Channel programs evolve toward outcome-based SLAs, reflecting buyer demand for guaranteed throughput and latency. Collectively, the top five suppliers control roughly 55–60% of global revenue, keeping the market in a phase of dynamic but not hyper-fragmented competition.

Server Storage Area Network Industry Leaders

Dell Technologies Inc.

Hewlett Packard Enterprise Company

NetApp Inc.

Pure Storage Inc.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Server Storage Area Network Market Companies Covered in this Report

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- NetApp Inc.

- Pure Storage Inc.

- Huawei Technologies Co., Ltd.

- International Business Machines Corporation

- Hitachi Vantara LLC (Hitachi Ltd.)

- Fujitsu Limited

- Inspur Electronic Information Industry Co., Ltd.

- Super Micro Computer, Inc.

- Lenovo Group Limited

- Western Digital Corporation

- Seagate Technology Holdings plc

- NEC Corporation

- Cisco Systems, Inc.

- VMware, Inc.

- Nutanix, Inc.

- StorCentric, Inc.

- QSAN Technology, Inc.

- Infinidat Ltd.

Recent Industry Developments in Server Storage Area Network Market

- August 2025: SanDisk unveiled a 256 TB SSD aimed at AI inference clusters, slated for 2026 shipment.

- July 2025: HPE completed its USD 14 billion acquisition of Juniper Networks to build an AI-native networking portfolio.

- May 2025: Dell introduced PowerEdge XE9780 and XE9785 servers with NVIDIA Blackwell GPUs plus an expanded Dell AI Data Platform.

- May 2025: Nutanix and Pure Storage released an integrated stack combining Nutanix Cloud Infrastructure with Pure FlashArray.

Global Server Storage Area Network Market Report Scope

Segmentation Overview

| Hardware |

| Software |

| Services |

| Fibre Channel SAN |

| iSCSI SAN |

| Hyper-converged / vSAN |

| NVMe-oF SAN |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| IT and Telecom |

| Healthcare and Life-Sciences |

| Media and Entertainment |

| Cloud Service Providers |

| Government and Public Sector |

| Manufacturing |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Hardware | ||

| Software | |||

| Services | |||

| By Technology Type | Fibre Channel SAN | ||

| iSCSI SAN | |||

| Hyper-converged / vSAN | |||

| NVMe-oF SAN | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | ||

| IT and Telecom | |||

| Healthcare and Life-Sciences | |||

| Media and Entertainment | |||

| Cloud Service Providers | |||

| Government and Public Sector | |||

| Manufacturing | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Server Storage Area Network market in 2025, and how fast will it grow?

The market stands at USD 24.35 billion in 2025 and is projected to expand to USD 37.31 billion by 2030 at an 8.91% CAGR.

Which product segment is expanding the quickest?

Services, delivered via subscription and storage-as-a-service models, is growing at an 11.23% CAGR through 2030.

Why are hyperscalers critical to future demand?

Cloud providers committed more than USD 676 billion to new AI-ready data centers in early 2025, driving massive orders for ultra-low-latency storage fabrics.

What technology transition is replacing Fibre Channel in new deployments?

NVMe-over-Fabrics, particularly RDMA-over-Converged-Ethernet, is displacing Fibre Channel due to microsecond latency and linear scalability.

How are supply-chain pressures affecting pricing?

NAND flash and high-speed transceiver shortages pushed enterprise SSD prices up more than 10% in March 2025, lengthening lead times to as much as 18 months for critical optics.

Which region will post the fastest growth?

Asia-Pacific is expected to register a 9.53% CAGR through 2030, propelled by data-sovereignty regulations and expanding digital-economy initiatives.

Page last updated on: