Serial Device Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 326.5 Million |

| Market Size (2031) | USD 436.80 Million |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Serial Device Server Market Analysis by Mordor Intelligence

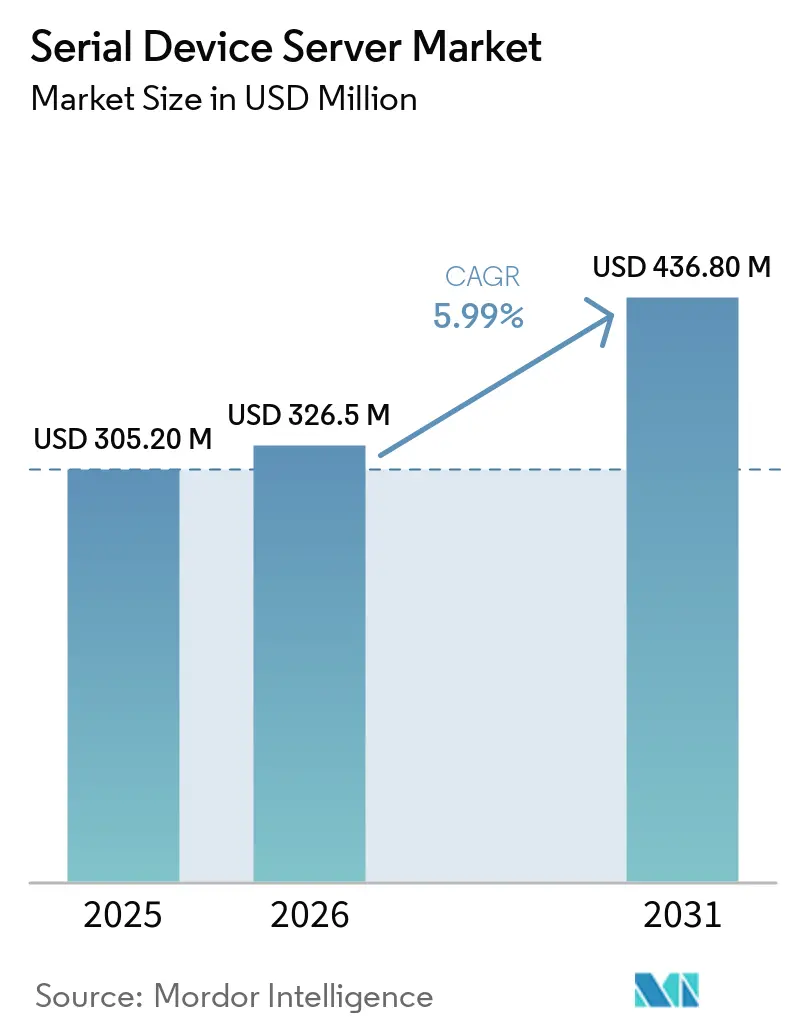

The serial device server market size is expected to increase from USD 326.50 million in 2026 to USD 436.80 million by 2031, growing at a CAGR of 5.99% over 2026-2031. Demand is rising as plant owners, utilities, and transport operators connect legacy RS-232, RS-422, and RS-485 equipment to modern Ethernet and cellular networks without replacing functional assets. Hardware refresh cycles in manufacturing and energy have shortened because security mandates such as NERC-CIP and IEC 62443 now treat unencrypted serial links as non-compliant. Vendors that certify to these standards secure preferred-vendor status, and pricing power follows. Asia-Pacific retrofit programs, North American cyber-security spending, and Europe’s rail-signal upgrades keep multi-port gateways in steady demand, while cellular options open remote oilfield and mining sites to predictive-maintenance analytics.

Key Report Takeaways

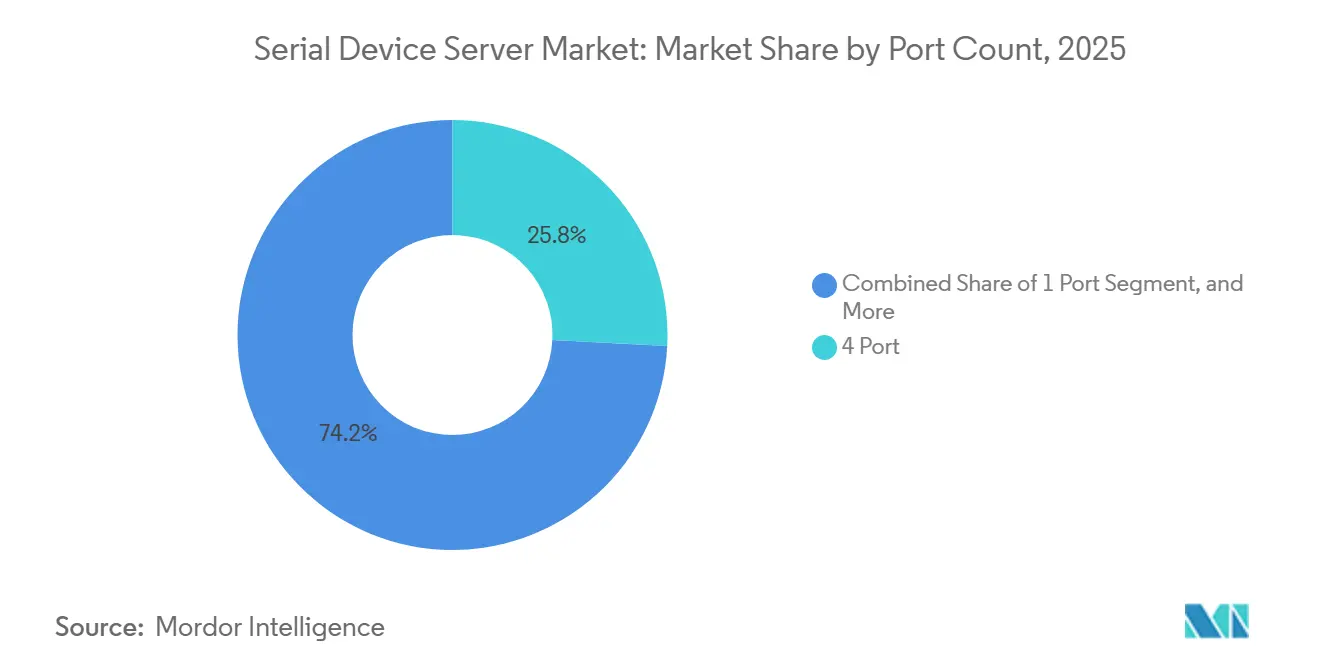

- By port count, 4-port devices led with 25.81% of the serial device server market share in 2025, and the 32-port-and-above segment will likely advance at a 7.80% CAGR through 2031.

- By connectivity, wired Ethernet accounted for 41.31% of revenue in 2025, while cellular gateways are likely to expand at 9.20% CAGR through 2031 in the serial device server market.

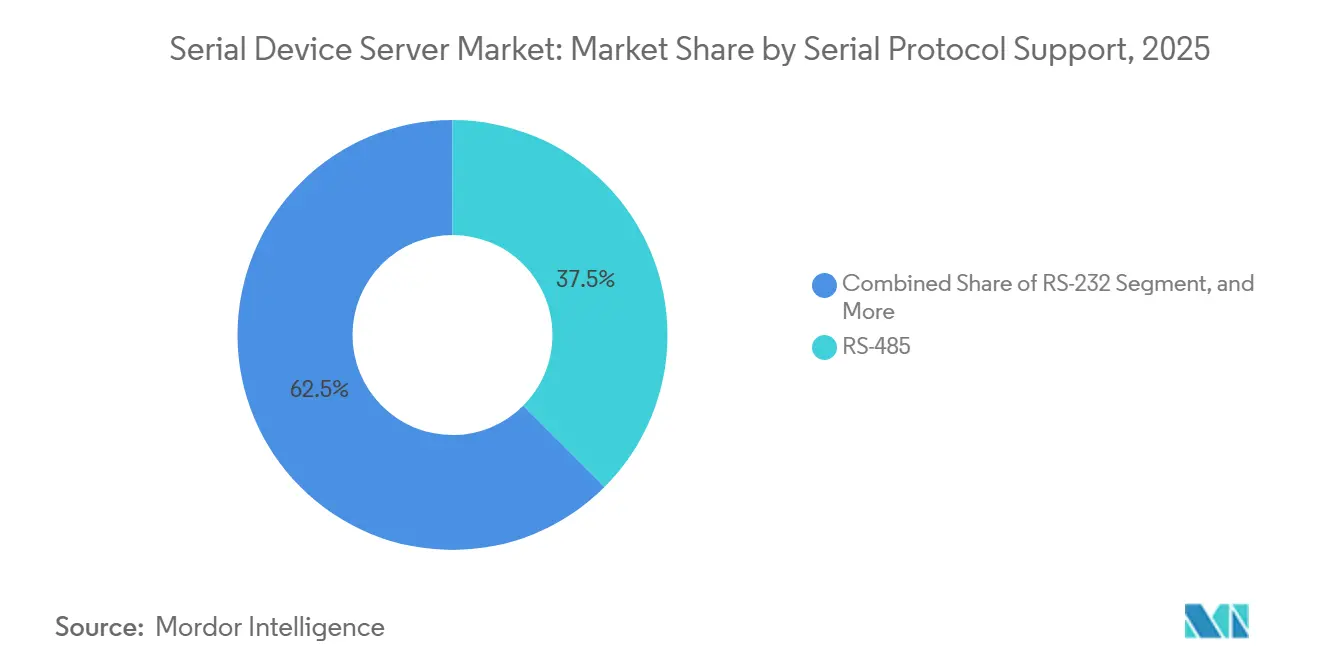

- By Serial Protocol, the RS-485 segment is expected to account for 37.50% revenue share in the serial device server market, while the Multi-Protocol (MEI) segment is likely to grow at 7.40% CAGR.

- By form factor, DIN-rail models accounted for 46.56% of the serial device server market in 2025, while the Embedded/Board-Level segment is expected to grow at a 6.90% CAGR during the forecast period.

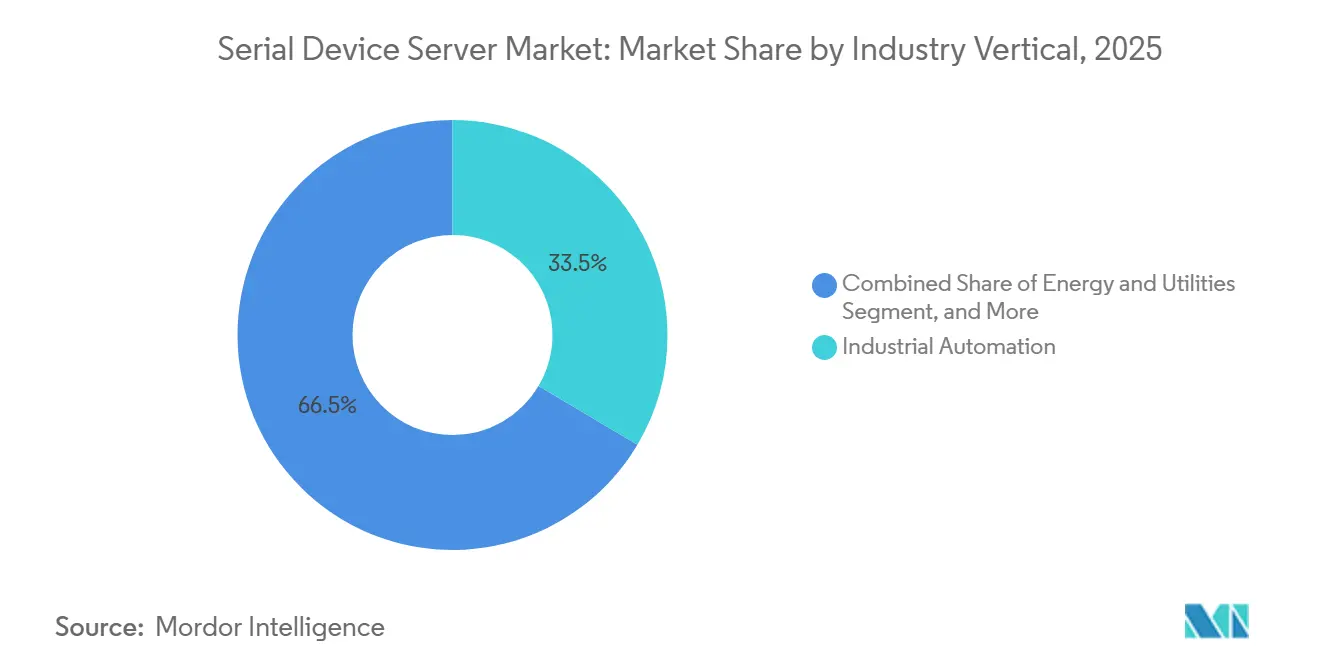

- By Industry Vertical, the Industrial automation segment is likely to account for around 33.52% of revenue in the serial device server market, with Healthcare and Medical Devices growing at a 8.05% CAGR.

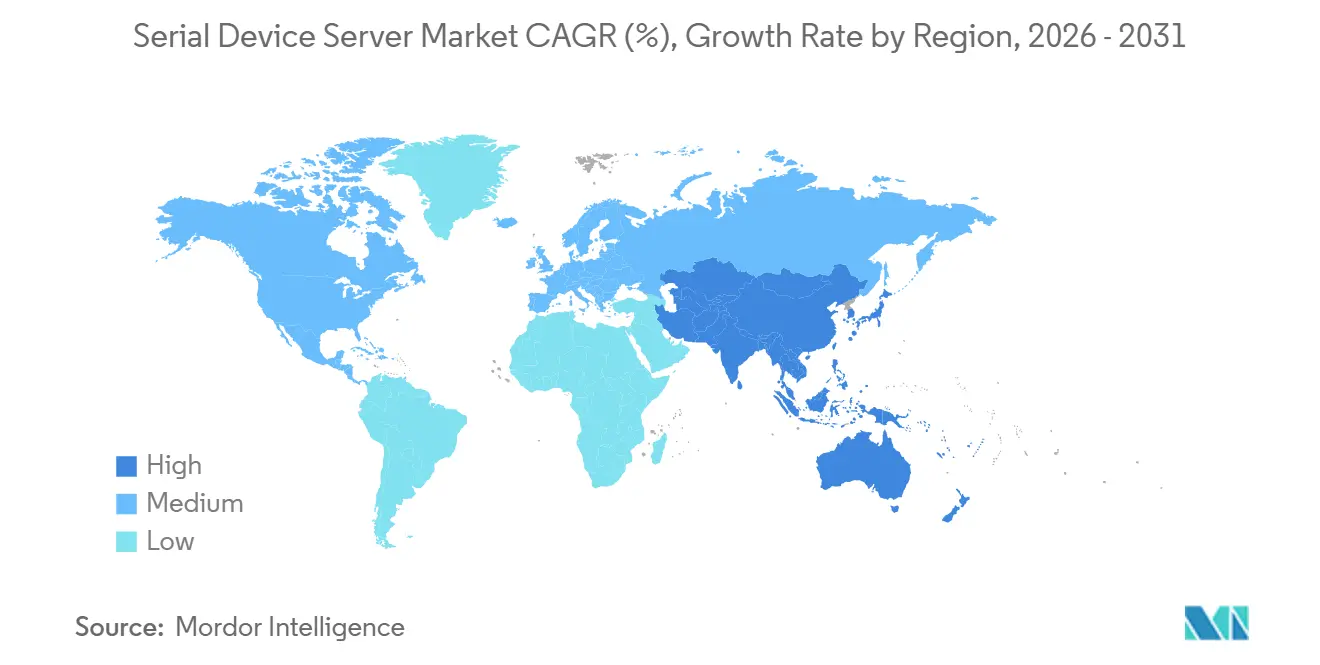

- By Geography, North America captured the majority of revenue in 2025, while Asia-Pacific is growing at a 9.30% CAGR through 2031 in the serial device server market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Serial Device Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Industry 4.0 and IIoT | +1.8% | Asia-Pacific, Europe | Medium term (2–4 years) |

| Transition from Serial to Ethernet Networks | +1.5% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Demand for Remote Device Management | +1.2% | North America, Asia-Pacific | Short term (≤ 2 years) |

| OT-Cyber-Security Compliance | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Edge-AI Inference at Gateways | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Legacy Connectivity Needs in Brown-Fields | +0.5% | Asia-Pacific, South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Industry 4.0 And IIoT

Manufacturers chasing real-time analytics must surface data locked inside decades-old PLCs and drives. Serial device servers preserve installed wiring while adding IP connectivity, preventing costly downtime from wholesale controller swaps. Multi-port models reduce switch counts, simplify topology, and deliver unified management, a critical step toward the higher productivity lift associated with full Industry 4.0 rollouts. Adoption is most intense in China and India, where pre-Ethernet machinery dominates, and in Germany and Italy, where energy-efficiency directives demand granular machine telemetry.

Transition From Serial To Ethernet Networks

Utilities and rail operators are decommissioning proprietary serial SCADA links in favor of Ethernet for bandwidth, standard management, and encrypted traffic. During migration, substation cabinets packed with RTUs still speak RS-485, making robust serial-to-Ethernet gateways indispensable. North American utilities expedite upgrades to comply with NERC-CIP, while European railways integrate legacy interlocking with IP-based train control systems.[1]North American Electric Reliability Corporation, “Critical Infrastructure Protection Standards,” nerc.com Ruggedized gateways with dual power feeds and wide temperature tolerances receive preference as cabinets often sit outdoors.

Demand For Remote Device Management And Predictive Maintenance

Edge intelligence allows teams to visualize barcode scanners, weigh scales, and medical devices from cloud dashboards, shifting maintenance from calendar-based to condition-based schedules. Serial device servers with MicroPython or similar scripting filter noise, convert proprietary packets, and push only actionable data upstream, trimming cellular bandwidth costs. Healthcare networks rely on patient-side gateways tested to IEC 60601-1, underscoring compliance as a differentiator.

OT-Cyber-Security Compliance Boosting Secure Gateways

NERC-CIP, IEC 62443, and the EU Cyber Resilience Act obligate encryption, role-based access control, and audit logging across operating technology. Gateways that meet IEC 62443-4-2 Security Level 2, like Moxa’s NPort 6000-G2 line, clear procurement checklists faster than uncertified rivals.[2]Moxa Inc., “Moxa Sets New Security Benchmark for Serial Device Servers With World's First IEC 62443-4-2 Certification,” moxa.comComponent makers achieving IEC 62443-4-1 validation further shrink supply-chain risk, giving certified vendors a material advantage in regulated verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Natively Ethernet-Enabled Devices | -1.2% | North America, Europe | Medium term (2–4 years) |

| Price Sensitivity in Emerging Economies | -0.9% | Asia-Pacific, Africa, South America | Short term (≤ 2 years) |

| Scarcity of IPv6-Ready Firmware | -0.5% | Europe, North America | Short term (≤ 2 years) |

| Radio-Spectrum Limits in Dense Cities | -0.3% | Asia-Pacific, Europe, North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Natively Ethernet-Enabled Industrial Devices

Greenfield automation projects now specify controllers, drives, and sensors with built-in Ethernet-APL or EtherNet/IP, eliminating the need for conversion altogether. Shorter hardware refresh cycles in the United States and Germany accelerate this drift, cutting replacement demand for standalone gateways. Vendors respond by embedding edge compute and protocol-translation scripts to stay relevant, yet the headwind persists.

Price Sensitivity In Emerging Economies

Small factories in Brazil, Nigeria, or Vietnam gravitate toward USD 10 USB-to-RS-232 dongles rather than USD 150 enterprise-grade servers. These low-cost widgets lack security, but near-term budget pressures trump life-cycle costs. Branded makers have introduced stripped-down SKUs, risking margin erosion. Integrators bundle installation and support to justify premiums, but the service model scales only where skilled labor is available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Port Count: Consolidation Drives High-Density Adoption

High-density chassis are replacing fleets of single-purpose boxes. In 2025, the 4-port tier accounted for 25.81% of revenue, while the 32-port-plus category is projected to post a 7.80% CAGR through 2031. Operators consolidate serial endpoints to cut rack units and streamline cabling. The 8-port class accounted for a significant share of the market in mid-sized control rooms, whereas 2-port gateways served remote wells or kiosks. Uptake of the 16-port tier in utilities remains steady as substations modernize gradually.

A parallel drive for remote configuration favors models with hot-swappable power and dual Ethernet uplinks. As firmware tools mature, a single technician can reassign ports from RS-232 to RS-485 without site visits, a critical advantage for multinationals managing thousands of cabinets. Hence, the serial device server market continues to gravitate toward flexible, high-density hardware that shrinks footprint and man-hours alike.

By Connectivity Type: Cellular Gateways Gain Share

Wired Ethernet remained dominant, accounting for significant revenue in 2025, while Cellular/ LTE options are expanding at a 9.20% CAGR. Utilities that monitor distributed energy resources use CAT-M and NB-IoT variants when fiber is unavailable. Wi-Fi accounted for a significant share of the market, especially on temporary lines at hospitals or exhibition centers. Serial-over-USB modules are used in fanless edge computers that need compact all-in-one cards.

The most profitable niche is dual-mode cellular plus Ethernet, allowing failover paths that satisfy stringent uptime contracts. Gateway makers now pre-install carrier eSIMs, speeding deployment in hard-to-reach geographies. As private 5G campuses proliferate, suppliers that field gateways certified for band n77 gain early access to smart factory budgets, strengthening the long-run outlook for cellular SKUs within the serial device server market.

By Serial Protocol Support: RS-485 Dominates Industrial Control

RS-485 accounted for 37.50% of revenue in 2025 because multi-drop Modbus lines remain ubiquitous in HVAC and process automation. RS-232 retained a significant share for point-to-point links in retail and diagnostics. Multi-protocol ports, configurable via software, are growing at 7.40% CAGR. The shift reduces SKU complexity for distributors and allows end users to repurpose stock as project scopes evolve.

OEMs prefer gateways that map obscure proprietary frames into MQTT or OPC UA, then forward them to public clouds, elevating multi-protocol capability from a convenience to a must-have. Suppliers embed scripting sandboxes so integrators can tackle one-off serial dialects without waiting for firmware releases, keeping brown-field retrofits on schedule.

By Form Factor: DIN-Rail Mounts Lead Industrial Deployments

The DIN-rail Mount segment accounted for 46.56% of revenue in 2025. Control-cabinet real estate is scarce, and installers want clip-in units sharing the same 35 mm rail as relays and breakers. Rack-mount servers, with a significant share, dominate data centers and central control rooms. The embedded/Board-level segment is expected to grow at a 6.90% CAGR, as machine builders integrate connectivity at the board level to reduce enclosure count.

Panel-mount boxes are used in kiosks and vending fleets, where visible status LEDs aid non-technical staff. Gateway makers harmonize firmware across all form factors, easing spares logistics and firmware rollouts. This multiplatform approach keeps the serial device server market responsive to wildly different cabinet geometries.

By Industry Vertical: Industrial Automation Leads, Healthcare Accelerates

Industrial automation accounted for 33.52% of revenue in 2025 as factories leaned into predictive analytics. Energy and utilities accounted for a significant share with grid hardening, and transportation accounted for a significant share as rail operators digitized signaling. Healthcare is the breakout, tracking a 8.05% CAGR to 2031, driven by electronic medical record integration and IEC 60601-1 proximity requirements.

Hospitals under healthcare and medical devices that suffered HIPAA penalties now specify TLS 1.3, VLAN tagging, and syslog export in every bid package, locking out commodity hardware. Retail and POS: still refreshing barcode scanners en masse, but margins remain thin. Building automation converts BACnet and Modbus HVAC loops to IP dashboards, securing 5.8% share.

Geography Analysis

Asia-Pacific led with 30.56% revenue in 2025 and will likely climb at 9.30% CAGR as China retrofits brownfield factories and India rolls out smart-city infrastructure. Low-cost domestic brands bundle protocol conversion apps with hardware, expanding adoption across tier-2 cities. Japanese robotics cells and Korean fabs, meanwhile, prize low-latency gateways with deterministic scheduling.

North America accounted for a significant share of revenue in 2025 and is projected to grow in the market. NERC-CIP enforcement drives bulk purchases by utilities, while freight carriers connect J1939 buses through certified cellular servers for real-time routing. United States component maker expansions in Illinois and Mexico reveal optimism in the domestic supply chain for the serial device server market.

Europe captured a significant share of revenue in 2025 and is set to grow at a significant CAGR. Building-automation retrofits gain pace as the EU Energy Performance of Buildings Directive demands transparent energy data. Rail modernization across Germany, France, and Spain integrates legacy signal boxes into IP backbones, fueling multi-port DIN-rail sales. Middle East and Africa together posted a high share, buoyed by Gulf oil patch LTE projects and South African grid upgrades.

Competitive Landscape

The serial device server market remains moderately concentrated; the top five brands accounted for more than half of revenue in 2025. Certification emerges as the new moat. Moxa’s IEC 62443-4-2 breakthrough sparked a certification race that Digi International, Advantech, Lantronix, and HMS Networks now chase. HMS widened its reach by buying Molex’s industrial NIC assets for USD 7 million, stacking Anybus and Ewon lines atop new North American accounts.[3]Source: HMS Networks AB, “HMS Networks Has Completed the Acquisition of Molex Industrial Communications Business,” hms-networks.com

Differentiation in the serial device server market has shifted to software. Gateways with Python runtimes, HTML5 dashboards, and cloud APIs entice buyers who value manageability over base hardware specs. Vendors are increasingly bundling device management platforms, over-the-air firmware update capabilities, and edge analytics tools to justify premium pricing. Protocol flexibility, including support for MQTT, OPC-UA, and Modbus, has become a baseline expectation rather than a differentiator. Smaller firms such as Tibbo and ACKSYS specialize in board-level modules and rugged Wi-Fi units, carving protected turf by targeting application-specific niches where larger vendors offer limited customization.[4]Tibbo Technology Inc., “Serial Device Servers,” tibbo.com

As buyers quantify downtime risk, lifecycle services become the tie-breaker, tilting share toward vendors bundling over-the-air firmware, asset-tracking portals, and 24×7 support.

Serial Device Server Industry Leaders

Moxa Inc.

Digi International Inc.

Lantronix Inc.

Advantech Co., Ltd.

Perle Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Moxa secured the world’s first IEC 62443-4-2 Security Level 2 certificate for serial servers, validated by Bureau Veritas.

- April 2026: Microchip Technology achieved UL Solutions IEC 62443-4-1 Maturity Level 2 for its secure-development lifecycle.

- January 2026: HARTING expanded manufacturing and research and development in Illinois and Mexico, boosting U.S. headcount by 64%.

- November 2025: HMS Networks signed to acquire the same Molex unit, confirming closure for Jan 2026.

Global Serial Device Server Market Report Scope

The Serial Device Server Market Report is Segmented by Port Count (1-Port, 2-Port, 4-Port, and More), Connectivity Type (Wired Ethernet, Wireless Wi-Fi, and More), Serial Protocol Support (RS-232, RS-422, RS-485, Multi-Protocol), Form Factor (DIN-Rail Mount, Rack-Mount, and Embedded / Board-Level, Panel Mount), Industry Vertical (Industrial Automation, Energy and Utilities, Transportation and Logistics, Retail and Point of Sale, Healthcare and Medical Devices, Building Automation and HVAC, Other Industry Vertical), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 1-Port |

| 2-Port |

| 4-Port |

| 8-Port |

| 16-Port |

| 32-Port and Above |

| Wired Ethernet |

| Wireless (Wi-Fi) |

| Cellular / LTE |

| Serial-over-USB |

| RS-232 |

| RS-422 |

| RS-485 |

| Multi-protocol (MEI) |

| DIN-Rail Mount |

| Rack-mount |

| Embedded / Board-Level |

| Panel Mount |

| Industrial Automation |

| Energy and Utilities |

| Transportation and Logistics |

| Retail and POS |

| Healthcare and Medical Devices |

| Building Automation and HVAC |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By Port Count | 1-Port | |

| 2-Port | ||

| 4-Port | ||

| 8-Port | ||

| 16-Port | ||

| 32-Port and Above | ||

| By Connectivity Type | Wired Ethernet | |

| Wireless (Wi-Fi) | ||

| Cellular / LTE | ||

| Serial-over-USB | ||

| By Serial Protocol Support | RS-232 | |

| RS-422 | ||

| RS-485 | ||

| Multi-protocol (MEI) | ||

| By Form Factor | DIN-Rail Mount | |

| Rack-mount | ||

| Embedded / Board-Level | ||

| Panel Mount | ||

| By Industry Vertical | Industrial Automation | |

| Energy and Utilities | ||

| Transportation and Logistics | ||

| Retail and POS | ||

| Healthcare and Medical Devices | ||

| Building Automation and HVAC | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

What is the current size of the serial device server market?

The serial device server market size stands at USD 326.5 million in 2026 and is projected to reach USD 436.80 million by 2031, according to Mordor Intelligence.

How fast is the market growing?

The market is registering a 5.99% CAGR during 2026-2031, driven by Industry 4.0 upgrades, cyber-security mandates, and cellular connectivity rollouts.

Which region contributes the most revenue?

North America leads with 39.6% of global revenue, supported by accelerating Industrial IoT deployment, factory automation upgrades, and continued modernization of legacy serial communication infrastructure.

Who are the top vendors?

Moxa, Digi International, Advantech, Lantronix, and HMS Networks collectively control more than 50% revenue, while specialists like 3onedata and ACKSYS serve price-sensitive or rugged niches.

Which connectivity option is growing fastest?

Cellular and LTE serial gateways are the fastest-growing, advancing at a significant CAGR, as utilities and oil-and-gas firms link remote assets without fiber.

What certification trends influence purchase decisions?

IEC 62443-4-2 for device security and IEC 62443-4-1 for secure development lifecycles are increasingly mandatory in RFPs, reshaping vendor qualification shortlists.

Page last updated on: