Network Attached Storage (NAS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 46.32 Billion |

| Market Size (2031) | USD 101.24 Billion |

| Growth Rate (2026 - 2031) | 16.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Network Attached Storage (NAS) Market Analysis by Mordor Intelligence

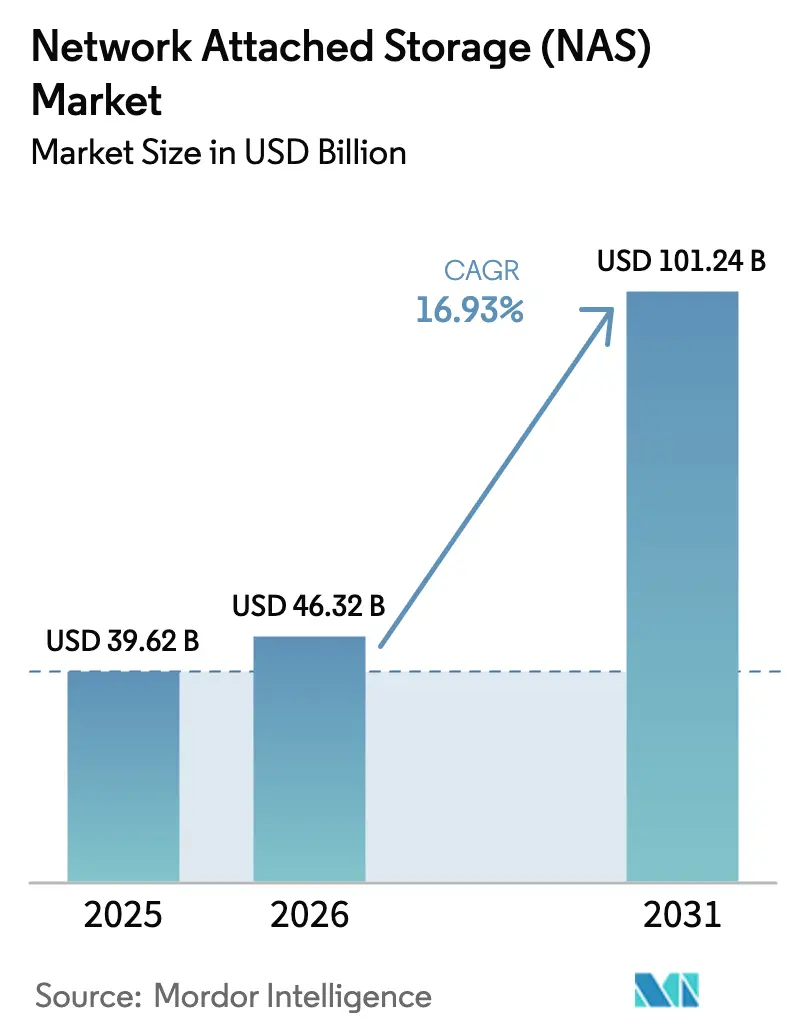

The Network Attached Storage Market size was valued at USD 39.62 billion in 2025 and is estimated to grow from USD 46.32 billion in 2026 to reach USD 101.24 billion by 2031, at a CAGR of 16.93% during the forecast period (2026-2031).

This growth reflects enterprises’ pivot toward file-storage systems that align with generative AI, hybrid-work persistence, and data-sovereignty mandates, reshaping procurement priorities and vendor roadmaps. Scale-out architectures, with their horizontal scalability and controller-less performance gains, continue to displace traditional scale-up designs as organizations target parallel file access for AI model checkpointing. On-premise systems still dominate because of latency, compliance, and egress-fee concerns, yet hybrid tiers that automatically shuttle cold files to object storage are multiplying fastest. Reshoring of NAS production, tariff-related cost pressures, and energy limits in dense urban data centers together temper the pace of cloud substitution and further reinforce demand for modular, power-efficient appliances that fit constrained footprints.

Key Report Takeaways

- By type, scale-out systems accounted for 53.81% of the network-attached storage market share in 2025. Further, this type is forecast to expand at a 17.33% CAGR through 2031, the fastest among all categories.

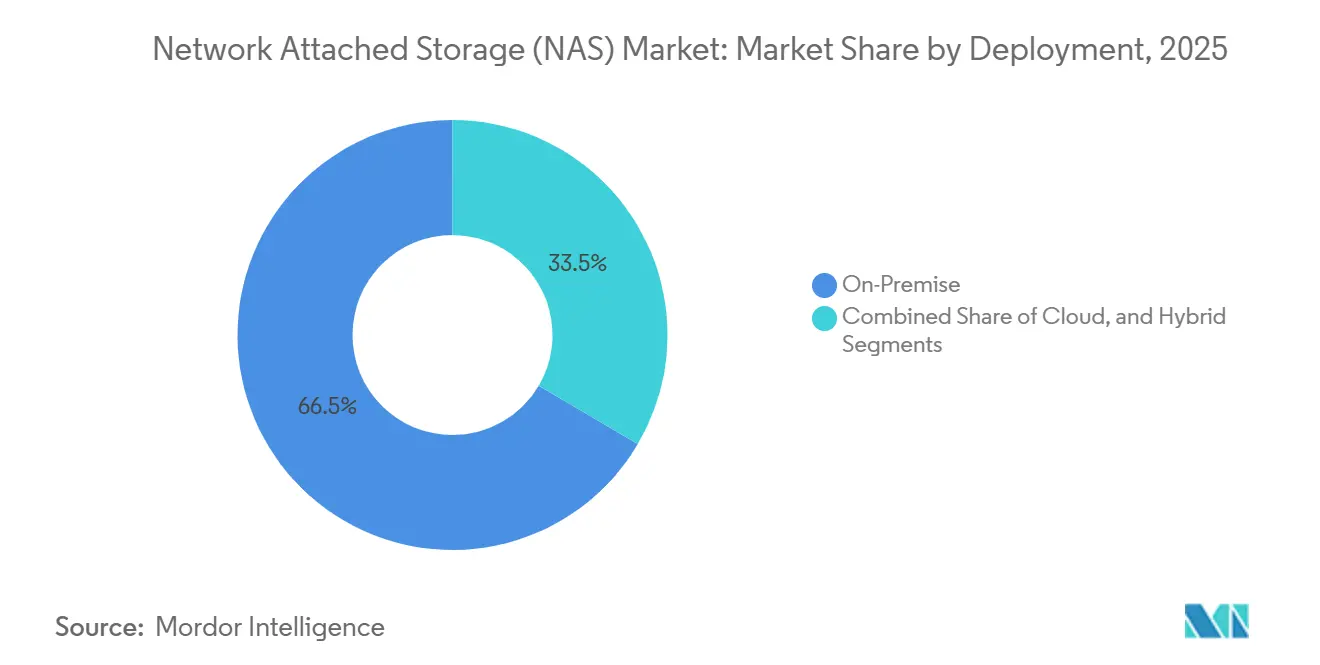

- By deployment, on-premises accounted for 66.53% of the network-attached storage market share in 2025, whereas hybrid configurations are set to rise at a 17.44% CAGR between 2026 and 2031.

- By end-user industry, IT and Telecom accounted for 28.61% of the network-attached storage market share in 2025, while healthcare is advancing at an 18.47% CAGR through 2031.

- By product tier, mid-market accounted for 45.91% of the network-attached storage market share in 2025; high-end/enterprise is the fastest-growing tier at a 17.56% CAGR through 2031.

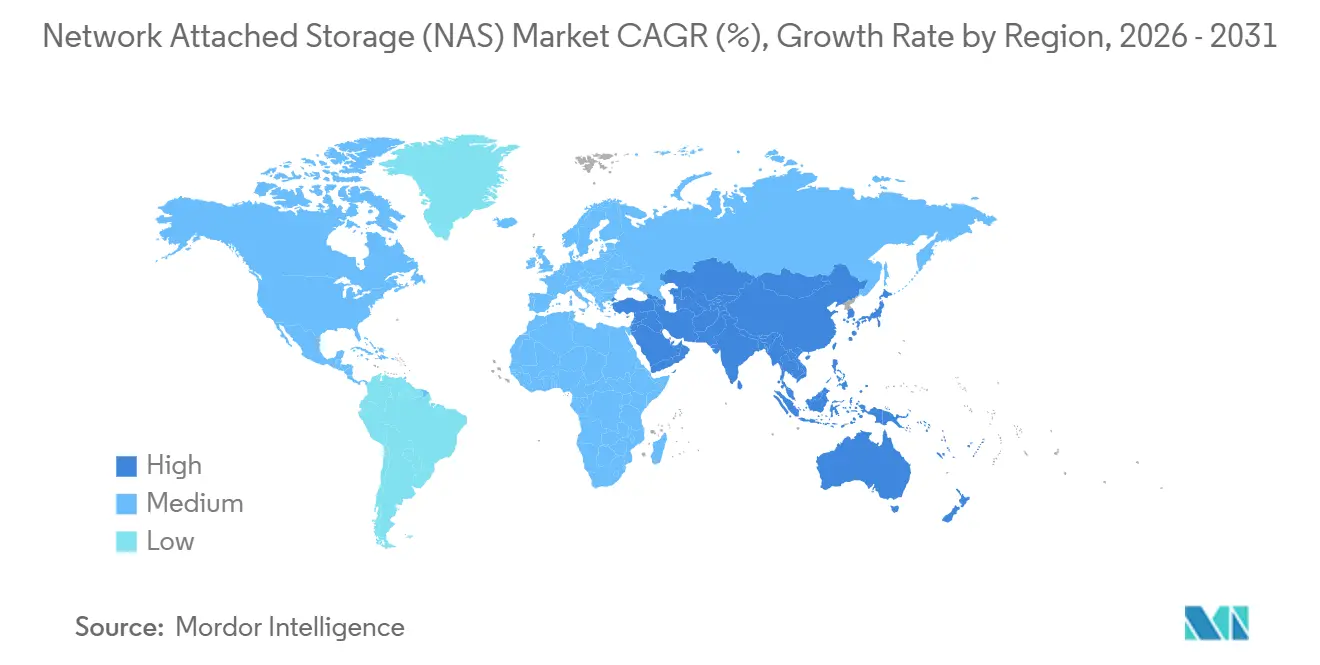

- By geography, North America held 39.66% revenue share of the network-attached storage market in 2025; Asia-Pacific is advancing at a 17.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Network Attached Storage (NAS) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of Unstructured Data | +3.2% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Remote and Hybrid-Work Data Surge | +2.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Data-Center Virtualization and Software-Defined NAS | +2.4% | North America, Europe, and Asia-Pacific enterprise markets | Medium term (2-4 years) |

| AI/ML Training Workloads Need Parallel File Access | +3.5% | North America and Asia-Pacific AI hubs, spillover to Europe | Long term (≥ 4 years) |

| 5G Edge Build-Out Boosts On-Prem NAS | +1.9% | Asia-Pacific core, North America metro areas, Middle East smart cities | Medium term (2-4 years) |

| Tariff-Driven Reshoring of NAS Production | +1.4% | North America and Europe manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosion of Unstructured Data

Up to 80% of enterprise information now arrives in unstructured form, and annual growth rates near 50% drive urgent capacity expansion on file-based platforms. Video surveillance, IoT telemetry, and collaborative content overwhelm legacy scale-up controllers, pushing buyers toward scalable clusters that add nodes without disrupting service. A parallel shift replaces backup-centric thinking with analytics-centric strategies, as data-lake projects rely on NAS to query files directly instead of staging them in data warehouses. Regulatory file-retention rules, such as SEC 17a-4 for broker-dealers, prolong on-premise storage lifecycles because cloud egress costs and jurisdictional risks complicate retention in object stores. Retailers likewise consolidate point-of-sale logs and omnichannel transcripts onto deduplicated NAS volumes that compress petabyte estates into affordable footprints.[1]U.S. Securities and Exchange Commission, “Rule 17a-4: Records to be Preserved,” SEC.gov

Remote and Hybrid-Work Data Surge

Permanent hybrid work doubled home-directory creation rates, magnifying branch-office storage traffic and fueling demand for edge-NAS appliances that cache files close to users. VPN-integrated NAS devices synchronize with core data centers overnight, cutting WAN bandwidth needs by more than 40%. Telehealth rollouts during 2025 generated persistent uploads of consultation recordings that hospitals store on HIPAA-compliant appliances, maintaining role-based access and immutable logs. Universities moved lecture videos onto local arrays after discovering that streaming archives from cloud regions incurred USD 0.09 per gigabyte in egress fees, a cost unsustainable at multi-terabyte scales.[2]U.S. Department of Health and Human Services, “HIPAA Security Rule: Technical Safeguards,” HHS.gov

Data-Center Virtualization And Software-Defined NAS

Hypervisor suites now embed file-share services into software-defined nodes, letting teams allocate capacity on commodity servers while scaling performance separately via NVMe drive pools. The model supports multitenancy, reduces capital spending by as much as one-third, and simplifies disaster-recovery failover by pushing replicas into temporary cloud instances, then repatriating them once local hardware is restored. HPE Alletra and NetApp ONTAP Select demonstrate these efficiencies in production, and many midsize firms adopt the pattern to sidestep tariffs on fully integrated arrays.[3]Hewlett Packard Enterprise, “HPE Alletra Storage MP Technical Specifications,” HPE.com

AI/ML Training Workloads Need Parallel File Access

Transformer models with 100 billion + parameters demand aggregate throughput beyond 200 GB/s for checkpoint operations. Scale-out NAS systems deliver the necessary parallelism through pNFS, GPUDirect, and NVMe-over-Fabrics to stream data directly into GPU memory. Pharmaceutical, automotive, and finance research clusters therefore favor on-premise NVMe-backed arrays over cloud object storage, as repeated S3 fetches eclipse on-site costs within two years of continuous operation. NVIDIA’s DGX SuperPOD underscores the architectural imperative by prescribing NAS arrays capable of 15 million IOPS to avoid GPU idle time.[4]NVIDIA Corporation, “DGX SuperPOD Reference Architecture,” NVIDIA.com

Restraints Impact Analysis of Network Attached Storage (NAS) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Storage Substitution | -2.1% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Performance Bottlenecks at Petabyte Scale | -1.3% | Global enterprise and hyperscale deployments | Long term (≥ 4 years) |

| Rising Cyber-Insurance Premiums for On-Prem File Systems | -0.9% | North America and Europe | Short term (≤ 2 years) |

| Power-Density Caps in Urban Data Centers | -0.7% | Asia-Pacific metros, Europe urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Storage Substitution

Hyperscaler object stores undercut NAS for cold archives, prompting some teams to offload backup volumes to pay-as-you-go buckets. However, egress charges near USD 90,000 per petabyte discourage retrieval, locking data in cloud silos and complicating analytics that require local proximity. Media studios confronted this when editing 4K masters, and many responded by adopting hybrid appliances that pin hot content on-site while tiering aged assets to Glacier or Archive classes.

Performance Bottlenecks at Petabyte Scale

Traditional dual-controller systems stall under billions of inodes, with metadata operations serialized into latency spikes that break sub-millisecond targets. Scale-out designs alleviate the bottleneck yet introduce namespace-management complexity and lengthy rebuild windows for 20 TB drives. Vendors now embed erasure coding and distributed parity while transitioning to NVMe-over-Fabrics interfaces; nevertheless, cost barriers restrict these high-end features to AI labs and high-frequency trading floors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Network Attached Storage (NAS) Market Segment Analysis

By Type:

Scale-Out Dominance Driven By AI ParallelismScale-out platforms captured 53.81% of 2025 revenue in the network attached storage market and will grow at a 17.33% CAGR through 2031. Their node-level elasticity lets operators align capacity and throughput with unpredictable AI training surges, enabling 200 GB/s aggregate bandwidth for GPU clusters. In turn, scale-out clusters often replace Hadoop Distributed File System deployments because standard NFS and SMB simplify application integration. Scale-up systems maintain a foothold among midsize firms that prize management simplicity over petabyte ambitions, but controller ceilings appear once file counts push beyond 100 million sessions.

Scale-up appliances remain attractive at price points below USD 10,000, dominated by Synology and QNAP units that address small departments. Yet their dual-controller architectures face CPU and RAM bottlenecks as clients proliferate, limiting viability in hyperscale AI environments. Consequently, the network attached storage market size for scale-up platforms is likely to expand more slowly than the overall 16.93% pace.

By End-User Industry:

Healthcare Acceleration Fueled By Imaging And GenomicsHealthcare leads growth at an 18.47% CAGR, driven by daily ingestion of terabytes of DICOM scans and genomic sequences. Electronic-health-record vendors integrate directly with NAS arrays, reinforcing demand for on-premise file stores that satisfy HIPAA and GDPR. IT and telecom firms, which held 28.61% network attached storage market share in 2025, spearheaded early virtualization and remain the largest spender, but maturation tempers their expansion rate.

BFSI players rely on tamper-proof NAS archives for regulatory communication logs, while retail and e-commerce operators use deduplication to store omnichannel transcripts efficiently. Media studios sustain heavy parallel-workflow demands, pushing all-flash NAS adoption, whereas government, education, and manufacturing accelerate modestly on sovereign-data and predictive-maintenance drivers. The network attached storage market size attributable to healthcare workloads is projected to eclipse USD 20 billion by 2031.

By Deployment:

Hybrid Configurations Balancing Cost And PerformanceOn-premise systems still delivered 66.53% of 2025 revenue, yet hybrid tiers advance fastest at a 17.44% CAGR as enterprises automate cloud tiering for cold archives. Unified-namespace software, exemplified by NetApp Cloud Volumes ONTAP, lets administrators move data without altering application mounts. Businesses trim local capacity needs 40-60% while avoiding bulk transfers that accrue prohibitive egress costs. Managed cloud NAS appeals for development environments and seasonal bursts, but variable IOPS and residency risks keep latency-sensitive datasets local. The network attached storage market size attached to hybrid deployments will almost double between 2026 and 2031.

By Product Tier:

Enterprise Systems Capturing AI Infrastructure SpendEnterprise arrays priced above USD 500,000 per petabyte are growing at 17.56% CAGR, feeding AI-training clusters that demand 10 million IOPS and GPUDirect migration paths. Dell PowerScale, NetApp AFF, and HPE Alletra dominate the tier by integrating inline data reduction and autonomous balancing. Mid-market platforms, holding 45.91% of 2025 revenue, deliver up to 1 PB capacity at sub-USD 50,000 budgets. They retain loyal SMB clients but face substitution from public-cloud file services for low-duty-cycle workloads. Meanwhile, SOHO devices confront direct competition from Dropbox, Google Workspace, and similar object-storage offerings, yet creative professionals still procure local arrays to avoid rendering delays.

Geography Analysis

North America Network Attached Storage (NAS) Market

North America accounted for 39.66% of network attached storage market revenue in 2025, supported by USD 120 billion-plus hyperscaler data-center spending and regulations that mandate tamper-proof on-premise storage. U.S. federal agencies deploy FedRAMP-authorized, air-gapped appliances for classified workloads, while Canadian banks rely on local arrays to avoid cross-border PIPEDA conflicts. Mexico’s automotive factories add edge-NAS nodes that perform real-time quality inspections without cloud latency.

APAC Network Attached Storage (NAS) Market

Asia-Pacific is the fastest-growing region at 17.91% CAGR, propelled by China’s USD 50 billion data-center build-out and India’s Digital India residency rules. Japanese autonomous-vehicle pilots and South Korean 5G edge rollouts depend on sub-10 ms local storage, catalyzing demand for ruggedized appliances. In India, HIPAA-equivalent health regulations steer hospitals toward sovereign NAS clusters, boosting the region’s share of the network attached storage market.

Europe Network Attached Storage (NAS) Market

Europe embraces hybrid deployments to navigate GDPR and DORA requirements that complicate multi-region cloud architectures. German Industry 4.0 plants store sensor telemetry locally for predictive analytics, while the United Kingdom’s MiFID II rules extend tape-replacement cycles and sustain archive NAS budgets. France’s HDS mandate keeps patient data inside certified on-premise infrastructure, driving further appliance sales.

MEA Network Attached Storage (NAS) Market

Middle East and Africa experience double-digit growth on the back of smart-city mega-projects. Saudi Arabia’s Vision 2030 funding underwrites NEOM’s massive edge-NAS rollout, caching 8K video feeds at tens of thousands of cameras. UAE retailers replicate similar architectures inside malls, and Israel deploys air-gapped clusters for defense analytics. South African finance and Egyptian municipal IT likewise invest to comply with data-protection statutes, although unreliable power grids impede broader adoption across sub-Saharan regions.

Regulatory Landscape

NAS procurement and architecture increasingly reflect data-sovereignty and cybersecurity requirements that favor verifiable local control, immutable retention, and auditability. File-retention and security rules in regulated industries keep on-premise NAS central to compliance programs, including SEC Rule 17a-4 for broker-dealer record preservation and the HIPAA Security Rule technical safeguards for protected health information.

In 2026, security baselines and conformity schemes added concrete certification and control anchors for enterprise and public-sector buyers. NIST published SP 800-172 Rev. 3 (Enhanced Security Requirements for protecting Controlled Unclassified Information), reinforcing expectations for hardening and monitoring of systems that store sensitive workloads. In Japan, QNAP reported that certain NAS products achieved JC-STAR Level 1 validation under the scheme operated by Japan Information-technology Promotion Agency (IPA), showing how country-specific security validation and procurement requirements intersect with NAS platform selection alongside GDPR and DORA-driven governance needs in Europe.

Value Chain Analysis

The NAS value chain spans component suppliers (HDD/SSD media, DRAM, CPUs/DPUs, NICs and storage controllers), platform software (file systems, snapshots, replication, security and management), OEMs and system integrators, and distribution through channel partners and cloud or managed-service providers. Upstream dependencies include silicon and packaging capacity (foundries and OSAT providers) and storage media availability, while downstream value is created through validated drive compatibility, lifecycle services, and integration with virtualization, backup, and hybrid tiering stacks.

In 2026, component-price and availability dynamics reinforced the need for multi-sourcing and ongoing qualification. NAND Research reported NAND flash contract prices rising 70-75% sequentially (May 2026), which increases BOM pressure on all-flash and NVMe-heavy NAS tiers and can shift configurations toward hybrid or capacity-optimized designs. Supply-side volatility also shows up in compatibility and inventory management, for example eRacks Systems noted re-verifying its NAS line to align defaults with available 24 TB and 32 TB drive inventory (July 2026), reflecting how OEM validation matrices and channel inventory can affect what SKUs ship and how quickly deployments scale.

Competitive Landscape

The top five vendors together hold roughly 45-50% share, placing the market in a moderately concentrated band. Dell Technologies, NetApp, and Hewlett Packard Enterprise continue to dominate enterprise bids by integrating predictive analytics, inline encryption, and autonomous tiering. Each has introduced consumption-based subscription models that wrap hardware, software, and support into opex contracts attractive to financial controllers.

Pure Storage and Huawei gain traction with all-flash or software-defined propositions that push density and throughput while reducing rack footprint by more than 60%. Synology and QNAP secure the mid-market through aggressively priced appliances and simplified management that eliminates the need for full-time storage engineers. Open-source builds using TrueNAS also nibble at market edges as cost-sensitive buyers assemble white-box clusters on commodity servers.

A flurry of patents in erasure coding and NVMe-over-Fabrics shows intensifying R&D as vendors race to offer 15 million IOPS in sub-10U footprints without exceeding power caps. ISO 27001, SOC 2, and soon DORA certifications have become prerequisites in regulated verticals, raising compliance barriers for smaller entrants.

Network Attached Storage (NAS) Industry Leaders

Hewlett-Packard Development Company

Dell Technologies Inc.

NetApp Inc.

Synology Inc.

Western Digital Corp.

- *Disclaimer: Major Players sorted in no particular order

Network Attached Storage (NAS) Market Companies Covered in this Report

- Dell Technologies Inc.

- NetApp Inc.

- Hewlett Packard Enterprise Co.

- Synology Inc.

- Western Digital Corp.

- Seagate Technology Holdings PLC

- QNAP Systems Inc.

- IBM Corp.

- Hitachi Vantara LLC

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Lenovo Group Ltd.

- Super Micro Computer Inc.

- Buffalo Inc.

- Zyxel Communications Corp.

- Asustor Inc.

- TerraMaster Technology Co. Ltd.

- Thecus Technology Corp.

- Promise Technology Inc.

- Infortrend Technology Inc.

- Netgear Inc.

- Pure Storage Inc.

- Fujitsu Ltd.

- NEC Corp.

Market Opportunities and Future Outlook

Enterprise whitespace is expanding around AI-ready file services, particularly where parallel access, low-latency checkpointing, and high IOPS gate GPU utilization. Product activity in 2026 reflects this shift. Synology brought PAS7700 to general availability (June 2026), positioning an active-active, all-flash NVMe system with 48 NVMe bays in 4U and up to 1.65 PB raw capacity, which raises the performance ceiling for NAS-style workflows that are sensitive to failover and metadata contention.

On the security side, standards work such as DMTF DSP0286 (SPDM to Storage Binding, published May 2025) creates room for differentiation through stronger device identity, attestation, and protected data paths across NVMe and SCSI transports. At the edge and prosumer creator tier, new entrants and refresh cycles are widening the addressable base for compact, high-throughput NAS appliances, including UGREENs NASync DXP GT lineup (June 2026) and Asustor Flashstor Gen3 models shown at Computex 2026. These launches align with demand for faster local workflows that avoid recurring cloud egress charges and support hybrid patterns, with hot data kept on-premise and cold data tiered to object storage. Data sovereignty and procurement certifications also provide an adoption lever for on-premise and hybrid NAS in public sector and regulated verticals, supported by Japans JC-STAR validation activity for NAS products and broader regulatory focus on controlling data location and auditability.

Recent Industry Developments in Network Attached Storage (NAS) Market

- June 2026: NetApp announced StorageGRID 12.1, adding a federated global namespace that supports management of globally distributed systems at massive scale, including up to 10 exabytes in a single namespace. The release supports hybrid architectures where NAS environments tier or archive colder data to object storage while keeping a unified operational view across sites.

- May 2026: Dell Technologies announced Dell PowerStore Elite, positioning the platform for mixed workload needs across block, file, virtual machines, and containers with mixed-generation clustering. With global availability stated for July 2026, the announcement signals continued convergence of file and block capabilities as enterprises modernize storage estates for virtualization and AI-adjacent pipelines.

- October 2025: Dell Technologies launched PowerScale F910, an all-NVMe scale-out NAS platform tuned for AI clusters. The product reinforces the shift toward NVMe-heavy scale-out designs that target high-throughput parallel file access and faster checkpoint operations in GPU-driven environments.

Network Attached Storage (NAS) Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers revenue earned from network-attached storage systems that provide file-level shared storage over standard networks for business and home use, including related NAS software that is sold as part of the NAS offering.

Scope exclusions: Direct-attached storage, storage area networks, and pure object storage platforms are not counted in this market sizing.

Segments Covered in This Report

- By Type

- Scale-Up

- Scale-Out

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare

- Retail and E-Commerce

- Media and Entertainment

- Government and Public Sector

- Education and Manufacturing

- Other End-User Industries

- By Deployment

- On-Premise

- Cloud

- Hybrid

- By Product Tier

- High-End / Enterprise

- Mid-Market

- Low-End / SOHO

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used first to set the market structure and build the initial data series, so later assumptions could be checked against real-world signals. We typically refer to public and official sources such as the US Census Bureau and Eurostat for ICT and business activity indicators, OECD datasets for digital economy metrics, and ITU releases for broadband and connectivity direction.

To keep the NAS lens practical, we also reviewed company annual reports, earnings decks, and product documentation to confirm what is being sold as NAS and how it is packaged. Patent databases were used selectively to understand where key capabilities are moving, for example, file services, snapshotting, and data protection features. A paid subscription focused on company financials and news helped validate revenue splits and major shipment announcements. The desk sources noted above are illustrative only, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test model assumptions that desk sources cannot fully explain, such as typical pricing bands, refresh cycles, and the share of hybrid deployments that still behave like NAS. We spoke with vendors, channel partners, system integrators, and enterprise buyers across key regions, and then used follow-up questions to close gaps where responses diverged.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 25% | EMEA: 29% |

| Smaller Players: 21% | Managers: 57% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build where enterprise storage spend and networked file storage adoption signals are translated into NAS revenue, and then split by region using ICT spending and data center activity indicators. To keep the result realistic, we corroborate totals with selective bottom-up approximations, such as sampled average selling prices multiplied by estimated unit volumes for common NAS form factors, followed by channel checks on mix shifts.

Key inputs used in the model include indicators such as growth in unstructured data and backup volumes, data center build-outs, SMB versus enterprise adoption patterns, average capacity shipped per system, and pricing progression for HDD and SSD configurations. These variables influence bill-of-material costs and street prices. Where gaps exist in bottom-up views, for example limited visibility for smaller local brands, we fill them using distributor feedback and regional shipment proxies. We then re-check the implied per-customer spend against interview ranges.

For forecasting, scenario analysis is used so the base case can reflect likely timing of refresh cycles, hybrid adoption, and macro IT budget changes, and then the scenarios are narrowed using what respondents expect for purchasing cadence and pricing pressure. The final forecast is only accepted after the growth path aligns with the market fingerprints above and does not break practical constraints, such as implausible price declines or sudden capacity jumps.

Data Validation & Update Cycle

Validation is done through multiple passes where outputs are compared against independent signals like enterprise infrastructure spend direction, storage media pricing movement, and data center expansion patterns, and then any odd jumps are investigated. If a region or year shows a variance that cannot be explained by a known driver, we re-check assumptions, revisit the split logic, and, where needed, re-contact sources to confirm what changed.

Before sign-off, the model and write-up go through an internal review so definitions, arithmetic, and logic stay consistent across chapters and exhibits. Reports are refreshed annually, and interim updates are triggered when there is a material event, such as a major product cycle shift or a large pricing change. A final freshness pass is then completed right before delivery so clients receive the latest view.

Mordor Intelligence's Network Attached Storage Nas Market Size Compared Against Other Published Estimates

Published NAS market values can vary widely because the included product set is not always the same, and because firms pick different base years and growth paths for pricing and demand. Differences also come from how hybrid systems are treated, and whether the estimate is anchored on storage infrastructure spend signals or on a narrower device shipment view.

Pure object storage platforms sit outside Mordor Intelligence's scope, which often widens the gap versus studies that bundle file and object storage under one networked storage bucket, even when buyers evaluate them side by side.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.62 B (2025) | |

| Global Consultancy A | USD 46.97 B (2025) | Uses a broader market framing with limited clarity on adjacent storage types and bundled solution scope, which can pull in revenue beyond NAS appliances and tightly-coupled NAS offerings. |

| Regional Consultancy B | USD 34.41 B (2024) | Anchors the base year on an earlier snapshot and appears to rely more on offering-level splits, which can undercount systems revenue when software and bundled services are reported differently across channels. |

Taken together, the spread is mainly explained by scope width and the year chosen for the starting point, followed by how pricing and bundled components are treated. By keeping the inputs traceable to file-level NAS demand signals and then cross-checking them with practical ASP and volume sanity checks, the result stays repeatable and easy to audit year over year.

Key Questions Answered in the Report

How large is the network attached storage market in 2026?

It stands at USD 46.32 billion and is on track to more than double by 2031, growing at a 16.93% CAGR.

Which end-user vertical shows the fastest growth in NAS demand?

Healthcare leads with an 18.47% CAGR, driven by imaging archives and genomics pipelines that require on-premise, low-latency storage.

Why are hybrid NAS deployments gaining popularity?

Enterprises blend on-premise performance with cloud economics, automatically tiering cold data to object storage while keeping hot datasets local to avoid egress fees and latency penalties.

What makes scale-out NAS preferable for AI workloads?

Scale-out clusters distribute metadata and I/O across nodes, delivering 200 GB/s or more of throughput that GPU training routines require for model checkpointing.

Which regions are expanding NAS capacity most rapidly?

Asia-Pacific is the fastest-growing region, advancing at 17.91% CAGR on the back of massive data-center construction in China, India, and 5G edge rollouts across Japan and South Korea.

How fragmented is the vendor landscape?

The top five vendors hold under 50% share, signaling moderate concentration that still allows emerging players like Pure Storage and Huawei to carve high-growth niches.

Page last updated on: