Market Overview

| Study Period | 2020 - 2031 |

|---|---|

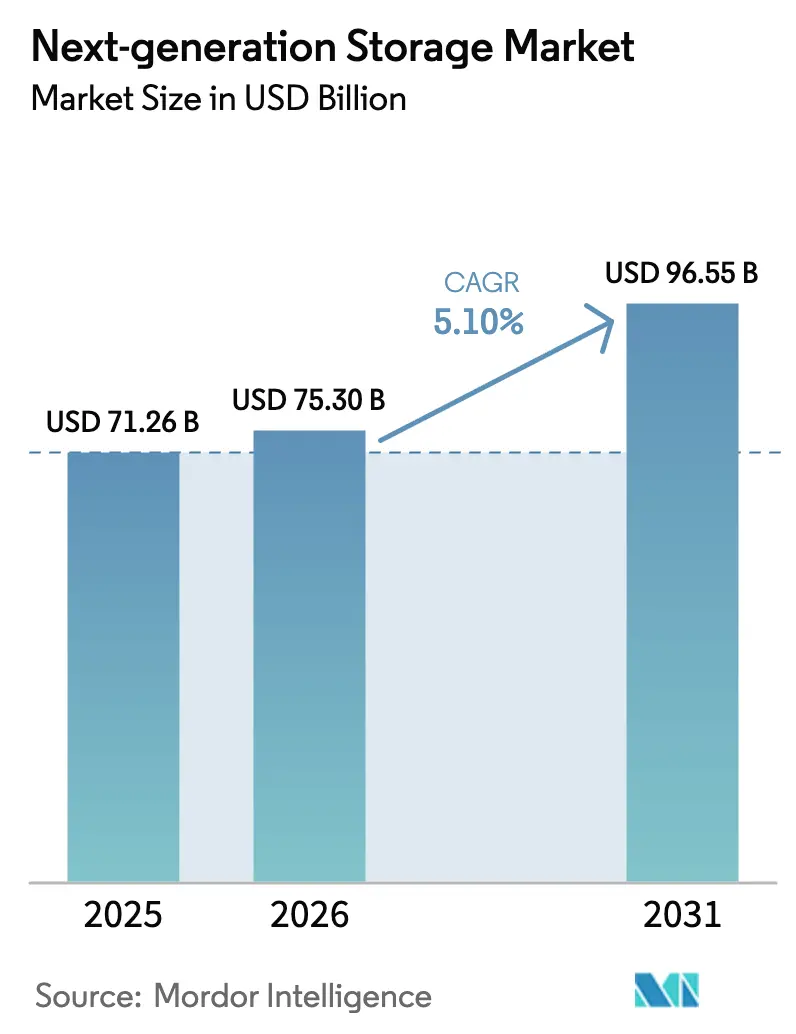

| Market Size (2026) | USD 75.30 Billion |

| Market Size (2031) | USD 96.55 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

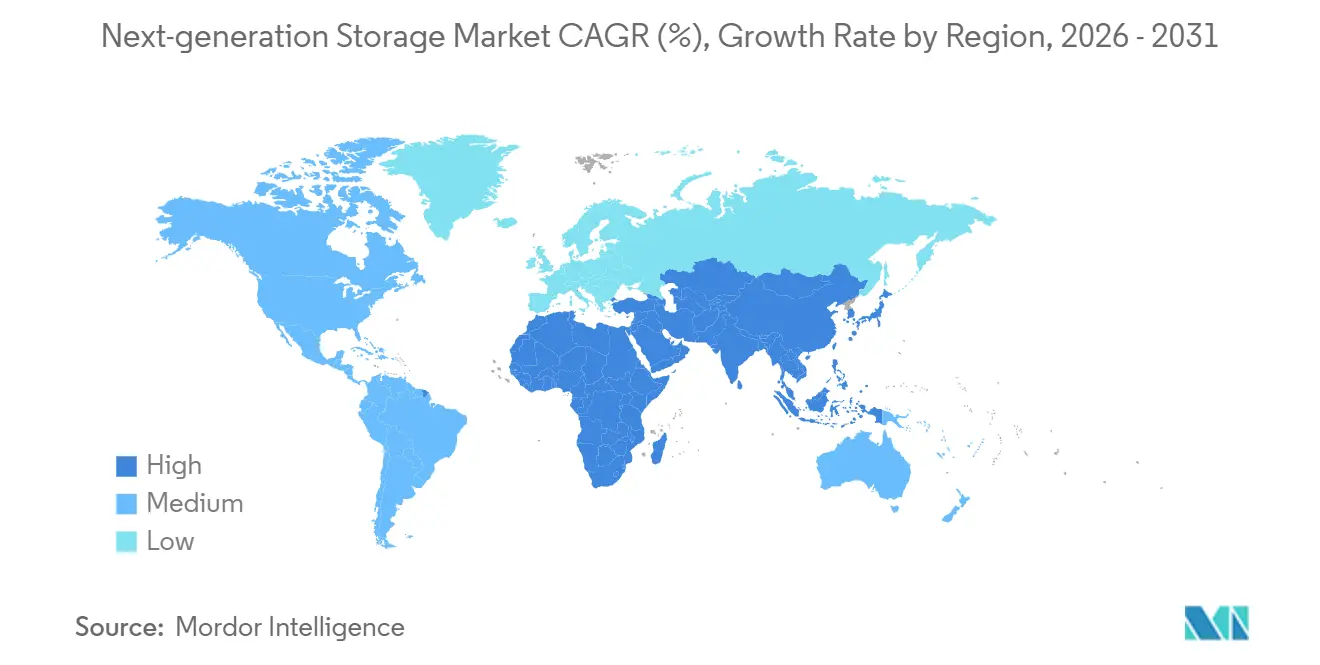

| Fastest Growing Market | Africa |

| Largest Market | North America |

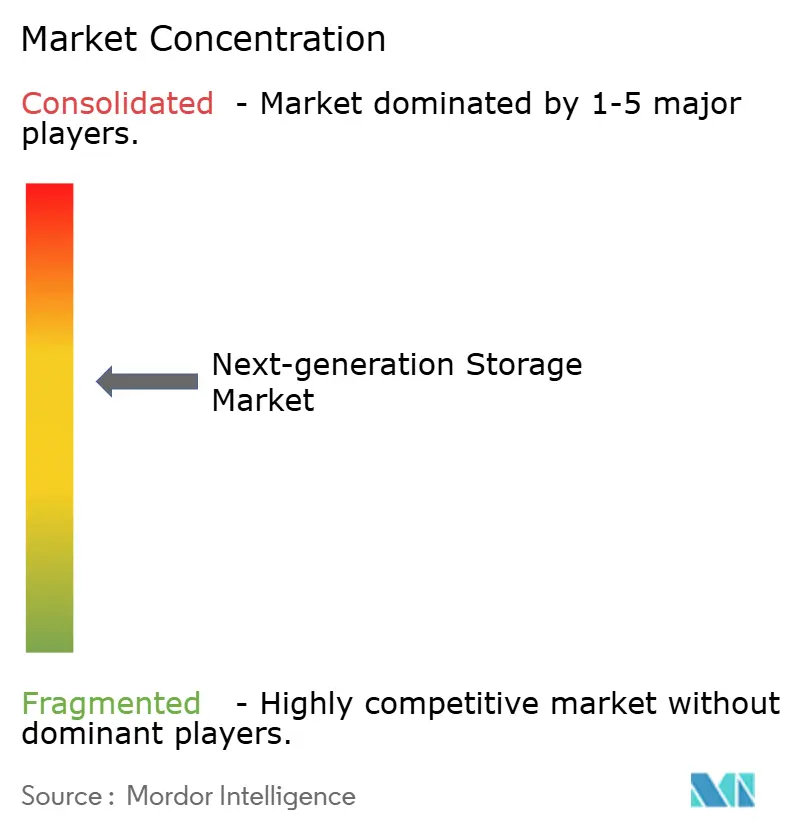

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Next-generation Storage Market Analysis by Mordor Intelligence

The Next-generation Storage Market size is expected to increase from USD 71.26 billion in 2025 to USD 75.30 billion in 2026 and reach USD 96.55 billion by 2031, growing at a CAGR of 5.10% over 2026-2031. Momentum stems from enterprises re-architecting data estates around software-defined, cloud-native platforms that sustain AI model training, real-time analytics, and edge workloads, which legacy arrays struggle to handle. Scale-out file and object repositories continue to displace traditional block-based Storage Area Networks as unstructured datasets explode in volume, while NVMe-over-Fabrics accelerates block throughput for latency-critical databases. Hyperscalers now bundle storage into broader consumption commitments that compress unit pricing and shorten refresh cycles, yet sovereign-cloud mandates counterbalance the off-premises shift by requiring local copies of sensitive data. Vendors that offer subscription pricing, immutable snapshots, and protocol convergence are well-positioned to capitalize on the expanding opportunity in the next-generation storage market.

Key Report Takeaways

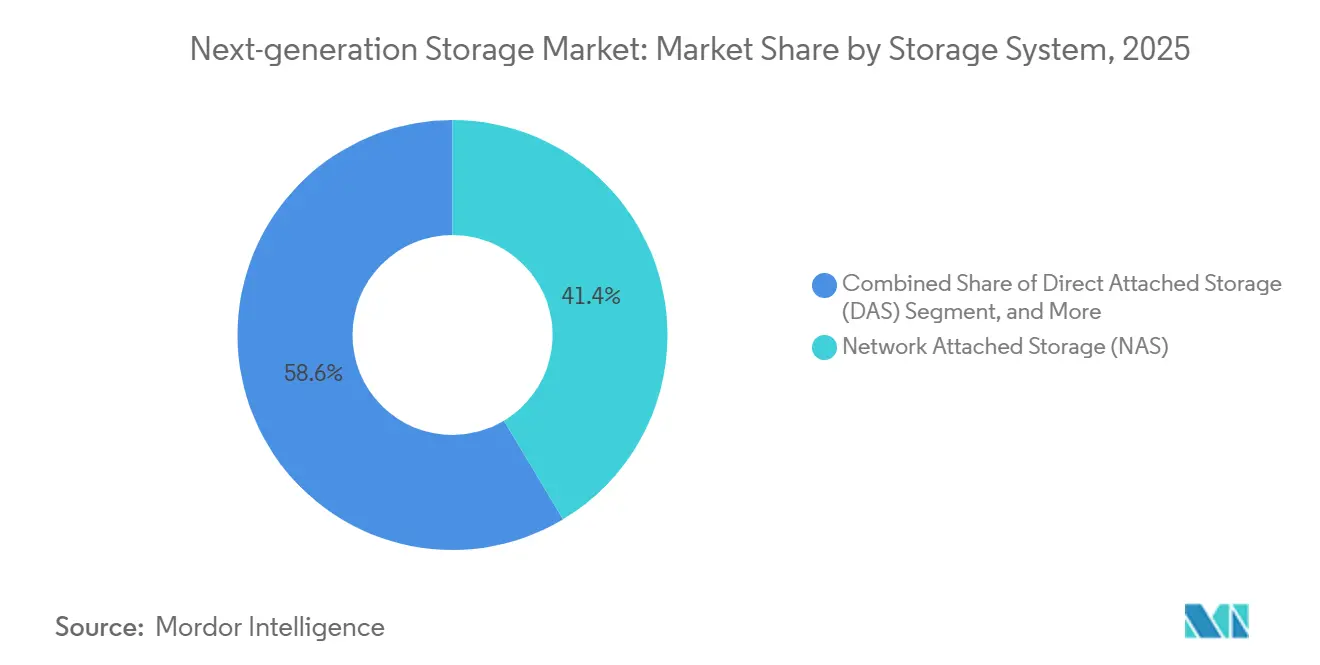

- By storage system, Network Attached Storage (NAS) held a 41.40% revenue share in the next-generation storage market in 2025 and is forecast to expand at a 11.50% CAGR through 2031.

- By storage architecture, file and object-based platforms commanded 57.80% of 2025 revenue, while block storage is expected to grow faster at a 9.46% CAGR to 2031.

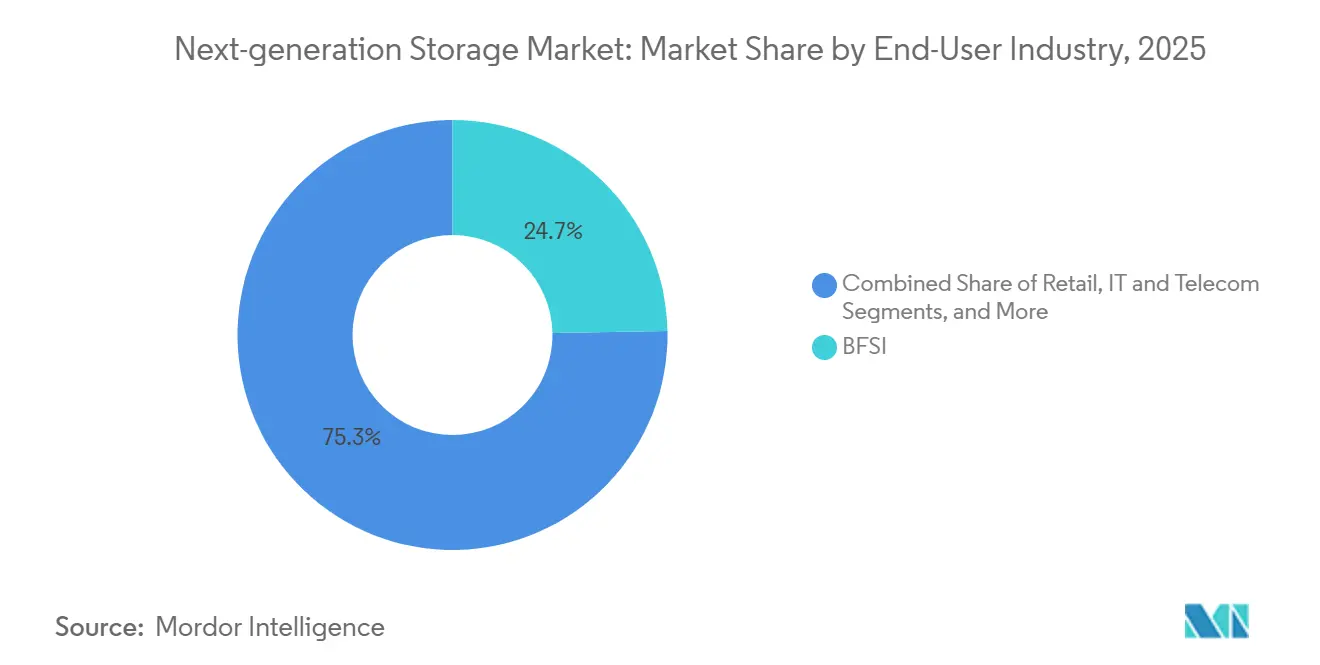

- By end-user industry, the Banking, Financial Services, and Insurance sector led with a 24.70% revenue share in 2025, while the healthcare sector is expected to track the highest CAGR at 14.20% from 2026 to 2031.

- By deployment model, cloud accounted for 56.80% of spending in 2025 and is projected to grow at a 12.80% CAGR through 2031.

- By geography, North America captured 37.46% of 2025 revenue; Africa is the fastest-growing region with a 14.10% CAGR projection to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Next-generation Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI-Driven Demand for Enterprise SSDs | +1.8% | Global, strong in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of Scale-Out NAS in Hybrid Clouds | +1.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| 5G-Enabled Edge Storage | +0.9% | Asia-Pacific core, spillover to North America and Middle East | Long term (≥ 4 years) |

| Regulatory Push for Sovereign Data-Residency Storage | +1.2% | Europe, Middle East, India, Emerging South America | Medium term (2-4 years) |

| Rising Adoption of Solid-State Devices | +0.7% | Global | Short term (≤ 2 years) |

| Increasing Volume of Digital Data | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid AI-Driven Demand for Enterprise SSDs

Generative AI training has turned storage throughput into a competitive differentiator, shrinking refresh cycles from five to three years as hyperscalers adopt all-flash clusters that deliver millions of random read IOPS. Enterprise SSD bit shipments surged 42% year-over-year in 2Q 2025, with Samsung’s PM9E1 and Micron’s 6550 ION surpassing 2 million IOPS in a single drive, enabling one server to replace multiple legacy nodes. Cloud operators now dictate the design of roadmaps, pushing vendors toward higher layer counts and lower power consumption per terabyte, which raises the total available market for next-generation storage.

Expansion Of Scale-Out NAS In Hybrid Clouds

Enterprises consolidating departmental filers onto distributed clusters that automatically tier cold data to public-cloud object stores are fueling double-digit growth in Network Attached Storage. NetApp’s all-flash NAS revenue climbed 28% in fiscal 3Q 2025, while Dell’s PowerScale added native S3 support, allowing the same namespace to span on-premises flash and cloud buckets.[1]Dell Technologies, “PowerScale Storage,” delltechnologies.com By eliminating gateways and manual migrations, scale-out NAS reduces administrative overhead and accelerates data mobility, thereby increasing its market share in the next-generation storage market.

Regulatory Push For Sovereign Data-Residency Storage

The European Union’s Digital Operational Resilience Act and Saudi Arabia’s Personal Data Protection Law mandate that financial and public-sector data remain within national borders, necessitating sovereign clouds that replicate hyperscale functionality under local control. Oracle and Amazon Web Services both launched Europe-only regions staffed exclusively by European nationals, a move that increases infrastructure cost by up to 30% yet unlocks protected revenue streams. Demand for regionalized infrastructure is therefore adding high-margin segments to the next-generation storage market.

5G-Enabled Edge Storage

Low-latency 5G applications, such as autonomous vehicles and augmented reality, require 10 terabytes to 50 terabytes of storage at the tower or campus edge to buffer sensor data before backhaul. Operators in Japan, South Korea, and China deployed more than 120,000 edge nodes in 2025, sparking the development of new product lines, such as Western Digital’s temperature-hardened Ultrastar SN861 SSD. These deployments diversify geographic revenue and cement edge as a durable growth avenue for the next-generation storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Supply-Chain Volatility for NAND Flash | -1.2% | Global, acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Data-Security Breaches in Cloud Services | -0.8% | Global, especially North America and Europe | Medium term (2-4 years) |

| High Up-Front Capex for All-Flash Arrays | -0.5% | Global | Short term (≤ 2 years) |

| Talent Shortage in Storage-Centric DevOps | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Supply-Chain Volatility For NAND Flash

Geopolitical frictions are causing erratic NAND pricing, with contract rates rising 18% in 1H 2025 before falling 8% in 3Q as new South Korean capacity came online. Vendor gross margins compress when hedging at elevated spot levels, prompting some customers to extend hybrid deployments that combine SSDs with hard-disk drives, thereby delaying the full adoption of next-generation storage architectures.

Data-Security Breaches In Cloud Services

Incidents such as the June 2024 Snowflake credential compromise and the February 2024 Change Healthcare ransomware attack have heightened scrutiny of public-cloud controls. IBM calculated the average cost of a cloud-storage breach at USD 4.88 million in 2025, 15% above on-premises incidents. As a result, regulated workloads are repatriating to enterprise-controlled arrays, tempering short-term growth prospects for the next-generation storage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage System: NAS Gains Momentum As Scale-Out Default

Network Attached Storage captured a 41.40% slice of the next-generation storage market share in 2025 and is forecast to climb at an 11.50% CAGR to 2031. The aggressive adoption of scale-out file clusters, which sustain petabyte-scale namespaces for AI training footage, media libraries, and genomics repositories, underpins this growth. Direct-Attached Storage is fading as converged infrastructure allows for pooled capacity, while Storage Area Networks remain relevant for deterministic latency in core banking and airline systems, yet they grow at only 3.2% annually.

The shift reflects the dominance of unstructured data, now accounting for more than 80% of generated bits, which naturally aligns with NAS protocols that permit billions of files in a single namespace. Vendors such as Qumulo report media customers writing 100 GB/s sustained to petabyte clusters, while NetApp’s ONTAP now includes autonomous ransomware detection that snapshots anomalous activity within seconds.[2]NetApp, “ONTAP Data Management Software,” netapp.com Security plus scalability accelerates NAS encroachment into workloads once reserved for object storage, reinforcing the ascendancy of NAS within the next-generation storage market.

By Storage Architecture: NVMe Breathes New Life Into Block Arrays

File and object-based systems controlled 57.80% of revenue in 2025, yet block arrays are on track for a 9.46% CAGR through 2031, reflecting renewed interest in ultra-low latency. SAP HANA, Oracle Exadata, and container persistent volumes rely on atomic writes, which file semantics cannot guarantee, prompting enterprises to adopt NVMe-over-Fabrics arrays that deliver 10 times the throughput of legacy Fibre Channel. Consequently, block arrays are reclaiming relevance for stateful microservices and in-memory analytics, expanding their slice of the next-generation storage market in transactional contexts.

Capacity-oriented archives still favor file and object platforms that deliver exabyte scalability at one-tenth the cost per terabyte. Cloudian claims average customer deployments exceed 5 PB, while Scality’s ARTESCA collapses multi-petabyte repositories into a single namespace with sub-second metadata lookups. This bifurcation leaves little room for hybrid architectures, positioning block storage for performance workloads and file storage for capacity, each integral to the broader next-generation storage market.

By End-User Industry: Healthcare Surges Past Mature BFSI

The Banking, Financial Services and Insurance sector represented 24.70% of 2025 revenue, driven by immutable audit trails and disaster-recovery mandates. Healthcare, however, is advancing at a 14.20% CAGR through 2031, buoyed by FDA guidance that permits cloud-based medical-device data systems, which shift radiology archives into sovereign clouds. Hospitals adopting vendor-neutral archives gain elastic capacity and AI-assisted diagnostics, positioning healthcare as a prime demand vector within the next-generation storage market.

Retail, media and entertainment, and telecommunications follow with edge-native deployments. Walmart now operates 30,000 store-level nodes caching catalogs locally, while Netflix stores more than 15 PB of raw footage in Amazon S3 accessed through gateways that appear as NAS shares. These use cases underscore the diverse industry pull shaping the next-generation storage market.

By Deployment Model: Cloud Dominates But Hybrid Persists

Cloud captured 56.80% of spending in 2025 and is projected to rise at a 12.80% CAGR through 2031 as hyperscalers eliminate same-region egress fees and introduce tiered pricing for AI training datasets. On-premises arrays hold a 28% share, driven by ultra-low-latency databases and air-gapped ransomware recovery vaults, although annual growth barely surpasses 2%. Hybrid models occupy the remaining 15.20% and are scaling at 8.5% CAGR, propelled by platforms that mirror on-premises snapshots into cloud buckets without disrupting applications.

Dell’s 2025 survey found 67% of enterprises operate across three or more clouds, but fewer than one-quarter automate data placement. NetApp Cloud Volumes ONTAP offers a uniform control plane that removes provider lock-in, while Pure Storage Portworx replicates Kubernetes volumes across regions for continuous availability. These capabilities transform the hybrid from a transitional compromise into a permanent operating model. As a result, the next-generation storage market size linked to hybrid deployments will continue to expand steadily, even as cloud continues to absorb the majority of new workloads.

Geography Analysis

North America held 37.46% of 2025 revenue, reflecting dense hyperscale footprints in Virginia, Texas, Oregon and Iowa. Spending tilts toward performance upgrades like Frontier’s 700 PB all-flash supercomputer in Tennessee. Canada’s data-residency rules spurred AWS to add a Calgary region in 2025, while Mexico’s nearshoring boom fuels edge deployments.

Europe fragments along sovereignty lines as the Digital Operational Resilience Act enforces EU-resident replicas, prompting Oracle and AWS to open Europe-only regions. Germany’s cybersecurity agency recommends on-premises arrays for classified workloads, slowing cloud migration, whereas post-Brexit United Kingdom institutions leverage U.S. regions for cost advantage.

Africa is the standout, predicted to grow at 14.10% CAGR to 2031. Microsoft Azure’s Kenya launch and Google Cloud’s forthcoming Lagos region satisfy in-country data mandates, catalyzing local adoption. Parallel momentum in the Middle East and South America rounds out the regional mosaic that sustains the next-generation storage market.

Regulatory Landscape

Regulation for next-generation storage increasingly combines cybersecurity controls with data-sovereignty and cross-border transfer requirements. NIST updated SP 800-209 on February 3, 2025, reinforcing security guidance for storage infrastructure used in enterprise and cloud deployments. In Europe, the EU Data Act began staged implementation from September 12, 2025, shaping interoperability and access obligations that vendors need to reflect in cloud-native and software-defined storage control planes.

Data residency and lawful transfer frameworks continue to influence region and architecture choices for regulated workloads. The EU-US Data Privacy Framework remains a primary mechanism for transatlantic data transfers as of July 2026, supported by an adequacy decision validated by the EU General Court in September 2025. Sovereign-cloud mandates such as the EU Digital Operational Resilience Act and Saudi Arabia's Personal Data Protection Law also reinforce in-country storage and replica requirements for financial and public-sector data. Energy-use transparency is becoming more visible in compliance programs, for example through Ofgem license conditions that require storage providers to record and report facility-specific electricity consumption data.

Value Chain Analysis

The value chain spans upstream NAND and controller IP, SSD manufacturing and qualification, storage-system OEM integration (arrays, scale-out NAS, object platforms, and NVMe-over-Fabrics), and downstream channels delivering on-premises, cloud, and hybrid services to enterprises. On the component side, roadmap cadence and yields in advanced NAND directly affect available capacities, power per terabyte, and BOM costs for all-flash systems: SK hynix began mass production of 321-layer 2Tb QLC NAND in August 2025, and Kioxia announced CM9 Series PCIe 5.0 NVMe SSD development in May 2025 using its 8th generation BiCS FLASH TLC 3D memory. These transitions raise the emphasis on qualification, firmware, and endurance validation across hyperscale and enterprise profiles.

Midstream, system vendors and cloud providers package flash, networking, and software into subscription and consumption models, with integration increasingly shaped by AI clusters and edge deployments that require predictable latency and fast rebuilds. Downstream demand from hyperscalers and large enterprise data centers is also tightening linkages to data center construction, power, and rack-level integration: in July 2026, Meta Platforms revised its investment plan to exceed USD 50 billion to expand its Hyperion data center campus in Richland Parish, Louisiana to 5GW, underscoring how storage demand ties to facility scale and power delivery. Across the chain, supply security and geopolitical volatility keep second-sourcing and regional procurement on the agenda for both component makers and storage-platform vendors.

Competitive Landscape

The next-generation storage market is moderately concentrated: the top five vendors, Dell Technologies, Hewlett Packard Enterprise, NetApp, Pure Storage, and Hitachi Vantara, command 42% of global revenue, yet none exceeds 15%. Incumbents are pivoting to subscription pricing, evidenced by Dell APEX’s 47% bookings growth and Pure Storage Evergreen’s 73% attach rate. This transition smooths revenue while compressing near-term growth.

Edge storage for 5G, sovereign-cloud mandates, and AI-optimized arrays form lucrative white spaces. Challengers such as Qumulo, Cloudian, and VAST Data are capturing unstructured workloads using disaggregated architectures that scale compute and storage independently. Chinese vendors Huawei and Inspur are winning in Asia-Pacific and Africa with 30%-40% lower pricing, backed by government incentives.[3]Financial Times, “Chinese Storage Vendors Gain Share in Emerging Markets,” ft.com

Patent activity suggests that the next front in competition will be computational storage and NVMe-over-TCP, rather than raw capacity. Over 60% of storage patents filed in 2024-2025 target in-situ analytics, suggesting performance differentiation will shift from controller throughput to data-centric processing.

Next-generation Storage Industry Leaders

Dell Inc.

Hewlett Packard Enterprise Company

NetApp Inc.

IBM Corporation

Pure Storage

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is storage engineered for AI data pipelines and inference, where performance and cyber resilience are treated as platform attributes rather than add-on tools. In June 2026, Gartner positioned cyberstorage as a baseline enterprise expectation, reinforcing demand for immutable snapshots, anomaly detection, and clean-recovery capabilities integrated into file, object, and block platforms used for AI and analytics datasets. Vendor roadmaps increasingly highlight packaging and controller advances that translate into higher density and better performance per watt across next-generation arrays and scale-out systems, aligning refresh cycles with AI throughput requirements.

Another opportunity is in convergence between high-performance flash tiers and longer-term, high-density archival approaches as data growth pushes organizations toward more explicit tiering strategies across cloud and on-premises. Huawei outlined a longer-horizon technology roadmap in its Data Storage 2030 white paper, including high-capacity SSD concepts and advanced packaging approaches, while NVMe work such as NVMe 2.3 under active development and emerging PCIe 6.0 controller demonstrations, including Phison at Computex 2026, point to continued headroom for NVMe-based performance storage. These shifts create room for vendors that can combine NVMe-scale performance with simpler hybrid data mobility and stronger governance for sovereign and regulated datasets.

Recent Industry Developments

- July 2026: Dell launched PowerRack, a turnkey rack-scale solution that combines compute, storage, and networking, with storage configurations planned for 2H 2026. The release packages infrastructure as an integrated system for AI factory-style deployments, tightening Dell's linkage between server platforms and next-generation storage modernization programs.

- June 2026: Everpure introduced Everpure Data Stream and Everpure Data Intelligence (based on acquired 1touch.io technology) to improve AI workload data pipelines. The release pushes storage-adjacent software toward governed data movement and classification, supporting enterprise efforts to feed AI models while maintaining control over sensitive datasets.

- June 2024: The Snowflake credential compromise and the Change Healthcare ransomware attack elevated scrutiny of cloud controls for storage and data platforms. These incidents reinforced demand for immutable backups, rapid recovery, and tighter identity and access governance across cloud and hybrid storage estates.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the next generation storage market is defined as revenue earned from modern enterprise and cloud storage systems and architectures that store, protect, and recover growing volumes of data, including large unstructured datasets, across key industries and regions.

Scope exclusions: Consumer retail storage devices for personal use and standalone removable media are excluded when they are not part of an enterprise or cloud storage solution.

Segmentation Overview

- By Storage System

- Direct Attached Storage (DAS)

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- By Storage Architecture

- File and Object-Based Storage (FOBS)

- Block Storage

- By End-User Industry

- BFSI

- Retail

- IT and Telecom

- Healthcare

- Media and Entertainment

- By Deployment Model

- On-Premises

- Cloud

- Hybrid

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and establish the first set of sizing inputs that can be checked consistently across regions. We leaned on public and official sources such as the US Census Bureau, Eurostat, the OECD, the International Telecommunication Union, and World Bank indicators to track digital adoption, connectivity growth, and IT spending direction that impacts storage demand.

Along with those references, we reviewed company annual reports, earnings transcripts, investor presentations, and product literature to understand how storage portfolios are being positioned and priced. Patent databases were also used to identify technology direction, for example changes in controller design, flash and hybrid approaches, and data management features. In countries where trade visibility is available, we selectively used an import export shipment-level database to sanity-check hardware movement patterns. These desk sources are not exhaustive, and additional public references were used during the research process for data collection, validation, and clarifications.

Primary Interviews and Surveys

Primary work was used to validate what was built from desk inputs, especially around adoption timing, pricing movement, and how buyers split storage between on-premises, cloud, and hybrid setups. We spoke with storage solution providers, channel and system integration participants, and enterprise IT buyers across major regions so that demand signals and supply signals could be compared, and any large gaps could be resolved.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 43% |

| Mid tier: 54% | Functional/Unit leaders: 28% | EMEA: 37% |

| Smaller Players: 16% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable storage demand pool using indicators tied to enterprise data creation and storage deployment, then allocates that pool across system and architecture types. To keep it practical, the model is anchored on a limited set of inputs that can be refreshed reliably, such as data center capacity additions, cloud adoption intensity, enterprise workload growth (including backup and recovery needs), relative mix shifts between file, object, and block storage, and typical price per capacity movement for common storage configurations.

Results are corroborated with selective bottom-up approximations to confirm the totals and adjust where needed. This includes sampling supplier revenue exposure to next generation storage, channel checks for shipment and deployment activity, and a volume times average selling price cross-check for a few representative sub-markets. When a data gap appears in a country or a segment, we use proxy variables such as installed IT base, enterprise count in storage-heavy industries, and regional cloud footprint to fill the hole, then re-check through interviews.

For forecasting, scenario analysis is used to translate key drivers into a range, and then a central case is set after reviewing what experts expect for refresh cycles, cloud and hybrid mix changes, and pricing pressure. Where a variable shows a stable historical pattern, simple time-series smoothing is applied to avoid reacting to short spikes. The final forecast is reviewed to keep it consistent with how storage procurement and refresh budgets typically move year to year.

Data Validation & Update Cycle

Validation is done in layers so that one weak input does not overly drive the final number. Model outputs are compared against independent signals such as data center build activity, cloud infrastructure expansion, and observed pricing direction, then reviewed for large variances before sign-off.

If a region or segment shows an unexpected jump, the assumptions are re-checked, the math is traced back to the driver level, and interviews are re-opened to confirm whether the change is real or an artifact of definitions. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is performed so the published view reflects the most current information available at the time.

Mordor Intelligence's Next Generation Storage Market Size Versus Other Published Estimates

Published market sizes for next generation storage often do not match because firms count different parts of the storage stack and they time their pricing and currency assumptions differently. The table shows how those choices can move the market value meaningfully even when the growth direction is similar.

The biggest gap drivers are usually about what is treated as in-scope storage revenue, how cloud and hybrid storage is valued, and whether older storage media and factory gate hardware values are blended into the same total. The table shows a spread that is largely explained by scope. In Mordor Intelligence's model, the market is counted around next generation storage systems, architectures, deployment models, and end-user demand signals rather than including factory gate values of broader device categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 71.26 B (2025) | |

| Technology Research House A | USD 76.98 B (2025) | Uses a technology-led definition that explicitly spans a wider set of next generation data storage technologies (including emerging media categories), which can pull additional revenue pools into the 2025 total. |

| Global Research Group B | USD 94.72 B (2025) | Counts market value at the factory gate and includes a broader device and media scope in its definition of next-generation data storage, which typically inflates the total versus a deployment and architecture focused scope. |

Taken together, the comparison points to definition control as the main reason values diverge, followed by how pricing and currency timing are handled. By keeping the steps tied to observable demand indicators and repeatable cross-checks, the estimate stays easier to audit and update when adoption mix or price per capacity shifts.

Key Questions Answered in the Report

What growth rate is forecast for the next-generation storage market through 2031?

The market is projected to expand at a 5.10% CAGR, climbing from USD 75.30 billion in 2026 to USD 96.55 billion by 2031.

Which storage system is expected to grow fastest?

Network Attached Storage leads with an 11.50% CAGR as scale-out file clusters support AI, media, and genomics workloads.

Why is healthcare adoption accelerating?

FDA approval for cloud-based medical-device data systems and vendor-neutral archives drives a 14.20% CAGR for healthcare deployments.

How are sovereign-cloud rules shaping demand?

Data-residency mandates in the EU, Middle East and India require in-country infrastructure, creating protected, higher-margin segments for vendors.

What technologies underpin block storage’s resurgence?

NVMe-over-Fabrics delivers 10× legacy Fibre Channel throughput, attracting latency-sensitive databases and container persistent volumes.

Which region offers the highest growth potential?

Africa is forecast to post a 14.10% CAGR as Microsoft, AWS and Google open availability zones that satisfy local data laws.

Page last updated on: