Software-Defined Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

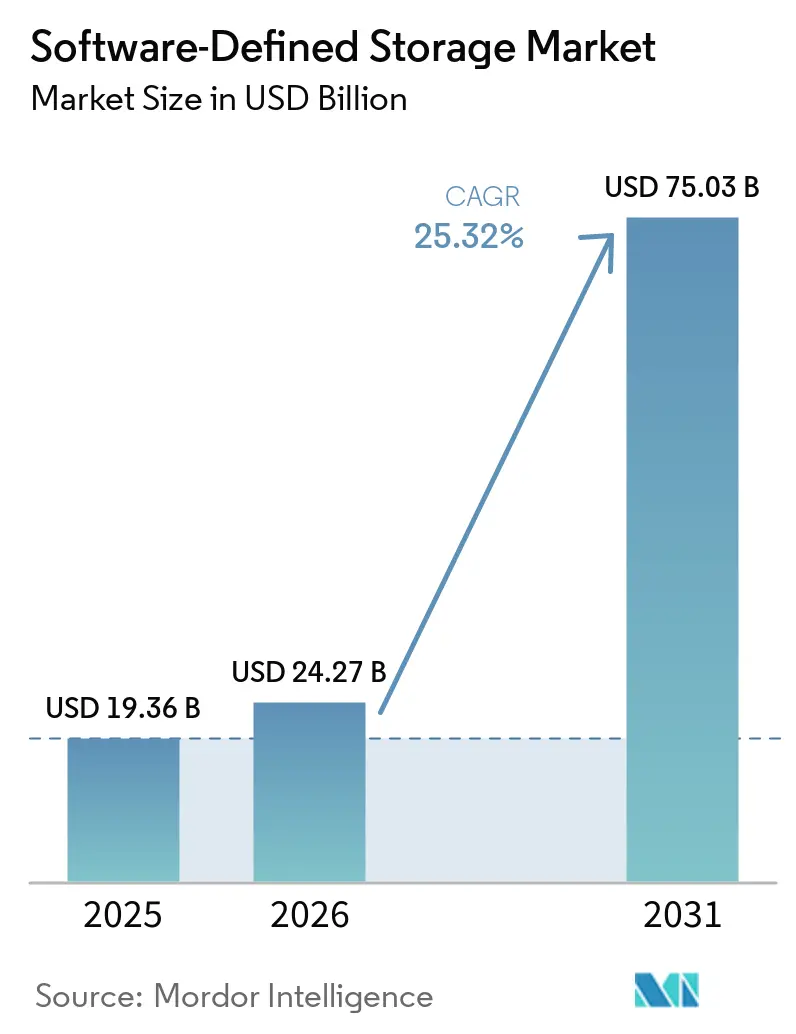

| Market Size (2026) | USD 24.27 Billion |

| Market Size (2031) | USD 75.03 Billion |

| Growth Rate (2026 - 2031) | 25.32% CAGR |

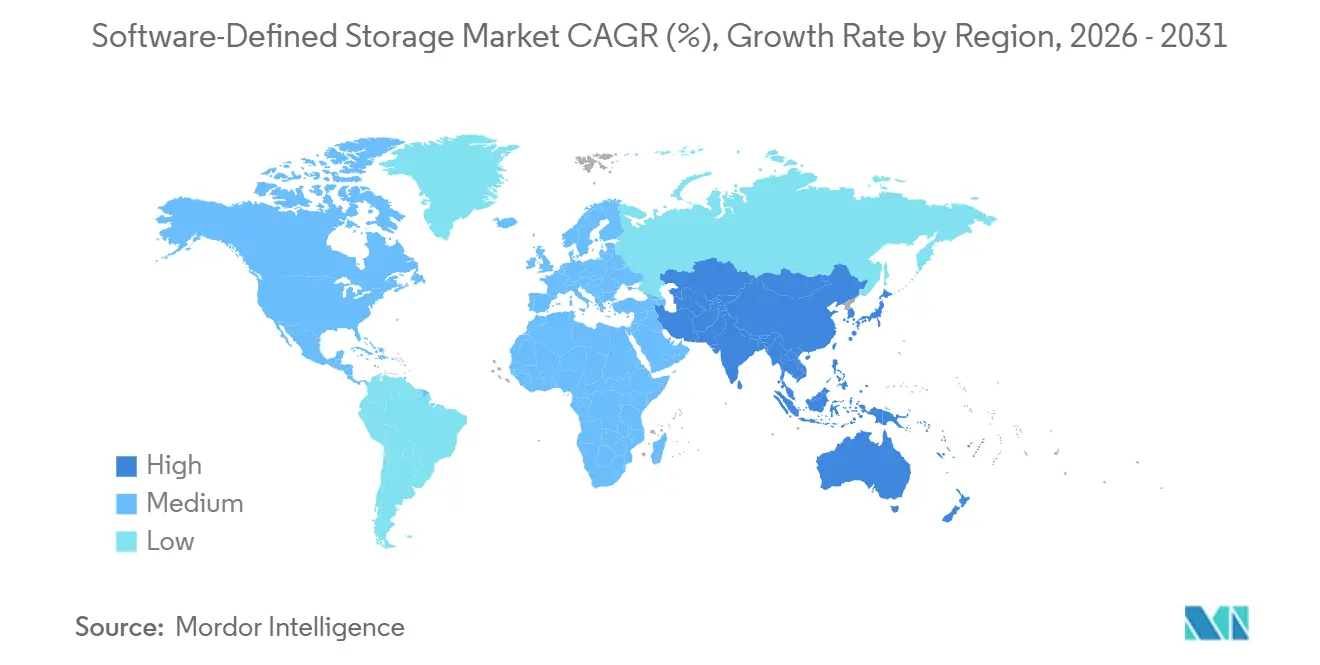

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software-Defined Storage Market Analysis by Mordor Intelligence

The software-defined storage market size reached USD 24.27 billion in 2026 and is projected to climb to USD 75.03 billion by 2031, reflecting a 25.32% CAGR over the forecast horizon. Enterprises are redirecting control from proprietary arrays to software layers that run on commodity x86 servers, lowering capital outlays by 40-60% while maintaining throughput for AI inference workloads. Public-cloud deployments delivered the majority of 2025 revenue, yet hybrid architectures are outpacing at 26.55% CAGR as regulated industries combine on-premises governance with cloud elasticity. Object protocols retained leadership at 42.64% share in 2025 and are expanding at 26.22% CAGR, propelled by S3-compatible APIs that simplify multi-cloud data movement. Large enterprises dominated spending, but small and medium organizations are closing the gap on the back of managed services and consumption-based pricing. Regionally, Asia-Pacific is the fastest riser at 26.45% CAGR, fueled by sovereign-cloud policies and 5G edge buildouts that demand distributed storage nodes.

Key Report Takeaways

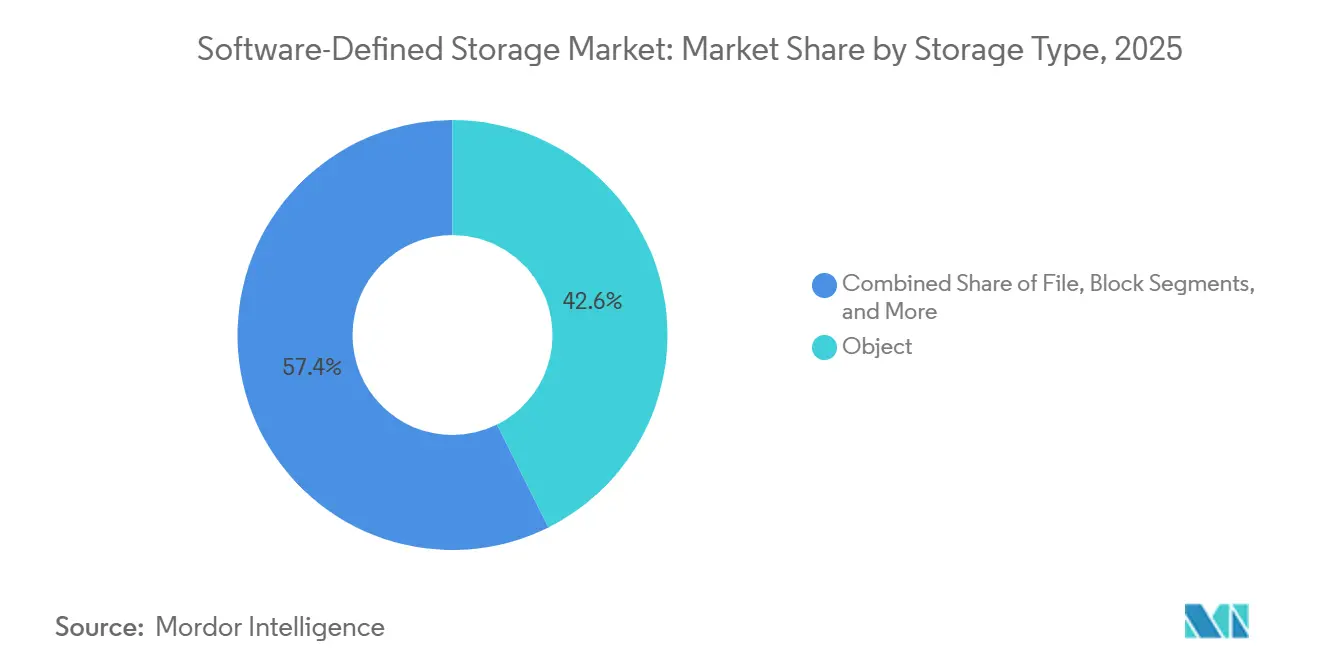

- By storage type, object storage accounted for 42.64% of the software-defined storage market revenue share in 2025, and the segment is forecast to advance at a 26.22% CAGR to 2031.

- By deployment mode, public cloud commanded 55.83% of the software-defined storage market share in 2025, whereas hybrid cloud posts the highest projected CAGR at 26.55% through 2031.

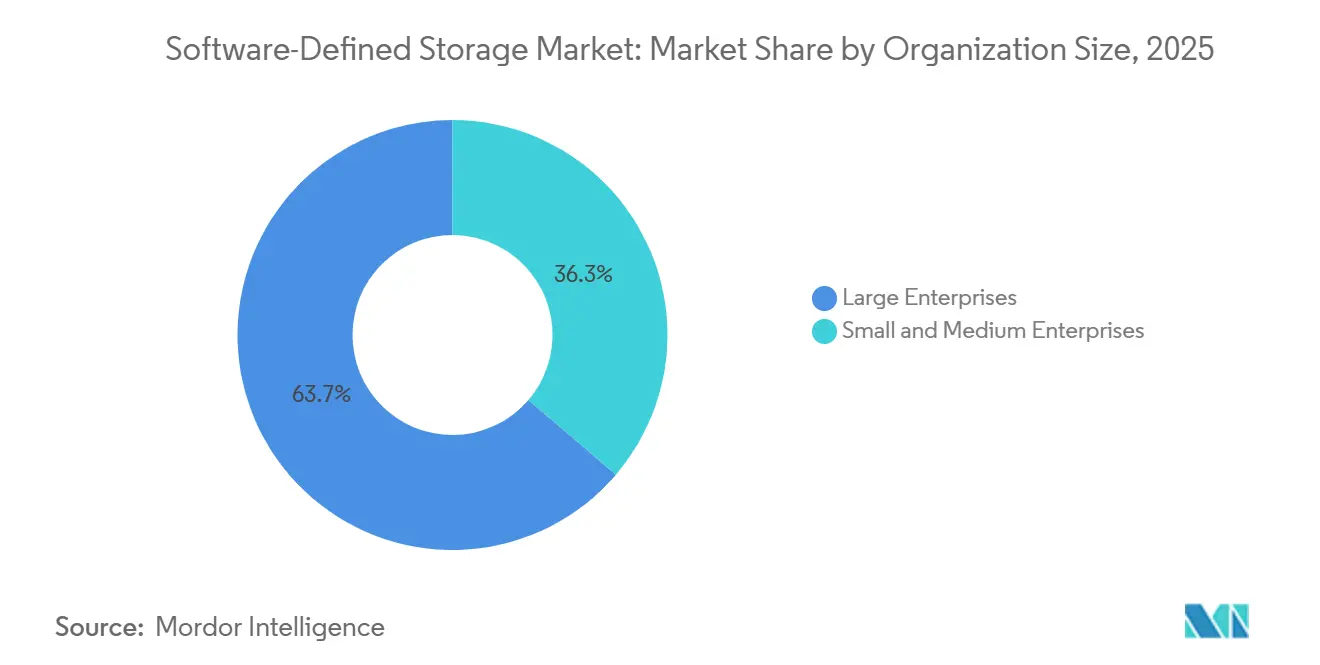

- By organization size, large enterprises accounted for 63.74% of the 2025 spending in the software-defined storage market, whereas small and medium enterprises registered a 26.78% CAGR over the forecast period.

- By end-user industry, BFSI led the software-defined storage market with 34.82% revenue share in 2025, while healthcare is set to grow at a 26.23% CAGR through 2031.

- By region, North America accounted for 38.73% of the 2025 turnover in the software-defined storage market, yet Asia-Pacific is on track for a 26.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Software-Defined Storage Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential growth of unstructured enterprise data | +5.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Cost-advantaged shift from proprietary arrays to commodity hardware | +4.9% | Global, early gains in North America and Europe | Short term (≤ 2 years) |

| Hybrid/multi-cloud adoption demanding storage abstraction | +5.2% | Global, led by North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| AI/ML-driven autonomous storage management and tiering | +3.7% | North America and Asia-Pacific core, emerging in Europe | Long term (≥ 4 years) |

| Container/Kubernetes-native persistent storage needs | +3.4% | Global, concentrated in cloud-native enterprises | Short term (≤ 2 years) |

| Edge computing and 5G creating low-latency SDS nodes | +2.3% | Asia-Pacific and Middle East, spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential Growth of Unstructured Data

The global datasphere expanded to a larger number of zettabytes in 2025, with most of the data comprising unstructured formats, such as video, sensor logs, and imaging files. Traditional scale-up arrays cannot ingest petabyte-per-month volumes economically, so enterprises are adopting horizontally scalable software-defined clusters that stripe metadata across key-value stores for linear capacity expansion. A trade-surveillance system, for example, archives 12 terabytes daily for MiFID II compliance at one-sixth the cost of block storage, thanks to S3 pricing of USD 0.004 per gigabyte-month.[1]Amazon Web Services, “Amazon S3 Pricing,” Aws.amazon.com Manufacturers running computer-vision inspection pump 800 gigabytes of imagery per line per day and need parallel object writes that keep latency under 100 milliseconds.[2]NVIDIA, “AI in Manufacturing: Computer Vision for Quality Inspection,” Blogs.nvidia.com Healthcare entities that rely on HIPAA rules now automate retention in software-defined archives, reducing audit preparation time by 70%.

Cost-Advantaged Shift from Proprietary Arrays to Commodity Hardware

Proprietary arrays cost USD 8-15 per usable gigabyte, while software-defined deployments on x86 servers deliver capacity at USD 0.50-2.00, a 75-90% saving.[3]Dell Technologies, “Software-Defined Storage: Unlocking Flexibility and Cost Savings,” DellTechnologies.com Enterprises extend hardware life by repurposing depreciated compute nodes, postponing USD 2 million in refresh spend for each 10-petabyte estate. NVMe-over-Fabrics eliminates historical latency penalties, enabling distributed storage to match array IOPS density. Emerging ARM-based clusters in India and Indonesia cut power draw 40%, lowering the total cost of ownership by another 18% in high-tariff zones.

Hybrid and Multi-Cloud Adoption Demanding Storage Abstraction

Most enterprises ran workloads across at least two public clouds in 2025. Software-defined layers create a single namespace so an on-premises PostgreSQL instance can migrate to Azure disks or AWS EBS with no code changes. European insurers replicate actuarial models to three clouds and retain 15-minute RPOs to appease Solvency II auditors. Kubernetes clusters rely on CSI drivers such as Rook to surface Ceph storage through YAML manifests, letting developers request persistent volumes without infrastructure tickets.

AI and ML-Driven Autonomous Storage Management and Tiering

Machine-learning models now analyze access patterns to relocate cold objects automatically, dropping storage bills by 42% for seasonal datasets. IBM Spectrum Virtualize uses anomaly detection to rebalance hot spots, removing human intervention for performance tuning. Predictive models ingest NVMe SMART data and forecast drive failures 14 days ahead with 91% accuracy, triggering proactive migrations. Genomics labs gain particular benefit as raw sequencing files shift to USD 0.0004 per gigabyte-month archive tiers once analysis completes, slashing long-term expense by 96%.

Restraints Impact Analysis of Software-Defined Storage Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity with legacy storage estates | -2.1% | Global, acute in North America and Europe with mature IT infrastructure | Short term (≤ 2 years) |

| Shortage of specialised SDS skills and organisational change | -1.8% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Performance determinism concerns for latency-sensitive apps | -1.3% | Global, concentrated in financial services and telecommunications | Medium term (2-4 years) |

| Fragmented standards increasing vendor-lock-in risk | -0.9% | Global, with regulatory pressure in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Storage Estates

Enterprises average 11 disparate storage systems, and migrating petabytes without downtime requires meticulous zoning and LUN mapping. Fibre Channel fabrics depend on proprietary controls that do not translate to NVMe-over-TCP, so protocol gateways add latency and become single points of failure. Legacy backup tools expect tape libraries, forcing virtual-tape emulation layers that dilute cloud economics. Financial institutions on IBM z/OS cannot simply swap FICON storage for x86 targets without recompiling decades-old channel programs. Chain-of-custody proof for data under legal hold further extends migration timelines by up to six months.

Shortage of Specialized SDS Skills and Organizational Change

Only 18% of storage administrators possessed distributed-systems fluency in 2025. Software-defined environments employ Terraform modules and Ansible playbooks, whereas legacy teams rely on GUI tools. Ceph tuning, CRUSH map edits, and erasure-coding math require six to nine months of upskilling. Salaries for Kubernetes storage engineers surpass USD 145,000, a 35% premium over traditional roles, tightening hiring budgets. Organizational silos slow adoption as storage, compute, and network teams defend budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Software-Defined Storage Market Segment Analysis

By Storage Type:

Object Protocols Extend Lead Amid AI Data LakesObject storage controlled 42.64% of the software-defined storage market share in 2025 and is forecast to grow at 26.22% CAGR on the back of S3 APIs that unify data lakes spanning on-premises and cloud buckets. The segment benefits from erasure coding that delivers eleven nines of durability at sub-USD 0.004 per gigabyte-month, reinforcing cost leadership. Block storage remains entrenched for latency-sensitive databases, integrating NVMe-over-TCP to push microsecond IOPS envelopes. File gateways layered on object back ends preserve SMB and NFS workflows for enterprise shares, broadening adoption in departmental use cases. Hyper-converged infrastructure weaves compute and storage on the same node, appealing to mid-market IT shops seeking turnkey installs. Regulatory influence steers healthcare toward object setups with WORM guarantees, while trading desks still pin core ledgers on block volumes to ensure predictable microsecond write response. The software-defined storage market size for object platforms is on track to double by 2031, supported by AI model training pipelines that demand parallel reads across thousands of GPUs. Vendors are adding GPU-direct protocols that bypass CPU copies and shave seconds off epoch times, further widening the gap with legacy arrays.

Object implementations now offer high-performance tiers using NVMe SSDs and low-cost HDD tiers in a single namespace, letting administrators define policies that age seldom-accessed logs automatically. MinIO and Ceph have shipped erasure-coding improvements that hit 90% storage efficiency on 16+4 layouts, narrowing the capacity overhead versus RAID 6. Meanwhile, cloud providers roll out single-zone turbo tiers offering sub-millisecond access for AI training, showing that object storage can satisfy both throughput and latency workloads. As enterprises adopt microservices, each service logs events directly to object buckets, eliminating the need for file systems and simplifying DevOps pipelines. Expect the software-defined storage market to see deeper convergence where object, file, and block semantics blend, driven by namespace virtualization that abstracts protocol differences.

By Deployment Mode:

Hybrid Cloud Bridges Regulatory GapsPublic cloud captured 55.83% revenue in 2025 as managed services removed procurement friction. Yet hybrid arrangements post a 26.55% CAGR because regulated sectors must keep certain data local while tapping cloud burst capacity. European banks pin primary copies on-premises for GDPR, then replicate anonymized sets to public clouds for fraud analytics, balancing compliance with scale. U.S. federal agencies lean on FedRAMP-authorized regions, but still maintain on-site replicas for continuity plans. Private clouds remain relevant among firms with sunk co-location investments, offering self-service portals that copy the hyperscale user experience. Air-gapped government networks deploy Ceph clusters for classified workloads, illustrating the role of sovereignty. Multi-cloud orchestration tools stitch policies across AWS, Azure, and Google, enabling failover without re-platforming. The software-defined storage market size tied to hybrid modes is projected to outpace pure public cloud spend beyond 2029 as organizations optimize placement for cost, latency, and regulation.

Technical innovation centers on bidirectional data mobility. Vendors now provide policy engines that snapshot on-premises VMware volumes and hydrate them natively into Amazon EBS or Azure Managed Disks. Cloud bursting for render farms has become routine, as studios spin up thousands of spot instances accessing the same object bucket. Disaster recovery RPOs have tightened to under 15 minutes through continuous-replication software that compresses and encrypts changed blocks before streaming them to target regions. Compliance audits cite immutable logs produced by software-defined platforms, reducing manual evidence collection cycles by 30%. Enterprises further adopt edge gateways that cache data locally in branch offices then migrate cold files to cloud archive tiers, reflecting a continuum rather than a binary choice between on-premises and public cloud. Consequently, the software-defined storage market continues its pivot from deployment silos to fluid data fabrics.

By Organization Size:

SMEs Harness Managed Services While Enterprises Centralize GovernanceLarge enterprises represented 63.74% spend in 2025, channeling budgets into global namespaces that span hundreds of sites and cloud accounts. They value fine-grained role-based access and key-management integration with HSM appliances. SMEs, however, register a 26.78% CAGR as consumption billing aligns with opex models and managed services remove the skills barrier. Branch offices deploy storage gateways that sync to cloud buckets, sparing local teams from provisioning arrays. Mid-market manufacturers favor hyper-converged appliances where a single admin can oversee compute and storage through a unified console. Audit burdens trigger uptake of pre-certified solutions embedding SOC 2 and ISO 27001 controls, trimming audit preparation by 60%. The software-defined storage market size attributable to SMEs is expected to triple by 2031 as SaaS vendors embed storage options directly into application subscriptions.

Enterprises with 5,000-plus employees pursue edge use cases as retail chains roll micro data centers into thousands of stores. These nodes run containerized point-of-sale apps that log to local object stores then sync nightly to a central cloud, shrinking latency from 80 to 12 milliseconds. SMEs meanwhile lean on service-provider marketplaces that bundle storage, backup, and ransomware protection into per-user fees. Reseller ecosystems are forming around turnkey clusters delivered as code via Terraform, cutting initial deployment to under one hour. Vendor roadmaps now segment features by tenancy scale, offering simplified dashboards for SMEs and API-driven governance suites for global corporations. As multi-tenant colocation providers adopt software-defined storage, even micro businesses can access enterprise-grade durability without hardware ownership, expanding the software-defined storage market reach.

By End-User Industry:

BFSI Anchors Growth, Healthcare Surges on Imaging AIBFSI consumed 34.82% of 2025 demand, depending on deterministic latency for fraud-detection engines and regulatory archives. Software-defined replicas span three regions to meet the Digital Operational Resilience Act, while encryption keys remain on-premises. Healthcare is the fastest mover at 26.23% CAGR as radiology archives shift from appliances to hybrid object stores integrated with diagnostic AI, reducing study retrieval to sub-2 seconds. Telecommunications operators deploy edge clusters to cache streaming video, cutting backhaul traffic by 40%. Government departments consolidate citizen records and automate FOIA request redaction through metadata tagging. Manufacturing harnesses computer vision to drive 12% scrap reductions by storing labeled defect images used in AI retraining. Media studios render 8K footage from cloud buckets, turning projects 30% faster than tape workflows. The software-defined storage market share of non-BFSI verticals is widening, balancing the previously finance-heavy customer mix.

Compliance frameworks shape solution choice. HIPAA drives object stores with immutable versions, while SEC Rule 17a-4 demands six-year retention of trade confirmations. Telecommunications regulators extend lawful-intercept storage durations, nudging carriers toward scalable clusters. Retail e-commerce platforms replicate product catalogs across continents, ensuring checkout continuity during regional outages. Research institutions ingest exabyte-scale physics data into Ceph clusters for long-term scientific analysis. Across sectors, AI workloads demand parallel I/O to feed GPU pods, and software-defined architectures meet this with RDMA transports that deliver high throughput without proprietary fabrics. Consequently, the software-defined storage market now spans mission-critical finance, life-saving healthcare, and data-hungry entertainment segments alike.

Geography Analysis

North America Software-Defined Storage Market

North America maintained 38.73% of 2025 revenue, buoyed by hyperscaler capital expenditure topping USD 180 billion and early Kubernetes CSI adoption that provisions persistent volumes in seconds. Federal agencies leverage FedRAMP-authorized clouds to slash data-center footprints by 50%. Canadian financial firms comply with PIPEDA by retaining customer data on-premises while analytics run in cloud sandboxes. Mexico’s fintech hubs adopt software-defined storage for real-time payments and data residency mandates.

APAC Software-Defined Storage Market

Asia-Pacific advances at 26.45% CAGR, driven by China’s cybersecurity law, India’s Digital Public Infrastructure, and ASEAN’s 5G edge rollouts. Mainland replicas stay within national borders to meet sovereign-cloud rules. India’s UPI processed 11.6 billion monthly transactions by December 2025, forcing horizontally scalable clusters. Japan’s privacy act catalyzes hybrid deployment among manufacturers and hospitals. South Korean carriers host AR content caches at base stations, cutting latency to 8 milliseconds. ASEAN nations establish sovereign zones that insist on local replicas.

EMEA and South America Software-Defined Storage Market

Europe tightens controls through GDPR and the Digital Operational Resilience Act, pushing automated data classification and immutable audit trails. Germany’s BSI urges multi-region replicas within EU borders. The United Kingdom’s NHS consolidates imaging archives, shrinking radiology report turnaround from 48 hours to 6 hours. France’s Health Data Hub manages 120 petabytes for research while upholding CNIL privacy mandates. South America rides Brazil’s LGPD and Argentina’s data-protection laws, while Middle East programs under Vision 2030 spur hyperscale builds in Riyadh. Africa’s growth accelerates as South African banks and Nigerian fintechs adopt cloud platforms compliant with POPIA.

Competitive Landscape

The software-defined storage market features moderate concentration. The top five suppliers, AWS, Microsoft, Dell Technologies, Hewlett Packard Enterprise, and NetApp, captured near half of 2025 revenue. Hyperscalers embed autonomous tiering that cuts customer spend by 30%, while Azure Blob offers lifecycle automation. Pure Storage counters with Portworx, integrating Kubernetes data services across block, file, and object protocols. NetApp’s ONTAP spans on-premises and cloud footprints, enabling policy-consistent replication.

Open-source stacks grow in verticals seeking transparency. Ceph powers CERN’s physics datasets, confirming resilience at exabyte scale. Red Hat’s OpenShift Data Foundation orchestrates multi-cluster replication in under five minutes, easing disaster recovery. MinIO raised USD 103 million to optimize S3 stores for AI workloads.

Vendor strategies include vertical integration; Dell enhanced PowerStore with AI workload placement, trimming response times by 35%. Horizontal expansion is evident with Nutanix supporting bare-metal Kubernetes to broaden addressable markets. White-space opportunities lie at the edge, where ARM-based servers run low-power clusters for retail and manufacturing. Emerging disruptors such as Qumulo target media studios with 8K-optimized file storage.

Software-Defined Storage Industry Leaders

Oracle Corporation

NetApp Inc.

Huawei Technologies Co. Ltd

Fujitsu Limited

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Software-Defined Storage Market Companies Covered in this Report

- Amazon Web Services, Inc.

- Microsoft Corporation

- International Business Machines Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- NetApp, Inc.

- Huawei Technologies Co., Ltd.

- Hitachi Vantara LLC

- Pure Storage, Inc.

- VMware, Inc.

- Nutanix, Inc.

- Oracle Corporation

- Cisco Systems, Inc.

- Fujitsu Limited

- DataCore Software Corporation

- Red Hat, Inc.

- Scality SA

- Cloudian, Inc.

- Infinidat Ltd.

- StarWind Software, Inc.

- FalconStor Software, Inc.

- Promise Technology, Inc.

- StorPool Storage AD

- MinIO, Inc.

- Qumulo, Inc.

Recent Industry Developments in Software-Defined Storage Market

- December 2025: Pure Storage launched Portworx Data Services 3.0 with sub-60-second RTOs for stateful Kubernetes workloads.

- November 2025: Microsoft extended Azure Elastic SAN to six new regions, delivering shared block storage with five nines availability.

- October 2025: Dell Technologies rolled out PowerStore 4.0 software featuring AI-driven workload placement.

- September 2025: NetApp acquired Instaclustr for USD 619 million to deepen managed open-source database offerings.

Global Software-Defined Storage Market Report Scope

The Software-Defined Storage Market Report is Segmented by Storage Type (Block, File, Object, Hyper-converged Infrastructure), Deployment Mode (On-premises, Private Cloud, Public Cloud, Hybrid Cloud), Organisation Size (Small and Medium Enterprises, Large Enterprises), End-user Industry (Banking Financial Services and Insurance, Telecom and Information Technology, Government and Public Sector, Healthcare and Life Sciences, Manufacturing, Media and Entertainment, Retail and e-Commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Block |

| File |

| Object |

| Hyper-converged Infrastructure |

| On-premises |

| Private Cloud |

| Public Cloud |

| Hybrid Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Telecom and Information Technology |

| Government and Public Sector |

| Healthcare and Life Sciences |

| Manufacturing |

| Media and Entertainment |

| Retail and e-Commerce |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Storage Type | Block | ||

| File | |||

| Object | |||

| Hyper-converged Infrastructure | |||

| By Deployment Mode | On-premises | ||

| Private Cloud | |||

| Public Cloud | |||

| Hybrid Cloud | |||

| By Organisation Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Telecom and Information Technology | |||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Retail and e-Commerce | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving enterprise adoption of software-defined storage?

The primary triggers are 40-60% capital savings from shifting to commodity servers, unified namespaces for hybrid and multi-cloud data, and autonomous tiering that trims operating costs.

How fast is Asia-Pacific spending on software-defined storage growing?

Asia-Pacific spending is advancing at a 26.45% CAGR, propelled by sovereign-cloud regulations and 5G edge deployments.

Which deployment mode is expanding the quickest?

Hybrid cloud is the fastest, with a 26.55% CAGR as firms blend on-premises compliance with cloud scalability.

Why is healthcare the fastest-growing vertical?

Picture archiving systems are moving to hybrid object stores that integrate with AI diagnostics, cutting retrieval times and boosting efficiency, resulting in a 26.23% CAGR.

How do software-defined platforms improve disaster recovery?

Continuous replication and policy-driven snapshots shrink recovery-point objectives to under 15 minutes while enabling cross-cloud failover without rewrites.

Page last updated on: