Americas Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

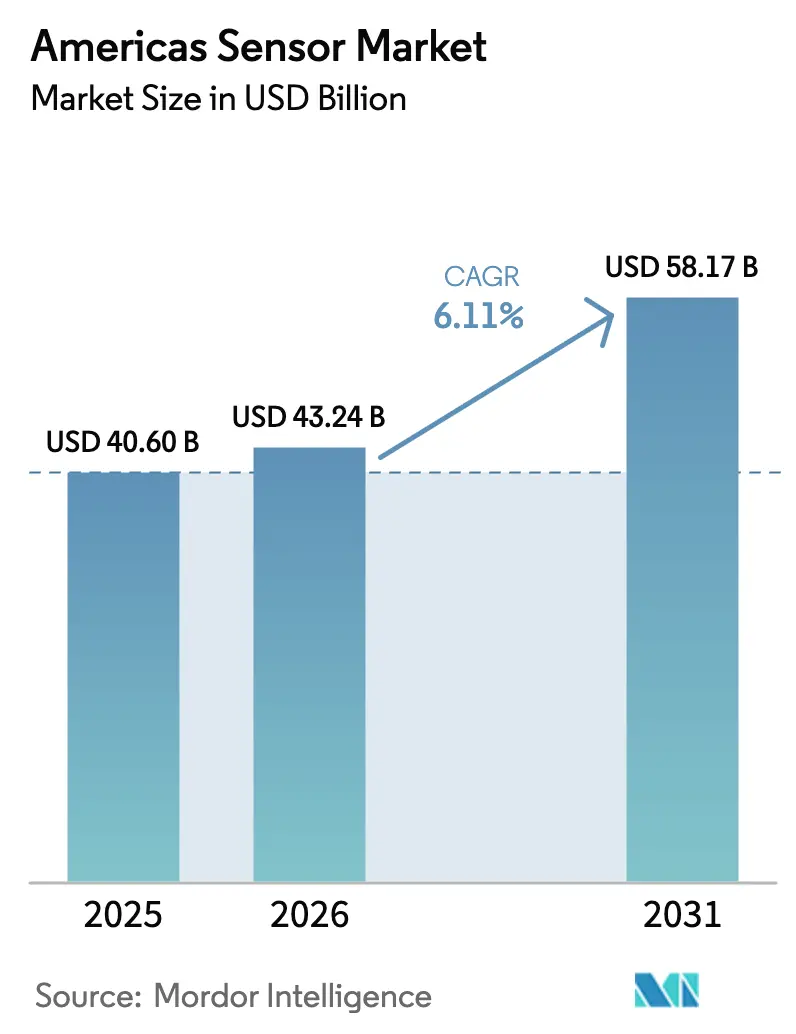

| Base Year Market Size (2025) | USD 40.60 Billion |

| Market Size (2026) | USD 43.24 Billion |

| Market Size (2031) | USD 58.17 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Sensor Market Analysis by Mordor Intelligence

The Americas sensor market size is expected to grow from USD 40.60 billion in 2025 to USD 43.24 billion in 2026 and is forecast to reach USD 58.17 billion by 2031 at 6.11% CAGR over 2026-2031. Accelerating adoption of edge-computing architectures is steering investment toward on-device inference, reducing cloud latency and supporting sovereign-AI mandates across North and South America. Momentum around LiDAR-equipped autonomous fleets and the rapid scale-up of electric vehicles is amplifying demand for multi-modal sensing suites. Fabrication economies of scale in micro-electro-mechanical systems (MEMS) are lowering average selling prices, encouraging substitution for bulk-silicon alternatives. Simultaneously, stricter environmental regulations are widening the commercial runway for chemical and environmental sensors while biodegradable prototypes attract sustainability-focused buyers.

Key Report Takeaways

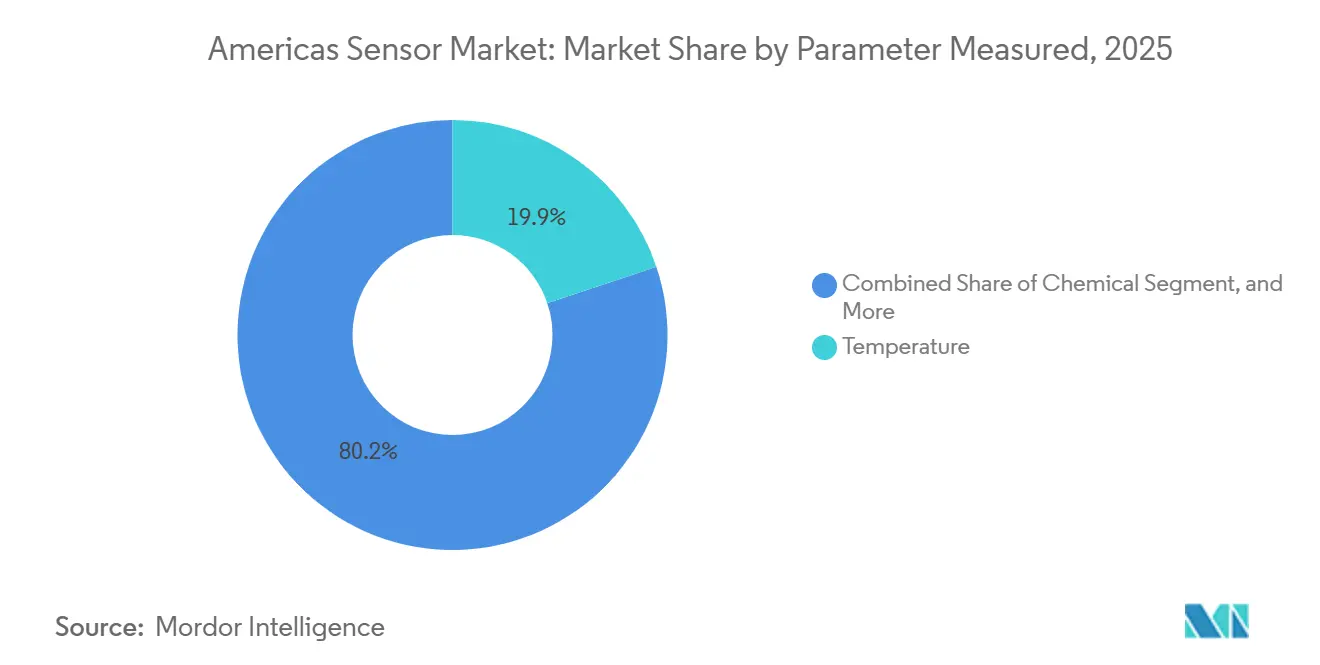

- By parameter measured, temperature devices led with 19.85% of the Americas sensor market share in 2025, whereas chemical sensors are projected to expand at a 6.59% CAGR through 2031.

- By mode of operation, optical sensing commanded 23.43% revenue in 2025, while LiDAR is forecast to grow fastest at 6.96% CAGR between 2026-2031.

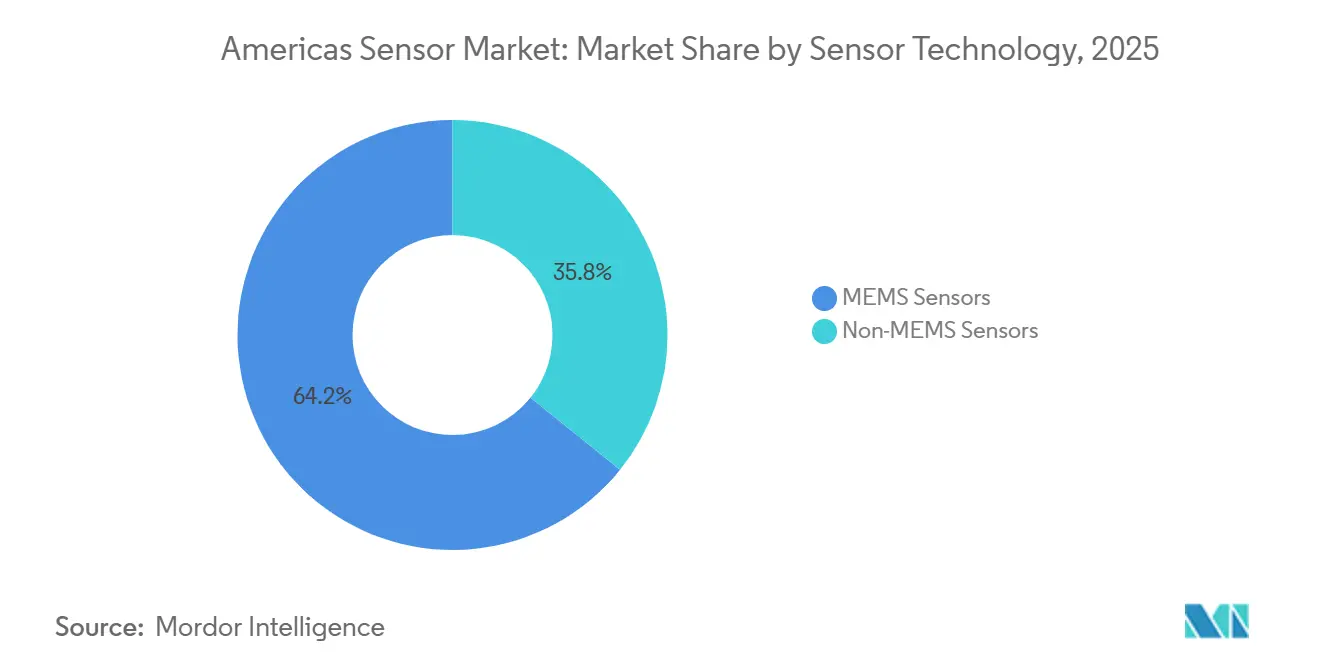

- By technology, MEMS devices accounted for 64.21% of the Americas sensor market size in 2025 and are anticipated to advance at a 7.11% CAGR during the forecast period.

- By end-user industry, automotive applications captured 26.17% revenue in 2025, but medical and wellness end-users are expected to record the highest 7.23% CAGR to 2031.

- By geography, the United States represented 38.34% of 2025 revenue, yet Brazil is predicted to grow at 7.15% CAGR on the back of the MOVER investment program.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of Consumer IoT Devices | +1.20% | North America, with spillover to urban centers in Brazil and Mexico | Medium term (2-4 years) |

| Rising Automation Investments in North and South American Manufacturing | +1.50% | United States, Canada, Mexico manufacturing corridors; São Paulo industrial belt | Long term (≥ 4 years) |

| Government Incentives for Smart-Infrastructure Retrofits | +0.90% | United States (SMART grants), Canada (Infrastructure Bank), Brazil (PAC program) | Medium term (2-4 years) |

| Expansion of Electric and Autonomous Vehicles Requiring Multi-Sensor Suites | +1.80% | United States, Canada; emerging in Brazil, Mexico under MOVER and ProMéxico initiatives | Long term (≥ 4 years) |

| Emergence of Low-Power Edge AI Enabling On-Sensor Analytics | +1.10% | Global, with early adoption in United States tech hubs and Canadian AI research clusters | Short term (≤ 2 years) |

| Growing Demand for Biodegradable Eco-Sensors to Meet ESG Targets | +0.40% | California, European Union subsidiaries in Americas; pilot projects in Chile agriculture | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Consumer IoT Devices

North American shipments reached 1.2 billion units in 2025, embedding temperature, proximity, and inertial components in wearables and home-automation systems.[1]Consumer Technology Association, “2025 North American IoT Shipments,” cta.tech Retailer mandates around the Matter protocol are pushing vendors to preload Bluetooth Low Energy 5.4 and Thread radios inside MEMS packages, trimming external component counts by 40%. Brazil’s ANATEL streamlined certification under Resolution 715, cutting local launch cycles to three months. These regulatory wins, paired with battery-life expectations beyond five years, are elevating ultra-low-power design to a core purchasing criterion. Retrofit gateways translating Zigbee traffic into Matter added USD 380 million in 2025 revenue, reflecting an interim interoperability opportunity.

Rising Automation Investments in Manufacturing

Industrial robot installations in the United States climbed 12% to 44,303 units during 2024, with force-torque, proximity, and vision sensors enabling safe human-robot collaboration.[2]Association for Advancing Automation, “Robot Installations 2024,” automate.org Sensor content per robot rose 28% in Mexico as vibration-monitoring systems cut unplanned downtime by 35%. Eighty percent of surveyed manufacturers now channel at least one-fifth of capital budgets into smart-factory assets where sensing hardware eclipses software on the priority list. Brazil’s Rota 2030 incentives, offering accelerated depreciation for sensor-equipped machinery, fuel retrofits of pre-2015 production lines.[3]Brazilian Ministry of Development, Industry and Trade, “MOVER Incentive Framework,” gov.br The reshoring of 244,940 U.S. jobs during 2024 further brightens domestic sensor demand.

Government Incentives for Smart-Infrastructure Retrofits

USD 85 million in SMART grants funded sensor-rich traffic systems across 12 U.S. municipalities during 2025.[4]U.S. Department of Transportation, “2025 SMART Grant Recipients,” transportation.gov Canada’s Infrastructure Bank pledged CAD 1.2 billion (USD 900 million) to smart-grid projects with power-quality sensors targeting 90% coverage by 2028. Brazil’s Program de Aceleração do Crescimento earmarked BRL 8.5 billion (USD 1.7 billion) to water-network upgrades featuring pressure and flow sensors. These programs favour modular platforms with open APIs, safeguarding municipalities against vendor lock-in. Chile’s 50,000-unit smart-streetlight pilot demonstrated 42% energy savings, encouraging replication in additional cities.

Expansion Of Electric and Autonomous Vehicles

U.S. electric-vehicle sales hit 1.6 million units in 2025, each embedding roughly 35 sensors for battery, current, and climate control compared with 18 in combustion models. Waymo’s 700-vehicle robotaxi fleet deploys 29 cameras, six LiDAR units, and five radar modules per car, generating four terabytes of data daily. Brazil’s MOVER program cut IPI taxes up to 20% for localized sensor output, prompting Bosch’s USD 150 million São Paulo expansion. ISO 26262 certification timelines stretched to two years, delaying some Level 3 autonomy launches. TE Connectivity’s Hermosillo plant, slated to ship 12 million EV temperature sensors annually from Q3 2026, highlights near-shoring traction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Certification for Safety-Critical Sensors | -0.80% | United States (FDA, NHTSA), Canada (Health Canada, Transport Canada), Brazil (ANVISA) | Medium term (2-4 years) |

| High Capital Expenditure for MEMS Fabrication Lines | -1.10% | United States, with limited impact in South America due to reliance on imports | Long term (≥ 4 years) |

| Supply-Chain Concentration in Exotic Materials (GaN, SiC) | -0.70% | Global, with acute pressure on North American EV and power-electronics sectors | Short term (≤ 2 years) |

| Cyber-Security Liabilities Tied to Sensor Data Integrity | -0.50% | United States, Canada; emerging concern in Brazil's industrial automation sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Certification for Safety-Critical Sensors

FDA premarket approvals for Class II and III devices averaged 14 months in 2025, with glucose and pressure sensors requiring ±10% accuracy across diverse cohorts. NHTSA’s June 2025 order mandates real-world performance data for any Advanced Driver Assistance System sensor tied to a crash, adding USD 2-3 million in annual compliance for tier-1 suppliers. Brazil’s ANVISA Resolution 822 now obliges local trials even when FDA clearance exists, effectively doubling time-to-market and giving domestic vendors an 18% share in consumer wellness wearables. Divergent rules across the Americas force vendors to maintain multiple product variants and documentation sets, inflating fixed costs and deterring small entrants. Harmonization lags despite regional trade pacts.

High Capital Expenditure for MEMS Fabrication Lines

A 200-millimeter MEMS fab now costs USD 1.2-1.8 billion, locking technology nodes for up to a decade. Intel’s USD 8.5 billion Ohio investment allocates USD 1.1 billion to MEMS but will not yield volume output until late 2027. Smaller startups pivot to fabless models through X-FAB or Teledyne DALSA, yet minimum orders of 50,000 wafers demand USD 15-20 million in working capital. South America lacks indigenous capacity, relying on imports currently subject to Brazil’s 4% temporary tariff that reverts to 16% in December 2026. Capital intensity, therefore, caps regional diversification and slows new-product cadence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Parameter Measured: Chemical Sensors Gain Ground in Environmental Compliance

Chemical devices are set for the fastest 6.59% CAGR during 2026-2031 as the United States enforces tighter particulate-matter and ozone standards, adding 1,200 continuous-monitoring sites. Temperature units, which held 19.85% of the Americas sensor market share in 2025, remain pivotal in HVAC and cold-chain logistics yet face price erosion that is moderating growth. Pressure products underpin shale extraction, with 8,500 downhole gauges deployed in the Permian Basin in 2025. Level instrumentation supports municipal water plants that collectively oversee 18 billion gallons daily.

Flow sensing in single-use bioreactors advanced when a disposable thermal mass-flow sensor cut validation cycles to three days. Proximity sensors enable 750,000 mobile robots in Amazon facilities, sustaining high-volume demand. Inertial modules, magnetics, vibration, and environmental detectors each address niche but expanding use cases from smartphones to predictive-maintenance suites, underscoring the broad terrain of the Americas sensor market.

By Mode Of Operation: LiDAR Surges with Autonomous Fleets

Optical sensing kept a 23.43% revenue slice in 2025, spanning photodiodes for smartphones and fiber-optic strain gauges on bridges. The Americas sensor market size attached to LiDAR is projected to rise at 6.96% CAGR on the heels of robotaxi scaling, with Waymo cleared to add 200 vehicles in Texas. Electrical resistance elements continue to anchor industrial temperature loops, shipping 12 million units in 2025. Biosensors broadened horizons when Abbott’s continuous ketone monitor secured FDA clearance in August 2025.

Piezoresistive automotive manifold sensors, stacked CMOS image sensors, capacitive touch controllers, piezoelectric ultrasound elements, and radar ICs together provide depth to the Americas sensor market, supporting applications from infotainment to adaptive cruise control. Collectively, these operational modes frame a versatile toolkit serving consumer, industrial, and mobility ecosystems.

By Sensor Technology: MEMS Dominance Reflects Economies of Scale

MEMS commanded 64.21% of 2025 revenue and should accelerate at 7.11% CAGR as 200-millimeter wafer production pushes per-unit costs under USD 0.40 for high-volume motion sensors. The Americas sensor market size devoted to MEMS reflects rapid uptake of wafer-level packaging and through-silicon vias that shrink modules below 1.5 square millimetres, vital for wearables and hearables. Non-MEMS alternatives, while resilient in extreme-temperature or high-overpressure niches, face slower 4.8% CAGR. Honeywell’s bonded-foil strain gauges still win in environments from -65 °C to 260 °C, a range MEMS struggles to match.

The technology gap is widening as intelligent sensor processing units integrate 32-bit cores onto the die, executing AI tasks at microjoule energy budgets. Adoption of RISC-V inside MEMS inertial sensors exemplifies this convergence of computation and sensing. In contrast, discrete thermistors and bulk piezoresistive designs rely on conventional signal chains, limiting miniaturization potential in mass-market electronics.

By End-User Industry: Medical and Wellness Outpaces Automotive

Automotive users retained 26.17% revenue in 2025, but medical and wellness devices are expected to post the top 7.23% CAGR through 2031 as reimbursement now covers continuous vital-sign monitoring. The Americas sensor market benefits from higher sensor density in electric and autonomous vehicles, yet regulatory drag on Level 3 autonomy tempers growth. Consumer electronics represented 22% share, buoyed by smartphones embedding 14 sensors each and wearables shipping 18 million units in 2025.

Energy and utilities drove smart-meter installations to 112 million by end-2025, relying on voltage and power-quality sensing. Industrial automation, construction, mining, aerospace, and defense each extend the demand curve, whether through predictive-maintenance rollouts on 2.8 million monitored assets or autonomous haulage trucks equipped with 18 sensors apiece. Such diversity underpins resilient, multi-sector growth for the Americas sensor market.

Geography Analysis

The United States generated 38.34% of 2025 revenue on the strength of CHIPS Act-backed fabrication, Midwest automotive output, and medical-device clusters. Ongoing fab construction is set to compress lead times from 16 weeks to eight, favourably impacting the Americas sensor market. Brazil is forecast to grow at 7.15% CAGR as MOVER and Rota 2030 incentives attract localized assembly and Industry 4.0 retrofits. Canada’s 8.2% share rides on oil-sands deployments of 22,000 downhole instruments and parts suppliers clustered in Ontario.

Mexico captured 9.1% in 2025, supported by 140 new near-shored manufacturing facilities averaging USD 1.8 million in sensor spend. Argentina is rebounding on lithium projects that installed 8,500 process sensors, accelerating a 5.8% CAGR.

Chile leverages copper-mine automation, installing 4,200 devices in Chuquicamata to trim operating costs by 11%. The rest of South America, including Colombia and Peru, collectively held 4.8%, propelled by smart-city pilots funded by the Inter-American Development Bank.

Competitive Landscape

The top ten suppliers held 52% of 2025 revenue, indicating moderate concentration that still allows specialized entrants to gain niche positions. Integrated analog front ends from Texas Instruments and Analog Devices now merge sensor interfaces, analog-to-digital converters, and signal conditioning, shaving customer design cycles to four months.

Pure-play firms such as Sensata and TE Connectivity expand vertically into module assembly and analytics to capture system-level margins. Patent filings hit 4,800 in 2025, emphasizing edge-AI inference and biodegradable substrates.

Disruptors include Wiliot, which raised USD 200 million for battery-free Bluetooth tags harvesting ambient RF, slashing operating costs in cold-chain logistics. Automotive original-equipment manufacturers like Tesla tape-out proprietary radar ASICs that trim per-vehicle sensor spend by USD 120 while boosting classification accuracy. Standards bodies continue to shape competition; firms active in ISO and IEC working groups can align new formats with their product roadmaps, erecting subtle entry barriers.

Americas Sensor Industry Leaders

ABB Limited

NXP Semiconductors

Honeywell International Inc.

Texas Instruments Incorporated

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: STMicroelectronics announces acquisition of NXP’s sensor business for USD 950 million, expanding MEMS and automotive portfolios.

- July 2025: Honeywell secures U.S. Department of Defense contracts for GPS-independent quantum navigation systems.

- June 2025: Boeing completes first quantum-navigation flight test using AOSense IMUs.

- March 2025: SICK and Endress+Hauser commence joint-venture operations focused on gas analysis and flow measurement.

Americas Sensor Market Report Scope

The Americas Sensor Market Report is Segmented by Parameter Measured (Temperature, Pressure, Level, Flow, Proximity, Environmental, Chemical, Inertial, Magnetic, Vibration, Other), Mode of Operation (Optical, Electrical Resistance, Biosensor, Piezoresistive, Image, Capacitive, Piezoelectric, LiDAR, Radar, Other), Sensor Technology (MEMS, Non-MEMS), End-User Industry (Automotive, Consumer Electronics, Energy and Utilities, Industrial Automation, Medical and Wellness, Construction Agriculture and Mining, Aerospace, Defense and Security), and Geography (United States, Canada, Brazil, Mexico, Argentina, Chile, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Temperature |

| Pressure |

| Level |

| Flow |

| Proximity |

| Environmental |

| Chemical |

| Inertial |

| Magnetic |

| Vibration |

| Other Parameter Measured |

| Optical |

| Electrical Resistance |

| Biosensor |

| Piezoresistive |

| Image |

| Capacitive |

| Piezoelectric |

| LiDAR |

| Radar |

| Other Mode of Operation |

| MEMS Sensors |

| Non-MEMS Sensors |

| Automotive | |

| Consumer Electronics | Smartphones |

| Tablets, Laptops and Computers | |

| Wearable Devices | |

| Smart Appliances | |

| Other Consumer Electronics | |

| Energy and Utilities | |

| Industrial Automation | |

| Medical and Wellness | |

| Construction, Agriculture and Mining | |

| Aerospace | |

| Defense and Security |

| North America | United States |

| Canada | |

| South America | Brazil |

| Mexico | |

| Argentina | |

| Chile | |

| Rest of South America |

| By Parameter Measured | Temperature | |

| Pressure | ||

| Level | ||

| Flow | ||

| Proximity | ||

| Environmental | ||

| Chemical | ||

| Inertial | ||

| Magnetic | ||

| Vibration | ||

| Other Parameter Measured | ||

| By Mode of Operation | Optical | |

| Electrical Resistance | ||

| Biosensor | ||

| Piezoresistive | ||

| Image | ||

| Capacitive | ||

| Piezoelectric | ||

| LiDAR | ||

| Radar | ||

| Other Mode of Operation | ||

| By Sensor Technology | MEMS Sensors | |

| Non-MEMS Sensors | ||

| By End-User Industry | Automotive | |

| Consumer Electronics | Smartphones | |

| Tablets, Laptops and Computers | ||

| Wearable Devices | ||

| Smart Appliances | ||

| Other Consumer Electronics | ||

| Energy and Utilities | ||

| Industrial Automation | ||

| Medical and Wellness | ||

| Construction, Agriculture and Mining | ||

| Aerospace | ||

| Defense and Security | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Americas sensor market in 2026?

The market is projected at USD 43.24 billion in 2026.

Which parameter segment is growing fastest across the region?

Chemical sensors lead with a forecast 6.59% CAGR through 2031.

Why are MEMS devices dominant in the Americas?

Wafer-level economies of scale push per-unit costs below USD 0.40, giving MEMS 64.21% share in 2025 and a 7.11% growth trajectory.

What geographic area offers the highest growth potential?

Brazil is forecast to expand at 7.15% CAGR, spurred by automotive and Industry 4.0 incentives.

How will new IoT security rules affect suppliers?

From March 2026, NIST mandates cryptographic attestation, adding 12-15% to compliance costs yet strengthening device integrity.

What is the outlook for sensor demand in autonomous vehicles?

LiDAR and multi-sensor suites should accelerate as U.S. robotaxi fleets expand, supporting a 6.96% CAGR for LiDAR through 2031.

Page last updated on: