Depth Sensing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

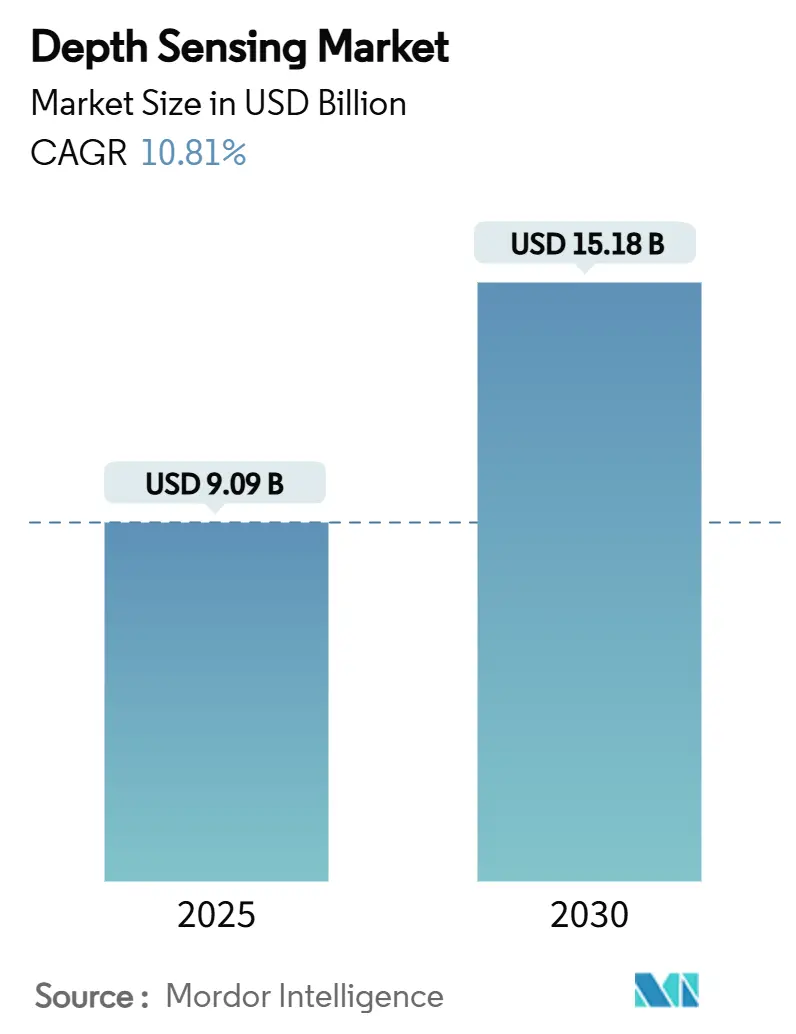

| Market Size (2025) | USD 9.09 Billion |

| Market Size (2030) | USD 15.18 Billion |

| Growth Rate (2025 - 2030) | 10.81% CAGR |

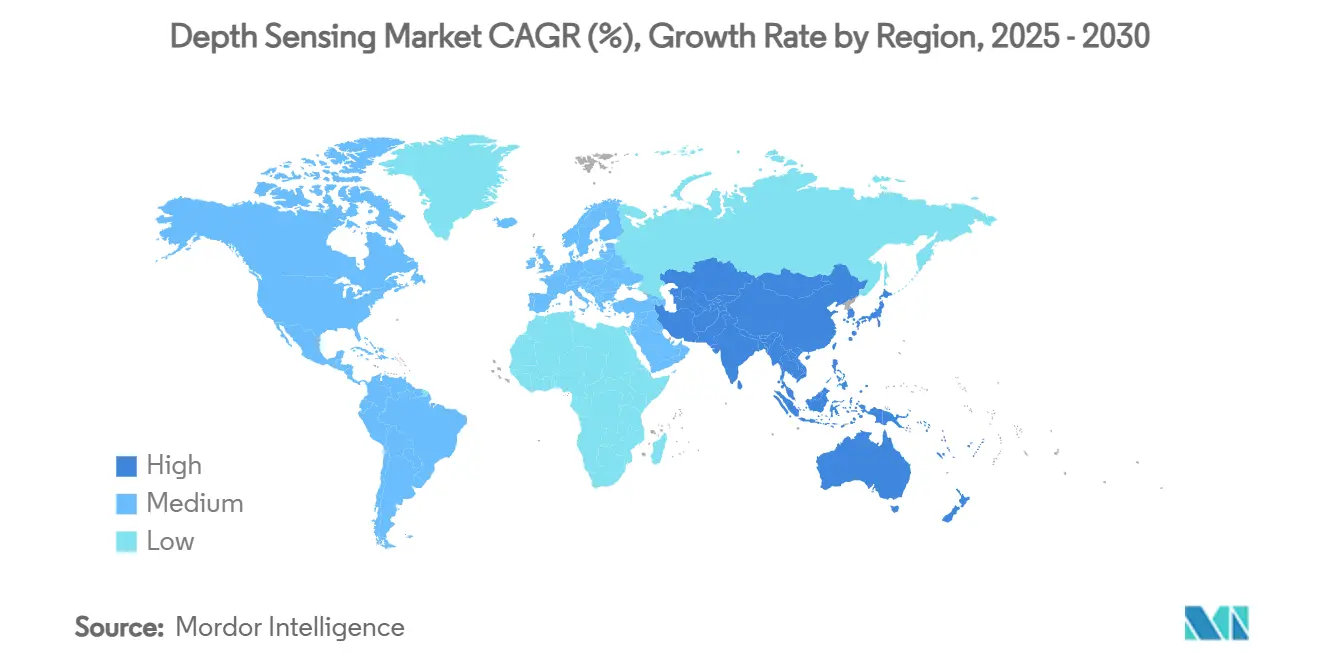

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

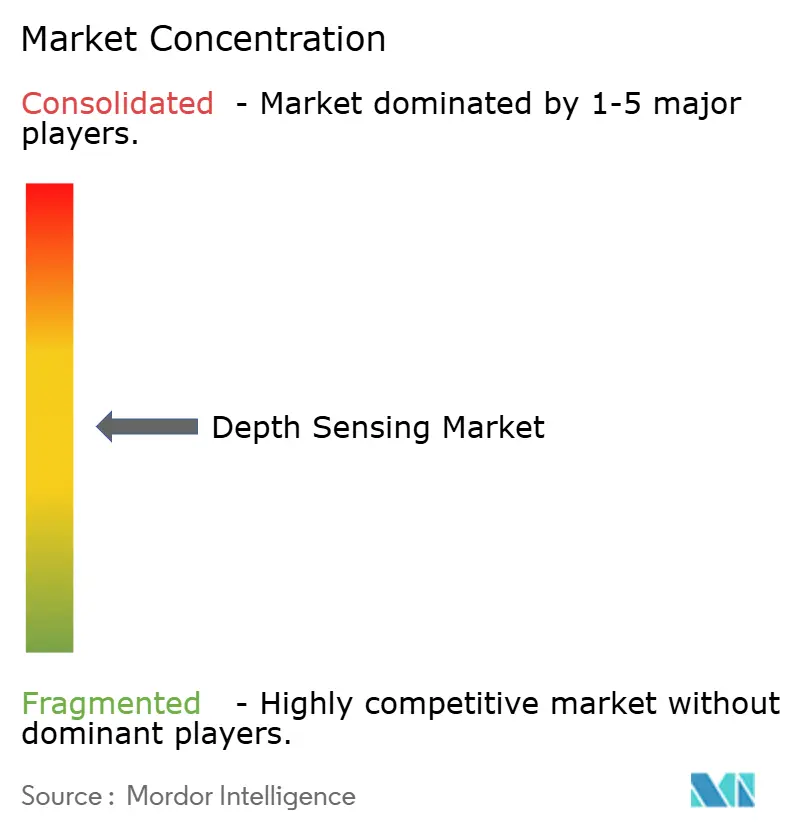

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Depth Sensing Market Analysis by Mordor Intelligence

The depth sensing market size stood at USD 9.09 billion in 2025 and is forecast to reach USD 15.18 billion by 2030, growing at a 10.81% CAGR over the period. This expansion reflects mainstream adoption across automotive, consumer electronics, and industrial verticals as artificial-intelligence processing converges with optical-sensing hardware. Production-scale LiDAR in passenger vehicles, 3D cameras in smartphones, and factory automation solutions are reducing unit costs and opening previously uneconomical use cases. Chinese suppliers have leveraged manufacturing scale to accelerate cost compression, while leading component makers in Japan, the United States, and Europe continue to introduce high-performance sensors tailored for long-range and harsh-environment operation. Regulatory mandates for driver-monitoring and collision-avoidance functions further reinforce long-term demand, offsetting cyclical softness in consumer segments. The resulting shift from experimental trials to volume deployment underpins a competitive race centred on ecosystem control, rather than isolated component performance.

Key Report Takeaways

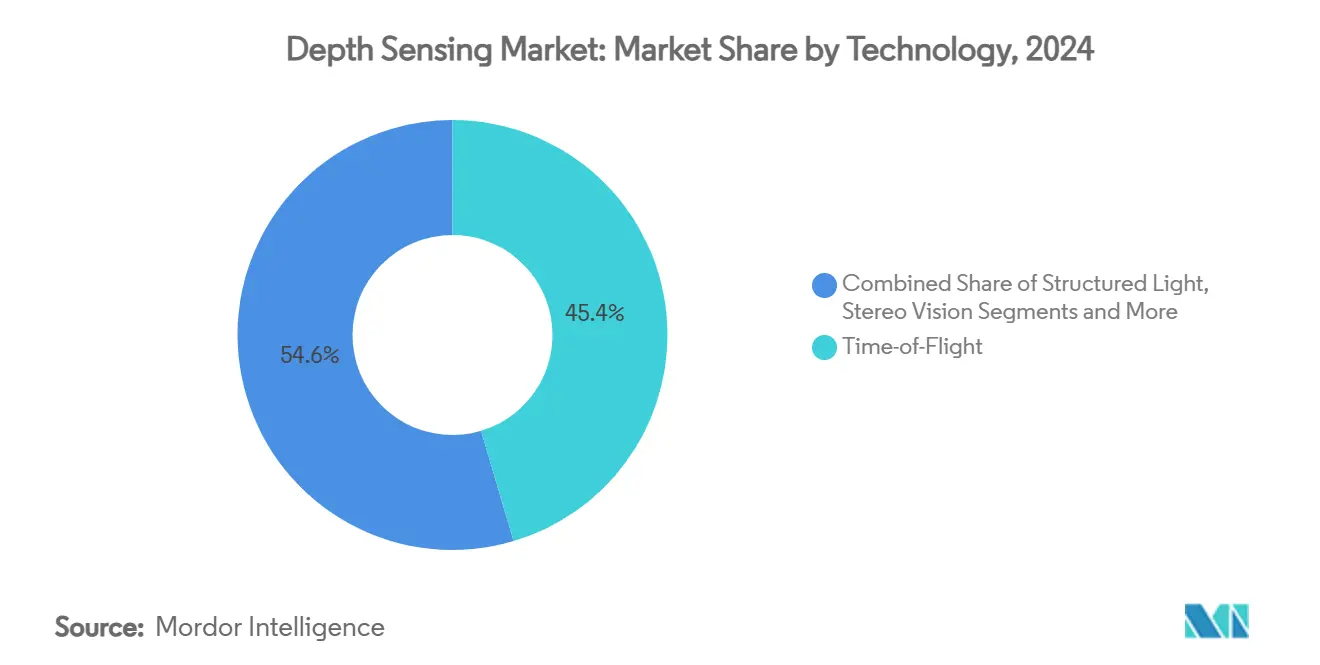

- By technology, Time-of-Flight held a 45.4% revenue share in 2024, while Flash LiDAR is forecast to expand at an 11.2% CAGR through 2030.

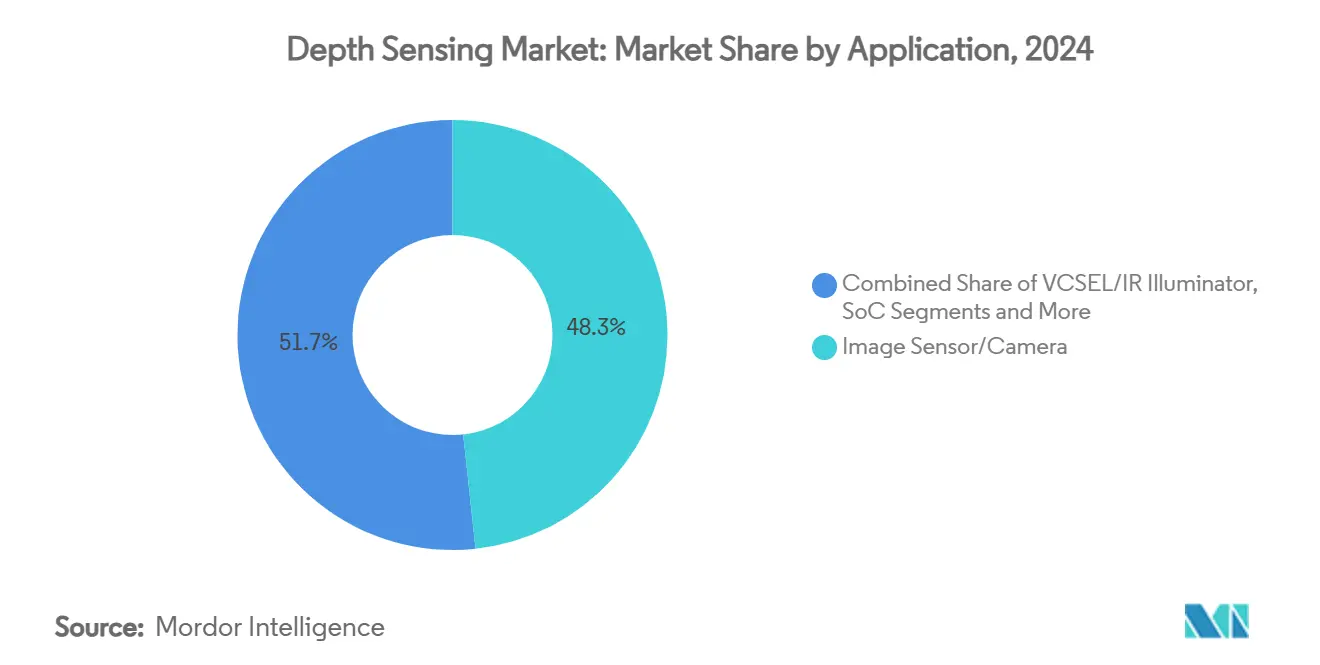

- By component, image sensors and cameras accounted for 48.3% of 2024 sales, whereas software and algorithms represent the fastest-growing sub-sector at an 11.3% CAGR to 2030.

- By application, consumer electronics retained 38.5% market share in 2024, but automotive ADAS and autonomous-vehicle systems are projected to grow at an 11.6% CAGR over the forecast window.

- By range, short-range deployments (<5 m) captured 56.7% of 2024 revenue, and long-range installations (>30 m) will advance at an 11.5% CAGR to 2030.

- By geography, North America led with 32.4% of 2024 revenue, while the Asia–Pacific region is poised to register an 11.7% CAGR during 2025-2030.

Global Depth Sensing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone OEM adoption of 3D face-authentication modules | +1.8% | Global; APAC manufacturing hubs | Medium term (2-4 years) |

| Surge in automotive LiDAR for ADAS and autonomy | +2.3% | North America, EU, APAC production centres | Long term (≥ 4 years) |

| Rapid AR/VR headset deployment | +1.5% | North America, EU early markets; APAC manufacturing | Medium term (2-4 years) |

| Edge-AI accelerators enabling on-device depth processing | +1.2% | Global; data-centre regions first adopters | Short term (≤ 2 years) |

| Retail shelf-analytics to offset labour shortages | +0.9% | North America, EU; developed APAC | Medium term (2-4 years) |

| Regulatory push for in-cabin occupant monitoring | +1.4% | EU by 2024; United States by 2026-2027 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smartphone integration widens despite design hurdles

Premium handset vendors continue to refine 3D face-authentication modules, balancing security requirements with bezel-less displays. Camera-under-panel roadmaps sustain demand for compact depth sensors with low-power vertical-cavity surface-emitting lasers (VCSELs). Contract manufacturers in China and South-East Asia are adding structured-light assembly capacity to meet multiyear procurement commitments from leading brands. Component suppliers report tight allocations of single-photon avalanche diode (SPAD) arrays for near-infrared receivers, underscoring a supply-demand imbalance that supports average selling prices. As mid-tier devices begin adopting simplified depth cameras for portrait-mode photography and video-chat background segmentation, the depth sensing market gains resilient unit volumes even when flagship growth plateaus.

Automotive LiDAR deployment hits production scale

The shift from prototype fleets to assembly-line installation marks an inflection point for the depth sensing market. Chinese vendors shipped more than 500,000 automotive LiDAR units in 2024, achieving full-year profitability and securing European design wins. European Union Regulation 2019/2144 mandates advanced driver-distraction warning systems for new vehicle types after July 2024, accelerating in-cabin 3D camera demand.[1]InterRegs, “EU Regulation on Advanced Driver Distraction Warning Systems Published,” interregs.com Tier-1 suppliers now bundle long-range LiDAR, short-range cameras, and edge-AI processors to deliver turn-key ADAS platforms. Sony’s new IMX479 stacked SPAD sensor extends detection to 300 m with 5 cm resolution, aligning with highway-speed automatic-emergency-braking scenarios. [2]Sony Semiconductor Solutions Group, “Sony Semiconductor Solutions to Release Stacked SPAD Depth Sensor for Automotive LiDAR Applications,” sony-semicon.com

AR/VR headsets spur sensor miniaturisation

Global headset shipments returned to double-digit growth in 2025 as enterprise training and mixed-reality collaboration matured. Head-mounted devices require low-latency, sub-millimetre depth accuracy for hand-tracking and spatial-anchor stabilisation. Manufacturers are therefore integrating stacked backside-illuminated SPAD arrays paired with on-chip histogram engines to deliver per-pixel time-of-flight calculations at fast frame rates. Parallel development of indirect-ToF sensors using multi-tap pixels mitigates power consumption while supporting bright indoor lighting conditions. The emphasis on low-power, compact optics filters into the broader depth sensing market, providing cost-effective modules for retail analytics, warehouse robotics, and smart-home devices.

Edge-AI integration lowers cloud dependency

Dedicated neural-processing engines, fabricated on advanced 6 nm and 7 nm nodes, are now packaged alongside depth cameras inside industrial robots and autonomous drones. NASA-verified radiation-resilient accelerators demonstrate the robustness of neuromorphic architectures, allowing high-altitude and spaceborne deployment. In factories, dual-lens configurations achieve 100 µm resolution at 10 cm, enabling inspection of reflective circuit-board traces and transparent substrates. [3]Kyocera Corporation, “Kyocera’s AI-Based High-Res Depth Sensor for Close Imaging,” kyocera.comPre-trained models built with synthetic computer-graphics data slash annotation costs, while on-device inference eliminates latency and privacy risks associated with cloud processing. As a result, depth-processing capacity decouples from network infrastructure, unlocking use cases in remote agriculture, disaster-response robotics, and wearable medical devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High bill-of-materials and integration costs | -1.9% | Global; mass-market segments most affected | Medium term (2-4 years) |

| Sunlight and weather performance limits for ToF sensors | -1.1% | Outdoor systems worldwide; severe in high-irradiance regions | Long term (≥ 4 years) |

| VCSEL eye-safety power ceiling | -0.8% | Global; automotive and outdoor systems | Long term (≥ 4 years) |

| VCSEL and SPAD supply-chain concentration | -0.7% | Primarily APAC manufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High integration costs constrain mass-market adoption

Complex optical-cavity alignment, temperature calibration, and safety-related firmware validation inflate development timelines for depth modules. Automotive-grade designs must pass stringent electromagnetic-compatibility and shock-vibration testing, raising non-recurring engineering expenses. Smartphone tier-2 vendors have delayed 3D-camera rollouts in mid-range handsets owing to cost sensitivities, preferring single-lens portrait-mode algorithms. Outsourced semiconductor assembly and test capacity remains concentrated in fewer than 10 facilities, exposing OEMs to geopolitical trade disruptions and wafer-pricing volatility. Collectively, these factors temper unit growth in price-elastic segments and compel suppliers to prioritise high-margin premium devices.

Environmental limits restrict outdoor deployment

Direct time-of-flight sensors struggle in peak-sunlight conditions because ambient-light photons saturate SPAD arrays, forcing longer integration times that degrade frame rates and accuracy. Automotive LiDAR suppliers incorporate high-peak-power laser diodes, yet eye-safety regulations cap permissible irradiance, creating a trade-off between range and compliance. Particle density, fog, dust, and rain further attenuate signal power and introduce multipath reflections, complicating algorithms. System designers therefore add multi-spectral redundancy—radar, ultrasonic, and thermal cameras—raising costs and integration complexity. Alternative FMCW architectures mitigate sunlight interference but introduce coherent detection challenges and still require sophisticated calibration procedures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: FMCW addresses long-range accuracy demands

Time-of-Flight techniques maintained a 45.4% depth sensing market share in 2024, anchored by their ubiquity in smartphones and tablets. However, Flash LiDAR is projected to grow at an 11.2% CAGR as solid-state beam steering and ASIC integration lower costs. Frequency-modulated continuous-wave designs are gaining traction for vehicles and industrial robots because heterodyne detection delivers centimetre-class accuracy at 300 m while providing Doppler velocity data. Stereo-vision systems benefit from convolutional-neural-network disparity estimation, extending reliable range without active illumination and thus avoiding VCSEL eye-safety limitations.

In the near term, FMCW makers emphasise wafer-level photonic integration to drive price parity with ToF. Aeva’s in-cabin demonstrator shows how compact FMCW modules can be embedded behind standard laminated glass without visible apertures, supporting upcoming Euro NCAP driver-monitoring protocols. Meanwhile, ToF suppliers are reducing photon-to-digital latency to under 10 ns, enhancing performance in fast-moving drone applications. The interplay of innovation and cost reduction keeps technology diversity high, offering system integrators flexibility to optimise for range, resolution, and ambient-light tolerance.

By Component: software captures growing value share

Image sensors and cameras commanded 48.3% of 2024 revenue, underscoring the foundational role of photodetectors in every architecture. Yet software and algorithms are projected to expand at an 11.3% CAGR, capturing value as depth estimation shifts towards learned stereo matching, temporal filtering, and semantic segmentation. Sony’s automotive sensor capable of simultaneously outputting RAW and YUV streams simplifies downstream processing and highlights hardware–software co-design trends.

Greater emphasis on software allows module makers to offer firmware-defined upgrades that improve accuracy post-deployment, extending product lifecycles and enabling subscription models. Turn-key depth modules integrating optics, drivers, firmware, and inference stacks reduce time-to-market for appliance and industrial OEMs. As capability migrates from discrete hardware to algorithms, suppliers with machine-learning expertise capture disproportionate share of incremental value, intensifying competition from AI-first start-ups.

By Application: automotive overtakes consumer-electronics growth

The depth sensing market size for consumer-electronics applications equalled 38.5% of 2024 revenue, reflecting entrenched use in mobile phones and tablets. Automotive advanced-driver-assistance systems, however, are forecast to expand at an 11.6% CAGR on the strength of mandated collision-avoidance and driver-monitoring functions. Luminar reported 45% sequential revenue growth as its Volvo EX90 launch demonstrated OEM willingness to pay for highway-speed LiDAR. In-cabin cameras leveraging structured-light or short-range ToF complement exterior sensors, providing occupant status data needed for airbag logic and hands-off driving certifications.

Beyond vehicles, augmented-reality headsets, warehouse robots, and industrial pick-and-place arms rely on precise depth maps for spatial interaction and navigation, sustaining multi-segment demand. The retail sector adopts shelf-monitoring systems to address labour shortages, while logistics providers deploy 3D vision for parcel dimensioning. Healthcare remains an early-stage vertical, yet hospitals testing non-contact patient monitoring illustrate the long-range potential for medical adoption once regulatory approvals mature.

By Range: long-range demand accelerates

Short-range configurations (<5 m) captured 56.7% of 2024 sales due to their dominance in mobile devices and smart-home cameras. Long-range systems (>30 m) are projected to grow at an 11.5% CAGR thanks to highway-speed ADAS and industrial automation needs. onsemi’s Hyperlux ID sensor offers real-time indirect-ToF operation out to 30 m, bridging the gap between short-range consumer modules and high-power LiDAR.[4]onsemi, “Managing Risk in Automotive Image Sensor Supply Chains,” onsemi.com Mid-range solutions (5-30 m) serve factory-floor safety curtains, automated guided vehicles, and logistics conveyors where distances exceed structured-light capabilities but do not require automotive-grade range.

The distinct range tiers require different optical power budgets, signal-processing pipelines, and thermal-management solutions, driving specialisation among suppliers. Long-range uptake signals maturation toward demanding applications that justify higher average selling prices and longer qualification cycles, supporting revenue diversification.

Geography Analysis

North America retained a 32.4% depth sensing market share in 2024 owing to early ADAS adoption, high smartphone penetration, and robust R&D ecosystems. The United States leads patent filings and venture investment, while Canada hosts specialised lidar-software start-ups. Intel’s July 2025 spin-off of RealSense, capitalised at USD 50 million, illustrates strategic repositioning aimed at agile robotics opportunities. Government safety mandates from the National Highway Traffic Safety Administration underpin steady demand, and semiconductor fabs in Arizona, Texas, and Oregon support regional supply-chain resilience.

Asia–Pacific is projected to post the fastest 2025-2030 growth at an 11.7% CAGR as Chinese, Japanese, Korean, and Taiwanese firms scale production. Hesai shipped 501,889 automotive LiDAR units in 2024, achieving first-year profitability and confirming the region’s cost-leadership advantage. Sony’s stacked SPAD roadmap and Samsung’s imaging-sensor initiatives sustain high-performance component supply, while Taiwan’s LIPS moves 3D vision from pilot to mass production after 12 years of R&D. Government incentives and large domestic electronics markets allow suppliers to amortise tooling rapidly and undercut overseas competitors.

Europe advances at a steady pace supported by stringent safety rules. EU Regulation 2019/2144 obliges new vehicle platforms to include advanced distraction-warning features, raising immediate in-cabin 3D camera requirements. Germany and Sweden host flagship automotive LiDAR deployments, with premium brands integrating long-range sensors as standard on top trims. The region also benefits from industrial automation programmes funded under national recovery plans, driving depth-camera adoption in smart factories and logistics hubs.

Competitive Landscape

The depth sensing industry features moderate fragmentation with a tilt toward consolidation in high-volume automotive segments. Top Chinese LiDAR suppliers and the five largest Japanese, European, and US component makers together hold roughly 55% of revenue, leaving ample space for new entrants. Price competition intensifies as manufacturing yields improve; however, performance differentiation persists in range, resolution, and functional-safety compliance. Sony, STMicroelectronics, and ams OSRAM retain strong image-sensor and VCSEL positions, while Hesai, Ouster, and Luminar push automotive LiDAR cost curves downward.

Strategically, firms pursue vertical integration and ecosystem control. Sony bundles photodetectors with ISP firmware, and Luminar pairs sensors with mapping-software stacks to capture per-vehicle service revenue. Intel’s RealSense carve-out exemplifies asset repositioning to address robotics, industrial inspection, and warehouse-automation niches without competing head-on with low-cost smartphone modules. Patent filings indicate ongoing innovation: stacked SPAD readouts, thermal-stabilised VCSEL arrays, and heterodyne FMCW chiplets highlight the technological race.

Partnerships between component makers and cloud-service providers emerge as an avenue to monetise data streams, while system integrators focus on pre-validated perception bundles to shorten OEM design cycles. Competitive intensity is expected to remain high as automotive volume ramps and mixed-reality devices transition from early adopters to mass markets.

Depth Sensing Industry Leaders

Sony Semiconductor Solutions

STMicroelectronics

ams OSRAM

Intel Corporation

Infineon Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Intel completed the spin-out of RealSense as a standalone company, securing USD 50 million in funding to advance AI vision in robotics applications.

- June 2025: Sony Semiconductor Solutions announced the IMX479 stacked SPAD depth sensor for automotive LiDAR, enabling 300 m detection with 5 cm resolution.

- June 2025: Taiwan’s LIPS readied mass production of 3D vision systems after extensive R&D, targeting multi-industry deployment.

- April 2025: Seeing Machines introduced a 3D camera co-developed with Airy3D for in-cabin monitoring, combining 5 MP RGB with depth data.

Global Depth Sensing Market Report Scope

| Time-of-Flight (ToF) |

| Structured Light |

| Stereo Vision |

| LiDAR (Flash, MEMS, OPA) |

| Ultrasound and Others |

| Image Sensor / Camera |

| VCSEL / IR Illuminator |

| SoC / Processor and AI Accelerator |

| Software and Algorithms |

| Complete Depth Module |

| Smartphones and Tablets |

| Automotive (Exterior LiDAR, In-cabin DMS) |

| AR/VR and Wearables |

| Robotics and Drones |

| Industrial Automation and Logistics |

| Security and Surveillance |

| Healthcare and Medical Imaging |

| Retail and Gesture Recognition |

| Short Range (< 5 m) |

| Mid Range (5 - 30 m) |

| Long Range (> 30 m) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Technology | Time-of-Flight (ToF) | ||

| Structured Light | |||

| Stereo Vision | |||

| LiDAR (Flash, MEMS, OPA) | |||

| Ultrasound and Others | |||

| By Component | Image Sensor / Camera | ||

| VCSEL / IR Illuminator | |||

| SoC / Processor and AI Accelerator | |||

| Software and Algorithms | |||

| Complete Depth Module | |||

| By Application | Smartphones and Tablets | ||

| Automotive (Exterior LiDAR, In-cabin DMS) | |||

| AR/VR and Wearables | |||

| Robotics and Drones | |||

| Industrial Automation and Logistics | |||

| Security and Surveillance | |||

| Healthcare and Medical Imaging | |||

| Retail and Gesture Recognition | |||

| By Range | Short Range (< 5 m) | ||

| Mid Range (5 - 30 m) | |||

| Long Range (> 30 m) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the depth sensing market?

The depth sensing market size reached USD 9.09 billion in 2025 and is projected to grow to USD 15.18 billion by 2030.

Which segment shows the fastest growth?

Automotive ADAS and autonomous-vehicle applications are forecast to expand at an 11.6% CAGR between 2025 and 2030 as regulatory mandates drive sensor adoption.

Which region will grow the quickest?

Asia–Pacific is expected to post the highest regional CAGR at 11.7% through 2030, propelled by large-scale manufacturing and strong domestic demand.

How important is software in depth sensing solutions?

Software and algorithms are the fastest-growing component category, forecast to rise at an 11.3% CAGR as value shifts from hardware capture to data-processing intelligence.

What technologies are competing in automotive LiDAR?

Time-of-Flight dominates current volumes, but FMCW LiDAR is gaining traction for long-range accuracy, Doppler velocity data, and sunlight immunity.

What are the biggest barriers to mass adoption?

High bill-of-materials costs, environmental performance limits under strong sunlight, and supply-chain concentration in VCSEL and SPAD production remain key hurdles.

Page last updated on: