Senolytics And Anti-Aging Pharmaceuticals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

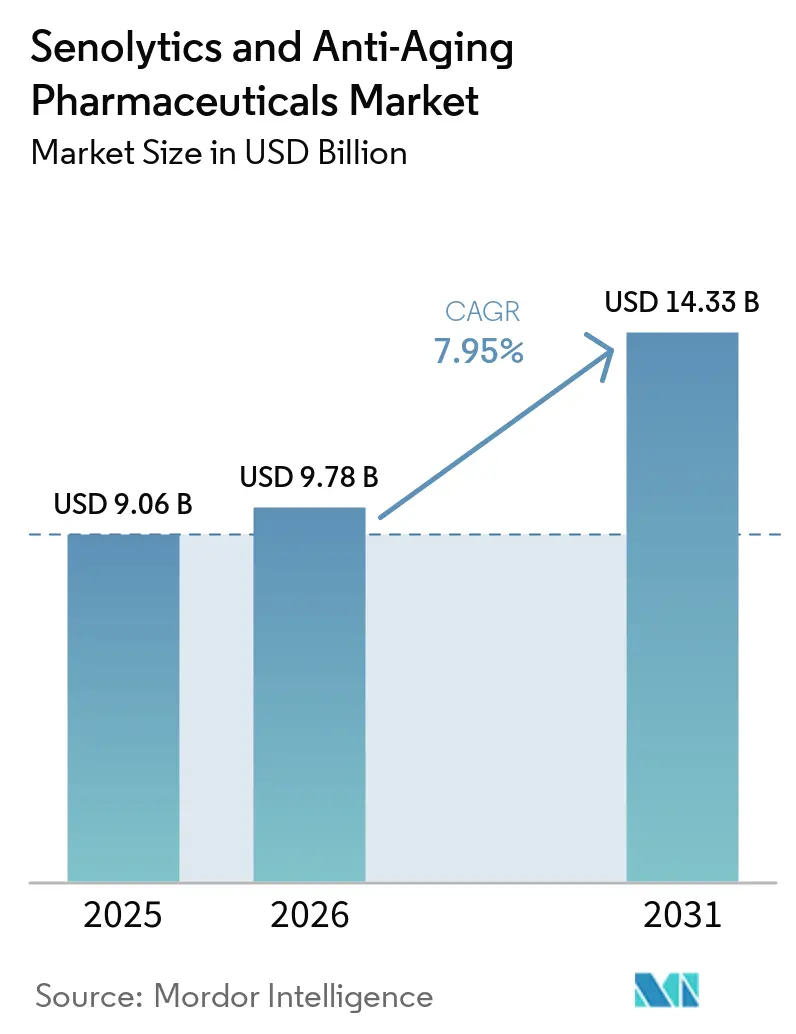

| Market Size (2026) | USD 9.78 Billion |

| Market Size (2031) | USD 14.33 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Senolytics And Anti-Aging Pharmaceuticals Market Analysis by Mordor Intelligence

The Senolytics And Anti-Aging Pharmaceuticals Market size is expected to grow from USD 9.06 billion in 2025 to USD 9.78 billion in 2026 and is forecast to reach USD 14.33 billion by 2031 at 7.95% CAGR over 2026-2031.

Therapies in the senolytics and anti-aging pharmaceuticals market are shifting focus. Instead of merely addressing diseases that manifest later in life, the emphasis is now on targeting the biology of aging. Cellular senescence has emerged as a pivotal therapeutic target as senescent cells evade normal clearance and emit inflammatory signals linked to ophthalmology, pulmonary fibrosis, frailty, and neurodegeneration. The commercial potential remains strong, driven by the rising burden of chronic diseases as populations live longer. Non-communicable diseases account for 50% of premature deaths in individuals under 70, highlighting the growing need for innovative solutions in this market.[1]World Health Organization, “World Health Statistics 2025, Monitoring Health for the SDGs,” World Health Organization, who.int

Key Report Takeaways

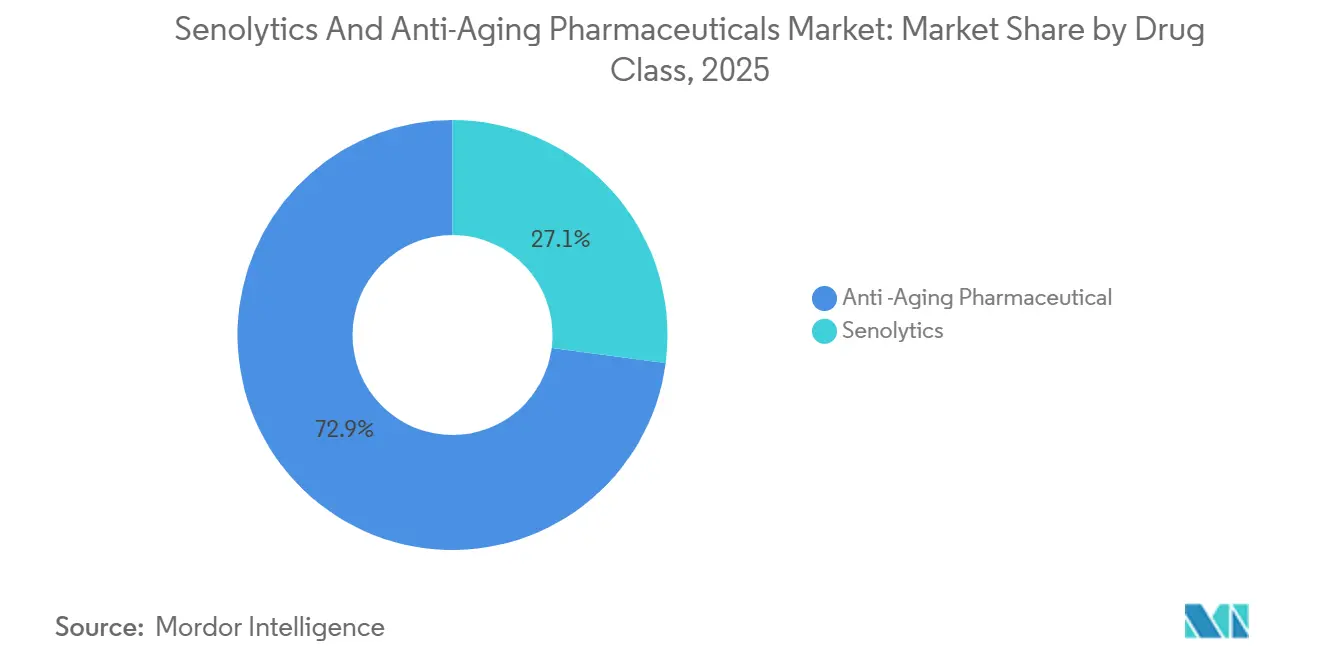

- By drug class, anti-aging pharmaceuticals held 72.95% of the senolytics and anti-aging pharmaceuticals market share in 2025, while senolytics is projected to expand at an 8.15% CAGR through 2031.

- By application, clinical use / off-label therapeutics accounted for 60.95% of the senolytics and anti-aging pharmaceuticals market size in 2025, while consumer wellness/longevity Use is expected to grow at an 8.35% CAGR through 2031.

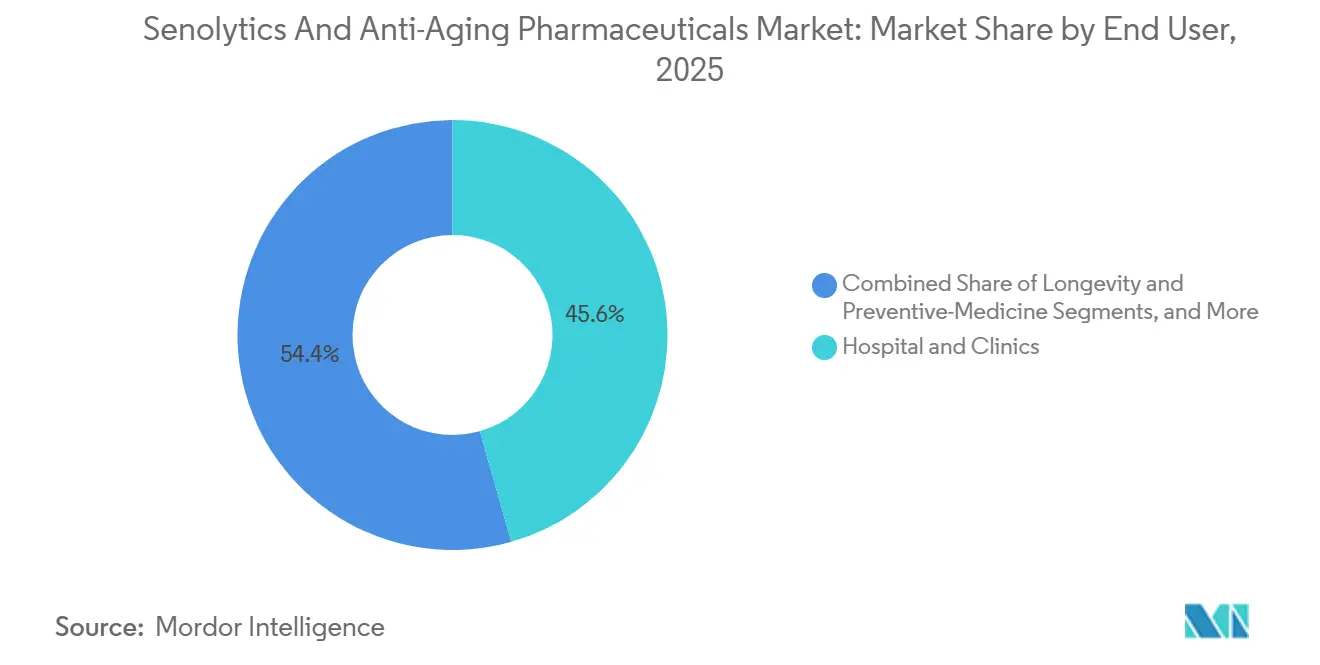

- By end user, hospitals and clinics captured 45.60% revenue share in 2025, while Longevity and preventive-medicine clinics are projected to record a 9.60% CAGR through 2031.

- By distribution, prescription-based channels represented 65.70% revenue share in 2025, while over-the-counter / supplements are expected to advance at a 10.40% CAGR through 2031.

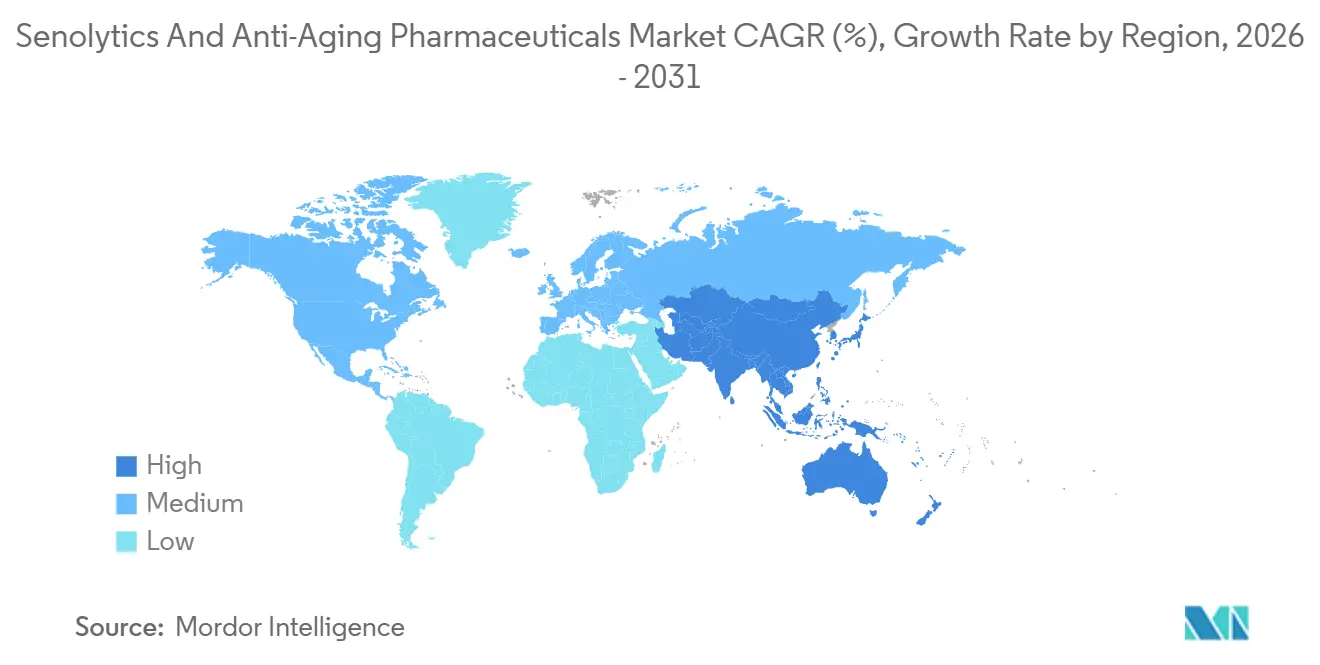

- By geography, North America led with 41.12% revenue share in 2025, while Asia-Pacific is projected to expand at an 11.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Senolytics And Anti-Aging Pharmaceuticals Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of age-related chronic diseases | +2.2% | Global, with highest intensity in APAC and North America | Long term (≥ 4 years) |

| Expanding geroscience R&D funding and private capital | +1.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Clinical proof-of-concept in ophthalmology, fibrosis, frailty, and kidney disease | +1.3% | North America, EU, Australia | Medium term (2-4 years) |

| Platform diversification beyond small molecules into gene, immune, and rejuvenation therapies | +0.9% | North America, with early gains in UK and South Korea | Long term (≥ 4 years) |

| Senescence atlas and biomarker infrastructure improving trial stratification | +0.7% | Global | Medium term (2-4 years) |

| Ophthalmology and dermatology as lower-risk first commercialization wedge | +0.5% | North America, EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Age-Related Chronic Diseases

The senolytics and anti-aging pharmaceuticals market continues to derive strong demand from the prevalence of chronic diseases in aging populations. In 2021, the global population aged 70 and older reached 494.4 million, with ischemic heart disease, stroke, and COPD as leading causes of death, all linked to senescence-related mechanisms. A 2025 study projected 75.5 million global deaths from non-communicable diseases by 2050, with cardiovascular disease as the largest contributor.[2]National Library of Medicine, “Global Burden and Future Projections of Non-Communicable Diseases 2000–2050,” PubMed, pubmed.ncbi.nlm.nih.gov As life expectancy increases without a proportional rise in healthy years, healthcare priorities are shifting toward therapies that reduce morbidity rather than merely extending survival. This positions the market at the intersection of medical need, payer interest, and preventive health demand.

Expanding Geroscience R&D Funding and Private Capital

Increased funding for geroscience programs is driving the senolytics and anti-aging pharmaceuticals market. Longevity investments rose to USD 8.49 billion across 325 deals in 2024, up from USD 3.82 billion in 2023, with 31% of the capital allocated to later-stage ventures. Investors are favoring milestone-driven platforms over open-ended research. Acquisition activity is also rising, as companies with promising clinical signals in regulated indications attract larger pharmaceutical players seeking faster market entry. Early proof-of-concept results are becoming critical for securing capital and advancing toward regulatory approval.

Clinical Proof-of-Concept in Ophthalmology, Fibrosis, Frailty, and Kidney Disease

Early clinical proof-of-concept results are strengthening the credibility of the senolytics and anti-aging pharmaceuticals market. UNITY Biotechnology’s Phase 2 BEHOLD study demonstrated sustained vision improvement in diabetic macular edema patients, establishing ophthalmology as a viable clinical setting. In frailty, a Phase 2 trial is evaluating dasatinib and quercetin in adults aged 50 and above, with completion expected in November 2026. Kidney disease research has also highlighted the role of cellular senescence in fibrosis, supporting the therapeutic potential of senolytics. These developments expand the evidence base, enabling multi-indication development strategies.

Platform Diversification Beyond Small Molecules

The senolytics and anti-aging pharmaceuticals market is diversifying beyond first-generation small molecules. Anti-aging medicine now includes epigenetic reprogramming, stem cell-based approaches, and mitochondrial augmentation, reflecting a shift toward precision reprogramming and selective intervention strategies. This diversification introduces varied reimbursement models, risk profiles, and market entry pathways, allowing the market to grow through multiple product architectures without a uniform clinical or pricing framework.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| No approved aging indication and unclear regulatory pathway for aging claims | -1.5% | Global, most acute in North America and EU | Long term (≥ 4 years) |

| Off-target toxicity and narrow therapeutic windows for systemic senolytics | -0.9% | Global | Medium term (2-4 years) |

| Beneficial senescence biology limits indiscriminate cell clearance | -0.6% | Global | Long term (≥ 4 years) |

| Biomarker heterogeneity complicates enrichment, dosing cadence, and duration | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unclear Regulatory Pathway for Aging Indications

The market for senolytics and anti-aging drugs faces significant regulatory challenges. Aging is not officially recognized as a disease, making it difficult for sponsors to demonstrate the efficacy of anti-aging treatments. Research must focus on specific age-related conditions like fibrosis, retinal diseases, frailty, or neurodegeneration, which fragments development, extends timelines, and limits data pooling. Additionally, payers may question the value of senescence clearance compared to established off-label drugs. For companies in this market, regulatory strategies are as critical as biological advancements, particularly when converting broad healthspan claims into disease-specific endpoints.

Off-Target Toxicity and Narrow Therapeutic Windows

The senolytics and anti-aging pharmaceuticals market is constrained by the broad effects of systemic senolytic activity, which can impact healthy cells sharing similar survival pathways. This limits the therapeutic window, as essential cells involved in tissue repair, immune balance, and wound healing may be affected. A study highlighted the variability of senolytic compounds on epigenetic age in vitro, stressing the importance of compound selection and dosing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Established Formulations Anchor Revenue, Senolytics Build the Next Growth Layer

In 2025, Anti-Aging Pharmaceuticals accounted for 72.95% of revenue, maintaining its lead in the senolytics and anti-aging pharmaceuticals market. This reflects the commercial maturity of NAD+ precursors, rapamycin-related therapies, and hormone-modulating products, which are accessible through prescription and over-the-counter channels. These products generate revenue as they are available without waiting for first-in-class senolytic approvals.

Senolytics are projected to grow at an 8.15% CAGR through 2031, outpacing the overall market growth. The pipeline includes small molecules, gene-based constructs, immune-directed strategies, and precision reprogramming concepts, highlighting growth driven by modality diversity. As results emerge in areas like ocular health, fibrosis, frailty, and inflammation, the gap between current revenue leaders and future pipeline potential is expected to narrow.

By Application: Clinical Use Leads, Consumer Wellness Scales Faster

In 2025, Clinical Use and Off-label Therapeutics held 60.95% of the market, making it the largest application segment. This is driven by the use of established agents like dasatinib, rapamycin, and metformin in defined medical settings. Academic medical centers and specialist clinics play a key role by combining trial enrollment, compassionate use, and protocol-based prescribing.

Consumer Wellness and Longevity Use is expected to grow at an 8.35% CAGR through 2031, making it the fastest-growing application. Growth is supported by wider biomarker access, direct-to-consumer diagnostics, and a shift from niche biohacking to mainstream healthspan management. Longevity programs increasingly use tools like biological age clocks and inflammatory panels to track responses, enhancing credibility.

By End User: Hospitals Stay Central, Longevity Clinics Expand Their Role

In 2025, Hospitals and Clinics accounted for 45.60% of revenue, leading the senolytics and anti-aging pharmaceuticals market. This reflects the concentration of senolytic activities in academic medical centers, hospital-based specialists, and research-linked care environments, which have the infrastructure and expertise for programs in frailty, ophthalmology, oncology, and fibrosis.

Longevity and Preventive-Medicine Clinics are projected to grow at a 9.60% CAGR through 2031, making them the fastest-growing end-user channel. Their growth is driven by demand for physician-supervised healthspan programs that bridge hospital care and self-directed wellness. These clinics are expanding access to biomarker-guided protocols and translating preclinical geroscience into consumer-friendly care models.

By Distribution: Prescription Channels Lead, OTC Formats Broaden Access

In 2025, Prescription-Based distribution captured 65.70% of revenue, dominating the senolytics and anti-aging pharmaceuticals market. This reflects reliance on physician-supervised treatments, off-label prescribing, and formal investigational pathways. Regulatory frameworks reinforce this structure by requiring defined medical rationales for therapy use.

Over-the-Counter and Supplements are forecast to grow at a 10.40% CAGR through 2031, making it the fastest-growing distribution channel. This growth reflects increasing consumer acceptance as science-backed longevity products enter mainstream retail. In April 2026, Nihon Iyakuhin Seiyaku launched SenoRich in Japan, the country’s first senolytic supplement featuring the proprietary SENOX25 compound, with patent applications in 159 countries. This highlights the narrowing gap between prescription-based senotherapeutics and consumer supplements.

Geography Analysis

In 2025, North America accounted for 41.12% of the revenue share in the senolytics and anti-aging pharmaceuticals market, making it the largest regional contributor. This leadership is driven by advanced clinical infrastructure, concentrated venture capital, and a growing network of physician-led longevity and preventive medicine clinics. The United States remains the key player due to its high concentration of clinical-stage longevity biotech firms that influence valuations, trial activities, and partnerships across the market.

Europe remains a significant region in the senolytics and anti-aging pharmaceuticals market, combining a strict regulatory framework with active scientific involvement in senescence research. Countries like Germany, the U.K., France, Italy, and Spain support both consumer adoption of anti-aging solutions and clinical-stage therapeutic advancements. The U.K. contributes through companies such as Genflow Biosciences and Juvenescence, while EU nations back early-phase programs in dermatology and fibrosis-related areas.

Asia-Pacific is the fastest-growing region in the senolytics and anti-aging pharmaceuticals market, with a projected CAGR of 11.37% through 2031. China and Japan drive this growth due to rising demand for aging-related solutions and increasing commercial interest in anti-aging products. Japan's April 2026 launch of SenoRich highlights the region's progress, showcasing both clinical potential and visible retail activity.

Competitive Landscape

In the fragmented senolytics and anti-aging pharmaceuticals market, no single company dominates either established anti-aging products or emerging senolytic therapeutics. Established firms generate near-term revenues from their formulations, while younger biotechs focus on translating senescence biology into unique clinical assets. This dynamic creates a two-speed market: one segment capitalizes on current demand, while the other cultivates future value through targeted indications, biomarker strategies, and innovative modalities.

Strategic moves highlight companies' efforts to secure early leadership in the market. In March 2026, Rubedo Life Sciences reported positive preliminary Phase 1 results for RLS-1496, targeting dermatological issues. Psoriasis patients showed a 20% average reduction in epidermal thickness, along with decreased senescent cell markers and inflammatory cytokines. Similarly, in May 2026, HAYA Therapeutics dosed the first cohort in Phase 1 for HTX-001, aimed at cardiac fibrosis, marking progress in precision cellular reprogramming for aging-related conditions. These developments reflect competition in indication selection, platform breadth, and rapid human data generation.

A clear divide is emerging between programs demonstrating measurable human biological effects and those still concept-driven. Biomarker research has become a critical competitive tool, enhancing patient stratification, improving response visibility, and streamlining clinical designs. Companies focusing on ocular and dermatological indications may maintain an edge, as these areas reduce systemic exposure risks while delivering meaningful translational evidence.

Senolytics And Anti-Aging Pharmaceuticals Industry Leaders

UNITY Biotechnology, Inc.

Oisín Biotechnologies

Cambrian BioPharma, Inc.

Retro Biosciences, Inc.

Cleara Biotech B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Retro Biosciences, valued at USD 1.8 billion, advanced its Phase 1 trial of RTR242 targeting lysosomal dysfunction in Alzheimer's patients. Interim data is expected in August 2026, with no dose-limiting toxicities reported.

- May 2026: HAYA Therapeutics began dosing the first cohort in its Phase 1 trial of HTX-001, an antisense oligonucleotide targeting WISPER lncRNA for cardiac fibrosis.

- April 2026: Nihon Iyakuhin Seiyaku launched SenoRich, Japan's first senolytic supplement with the proprietary SENOX25 compound. Patent applications were filed in 159 countries.

- February 2026: BioAge Labs raised USD 132.3 million through a follow-on public offering. Phase 1 data for BGE-102 showed an 86% median reduction in hsCRP by Day 14, with 93% of participants achieving levels below 2 mg/L.

Global Senolytics And Anti-Aging Pharmaceuticals Market Report Scope

As per the scope of the report, senolytics are a targeted class of anti-aging pharmaceuticals that selectively destroy "senescent" (zombie) cells. These are old, damaged cells that stop dividing but refuse to die, lingering in tissues and secreting toxins that trigger chronic inflammation and accelerate aging-related diseases.

The senolytics and anti-aging pharmaceuticals market is segmented by drug class, application, end-user, distribution channel, and geography. By drug class, the market includes senolytics and anti-aging pharmaceuticals. By application, the market is segmented into clinical use/off-label therapeutics and consumer wellness/longevity use. By end-user, the market is categorized into hospitals and clinics, biopharmaceutical companies and virtual biotechs, longevity and preventive-medicine clinics, and others. By distribution channel, the market is segmented into prescription-based, over-the-counter (OTC)/supplements, and clinical trials/compassionate use. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Senolytics |

| Anti -Aging Pharmaceutical |

| Clinical Use / Off-label Therapeutics |

| Consumer Wellness / Longevity Use |

| Hospital and Clinics |

| Biopharmaceutical Companies and Virtual Biotechs |

| Longevity and Preventive-Medicine Clinics |

| Others |

| Prescription-Based |

| Over-the-Counter (OTC) / Supplements |

| Clinical Trials / Compassionate Use |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Senolytics | |

| Anti -Aging Pharmaceutical | ||

| By Application | Clinical Use / Off-label Therapeutics | |

| Consumer Wellness / Longevity Use | ||

| By End User | Hospital and Clinics | |

| Biopharmaceutical Companies and Virtual Biotechs | ||

| Longevity and Preventive-Medicine Clinics | ||

| Others | ||

| By Distribution | Prescription-Based | |

| Over-the-Counter (OTC) / Supplements | ||

| Clinical Trials / Compassionate Use | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the senolytics and anti-aging pharmaceuticals market?

The senolytics and anti-aging pharmaceuticals market is valued at USD 9.06 billion in 2026 and is projected to reach USD 14.33 billion by 2031 at a 7.95% CAGR.

Which drug class currently leads revenue generation?

Anti-Aging Pharmaceuticals leads with 72.95% revenue share in 2025, supported by established formulations such as NAD+ precursors, rapamycin-related products, and hormone modulators.

Which application area is expanding the fastest through 2031?

Consumer Wellness / Longevity Use is the fastest-growing application segment, with an 8.35% CAGR over 2026-2031.

Which region is leading today and which one is growing the fastest?

North America leads with 41.12% revenue share in 2025, while Asia-Pacific is the fastest-growing region with an 11.37% CAGR through 2031.

Why are biomarkers important for senolytic development?

Biomarkers such as p16, p21, and SASP cytokine panels can improve patient selection, sharpen pharmacodynamic measurement, and help sponsors run more efficient clinical trials.

What is the biggest challenge facing commercialization?

The biggest challenge is regulatory, because aging is not recognized as a formal disease indication, so companies must pursue disease-specific endpoints instead of broad healthspan claims.

Page last updated on: