Skincare Serums Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

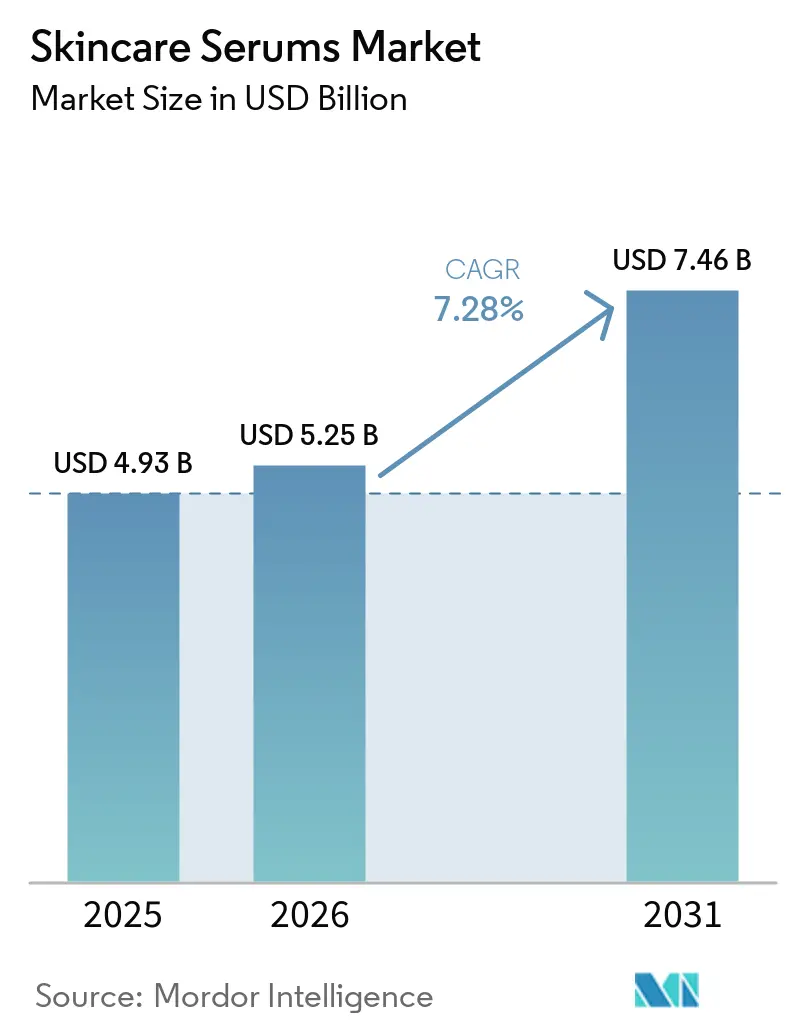

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

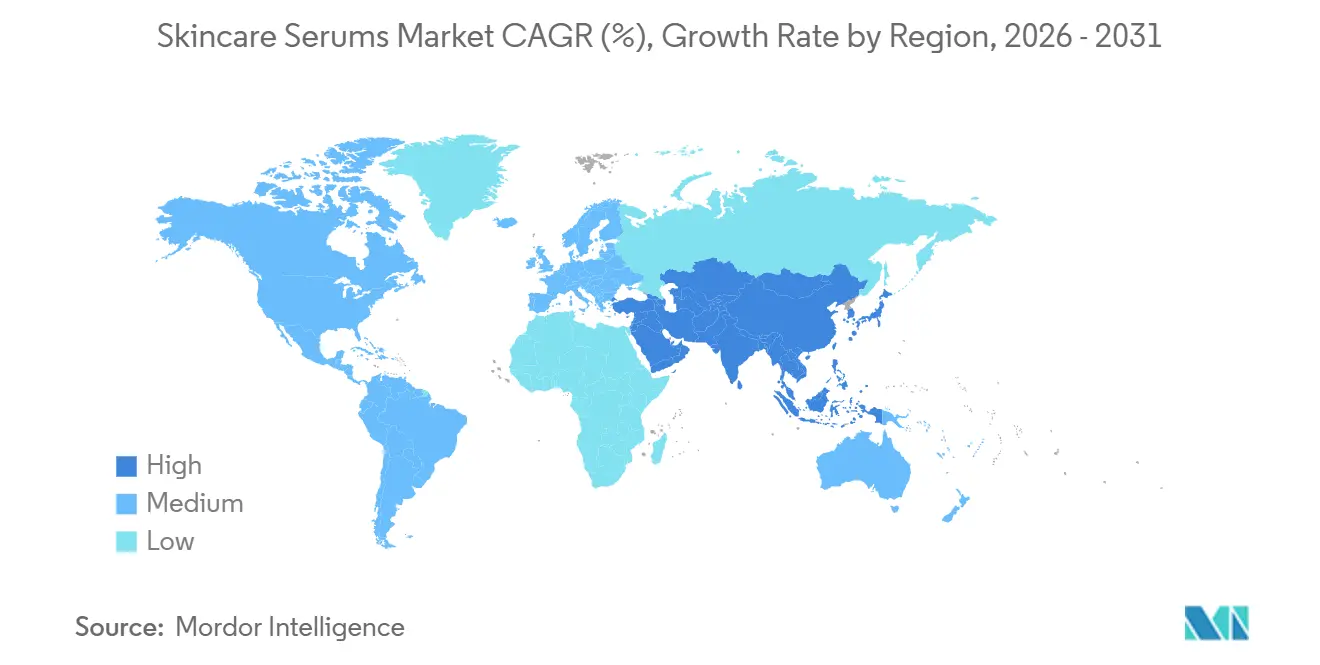

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skincare Serums Market Analysis by Mordor Intelligence

The Skincare Serums Market size is expected to increase from USD 4.93 billion in 2025 to USD 5.25 billion in 2026 and reach USD 7.46 billion by 2031, growing at a CAGR of 7.28% over 2026-2031.

Demand is shifting toward concentrated actives that promise visible clinical outcomes, while single-step hybrid formulations gain ground as consumers trim multi-product routines. North America still contributes the largest value pool, yet Asia-Pacific is outpacing every other region on the back of rising disposable incomes, pollution concerns, and the rapid ascent of Chinese and Korean brands. Competitive intensity is elevated: multinationals are acquiring clinical indie labels, direct-to-consumer (DTC) start-ups iterate formulations in six-month cycles, and patent filings in encapsulation and peptide science continue to rise. Regulatory tightening in the United States, European Union, and China favors companies able to generate robust efficacy dossiers, nudging the skincare serums market toward science-led positioning and dermatologist endorsement.

Key Report Takeaways

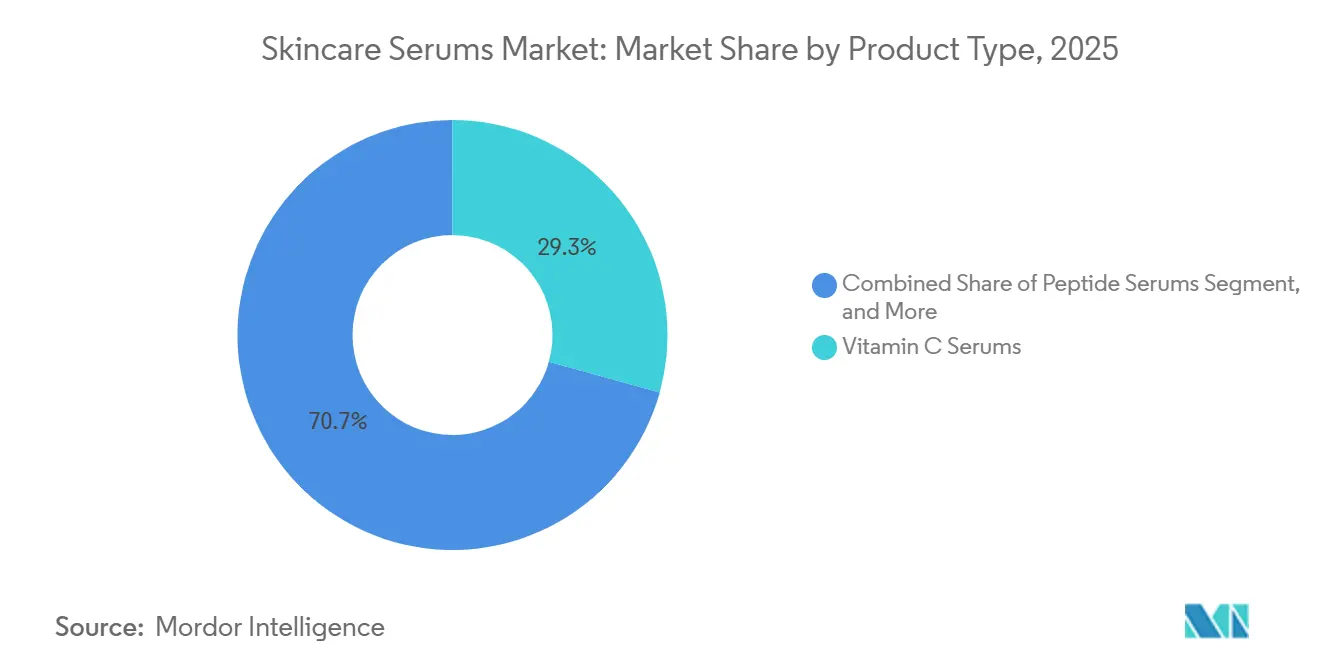

- By product type, vitamin C serums held 29.31% skincare serums market share in 2025, while peptide serums are projected to grow at an 8.12% CAGR through 2031.

- By skin concern, anti-aging dominated with 41.58% revenue share in 2025; repair & barrier support is advancing at a 10.01% CAGR through 2031.

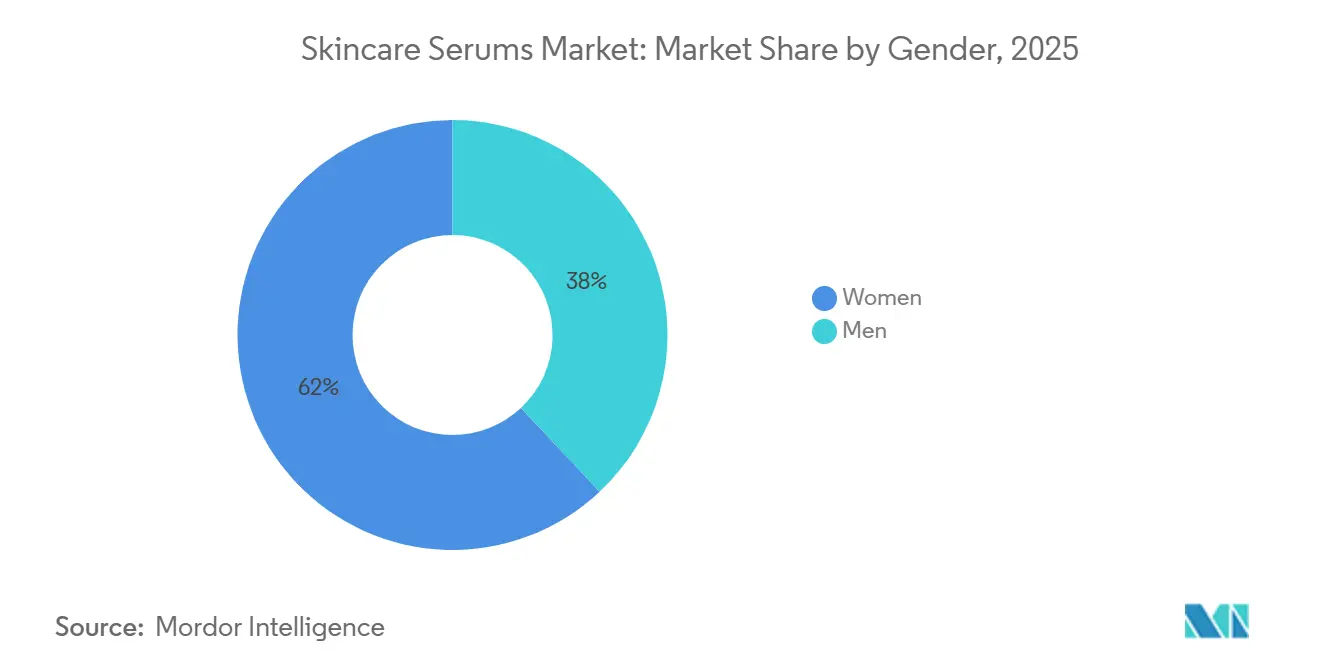

- By gender, women accounted for 62.02% of the skincare serums market size in 2025, whereas the men’s segment is forecast to expand at 11.84% CAGR between 2026 and 2031.

- By distribution channel, offline retail captured 56.13% of 2025 revenue, yet online retail is growing at 12.81% CAGR through 2031.

- By geography, North America captured 37.83% share in 2025; Asia-Pacific registers the fastest regional CAGR at 14.67% through 2031 in the skincare serums market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Skincare Serums Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Anti-aging demand surge among 30-45 cohort | +1.8% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rising skin-health awareness | +1.5% | Asia-Pacific, North America | Long term (≥4 years) |

| Rising disposable incomes in developing Asia | +1.2% | India, Southeast Asia, Middle East & Africa | Long term (≥4 years) |

| E-commerce & DTC lowering entry barriers | +1.4% | Global, early gains in the United States, Western Europe, urban China | Short term (≤2 years) |

| Pollution-related skin issues | +1.0% | China, India, Southeast Asia | Medium term (2-4 years) |

| Micro-dose actives for sensitive skin | +0.9% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Anti-Aging Demand Surge Among 30-45 Demographic

Clinical studies confirm that chronic PM2.5 exposure accelerates extrinsic aging by activating the aryl hydrocarbon receptor, upregulating matrix metalloproteinases, and degrading dermal collagen.[1]National Institutes of Health, “Pollution and Skin Aging: Oxidative Stress and Aryl Hydrocarbon Receptor Activation,” nih.gov Consumers aged 30-45, therefore, prioritize serums integrating palmitoyl pentapeptide-4, copper tripeptide-1, and niacinamide, seeking proactive collagen synthesis instead of reactive antioxidant defense. Brands answer with hybrid SKUs that blend retinoids, peptides, and barrier-supportive actives, compressing multi-step routines into a single bottle. Third-party dermatology seals and published clinical trials now influence purchase decisions as much as influencer marketing. North America and Western Europe lead this science-centric narrative, assisted by strict claim-substantiation rules from the FDA and European Commission.[2]European Commission, “Regulation (EU) 2024/996 on Cosmetic Products,” ec.europa.eu

Rising Skin-Health Awareness

Discussions once limited to wrinkles now cover barrier integrity, ceramide replenishment, and microbiome balance. Pollution-induced oxidative stress erodes tight-junction proteins and ceramide levels, undermining water retention, yet serums fortified with ceramide precursors, niacinamide, and multi-weight hyaluronic acid are reversing this decline. K-beauty’s “skin-first” approach, underscored by South Korea’s USD 11.4 billion cosmetics exports in 2025, spreads this barrier-centric mindset worldwide. China’s USD 3.5 billion online beauty-consultation sector reinforces the trend with AI diagnostics that recommend serums based on transepidermal water loss and sebum metrics. Gen Z and millennials gravitate toward such data-backed personalization, intensifying demand for measurable skin-health outcomes.

E-Commerce & DTC Brands Lowering Entry Barriers

Global beauty e-commerce rose from 26% of sales in 2024 to a projected 31% by 2030, yet only 17% of U.S. adults currently buy directly from brands, while South Korean ODM partners cut minimum order quantities to 1,000 units and shrink concept-to-launch cycles below six months. Multinationals respond via acquisitions such as L’Oréal’s EUR 1 billion purchase of Medik8 in 2025. Although counterfeit trade, worth EUR 3 billion in lost EU sales between 2016 and 2019, remains a drag on consumer trust, investments in blockchain tracing and tamper-evident packaging are beginning to mitigate the threat.

Increasing Concerns Over Pollution-Induced Skin Issues

Urban Asian centers record PM2.5 levels multiple times higher than WHO targets, prompting consumers to seek serums containing film-forming polymers like pullulan and biosaccharide gum-1 that physically repel pollutants. Brands also incorporate niacinamide, resveratrol, and green-tea extracts to inhibit AhR signaling and oxidative cascades. Clinical data show vitamin C–ferulic acid combinations limiting pollutant-triggered lipid peroxidation in keratinocytes. China’s skincare retail climbs at 8.7% CAGR to RMB 701.1 billion by 2028, with “anti-pollution” a core marketing claim. Laboratories increasingly validate products through AhR-luciferase assays, reinforcing credibility among science-literate buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit & grey-market products | –0.8% | EU, North America, premium Asia-Pacific | Short term (≤2 years) |

| Regulatory crackdown on exaggerated claims | –0.6% | United States, EU, ASEAN, China | Medium term (2-4 years) |

| Supply tightness for pharma-grade niacinamide | –0.4% | Global, supply chains concentrated in China and India | Short term (≤2 years) |

| “Skin-minimalism” compressing SKU counts | –0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit & Grey-Market Products Eroding Trust

EU authorities estimate EUR 3 billion in lost cosmetics revenue and 31,717 job losses from counterfeit trade between 2016-2019. Premium serums suffer disproportionate harm because high-purity niacinamide or L-ascorbic acid is swapped for cheaper analogs that provoke irritation, denting repeat sales. Third-party sellers on global marketplaces exploit patchy brand-verification processes, while cross-border fulfillment complicates jurisdictional enforcement. Blockchain batch tracing, serialized QR codes, and customs partnerships are gaining ground, but counterfeiters now mimic holograms and serial numbers, keeping the cat-and-mouse game alive.

Regulatory Crackdown on Exaggerated Efficacy Claims

The FDA’s Modernization of Cosmetics Regulation Act tightens facility registration and adverse-event reporting, reinforcing scrutiny of “drug-like” language. Europe’s Regulation (EU) 2024/996 caps retinol and bans certain skin-lighteners, forcing reformulations or SKU withdrawals. China’s NMPA imposes laboratory trials for anti-aging and whitening claims, stretching launch lead-times by up to one year. India, meanwhile, adds a 90-day registration window, complicating supply planning. Together, these frameworks elevate compliance expenses and extend R&D cycles, slowing innovation tempo.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Peptides Leapfrog Legacy Antioxidants

Peptide serums will outpace the overall skincare serums market at 8.12% CAGR through 2031, whereas vitamin C formulations, in spite of their 29.31% revenue, will confront maturity in North America and Europe. Clinical demonstrations that palmitoyl pentapeptide-4 and hexapeptide-8 stimulate fibroblast activity are swaying formulators toward collagen-synthesis approaches. In contrast, free L-ascorbic acid remains unstable above pH 3.5, nudging brands toward costlier derivatives, which dilutes potency and slows velocity. Retinol/retinoid serums face additional headwinds from the EU’s 0.3% cap, encouraging the rapid spread of microencapsulated delivery systems that comply without efficacy loss. Hybrid, multi-active SKUs retinol plus niacinamide plus peptides satisfy the 81% of U.K. women who now prefer fewer routine steps.

Hyaluronic-acid-based serums retain a hydration niche by layering 10 kDa fractions for dermal penetration atop 2,000 kDa polymers that form a surface film. Niacinamide serums have gone mainstream thanks to wide-ranging benefits from ceramide upregulation to melanin-transfer inhibition, backed by robust safety data. ODM labs in Seoul and Incheon now prototype peptide or niacinamide hybrids for indie labels within six months, further compressing time-to-market.

By Skin Concern: Barrier Repair Accelerates Past Classic Anti-Aging

Repair & barrier support will record a 10.01% CAGR through 2031, eclipsing the legacy anti-aging focus, even though the latter still contributes the single largest revenue share of 41.58% in 2025. Exhaustive studies show pollution-triggered depletion of ceramides and tight-junction proteins, intensifying demand for formulations combining ceramide NP, cholesterol, and free-fatty acids in physiological ratios. Anti-aging lines persist, yet they increasingly embed barrier-repair code in their marketing scripts, reflecting the emerging consensus that structurally sound skin ages more slowly.

Hydration-led serums leverage multi-weight hyaluronic acid to lock in surface moisture and hydrate the dermis, whereas acne/blemish solutions deploy encapsulated salicylic acid and niacinamide to reduce inflammation without peeling. Brightening options contend with ingredient bans: Europe’s constraints on arbutin and kojic acid channel R&D into tranexamic acid or low-dose alpha-arbutin. Sensitivity-focused SKUs concentrate on AhR inhibition and TRPV1 damping via Centella asiatica or green-tea ferment, capitalizing on the rise of stressed-skin phenotypes in urban environments.

By Gender: Targeted Men’s Launches Drive Double-Digit Growth

Still just 38% of 2025 demand, men’s serums are slated to expand at 11.84% CAGR, three-quarters faster than the total skincare serums market. Formulations that merge oil control, post-shave soothing, and pore-size reduction into a single application resonate with male consumers who prefer three steps or fewer and clear ingredient labels. Sub-USD 20 price points and functional naming conventions, Niacinamide 10% + Zinc 1% used by The Ordinary and The Inkey List, erode legacy price premiums.

Female purchasers, though dominant, see slowing incremental growth in North America and Western Europe as penetration nears ceiling levels, pushing brands toward gender-neutral storytelling. Korea’s USD 11.4 billion cosmetics exports reveal that men’s K-beauty SKUs, once niche, now appeal globally owing to package minimalism and fragrance-light chemistries.

By Distribution Channel: Online Retail Extends Lead on DTC Momentum

Online retail is forecast to climb 12.81% CAGR to 2031, fueled by AI-enabled skin diagnostics on Chinese platforms, subscription models, and cost savings that brands reinvest in R&D. In China, digital channels already capture 52-57% of skincare purchases, dwarfing brick-and-mortar reliance. DTC gives labels immediate shopper data, enabling rapid A/B testing of ingredient percentages and packaging layouts.

Physical points of sale still command 56.13% of 2025 value, especially for first-time buyers who prefer tactile sampling. Pharmacies and drugstores leverage dermatologist trust to justify premium positioning for brands like La Roche-Posay, while specialist boutiques such as Sephora curate discovery zones that funnel consumers into online replenishment loops. The future appears resolutely omnichannel: showrooming drives trial, and e-commerce secures replenishment.

Geography Analysis

North America generated 37.83% of revenue in 2025, but growth is plateauing as per-capita usage approaches saturation levels and skin-minimalism curtails SKU breadth. The FDA’s heightened oversight post-MoCRA raises compliance budgets but simultaneously boosts consumer confidence when products meet reporting thresholds. Mass-channel blockbusters such as Olay Super Serum reached #1 in U.S. unit sales following a 2024 reformulation that merged peptides, niacinamide, and vitamin C in one flask. Canada and Mexico deliver steady incremental volume, though U.S. DTC dominance limits domestic challenger headroom.

Asia-Pacific is set to grow at 14.67% CAGR, the fastest worldwide. China’s skincare retail climbs toward RMB 701.1 billion by 2028, with domestic labels controlling 49.9% of 2024 share as they fuse ginseng, snow-mushroom, and rice-ferment storytelling with rapid ODM cycles. South Korea shipped USD 11.4 billion in cosmetics during 2025, helped by Cosmax and Kolmar Korea, which slashed launch timelines to under six months. India races toward USD 20 billion beauty spending by 2025 despite registration delays. Japan advances an epigenetic R&D storyline, exemplified by Shiseido’s 2025 global rollout of New Ultimune.

Europe wrestles with tighter cosmetic legislation that caps retinol and bans certain lighteners. Beiersdorf’s August 2025 release of EPICELLINE, validated through 18 months of clinical work, shows how brands respond by generating peer-reviewed dossiers. Counterfeit proliferation erodes trust and sales despite customs seizures. Elsewhere, Gulf Cooperation Council states favor halal-certified serums, while South America’s macro volatility restrains discretionary spend, though Natura & Co leverages Amazonian botanicals for differentiation.

Competitive Landscape

The skincare serums market remains moderately fragmented: the top five multinationals L’Oréal, Estée Lauder, Shiseido, Unilever, and Beiersdorf command significant share, whereas hundreds of indie and DTC brands fill the remainder. L’Oréal’s EUR 1 billion Medik8 takeover in 2025 highlights the chase for clinical IP and dermatologist channels. Estée Lauder’s serum category contributed materially to the firm’s USD 7.9 billion skincare sales in FY 2024, underscoring the strategic weight of concentrated actives.

Technological differentiation centers on liposomal, nanoparticle, and cyclodextrin encapsulation that lets brands abide by the EU’s 0.3% retinol cap without sacrificing outcome claims. AI-driven skin diagnostics, especially in China’s growing USD 3.5 billion online consultation market, personalize product recommendations and lift basket sizes. Blockchain authentication and tamper-evident closures seek to stem counterfeit erosion, although counterfeit sophistication continues to rise.

Converging consumer preferences toward hybrid, barrier-restoring, and gender-neutral formulas squeeze portfolios bloated with single-benefit SKUs. Companies able to pivot quickly, often those leveraging South Korean ODM plants with 1,000-unit minimums, capitalize on micro-trend windows before they sunset. Meanwhile, price-point democratization below USD 20, championed by The Ordinary and The Inkey List, complicates premium positioning for legacy players unless accompanied by verifiable clinical superiority.

Skincare Serums Industry Leaders

Galderma SA

L’Oréal Group

Procter & Gamble

Pierre Fabre Group

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Beiersdorf introduced EPICELLINE, an epigenetic serum targeting DNA methylation pathways to reverse photoaging. The formulation underwent 18 months of clinical validation and received endorsement from the European Dermatology Forum.

- June 2025: L'Oréal acquired Medik8, a UK-based clinical skincare brand, for an estimated EUR 1 billion. The transaction grants L'Oréal access to Medik8's dermatologist network and vitamin C stabilization technology, with plans to expand distribution into Asia-Pacific and North America.

- February 2025: Shiseido launched NEW ULTIMUNE globally, a reformulated serum incorporating iris-root extract and reishi-mushroom ferment to modulate skin's innate immunity. The launch was supported by a USD 50 million marketing campaign spanning digital, in-store, and influencer channels.

Global Skincare Serums Market Report Scope

The skincare serums market encompasses all products formulated as serums that target specific skin concerns such as aging, hydration, pigmentation, acne, and dullness. These products typically contain higher concentrations of active ingredients compared to creams or lotions and are applied after cleansing but before moisturizing.

The skincare serums market is segmented by product type, skin concern, gender, distribution channel, and geography. By product type, the market is segmented into vitamin C serums, hyaluronic acid serums, retinol/retinoid serums, peptide serums, niacinamide serums, and multi-ingredient/hybrid serums. By skin concern, the market is segmented into anti-aging, hydration and moisturizing, acne & blemish control, brightening & pigmentation, sensitivity & redness, and repair & barrier support. By gender, the market is segmented into women and men. By distribution channel, the market is segmented into offline and online. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Vitamin C Serums |

| Hyaluronic Acid Serums |

| Retinol/Retinoid Serums |

| Peptide Serums |

| Niacinamide Serums |

| Multi-ingredient/Hybrid Serums |

| Anti-Ageing |

| Hydration & Moisturising |

| Acne & Blemish Control |

| Brightening & Pigmentation |

| Sensitivity & Redness |

| Repair & Barrier Support |

| Women |

| Men |

| Offline Retail | Super-/Hyper-markets |

| Beauty Specialty Stores | |

| Pharmacies & Drugstores | |

| Online Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vitamin C Serums | |

| Hyaluronic Acid Serums | ||

| Retinol/Retinoid Serums | ||

| Peptide Serums | ||

| Niacinamide Serums | ||

| Multi-ingredient/Hybrid Serums | ||

| By Skin Concern | Anti-Ageing | |

| Hydration & Moisturising | ||

| Acne & Blemish Control | ||

| Brightening & Pigmentation | ||

| Sensitivity & Redness | ||

| Repair & Barrier Support | ||

| By Gender | Women | |

| Men | ||

| By Distribution Channel | Offline Retail | Super-/Hyper-markets |

| Beauty Specialty Stores | ||

| Pharmacies & Drugstores | ||

| Online Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the skincare serums market be by 2031?

The skincare serums market size is projected to reach USD 7.46 billion by 2031, expanding at a 7.28% CAGR from 2026 to 2031.

Which product type is growing the fastest?

Peptide serums are set to expand at 8.12% CAGR through 2031 as brands pivot from antioxidant defense to collagen-stimulating actives.

What drives the fastest regional growth?

Asia-Pacific leads with a 14.67% CAGR through 2031, propelled by China’s domestic-brand boom, South Korea’s export momentum, and rising disposable incomes in India.

How important is online retail to future sales?

Online retail is forecast to grow at 12.81% CAGR to 2031, nearly double that of offline channels, as AI diagnostics and DTC models widen access and personalization.

What regulatory changes affect retinol serums?

Regulation (EU) 2024/996 limits retinol to 0.3% in leave-on cosmetics, compelling brands to adopt encapsulation or shift toward alternatives like bakuchiol.

Page last updated on: