Medical Tricorder Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

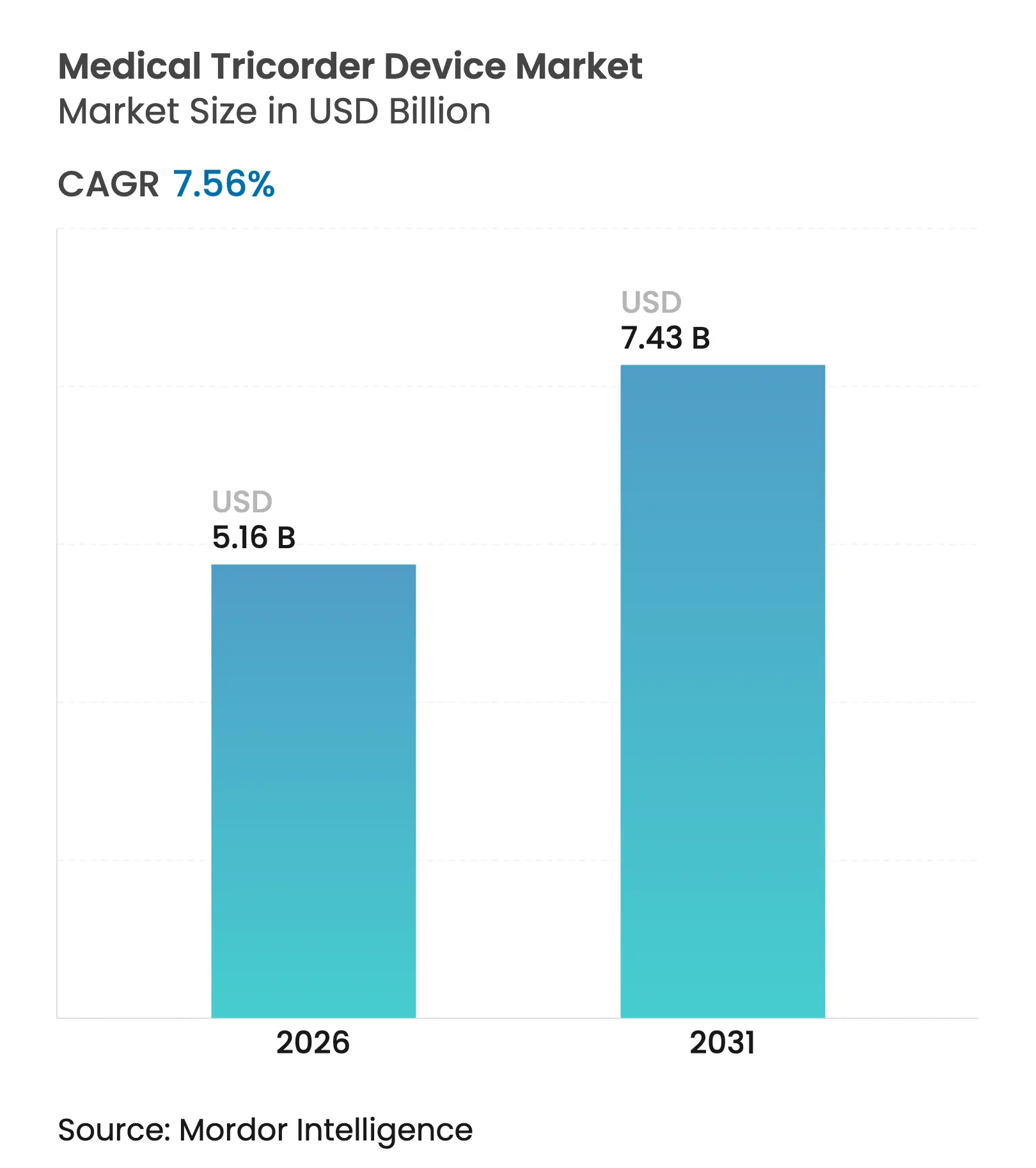

| Market Size (2026) | USD 5.16 Billion |

| Market Size (2031) | USD 7.43 Billion |

| Growth Rate (2026 - 2031) | 7.56 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Medical Tricorder Device Market Analysis by Mordor Intelligence

The medical tricorder market size in 2026 is estimated at USD 5.16 billion, growing from 2025 value of USD 4.8 billion with 2031 projections showing USD 7.43 billion, growing at 7.56% CAGR over 2026-2031. Growing acceptance of AI-enabled diagnostics, steady chronic-disease incidence, and an ongoing push for decentralized care position the technology as a cornerstone of point-of-care innovation. Semiconductor shortages that affect roughly half of connected medical devices highlight supply-chain fragility and underline the need for resilient sourcing strategies. Hardware still dominates revenue, yet accelerating software growth indicates a structural pivot toward intelligence-driven platforms where algorithms, not sensors alone, define performance. North America leads on account of mature reimbursement and regulatory clarity, while Asia Pacific’s rapid 8.1% growth signals the next expansion frontier as China and other economies streamline device approvals.

Key Report Takeaways

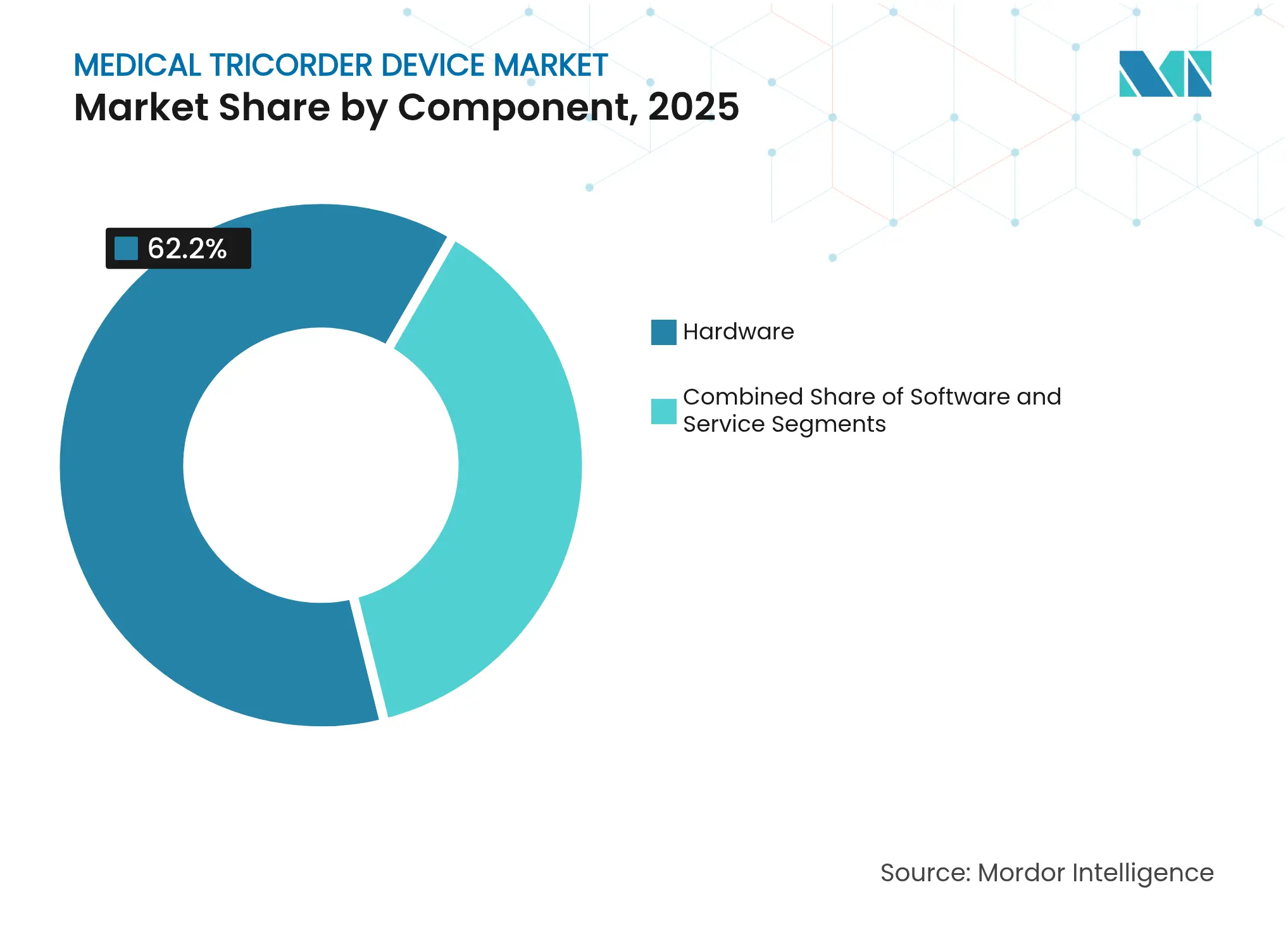

- By component, hardware led with 62.20% revenue share in 2025; software is advancing at a 9.63% CAGR through 2031.

- By technology, vital-sign monitoring captured 48.02% of medical tricorder market share in 2025, while lab-in-a-chip solutions are projected to expand at an 11.12% CAGR to 2031.

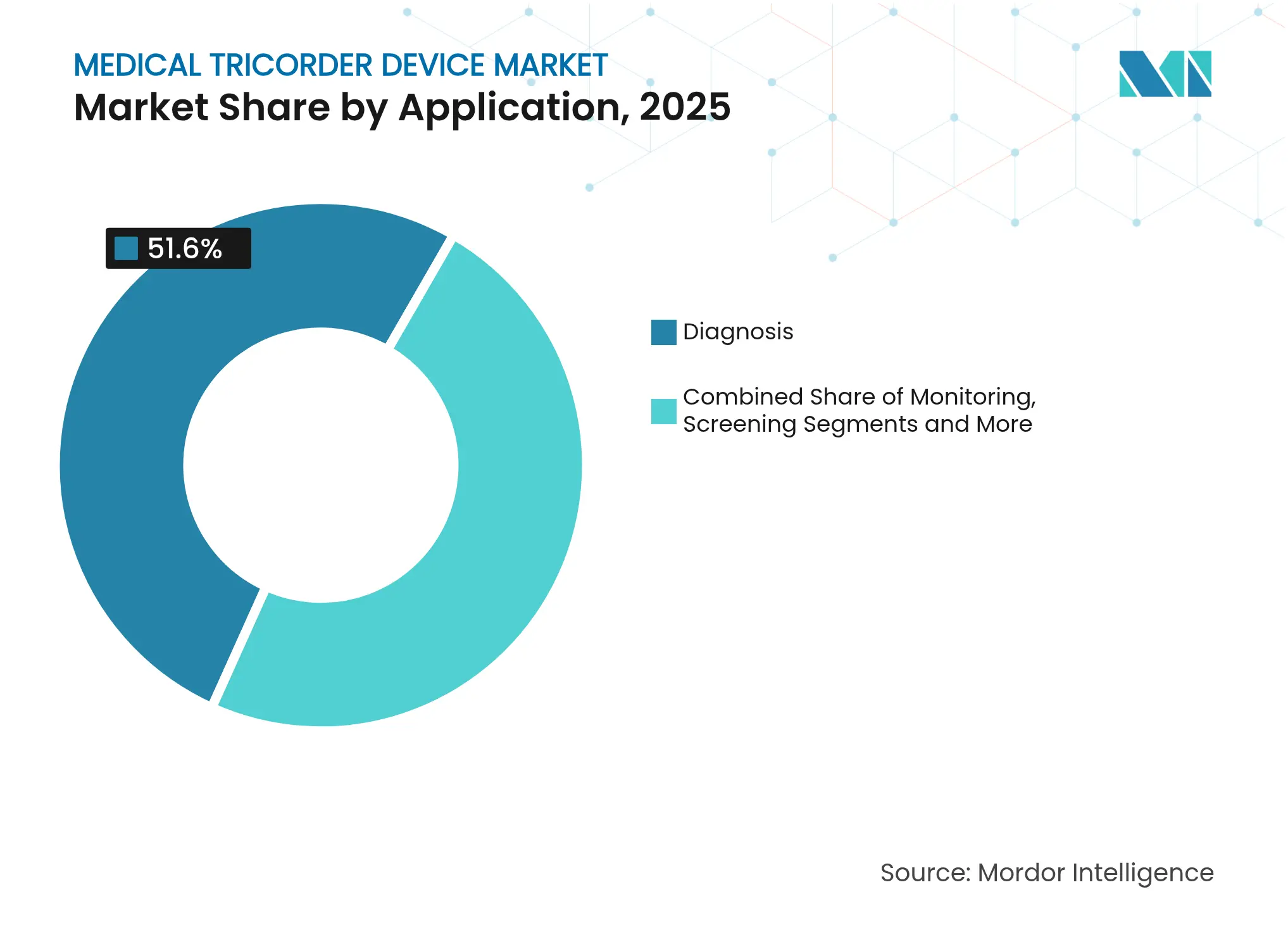

- By application, diagnosis held 51.60% of the medical tricorder market size in 2025; screening and early detection are forecast to grow at a 9.78% CAGR.

- By end user, hospitals accounted for 41.30% revenue share in 2025, whereas home healthcare exhibits the fastest 8.62% CAGR.

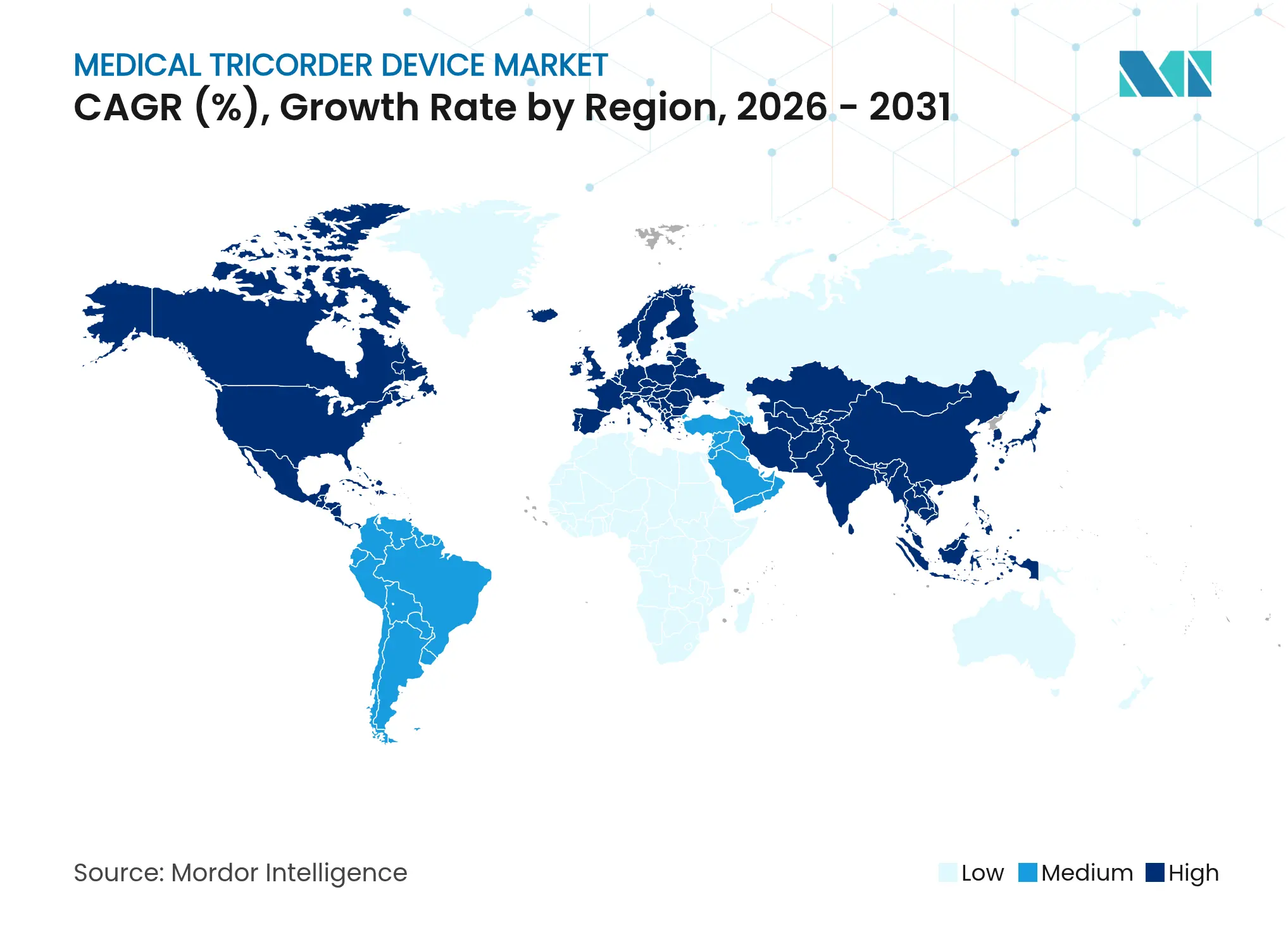

- By geography, North America commanded 38.04% revenue share in 2025; Asia Pacific records the highest regional CAGR at 7.78%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Tricorder Device Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Technological Miniaturization & Sensor Fusion Technological Miniaturization & Sensor Fusion | +2.10% | Global, with APAC manufacturing advantages | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.10% | Geographic Relevance:Global, with APAC manufacturing advantages | Impact Timeline:Medium term (2-4 years) |

Rising Prevalence Of Chronic Diseases Rising Prevalence Of Chronic Diseases | +1.80% | Global, concentrated in aging populations | Long term (≥ 4 years) | |||

Push For Decentralized Healthcare & Home Diagnostics Push For Decentralized Healthcare & Home Diagnostics | +1.50% | North America & EU leading, APAC following | Short term (≤ 2 years) | |||

Government Funding & Pilot POC Programs Government Funding & Pilot POC Programs | +1.20% | North America & EU primary, selective APAC | Medium term (2-4 years) | |||

Space & Defense R&D Spill-Over Into Healthcare Space & Defense R&D Spill-Over Into Healthcare | +0.80% | US, EU, China, India defense sectors | Long term (≥ 4 years) | |||

Remote Clinical-Trial Adoption Remote Clinical-Trial Adoption | +0.70% | Global, regulatory-dependent regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Technological Miniaturization & Sensor Fusion

Advances in nanofluid sensors raise biomolecule-detection sensitivity tenfold, bringing lab-grade performance to handheld devices. Carbon-nanotube bioFET arrays paired with local amplifiers deliver label-free assays that improve diagnostic specificity while reducing power drain, enhancing portability. Gold-nano interdigitated electrodes enable self-driven microfluidic flow, eliminating external pumps yet sustaining precise analyte control. These innovations collectively shrink instrument footprints, cut sample volumes, and support multimodal data fusion, which in turn elevates diagnostic accuracy beyond the limits of single-sensor tools.

Rising Prevalence of Chronic Diseases

Diabetes, cardiovascular illness, and respiratory disorders continue to tax global health systems, intensifying demand for continuous, non-invasive diagnostics. Point-of-care cardiac troponin assays now achieve 100% sensitivity and superior specificity versus centralized labs, accelerating treatment initiation.[1]BMJ Open Heart, “Point-of-Care Troponin Accuracy,” openheart.bmj.com Near-infrared spectroscopy platforms show glucose-measurement accuracy within 3% of finger-stick methods, removing one of the main adoption barriers for patients with diabetes. Economic analysis of remote-monitoring programs shows average savings of USD 2,200 per member per year by lowering emergency and inpatient use.

Push for Decentralized Healthcare & Home Diagnostics

Remote-care models gained momentum after the pandemic, aligned with Medicare reimbursement that jumped from USD 6.8 million in 2019 to USD 194.5 million in 2023. Hospital-at-home pilots now record patient-satisfaction scores higher than those earned by leading consumer-technology firms.[2]MDPI Diagnostics, “Near-Infrared Glucose Monitoring,” mdpi.comAI-embedded handheld devices supply real-time guidance, allowing users to self-triage and obtain immediate feedback, which relieves clinical bottlenecks.

Government Funding & Pilot POC Programs

The UK’s TRICORDER program, covering 100 general-practice sites, demonstrates scalable deployment and real-world outcome gains. NASA’s work on autonomous diagnostic kits for space travel accelerates component ruggedization that later migrates to consumer healthcare.[3]American Medical Association, “Remote Patient Monitoring ROI,” ama-assn.orgThe FDA draft guidance released in 2025 clarifies lifecycle requirements for AI-enabled devices, shortening submission iterations and increasing investment appeal.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent Multi-Jurisdiction Device Regulations Stringent Multi-Jurisdiction Device Regulations | -1.40% | Global, varying by regulatory maturity | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.40% | Geographic Relevance:Global, varying by regulatory maturity | Impact Timeline:Medium term (2-4 years) |

Data Privacy & Cybersecurity Concerns Data Privacy & Cybersecurity Concerns | -1.10% | EU (GDPR), US (HIPAA), expanding globally | Short term (≤ 2 years) | |||

Supply-Chain Constraints For Biosensing Chips Supply-Chain Constraints For Biosensing Chips | -0.90% | Global, concentrated in APAC manufacturing | Short term (≤ 2 years) | |||

Clinician Liability & Diagnostic-Accuracy Skepticism Clinician Liability & Diagnostic-Accuracy Skepticism | -0.70% | North America & EU primarily, professional liability focus | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Multi-Jurisdiction Device Regulations

Divergent approval pathways weigh on go-to-market speed. The EU Medical Device Regulation raises evidence standards, while FDA staffing cuts have lengthened review cycles, extending global launch timelines by up to two years. Limited harmonization compels companies to fund separate clinical studies for each region, inflating compliance costs and hindering smaller entrants.

Data Privacy & Cybersecurity Concerns

Connected diagnostics face a 59% surge in reported vulnerabilities, prompting the FDA to require formal cybersecurity plans within every premarket submission. GDPR and HIPAA enforcement obligate sophisticated encryption and audit processes, while only 22.1% of cleared AI devices disclose demographic fairness data, drawing scrutiny over potential algorithmic bias. Continuous patching, monitoring, and recurring costs remain vital to safeguard patient trust.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Hardware held a 62.20% revenue share in 2025 and still anchors the medical tricorder market through integrated sensor arrays and microfluidic structures that guarantee accuracy at the bedside. However, software revenues are growing 9.63% annually as algorithm updates now outpace physical redesign cycles. Regulatory acceptance of adaptive AI models, alongside 107 FDA clearances for software-driven devices in 2024, amplifies the shift toward code-based differentiation.

Software’s climb suggests a rebalancing of the medical tricorder market size, with post-launch algorithm refinements improving sensitivity without new hardware. Planned-change control policies let firms upload validated updates in days, sustaining competitive edges. Services complete the value mix by keeping installed fleets compliant and calibrated, often through cloud-delivered diagnostics that pre-empt downtime.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Lab-in-a-Chip Innovation Challenges Vital-Sign Monitoring Leadership

Vital-sign instruments owned 48.02% of 2025 revenue on the strength of decades-old sensor maturity. Lab-in-a-chip devices, though smaller in today’s revenue mix, are scaling at an 11.12% CAGR and are expected to widen the overall medical tricorder market. Innovations such as gold-nano electrode chips deliver controlled flow without pumps, shrinking portable molecular-testing footprints to smartphone dimensions.

Convergence is visible in hybrid units that merge imaging, biochemical, and physiologic data streams for a unified clinical snapshot. Such platforms illustrate how the medical tricorder market share will favor multi-modal systems that can screen, diagnose, and triage in one workflow. Regulatory familiarity with multiplex assays further accelerates label expansion, deepening technology stickiness across primary care and emergency settings.

By Application: Screening & Early Detection Disrupts Diagnosis Focus

Diagnosis kept 51.60% of 2025 revenue as clinicians rely on quick, rule-out tests at the point of care. Screening and early detection, advancing 9.78% per year, is steadily enlarging its proportion of the medical tricorder market size as preventive medicine gains policy backing. Handheld retinal-imaging AI achieves over 90% sensitivity in ophthalmic screening, illustrating the gains possible when triage moves upstream.

Continuous arrhythmia monitoring via wearable photoplethysmography validates the trend: 87.9% patient compliance and nighttime-peak detection rates elevate chronic-care outcomes. As payers shift to value-based reimbursement, economic rewards align with early-stage intervention, consolidating demand for compact, multi-analyte screening tools.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home Healthcare Acceleration Challenges Hospital Dominance

Hospitals still accounted for 41.30% revenue in 2025, thanks to entrenched purchasing channels and established credentialing. Yet home healthcare’s 8.62% CAGR signals a decisive swing in the medical tricorder market toward patient-managed diagnostics. Ochsner Health’s remote-monitoring program documented savings of USD 2,200 per member yearly, proving that decentralized models can drive both clinical and financial benefits.

User experience now rivals clinical performance: feedback from device clinics cites connectivity issues and alert fatigue as limiting factors, incentivizing new designs that embed AI triage to cut false alarms. Military and defense pilots continue to validate ruggedization requirements, which then cascade into consumer versions robust enough for daily wear.

Geography Analysis

North America’s 38.04% revenue leadership in 2025 reflects clear regulatory precedents and robust clinical-validation networks. Medicare’s reimbursement surge to USD 194.5 million in 2023 for remote monitoring, evidence sustained policy momentum, while more than 1,000 FDA-authorized AI devices normalize advanced diagnostics across settings. Recent FDA headcount reductions, however, extend review queues, creating windows for APAC makers that navigate shorter domestic pathways. The UK’s 100-site TRICORDER rollout further demonstrates scalable public-health deployment, providing a template for regional replication.

Asia Pacific posts the fastest regional CAGR at 7.78%, underpinned by rising chronic-disease prevalence and government digitization drives. China’s 2027 reforms streamline innovative-device reviews through 24 process upgrades, accelerating commercialization cycles. Despite a 22% fall in venture funding since 2021, a projected USD 225 billion medical technology spend by 2030 underwrites demand. Regional AI spend on medtech is set to hit USD 250 million by 2028, emphasizing local appetite for intelligence-driven care.

Europe, the Middle East & Africa, and South America present mixed landscapes. Stricter EU device regulations elevate compliance costs but fortify long-term confidence. Australia expands reference-market inclusion to quicken approvals, offering an alternate access route for multinational suppliers. Global chip shortages continue to squeeze production, especially across emerging markets with fragile logistics chains.

Competitive Landscape

Market Concentration

Fragmentation defines today’s medical tricorder market, with legacy med-device leaders, consumer-electronics entrants, and AI specialists competing on sensor fidelity, algorithm quality, and clinical validation. No firm holds a dominant global share, keeping the market open for leapfrog innovation. Partnerships between silicone-design houses and cloud-analytics vendors proliferate, recognizing that future wins depend on integrated software ecosystems rather than standalone hardware.

The FDA’s clearance of 107 AI-enabled devices in 2024, 75% in radiology, demonstrates regulators’ growing comfort with algorithmic tools, pushing competitors to secure machine-learning talent. Patent filings around microfluidic and sensor-fusion techniques surge, with nanofluid sensors achieving a ten-fold sensitivity boost and carbon-nanotube bioFET designs reaching label-free detection thresholds. Chip shortages that delay 80% of medtech projects by over a year have become a differentiator, advantaging companies that diversified their fabs before the crunch.

As reimbursement shifts to outcome-based models, competitive emphasis falls on clinical-outcome evidence. Firms demonstrating statistically significant mortality or cost-of-care reductions secure favorable formulary and payer contracts, reinforcing a flywheel where validated data fuels market share gains.

Medical Tricorder Device Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Neko Health raised USD 260 million to accelerate next-generation portable health-scanner rollouts.

- January 2025: The FDA released comprehensive draft guidance for AI-enabled medical device developers, providing regulatory clarity for lifecycle management and marketing submission requirements that could accelerate tricorder platform approvals.

- November 2024: AEYE Health obtained FDA clearance for the first fully autonomous handheld diabetic-retinopathy screening device.

- July 2024: Chronus Health revealed electrical-sensing blood-test technology capable of real-time results in urgent-care settings.

Table of Contents for Medical Tricorder Device Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Technological Miniaturization & Sensor Fusion

- 4.2.2Rising Prevalence Of Chronic Diseases

- 4.2.3Push For Decentralized Healthcare & Home Diagnostics

- 4.2.4Government Funding & Pilot POC Programs

- 4.2.5Space & Defense R&D Spill-Over Into Healthcare

- 4.2.6Remote Clinical-Trial Adoption

- 4.3Market Restraints

- 4.3.1Stringent Multi-Jurisdiction Device Regulations

- 4.3.2Data Privacy & Cybersecurity Concerns

- 4.3.3Supply-Chain Constraints For Biosensing Chips

- 4.3.4Clinician Liability & Diagnostic-Accuracy Skepticism

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Component

- 5.1.1Hardware

- 5.1.2Software

- 5.1.3Services

- 5.2By Technology

- 5.2.1Vital-sign Monitoring Tricorder

- 5.2.2Imaging Tricorder

- 5.2.3Lab-in-a-Chip/Biosensing Tricorder

- 5.2.4Multi-modal/Hybrid

- 5.3By Application

- 5.3.1Diagnosis

- 5.3.2Monitoring

- 5.3.3Screening & Early Detection

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Clinics

- 5.4.3Home Healthcare

- 5.4.4Military & Defense

- 5.4.5Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1QuantuMDx Group Ltd.

- 6.3.2Cloud DX

- 6.3.3Basil Leaf Technologies, LLC

- 6.3.4Medipense Inc.

- 6.3.5Aidar Health Inc.

- 6.3.6SensoDX II LLC

- 6.3.7Accurable Ltd.

- 6.3.8Caretaker Medical, LLC

- 6.3.9Chronisense Medical Ltd.

- 6.3.10Cardiomo Inc.

- 6.3.11VitalConnect Inc.

- 6.3.12Avidhrt Inc.

- 6.3.13Creative Medical (Creative Industry Co., Ltd.)

- 6.3.14TytoCare Ltd.

- 6.3.15MedWand Solutions Inc.

- 6.3.16Healthy.io Ltd.

- 6.3.17Scanwell Health Inc.

- 6.3.18Eko Devices Inc.

- 6.3.19BioIntelliSense Inc.

- 6.3.20Withings SA

- 6.3.21Omron Healthcare Inc.

- 6.3.22Fitbit (Google LLC)

- 6.3.23Apple Inc.

- 6.3.24Masimo Corporation

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Medical Tricorder Device Market Report Scope

As per the scope of the report, a medical tricorder is a handheld and portable scanning device that can be used by people for self-diagnosis and monitoring physiological vitals in minimum time and with ease. The medical tricorder can be deployed as a general tool for measuring blood flow, body temperature, heart rate, blood pressure, etc. Also, it can diagnose the condition by analyzing patients' key health factors and send information to healthcare practitioners anywhere in the world. The Medical Tricorder Device Market is segmented by Type (USB Camera, Fibre Optic Camera, Wireless, Corded, and Others), Application (Diagnosis and Monitoring), End-User (Hospitals, Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD million) for the above segments.