Self-Administered Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

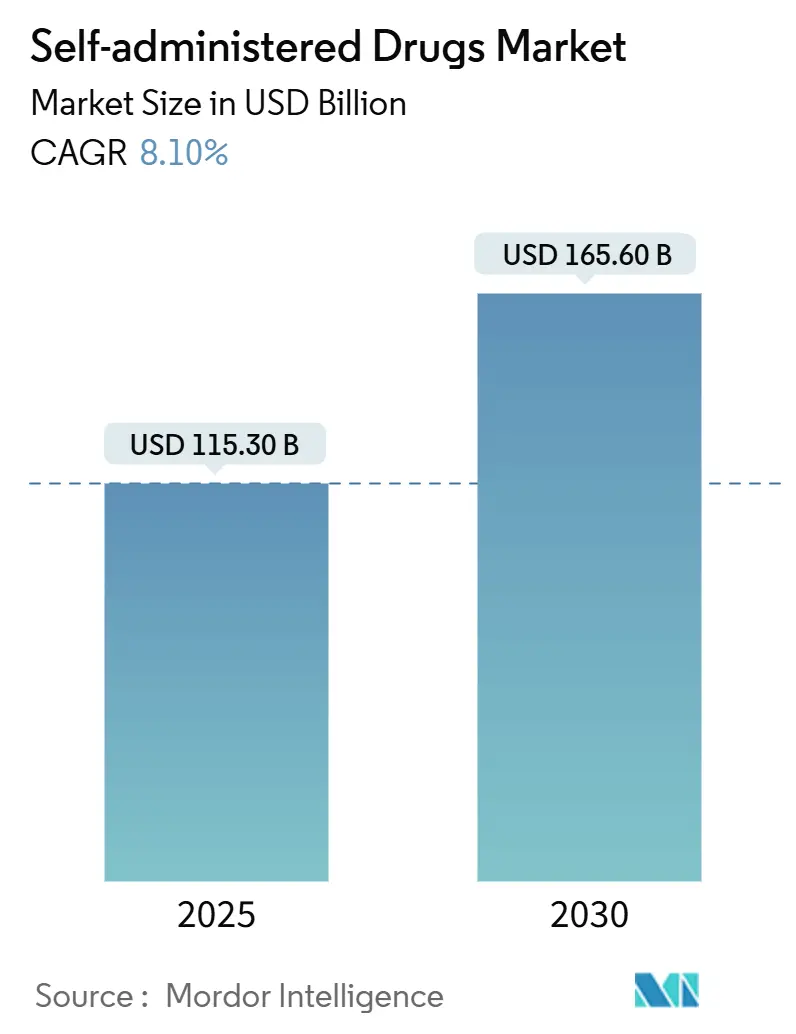

| Market Size (2025) | USD 115.30 Billion |

| Market Size (2030) | USD 165.60 Billion |

| Growth Rate (2025 - 2030) | 8.10% CAGR |

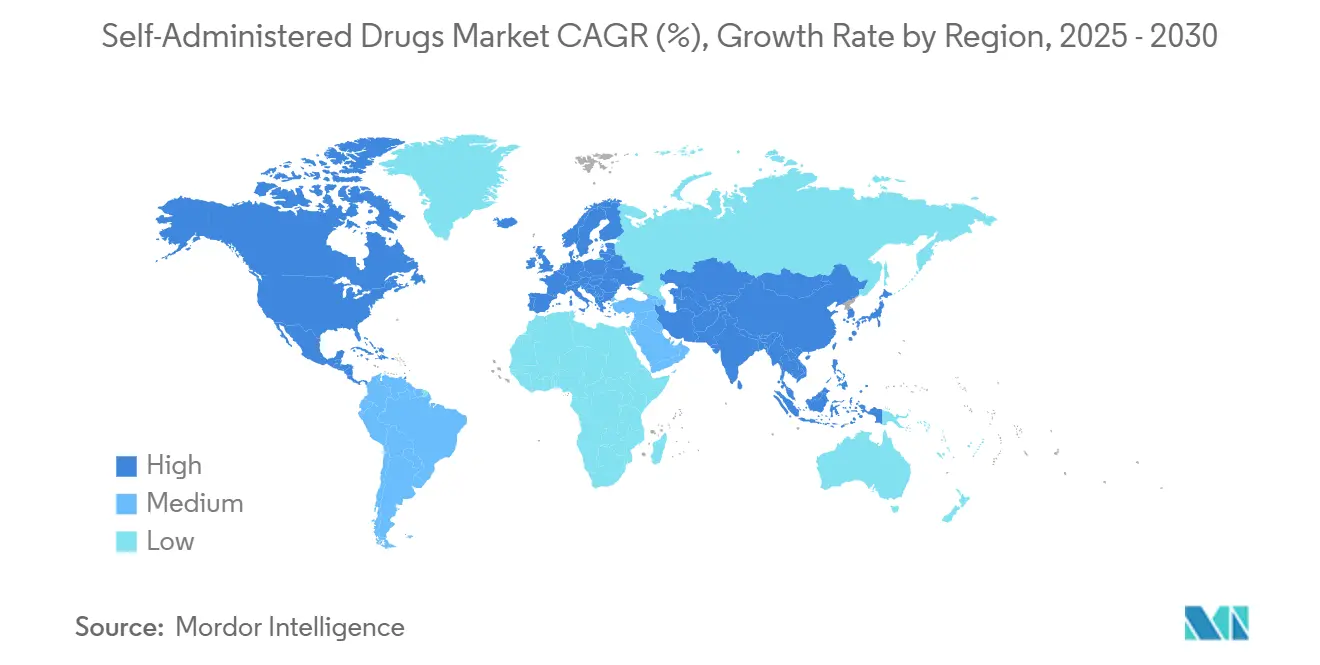

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Administered Drugs Market Analysis by Mordor Intelligence

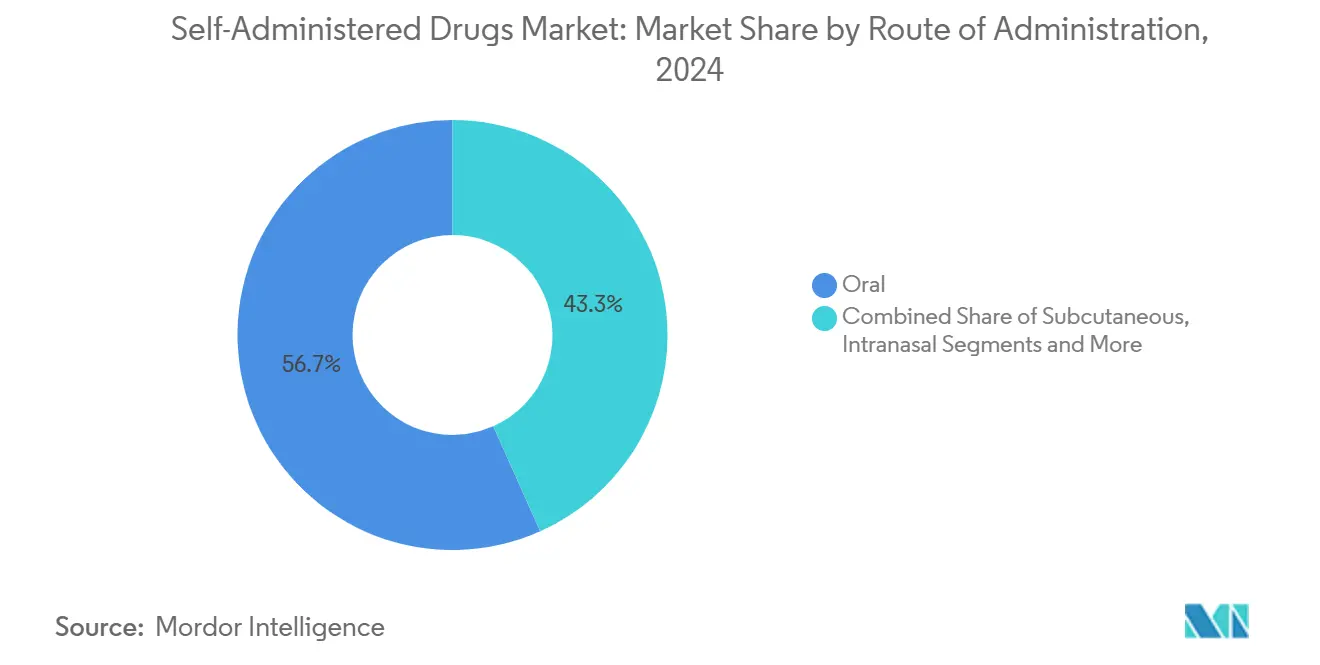

The self-administered drugs market size stood at USD 115.3 billion in 2025 and is forecast to reach USD 165.6 billion by 2030, advancing at an 8.1% CAGR. Continued progress in digital health tools, streamlined regulatory reviews for at-home biologics, and the maturation of user-friendly delivery devices are moving the locus of care from clinics to the home. North America and Europe jointly generated roughly 65% of global revenue in 2024, buoyed by robust reimbursement policies and well-established cold-chain logistics. At the same time, the Self-administered drugs market is widening rapidly in Asia-Pacific, where middle-class expansion, government support for home-based care, and rising chronic disease prevalence underpin a regional CAGR above 10%. Oral formulations retained the largest route-of-administration foothold at a 56.7% Self-administered drugs market share in 2024. Yet, subcutaneous auto-injectables are growing faster as device ergonomics improve and patient training scales. Across device formats, innovative connected solutions—ranging from dose-tracking pens to sensor-enabled inhalers—are attracting pay-for-performance incentives that reward documented adherence.

Key Report Takeaways

- By route of administration, oral products held 56.7% of the Self-administered drugs market share in 2024, while subcutaneous self-injectables are projected to post the quickest expansion at a 10.6% CAGR through 2030.

- By therapeutic area, diabetes accounted for 34.5% of the Self-administered drugs market size in 2024; autoimmune and biologic therapies are poised to rise at a 12% CAGR between 2025 and 2030.

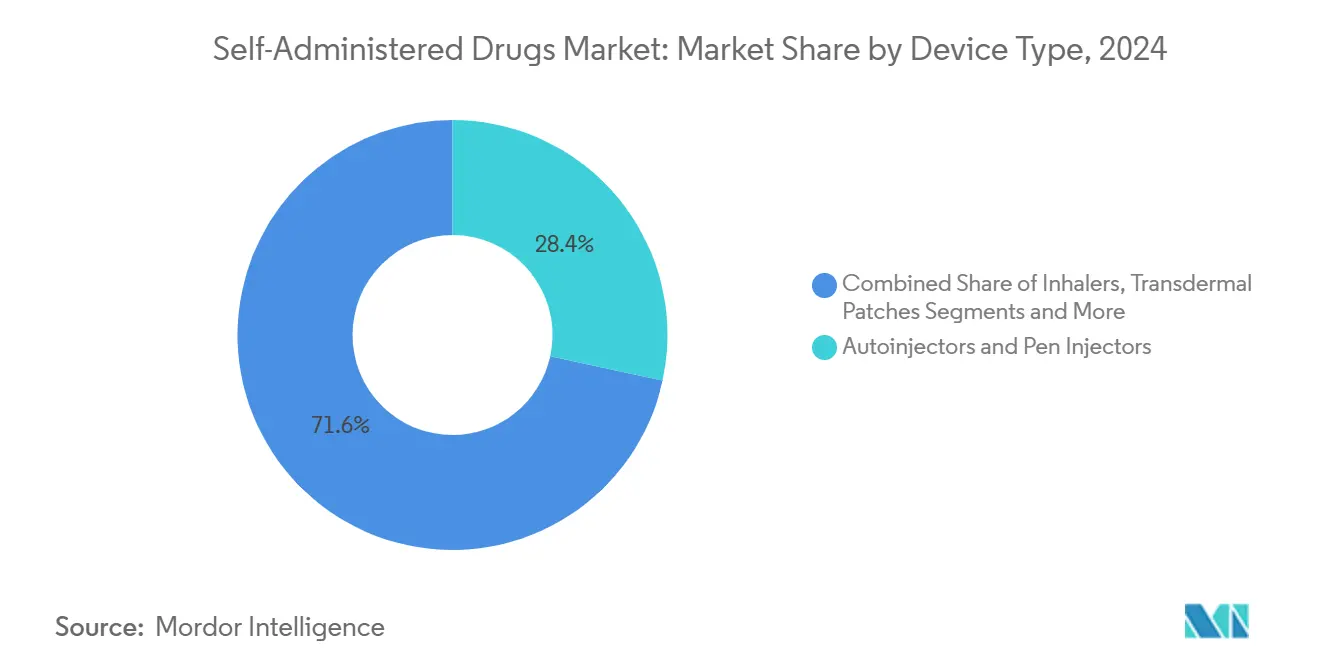

- By device type, autoinjectors and pen injectors led with 28.4% revenue share in 2024, yet smart connected devices are forecast to scale at a 15.1% CAGR to 2030.

- By distribution channel, retail pharmacies commanded 48.1% of 2024 sales, whereas online pharmacies are on track for the fastest growth at a 15.7% CAGR through 2030.

- By geography, North America dominated with a 45% share in 2024; Asia-Pacific represents the most dynamic region, set to expand above a 10% CAGR during the outlook period.

Global Self-Administered Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.80% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Growing preference for home healthcare & convenience | +1.50% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Technological advances in self-injectors & inhalers | +1.20% | North America & EU lead, APAC follows | Medium term (2-4 years) |

| Supportive regulatory pathways for at-home biologics | +1.00% | Primarily North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Digital adherence monitoring linked to pay-for-performance | +0.80% | North America lead, selective EU uptake | Short term (≤ 2 years) |

| Pharmacist-prescribed therapeutics & upcoming OTC biologic switches | +0.60% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Escalating rates of diabetes, cardiovascular disorders, and autoimmune conditions are altering care pathways, making at-home delivery the practical default for long-term therapy. Diabetes alone represented a USD 37.8 billion subset of the Self-administered drugs market in 2025, powered by continuous-glucose-monitoring integrations that enable dose titration in real time.[1]Chih-Yuan Chen et al., “Real-World Effectiveness of the Gla-300 + Cap + App Program in Adult Users Living with Type 2 Diabetes in Taiwan,” Diabetes Therapy, springer.com Aging demographics and lifestyle risks heighten demand for self-management solutions, while regulators fast-track combination drug-device filings to relieve systemwide cost pressures. Integrated platforms that track outcomes remotely amplify clinical value and are accelerating pay-for-performance contracts in high-income regions.

Growing Preference for Home Healthcare & Convenience

Consumer expectations forged by the pandemic now emphasize autonomy, lower visit burdens, and digital connectivity. Rheumatoid arthritis saw a 23% jump in autoinjector adoption during 2024, attributed to refined ergonomics and comprehensive coaching resources.[2]Mallinckrodt plc, “Acthar Gel SelfJect Injector Availability,” mallinckrodt.com Younger cohorts accustomed to app-based services welcome delivery models that mesh with daily routines. Health systems are redesigning pathways to keep stable patients home, reallocating nurse capacity and expanding virtual check-ins. Drug makers that bundle onboarding apps, adherence nudges, and teleconsult access are capturing stickier market share.

Technological Advances in Self-Injectors & Inhalers

Engineering progress—covering needle-free propulsion, high-viscosity handling, and integrated sharps-safety locks—has unlocked at-home use for molecules once limited to infusion suites. Smart inhalers with usage sensors feed granular data to clinicians, narrowing the persistence gap in asthma and COPD. Rapid device miniaturization allows elderly patients with limited dexterity to self-dose confidently. Capacity ramps such as SHL Medical’s USD 220 million plant in South Carolina underscore confidence in sustained demand.

Supportive Regulatory Pathways for At-Home Biologics

Agencies on both sides of the Atlantic have condensed timelines by treating real-world device analytics as evidence of effectiveness. The FDA’s green light for Neffy, the first needle-free epinephrine, cemented a precedent for emergency therapeutics in spray form. EMA’s endorsement of patient-controlled rozanolixizumab infusion pumps similarly signals willingness to trust well-trained patients. Harmonization initiatives are smoothing multiregional launches, particularly for biosimilars pivoting to self-injected formats.[3]European Medicines Agency, “Human Medicines 2024,” ema.europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Needle-phobia and adherence challenges | -1.20% | Global, higher in pediatric populations | Medium term (2-4 years) |

| Safety concerns & dosing errors outside clinical settings | -0.90% | Primarily emerging markets | Short term (≤ 2 years) |

| Cold-chain failures for temperature-sensitive biologics | -0.70% | APAC & emerging markets | Long term (≥ 4 years) |

| Data-privacy uncertainty for patient-generated device data | -0.50% | GDPR regions, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Needle-Phobia and Adherence Challenges

Injection anxiety affects up to 25% of adults and 63% of children, capping reach for injectable biologics, particularly in pediatrics. Neffy’s nasal route sets a template for broader needle-free innovation that can convert hesitant segments. Sustained adherence also hinges on ongoing technical support, given the risk of device malfunction or forgotten doses over long regimens. Programs that pair behavioral coaching with alternative delivery routes—sublingual films, intranasal sprays, or long-acting implants—are alleviating discontinuation risk.

Safety Concerns & Dosing Errors Outside Clinical Settings

High-potency monoclonals have narrow therapeutic windows; even minor errors can trigger adverse events. The FDA has issued device-safety guidance urging mandatory confirmation steps on pen injectors. Manufacturers are responding with dual-chamber syringes that deliver audible confirmation clicks and lockouts after full dose transfer. Telemetry-enabled wearables send dosing data to clinicians, creating rapid feedback loops, yet adoption remains uneven in markets with limited broadband penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Oral Dominance Challenged by Injectable Innovation

Oral therapies retained a 56.7% Self-administered drugs market share in 2024, buoyed by manufacturing familiarity and patient comfort. Nevertheless, subcutaneous formats are accelerating at a 10.6% CAGR on the back of biologic uptake and autoinjector ease. Rapid-absorption intranasal sprays, such as needle-free epinephrine, have showcased commercial potential by eliminating injection barriers. Continuous progress in pulmonary delivery, including digital inhalers that record every actuation, is recasting adherence standards in respiratory care. Transdermal patches now incorporate micro-sensors that verify skin contact duration, ensuring dose integrity over multi-day wear periods. Regulatory agencies are granting accelerated reviews where new routes replace costly infusion center visits.

Second-generation depot injectables and wearable pumps further shrink clinic touchpoints. As patient training curricula expand via virtual reality modules, even complex multi-step injections are completed successfully by elderly cohorts. Over the forecast horizon, innovators will likely package multiple routes within a single therapeutic franchise—oral maintenance tablets flanked by on-demand nasal rescue sprays—creating responsive dosing ecosystems inside the broader Self-administered drugs market.

By Therapeutic Area: Diabetes Leadership Faces Autoimmune Growth Surge

Diabetes anchored 34.5% of 2024 revenue, supported by mature insulin pens, continuous glucose sensors, and established reimbursement. The segment’s advance now focuses on closed-loop algorithms that auto-titrate delivery. Autoimmune conditions—including rheumatoid arthritis and multiple sclerosis—are slated for the fastest lift, growing at a 12% CAGR as high-value biologics migrate to patient-controlled autoinjectors. With the Self-administered drugs market size for autoimmune biologics expanding swiftly, device refinements that handle high-viscosity solutions are critical.

Anticoagulants and migraine therapies also benefit from at-home usability gains, lowering emergency department reliance. Hormone-replacement segments leverage discreet patches and pens that align with lifestyle needs. Respiratory disorders integrate smart inhalers that feed data directly into electronic health records, enabling real-time clinician interventions. Pain-management autoinjectors delivering non-opioid formulations present a compelling option for acute episodes, reducing refill regulatory burdens. Therapeutic diversification underscores a central finding: once self-administration is proven safe, payers and providers rapidly broaden indications to free clinic bandwidth.

By Device Type: Smart Technology Disrupts Traditional Autoinjector Leadership

Autoinjectors and pen injectors captured 28.4% of 2024 sales, long lauded for dose precision and sharps safety. Connected add-ons—Bluetooth chips that log timestamped injections—are now table stakes for new launches. Smart devices, though still emerging, are projected to have a 15.1% CAGR, cementing them as the pivotal growth lever in the Self-administered drugs market. Inhalers embed pressure sensors and app-linked reminders, flipping historically poor compliance into quantifiable data streams. Transdermal patches embed micro-processors that alert users if adhesion loosens, protecting pharmacokinetics.

Nasal rescue devices demonstrate the viability of needle-free formats in life-threatening indications, widening the funnel for needle-averse populations. Oral smart packaging, using NFC tags to record pill removal, feeds adherence scores to payers that reimburse on outcome metrics. These digital footprints generate real-world evidence pivotal for accelerated label expansions and reimbursement negotiations. Device makers investing in robust, cloud-native security architectures are likely to lead as data-privacy scrutiny rises.

By Distribution Channel: Online Growth Challenges Retail Pharmacy Dominance

Retail outlets maintained a 48.1% revenue stake in 2024, leveraging walk-in counseling and insurance navigation. Yet shifting consumer expectations place convenience first, propelling e-pharmacies to a 15.7% CAGR through 2030 as cold-chain carriers prove capable of last-mile biologic delivery. Younger, digitally native users gravitate toward subscription refill models bundled with teleconsults. Specialty pharmacies are strengthening positions through full-service hubs that coordinate prior authorizations, patient education, and adverse-event triage in one ecosystem.

Hospital pharmacies still dominate induction dosing for complex therapies, but increasingly hand off maintenance scripts to community channels once adherence is demonstrated. Crucially, omnichannel strategies—click-and-collect lockers, AI-powered refill reminders, and pharmacist video chats—are blurring historical boundaries. Regulators are updating e-prescription statutes to seal safety gaps, thereby legitimizing web-based dispensers as co-equals to brick-and-mortar counterparts in the Self-administered drugs market.

Geography Analysis

North America wielded a commanding 45% share of 2024 revenue, reflecting early adoption of connected devices and payer enthusiasm for at-home biologics. The United States leads in outcome-based reimbursement that ties payment to digitally verified adherence metrics. Canada is following suit, recently approving methotrexate pens for autoimmune cases to ease clinic bottlenecks. Across the region, value-based care contracts are accelerating the uptake of smart autoinjectors that furnish real-time dosing data.

Europe ranked second with a roughly 25% share, underpinned by the European Medicines Agency’s progressive stance on self-administration safety. Germany and the United Kingdom spearhead e-prescription integration, allowing connected inhalers to export adherence logs directly into national health records. Biosimilar penetration is notable: payers are channeling cost savings from interchangeable self-injected versions into broader patient-support services. The continent’s strong privacy regulations, however, compel manufacturers to deploy sophisticated encryption protocols, slightly lengthening device certification cycles.

Asia-Pacific stands out for momentum, surpassing a regional CAGR of 10% through 2030 as middle-class populations swell. China’s reformed approval docket has cut median launch times for combination products by 12 months, propelling domestic biotechs into the Self-administered drugs market faster. India’s new materiovigilance norms build confidence in locally made pens and patches, while Japan’s super-aging society demands ergonomic designs. Cold-chain gaps and clinician training shortages remain headwinds, yet they simultaneously nurture partnerships in portable refrigeration and e-learning platforms.

Competitive Landscape

The self-administered therapeutics industry shows moderate concentration: the top five players collectively control nearly half of global revenue, leveraging end-to-end capabilities spanning molecule discovery, device engineering, and patient-support programming. Integrated portfolios allow incumbents to cross-subsidize innovations such as connected autoinjectors without relying solely on unit margins. BD’s alliance with Ypsomed on high-viscosity syringes typifies device-centric collaborations that unlock new biologic classes.

M&A activity is brisk. The 2025 Kindeva-Meridian merger created a contract-development powerhouse with 300+ autoinjector patents and expanded fill-finish capacity for inhalation and parenteral projects. Big Pharma’s verticalization runs parallel to biotech–device partnerships like Novartis and Lindy Biosciences, which are converting IV biologics to subcutaneous formats that fit at-home care models. Despite incumbent scale, white-space persists in pediatric-specific devices and latency-free digital dashboards.

Start-ups are capitalizing on cloud-native architectures and AI-driven dosing algorithms, often licensing molecules from mid-tier pharma to prove platform utility. Regional contenders in China and India are targeting price-sensitive segments with simplified mechanical pens. Data-governance expertise is emerging as a differentiator; manufacturers able to demonstrate GDPR-compliant data pipelining gain an edge in EU tenders. Overall, sustained device innovation and real-world-data fluency underpin competitive advantage across the Self-administered drugs market.

Self-Administered Drugs Industry Leaders

Novo Nordisk A/S

Eli Lilly & Co.

Sanofi

GlaxoSmithKline plc

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SHL Medical opened a USD 220 million autoinjector plant in North Charleston to boost annual output to 1.5 billion devices, serving cardiometabolic demand.

- March 2025: Novartis invested USD 20 million with Lindy Biosciences to microglassify intravenous biologics into self-injected formulations.

- February 2025: Kindeva Drug Delivery and Meridian Medical Technologies merged, forming a global CDMO for combination products.

- December 2024: BD pledged USD 1.2 billion to expand pre-fillable syringe capacity, supporting temperature-sensitive therapeutics.

Global Self-Administered Drugs Market Report Scope

| Oral |

| Subcutaneous (Self-injectables) |

| Intranasal |

| Pulmonary / Inhalation |

| Transdermal |

| Others (Ocular, Buccal, etc.) |

| Diabetes Care |

| Anticoagulation |

| Hormone & Reproductive Health |

| Respiratory Disorders |

| Pain Management & Migraine |

| Autoimmune & Biologics |

| Others |

| Prefilled Syringes |

| Autoinjectors & Pen Injectors |

| Inhalers (MDI, DPI, Soft-mist) |

| Transdermal Patches |

| Nasal Sprays |

| Oral Solid Dosage |

| Smart Connected Devices |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| Specialty Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Route of Administration | Oral | |

| Subcutaneous (Self-injectables) | ||

| Intranasal | ||

| Pulmonary / Inhalation | ||

| Transdermal | ||

| Others (Ocular, Buccal, etc.) | ||

| By Therapeutic Area | Diabetes Care | |

| Anticoagulation | ||

| Hormone & Reproductive Health | ||

| Respiratory Disorders | ||

| Pain Management & Migraine | ||

| Autoimmune & Biologics | ||

| Others | ||

| By Device Type | Prefilled Syringes | |

| Autoinjectors & Pen Injectors | ||

| Inhalers (MDI, DPI, Soft-mist) | ||

| Transdermal Patches | ||

| Nasal Sprays | ||

| Oral Solid Dosage | ||

| Smart Connected Devices | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| Specialty Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Self-administered therapeutics market by 2030?

The market is expected to reach USD 165.6 billion in 2030 underpinned by an 8.1% CAGR.

Which region is expanding fastest in Self-administered therapeutics?

Asia-Pacific is forecast to compound above 10% annually, supported by policy reforms and growing middle-class demand.

Which therapeutic area currently generates the most revenue?

Diabetes care leads, accounting for 34.5% of 2024 revenue thanks to mature insulin delivery ecosystems.

Which device category is growing quickest?

Smart connected delivery systems, including sensor-enabled autoinjectors and inhalers, are on track for a 15.1% CAGR through 2030.

How are distribution channels shifting?

Retail pharmacies still dominate sales, but online pharmacies are expanding at a 15.7% CAGR as cold-chain home delivery matures.

What are the main barriers to broader adoption?

Needle-phobia, safety concerns with at-home dosing, cold-chain challenges in emerging markets, and data-privacy regulations temper uptake.

Page last updated on: