Electronic Drug Delivery Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

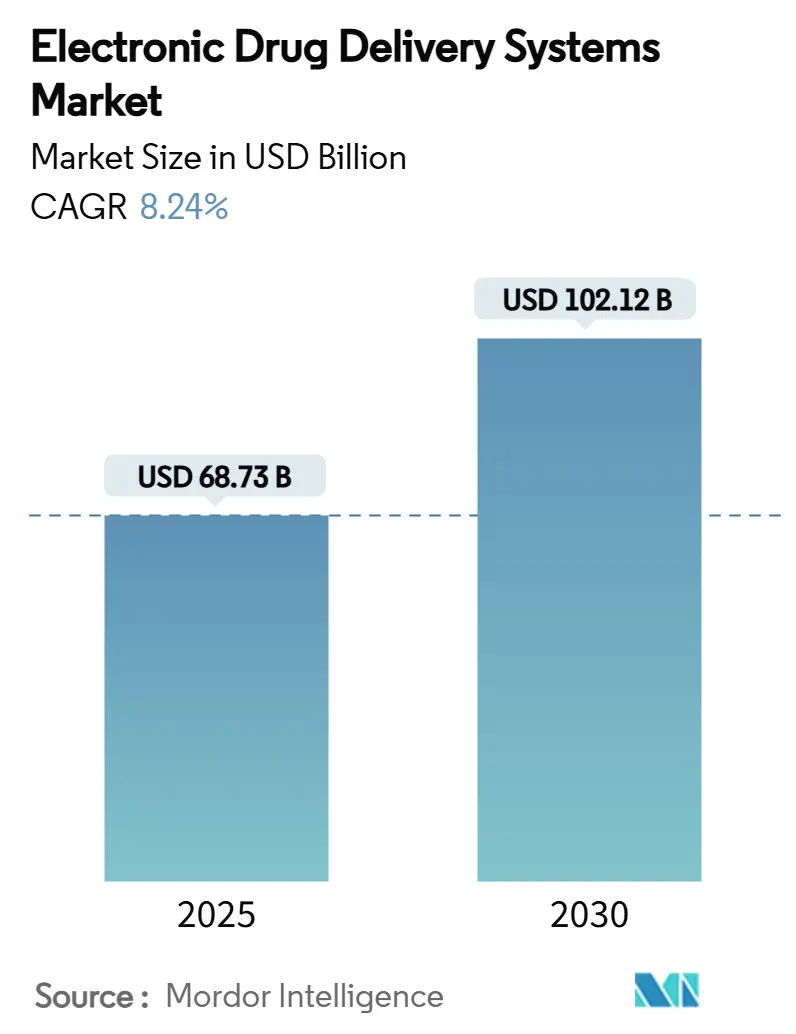

| Market Size (2025) | USD 68.73 Billion |

| Market Size (2030) | USD 102.12 Billion |

| Growth Rate (2025 - 2030) | 8.24% CAGR |

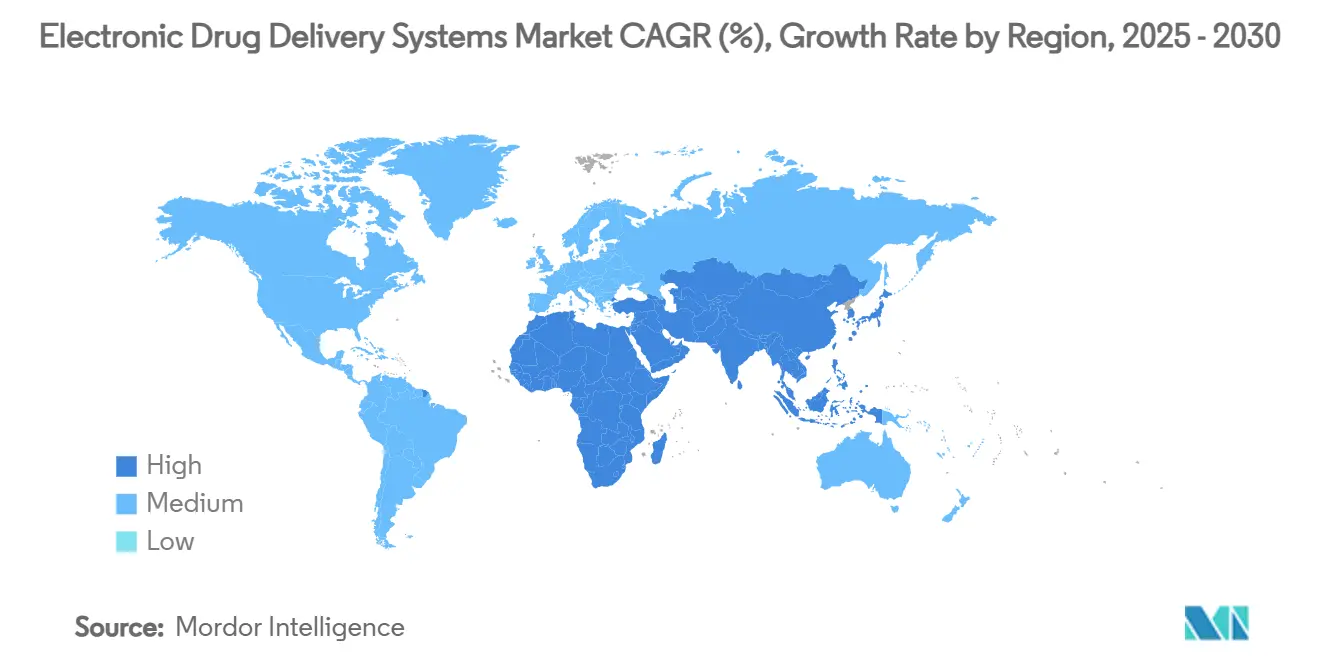

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Drug Delivery Systems Market Analysis by Mordor Intelligence

The electronic drug delivery systems market size stands at USD 68.73 billion in 2025 and is projected to reach USD 102.12 billion by 2030, reflecting an 8.24% CAGR over the forecast period. Growing demand for home-based care, stricter cybersecurity rules for connected devices, and rapid digitalisation of healthcare are combining to create durable tailwinds for revenue expansion. Device makers able to marry robust security with intuitive, app-enabled user interfaces are widening their addressable base as payers increasingly reimburse for technology that demonstrably lowers downstream treatment costs. Meanwhile, energy-harvesting power modules and AI-driven dosing algorithms are propelling a new generation of long-life, self-optimising implants that promise fewer hospital visits and smoother chronic-care pathways. Intensifying recall scrutiny is paradoxically consolidating competitive power around manufacturers that can finance comprehensive quality systems and navigate a complex global regulatory matrix.

Key Report Takeaways

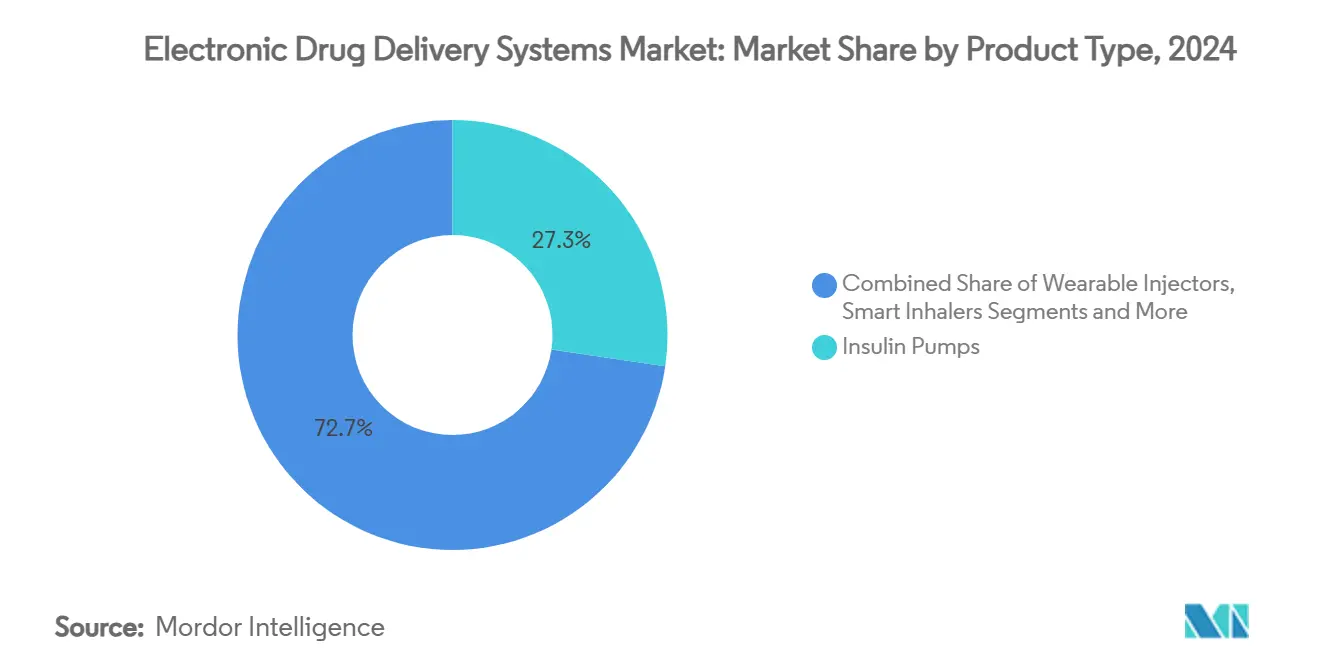

- By product type, insulin pumps accounted for 27.32% of electronic drug delivery systems market share in 2024, while smart inhalers are advancing at a 12.94% CAGR through 2030.

- By application, diabetes held 39.53% of electronic drug delivery systems market size in 2024 and neurological disorders are tracking a 10.34% CAGR to 2030.

- By end user, hospitals and clinics commanded 49.66% of revenue in 2024; home-care settings are pacing at a 12.33% CAGR over the forecast horizon.

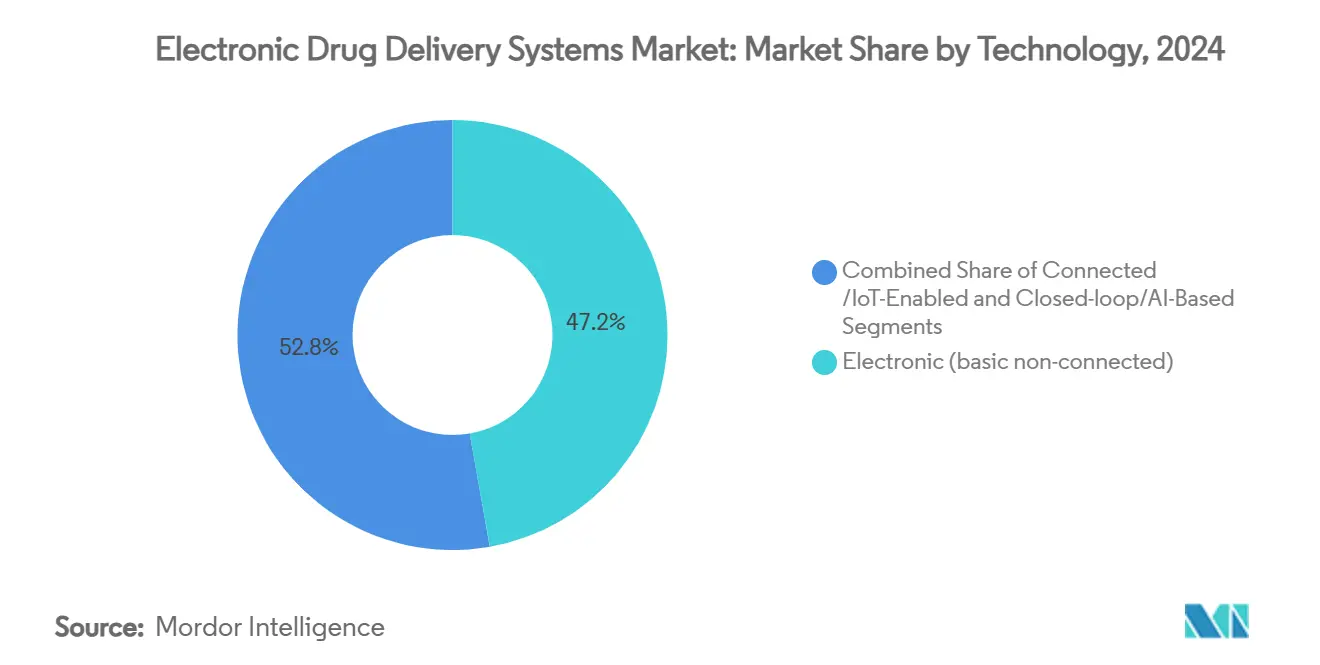

- By technology, electronic platforms led with 47.23% revenue share in 2024 whereas closed-loop and AI-based systems are set to expand at 11.57% CAGR.

- By component, hardware captured 53.63% revenue in 2024; software and algorithms are forecast to rise at a 12.73% CAGR to 2030.

- By geography, North America generated 41.23% of 2024 revenue; Asia-Pacific is positioned for the fastest regional growth at 10.89% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electronic Drug Delivery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes & chronic disease prevalence | +2.1% | Global, strongest in North America & Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of wearable/patch pumps | +1.8% | North America & EU, expanding into Asia-Pacific | Medium term (2-4 years) |

| Favourable reimbursement & home-care push | +1.5% | North America & EU; selective APAC markets | Medium term (2-4 years) |

| Miniaturisation & smart-mobile connectivity | +1.3% | Global technology hubs | Short term (≤ 2 years) |

| Mandatory cybersecurity updates for connected devices | +0.9% | Global, strictest in US & EU | Short term (≤ 2 years) |

| Energy-harvesting micro-batteries enabling long-life implants | +0.8% | Developed markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes & Chronic Disease Prevalence

More than 537 million adults live with diabetes, and the figure is climbing, making continuous, automated insulin delivery an essential therapeutic pillar.[1]Anna Peters, “Automated Insulin Delivery for Young People With Type 1 Diabetes and Elevated A1c,” NEJM Evidence, nejm.org FDA clearance of the MiniMed 780G system for children as young as 7 shows how regulators are smoothing pathways for closed-loop solutions that lighten disease-management burdens. Similar momentum is visible in pain medicine after the FDA green-lit Abbott’s Proclaim spinal cord stimulation platform for diabetic neuropathy, proving electronic delivery can cross therapeutic silos. Ageing populations amplify chronic-care volumes, and real-world data confirm automated delivery systems cut glycated-haemoglobin levels versus manual regimens. Payers increasingly view advanced pumps and sensors as a hedge against expensive, complication-driven admissions, cementing a structural upswing for the electronic drug delivery systems market.

Growing Adoption of Wearable/Patch Pumps

Miniaturised, on-body injectors are reshaping patient expectations by reducing clinic visits and simplifying multi-dose regimens. Enable Injections reported 60% uptake of its enFuse device within four months of launch, underlining how discreet form factors drive stickiness.[2]Jordan Rosenfeld, “On-Body Delivery System enFuse Saves Time, Improves QOL for Patients,” AJMC, ajmc.comPhase 3 data for subcutaneous isatuximab delivered via the same platform met non-inferiority against IV therapy while boosting quality-of-life metrics, signalling oncology’s pivot toward at-home biologic administration. Partnerships such as BD-Ypsomed’s alliance on high-viscosity biologics show incumbent players repositioning around patch technology to defend share. Newly issued FDA draft guidance clarifies performance benchmarks, trimming regulatory ambiguity for innovators. With 82% of US insurers expressing willingness to cover user-friendly wearable pumps, payers are accelerating adoption curves.

Favourable Reimbursement & Home-Care Push

Medicare’s 2025 Home Health update delivers a 2.7% payment bump and adds bundled payments for complex IV therapies, effectively underwriting connected delivery tools in the living room.[3]Centers for Medicare & Medicaid Services, “CY 2025 Home Health PPS Rate Update,” cms.gov The FDA’s digital-health qualification programme gives developers clearer coding routes, further aligning economic and regulatory incentives. Europe mirrors the trend: EMA guidance on drug-device combinations streamlines dossier expectations, lowering market-entry friction. Real-world evidence from Bigfoot Unity shows technology-enabled insulin delivery trims emergency visits and improves glycaemic metrics, reinforcing the value proposition for home-care deployment. Together, policy and data are turning domiciliary treatment from a niche into a mainstream channel for the electronic drug delivery systems market.

Miniaturisation & Smart-Mobile Connectivity

Shrinking components coupled with ubiquitous smartphones are enabling real-time dose titration and integrated decision support. Medtronic’s InPen app syncs with its Simplera continuous glucose monitor, converting a legacy pen into a data-rich therapeutic hub. Twiist’s automated system captures flow data on every micro-dose, demonstrating the granularity achievable with next-generation sensors. Patent disclosures reveal modular wearables housing both monitoring and drug-reservoir compartments, pointing to multipurpose devices that can flex across indications. Material-science advances have yielded flexible, AI-powered implants that adapt therapy to brain-signal patterns, underscoring the convergence of neurotechnology and pharmacology. In short, miniaturisation is turning hardware into software-defined treatment tools, elevating the intelligence layer as a key differentiator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device recalls & safety litigation exposure | -1.4% | Global; most acute in US | Short term (≤ 2 years) |

| High device cost & reimbursement gaps in emerging markets | -1.1% | Emerging economies | Medium term (2-4 years) |

| Complex multi-jurisdiction regulatory pathways | -0.8% | Global | Medium term (2-4 years) |

| Semiconductor supply-chain volatility for MCUs | -0.6% | Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Device Recalls & Safety Litigation Exposure

A spate of Class I insulin and infusion pump recalls during 2023-24 rattled clinician confidence and triggered cost-intensive litigation. Battery life faults, fluid leaks, and occlusions forced large-scale replacements, tightening FDA post-market surveillance and elongating new-product review. Legal settlements inflate insurance premiums and redirect capital away from R&D. Smaller players lacking robust quality systems face existential threats, accelerating market consolidation. Over time, stringent oversight should raise baseline safety, yet near-term drag on the electronic drug delivery systems market persists.

High Device Cost & Reimbursement Gaps In Emerging Markets

Closed-loop insulin systems can cost more than USD 10,000 annually versus under USD 1,000 for conventional therapy, a disparity that caps adoption in price-sensitive nations. While Medicare and many EU payers cover advanced devices, reimbursement in emerging economies remains patchy, leaving patients to shoulder most costs. Drug-device combination products add complexity, requiring hybrid regulatory filings that deter fast-track approvals in resource-constrained jurisdictions. Currency swings and limited technical-support networks further weigh on roll-out prospects. Without innovative financing models, the electronic drug delivery systems industry will struggle to unlock full emerging-market potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accelerating Shift Toward Smart Inhalers

Insulin pumps delivered 27.32% of 2024 revenue, validating decades of clinical proof and insurance coverage. Smart inhalers, however, are expanding at a 12.94% CAGR, propelled by the FDA’s landmark approval of the Airsupra combination therapy that repositions inhaled corticosteroids as rescue medication. This regulatory milestone galvanises R&D investment in sensor-embedded inhalers that track usage and transmit adherence data to care teams. Wearable injectors are also gaining favourable momentum through partnerships targeting high-viscosity biologics, while auto-injectors sustain emergency-medicine relevance. The electronic drug delivery systems market size for smart inhalers is projected to outpace pumps in incremental dollar terms over the forecast window as respiratory care digitalises. Competitive jockeying centres on cloud connectivity, dose-tracking precision, and pay-per-use financing aimed at widening access.

The product landscape is simultaneously diversifying. Smart pills integrate micro-cameras and telemetry to perform targeted GI delivery and diagnostics in a single pass, though uptake hinges on patient acceptance and reimbursement clarity. Implantable infusion pumps benefit from energy-harvested power sources that extend functional life without surgery, promising differentiated value in oncology and pain medicine. Across categories, manufacturers race to blend robust hardware with adaptive software that tailors dosing to shifting physiological cues, redefining performance benchmarks for the electronic drug delivery systems market.

By Application: Neurological Disorders Break Out

Diabetes retained 39.53% of 2024 revenue, supported by integrated CGM-pump ecosystems and strong payer evidence bases. Yet neurological disorders are climbing fastest at a 10.34% CAGR, thanks to closed-loop spinal cord stimulators and AI-modulated pain implants capable of real-time signal interpretation. On-label expansion of Proclaim SCS platforms validates a broader clinical addressable base, triggering fresh R&D in migraine and movement disorders. The electronic drug delivery systems market size for neurological applications is on track to double by 2030 if pipeline devices clear regulatory hurdles.

Respiratory disease applications continue stable growth underpinned by smart inhaler penetration, while oncology is pivoting from IV to on-body subcutaneous delivery, unlocking hospital-capacity savings and improved patient comfort. Cardiovascular programmes are testing ambulatory pumps for heart-failure medication titration, whereas GI and endocrine disorders are early beneficiaries of ingestible sensor therapy. This widening therapeutic canvas compels suppliers to architect modular platforms able to swap drug cassettes and algorithm packages, ensuring lifecycle flexibility.

By End User: Home-Care Outpaces Institutional Settings

Hospitals and clinics still house nearly half of global installations, reflecting their pivotal role in initial therapy titration and acute-care management. Nonetheless, home-care settings are sprinting ahead at 12.33% CAGR as reimbursement, remote-monitoring reliability, and patient preference align. Medicare’s bundled payment for home IVIG and diabetes tech underscores systemic recognition that decentralised care can trim readmissions while enhancing quality of life. The electronic drug delivery systems market share accruing to domiciliary channels is set to rise steadily through 2030.

Ambulatory surgery centres adopt delivery systems for same-day procedures, cushioning throughput pressures on hospitals. Specialty clinics exploit algorithmic dosing to differentiate service lines in oncology and neurology. As device instruction manuals shrink to smartphone tutorials and cloud dashboards flag anomalies in real time, care teams can safely extend sophisticated therapies beyond institutional walls, redrawing healthcare logistics.

By Technology: AI-Driven Platforms Gather Speed

Non-connected electronic devices still generate 47.23% of revenue, yet growth tilts toward connected and AI-centric models advancing at 11.57% CAGR. Clearance of the Beta Bionics iLet ACE pump, which auto-tunes insulin delivery via machine-learning algorithms, evidences regulatory faith in autonomous dosing software. Connected inhalers stream adherence metrics to cloud portals, enabling proactive coaching interventions. For clinicians, integrated data reduces cognitive overload by distilling actionable insights rather than raw numbers.

Hardware miniaturisation makes room for redundant sensors and over-the-air firmware upgrades, ensuring platforms evolve post-sale. Interoperability designations allow third-party innovators to plug specialty modules into baseline pumps, creating an ecosystem-style electronic drug delivery systems market. Cyber-secure APIs are, therefore, as crucial as the cannulas they control.

By Component: Software & Algorithms Lead Value Creation

Hardware remains the revenue anchor at 53.63%, but software and algorithms grow fastest at 12.73% CAGR because they unlock recurring revenue from updates, analytics, and premium decision-support tiers. Medtronic’s enhanced InPen app illustrates how incremental code releases can refresh a mature device franchise without fresh hardware. Connectivity platforms translate raw sensor feeds into longitudinal treatment dashboards, tightening feedback loops between patients and clinicians. The electronic drug delivery systems market size attributable to software is poised for structural uplift as more jurisdictions reimburse for algorithm-enabled outcomes.

Sensor suites gain sophistication through bi-electrode arrays and impedance spectroscopy that detect occlusions or leakage before clinical impact. Meanwhile, oxygen-powered or triboelectric generators shrink power modules, extending device life and reducing service intervals. Consumables ride the installed-base wave, with proprietary cartridges anchoring customer lock-in and driving predictable annuity streams.

Geography Analysis

North America generated 41.23% of 2024 revenue, underpinned by advanced payer systems, proactive FDA guidance, and deep digital-health adoption. Medicare’s latest payment schedule further cements home-based eligibility, solidifying a local demand runway. Tight enforcement of Section 524B also makes the region a bellwether for cybersecurity compliance, indirectly setting design norms for global vendors.

Asia-Pacific is the fastest-growing cluster at 10.89% CAGR. China scales production capacity for smart pumps, while Japan and Australia accelerate approvals for AI-enabled devices under harmonised review frameworks. India’s Ayushman Bharat digital-health backbone positions local providers to leapfrog into cloud-connected care. Regional manufacturers increasingly design for both domestic need and EU/US standards, raising export readiness.

Europe shows steady, regulation-driven expansion. Implementation of Medical Device Regulation has elongated some timelines but ultimately boosts quality perception, aiding adoption of high-viscosity wearable injectors through BD-Ypsomed collaborations. Central- and Eastern-European payers begin pilot reimbursements for automated insulin delivery, widening the addressable cohort. South America, Middle East, and Africa display emerging-market dynamics: an urban elite adopts premium tech, but broader diffusion awaits cost-down models and public-sector reimbursement reform.

Competitive Landscape

Market concentration is moderate. Medtronic, Insulet, and Novo Nordisk continue to anchor the leaderboard with vertically integrated portfolios and extensive KOL networks. However, recalls have spotlighted quality credentials, nudging hospitals to fact-check supplier track records. Enable Injections’ rapid patient uptake demonstrates how nimble specialists can out-innovate giants on user experience in select niches.

Strategic themes converge around AI algorithm differentiation, energy-harvesting power solutions, and service-wrapped device offerings. Patent filings on implantable, oxygen-powered pumps indicate a pivot from product to platform, where consumables, data services, and algorithm upgrades fuel lifetime value. Tech firms offer security-as-a-service layers, letting smaller OEMs outsource compliance. M&A appetite remains healthy as incumbents acquire analytics start-ups to fortify software stacks. Against this backdrop, the electronic drug delivery systems market rewards scale in manufacturing yet prizes agility in code development, creating a two-speed competitive race.

Electronic Drug Delivery Systems Industry Leaders

Insulet Corporation

Medtronic plc

Novo Nordisk A/S

Tandem Diabetes Care

Ypsomed AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Enable Injections reported Phase 3 success for subcutaneous isatuximab via its on-body system, signalling a move into oncology dosing.

- November 2024: Medtronic secured FDA clearance for the InPen smart-pen app, paving the way for its Simplera-linked Smart MDI launch.

- August 2024: FDA broadened Insulet’s SmartAdjust technology to type 2 diabetes adults, marking the first automated insulin-delivery clearance for this population

Global Electronic Drug Delivery Systems Market Report Scope

| Insulin Pumps |

| Wearable Injectors |

| Smart Inhalers |

| Smart Pills |

| Implantable Infusion Pumps |

| Transdermal Patches |

| Auto-Injectors |

| Microneedle Patches |

| Diabetes |

| Respiratory Diseases (Asthma, COPD) |

| Pain Management |

| Oncology |

| Cardiovascular Diseases |

| Neurological Disorders |

| Gastro-intestinal Disorders |

| Hormone Therapy |

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Home-care Settings |

| Specialty Clinics |

| Electronic |

| Connected / IoT-Enabled |

| Closed-loop / AI-Based |

| Hardware |

| Software & Algorithms |

| Connectivity Platform |

| Sensors & Power Modules |

| Consumables / Cartridges |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Insulin Pumps | |

| Wearable Injectors | ||

| Smart Inhalers | ||

| Smart Pills | ||

| Implantable Infusion Pumps | ||

| Transdermal Patches | ||

| Auto-Injectors | ||

| Microneedle Patches | ||

| By Application | Diabetes | |

| Respiratory Diseases (Asthma, COPD) | ||

| Pain Management | ||

| Oncology | ||

| Cardiovascular Diseases | ||

| Neurological Disorders | ||

| Gastro-intestinal Disorders | ||

| Hormone Therapy | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgery Centers | ||

| Home-care Settings | ||

| Specialty Clinics | ||

| By Technology | Electronic | |

| Connected / IoT-Enabled | ||

| Closed-loop / AI-Based | ||

| By Component | Hardware | |

| Software & Algorithms | ||

| Connectivity Platform | ||

| Sensors & Power Modules | ||

| Consumables / Cartridges | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the electronic drug delivery systems market in 2025?

The electronic drug delivery systems market size is USD 68.73 billion in 2025 and is forecast to hit USD 102.12 billion by 2030, growing at an 8.24% CAGR.

Which product category leads revenue today?

Insulin pumps hold the largest share at 27.32% of 2024 revenue, supported by decades of clinical data and robust reimbursement frameworks.

What is the fastest-growing therapeutic application?

Neurological disorders are advancing at a 10.34% CAGR through 2030 on the back of AI-enabled spinal cord stimulation and adaptive pain-management implants.

Why is Asia-Pacific growing faster than other regions?

Rapid digital-health investments, rising chronic-disease prevalence, and increasingly supportive regulatory regimes lift Asia-Pacific revenue at 10.89% CAGR.

How are reimbursement trends shaping the industry outlook?

Medicare’s 2025 payment update and similar EU policies enhance coverage for home-based, connected therapies, bolstering demand for advanced delivery platforms.

Page last updated on: