Animal Drug Compounding Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

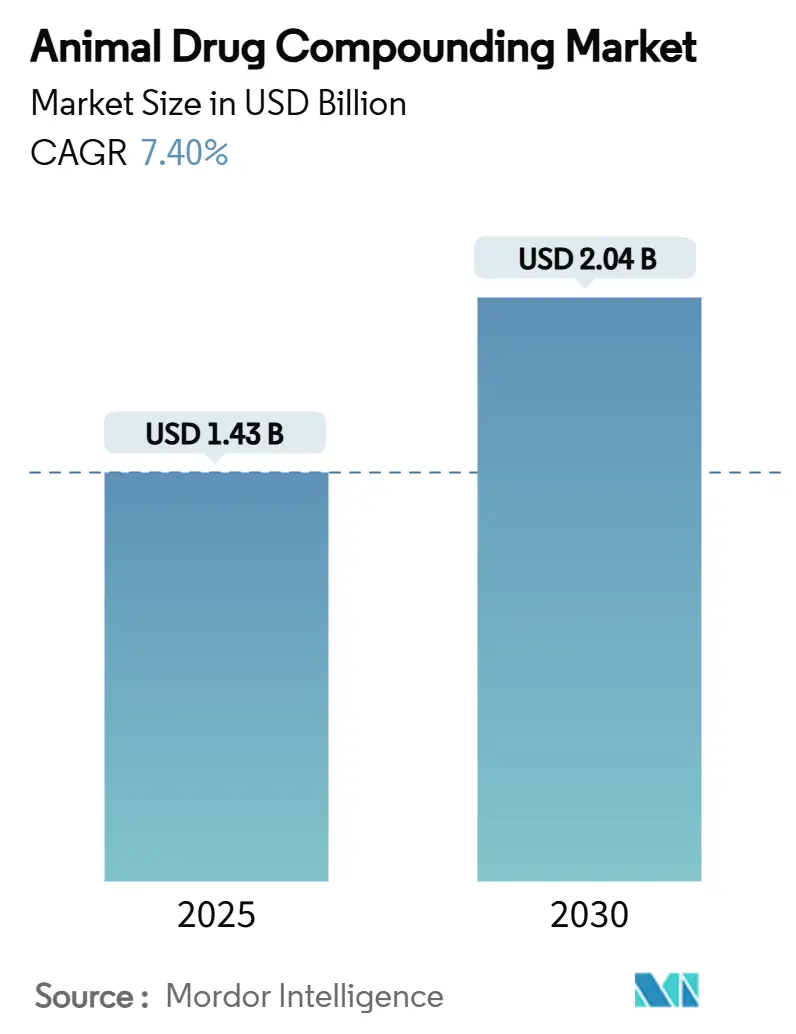

| Market Size (2025) | USD 1.43 Billion |

| Market Size (2030) | USD 2.04 Billion |

| Growth Rate (2025 - 2030) | 7.40% CAGR |

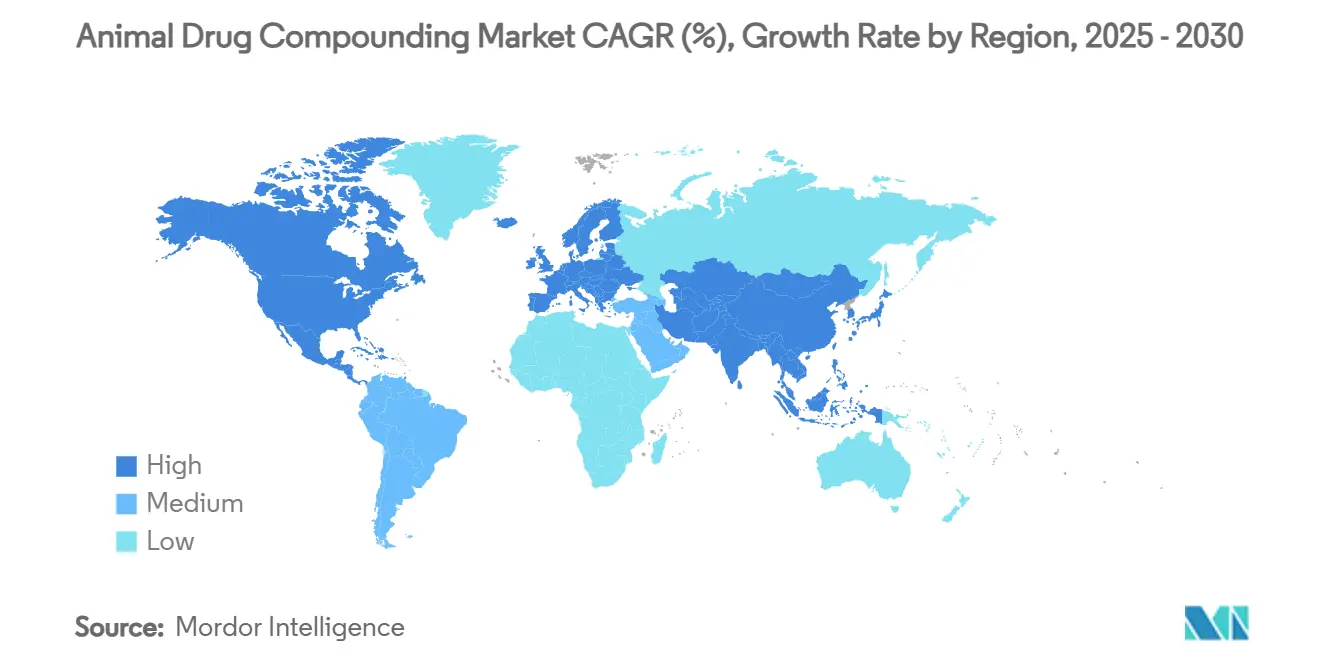

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Drug Compounding Market Analysis by Mordor Intelligence

The animal drug compounding market size stands at USD 1.43 billion in 2025 and is projected to reach USD 2.04 billion by 2030, reflecting a 7.40% CAGR across the forecast period. The upward trajectory is supported by an expanding pool of personalized pet therapies, the commercial success of cannabinoid-based formulations, and the continued registration of 503B outsourcing facilities that apply current Good Manufacturing Practices. Critical drug shortages documented by the FDA are encouraging veterinarians to shift toward compounded substitutes, while AI-guided formulation platforms shorten development timelines and improve dose precision. Regulatory headwinds, notably the enforcement of Guidance for Industry #256, raise compliance costs but also favor larger, automation-enabled players. Meanwhile, tariff-driven raw-material inflation and limited reimbursement coverage temper demand elasticity, prompting pharmacies to emphasize value-added services and exotic-species expertise.

Key Report Takeaways

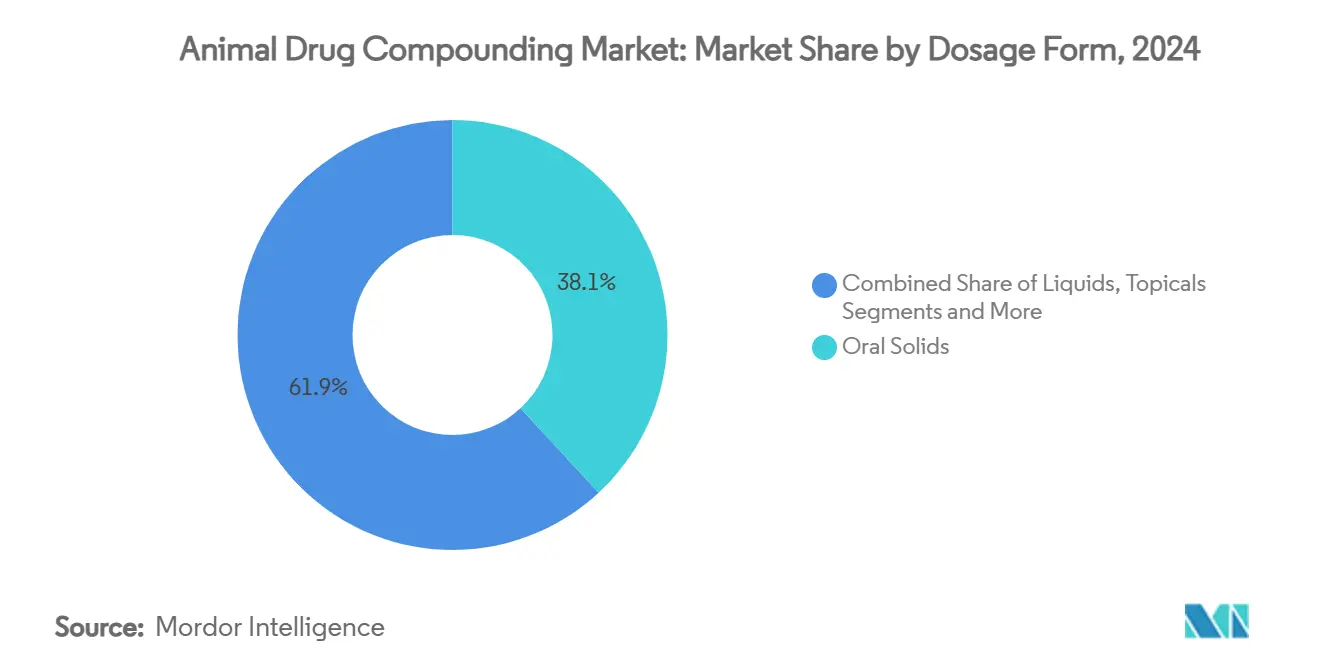

- By dosage form, oral solids accounted for 38.1% of the animal drug compounding market share in 2024; sterile injectables are forecast to expand at a 9.8% CAGR through 2030.

- By animal type, companion animals led with 67.3% revenue share in 2024; exotic and zoo species are projected to advance at a 12.4% CAGR to 2030.

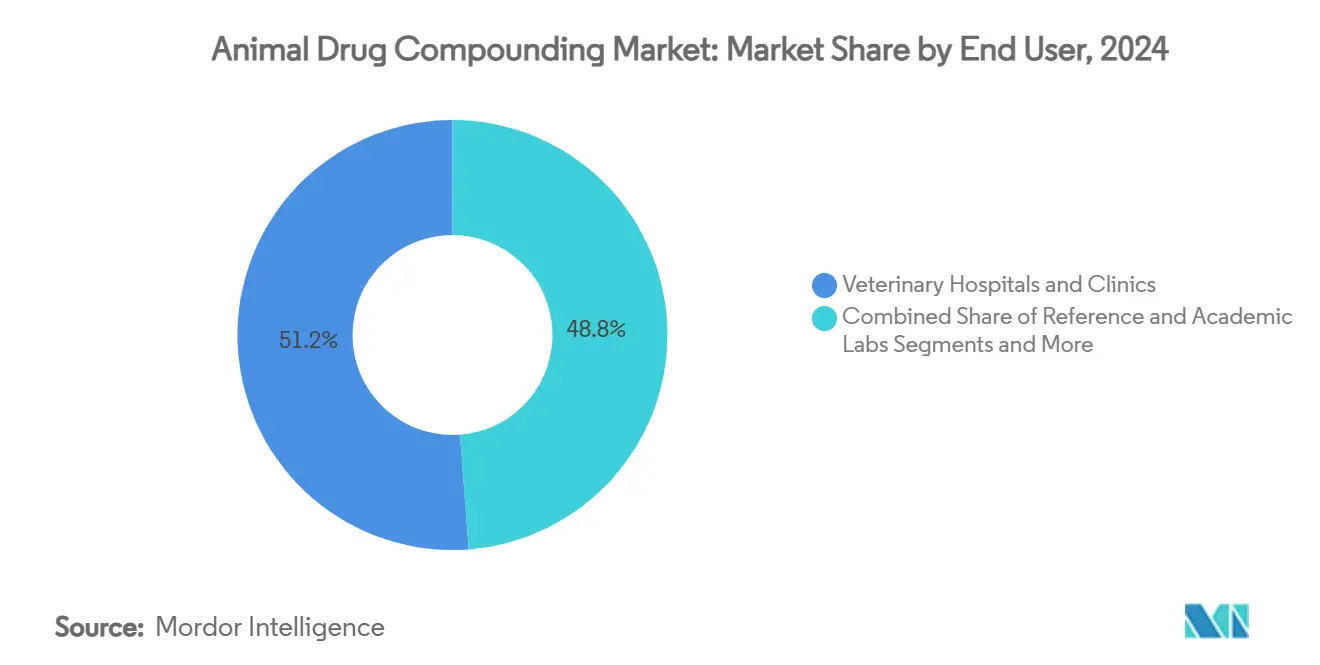

- By end user, veterinary hospitals and clinics held 51.2% of the animal drug compounding market share in 2024, while 503B outsourcing facilities are set to grow at 10.6% CAGR through 2030.

- By compounding type, non-sterile preparations commanded 59.5% share of the animal drug compounding market size in 2024; hazardous-drug compounding under USP 800 guidelines is progressing at an 11.7% CAGR over the same horizon.

- By therapeutic area, pain and inflammation treatments captured 33.4% of the animal drug compounding market size in 2024; cannabinoid-based therapies are expected to surge at a 15.2% CAGR to 2030.

- By geography, North America contributed 49.1% revenue share in 2024, whereas Asia Pacific is poised to register the quickest regional CAGR at 7.6% through 2030.

Global Animal Drug Compounding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference For Personalized Pet Therapies | +1.20% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Escalating FDA Drug-Shortage Lists Prompting Veterinary Compounding | +1.80% | North America, spillover to Canada | Short term (≤ 2 years) |

| Expansion Of 503B Outsourcing Facilities With GMP Automation | +1.10% | North America & EU regulatory zones | Medium term (2-4 years) |

| Surge In Equine Sports Medicine Requiring Specialty Formulations | +0.70% | Global, concentrated in racing jurisdictions | Long term (≥ 4 years) |

| Rapid Uptake Of Cannabinoid-Based Animal Therapeutics | +1.40% | North America, selective EU markets | Short term (≤ 2 years) |

| AI-Guided Dose-Form Customization Cutting Formulation Cycle-Time | +0.60% | APAC core, spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Personalized Pet Therapies

Individualized treatments are rising as pet owners expect the same precision medicine offered in human healthcare, prompting veterinarians to tailor dosage forms to species-specific pharmacokinetics.[1]American Veterinary Medical Association, “Compounding from Bulk Drug Substances,” avma.org Weight-based adjustments, palatability enhancements, and compliance-oriented delivery routes support premium price realization and reinforce pharmacy-veterinarian relationships. Companion-animal lifespans lengthen, increasing chronic disease prevalence and the need for long-term, customized regimens. Exotic-species growth amplifies demand for unique strengths, as commercial drugs rarely list validated dosing for reptiles, birds, or small mammals. Pharmacies able to replicate hospital formularies with rapid turnaround times gain sustained competitive differentiation through service intimacy and therapeutic diversity.

Escalating FDA Drug-Shortage Lists Prompting Veterinary Compounding

FDA shortage notifications rose sharply in 2024, affecting critical injectables and interrupting care protocols for both companion and food-producing animals.[2]Food and Drug Administration, “Agency Information Collection Activities,” federalregister.gov 503A pharmacies and 503B facilities exploit the disruption by mobilizing bulk drug substances under medical-need exemptions, though the documentation burden has intensified. Veterinarians rely on compounding partners for uninterrupted supply, especially when withdrawal periods restrict substitutes in livestock. Shortages have also accelerated facility registrations under section 503B because these entities can build inventory in anticipation of demand. The short-term boost to revenues is tempered by closer FDA surveillance that scrutinizes deviation from approved pathways, pressing operators to strengthen quality-management systems.

Expansion of 503B Outsourcing Facilities with GMP Automation

503B outsourcing facilities deploy robotic sterile platforms and closed-loop workflow management to achieve lot-level consistency that rivals industrial pharmaceutical lines.[3]United States Pharmacopeia, “USP Compounding Standards,” usp.org Automation cuts human error during aseptic transfers, raises output, and enables national distribution without patient-specific prescriptions. Veterinary hospitals prefer 503B partners for predictable availability of high-demand injectables, thereby simplifying procurement and reducing staff compounding load. Start-up costs remain high because USP 797 and 800 suites require segregated air handling, redundant monitoring, and rigorous validation. Consequently, economies of scale favor multi-site operators that can amortize compliance investments, driving gradual consolidation within the animal drug compounding market.

Rapid Uptake of Cannabinoid-Based Animal Therapeutics

Cannabinoid-derived treatments for pain, anxiety, and epilepsy gained acceptance despite a lack of FDA-approved veterinary labels, reflecting consumer preference for plant-based interventions. Sales momentum follows legislation that legalized hemp extracts, even though uniform dosing guidance remains absent. Compounding pharmacies address variability by standardizing CBD purity and formulating strengths aligned with emerging clinical literature. Veterinarians in states with permissive rules prescribe CBD faster, but they still navigate liability concerns and recommend only laboratory-verified preparations. The capability to incorporate microencapsulated cannabinoids into treats and transdermal formats broadens the therapeutic toolkit while creating product lines with significant margin potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter FDA GFI-256 Enforcement On Bulk Drug Substances | -1.90% | North America, regulatory spillover globally | Short term (≤ 2 years) |

| Limited Reimbursement & High Out-Of-Pocket Pet Spend | -1.30% | Global, acute in developed markets | Medium term (2-4 years) |

| Scarcity Of Stability Data For Exotic-Species Formulations | -0.80% | Global, concentrated in specialty practices | Long term (≥ 4 years) |

| Rising Raw-Material Costs For Pharmaceutical-Grade APIs | -1.10% | Global, supply chain dependent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter FDA GFI-256 Enforcement on Bulk Drug Substances

Guidance #256 mandates medical justification and record retention whenever veterinarians prescribe compounded drugs from bulk substances, adding administrative weight and potential civil penalties. The agency estimates more than 8 million annual form submissions, consuming thousands of practitioner hours. Small 503A pharmacies feel disproportionate pressure because compliance systems divert limited staff from revenue-generating tasks. Some facilities restrict bulk compounding to avoid scrutiny, narrowing therapeutic options for complex cases. The rule unintentionally shifts demand toward 503B manufacturers, which follow separate pathways but still face higher validation costs, eventually feeding through to customer pricing.

Limited Reimbursement and High Out-of-Pocket Pet Spend

Most insurance policies categorically exclude compounded preparations, leaving pet owners responsible for the entire invoice regardless of medical necessity. Chronic diseases such as endocrine disorders may require monthly refills exceeding USD 100, prompting some clients to downgrade therapeutic plans or discontinue treatment. Insurers cite opaque pricing and variable quality among pharmacies as reasons for exclusion. Although specialized riders are emerging, penetration remains narrow relative to the broader premium pet-insurance market. Demand, therefore, tracks discretionary income trends, exposing the animal drug compounding market to macroeconomic cycles and inflationary pressures on household budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Injectable Innovation Gains Traction

The injectable segment recorded the quickest advance at 9.8% CAGR between 2025 and 2030, fueled by demand for sterile, precise dosing in critical-care and equine applications. Long-acting depot formulations lessen administration frequency and heighten adherence, especially for skittish animals. Oral solids retained the largest 38.1% revenue slice in 2024, owing to formulation simplicity, extended stability, and pet owner familiarity. Topical and transdermal dosage forms benefit dermatology and chronic-pain cases where systemic exposure is undesirable. Ophthalmic preparations leverage advanced viscosity modifiers to prolong corneal contact time, while single-dose otic suspensions like FDA-approved Otiserene reduce in-clinic procedures.

Product-development pipelines increasingly favor aseptic fill-finish technologies that satisfy USP 797 and 800 mandates. Automated barrier isolators trim labor requirements and secure particulate control. The animal drug compounding market size for injectables is projected to reach USD 640 million by 2030, expanding its contribution to overall revenues even as oral forms maintain volume leadership. Compounding pharmacies that offer integrated microbiology testing and real-time environmental monitoring attract referral channels from tertiary veterinary centers focused on oncology and intensive care.

By Animal Type: Exotic-Species Momentum Accelerates

Exotic and zoo species therapy outpaced all other segments with a 12.4% CAGR, supported by rising ownership of reptiles, birds, and small mammals as well as heavier investment in wildlife rehabilitation. In contrast, companion animals continued to dominate value, supplying 67.3% of 2024 revenue. Compounded therapies fill pharmacological gaps for non-traditional pets because few approved drugs offer species-specific labeling. The animal drug compounding market size for exotic species is forecast to double by 2030 as zoological institutions adopt preventive care protocols and apply individualized dosing models for nutrition-related disorders.

Livestock remains a niche because food-animal rules around residues limit extra-label usage. Nonetheless, bovine mastitis outbreaks occasionally trigger compounded intramammary infusions during commercial shortages. Equine sports medicine drives high-unit-value prescriptions, including buffered omeprazole injections that meet stringent withdrawal periods ahead of competitive events. Pharmacies with exotic-species specialization record lower churn because alternative supply channels are scarce, cementing long-term veterinarian alliances and reinforcing market resilience.

By End User: 503B Facilities Capture Share

Veterinary hospitals and clinics generated 51.2% of the 2024 demand, but 503B outsourcing facilities posted the steepest 10.6% CAGR by capitalizing on industrialized GMP processes. Hospitals leverage 503B inventory for perioperative injectables and specialty analgesics, circumventing delays inherent in patient-specific compounding. Telehealth platforms and integrated pharmacy software further streamline order cycles, reinforcing the convenience narrative. The animal drug compounding market share commanded by 503B entities is projected to climb to 24% by 2030 as additional facilities clear FDA inspection backlogs.

E-commerce channels gain incremental traction with direct-to-consumer refills, though regulatory vet-client-patient relationships impose guardrails. Academic laboratories consume limited volumes for preclinical research, showing flat growth. Overall, multi-site practice groups sign national agreements with select compounding partners to standardize formularies, encouraging market consolidation and reinforcing stringent quality expectations across regional networks.

By Compounding Type: Hazardous-Drug Protocols Underpin Growth

Non-sterile preparations controlled 59.5% of revenue in 2024, but hazardous-drug compounding exhibited an 11.7% CAGR as USP 800 enforcement heightened practitioner safety awareness. Oncology-focused clinics mandate negative-pressure rooms, closed-system transfer devices, and technician certification, setting high entry hurdles. Pharmacies that obtained NIOSH-compliant infrastructure reported improved referrals for long-term chemotherapy regimens.

Flavor-enhanced preparations experienced stable mid-single-digit expansion as compliance initiatives focus on palatability. Controlled substances face DEA scrutiny, necessitating biometric vault access and perpetual inventory logs. Facilities that combine sterile and hazardous capabilities under one roof shorten procurement cycles for specialty clinics that require both chemotherapeutic injectables and supportive oral medications, reinforcing vendor lock-in.

By Therapeutic Area: Cannabinoid Therapies Surge

Pain and inflammation maintained the most prominent 33.4% revenue position in 2024 because osteoarthritis remains prevalent in aging dogs and cats. Nonetheless, cannabinoid-based therapies are expanding at a 15.2% CAGR as owners favor natural analgesic alternatives. Anxiety management in felines and canines underpins a secondary wave of growth, while epilepsy protocols exploit synergistic effects with conventional anticonvulsants. The animal drug compounding market size for cannabinoid therapies is expected to approach USD 210 million by 2030, still modest but highly profitable, owing to premium raw-material sourcing.

Anti-infective demand oscillates with commercial availability, spiking during shortages of injectable antibiotics. Endocrinology prescriptions for trilostane and desoxycorticosterone pivot on precise titration that only custom compounding can provide. Dermatology applications capitalize on the rising atopic dermatitis diagnoses, leveraging topical cyclosporine and tacrolimus. Finally, neurology and behavior therapies reflect growing recognition of cognitive dysfunction syndromes, increasing the call for compounded selegiline and melatonin.

Geography Analysis

North America generated 49.1% of global revenue in 2024, anchored by robust regulatory frameworks and advanced veterinary infrastructure. Tariff-related raw-material costs climbed from 2.5% to 27%, challenging gross margins yet spurring price-pass-through strategies. Veterinary corporations leverage economies of scale to negotiate ingredient contracts, cushioning inflation impacts. The United States continues to pilot AI-guided compounding tools, with roughly 30% of clinics deploying machine-learning models for dosage design. Canada follows similar trends but benefits from provincial subsidies that offset exotic-species rehabilitation expenses, lifting demand for specialized compounding.

Europe presents balanced growth under Regulation (EU) 2019/6, which aims to broaden veterinary medicine accessibility without sacrificing antimicrobial stewardship. Equine sports medicine thrives in racing hubs such as France, Ireland, and the United Kingdom, where stringent anti-doping oversight fuels precision compounding. The European Medicines Agency’s essential substance list for equines sets explicit withdrawal periods, enabling pharmacies to develop compliant formulations. Brexit temporarily disrupted cross-channel distribution but also galvanized local compounding facilities to plug supply gaps.

Asia Pacific represents the fastest-growing region at 7.6% CAGR, buoyed by rising disposable income and urban pet adoption. Japan integrates pharmacists into veterinary workflows, improving medication counselling and safety checks. Australia sees practice consolidators like VetPartners expanding to 267 clinics, creating national platforms for compounding partnerships. Regulatory fragmentation across Southeast Asia remains a hurdle, yet harmonization efforts under ASEAN standard technical requirements show progress, suggesting incremental market openness for cross-border distributors.

Competitive Landscape

The animal drug compounding market retains moderate fragmentation as regional pharmacies coexist with scaling 503B manufacturers and corporate veterinary groups. Grey Wolf Animal Health executed two notable deals in 2024–2025, paying USD 22.5 million for The Compounding Pharmacy of Manitoba and later acquiring Trutina Pharmacy to bolster equine formulations. Mission Veterinary Partners and Southern Veterinary Partners announced a merger that will yield 730 practices pending regulatory approval, potentially channelling prescription volume toward preferred compounding vendors.

503B facilities differentiate through GMP audits and robotic sterile lines such as the Automated Pharmacy Admixture System, patented under US 7930066 B2. Smaller 503A pharmacies compete on bespoke services, rapid turnaround, and exotic-species know-how. Private equity interest intensifies because automation drives margin scalability, exemplified by EQT’s purchase of VetPartners, which unlocks downstream compounding synergies across Australia and New Zealand. Technology collaborations surface between software vendors and pharmacies to integrate e-prescribing with inventory analytics, tightening fulfilment cycles and lowering stockouts.

Competitive dynamics revolve around quality accreditation, with PCAB and NABP inspections serving as trust signals. Pharmacies investing in environmental monitoring, particle counters, and ISO-classified cleanrooms secure referral pipelines from specialty hospitals. Conversely, rising compliance expenses accelerate exit decisions among sole proprietors, creating roll-up opportunities. Intellectual-property portfolios remain limited; however, select entities file formulation patents—such as Epicur Pharma’s injectable omeprazole for equines—that confer temporary exclusivity and premium pricing power.

Animal Drug Compounding Industry Leaders

Wedgewood Pharmacy

Covetrus

Epicur Pharma

Fagron NV

Mixlab

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Grey Wolf Animal Health Corp acquired Trutina Pharmacy, expanding equine-focused compounding capacity in Canada.

- May 2025: Dechra obtained FDA clearance for Otiserene, the first single-dose, long-acting marbofloxacin-terbinafine-dexamethasone otic suspension for dogs.

- February 2025: Epicur Pharma and Bova collaborated to introduce a patented injectable omeprazole for equine gastric ulcers in the United States.

- December 2024: Grey Wolf Animal Health Corp purchased The Compounding Pharmacy of Manitoba for USD 22.5 million.

Global Animal Drug Compounding Market Report Scope

| Oral Solids |

| Oral Liquids |

| Topicals & Transdermals |

| Ophthalmic & Otic |

| Sterile Injectables |

| Companion Animals |

| Livestock |

| Equine |

| Exotic & Zoo Species |

| Wildlife & Rehabilitation |

| Veterinary Hospitals & Clinics |

| Reference & Academic Labs |

| 503A Community Pharmacies |

| 503B Outsourcing Facilities |

| E-commerce & Mail-order Platforms |

| Sterile |

| Non-sterile |

| Hazardous (USP-800) |

| Controlled-substance |

| Flavor-enhanced |

| Pain & Inflammation |

| Anti-infectives |

| Endocrinology & Hormone |

| Dermatology |

| Neurology & Behavior |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Oral Solids | |

| Oral Liquids | ||

| Topicals & Transdermals | ||

| Ophthalmic & Otic | ||

| Sterile Injectables | ||

| By Animal Type | Companion Animals | |

| Livestock | ||

| Equine | ||

| Exotic & Zoo Species | ||

| Wildlife & Rehabilitation | ||

| By End User | Veterinary Hospitals & Clinics | |

| Reference & Academic Labs | ||

| 503A Community Pharmacies | ||

| 503B Outsourcing Facilities | ||

| E-commerce & Mail-order Platforms | ||

| By Compounding Type | Sterile | |

| Non-sterile | ||

| Hazardous (USP-800) | ||

| Controlled-substance | ||

| Flavor-enhanced | ||

| By Therapeutic Area | Pain & Inflammation | |

| Anti-infectives | ||

| Endocrinology & Hormone | ||

| Dermatology | ||

| Neurology & Behavior | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the animal drug compounding market?

The market is valued at USD 1.43 billion in 2025 and is projected to grow to USD 2.04 billion by 2030.

Which dosage form is expanding fastest in the animal drug compounding market?

Sterile injectables record the quickest growth at a 9.8% CAGR through 2030, driven by demand for precise dosing in critical-care settings.

Why are 503B outsourcing facilities gaining traction?

503B facilities operate under GMP conditions, maintain on-hand inventory, and can ship nationwide without individual prescriptions, supporting a 10.6% CAGR.

How significant are cannabinoid therapies in this market?

Cannabinoid-based compounded products are advancing at 15.2% CAGR, reflecting strong pet-owner demand for natural pain and anxiety relief.

Which region leads the market and which is growing fastest?

North America accounts for 49.1% of global revenue, while Asia Pacific is the fastest-growing region at 7.6% CAGR.

What are the main regulatory challenges facing compounding pharmacies?

Key challenges include FDA enforcement of Guidance #256, higher documentation burdens, and USP 800 compliance for hazardous-drug handling.

Page last updated on: