Smart Pills Drug Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

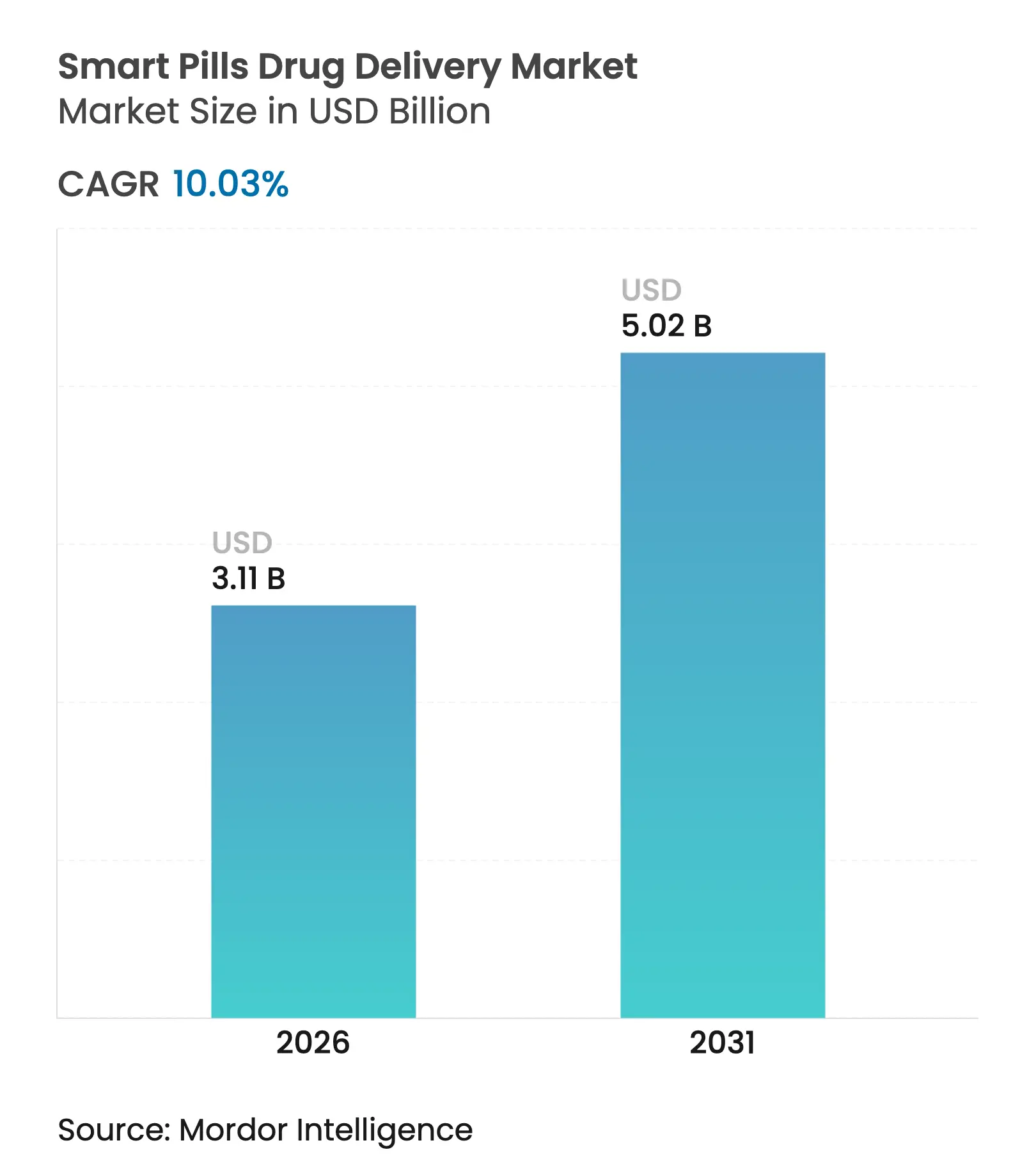

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 10.03 % CAGR |

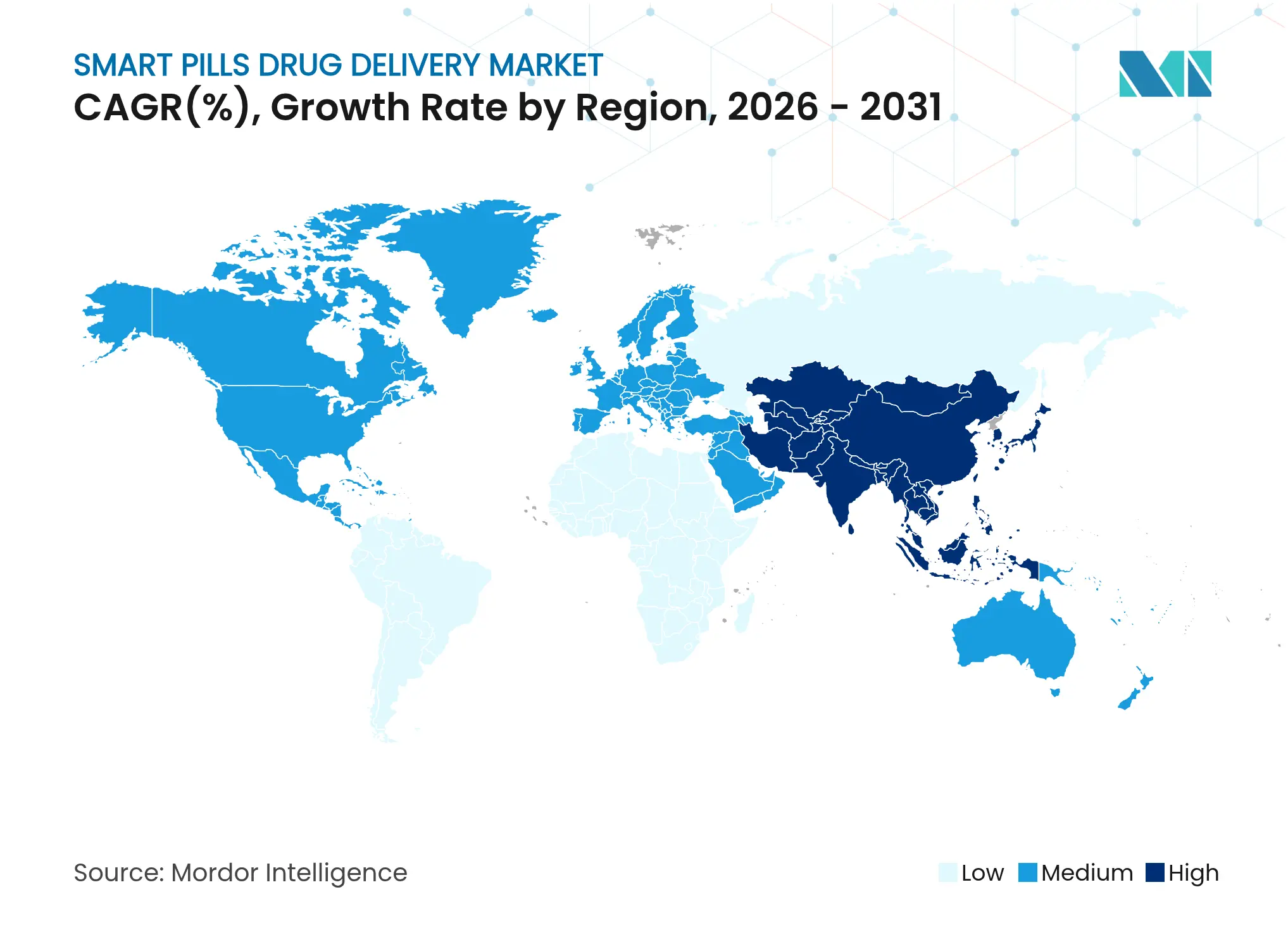

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Smart Pills Drug Delivery Market Analysis by Mordor Intelligence

The smart pills drug delivery market size was valued at USD 2.83 billion in 2025 and estimated to grow from USD 3.11 billion in 2026 to reach USD 5.02 billion by 2031, at a CAGR of 10.03% during the forecast period (2026-2031). Growing integration of miniaturized electronics, ingestible sensors, and AI analytics positions ingestible devices as a core pillar of precision medicine. Recent FDA cybersecurity guidance and the Transitional Coverage for Emerging Technologies pathway address earlier regulatory and reimbursement barriers, clearing the way for faster commercialization. Capsule endoscopy retains a strong installed base, yet drug-delivery capsules show the highest momentum as therapeutic use cases expand. Asia-Pacific’s double-digit growth rate underscores rising healthcare investment, while North America benefits from early adopter health systems and robust venture funding. Competitive intensity is increasing as large device makers add smart pill portfolios and specialized start-ups drive niche innovations.

Key Report Takeaways

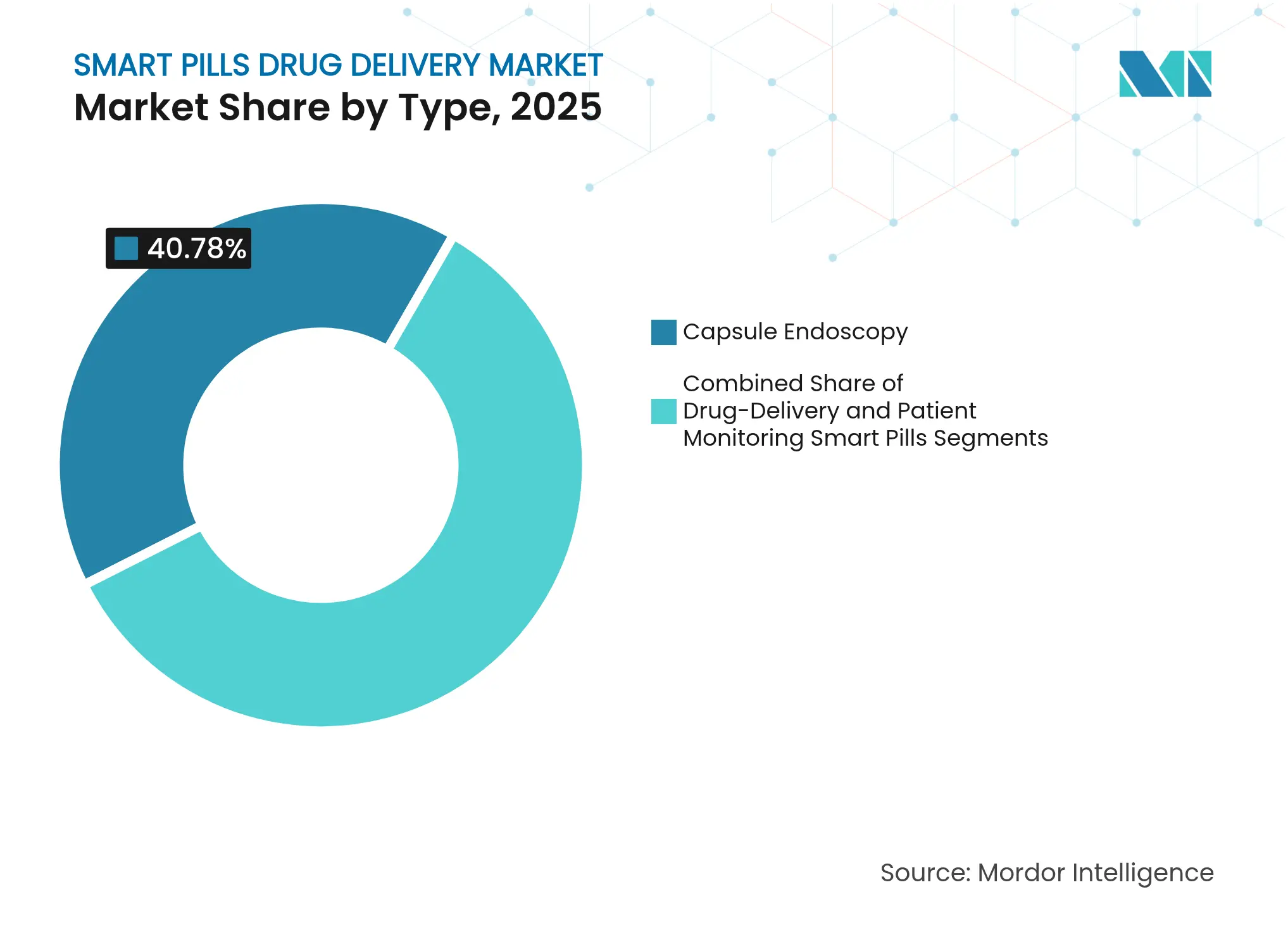

- By type, capsule endoscopy led with 40.78% revenue share in 2025; drug-delivery capsules are forecast to expand at a 14.12% CAGR to 2031.

- By component, ingestible sensors held 51.76% of the smart pills drug delivery market share in 2025, while software and analytics platforms are advancing at a 14.45% CAGR through 2031.

- By application, diagnostic imaging accounted for a 46.92% share of the smart pills drug delivery market size in 2025; targeted drug delivery is rising at a 13.18% CAGR.

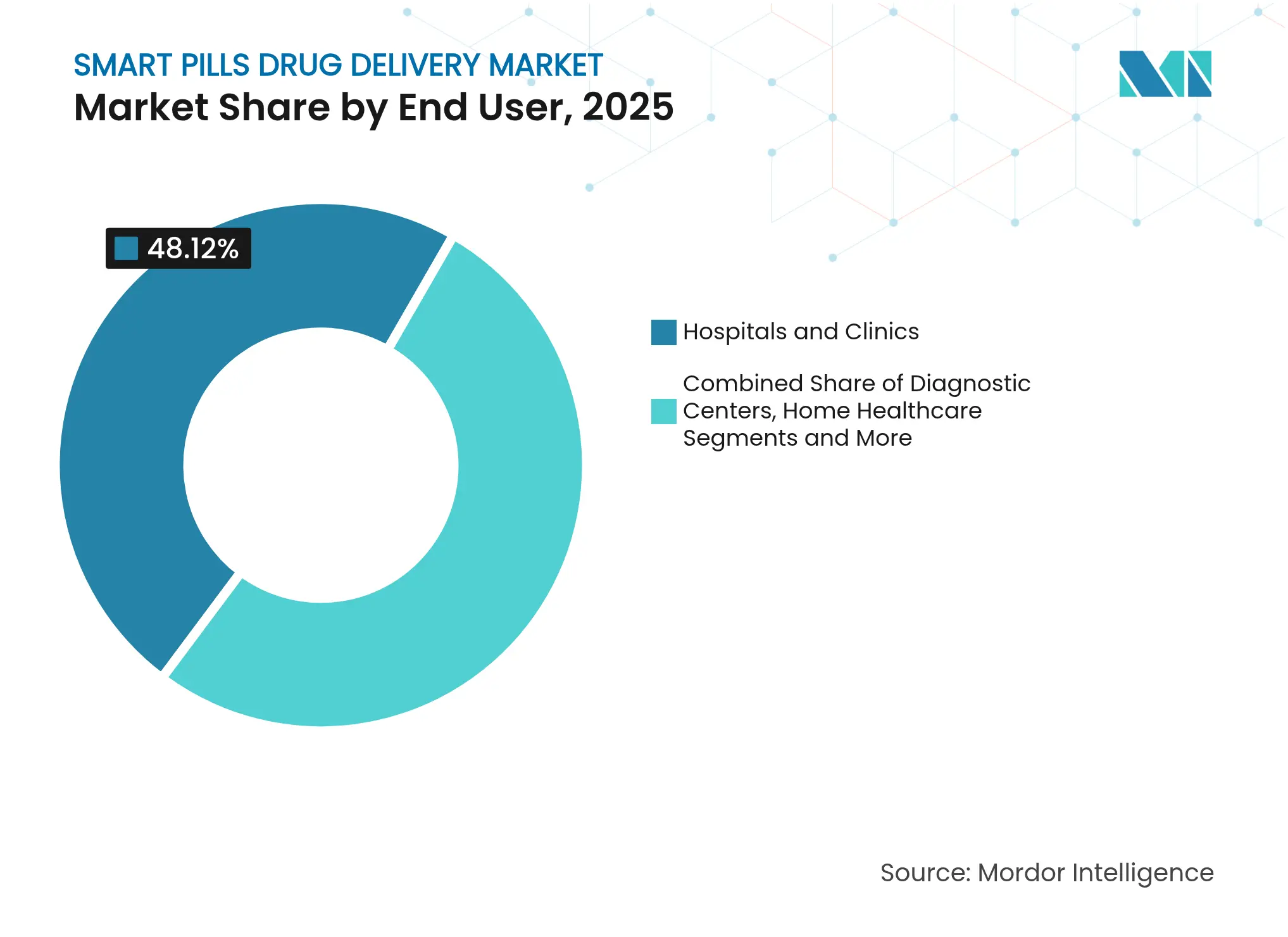

- By end user, hospitals and clinics controlled 48.12% of revenue in 2025; home healthcare is growing fastest at a 13.22% CAGR.

- By geography, North America commanded 44.01% market share in 2025; Asia-Pacific is registering a 12.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Pills Drug Delivery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid adoption of capsule endoscopy

for GI diagnostics

Rapid adoption of capsule endoscopy

for GI diagnostics

| +2.1% | Global; strongest in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

Global; strongest in North America

& Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Preference for minimally invasive

patient monitoring

Preference for minimally invasive

patient monitoring

| +1.8% | Global | Long term (≥ 4 years) | |||

Growing chronic-disease burden and

poly-pharmacy

Growing chronic-disease burden and

poly-pharmacy

| +1.6% | Global; aging populations | Long term (≥ 4 years) | |||

Integration with telehealth and

remote adherence platforms

Integration with telehealth and

remote adherence platforms

| +1.4% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Venture-capital shift toward

ingestible bio-electronics

Venture-capital shift toward

ingestible bio-electronics

| +1.2% | North America & EU | Short term (≤ 2 years) | |||

Defense and space-medicine funding

for “inside-out” vitals sensing

Defense and space-medicine funding

for “inside-out” vitals sensing

| +0.9% | North America, spill-over worldwide | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid Adoption of Capsule Endoscopy for GI Diagnostics

Capsule endoscopy has matched traditional colonoscopy in polyp detection, reaching pooled detection rates of 0.61 in 2024 clinical trials. Patient acceptance is higher because the procedure eliminates sedation and hospital stays. AI-driven lesion recognition and magnetic steering now enable precise localization, opening a path to targeted therapy delivery. Research prototypes featuring robotic functions already combine imaging with site-specific drug release.[1]Qing Cao et al., “Robotic Wireless Capsule Endoscopy: Recent Advances and Upcoming Technologies,” Nature Communications, nature.com This progression from passive imaging to autonomous intervention keeps capsule endoscopy at the center of smart pills drug delivery market innovation.

Preference for Minimally Invasive Patient Monitoring

Consumers increasingly favor noninvasive monitoring, driving uptake of ingestible sensors that map gut gases in three dimensions and flag disease biomarkers in real time.[2]Angsagan Abdigazy et al., “3D Gas Mapping in the Gut with AI-Enabled Ingestible and Wearable Electronics,” Cell Reports Physical Science, cell.com USC engineers recently demonstrated GPS-like smart pills that pair optical gas sensing with wearable magnetic coils for sub-millimeter localization. Cloud-based AI transforms raw signals into actionable alerts, widening clinical acceptance while preparing the smart pills drug delivery market for at-home deployment.

Growing Chronic-Disease Burden & Poly-Pharmacy

Medication nonadherence costs the United States USD 300 billion annually. Digital medicine studies reported 75.9% median verified ingestion among patients with serious mental illness. Timed-release capsules that deliver multiple color-coded doses now progress toward commercialization following FDA clearance of component materials. As health systems confront escalating chronic-disease incidence, smart pills provide a toolset to optimize adherence and fine-tune dosing.

Integration With Telehealth & Remote Adherence Platforms

Connected-health frameworks integrate ingestible sensors with edge devices, allowing clinicians to monitor patients continuously without in-person visits.[3]Adriana Alexandru, “Enhancing Connected Health Ecosystems Through IoT-Enabled Monitoring Technologies: A Case Study of the Monit4Healthy System,” Sensors, mdpi.com Remote patient-monitoring pilots use blockchain for secure data sharing and AI to flag early deterioration. These capabilities bolster the smart pills drug delivery market by turning episodic care into longitudinal insight.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent FDA & EMA device–drug

combination approval path

Stringent FDA & EMA device–drug

combination approval path

| -1.4% | Global; heavier in North America & EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

Global; heavier in North America

& EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Adverse events: capsule retention

& GI obstruction

Adverse events: capsule retention

& GI obstruction

| -1.1% | Global | Long term (≥ 4 years) | |||

Cybersecurity risks of

sensor-to-cloud data flow

Cybersecurity risks of

sensor-to-cloud data flow

| -0.9% | Global; regulated sectors | Short term (≤ 2 years) | |||

Reimbursement gaps for digital

ingestion event markers

Reimbursement gaps for digital

ingestion event markers

| -0.8% | North America & EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent FDA & EMA Device–Drug Combination Approval Path

Smart pills often fall under Class III review, demanding lengthy clinical trials and extensive cybersecurity documentation. The FDA now also requires predetermined change-control plans for AI functions. Navigating parallel EMA rules increases costs and can delay multi-region rollouts, tempering the smart pills drug delivery market growth trajectory.

Cyber-Security Risks of Sensor-to-Cloud Data Flow

Interconnected capsules, wearables, apps, and clouds form large attack surfaces. FDA draft guidance mandates secure design and lifecycle management, compelling manufacturers to invest heavily in encryption, authentication, and post-market patching. Hospitals wary of ransomware remain cautious about adding networked ingestibles, slowing adoption.

Segment Analysis

By Type: Drug-Delivery Applications Drive Innovation

Drug-delivery capsules recorded the highest 14.12% CAGR, despite capsule endoscopy retaining 40.78% 2025 revenue leadership. This divergence shows the market’s therapeutic shift as companies harness smart pills for precise dosing. MIT’s once-weekly risperidone capsule validates sustained psychiatric dosing, underscoring new care models. Active-pumping capsules now pair biomarker sensing with on-demand release, enabling closed-loop therapy and boosting the smart pills drug delivery market’s clinical value.

Drug-delivery tools answer unmet needs in inflammatory bowel disease and localized cancers. Magnetically navigated capsules allow clinicians to linger at sites of interest, overcoming historic limits of passive transit. As these devices progress through trials, healthcare providers anticipate better outcomes and lower systemic drug exposure, reinforcing adoption.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Platforms Capture Value Migration

Ingestible sensors held 51.76% revenue, but AI-driven software platforms grew fastest at 14.45% CAGR. Providers seek insights rather than data, shifting value upstream to analytics that interpret ingestion patterns, lesion images, and physiological signals. FDA guidance on algorithm change-control fosters iterative updates while safeguarding safety. This regulatory clarity accelerates deployment, deepening reliance on analytics layers inside the smart pills drug delivery market.

Wearable receivers bridge capsules and clouds, ensuring uninterrupted data flow even in low-connectivity settings. As sensor miniaturization proceeds, stakeholders anticipate multi-parameter chips that integrate pH, temperature, and pressure sensing, further amplifying the role of software in deriving clinical meaning.

By Application: Targeted Delivery Transforms Treatment Paradigms

Diagnostic imaging retained 46.92% revenue in 2025, yet targeted drug delivery led growth at 13.18% CAGR. Magnetically steered capsules equipped with multimodal release profiles deliver chemo-, sono-, or photo-therapies directly to disease sites. Such precision lowers systemic toxicity and aligns with oncology’s push toward localized intervention, propelling the smart pills drug delivery market.

Medication adherence tracking blends diagnostic and therapeutic functions, verifying dose ingestion while capturing physiological responses. Aggregated datasets inform population-health analytics, enabling payers to benchmark adherence programs and refine formulary strategies.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: Home Healthcare Drives Accessibility

Hospitals and clinics held 48.12% revenue in 2025, but home healthcare advanced at a 13.22% CAGR as telehealth infrastructure matured. Medtronic’s PillCam Genius SB Kit lets patients complete procedures at home, reducing facility bottlenecks. Simplified user interfaces and automated data uploads expand access beyond tertiary centers, broadening the smart pills drug delivery market user base.

Diagnostic centers sustain demand for capsule endoscopy interpretation services, while research institutes pilot next-generation prototypes. Home-based models align with payer incentives to cut inpatient costs, accelerating decentralized care.

Note: Segment shares of all individual segments available upon report purchase

By Disease Indication: Oncology Applications Accelerate Growth

Gastrointestinal disorders retained 52.88% revenue in 2025, yet oncology posted a 13.91% CAGR as nanorobot-enabled capsules infiltrated tumor microenvironments. Smart pills equipped with sensing and drug-release modules adapt doses to real-time biomarker changes, tailoring therapy and underscoring the smart pills drug delivery market’s potential in precision oncology.

Obesity and metabolic disorder applications emerge through ingestible balloons and nutrient-absorption modifiers. Such innovations diversify revenue streams and attract multidisciplinary collaborations.

Geography Analysis

North America controlled 44.01% revenue in 2025, supported by FDA pathways and strong venture funding. CMS’s Transitional Coverage for Emerging Technologies expedites reimbursement for breakthrough devices, reducing payback risk. Defense budgets dedicate USD 1.66 billion to chemical and biological countermeasures, some of which fund ingestible diagnostics. These factors cement regional leadership in the smart pills drug delivery market.

Asia-Pacific is the fastest-growing region at 12.98% CAGR through 2031. Japan’s Pharmaceuticals and Medical Devices Agency accelerates approvals, while China’s digital-health investments integrate smart pills into chronic-care platforms. India’s Medical Device Rules 2018 clarify classification and compliance, encouraging local production. Economies of scale in electronics manufacturing lower unit costs, fueling regional penetration.

Europe exhibits stable growth within a stringent data-protection context. Germany, the United Kingdom, and France showcase hospital pilots combining smart pills with AI interpretation. The EU Medical Device Regulation ensures safety but lengthens certification cycles, prompting firms to deploy North America first. South America and Middle East & Africa follow with nascent though expanding adoption as healthcare access broadens.

Competitive Landscape

Market Concentration

The market remains moderately fragmented. Medtronic, Olympus, and Philips leverage distribution scale to commercialize smart pills globally, while CapsoVision, etectRx, and Proteus Digital Health specialize in adherence monitoring. Partnerships between pharma and tech firms accelerate combination products. Patent races focus on AI lesion detection, energy-harvesting circuits, and triggered drug-release mechanisms.

Strategic moves include Medtronic’s 2024 launch of the PillCam Genius SB Kit, which added haptic alerts for home procedures, and DARPA grants that fund prototype ingestibles for military wound monitoring. Start-ups such as etectRx secure FDA clearances for medication ingestion tracking, signing data-licensing deals with pharmaceutical sponsors. Price competition remains subdued because clinical performance and regulatory approval act as primary differentiators.

Smart Pills Drug Delivery Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: MIT researchers reported phase 3 success for a once-weekly risperidone capsule delivering stable plasma levels over seven days.

- February 2025: DARPA unveiled the Bioelectronics for Enhancement of Soldier Survivability program focused on autonomous wound-treatment devices.

- December 2024: Medtronic completed the first ingestion of PillCam Genius SB Kit, enabling at-home capsule endoscopy.

- June 2024: University of Southern California introduced GPS-like smart pills capable of detecting stomach gases linked to gastric cancers.

Table of Contents for Smart Pills Drug Delivery Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapid Adoption Of Capsule Endoscopy For GI Diagnostics

- 4.2.2Preference For Minimally-Invasive Patient Monitoring

- 4.2.3Growing Chronic-Disease Burden & Poly-Pharmacy

- 4.2.4Integration With Telehealth & Remote Adherence Platforms

- 4.2.5Venture-Capital Shift Toward Ingestible Bio-Electronics

- 4.2.6Defense / Space-Medicine Funding For “Inside-Out” Vitals Sensing

- 4.3Market Restraints

- 4.3.1Stringent FDA & EMA Device–Drug Combination Approval Path

- 4.3.2Adverse Events: Capsule Retention & GI Obstruction

- 4.3.3Cyber-Security Risks Of Sensor-To-Cloud Data Flow

- 4.3.4Reimbursement Gaps For Digital Ingestion Event Markers

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Type

- 5.1.1Capsule Endoscopy

- 5.1.2Patient Monitoring Smart Pills

- 5.1.3Drug-Delivery Smart Pills

- 5.2By Component

- 5.2.1Ingestible Sensor

- 5.2.2Wearable Receiver/Patch

- 5.2.3Software & Analytics Platform

- 5.3By Application

- 5.3.1Diagnostic Imaging

- 5.3.2Medication Adherence Tracking

- 5.3.3Targeted Drug Delivery

- 5.4By End User

- 5.4.1Hospitals & Clinics

- 5.4.2Diagnostic Centers

- 5.4.3Home Healthcare

- 5.4.4Research Institutes

- 5.5By Disease Indication

- 5.5.1Gastro-intestinal Disorders

- 5.5.2Oncology

- 5.5.3Obesity & Metabolic Disorders

- 5.5.4Others

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1Medtronic plc

- 6.3.2Olympus Corp

- 6.3.3Philips NV

- 6.3.4CapsoVision Inc.

- 6.3.5Jinshan Science & Tech

- 6.3.6Check-Cap Ltd.

- 6.3.7etectRx Inc.

- 6.3.8Otsuka Pharmaceutical Co.

- 6.3.9HQ Inc.

- 6.3.10IntroMedic Co.

- 6.3.11BodyCap Medical

- 6.3.12Proteus Digital Health

- 6.3.13RF Tracking Systems

- 6.3.14AnX Robotica

- 6.3.15Chongqing Science & Tech

- 6.3.16PENTAX Medical

- 6.3.17Karl Storz SE & Co. KG

- 6.3.18Fujifilm Holdings Corp

- 6.3.19Boston Scientific Corp

7. Market Opportunities and Future Outlook

- 7.1White-Space and Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Type

- Capsule Endoscopy

- Patient Monitoring Smart Pills

- Drug-Delivery Smart Pills

- Capsule Endoscopy

- By Component

- Ingestible Sensor

- Wearable Receiver/Patch

- Software & Analytics Platform

- Ingestible Sensor

- By Application

- Diagnostic Imaging

- Medication Adherence Tracking

- Targeted Drug Delivery

- Diagnostic Imaging

- By End User

- Hospitals & Clinics

- Diagnostic Centers

- Home Healthcare

- Research Institutes

- Hospitals & Clinics

- By Disease Indication

- Gastro-intestinal Disorders

- Oncology

- Obesity & Metabolic Disorders

- Others

- Gastro-intestinal Disorders

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Smart Pills Drug Delivery Baseline Stays Credible

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.83 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 4.85 B (2024) | Global Consultancy A | Counts ingestible sensors and service revenues beyond prescription capsules | ||

USD 0.69 B (2024) | Global Consultancy B | Restricts scope to U.S./EU approved drug-device combos only | ||

USD 4.22 B (2023) | Industry Analytics C | Merges wellness ingestibles and diagnostic capsules without triangulating usage data |