Drug Repurposing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

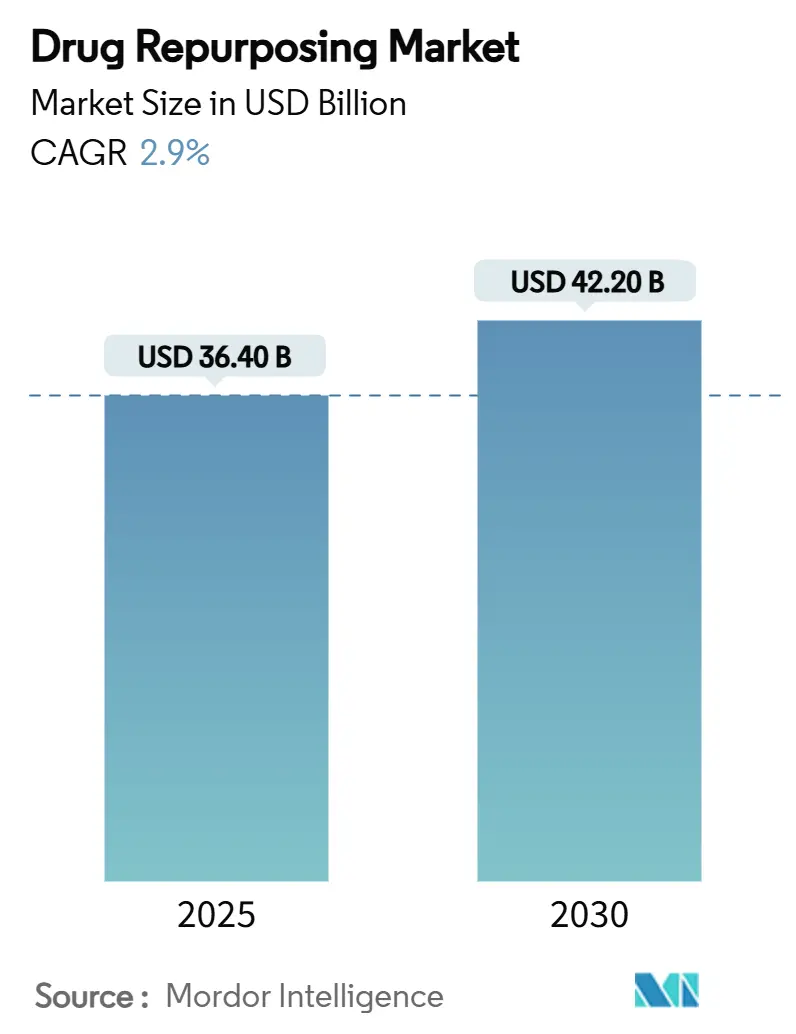

| Market Size (2025) | USD 36.40 Billion |

| Market Size (2030) | USD 42.20 Billion |

| Growth Rate (2025 - 2030) | 2.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

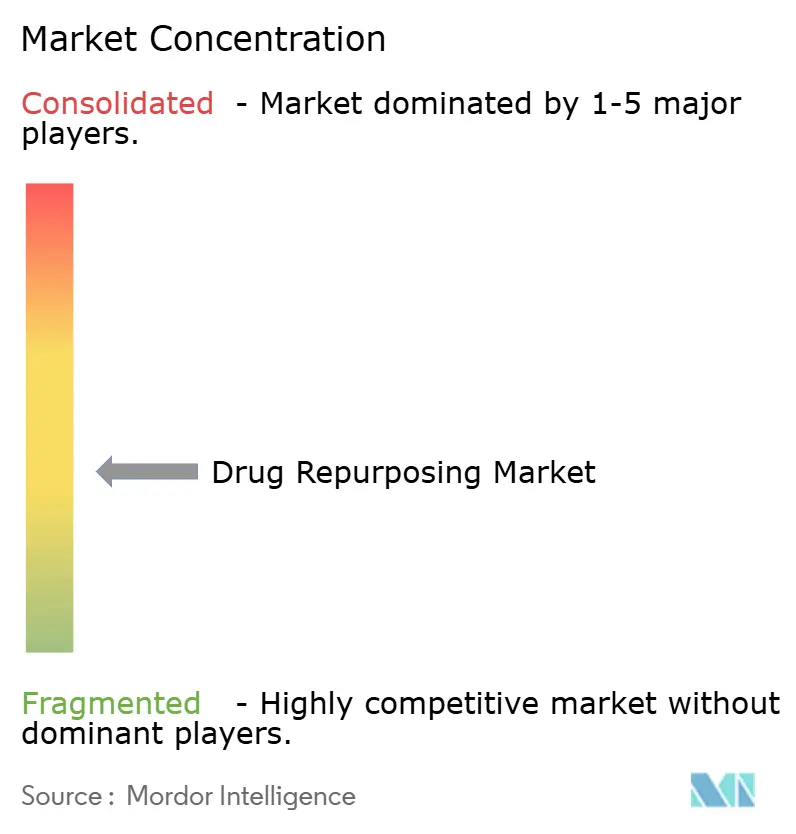

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drug Repurposing Market Analysis by Mordor Intelligence

The drug repurposing market size stood at USD 36.4 billion in 2025 and is expected to climb to USD 42.2 billion by 2030, translating into a 2.9% CAGR during the forecast period. Within this measured growth curve, established pharmaceutical companies, smaller biotechnology firms, and contract research organizations (CROs) are all intensifying their focus on re-evaluating approved or shelved molecules to shorten development timelines, lower R&D expenditure, and extend product lifecycles. Intensifying patent-cliff pressure, such as USD 183.5 billion in at-risk revenue by 2030, has pushed leading innovators to expand high-throughput in silico screening programs, frequently powered by AI, and to prioritize 505(b)(2) pathway submissions that recycle existing safety data. Oncology retains strategic primacy. Yet, rare and orphan indications are accelerating fastest, supported by venture funding spikes and favorable orphan-drug incentives. Small molecules continue to dominate the pipeline, though peptides and other biologics are closing the gap as manufacturing costs fall. North America anchors global demand thanks to well-defined FDA guidance that now embraces real-world evidence. At the same time, Asia-Pacific benefits most from rapidly scaling clinical-trial infrastructure and cost advantages.

Key Report Takeaways

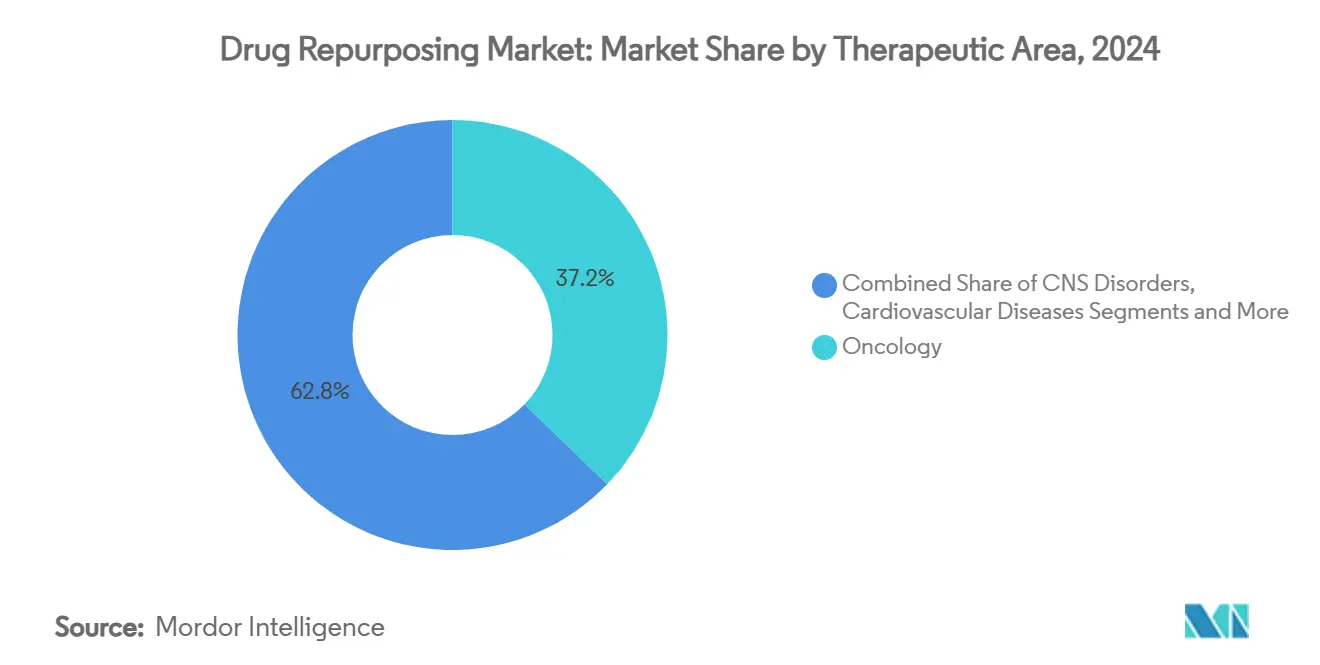

- By therapeutic area, oncology led with a 37.2% revenue share in 2024, while rare and orphan diseases are projected to grow at a 14.8% CAGR through 2030.

- By molecule type, small molecules accounted for 64.5% of the drug repurposing market share in 2024; peptides and other biologics are advancing at a 13.1% CAGR through 2030.

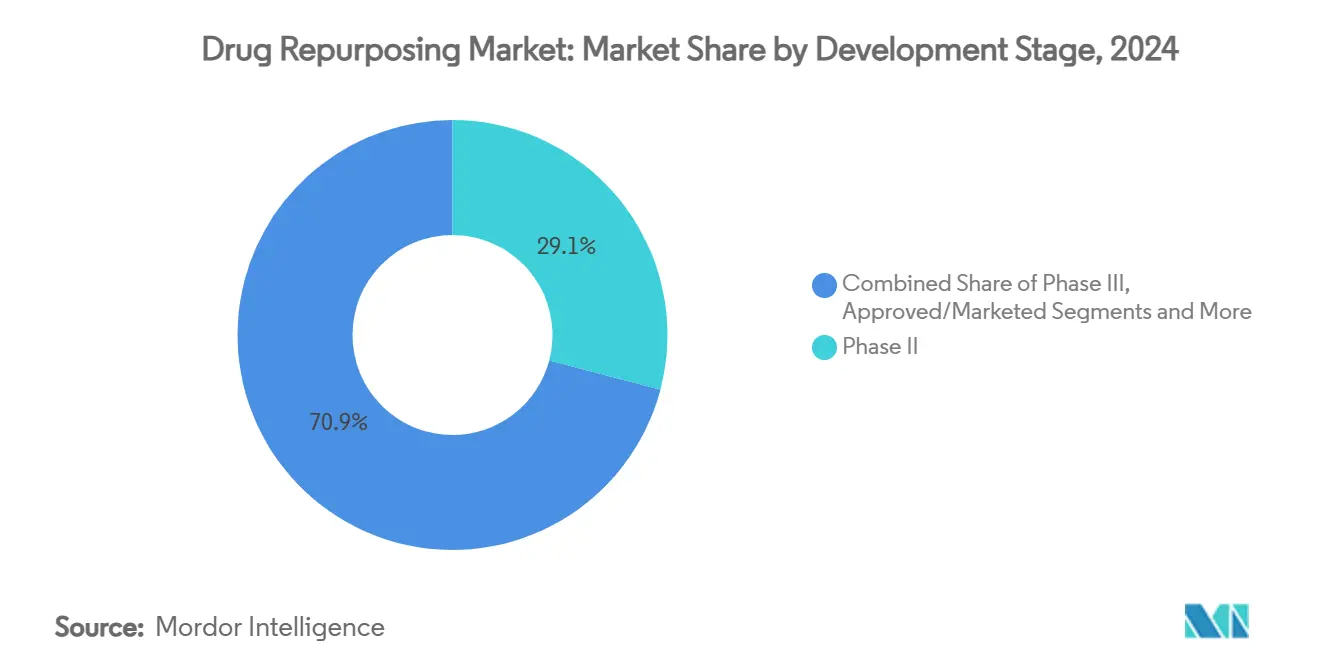

- By the development stage, Phase II held 29.1% of the drug repurposing market size in 2024, whereas the pre-clinical stage expanded at a 15.9% CAGR to 2030.

- By end user, pharmaceutical and biotechnology companies captured 54.8% of 2024 revenue; contract research organizations are set to expand at a 12.4% CAGR through 2030.

- By geography, North America commanded 45.3% of 2024 revenue, and Asia-Pacific is forecast to rise at an 11.6% CAGR through 2030.

Global Drug Repurposing Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled high-throughput in-silico screening | +0.80% | North America, EU, increasingly global | Medium term (2-4 years) |

| Growing FDA 505(b)(2) approvals pathway | +0.60% | North America, EU | Short term (≤ 2 years) |

| Venture funding surge for orphan & rare disease repurposing | +0.50% | North America, EU | Medium term (2-4 years) |

| Pandemic-driven interest in broad-spectrum antivirals | +0.40% | Global | Short term (≤ 2 years) |

| Real-world evidence (RWE) data-lake availability | +0.30% | North America, EU, APAC | Medium term (2-4 years) |

| Pharma patent-cliff risk mitigation | +0.70% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled High-Throughput In-Silico Screening

Compute-intensive image-based models now evaluate millions of morphological signatures across compound libraries in weeks instead of the years required by traditional wet-lab assays. Recursion’s BioHive-2 quadrupled its own prior compute, enabling the Phenom-1 model to scour while simultaneously annotating complex phenotypes. Start-ups such as Healx raised USD 47 million in 2024 to propel similar architectures, especially for rare diseases. These cloud-native pipelines push smaller firms into direct competition with Big Pharma by eliminating the need for expansive physical labs. The resulting efficiency allows rapid re-prioritization of hits into niche indications, widening the opportunity set and compressing cost per program. As the algorithms mature, they are predicted to feed a continuous flow of de-risked, mechanism-based assets into the drug repurposing market, further reinforcing its steady expansion path.

Growing FDA 505(b)(2) Approvals Pathway

The 505(b)(2) framework grants sponsors permission to integrate existing clinical and non-clinical data into a single submission, shortening average approval timelines by up to two years. Forty-eight approvals used the route in 2016, and the total has climbed every year since as sponsors seek capital-efficient routes to market. Recent FDA draft guidance on “Platform Technology Designation” broadens the flexibility by letting developers reuse prior regulatory findings across multiple submissions, thus curbing redundant review cycles.[1]FDA, “Platform Technology Designation Program for Drug Development,” fda.gov In parallel, master protocols and adaptive designs are being welcomed to address the heterogeneity inherent in repurposing research. Together, these regulatory facilitators lower risk, attract fresh investment, and underpin the rising contribution of 505(b)(2) approvals to overall drug repurposing market growth.

Venture Funding Surge for Orphan & Rare Disease Repurposing

Only 5% of an estimated 7,000 rare diseases have an approved therapy, leaving a large addressable gap. Recent capital inflows underscore investor conviction that repurposing can marry speed with robust returns. The FELIQS round of USD 9 million for FLQ-101 in retinopathy of prematurity typifies funding directed at narrowly defined pediatric indications. Orphan-drug designations in major markets assure seven-to-ten-year exclusivity, premium reimbursement, and regulatory fee waivers, enhancing the economic reward. Academic groups, patient foundations, and CROs increasingly form tripartite alliances to share data, thereby channeling more candidates into the drug repurposing market sooner and at lower cost.

Pandemic-Driven Interest in Broad-Spectrum Antivirals

COVID-19 tested the resilience of drug-development pipelines and highlighted repurposing as a first-line response mechanism. RTI’s READDI alliance scanned thousands of molecules to fast-track candidates against coronaviridae.[2]RTI International, “READDI Forethought: A 2024 Update,” rti.org Independent screens later flagged biapenem, adefovir dipivoxil, and dovitinib as entry inhibitors for SARS-CoV-2.[3]Frontiers in Pharmacology Authors, “FDA-approved drug repurposing screen identifies SARS-CoV-2 inhibitors,” frontiersin.org Beyond acute crises, durable translational capabilities have been built—specialized BSL-3 labs, compound libraries annotated for viral mechanisms, and standing public-private task forces. These assets now stand ready to address future outbreaks swiftly and strengthen the drug repurposing market’s relevance to global health security.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex IP ownership & exclusivity disputes | -0.40% | Developed markets | Long term (≥ 4 years) |

| Limited reimbursement frameworks for off-label indications | -0.30% | North America, EU | Medium term (2-4 years) |

| Clinical-trial recruitment challenges for niche indications | -0.20% | Global | Medium term (2-4 years) |

| Data-bias risk in AI prediction models | -0.10% | AI-adopting regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex IP Ownership & Exclusivity Disputes

Where originator patents have lapsed, competing stakeholders often stake overlapping claims on formulation, method-of-use, or delivery mechanisms. Ongoing litigation—such as Eli Lilly’s disagreement with FDA over retatrutide’s product class—illustrates how classification alone can decide exclusivity periods and generic entry. GLP-1 agonists demonstrate the use of intricate formulation patents to erect protective “thickets,” raising legal ambiguity for follow-on developers. Uncertainty depresses venture backing for off-patent molecules and prolongs negotiations around data-sharing. Unless legislative updates offer predictable exclusivity windows, IP complexity will continue to shave growth from the drug repurposing market.

Limited Reimbursement Frameworks for Off-Label Indications

Even when regulatory hurdles are cleared, payers may decline coverage outside original labels, citing cost containment or insufficient evidence. U.S. drug-price negotiations introduced under the Inflation Reduction Act add another variable that may deter sponsors from adding marginal indications. In China, 2021 legislation now mandates formal evidence reviews and consent processes before off-label prescribing, adding administrative friction. Emerging “interventional pharmacoeconomic” trials seek to generate payer-friendly cost-effectiveness data, yet adoption remains limited. Until standardized reimbursement benchmarks mature, payer gatekeeping will curb uptake in the drug repurposing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Area: Oncology Dominates While Rare Diseases Accelerate

The drug repurposing market size for oncology reached 37.2% of overall revenue. PD-(L)1 inhibitors, kinase blockers, and DNA-damage response agents now account for the lion’s share of activity, supported by well-developed biomarker ecosystems. Eight tumor-agnostic approvals—such as pembrolizumab for MSI-H malignancies—validate the tissue-agnostic paradigm and signal wider acceptance of molecularly driven repositioning. Basket and umbrella protocols reduce statistical penalties, thereby encouraging developers to pivot a single compound across multiple histologies. Second-order gains appear in combination regimens where repurposed low-cost agents potentiate expensive biologics, extending their profitability curve.

Rare and orphan conditions are growing at 14.8% CAGR through 2030, the fastest of any therapeutic group. Ultra-small patient populations justify premium pricing and long exclusivity windows, making the segment attractive despite volume constraints. Regulatory bodies waive certain fees, and advocacy groups provide trial-ready registries, trimming development friction. The confluence of financial incentives and societal need aligns capital behind rare-disease initiatives, ensuring durable expansion of this sub-segment of the drug repurposing market.

By Molecule Type: Small-Molecule Prevalence vs. Peptide Momentum

Small-molecule assets controlled 64.5% of drug repurposing market share in 2024, reflecting decades of accumulated safety data and scalable oral manufacturing pathways. Structural tractability simplifies formulation tweaks, dosage-form changes, and label extensions. Moreover, oral bioavailability aligns with cost-sensitive global markets seeking self-administered regimens.

Peptides and larger biologics are set to rise 13.1% annually to 2030, boosted by process intensification, continuous bioreactors, and lyophilized formulations that ease logistics. Peptide approvals constituted 11% of FDA clearances between 2016-2024, signaling mainstream confidence. The GLP-1 agonist class serves as a template: semaglutide and tirzepatide now target obesity and cardiovascular indications in addition to diabetes. Although cold-chain and immunogenicity hurdles persist, incremental process refinements are eroding these barriers, broadening biologics’ footprint in the drug repurposing market.

By Development Stage: Pre-Clinical Investments Propel Future Pipeline

The pre-clinical segment showed 15.9% CAGR from 2024 through 2025, driven by AI screens that filter vast compound pools before costly human trials. Cloud-native modeling cuts cycle times, yielding more validated leads for further investment.

Phase II represented 29.1% of overall drug repurposing market size in 2024, serving as the crucible for proof-of-concept and biomarker validation. Adaptive enrichment strategies permit continuous signal detection, trimming attrition. Approved and marketed products now undergo life-cycle management to preserve revenues against biosimilar encroachment—typified by Karuna Therapeutics’ long-running xanomeline program that culminated in a USD 14 billion exit.

By Route of Administration: Oral Delivery Innovation Expands Access

Injectable formats still dominate high-value peptides and monoclonals; however, oral delivery is the fastest-growing node, aided by permeation enhancers, nanoparticle carriers, and micro-needle capsules. Oral liraglutide nanomicelles achieved 4.63-fold bioavailability gains, showcasing feasibility for converting once-weekly injections into pills. These advances unlock adherence gains, improve quality of life, and enlarge the addressable base for the drug repurposing market.

By End User: CROs Capture Outsourcing Wave

Pharmaceutical and biotech firms held 54.8% revenue share in 2024 but are offloading operational burden to specialized CRO partners at 12.4% CAGR. CROs bring regulatory acumen in 505(b)(2) filing, access to patient networks, and data-management platforms tuned for repurposing. Academic hubs such as the Broad Institute’s 6,000-compound Drug Repurposing Hub supply validated reagents and assays, facilitating seamless public-private handoffs. Hence, CRO integration remains a pivotal efficiency driver of the drug repurposing market.

Geography Analysis

North America controlled 45.3% of 2024 revenue, underpinned by the FDA’s growing acceptance of RWE, broader use of the 505(b)(2) pathway, and commissioner-level initiatives to fast-track non-animal methods. Venture capital depth fosters AI start-ups that replenish the early-stage pipeline, reinforcing the region’s leadership in drug repurposing market innovation.

Asia-Pacific, led by China, is forecast to post an 11.6% CAGR to 2030. Chinese interventional studies swelled from about 600 in 2017 to nearly 2,000 in 2024, aided by multi-agency reforms that simplify IND paperwork and grant rolling reviews. Lower trial-site costs and large naïve patient pools further enhance appeal. Countries such as India and South Korea are scaling similar regulatory sandboxes, positioning APAC as a key volume driver for the drug repurposing market.

Europe retains robust academic output and orchestrates cross-border approvals through EMA harmonization. Proposed EU legislation to expedite label extensions will curtail administrative delays and inject additional momentum into drug repurposing programs. Latin America and the Middle East & Africa remain nascent but are exploring domestic manufacturing tie-ins and public-sector partnerships to localize repurposed therapies, creating optional upside for long-term market penetration.

Competitive Landscape

The drug repurposing market tilts toward moderate fragmentation. Big Pharma defends cash-flow resilience by redeploying historical molecule libraries, while AI-centric biotechs such as Recursion and Exscientia combine massive phenotypic datasets with algorithmic engines to leapfrog discovery phases. Strategic alliances dominate: Bayer pledged USD 1.5 billion to access Recursion’s phenomics platform, whereas Sanofi partnered with Formation Bio and OpenAI to build bespoke LLMs for molecule analysis.

Therapeutic focus diversifies competitive intensity: oncology remains crowded with multinationals, whereas rare-disease niches see nimble developers advance under fast-track and orphan-drug rules. CRO consolidation accelerates, enabling full-service offerings and risk-sharing contracts that reduce up-front cash drain for sponsors.

Ultimately, firms that achieve tight vertical integration—combining computational selection, rapid pre-clinical throughput, and lean pivotal trials—are best positioned to capture incremental share in the drug repurposing market.

Drug Repurposing Industry Leaders

Recursion Pharmaceuticals

BenevolentAI

Novartis AG

Pfizer Inc.

Roche Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sanofi’s tolebrutinib accepted for priority FDA review in non-relapsing secondary progressive multiple sclerosis.

- March 2025: Sanofi set aside up to USD 1.9 billion to acquire Dren Bio’s bispecific antibody DR-0201 for autoimmune disease.

- January 2025: Lantheus Holdings, Johnson & Johnson, Eli Lilly, and GSK completed neuroscience and oncology-focused takeovers.

- November 2024: Recursion finalized its merger with Exscientia, consolidating more than 10 pipeline programs under a shared AI backbone.

Global Drug Repurposing Market Report Scope

| Oncology |

| CNS Disorders |

| Cardiovascular Diseases |

| Infectious Diseases |

| Metabolic Disorders |

| Small-molecule Drugs |

| Biologics & Peptides |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Approved / Marketed |

| Oral |

| Injectable |

| Topical / Others |

| Pharmaceutical & Biotech Companies |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Area | Oncology | |

| CNS Disorders | ||

| Cardiovascular Diseases | ||

| Infectious Diseases | ||

| Metabolic Disorders | ||

| By Drug Molecule Type | Small-molecule Drugs | |

| Biologics & Peptides | ||

| By Development Stage | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Approved / Marketed | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Topical / Others | ||

| By End User | Pharmaceutical & Biotech Companies | |

| Academic & Research Institutes | ||

| Contract Research Organizations (CROs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the drug repurposing market?

The drug repurposing market size reached USD 36.4 billion in 2025 and is projected to rise to USD 42.2 billion by 2030.

Which therapeutic segment leads revenue?

Oncology holds the largest share at 37.2% of 2024 revenue, driven by biomarker-guided, tissue-agnostic approvals.

Why are rare diseases attracting increased investment?

Orphan-drug incentives, premium pricing, and low competition push rare-disease repurposing to the fastest growth rate at 14.8% CAGR through 2030.

How important are AI platforms to repurposing success?

AI-enabled in-silico screening adds an estimated +0.8% to forecast CAGR by compressing target-identification timelines and broadening accessible indication space.

Which region will grow fastest?

Asia-Pacific is set to post an 11.6% CAGR through 2030, underpinned by regulatory reform and a surge in clinical-trial activity.

What role do CROs play?

Outsourcing to CROs is expanding at 12.4% CAGR as sponsors leverage specialized regulatory, recruitment, and data-management capabilities to accelerate repurposing programs.

Page last updated on: