Seed Processing Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 6.72 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

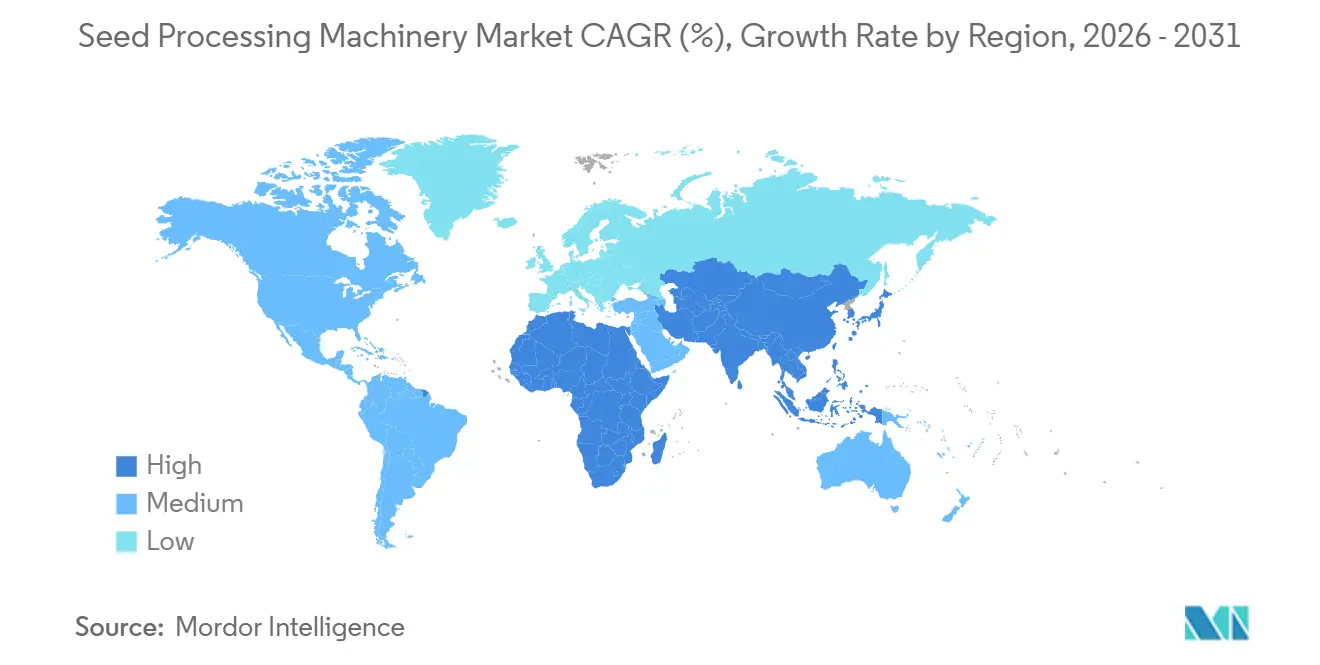

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Seed Processing Machinery Market Analysis by Mordor Intelligence

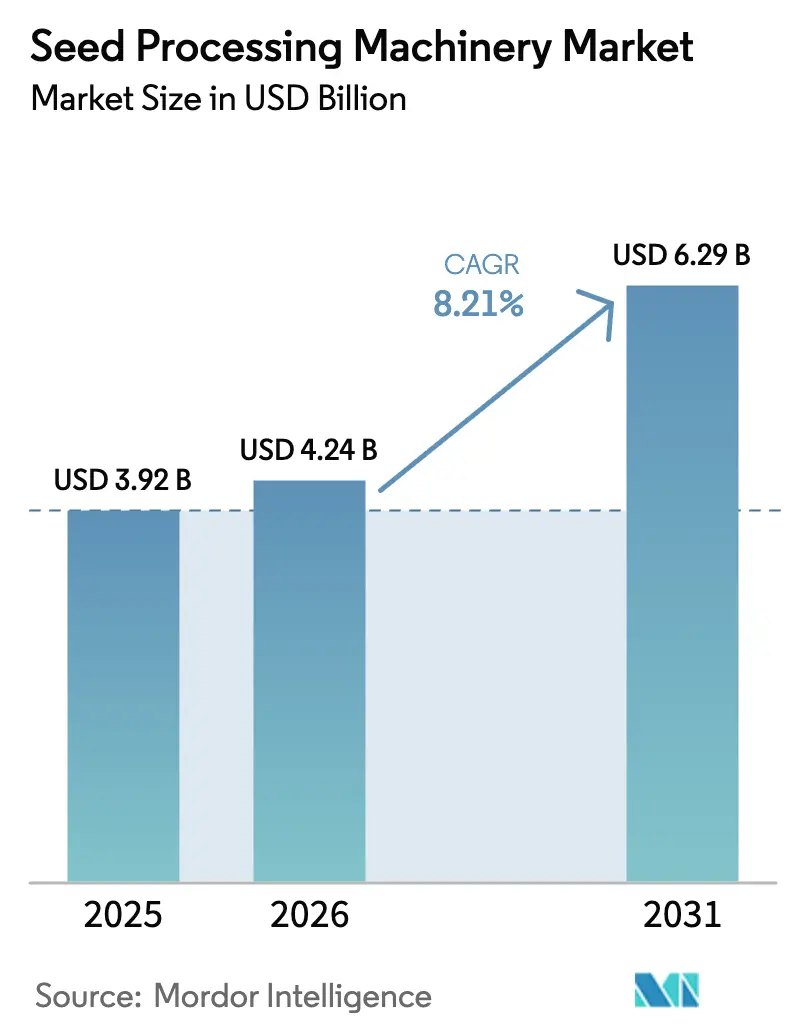

The seed processing machinery market size was valued at USD 3.92 billion in 2025 and is projected to increase to USD 4.81 billion in 2026, reaching USD 6.72 billion by 2031, growing at a CAGR of 6.92% from 2026 to 2031. Greater emphasis on seed quality, food-safety compliance, and the economics of treated seeds is reshaping procurement priorities. The automation of optical sorting and sensor-based moisture control is reducing labor costs and enhancing germination rates, prompting processors to phase out manual and semi-automatic lines. Subsidized credit programs in countries such as India, Brazil, and the United States are lowering initial costs, encouraging small- and midsize buyers to invest in seed-processing machinery. However, competition is intensifying as Chinese and Indian suppliers offer lower prices, challenging established European brands and squeezing margins in the 1–10 metric tons per hour category. Supply chain delays for hyperspectral cameras and industrial sensors, along with concerns over data sovereignty in the European Union and North America, continue to pose challenges.

Key Report Takeaways

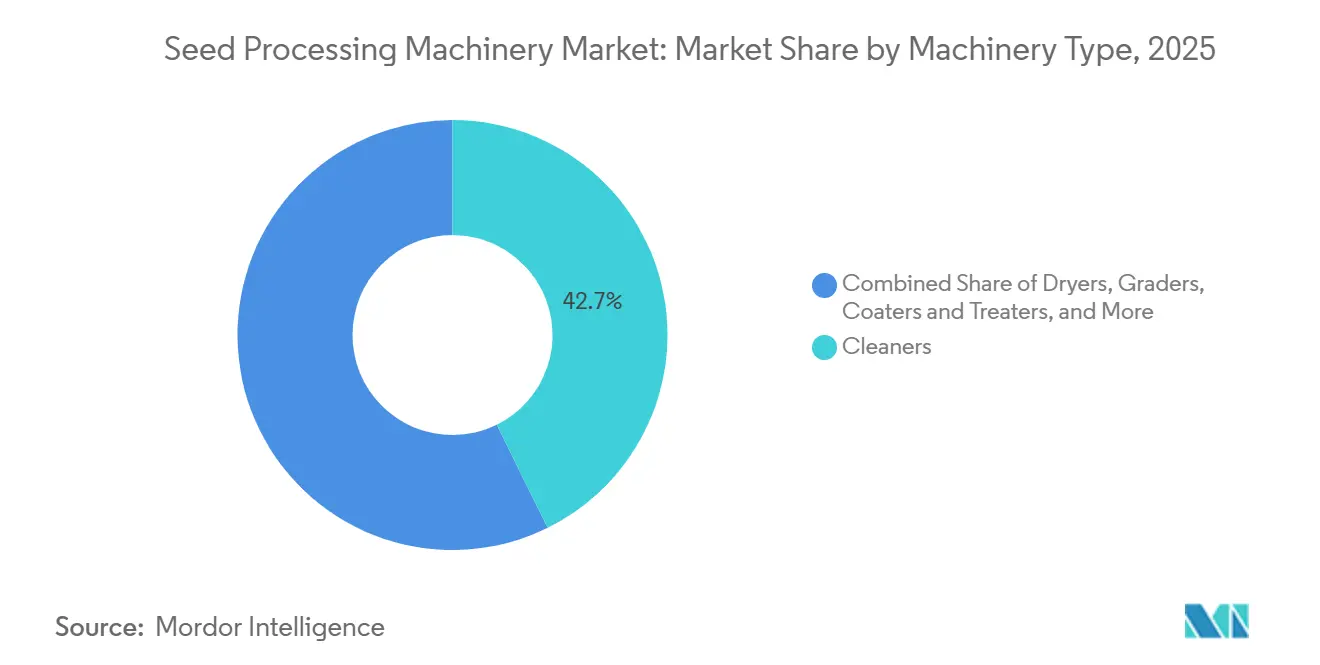

- By machinery type, cleaners led with 42.7% of the seed processing machinery share market in 2025, and optical sorters are projected to post the fastest growth, advancing at a 7.6% CAGR to 2031.

- By operation mode, automatic systems commanded 70.6% of 2025 installations and are projected to record the highest CAGR at 8% through 2031.

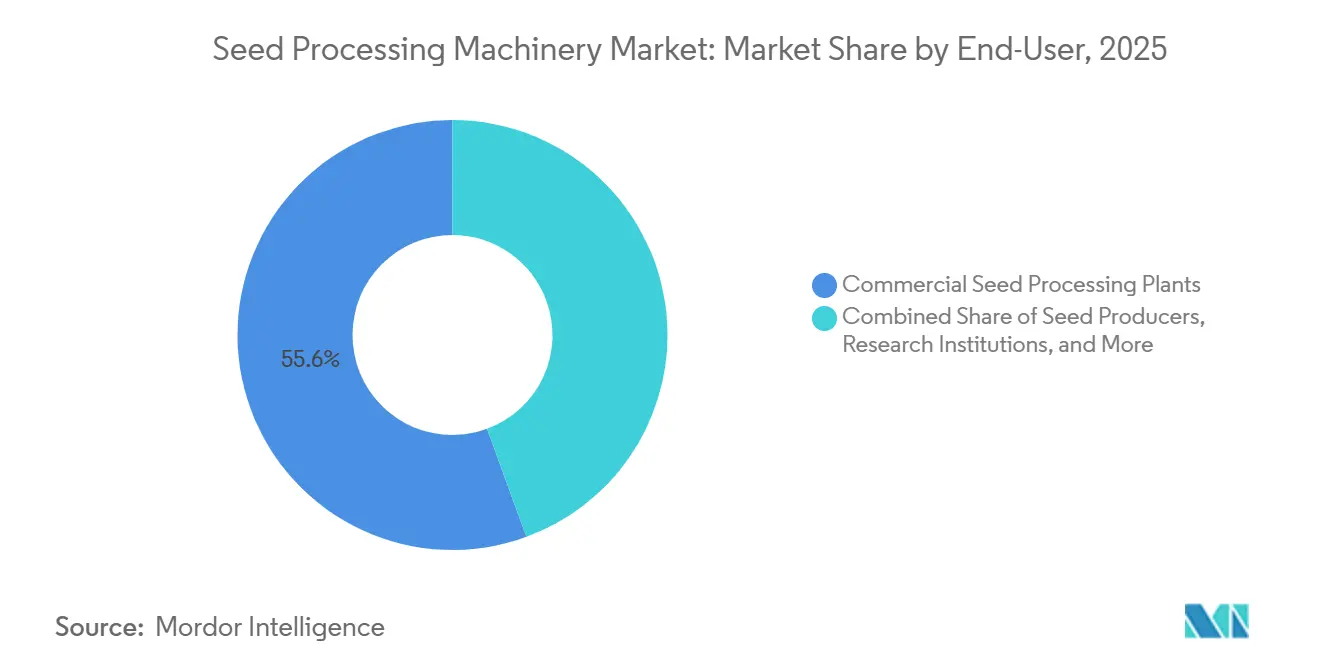

- By end-user, commercial plants accounted for 55.6% of the seed processing machinery market size in 2025, whereas on-farm facilities are expanding at a 6.4% CAGR through 2031.

- By capacity, systems above 10 metric tons/hour captured 63.5% of the 2025 market size, while systems below 1 metric ton/hour are growing at a 7.5% CAGR.

- By geography, North America accounted for 34.1% of the market share in 2025, whereas Asia-Pacific is forecast to post the fastest CAGR of 8.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Seed Processing Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automation of optical sorting enhances efficiency and reduces labor costs | +1.0% | North America and Western Europe, and widening to global | Medium term (2-4 years) |

| Increasing demand for treated and value-added seeds | +0.9% | North America, Europe, and Brazil | Long term (≥ 4 years) |

| Government subsidies boost post-harvest mechanization efforts | +1.0% | India, China, Brazil, and Sub-Saharan Africa | Medium term (2-4 years) |

| Growth in commercial seed multiplication centers | +0.7% | United States, Brazil, India, and China | Long term (≥ 4 years) |

| Sensor-based moisture control enhances germination rates | +0.6% | Global, led by hybrid corn and vegetable segments | Short term (≤ 2 years) |

| Investments aimed at halving post-harvest losses | +0.8% | Asia-Pacific, Sub-Saharan Africa, and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automation of Optical Sorting Enhances Efficiency and Reduces Labor Costs

Widespread deployment of hyperspectral imaging and machine-learning classifiers is transforming quality control. Optical sorting systems utilizing hyperspectral imaging and machine-learning classifiers are replacing manual grading and traditional mechanical separators in commercial seed processing plants. These systems reduce labor costs while enhancing defect-detection accuracy. PETKUS Technologie GmbH demonstrated comparable modular platforms in 2024 that combine optical and pneumatic separation to avoid cross-contamination, a key requirement for organic and non-GMO lots. The OECD Employment Outlook 2025 highlights that labor shortages are widespread across various sectors, including agriculture, where recruitment challenges hinder both production and innovation[1]Source: Organisation for Economic Cooperation and Development, “Agricultural Policy Monitoring and Evaluation,” oecd.org. Falling component prices will allow emerging-market processors to follow suit over the medium term. As the technology migrates downstream, the seed processing machinery market will see automatic lines become the default specification.

Increasing Demand for Treated and Value-Added Seeds

Higher premiums for treated seeds compared to untreated seeds for hybrid corn, soybean, and cotton are encouraging investments in upgrading equipment. Concurrently, regulatory frameworks are becoming increasingly stringent, with the European Union's Farm to Fork strategy setting an ambitious goal of reducing chemical pesticide use by 50% by 2030[2]Source: European Commission, "Farm to Fork Strategy," ec.europa.eu. This regulatory push is compelling seed producers to transition toward biological coatings, which require advanced equipment capable of handling water-based formulations effectively. Precision applicators, designed to maintain a consistent 50–100 micron film thickness, have become indispensable, rendering older drum coaters obsolete. As the adoption of biological treatments continues to grow, with their market value projected to rise significantly from 2024 to a projected peak by 2030, the seed processing machinery market is anticipated to undergo a substantial transformation. This shift will prioritize gentler, water-based processes that demand greater precision and tighter tolerances to meet the evolving industry requirements.

Government Subsidies Boost Post-Harvest Mechanization Efforts

Government subsidies play a significant role in driving the seed processing machinery market by providing financial incentives, including capital subsidies for project costs related to cleaning, grading, and packaging infrastructure. Public funding is lowering borrowing costs and compressing payback periods. India’s Agriculture Infrastructure Fund allotted USD 7.9 billion in 2025, covering a significant portion of equipment costs for processors installing dryers, cleaners, and optical sorters[3]Source: National Bank for Agriculture and Rural Development, “Agriculture Infrastructure Fund,” nabard.org. Brazil's 2024-2025 Plano Safra allocates BRL 475.5 billion (USD 88.2 billion) for agricultural credit, emphasizing sustainability and enhancing production capacity[4]Source: Government of Brazil, “Plano Safra 2024-2025,” gov.br. This funding facilitates the adoption of modern, high-efficiency equipment, which is projected to drive demand for seed-processing machinery as part of broader agricultural modernization initiatives. The United States Department of Agriculture (USDA) provides significant subsidies, loans, and grants for seeds and equipment through the Farm Service Agency (FSA). These include Farm Operating Loans and specialized microloans designed for small and beginning farmers. These incentives shorten return-on-investment horizons and intensify competition, driving deeper penetration of the seed processing machinery market into second-tier cooperatives and mid-size farms.

Sensor-Based Moisture Control Enhances Germination Rates

Near-infrared sensors integrated into dryers now maintain precise moisture levels, significantly enhancing germination rates in high-value hybrid seeds. Ag Growth International Inc.’s STX3 auger automatically adjusts airflow and temperature, resulting in significant reductions in energy use. Tropical processors benefit the most, as ambient humidity can vary widely within a single batch, increasing the risk of mold or seed brittleness. Adoption is advancing steadily as sensor prices continue to decline. Integrated controls are projected to become a standard feature in the seed processing machinery market, driving the evolution toward fully connected, automated plants.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front cost of smart machinery | -0.8% | Emerging markets with limited credit | Medium term (2-4 years) |

| Supply chain volatility for precision components | -0.6% | Markets dependent on imported electronics | Short term (≤ 2 years) |

| Data ownership and cyber security concerns | -0.4% | North America and Europe | Medium term (2-4 years) |

| Tariff and trade policy shocks distort equipment pricing | -0.5% | United States–China and European Union–China corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost of Smart Machinery

A fully automated production line with moderate capacity requires a substantial financial investment, which limits its adoption among cooperatives in Bangladesh, where commercial interest rates are significantly high. Payment terms have been extended, creating additional financial strain on supplier balance sheets. Although leasing options are gradually emerging as an alternative, uncertainties about the equipment's long-term residual value reduce their overall attractiveness. Without broader access to structured financing solutions, the seed processing machinery market is likely to remain divided, with financially strong corporations dominating while smallholders continue to face limited access to credit.

Data Ownership and Cybersecurity Concerns

Cloud-based predictive maintenance portals transmit proprietary data on throughput and quality. Following the Cybersecurity and Infrastructure Security Agency's identification of vulnerabilities in Deere and Company’s Operations Center, processors have increasingly demanded on-premises storage and air-gapped modes to enhance data security. Compliance with the European Union General Data Protection Regulation has significantly increased hardware costs per installation, creating additional financial burdens for companies. Furthermore, a substantial proportion of European buyers expressed a willingness to pay higher prices for solutions that ensure local data custody. Without meaningful improvements to trust frameworks, stakeholder skepticism may limit the growth potential of smart factories in the seed processing machinery market.

Segment Analysis

By Machinery Type: Cleaners Anchor Multi-Stage Lines

Cleaners are the largest machinery type, accounting for 42.7% of the seed processing machinery market share in 2025, making them the single largest contributor to the market. Plants deploy air-screen units and gravity tables early in the flow to strip debris that would otherwise impair dryers, graders, and coaters. Their ubiquity ensures steady replacement demand. Mixed-flow dryers follow in value importance, drawing interest wherever harvest moisture exceeds storage thresholds. Meanwhile, separators, destoners, and polishers address crop-specific contaminants that can damage film coats or shorten shelf life. Taken together, these staples anchor long amortization schedules and embedded service contracts, stabilizing the seed processing machinery market.

Optical sorters are pacing the field with a 7.6% CAGR through 2031, the highest rate among equipment classes, thereby lifting the overall seed processing machinery market size. Capital costs continue to fall, and machine-learning models improve with every batch processed, tightening defect thresholds and curbing recalls. Hyperspectral imaging now identifies subtle mycotoxin footprints, allowing processors to charge premiums for food-safety-verified seed. As component shortages ease, mid-tier buyers in Asia-Pacific and South America will convert from mechanical color sorters, accelerating scale economies that reinforce the technology’s virtuous cycle.

Note: Segment shares of all individual segments available upon report purchase

By Operation Mode: Automation Narrows Labor Gaps

Automatic lines are the largest operating mode and accounted for 70.6% of the seed processing machinery market size in 2025, growing fastest at 8.0% CAGR during 2026-2031, reflecting their ability to slash headcount by two-thirds and boost uptime through predictive alerts. Integrated supervisory control and data acquisition platforms harmonize in-line cleaners, dryers, graders, and packagers, allowing a single technician to oversee entire shifts. High-wage regions such as Canada and Western Europe provide fertile ground because labor accounts for a majority of processing overhead. Consequently, automated systems enhance revenue visibility for manufacturers and expand the seed processing machinery market by capturing aftermarket analytics subscriptions.

Semi-automatic lines stay relevant in India, Nigeria, and parts of Southeast Asia, where plentiful labor and constrained capital tip the calculus. Manual bagging or visual grading stations reduce sticker prices versus fully automated peers, keeping the seed processing machinery market accessible to smallholders. Suppliers create modular skids so processors can upgrade piecemeal as cash flow improves, preserving installed-base loyalty.

By End-User: Commercial Seed Processing Plants Dominate while On-Farm Units Surge

Commercial seed processing plants are the largest end-users and captured 55.6% of the seed processing market share in 2025 due to superior economies of scale, which reduce per-metric-ton processing costs by up to 40% compared to decentralized networks. Bayer AG’s Indian greenfield facility and Corteva Agriscience’s North American upgrades showcase how multi-crop flexibility and optical sorting support brand differentiation. Because downtime incurs significant opportunity costs, these plants favor premium vendors with round-the-clock field service, thereby reinforcing the mid-to-high segment of the seed processing machinery market.

On-farm facilities, however, are the fastest growing at a 6.4% CAGR through 2031. Contract farming and organic certification encourage producers to process near the field to maintain identity preservation. Containerized plants from PETKUS Technologie GmbH (PETKUS Holding GmbH) can be transported between regional hubs, slicing logistics expense and protecting high-value heirloom varieties. As subsidy programs trim entry barriers, hundreds of micro-installations collectively add incremental lift to the seed processing machinery market size, even if each unit is modest.

Note: Segment shares of all individual segments available upon report purchase

By Capacity: Polarization between Mega-Plants and Micro-Lines

Systems above 10 metric tons/hour are the largest capacity and hold 63.5% of the seed processing machinery market share in 2025, driven by export-oriented hubs in Brazil, Argentina, and the United States. These configurations justify sophisticated automation, cosmopolitan spare-parts inventories, and contractual service levels. Their high utilization in peak season ensures rapid depreciation recovery, assuring steady demand for next-generation optics and internet-of-things add-ons, which keeps the lead in the seed processing machinery market.

Lines for less than 1 metric ton/hour are scaling rapidly at a 7.5% CAGR through 2031, as smallholder cooperatives, research institutes, and specialty crop nurseries invest in flexible, easily moved skids. Typical packages are priced within a broad range and offer a payback period of approximately 3 years when used for processing premium vegetable or organic seeds. Although the per-unit value is relatively modest, the aggregated volumes significantly contribute to the long tail of the seed processing machinery market, creating opportunities for future upselling.

Geography Analysis

North America is the largest geography and accounted for 34.1% of the seed processing machinery market in 2025, sustained by entrenched hybrid corn and soybean pipelines. Value-added producer grants covered up to half the cost of on-farm installations, encouraging adoption beyond integrated seed companies. The Comprehensive and Progressive Agreement for Trans-Pacific Partnership removed import duties on goods entering Canada, increasing brand options. Demand is primarily driven by replacement rather than greenfield capacity, with optical sorters and predictive-maintenance retrofits contributing significantly, enhancing the aftermarket annuity potential of the seed processing machinery market.

Asia-Pacific is expanding at an 8.1% CAGR through 2031, the fastest trajectory worldwide. India's electronic National Agriculture Market connects smallholders with institutional buyers, supported by a significant subsidy under the Agriculture Infrastructure Fund that reduces the effective cost of equipment to a more affordable range. China's objective to achieve a high level of mechanization in commercial seed production within the next few years is driving demand for both domestic brands and European specialists. Collaborations, such as the 2024 partnership between PETKUS Technologie GmbH (PETKUS Holding GmbH) and LOCAL Engineering, enhance service availability across countries like Indonesia, Thailand, and Vietnam, where hybrid rice cultivation is expanding. Furthermore, rising disposable incomes are driving higher demand for certified vegetable seeds, contributing to the overall growth of the seed processing machinery market.

Europe contributed a significant share of the projected 2025 sales, supported by the implementation of the Common Agricultural Policy's strategic plans, which effectively lower borrowing costs. The Farm to Fork strategy has necessitated a shift toward biological seed coatings, driving a replacement cycle for drum coaters that are incompatible with water-based films. Bühler AG's (ASKO Holdings) Grain Innovation Center in Germany enables processors to experiment with tailored configurations, reducing the risks associated with substantial investments. Challenges such as currency fluctuations and sanctions have made procurement in Russia more difficult, prompting suppliers to redirect their focus to Turkey and Eastern Europe. The region remains highly competitive, fostering innovation that has a significant impact on the global seed processing machinery market.

Competitive Landscape

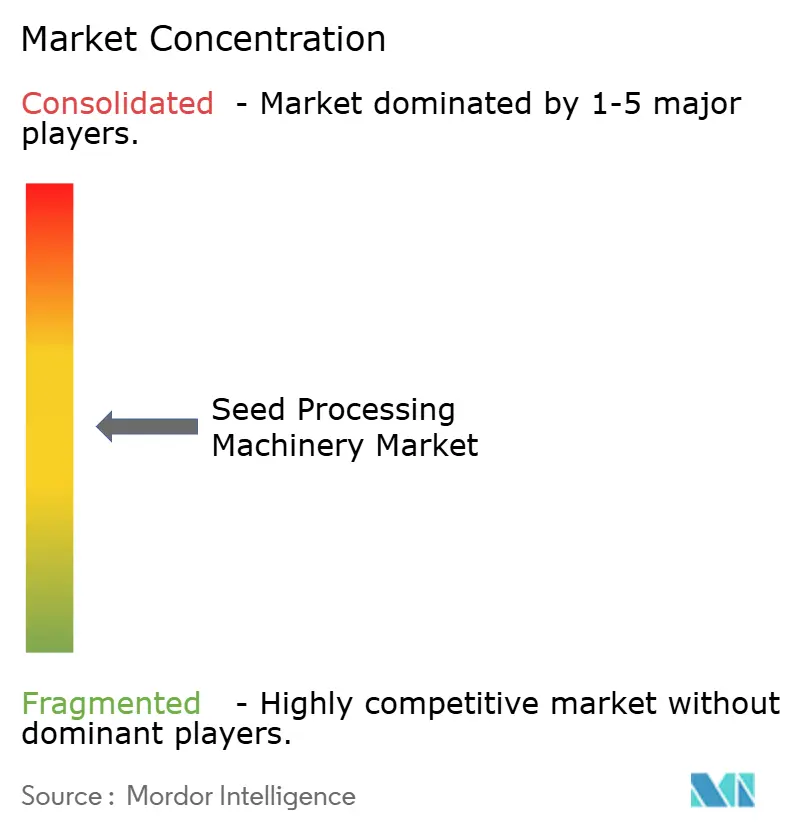

The seed processing machinery market is moderately fragmented. European leaders such as Bühler AG (ASKO Holdings), Cimbria A/S (American Industrial Partners), and PETKUS Technologie GmbH (PETKUS Holding GmbH) bank on advanced optics, modular plant architecture, and lifecycle service contracts to protect their share. North American specialists Ag Growth International Inc. and Bratney Companies emphasize retrofit kits that overlay internet-of-things telemetry on legacy equipment, extending functionality without full-line swaps. Their collective focus on high-specification engineering sustains premium pricing even as lower-cost Asian entrants nip at mid-tier niches.

Price-driven competition is intensifying in the small-capacity segment, where manufacturers from China and India are offering products at significantly lower prices compared to Western brands. In response, some European companies are setting up final assembly operations in regions with favorable tariff conditions to avoid the United States' duties. Mergers remain selective, as larger companies focus on acquiring smaller firms with expertise in biological coatings or advanced artificial intelligence software, rather than pursuing full consolidation. Initial trials of equipment-as-a-service models, where processors pay based on the volume of material handled, are gaining momentum in markets with limited capital availability. These models have the potential to transform revenue structures in the seed processing machinery market, provided that challenges related to residual value are effectively addressed.

Technological advancements in the seed processing machinery market are focused on hyperspectral optics and predictive analytics. Bühler AG (ASKO Holdings)'s SPARK sorter demonstrates high processing capacity, while PETKUS Technologie GmbH (PETKUS Holding GmbH)'s HySeed steam unit effectively eliminates pathogens without relying on chemical treatments, ensuring compliance with European regulations. Adherence to International Organization for Standardization (ISO) standards, such as ISO 9001 and ISO 14001, is increasingly becoming a critical requirement in tender processes. This trend is driving companies to improve their documentation practices and enhance energy efficiency measures. Overall, the pace of innovation and the range of service offerings are becoming significant factors influencing market momentum and shaping long-term value creation, beyond the scale of the installed base.

Seed Processing Machinery Industry Leaders

-

Bühler AG (ASKO Holdings)

-

Cimbria A/S (American Industrial Partners)

-

PETKUS Technologie GmbH (PETKUS Holding GmbH)

-

Satake Corporation

-

Ag Growth International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Elsoms Seeds has inaugurated a new seed processing facility, representing a substantial investment that underscores the company’s ongoing growth and dedication to providing high-quality seeds to growers and industry partners globally. The facility is equipped with advanced machinery designed to increase processing capacity, improve grading precision, enhance quality control, and enable customer-specific treatments, thereby adding value to the seeds.

- January 2026: Ashburton-based Carrfields has expanded its agricultural presence in New Zealand by becoming the national distributor for StocksAG machinery and acquiring Hinds Seed Cleaning. These developments, combined with new Manitou distribution rights and the opening of South Island branches, enhance their expertise in precision application, machinery, and seed processing.

- March 2025: Mediterranea Sementi, a leading Italian seed producer, collaborated with Cimbria A/S (American Industrial Partners) to establish advanced processing lines in Teramo and Ravenna. These lines are designed to ensure superior seed purity and high germination quality, with a focus on alfalfa. The equipment includes Cimbria's Delta Screen Cleaners, SEA.CX Optical Sorters, Gravity Separators, and Indented Cylinders, providing a weekly processing capacity of 1,000 quintals.

Global Seed Processing Machinery Market Report Scope

Seed processing machinery encompasses equipment used in agriculture to clean, sort, grade, dry, treat, and package seeds, improving their quality and viability for planting. These machines play a critical role in removing impurities, ensuring uniformity, and safeguarding seeds from pests and diseases. Seed Processing Machinery Market Report is Segmented by Machinery Type (Pre-Cleaners, Cleaners, Dryers, Graders, Coaters and Treaters, Separators and Destoners, Polishers, Optical Sorters, Seed Packagers, and Other Specialized Equipment), by Operation Mode (Automatic and Semi-Automatic), by End-User (Commercial Seed Processing Plants, Seed Producers, Research Institutions, On-Farm Facilities, and Grain Handling Facilities), by Capacity (Less Than 1 Metric Ton/Hour, 1–10 Metric Tons/Hour, and More Than 10 Metric Tons/Hour), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Pre-cleaners |

| Cleaners |

| Dryers |

| Graders |

| Coaters and Treaters |

| Separators and Destoners |

| Polishers |

| Optical Sorters |

| Seed Packagers |

| Other Specialized Equipment |

| Automatic |

| Semi-Automatic |

| Commercial Seed Processing Plants |

| Seed Producers |

| Research Institutions |

| On-Farm Facilities |

| Grain Handling Facilities |

| Less Than 1 Metric Ton/Hour |

| 1-10 Metric Tons/Hour |

| More Than 10 Metric Tons/Hour |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Machinery Type | Pre-cleaners | |

| Cleaners | ||

| Dryers | ||

| Graders | ||

| Coaters and Treaters | ||

| Separators and Destoners | ||

| Polishers | ||

| Optical Sorters | ||

| Seed Packagers | ||

| Other Specialized Equipment | ||

| By Operation Mode | Automatic | |

| Semi-Automatic | ||

| By End-User | Commercial Seed Processing Plants | |

| Seed Producers | ||

| Research Institutions | ||

| On-Farm Facilities | ||

| Grain Handling Facilities | ||

| By Capacity | Less Than 1 Metric Ton/Hour | |

| 1-10 Metric Tons/Hour | ||

| More Than 10 Metric Tons/Hour | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will automated optical sorters grow in the seed processing machinery market?

Optical sorters are projected to log a 7.6% CAGR through 2031 as falling component costs and demand for near-perfect defect detection persuade processors to upgrade.

Which region is projected to add the most new capacity?

Asia-Pacific leads with an 8.1% CAGR to 2031, buoyed by Indian and Chinese subsidy programs that cut equipment costs by up to 35%.

What financing tools help smallholders buy smart machinery?

Subsidized loans under India’s Agriculture Infrastructure Fund and Brazil’s Plano Safra, along with emerging pay-per-metric-ton equipment-as-a-service models, reduce up-front cash burdens.

Why are biological seed coatings influencing machinery design?

European pesticide reduction targets require water-based biological films that need precise 50–100 micron application, pushing demand for advanced coaters and inline quality sensors.

How severe are supply chain delays for precision components?

Lead times for hyperspectral cameras doubled to 26 weeks in early 2025, delaying shipments worth USD 25 million and forcing modular retrofit strategies.