Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

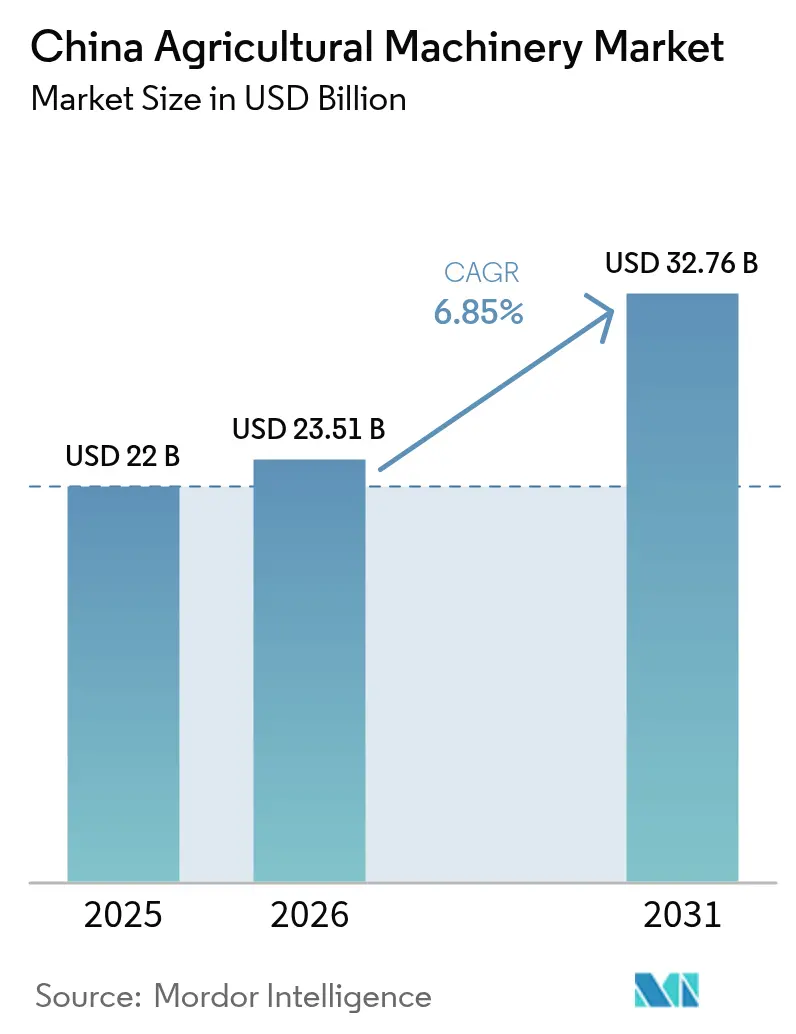

| Base Year Market Size (2025) | USD 22.0 Billion |

| Market Size (2026) | USD 23.51 Billion |

| Market Size (2031) | USD 32.76 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Agricultural Machinery Market Analysis by Mordor Intelligence

The China agricultural machinery market size was valued at USD 22.0 billion in 2025 and estimated to grow from USD 23.51 billion in 2026 to reach USD 32.76 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031). This growth is fueled by a strong policy drive to increase mechanization across crop production, accelerating the shift from manual labor to machine-based farming.[1]International Trade Administration, “China Agricultural Machinery Market,” trade.gov Government incentives for smart and high-powered tractors, along with strategic investment in digital infrastructure, are encouraging equipment upgrades. A shrinking rural workforce further amplifies demand for automation. Manufacturers benefit from favorable resource allocation, which helps stabilize supply chains and expand domestic production. Meanwhile, the rising adoption of IoT systems and autonomous technologies is unlocking new service-based revenue streams. However, fragmented landholdings, fluctuating input costs, and uneven access to credit continue to challenge profitability and limit uniform adoption across regions.

Key Report Takeaways

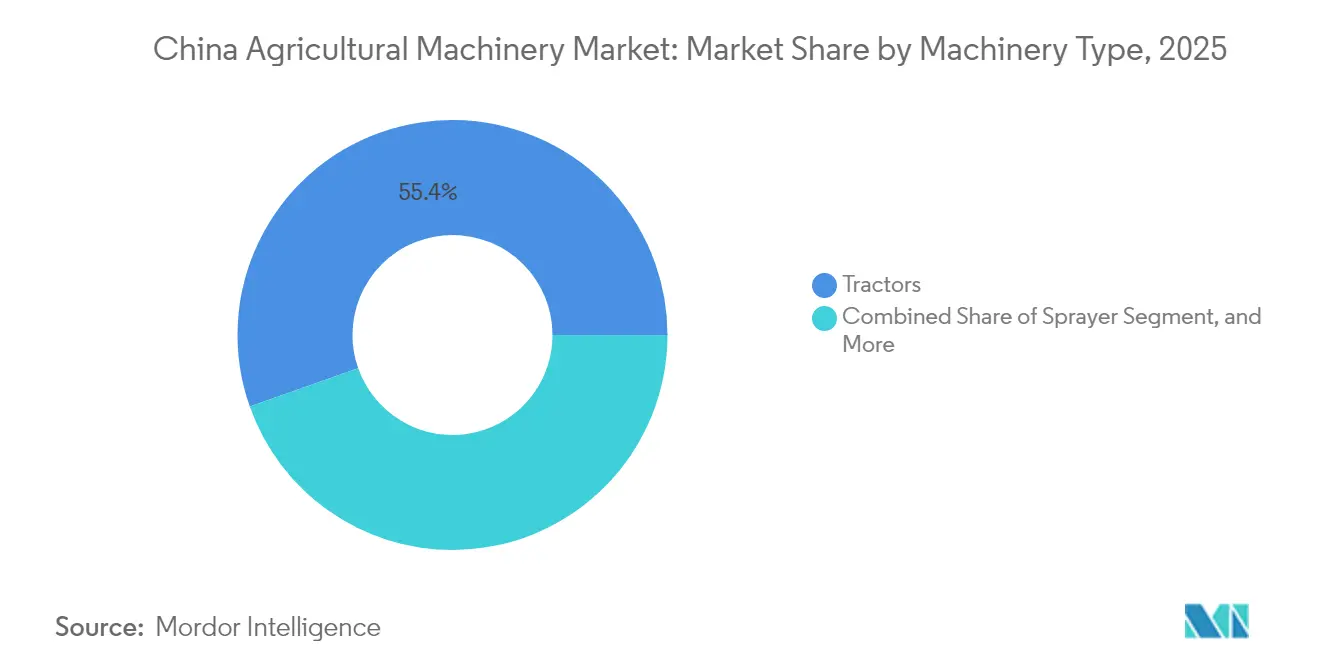

- By machinery type, tractors led with 55.40% of the China agricultural machinery market share in 2025, while sprayers are on track to post an 8.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Rural Labor Pool Accelerating Mechanization | +2.1% | National, with higher impact in eastern and central provinces | Medium term (2-4 years) |

| Generous Subsidies for High-horsepower and Smart Tractors | +1.8% | National, concentrated in major grain-producing areas | Short term (≤ 2 years) |

| Rapid Technology Upgrades | +1.5% | Eastern regions leading, expanding to central and western areas | Long term (≥ 4 years) |

| Food-security Push Raising Grain-output Targets | +1.2% | National, emphasis on major grain-producing provinces | Medium term (2-4 years) |

| AI-driven Predictive-maintenance Service Bundles | +0.9% | Eastern and central regions initially, gradual national rollout | Long term (≥ 4 years) |

| Adoption of Electric Power-trains | +0.7% | Pilot regions expanding to national coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shrinking Rural Labor Pool Accelerating Mechanization

China's agricultural sector is undergoing mechanization due to rural-urban migration and a declining agricultural workforce. China's urbanization rate reached 66.16% in 2023, an increase of 0.94% from the previous year, driven by youth migration from rural areas.[3]National Bureau of Statistics of China, “Statistical Communiqué of the People's Republic of China on the 2023 National Economic and Social Development,” stats.gov.cn This demographic shift has increased demand for automated equipment, including combine harvesters and precision planters. Government-supported service cooperatives enable smallholder farmers to access shared machinery. The mechanization trend is most prominent in coastal grain-producing regions, which experience higher urbanization rates and seasonal labor costs.

Generous Subsidies for High-horsepower and Smart Tractors

Government programs offer enhanced subsidies for high-horsepower, precision-ready tractors to encourage technology adoption. These initiatives support farmers in upgrading from older, low-horsepower equipment to modern systems. Trade-in programs reduce purchase costs, particularly benefiting regions with significant off-farm employment. The policy support has also strengthened domestic manufacturers' market position.

Rapid Technology Upgrades

China's smart agriculture initiatives are accelerating the implementation of digital tools and autonomous machinery. Modern agricultural equipment incorporates satellite navigation, drones, and AI-powered monitoring systems.[2]Zhang X., “Guidance on Smart Agriculture,” gov.cn Testing of neural-network yield prediction and 5G-enabled tractors demonstrates improvements in operational efficiency. Equipment manufacturers are expanding into integrated data services, implementing cloud-based dashboards and smart sensors. This technological advancement enables farmers to implement data-driven crop management strategies.

Food-security Push Raising Grain-output Targets

National food security policies are increasing the demand for large-scale agricultural machinery. Targets for high grain output drive investments in combines, seeders, and precision sprayers. Major crop-producing provinces are implementing mechanization programs, supported by long-term research initiatives and direct subsidies. Specialized zones focus on seed technology innovation, contributing to production stability and efficiency improvements in key agricultural regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Uneven Credit Access | -1.4% | National, more severe in western and remote regions | Short term (≤ 2 years) |

| Fragmented Farm Plots Lowering Operational Efficiency | -0.8% | National, particularly affecting central and southern regions | Medium term (2–4 years) |

| Volatile Raw-material and Battery Prices | -1.1% | National, with higher sensitivity in industrial belts | Short to medium term (1–3 years) |

| Farmer Data-privacy and Cyber-security Concerns | -0.6% | Emerging in digitally active zones, especially northern and urban regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Uneven Credit Access

Advanced agricultural machinery costs present significant challenges for small-scale farmers. Limited financial resources and inconsistent rural credit access restrict equipment purchases. While insurance programs improve risk assessment, agricultural loan availability varies by region. Machinery outsourcing services provide an alternative but have limited reach in remote and mountainous areas. The lack of comprehensive financial solutions continues to impede operational upgrades.

Fragmented Farm Plots Lowering Operational Efficiency

The prevalence of small, dispersed agricultural plots in China reduces the efficiency of high-powered machinery operations. Despite expanding land-transfer programs, farmers often resist land consolidation efforts. This fragmentation affects the economic feasibility of large equipment investments and slows mechanization progress. Current land arrangement practices limit the optimal utilization of advanced machinery across many agricultural zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Dominance of Tractors Underpins the Smart-farming Pivot

Tractors account for 55.40% of the China agricultural machinery market share in 2025. Large-frame units are increasing in popularity due to farm consolidation, while two-wheel-drive models remain predominant in existing fleets. Government incentives support the transition to four-wheel-drive CVT platforms that accommodate multi-function implements. The tractor segment shows steady growth potential through technology integration, though smaller manufacturers struggle to meet software requirements, making them potential acquisition targets.

Sprayers demonstrate the highest revenue growth at an 8.4% CAGR through 2031, driven by environmental regulations and variable-rate technology adoption. Domestic manufacturers are combining ground sprayers with unified control systems using BeiDou navigation to minimize chemical waste. Harvesting equipment volumes continue to increase, particularly in wheat-producing regions, despite pricing pressures in lower-horsepower segments. Guidance systems, telematics, and predictive maintenance capabilities are becoming standard features across machinery types.

Geography Analysis

Eastern provinces such as Jiangsu, Zhejiang, Shandong, and Fujian demonstrate higher agricultural mechanization rates due to higher incomes, flat terrain, and established service ecosystems. These coastal producers benefit from efficient logistics and spare-parts networks, ensuring optimal fleet availability during peak seasons. Central provinces, including Henan, Anhui, and Hubei, function as transitional zones, where mechanization advances through service cooperatives and equipment-sharing models.

Western regions, including Sichuan, Yunnan, Gansu, and Xinjiang, show lower mechanization rates due to challenging topography and fragmented land holdings. While government initiatives fund farmland improvement projects for terracing and plot consolidation, adoption remains limited. Restricted access to agricultural credit further limits machinery purchases. The mechanization progress in eastern provinces influences neighboring regions, though geographic disparities continue.

Regional variations also influence pest-control approaches. Provinces with centralized monitoring systems implement UAV sprayers more effectively, improving chemical application precision and crop yields. Southern provinces, including Guangxi and Guangdong, prefer aerial sprayers for paddy fields, while northern regions such as Inner Mongolia and Hebei utilize ground sprayers with gasoline engines due to climate conditions. These regional requirements influence manufacturers' equipment development strategies.

Regulatory Landscape

China's agricultural machinery demand is shaped by subsidy rules administered by the Ministry of Agriculture and Rural Affairs (MARA) and the Ministry of Finance under the 2024-2026 framework, which sets central fiscal maximum subsidy amounts and uses fleet-structure optimization tools such as "superior machinery, superior subsidies" and entry-exit mechanisms. The subsidy catalog was broadened in 2025 with additional machinery categories (including plant protection drones and grain dryers), reinforcing policy-backed pull for higher-spec equipment rather than basic replacements.

Compliance requirements are tightening around safety and intelligent-operation standards. The mandatory national safety standard GB 18447-2025 (Safety Technical Specifications for Tractors) takes effect on July 1, 2026 and extends coverage beyond tractors to include combine harvesters and mechanical plant protection equipment, raising the bar for new equipment placed on the market. In parallel, voluntary national standards such as GB/T 46268-2025 and GB/T 46270-2025 for BeiDou (BDS)-based operation monitoring and automatic driving systems support the push for connected and autonomous features, while policy guidance under the 15th Five-Year Plan for accelerating agricultural and rural modernization (issued in June 2026) emphasizes intelligent and hill-mountain machinery development and links performance to subsidy outcomes through "best machine for best subsidy" principles.

Competitive Landscape

The China agricultural machinery market share comprises established state enterprises, international companies, and emerging domestic manufacturers. Sinomach-China National Machinery Industry Corporation (YTO Group Corporation) maintains market presence through integrated manufacturing capabilities and government relationships, supporting national mechanization initiatives. Zoomlion Heavy Industry Science and Technology Co., Ltd. focuses on technological advancement, investing international revenues in AI systems and maintenance platforms.

International manufacturers Kubota Corporation and Deere & Company expand local assembly and service operations despite policies favoring domestic digital systems. CNH Industrial N.V. emphasizes precision agriculture technology, incorporating data capabilities into equipment. AGCO Corporation and CLAAS KGaA mbH concentrate on specialized segments, including advanced harvesters and planting equipment, offering solutions for specific agricultural applications.

Domestic manufacturers such as Jiangsu Changfa Group and Weichai Group (Shandong Heavy Industry Group Co., Ltd.) are expanding through industry partnerships and research collaborations, particularly in areas like BeiDou integration and electric tractor systems. Competition is increasingly centered on technological strength, with companies building cloud platforms, developing analytics services, and securing patents to differentiate themselves from one another. Achieving strong outcomes requires continuous innovation, robust connectivity, and the ability to adapt to evolving market conditions.

China Agricultural Machinery Industry Leaders

Sinomach-China National Machinery Industry Corporation (YTO Group Corporation)

Zoomlion Heavy Industry Science and Technology Co., Ltd.

Kubota Corporation

Deere & Company

Weichai Group (Shandong Heavy Industry Group Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-driven upgrading creates whitespace in high-horsepower, smart, and terrain-adapted equipment portfolios as the 2024-2026 subsidy framework steers demand toward higher-performing models via differentiated subsidy treatment and tighter catalog management. The June 2026 State Council 15th Five-Year Plan anchors opportunities around high-end intelligent machinery, new-energy agricultural equipment, and machinery suited to hilly and mountainous regions, aligning product development with areas where current mechanization gaps and terrain constraints limit utilization of large conventional equipment.

A second opportunity track is the shift from standalone machines to integrated digital and service offerings that bundle connectivity, automation, and agronomic execution. MARA reporting on spring 2026 farming highlighted adoption of integrated digital solutions and AI-enabled equipment such as pneumatic intelligent seeding systems with onboard computing for precise depth and seeding-volume control, signaling practical on-farm use cases for precision planters, guidance, telematics, and monitoring packages. With national grain-production objectives emphasized in policy (around the 700 million metric ton level referenced in the 2026 policy outlook) and an ongoing focus on raising the agricultural science and technology contribution rate (above 64% as of 2025), manufacturers and service cooperatives have room to scale offerings that improve timeliness and accuracy of planting, spraying, and harvesting operations, particularly where labor scarcity and fragmented plots favor shared-use models and outcome-linked upgrades.

Recent Industry Developments

- June 2026: Zoomlion debuted seven high-end hybrid and power-shift tractors at the Elders FarmFest in Queensland, Australia, marking its entry into the Australian market. The launch extended its portfolio of higher-spec tractors in a market with demanding performance and service requirements, supporting brand positioning for hybrid powertrains and advanced transmissions.

- April 2026: YTO Group Corporation and China Machinery Engineering Corporation (CMEC), both under Sinomach, delivered 30 YTO tractors to the Republic of the Congo as part of an integrated agricultural machinery and technical service project. The structure moved beyond unit exports into bundled equipment plus services, strengthening after-sales capability and operator support as part of international delivery models.

- October 2024: ComNav Technology launched its agricultural machinery solutions at the 2024 China International Agricultural Machinery Exhibition, showcasing autosteering systems aimed at improving field efficiency and reducing labor intensity. The product emphasis reinforced the market shift toward guidance and precision add-ons that can be retrofitted or bundled with new equipment to raise utilization and performance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the value of agricultural machinery sold and used for farm operations in China, covering equipment used for land preparation, planting, crop care, harvesting, and forage handling, measured in USD at the point of sale.

Scope exclusions: It excludes used equipment resale, spare parts and routine servicing revenue, and machines used mainly for construction or non-farm industrial work.

Segmentation Overview

- By Machinery Type

- Tractors

- 25-100 HP

- Above 100 HP

- Equipment

- Plows

- Harrows

- Rotovators and Cultivators

- Seed and Fertilizer Drills

- Fertilizer Spreaders

- Other Equipment

- Sprayers

- Field-crop Sprayers

- Orchard Sprayers

- Other Sprayers

- Harvesting Machinery

- Combine Harvesters

- Forage Harvesters

- Other Harvesting Machinery

- Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

- Other Agricultural Machinery

- Tractors

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the China demand context and to anchor the model with official time series that can be checked year to year. We referenced public sources such as the National Bureau of Statistics of China, UN Comtrade trade flows, FAOSTAT crop and farm structure indicators, World Bank macro series, and customs and tariff schedules where machinery categories are clearly mapped.

On the industry side, filings and investor materials from listed machinery makers, distributor announcements, and agriculture association publications were reviewed to understand product mix changes, pricing direction, and subsidy signals. For cross-checks, we also used paid subscriptions for company financials and news screening, plus a shipment-level trade database when import and export movements had to be reconciled with local production. The desk sources listed here are illustrative only, and we reviewed many other public references to validate assumptions and clarify gaps.

Primary Interviews and Surveys

Primary work focused on converting broad mechanization trends into practical sizing inputs, especially where public data is delayed or not consistent by machine category. We interviewed and surveyed a mix of OEM-side experts, dealers, large farm operators, service contractors, and policy-linked stakeholders across major grain, cash-crop, and horticulture provinces, then used their inputs to confirm replacement cycles, typical equipment bundles, and pricing movement.

Field feedback was also used to pressure-test adoption differences between smallholder areas and large-scale farming clusters, before finalizing assumptions that sit behind volumes, average selling prices, and the split between new purchases and replacements.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 30% | |

| Smaller Players: 20% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where China cropping patterns, cultivated area, mechanization intensity, and replacement demand are translated into annual equipment demand pools by major machinery groups, then expressed in value using observed price bands. Once this structure is stable, we use selective bottom-up checks to confirm the totals, such as dealer sell-through checks, import and export sanity checks, and limited supplier roll-ups in categories where reporting is clearer.

Key inputs that materially move the model include tractor horsepower mix shifts, combine and forage harvester penetration in core grain belts, subsidy focus by equipment type, rural labor availability signals, and the pace of farm consolidation (which affects utilization and replacement timing). Forecasts are built using scenario analysis supported by near-term demand signals from primary interviews, and then adjusted for expected price progression where higher-spec machines take share. Where direct visibility is weaker, gaps are handled through proxy indicators like cropped-area trends and equipment-to-hectare ratios, which were validated with channel participants.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the totals remain consistent with independent signals like trade movements, production proxies, and the direction of subsidy support. When the model shows unusual jumps in a category or an unrealistic price change, we review the relevant assumptions again and trigger clarifying calls with the appropriate respondents.

Before sign-off, a second analyst reviews the calculation logic, and any variances against prior editions are documented with the driver that caused the change. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy shifts, sharp commodity price moves, or abrupt demand changes. Right before delivery, a final sweep is done to ensure the latest public releases and field feedback are reflected.

Mordor Intelligence's China Agricultural Machinery Market Sizing Compared With Other Published Estimates

Different published market values for China agricultural machinery can vary even when the topic name looks identical, because the scope and counting rules are not always aligned. The biggest differences usually come from what is treated as agricultural machinery revenue, how pricing is averaged across horsepower and equipment classes, and whether the estimate is tied to realistic replacement cycles.

Some estimates fold in adjacent revenue like irrigation infrastructure projects, telematics services, or aftermarket parts, which lifts totals even if unit demand is unchanged. Other gaps come from using aggressive price escalation, mixing manufacturer output with end-market sales, or applying a single growth curve across all equipment types without checking subsidy focus and regional crop patterns. The spread narrows when the sizing is tied to cultivated-area demand pools and replacement timing by machine type, which is how the 2025 total is constructed here, a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 22.00 B (2025) | |

| Regional Consultancy A | USD 21.80 B (2025) | Uses a similar equipment list but appears to apply a faster near-term growth ramp and a broader channel view that can blend factory dispatch with retail sales in some categories. |

| Trade Journal B | USD 25.80 B (2025) | Likely includes adjacent buckets such as smart and precision add-ons and parts-like spend, and may use higher blended ASP assumptions without separating horsepower mix shifts by tractor class. |

Across the three figures, most of the gap is explained by what gets counted as core equipment sales versus add-on and aftermarket spend, and by how mix-driven pricing is treated. By keeping the demand pool tied to farming activity and checking it against practical replacement behavior, the estimate stays traceable to simple variables that can be reviewed and repeated each year.

Key Questions Answered in the Report

What is the current China agricultural machinery market size, and how is it projected to grow by 2031?

It stands at USD 23.51 billion in 2026 with a 6.85% CAGR heading toward USD 32.76 billion in 2031.

Which machinery type contributes the most revenue?

Tractors deliver 55.40% of market revenue, supported by high-horsepower upgrades and smart features.

How does government policy influence equipment demand?

Subsidies, trade-in programs, and the Smart Agriculture Action Plan lower acquisition costs and accelerate adoption of IoT-enabled machines.

What restraints limit growth?

High upfront costs combined with uneven rural credit access and fragmented land parcels reduce machinery utilization and delay purchases.

Page last updated on: