Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 9.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seed Coating Materials Market Analysis by Mordor Intelligence

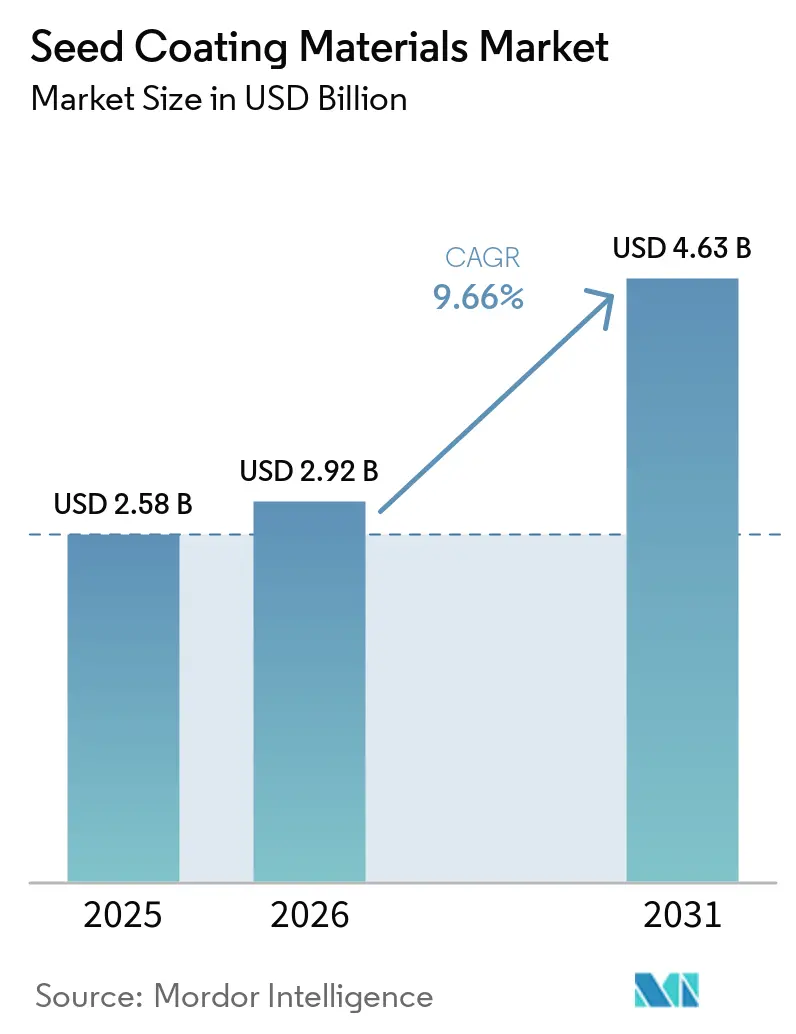

The seed coating materials market size was valued at USD 2.58 billion in 2025 and estimated to grow from USD 2.92 billion in 2026 to reach USD 4.63 billion by 2031, at a CAGR of 9.66% during the forecast period 2026-2031. The rising commercialization of treated hybrid seeds and the stronger grower focus on uniform seedbed establishment continue to support the seed coating materials market. The seed coating materials market is also moving away from basic color identification layers toward multifunctional systems that combine seed protection actives, biological inoculants, and micronutrient packages in one application step. Procurement standards at major seed companies are shifting from simple price comparison to performance validation, especially where planter flow, dust-off control, and biological compatibility now shape supplier selection. Regulatory pressure in Europe is pushing bio-based reformulation, while similar product and certification expectations are beginning to influence Asia, Brazil, China, and Germany through tighter coating quality standards. Competitive advantage increasingly favors established formulators with proprietary compatibility testing, porosity engineering, regulatory depth, and embedded positions in certified seed supply chains, while cost pressure from microplastic-compliant reformulation remains the most immediate margin risk.

Key Report Takeaways

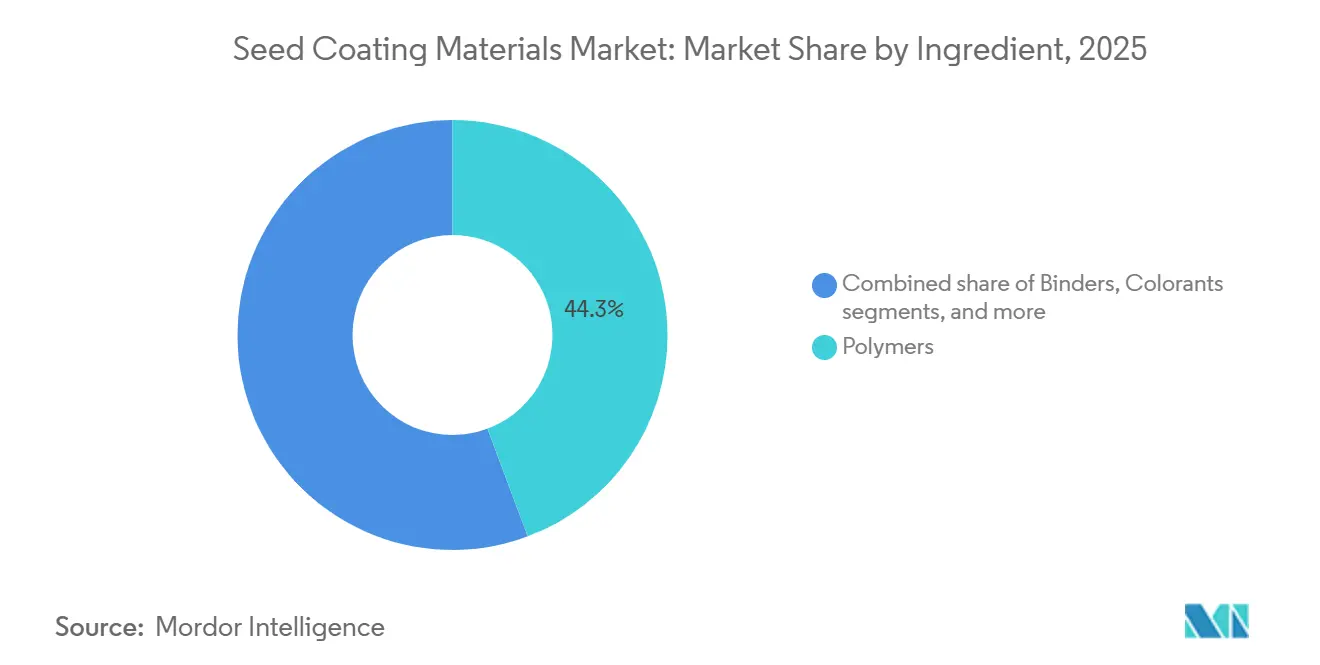

- By ingredient, polymers held the largest segment, accounting for 44.3% of the seed coating materials market share in 2025, while binders will grow the fastest at 11.2% CAGR during 2026-2031.

- By form, liquid was the largest segment with a 60.5% share in 2025, while solid will be the fastest-growing segment at a 10.2% CAGR during 2026-2031.

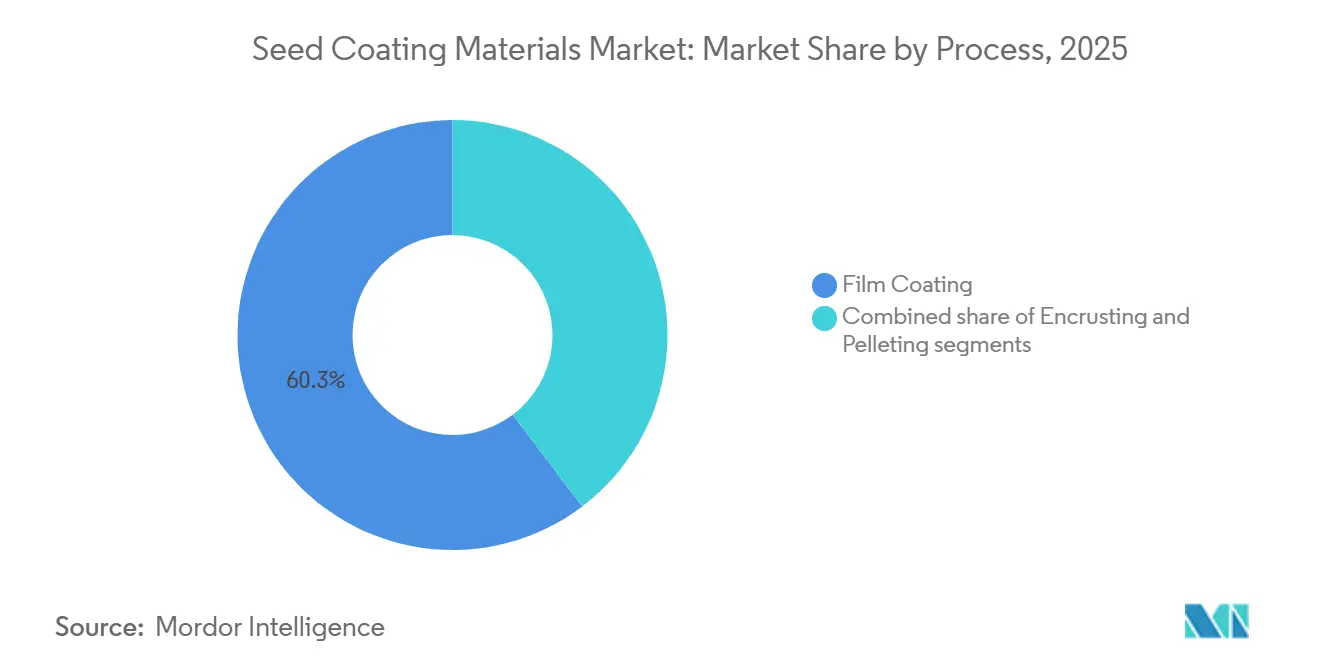

- By process, film coating was the largest segment, accounting for 60.3% of revenue in 2025, while pelleting is projected to be the fastest-growing segment at a 10.6% CAGR during 2026-2031.

- By function, seed protection was the largest segment, accounting for a 77.8% of the seed coating materials market size in 2025, while seed enhancement is anticipated to be the fastest-growing segment, with a 11.0% CAGR during 2026-2031.

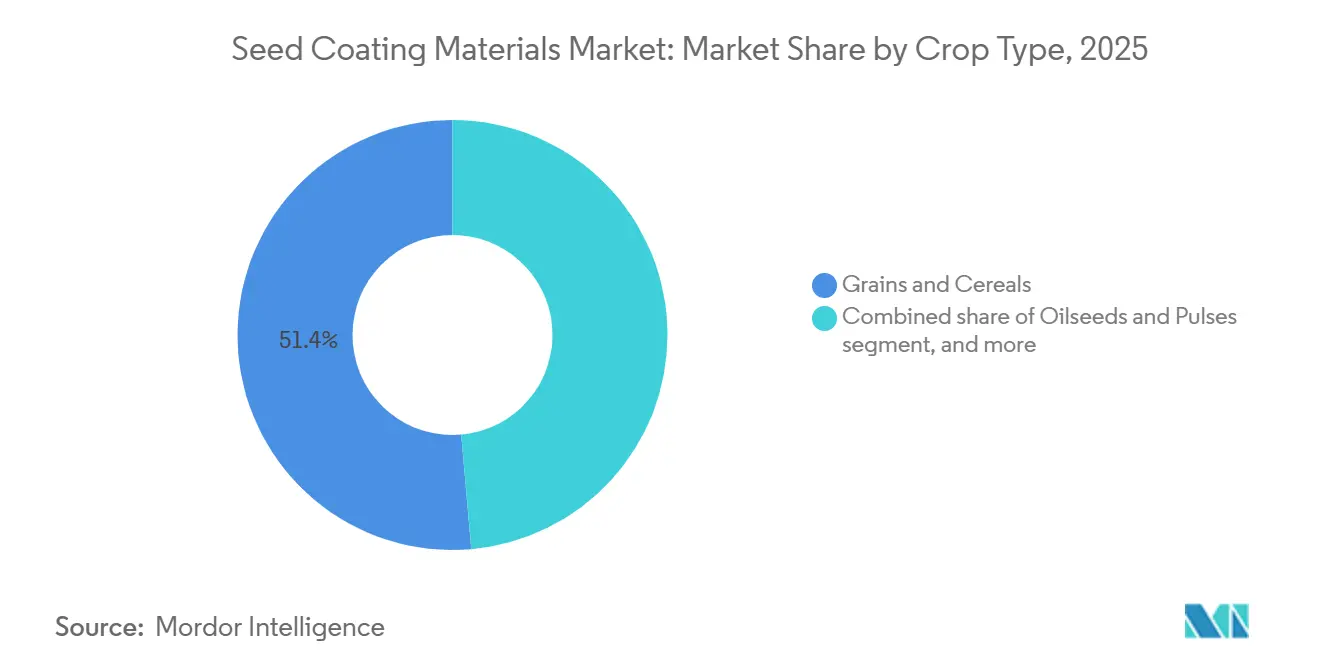

- By crop type, grains and cereals were the largest segment, with a 51.4% share in 2025, while fruits and vegetables will be the fastest-growing segment, with an 11.1% CAGR during 2026-2031.

- By coating type, synthetic was the largest segment with 71.9% share in 2025, while bio-based is the fastest segment at 11.6% CAGR during 2026-2031.

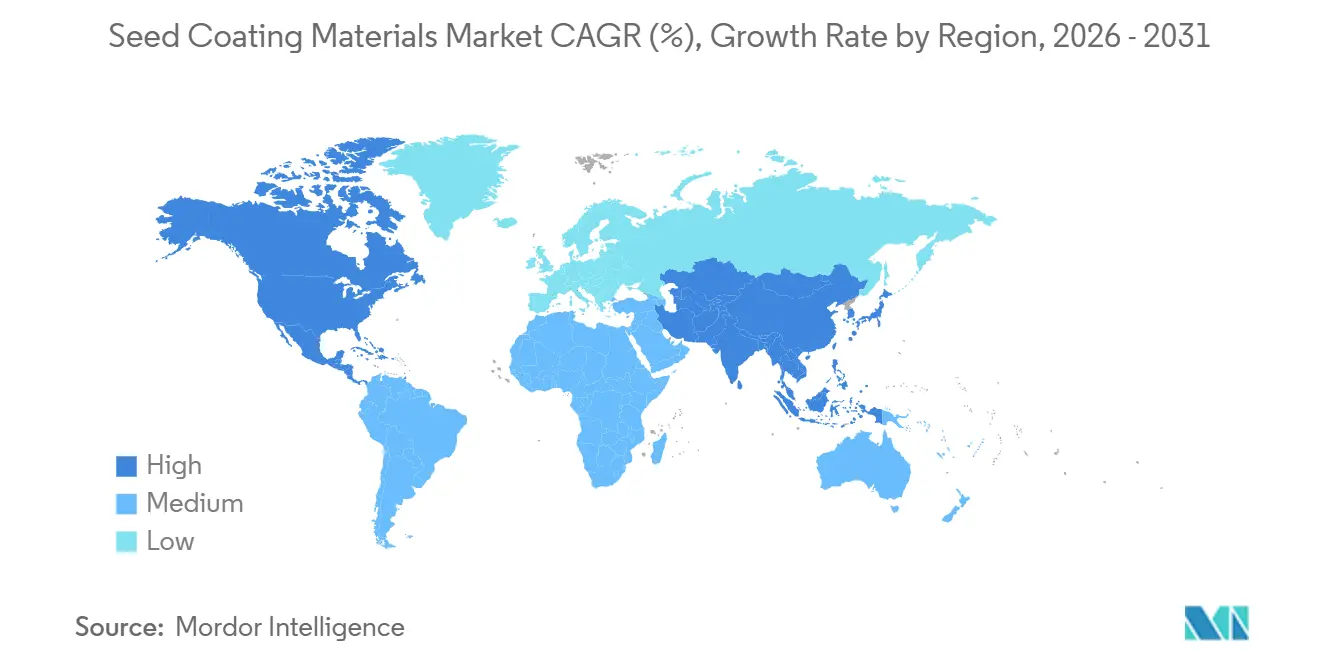

- By geography, North America was the largest segment with 43.7% share in 2025, while Asia-Pacific will be the fastest segment at 10.9% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Seed Coating Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Coated Hybrid and Premium Seeds | +2.50% | Strongest in North America and Europe, with growing hybrid seed demand in China | Short term (≤ 2 years) |

| Precision Planting and Plantability Requirements | +1.80% | High relevance in North America and Europe, with rising adoption in Brazil and Argentina | Medium term (2-4 years) |

| Shift toward Biodegradable and Microplastic-Free Coatings | +1.60% | Led by Europe, with increasing influence across Asia-Pacific | Medium term (2-4 years) |

| Growth of Seed-Applied Biologicals and Micronutrient Loading | +1.50% | Strong traction in North America, Brazil, and key soybean-growing regions | Long term (≥ 4 years) |

| Compatibility Demand from Complex Active Ingredient Packages | +1.10% | Most relevant in North America and Europe, with growing use in India and China | Medium term (2-4 years) |

| Need for Crop-Specific Coatings for Irregular and Sensitive Seeds | +0.90% | Prominent in Asia-Pacific, Europe, and South America horticulture markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Coated Hybrid and Premium Seeds

The proportion of commercial seed sold in pre-coated form has continued to rise across major crops, supporting steady volume growth in the seed coating materials market. Hybrid corn, sunflower, and canola programs now routinely specify film-coated seed with colorant, fungicide, and flow agent as a delivery standard across North America and Western Europe. This makes coating demand less dependent on short-term grower spending decisions because it is tied directly to seed production volume and contract supply. A May 2025 assessment published in Legume Research reported that pre-coated seed lots delivered 12-18% higher germination uniformity than bare seed in controlled planting trials, further strengthening the case for coated seed in commercial procurement standards. In April 2025, the Mudanjiang City Agriculture Bureau in China also mandated coating uniformity thresholds for distributed hybrid rice seed lots, showing that minimum performance expectations are rising beyond Western markets[1]Source: Mudanjiang City Agriculture Bureau, “Hybrid Rice Seed Coating Uniformity Requirements,” mudanjiang.gov.cn.. With the expansion of hybrid seed penetration and the standardization of coated delivery formats by seed suppliers, the global demand for advanced binders, polymers, pigments, and flow-enhancing materials in the seed coating materials market is anticipated to grow steadily.

Precision Planting and Plantability Requirements

High-speed pneumatic planters with optical seed-singulation sensors have raised the minimum performance standard for coating consistency, pushing the seed coating materials market toward higher-value formulations. Variability in coating thickness, surface texture, or dust-off rate can cause sensor misreads and seeding gaps, making planter compatibility a direct commercial requirement for large seed programs. That shift is separating generic film-coat suppliers from formulators that can demonstrate consistent viscosity control, clean flow behavior, and low dust release under commercial planting conditions. High-speed precision planting systems have increased demand for low-dust, abrasion-resistant seed coatings because planter performance is increasingly tied to coating flowability and singulation consistency. Coated corn seed linked dust-off behavior and coating mechanical properties directly with planter performance outcomes, accelerating demand for advanced polymer-based seed coating formulations.

Shift toward Biodegradable and Microplastic-Free Coatings

The shift toward biodegradable, microplastic-free formulations is influencing raw-material priorities in the seed-coating market. The European Union Regulation 2023/2055 restricts the use of intentionally added synthetic polymer particles that release microplastics into soil, driving reformulation efforts across the polymer and binder categories. The European Chemicals Agency has provided additional guidance through 2025, outlining implementation requirements, including timelines for derogations and applications requiring earlier reformulation. This guidance offers suppliers a clearer roadmap for technology development and compliance. Consequently, the development of biodegradable polysaccharide- and protein-based coating systems is gaining momentum as seed companies and formulators prioritize lower-emission alternatives to traditional synthetic binders while ensuring coating durability, flowability, and dust-control performance. Germany’s Agency for Renewable Resources extended biodegradable seed-coating research grants in August 2025, indicating continued public support for alternative development[2]Source: Agency for Renewable Resources, “Bioeconomy Research Grants for Biodegradable Seed Coating Development,” fnr.de.. Such funding initiatives are driving advancements in biodegradable agricultural input technologies, including next-generation sustainable formulations for the seed coating materials market.

Growth of Seed-Applied Biologicals and Micronutrient Loading

Biological inoculants, mycorrhizal fungi, biopesticide actives, and micronutrient packages are driving the demand for advanced coating matrices, creating growth opportunities in the seed coating materials market. Unlike traditional chemical seed treatments, biological formulations require coating systems that preserve microbial stability during storage while withstanding drying, mechanical handling, and pneumatic planting conditions without compromising germination performance. A 2024 study published in the International Journal for Multidisciplinary Research examined Bacillus and Azospirillum-based biofertilizer seed coatings and found that hydroxypropyl methylcellulose and dextrin film-coating systems enhanced microbial retention, seedling vigor, and rhizosphere colonization during storage and post-planting development. As biological seed treatments transition from specialty applications to large-acreage row crops, coating suppliers are increasingly tasked with developing multi-functional formulations that stabilize living microorganisms, support higher micronutrient loading, and maintain planter-compatible flow performance. This trend is driving demand for advanced polymer and binder technologies in the seed coating materials market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Reformulation Cost under Microplastic Restrictions | -2.20% | Most acute in Europe, with global impact on multinational product portfolios | Short term (≤ 2 years) |

| Biological Viability and Shelf-Life Limitations | -1.50% | Strongest in Brazil, India, and Southeast Asia due to warm supply chain conditions | Medium term (2–4 years) |

| Dust-off and Abrasion Compliance Challenges | -1.00% | Most visible in North America and Europe, with rising relevance in China | Medium term (2–4 years) |

| Coating Thickness Trade-off with Germination and Gas Exchange | -0.70% | Important across global horticulture and small-seeded crop programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Reformulation Cost under Microplastic Restrictions

The most immediate cost restraint in the seed coating materials market comes from the need to reformulate polymer and binder systems away from restricted synthetic materials. A full reformulation cycle involves application testing, planter compatibility validation, and regulatory documentation, and that process can stretch across 18-36 months. Mid-tier and regional suppliers may not have the research capacity or balance sheet to complete those cycles as quickly as larger companies. Croda International Plc stated in its 2025 annual report that research and development investment in biodegradable seed enhancement formulations increased within its Incotec Group BV business unit, which reflects the scale of work required to maintain compliant portfolios[3]Source: Croda International Plc, “Annual Report 2025,” Croda International Plc, croda.com.. The seed coating materials market is also facing margin pressure because bio-based alternatives currently carry a 30-60% premium over conventional synthetic polymers, and that cost cannot always be passed to seed company customers. Hence, the seed coating materials market is entering a phase in which compliance-driven reformulations, rising raw material costs, and prolonged validation cycles are intensifying competitive pressures and creating higher barriers to entry, especially for suppliers lacking advanced formulation and regulatory expertise.

Biological Viability and Shelf-Life Limitations

Shelf-life limitations of biologically-loaded systems continue to pose a significant challenge in the seed coating materials market. Many commercially important rhizobacterial and fungal species experience rapid viability loss when exposed to elevated temperatures and humidity, particularly during extended storage periods beyond short distribution windows. This issue is especially critical in tropical and subtropical supply chains, where ambient storage temperatures often exceed the optimal range for microbial survival, and cold-chain infrastructure is frequently inadequate. A 2024 study published in the South African Journal of Botany evaluated cyanobacteria-based microbial seed coatings for chickpea and found that storage duration, coating composition, and environmental conditions significantly influenced microbial survivability, seed germination, and vigor retention during post-treatment storage. These findings underscore that there is still room to grow focus within the seed coating materials market on developing moisture-regulating binders, protective encapsulation systems, and temperature-tolerant polymer technologies to enhance biological shelf stability during commercial distribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Polymers Lead but Binders Gain Formulation Centrality

Polymers accounted for 44.3% of the seed coating materials market size within ingredient segments in 2025, making them the largest segment, as they remain the primary film-forming and carrier matrix across film coating, encrusting, and pelleting applications. Their position reflects long-standing formulation standardization around polyvinyl acetate, polyacrylate, and cellulose-based systems that provide the structural base for most commercial coating designs. Colorants, active ingredients, minerals, pumice, and other additives continue to play important roles in seed identification, flow improvement, and direct treatment delivery, but their demand remains tied to the polymer layer that holds the system together. This pattern keeps the seed coating materials industry centered on polymer performance even as customer specifications become broader and more technical. The strength of polymers in the seed coating materials market also reflects their ability to serve both large-volume grain programs and more specialized horticulture applications through formulation adjustments rather than full-process redesign.

Binders are the fastest-growing ingredient segment, with a 11.2% CAGR during 2026-2031, as coating systems carry greater biological and micronutrient payloads and require tighter control over suspension stability, adhesion, and viscosity. That is changing the role of binders from basic adhesion aids into active performance drivers within multifunctional systems. As formulation complexity rises, the seed coating materials market share held by binders is anticipated to expand, as more projects depend on reliable mixing, holding, and delivery across different crop and process combinations. The ingredient structure of the seed coating materials market is therefore becoming more performance-led, even though polymers still account for the largest current revenue base.

By Form: Liquid Systems Anchor Volume, Solid Pelleting Commands a Growth Premium

Liquid formulations accounted for 60.5% of the seed coating materials market share by form in 2025, making them the largest segment because they fit standard drum and pan coating equipment used in large commercial seed treatment facilities. Liquid systems allow continuous adjustment of application rate and solids loading without major equipment changeover, which is important for large grain and oilseed programs. This operational flexibility keeps liquids well-positioned across North and South America, where high-throughput processing is a core requirement. The seed coating materials market has therefore retained a strong liquid bias in volume terms, even as customers seek more specialized outcomes. That volume base is also reinforced by the fact that many large-seed crops do not require the heavier build and geometric transformation associated with solid pelleting systems.

Solid form coatings are the fastest-growing segment, with a 10.2% CAGR during 2026-2031, because horticulture and specialty crops require precise pellet structure, size consistency, and controlled handling. Demand is particularly strong in Europe, Japan, and South Korea, where smaller seeds and protected agriculture programs make pelleting more common. Recent research published in Seed Science and Technology in 2025 showed that pelleting filler composition significantly affects pellet stability, humidity tolerance, and sowing performance in small-seeded vegetable crops, with zeolite-, vermiculite-, and calcium-based systems outperforming several conventional clay-heavy formulations. This is accelerating the shift toward higher-value engineered solid coating materials in the seed coating materials market, particularly for vegetable and horticultural seeds where precision sowing and automated transplanting require greater pellet uniformity and flow consistency.

By Process: Film Coating Holds the Volume Base, Pelleting Outpaces on Rate

Film coating accounted for 60.3% of the seed coating materials market by process in 2025, making it the largest segment because it works across the widest range of crop types and ingredient combinations. Its thin, uniform application layer suits seeds that already have an acceptable size and shape for planting, including most commercial grain, oilseed, and large-seeded vegetable programs. That flexibility has made film coating the default process for high-volume programs where throughput, treatment retention, and cost control must all remain balanced. The seed coating materials market continues to rely on this process because it offers the broadest applicability without requiring major physical transformation of the seed. Encrusting remains important in selected specialty uses, but its role is narrower than that of film coating and pelleting.

Pelleting is the fastest-growing segment, with a 10.6% CAGR during 2026-2031, as more precision horticulture programs use small seeds that require precise shape and weight for automated planting. That growth is linked to the expansion of protected agriculture, automated transplanting systems, and the greater use of high-value seed lots for vegetables and specialty crops. Research published in Seed Science and Technology in 2025 showed that pellet composition significantly affected emergence consistency, moisture response, and sowing performance in small-seeded crops, reinforcing the importance of engineered pellet systems for precision planting applications. The seed coating materials market is responding with more interest in engineered mineral systems, crop-specific binders, and pellet structures that deliver consistent flow and emergence.

By Function: Seed Protection Dominates but Enhancement Grows Fastest

Seed protection held 77.8% of the market by function in 2025, making it the largest segment, as fungicide and insecticide incorporation remains the main commercial reason for coating across grain, oilseed, and vegetable seeds. This role has been built over many years and remains structurally strong while seed-applied crop protection continues to be a default delivery route in commercial programs. The seed coating materials market still depends heavily on protection-oriented demand because it anchors volume across broad-acre crops with standardized treatment protocols. That base is supported by established grower expectations, commercial treatment workflows, and the continued need for early-stage protection at planting. Even when biologicals are added, protection remains the primary justification for coating investment.

Seed enhancement is the fastest-growing segment, with a 11.0% CAGR during 2026-2031, as the coating layer is increasingly used to deliver biologicals, biostimulants, and micronutrients that support early establishment. Research published in 2024 in Ecology, Environment and Conservation found that zinc biofortification treatments significantly affected nodulation, nutrient uptake, and yield parameters in chickpea systems. Consequently, the seed coating materials market is witnessing a shift as coating systems increasingly integrate protection, nutrition, and biological delivery within layered structures. This development is driving demand for advanced binders, compatibility-focused polymers, and controlled-release coating materials that can deliver multiple active ingredients without affecting planter performance or seed response.

By Coating Type: Synthetic Polymers Hold the Present, Bio-based Defines the Trajectory

Synthetic coatings accounted for 71.9% of market demand in 2025, making them the largest segment, as polyacrylate and polyvinyl acetate-based formulations still have the broadest commercial track record and the strongest raw material availability. Their established performance in grain, oilseed, and vegetable programs has made them the default choice in large-volume procurement. The seed coating materials market still relies on synthetic systems for scale, consistency, and cost balance in mainstream applications. That position is reinforced by long-standing supplier relationships and the installed process knowledge built around existing synthetic portfolios. Even where reformulation is underway, synthetic coatings remain the largest current revenue base across most regions.

Bio-based coatings are the fastest-growing segment, with a 11.6% CAGR during 2026-2031, as regulatory pressure, sustainability priorities, and improving technical performance converge. Argentina’s National Institute of Agricultural Technology and National Scientific and Technical Research Council developed a biopolymer coating platform in 2025 for soybean and corn using regionally derived feedstocks, showing that bio-based development is spreading beyond Europe. The seed coating materials market is therefore moving toward a dual structure, where synthetics remain the largest segment in the near term while bio-based systems are the fastest-growing. That shift is especially important where compliance and procurement policies are increasingly aligned around lower microplastic risk.

By Crop Type: Grains and Cereals Anchor Volume, Fruits and Vegetables Set the Pace

Grains and cereals accounted for 51.4% of demand in 2025, making them the largest segment because hybrid corn, wheat, rice, and barley move through commercial coating facilities in the highest volumes. The North American corn belt, the European wheat zone, and major Asian rice corridors together form the broad volume base for the seed coating materials market in this crop group. Large and relatively uniform seeds also fit well with high-throughput coating systems, which keep per-unit processing efficient and consistent. Oilseeds and pulses remain an important middle layer of demand, especially as biological inoculant programs expand in soybean production. Flowers, ornamentals, turf, and forage grasses are smaller in volume, but they remain technically demanding and command higher value per kilogram in specialized applications.

Fruits and vegetables are the fastest-growing segment, with a 11.1% CAGR during 2026-2031, because protected agriculture, seed premiumization, and automated transplanting systems all require more precise seed sizing and handling. These crops often involve small, irregular, or delicate seed lots where pelleting quality and coating uniformity directly affect planting performance. That makes horticulture one of the most specialized demand pools within the seed coating materials market. Brazil’s Federal Law 15070/2024 introduced phytosanitary registration requirements for treated seed sold commercially, including coated seed used in fruit and vegetable programs, which strengthens the preference for certified suppliers over decentralized on-farm application. The fastest growth in this crop group is therefore tied to both agronomic value and rising compliance expectations.

Geography Analysis

North America accounted for 43.7% of the seed coating materials market in 2025, making it the largest regional segment, as it has the highest concentration of commercially treated seed across corn, soybean, canola, and cotton programs. The United States forms the core of this position because nearly all hybrid corn seed and a large share of soybean seed are sold in pre-coated form with fungicide, insecticide, and flow-enhancement materials. Canada adds scale through canola, while Mexico expands the regional base through specialty vegetable programs. Precision planter adoption across the United States Corn Belt has also raised coating quality requirements, which supports premium formulations over generic alternatives.

Asia-Pacific is the fastest regional segment at 10.9% CAGR during 2026-2031, and Europe remained a major revenue center even while reformulation work is absorbing a larger share of supplier resources. In the Asia-Pacific region, government-backed seed modernization in China and India is increasing the share of seed distributed in coated form, while Japan and South Korea are supporting higher-value demand through protected agriculture and precision vegetable programs. That expansion is giving the seed coating materials market a broader growth base outside mature Western seed systems. Europe remains important because it houses advanced seed programs and major formulation expertise, but European suppliers are also carrying the heaviest near-term compliance burden under Regulation 2023/2055 and related guidance. This is increasing demand for low-abrasion binders, stable colorant systems, and higher-performance coating materials within the seed coating materials market.

South America is a growth region led by Brazil, where soybean scale and expanding use of biological seed treatments are strengthening demand for higher-performance coating systems. The bioinputs market in Brazil is growing at approximately 4 times the global average, primarily driven by soybean, corn, and sugarcane production systems. Concurrently, industrial seed treatment programs in the country are expanding as seed companies and growers adopt precision-applied treatment systems, driving demand in the seed coating materials market for advanced binders, dust-control additives, and bio-compatible polymer systems. In the Middle East, Saudi Arabia and the United Arab Emirates are creating niche demand through protected agriculture and precision vegetable seed programs. Africa remains at an earlier adoption stage, led by South Africa and Egypt, where access to certified coated seed is increasing through structured agricultural programs, creating an opening for cost-effective formulations that do not yet face the same compliance burden as in Europe.

Competitive Landscape

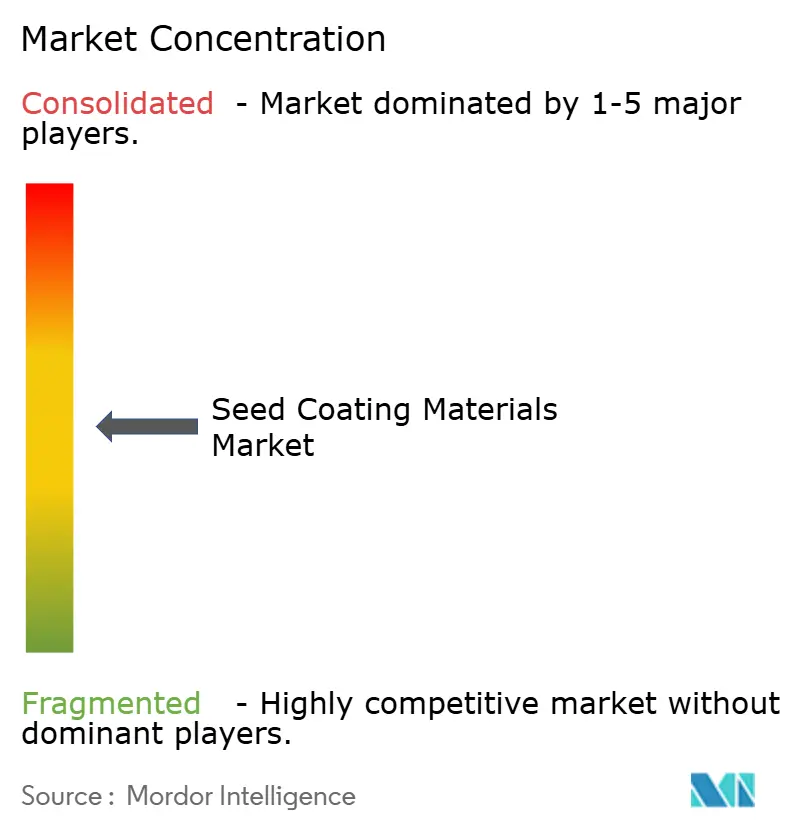

The seed coating materials market was moderately fragmented in 2025, with BASF SE, Croda International Plc, Clariant AG, Syensqo SA/NV, and Sensient Technologies Corporation as the key players. This balance reflects the presence of global specialty chemical groups with broad polymer, binder, and colorant capabilities, alongside regional formulators and coating service providers that still retain meaningful positions. The established players are supported by deep formulation expertise and regulatory capabilities, while emerging players such as Germains Seed Technology, Summit Seed Coatings, Universal Coating Systems LLC, and Centor Oceania compete through crop-specific expertise and local responsiveness. The seed coating materials market is therefore not consolidated enough for a few players to dominate pricing across all segments.

Strategic competition is concentrating on biological compatibility engineering, microplastic-free polymer development, and process performance under tighter planting and certification standards. BASF SE disclosed patent WO2024256589A1 in December 2024 for a binder system designed to stabilize biological actives while maintaining film integrity during high-speed coating, which shows how leading suppliers are protecting formulation advances. Croda International Plc, through Incotec Group BV, disclosed patent US20250049039A1 in February 2025 for porosity-modulating film coating formulations aimed at next-generation planter sensor tolerances, which indicates a similar push toward performance-specific intellectual property. The seed coating materials market is rewarding suppliers that can combine regulatory readiness with measurable planting, storage, and biological performance.

Strategic expansion is also coming from adjacent specialty chemistry players and from portfolio repositioning by established incumbents. In September 2025, Ashland Inc. expanded its cellulose and polyvinylpyrrolidone platform into seed-coating binder demand, using existing polymer know-how to address reformulation needs without building a dedicated legacy seed-coatings base. Syensqo SA/NV continues to position its inherited Peridiam coating systems around compatibility and formulation specialization, which differentiates it as buyers move away from commodity selection toward application performance. The seed coating materials market still offers open competitive space for tropical, biologically compatible binders, micronutrient-ready polymer matrices for pulses, and bio-based pelleting systems that meet both compliance and operating standards. That means leadership in the next phase is likely to depend less on sheer scale alone and more on who can solve the most difficult compatibility and reformulation problems first.

Seed Coating Materials Industry Leaders

BASF SE

Clariant AG

Croda International PLC

Syensqo SA/NV

Sensient Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ashland Inc. received United States Environmental Protection Agency approval for its Agrimer Eco-Coat seed coating polymer, a nature-based and microplastic-free technology developed using transformed vegetable oil chemistry. The formulation was designed to improve dust-off reduction, active ingredient retention, and regulatory compliance for vegetable, grain, fruit, and floral seed treatment applications.

- August 2025: Brazil’s Ministry of Agriculture issued updated phytosanitary standards for commercially distributed coated seed, mandating minimum coating uniformity and dust-off tolerance thresholds across grain, oilseed, and vegetable categories. The regulation is accelerating procurement consolidation toward certified large-scale coating material suppliers.

- February 2025: Incotec Group BV, part of Croda International Plc, published patent US20250049039A1 disclosing precision porosity-modulating film coating formulations designed to meet next-generation planter sensor tolerances. The patent signals a shift toward performance-specific claims rather than broad coverage of polymer formulas.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we treat the seed coating materials market as the value generated from binders, polymers, additives, and colorants that are purposely applied as a discrete layer on commercial crop seed, either by film-coating, encrusting, or pelleting, to deliver protection or enhancement benefits before sowing.

All aftermarket seed dressings, on-farm slurry mixes, and standalone biological inoculants sold without a coating matrix are kept outside this calculation.

Segmentation Overview

- By Ingredient

- Polymers

- Binders

- Colorants

- Active Ingredients

- Minerals and Pumice

- Other Additives

- By Form

- Liquid

- Solid

- By Process

- Film Coating

- Encrusting

- Pelleting

- By Function

- Seed Protection

- Seed Enhancement

- By Coating Type

- Synthetic

- Bio-based

- By Crop Type

- Grains and Cereals

- Oilseeds and Pulses

- Fruits and Vegetables

- Flowers and Ornamentals

- Turf and Forage Grasses

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To refine model inputs, we interview coating formulators, contract treaters, and farm-supply dealers across North America, Europe, Brazil, India, and Australia. Their insights on polymer price pass-through, film-coating versus pelleting share shifts, and grower adoption triggers let us challenge desk estimates and fine-tune regional penetration curves.

Desk Research

Our analysts sift through freely available yet authoritative data streams such as USDA crop acreage surveys, Eurostat pesticide statistics, FAOSTAT commodity balances, and ISF trade papers to size the sown seed pool and typical treatment penetration. Company 10-Ks, patent filings captured through Questel, and Dow Jones Factiva news archives supply pricing clues and technology timelines, while trade-body briefs from CropLife International and the American Seed Trade Association clarify regulatory milestones that shape ingredient uptake. The sources named here illustrate, not exhaust, the secondary backbone we reference.

Market-Sizing & Forecasting

We begin with a top-down construct that rebuilds the demand pool from certified seed output, average treatment rate (kilograms of coating per metric ton of seed), and ingredient blended value; selective bottom-up roll-ups of supplier shipments and sampled ASP × volume checks act as guardrails. Key variables like hectares under precision planting, polymer-to-bio-binder substitution ratios, EU microplastic phase-out deadlines, and cereal seed replacement cycles feed a multivariate regression that projects value through 2030. Where bottom-up totals diverge beyond a ±5 % band, assumptions are revisited with interviewees before final lock.

Data Validation & Update Cycle

Every draft passes a two-level analyst review in which outliers are flagged against historical series, competitor filings, and customs codes. Models refresh annually, yet trigger events, such as regulatory bans, large M&A, or a ≥10 % raw-material price swing, prompt an interim update so clients always see our freshest view.

Why Mordor's Seed Coating Materials Baseline Inspires Confidence

Published numbers vary because firms choose dissimilar ingredient baskets, coating processes, and refresh frequencies.

Scope breadth, price defaults, and assumed coating rates shift totals further.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.10 B (2025) | Mordor Intelligence | - |

| USD 2.19 B (2025) | Global Consultancy A | Omits bio-based binders; applies single flat ASP across regions |

| USD 2.21 B (2025) | Industry Journal B | Uses seed volume for top five crops only; refresh cadence biennial |

| USD 2.68 B (2025) | Regional Consultancy C | Relies on manufacturer shipment lists without adjusting for distributor mark-ups |

The comparison shows how narrower scope or slower updates compress totals.

By combining continually refreshed public statistics with expert cross-checks and dual-track modeling, Mordor delivers a transparent, balanced baseline that decision-makers can retrace and replicate.

Key Questions Answered in the Report

What is the current size of the seed coating materials market in 2026?

The seed coating materials market is valued at USD 2.92 billion in 2026 and is projected to reach USD 4.63 billion by 2031 at a 9.66% CAGR during 2026-2031.

Which ingredient category leads revenue generation?

Polymers was the largest ingredient segment, accounting for 44.3% in 2025 because they remain the main film-forming and carrier matrix across major coating processes.

Which coating type is expanding the fastest through 2031?

Bio-based coatings are the fastest segment, advancing at 11.6% CAGR during 2026-2031 as regulatory pressure and technical progress support reformulation.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific was the fastest regional segment at 10.9% CAGR during 2026-2031 because seed modernization programs in China and India are increasing coated seed penetration and horticulture demand is rising.

What is the main near-term risk for suppliers?

The biggest near-term risk is reformulation cost under microplastic restrictions because suppliers must invest in new binders and polymers while managing margin pressure.

Page last updated on: