Market Overview

| Study Period | 2020 - 2030 |

|---|---|

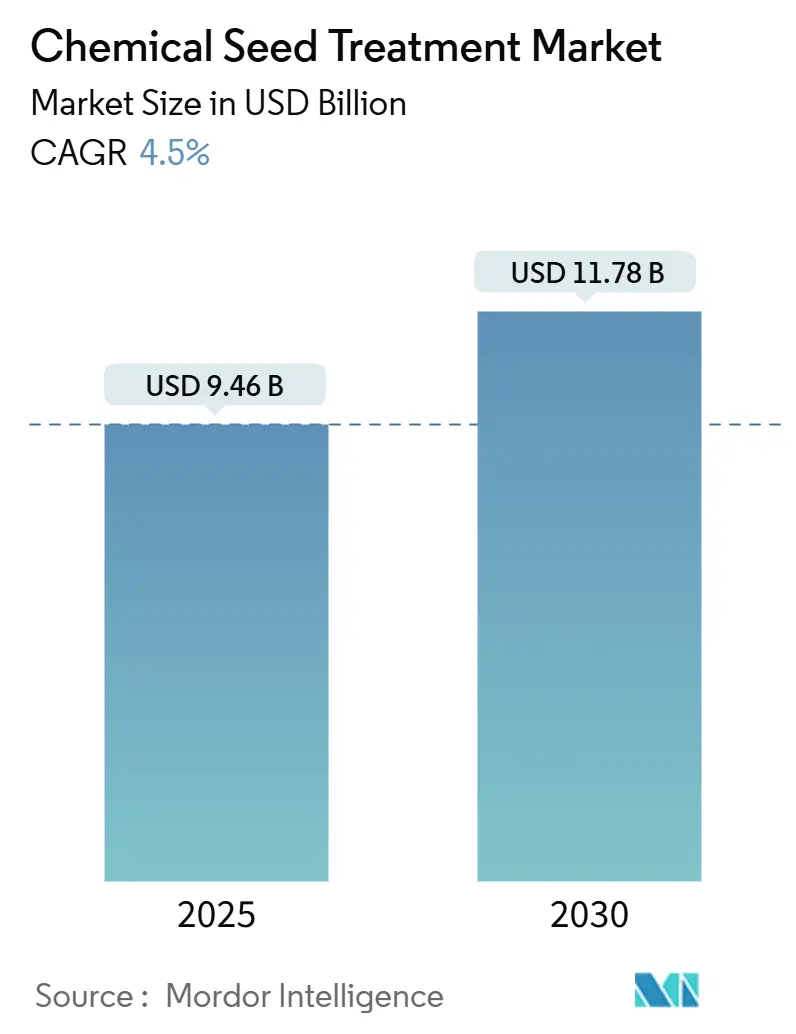

| Market Size (2025) | USD 9.46 Billion |

| Market Size (2030) | USD 11.78 Billion |

| Growth Rate (2025 - 2030) | 4.50% CAGR |

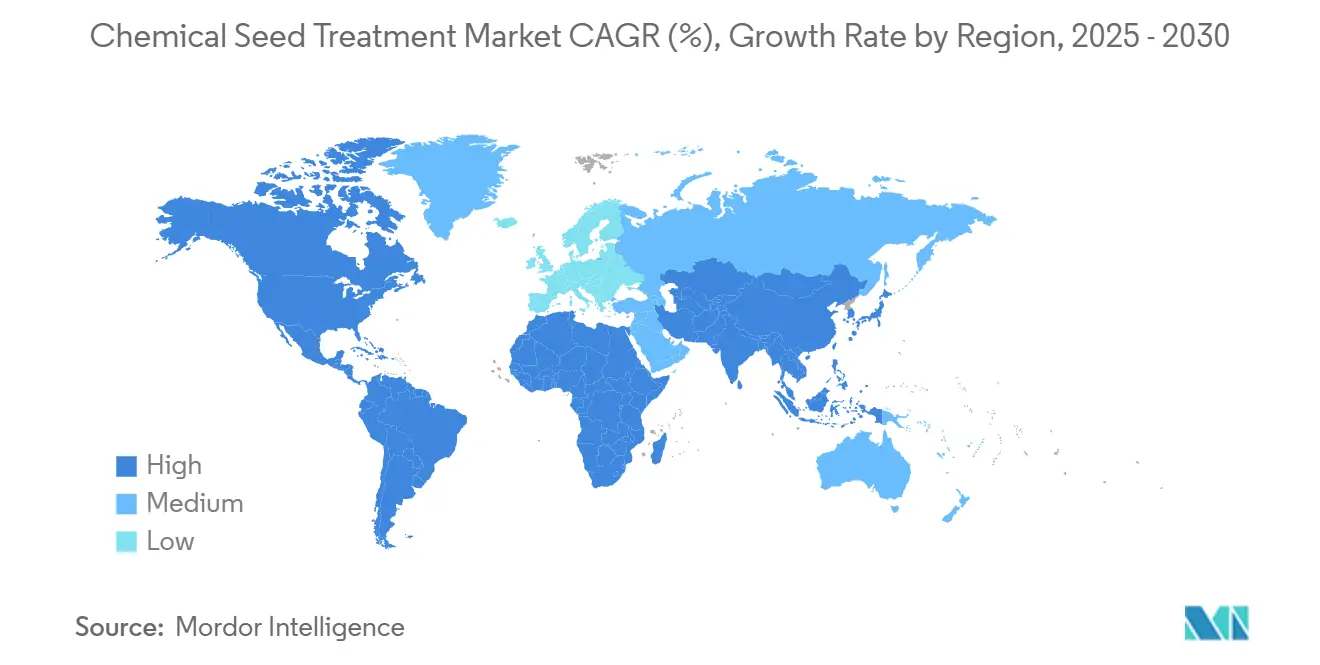

| Fastest Growing Market | North America |

| Largest Market | South America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chemical Seed Treatment Market Analysis by Mordor Intelligence

The chemical seed treatment market size, valued at USD 9.46 billion in 2025, is projected to reach USD 11.78 billion by 2030, growing at a CAGR of 4.50%. The market growth is driven by farmers' requirements for higher crop yields amid weather uncertainties, increasing biotech seed costs, and growing demands for food security. The integration of artificial intelligence in formulation development has reduced research and development timelines, while advanced planting equipment enables precise seed treatment application. The expansion of carbon credit initiatives provides additional incentives for farmers adopting efficient input practices, including chemical seed treatments. Market competition has intensified as major suppliers invest in vertical integration, while improved formulations such as suspension concentrates and seed pelleting technologies offer enhanced application precision and handling benefits.

Key Report Takeaways

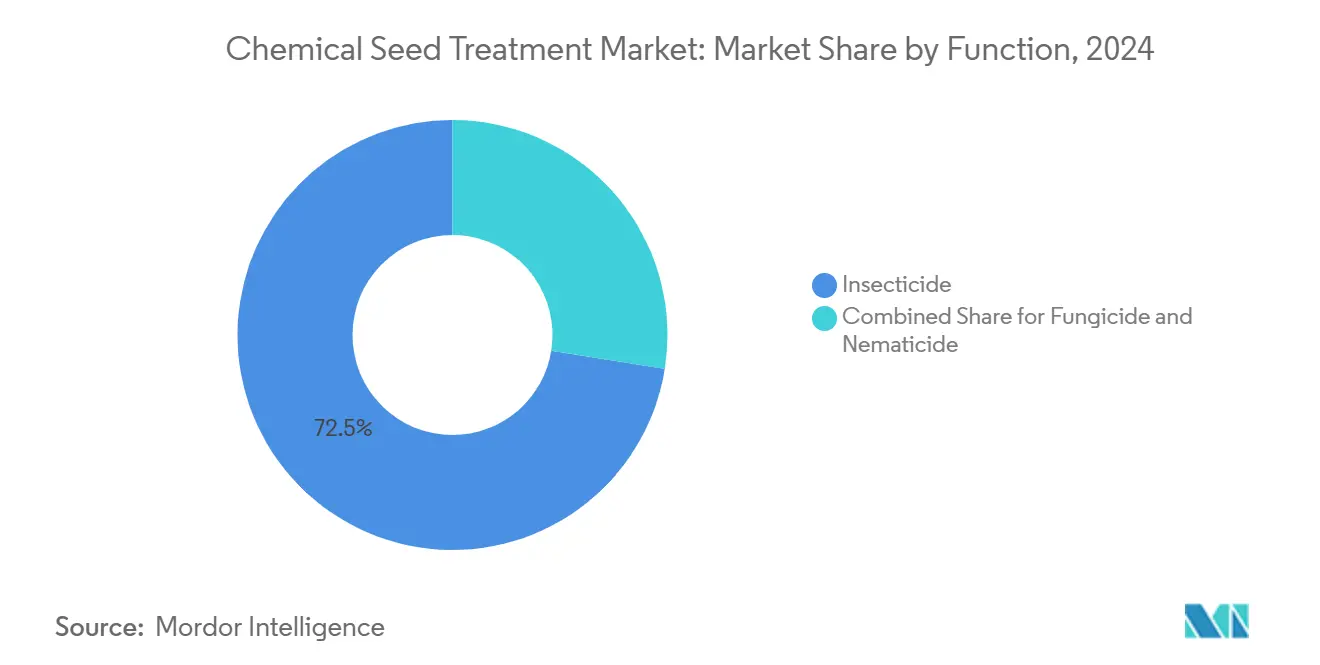

- By function, insecticides accounted for 72.5% of the chemical seed treatment market share in 2024 and are projected to grow at a CAGR of 4.7% through 2030.

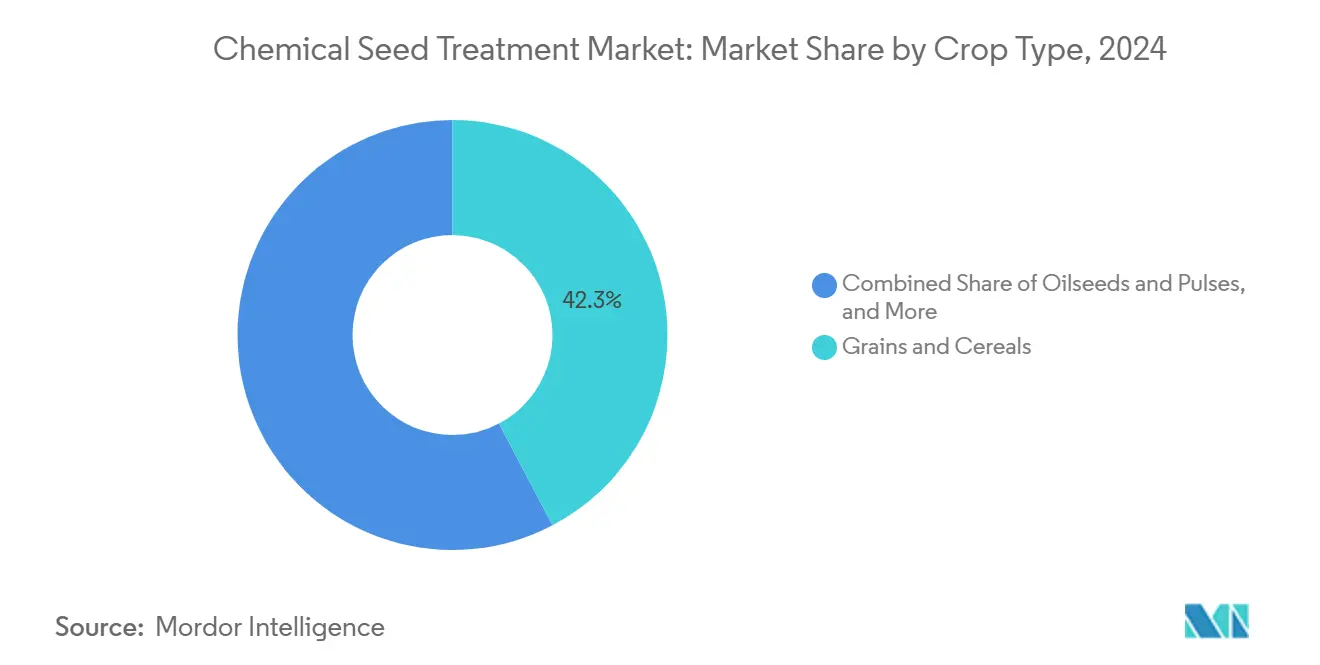

- By crop type, grains and cereals account for 42.3% of the chemical seed treatment market size, while pulses and oilseeds are projected to expand at a CAGR of 4.6% through 2030.

- By geography, South America maintained 44.6% market share in 2024, with North America exhibiting the fastest growth at 4.8% CAGR through 2030.

- The chemical seed treatment market demonstrates a moderate competitive intensity, with the top five players, Syngenta Group, BASF SE, Bayer AG, Corteva Agriscience, and FMC Corporation, collectively holding more than 50% of the market share.

Global Chemical Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing need to maximize crop yields for food security | +1.8% | Global, highest in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Rapid research and Development in Multi-Mode SDHI and Diamide Chemistries | +1.2% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift to treated seed to offset rising price of biotech/GM seeds | +0.9% | North America, Brazil, and Argentina | Medium term (2-4 years) |

| Growth of integrated one-pass planting equipment enabling precise on-seed dosing | +0.7% | North America, Europe, and Australia | Long term (≥ 4 years) |

| AI-guided formulation platforms reducing time-to-market for customized chemistries | +0.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Expansion of carbon-credit programs rewarding input-efficient practices | +0.6% | North America, Europe, and Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Need to Maximize Crop Yields for Food Security

Population growth, weather variability, and declining arable land have established chemical seed treatments as a critical agricultural safeguard for early-season plant development and yield potential.[1]Source: Food and Agriculture Organization, “Global Food Outlook 2025,” fao.org Seed treatments incorporating insecticides and fungicides provide essential protection during germination phases when foliar applications demonstrate limited efficacy. Agricultural producers in Asia encounter substantial operational challenges due to double-cropping systems that restrict replanting opportunities. Economic analyses demonstrate that treated seeds enable farmers to minimize replanting expenditures and maintain scheduled harvest periods, thereby preserving profit margins within price-sensitive commodity markets.

Rapid Research and Development in Multi-Mode SDHI and Diamide Chemistries

The incorporation of new SDHI (succinate dehydrogenase inhibitor) fungicides, specifically pydiflumetofen, and next-generation diamides improves pest control through multiple modes of action. This integration delays resistance development and extends protection beyond standard 30-day intervals. The implementation of artificial intelligence in molecular design reduces discovery timelines to six to seven years, facilitating the expedited development of new active ingredients. The enhanced duration of effectiveness supports extended growing seasons in temperate regions and aligns with the transition to single-pass planting methods in North America and Europe.

Shift to Treated Seed to Offset Rising Price of Biotech/GM Seeds

Premium, genetically modified corn and soybean seeds cost more than USD 400 per bag, compelling agricultural producers to invest in comprehensive seed-treatment packages to safeguard their genetic investments from early-stage losses. Return-on-investment analyses across South America indicate that treated seeds generate payback ratios of 3:1 to 5:1 through enhanced plant preservation and yield stabilization, supporting sustained adoption despite initial capital requirements.

Growth of Integrated One-Pass Planting Equipment Enabling Precise On-Seed Dosing

Agricultural planters integrate hydraulic systems, digital controllers, and GPS technology to deliver seed treatments at variable rates during planting operations. This integration eliminates separate treatment processes and reduces labor requirements. The precise application enables reduced chemical usage in areas with minimal pest pressure while facilitating targeted treatment in high-risk zones, optimizing both operational costs and environmental performance.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global regulations for agricultural chemical usage | -1.4% | Global, highest in Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Rising adoption of organic and biological seed-treatment alternatives | -0.8% | Europe, North America, and Brazil | Medium term (2-4 years) |

| Evidence of evolving pest resistance to systemic insecticide treatments | -0.6% | Global, intensive cropping zones | Medium term (2-4 years) |

| Investor pushback on PFAS-containing seed-coat polymers | -0.4% | Europe, North America, rising Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Regulations for Agricultural Chemical Usage

The European Union-27's phase-out of per- and polyfluoroalkyl substances (PFAS) and California's restrictions on neonicotinoids increase regulatory compliance costs and extend registration timelines, compelling suppliers to reformulate their products or develop alternative chemical solutions [2]Source: European Chemicals Agency, "ECHA announces timeline for PFAS restriction, echa.europa.eu. Similar regulatory implementations emerging in the Asia-Pacific region establish additional approval requirements that delay product launches and limit near-term market expansion.

Evidence of Evolving Pest Resistance to Systemic Insecticide Treatments

Documented cases of imidacloprid-resistant Drosophila suzukii and fluopyram-tolerant nematodes highlight the adaptive challenges faced by growers, necessitating the rotation or combination of modes of action[3]Source: United States Department of Agriculture, “Pest Resistance Monitoring 2024,” usda.gov. This increases complexity and reduces the effectiveness of single-mode products. These resistance issues emphasize the importance of integrated pest management strategies, including the use of biological controls, cultural practices, and chemical rotation, to mitigate the risk of resistance development and maintain long-term efficacy of pest control measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides Gain Momentum

Insecticides lead the market, holding a 72.5% of the chemical seed treatment market share in 2024, underscoring the significance of early pest management. Their adoption is projected to grow at a CAGR of 4.7% as farmers increasingly utilize these formulations. This growth is driven by the rising prevalence of pest infestations, which can significantly impact crop yields, and the need for effective solutions to protect seeds during the critical germination and early growth stages. Advancements in insecticide formulations, including improved efficacy and targeted pest control, have further encouraged their adoption. The increasing awareness among farmers about the economic benefits of preventing pest damage at the seed level also contributes to this trend.

Precision agriculture technologies support this trend by enabling the accurate application of combination products. These systems help reduce excess application and align with carbon-credit programs that require documented reductions in input use. Nematicide use is increasing, particularly in high-value vegetable crops where root pests cause significant economic damage. In mechanized markets, single-component fungicide and insecticide treatments are being gradually replaced by combination products, reflecting a broader transformation in agricultural input management.

By Crop Type: Protein Crops and Pulses Accelerate

Grains and cereals account for 42.3% of the chemical seed treatment market size due to their extensive planting areas. Pulses and oilseeds are experiencing significant growth, with a projected CAGR of 4.6% through 2030. This growth is driven by increasing global protein demand and the natural nitrogen-fixing properties of legumes, which encourage farmers to expand cultivation areas and adopt seed treatments. Seed treatments enhance germination rates, improve seedling vigor, and contribute to higher crop yields. These advantages, combined with the cost-effectiveness of seed treatments compared to other crop protection methods, are driving their growing adoption among farmers seeking to optimize productivity and reduce risks associated with crop failure.

For fruits and vegetables, seed treatments are especially important as these crops are highly vulnerable to soil-borne diseases and pests during their early growth stages. These treatments not only protect seeds from pathogens and pests but also enhance germination rates and seedling vigor, ensuring better crop establishment. The targeted protection offered by seed treatments helps minimize the need for excessive pesticide use, aligning with the increasing demand for sustainable and residue-free agricultural practices. This has further contributed to their growing adoption in these high-value crop segments.

Geography Analysis

South America accounts for 44.6% of the chemical seed treatment market share in 2024, driven by the adoption of mechanized row-crop systems and robust intellectual property protection frameworks. The chemical seed treatment market is projected to grow, driven by carbon-insetting programs and variable-rate seed treatment technology. The production of corn and soybeans drives Brazil's market growth, while Argentina's oilseed export sector is increasing the adoption of seed treatments.

North America exhibits the highest growth rate, with a CAGR of 4.8%, driven by the demand for increased agricultural productivity on limited land and the rising adoption of precision farming techniques. The region serves as a major exporter of agricultural products, characterized by large-scale operations with a strong emphasis on exports. North America's well-organized distribution chain, combined with factors such as fertile soil, ample water availability, extensive land, entrepreneurial farmers, and efficient infrastructure, provides significant competitive advantages in the market.

The Asia-Pacific region is another important market for seed treatment, with India ranking as the fourth-largest agrochemical manufacturer and China making advancements in commercial agricultural technology. Intensive double-cropping practices and limited arable land availability drive market growth in this region. In China, treated seeds are utilized in the northeast corn production regions to enhance yield stability, supported by government-led modernization initiatives. Europe maintains a significant market presence, despite slower growth, due to its strict chemical regulations. The 2025 REACH revision provides temporary allowances for pesticides while encouraging development in SDHI and diamide solutions. The Middle East and Africa show growth potential, with mechanization programs anticipated to increase chemical seed treatment adoption from current single-digit levels to mid-teens by 2030.

Competitive Landscape

The chemical seed treatment market shows moderate consolidation, with the top five players, Syngenta Group, Bayer AG, Corteva Agriscience, BASF SE, and FMC Corporation, holding a significant market share in 2024. These companies invest significantly in AI-enabled discovery platforms, polymer technologies, and partnerships to strengthen their intellectual property and enhance customer retention. Syngenta Group's USD 140 million investment in expanding its research and development facility in Greensboro, adding 220,000 ft² of formulation and analytics capacity, demonstrates the substantial capital requirements needed to address regulatory challenges and pest resistance issues.

Industry partnerships continue to expand, with companies combining chemical expertise with digital innovations. Bayer has partnered with Source.ag to implement AI in greenhouse crop optimization. Smaller companies, particularly university spin-offs, focus on specialized technologies such as biodegradable coatings and peptide-based microactuators, making them potential acquisition targets once they have demonstrated field-level effectiveness.

Patent developments concentrate on controlled-release microcapsules, low-dust polymer films, and AI-generated molecular structures. Market entry barriers include established relationships with large-scale seed treaters, extensive regulatory requirements, and the need for reliable supply chain management. These factors help established companies maintain their market position while necessitating continued investment in research and development. Companies that develop portfolios aligned with carbon-credit systems and ESG-compliant polymers may gain competitive advantages in premium market segments.

Chemical Seed Treatment Industry Leaders

-

Syngenta Group

-

Bayer AG

-

BASF SE

-

FMC Corporation

-

Corteva Agriscience

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Acadian Plant Health has introduced a seed treatment chemical designed to improve crop resilience under environmental stress conditions. This product aims to enhance the ability of crops to withstand adverse factors such as drought, extreme temperatures, and poor soil quality, thereby supporting better agricultural productivity.

- March 2025: Syngenta Group reported sales of USD 28.8 billion, driven by strong demand for seed treatment products, particularly those utilizing PLINAZOLIN and ADEPIDYN technologies. The company highlighted that these technologies have been instrumental in addressing key challenges in crop protection, offering enhanced efficacy and reliability. This growth reflects the increasing adoption of advanced agricultural solutions to improve yield and sustainability.

- August 2024: Corteva Agriscience significantly expanded its LumiGEN seed treatment portfolio for soybeans by introducing Lumiante fungicide seed treatment and Phalanx insecticide seed treatment, designed to enhance crop protection and improve yield potential for soybean growers.

Global Chemical Seed Treatment Market Report Scope

Seed treatment products or the chemicals that are used to coat or treat the seeds before sowing to ensure a high germination percentage. The Chemical Seed Treatment Market is segmented by Chemical Type (Insecticides, Fungicides, and Other Chemicals), Crop Type (Corn, Soybean, Wheat, Rice, Canola, Cotton, and Other Crop Types), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East & Africa). The report offers market size and forecast in terms of value (USD) for all the segments.

By Function

| Insecticide |

| Fungicide |

| Nematicide |

By Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Turf and Ornamental |

| Commercial Crops |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Ukraine | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Myanmar | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| UAE | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Function | Insecticide | |

| Fungicide | ||

| Nematicide | ||

| By Crop Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Turf and Ornamental | ||

| Commercial Crops | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Myanmar | ||

| Pakistan | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the chemical seed treatment market size in 2025?

The market is valued at USD 9.46 billion in 2025.

What CAGR will the chemical seed treatment market record between 2025 and 2030?

The market is projected to expand at a 4.50% CAGR through 2030.

Which region shows the fastest growth for chemical seed treatments?

North America is projected to grow the quickest with an 4.8% CAGR to 2030, driven by North America’s manufacturing scale-up and modernization programs.

How do stricter global regulations affect chemical seed treatment suppliers?

New PFAS and neonicotinoid restrictions increase compliance costs and push companies to reformulate with newer, safer actives.

Page last updated on: