Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

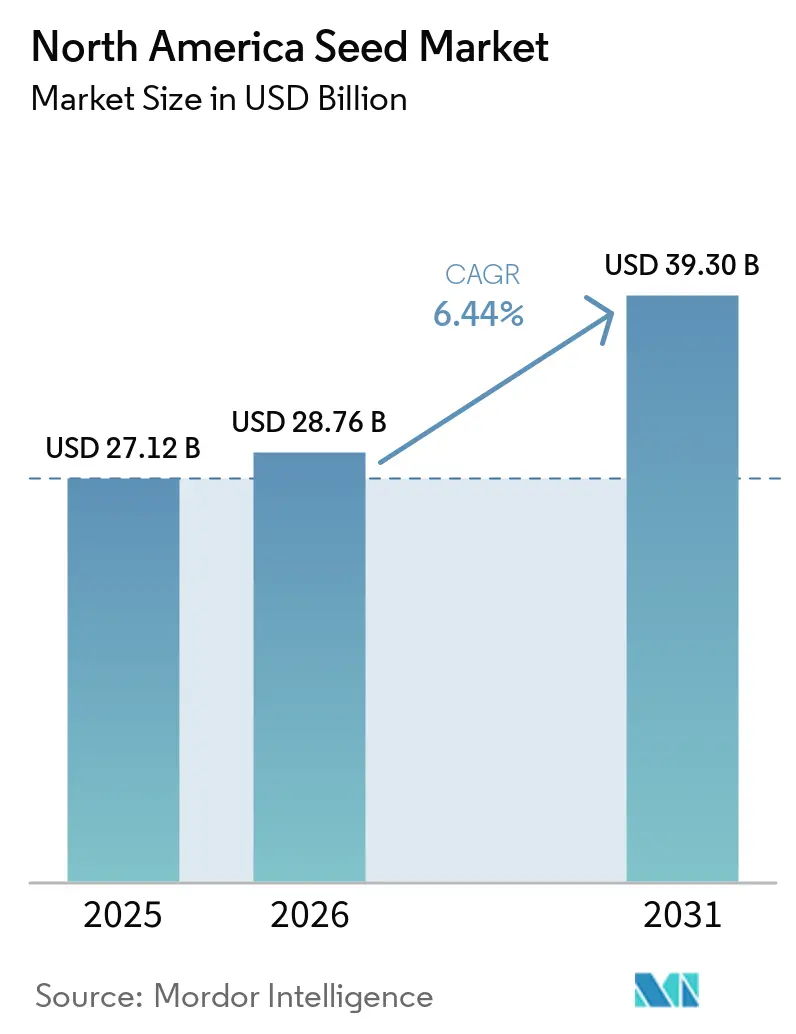

| Base Year Market Size (2025) | USD 27.12 Billion |

| Market Size (2026) | USD 28.76 Billion |

| Market Size (2031) | USD 39.30 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Seed Market Analysis by Mordor Intelligence

The North America seed market size is projected to expand from USD 27.1 billion in 2025 and USD 28.8 billion in 2026 to USD 39.2 billion by 2031, registering a CAGR of 6.3% between 2026 to 2031. The growth base of the North America seed market rests on advanced row-crop genetics, deeper biotech trait stacking, and acreage support linked to renewable fuels. Premium demand is also shifting toward greenhouse and controlled-environment systems, where growers need genetics built for disease control, uniformity, and shelf life. The North America seed market is also benefiting from better field-level placement tools, which help farmers match hybrids to local soil and yield conditions and make seed performance more measurable. Competitive behavior is moving toward greater trait pipeline depth, annual genetic gain, and targeted portfolio design rather than pure volume growth. The region also shows a split demand pattern between transgenic-heavy systems in the United States and Canada and more non-transgenic opportunities in parts of Mexico, which creates room for companies with broader hybrid portfolios.

Key Report Takeaways

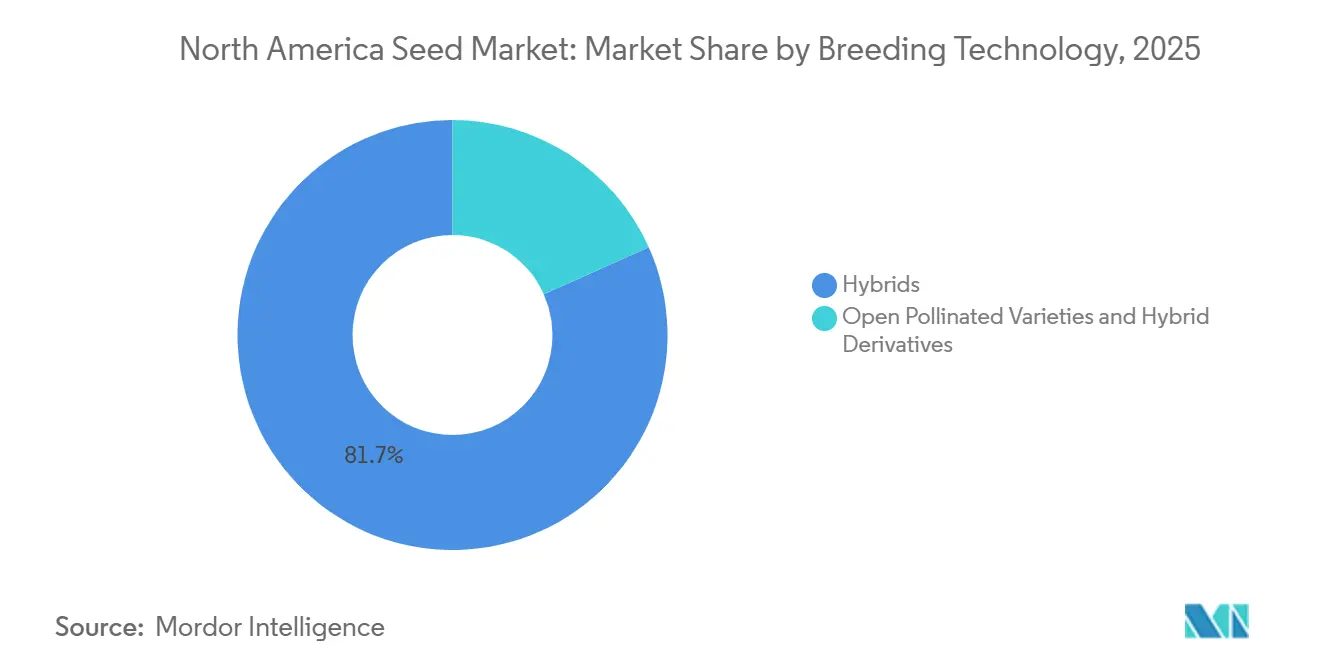

- By breeding technology, hybrids are the largest segment, 81.7% of the North America seed market share in 2025, and are the fastest-growing segment, forecast to grow at a 6.6% CAGR through 2026 to 2031.

- By cultivation mechanism, open-field cultivation is the largest segment, accounting for 99.7% of the North America seed market size in 2025, while protected cultivation is the fastest-growing segment, forecast to grow at a 7.6% CAGR through 2026 to 2031.

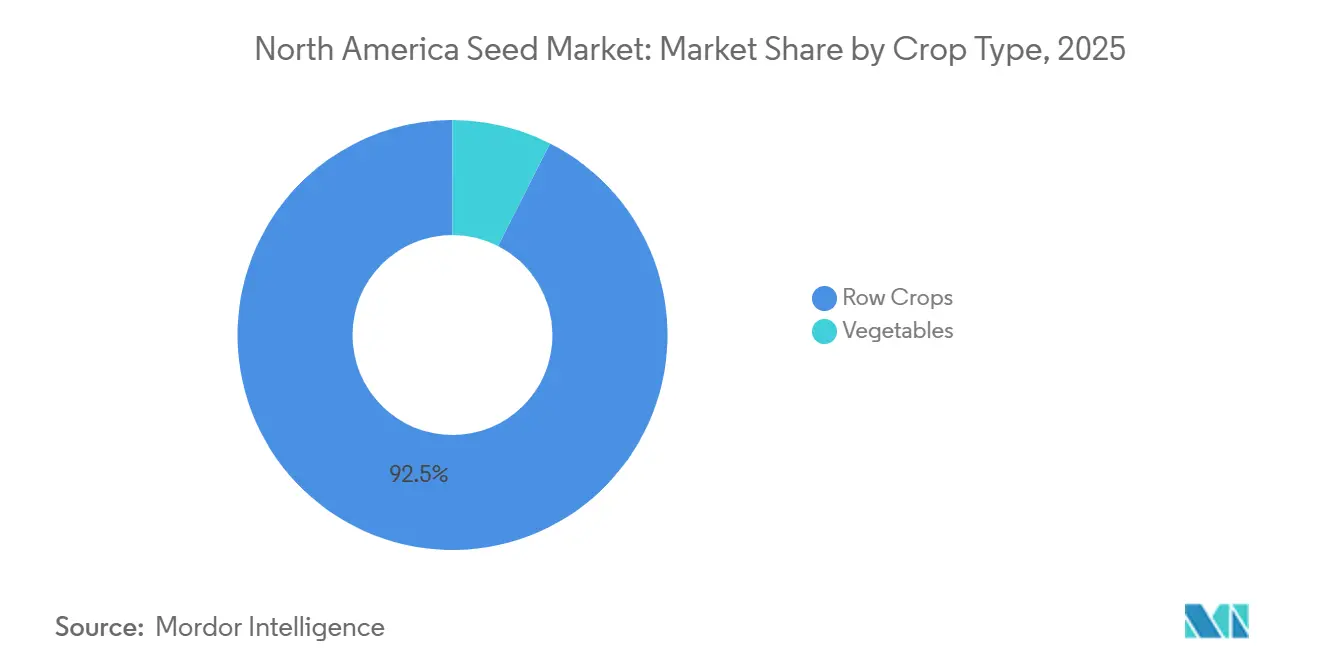

- By crop type, row crops are the largest segment, representing 92.5% of the North America seed market share in 2025, while row crops are the fastest-growing segment, forecast to grow at a 6.5% CAGR through 2026 to 2031.

- By geography, the United States is the largest country, 77% of the North America seed market size in 2025, while it is also the fastest-growing geography with a 6.9% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield Improvements with Advanced Transgenic Hybrids | +1.8% | United States and Canada core, with secondary spill-over to Mexico non-transgenic hybrid tier | Short term (≤ 2 years) |

| Biofuel Feedstock Acreage Support for Corn and Soybean Seed Demand | +1.2% | United States Corn Belt and Canadian prairies, with partial uplift in Mexico oilseed corridor | Medium term (2-4 years) |

| Precision Seeding and Hybrid Prescription Adoption | +1.0% | United States and Canada, expanding to Mexico's Pacific Coast commercial corn belt | Medium term (2-4 years) |

| Protected Cultivation Lift for Premium Vegetable Seed Demand | +0.8% | Mexico protected-cultivation export belt, Canada greenhouse cluster, United States controlled-environment corridor | Medium term (2-4 years) |

| Identity-Preserved and High-Oleic Specialty Crop Programs | +0.5% | United States Midwest and Mid-Atlantic, expanding to Ontario and Quebec in Canada | Long term (≥ 4 years) |

| Biological Seed-Treatment Bundling Around Premium Genetics | +0.5% | United States, with early adoption in Canada, nascent in Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Yield Improvements with Advanced Transgenic Hybrids

Multi-trait stacking remains the strongest value driver in the North America seed market, especially across corn and soybeans. According to the United States Department of Agriculture (USDA), 87% of cotton acres and 84% of corn acres were planted with stacked seeds in 2025[1]Source: U.S. Department of Agriculture, National Agricultural Statistics Service, “Acreage,” U.S. Department of Agriculture, downloads.usda.library.cornell.edu. This replacement cycle is tied to clear field performance, which supports premium pricing when yield and protection gains are visible season after season. The premium pricing is supported by the yield advantage, which helps sustain grower margins despite fluctuating commodity prices. Furthermore, multi-mode insect protection minimizes the need for refuge areas, streamlining field operations.

Biofuel Feedstock Acreage Support for Corn and Soybean Seed Demand

Renewable fuel policy is one of the most durable acreage supports for the North America seed market. In the United States, policy support, such as the Renewable Fuel Standard (RFS) and rising mandates for renewable diesel, are encouraging greater use of corn for ethanol and soybean oil for biodiesel. The United States Department of Agriculture (USDA) Economic Research Service projected soybean oil use for biomass-based diesel at 13.9 billion pounds in 2025, a 6% increase from the prior year's revised estimate, signaling stronger demand for oilseed-oriented genetics. This has strengthened demand for both crops, leading farmers to maintain or expand planted acreage. Recent analyses show that biofuel policies are projected to be a critical factor absorbing growing corn and soybean supplies and supporting farm-level prices, especially as yield improvements continue to increase output per acre.

Precision Seeding and Hybrid Prescription Adoption

Precision seeding is changing the commercial logic of the North America seed market because growers are more willing to pay for hybrids that perform well in clearly defined field zones. A USDA-supported University of Florida EDIS analysis published in January 2025 found a 69% increase in variable-rate technology adoption across major United States commodity crops in 2023, with corn at 71% and soybean at 76%. That shift reduces commodity-style seed purchasing because placement decisions now depend more on hybrid fit than on broad category labels. As more growers use field prescriptions, seed companies can defend premium pricing with better zone-level performance evidence. This makes precision placement an important demand quality driver for the North America seed market, even when planted acreage itself grows within a normal range.

Protected Cultivation Lift for Premium Vegetable Seed Demand

Protected cultivation is driving increased demand for premium vegetable seeds in the North America seed market. According to the Mexican Association of Protected Horticulture (AMHPAC), Mexico is expanding its protected cultivation capacity by over 1,500 hectares annually, with export-oriented tomato producers heavily relying on hybrid varieties optimized for greenhouse performance. These hybrids prioritize traits such as disease resistance, uniform ripening, and extended shelf life, rather than broad adaptation for open-field conditions. Similar trends are observed in Canada and parts of the United States, where greenhouse and controlled-environment growers are adopting specialized hybrid seed portfolios. This expansion of protected cultivation is creating a higher-value demand stream in the North America seed market, reducing reliance on traditional broad-acre row-crop cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trait-Stack Approval and Stewardship Delays | -1.2% | United States and Canada primary, Mexico secondary through USMCA alignment | Medium term (2-4 years) |

| Farm-Saved Seed Pressure in Pulses and Forage | -0.8% | Canada pulse and forage corridor, US forage market, Rest of North America | Long term (≥ 4 years) |

| Corn Rootworm Resistance Eroding Premium Trait Value | -0.5% | United States Corn Belt, secondary in Ontario and Quebec | Short term (≤ 2 years) |

| Dicamba Trait-System Regulatory Volatility | -0.4% | United States soybean and cotton belt, Canada moderate, Mexico low | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Trait-Stack Approval and Stewardship Delays

Regulatory timelines still slow parts of the North America seed market, especially for stacked biotech products that need coordinated review across the Animal and Plant Health Inspection Service (APHIS), Environmental Protection Agency (EPA), and Food and Drug Administration (FDA). The process became less predictable after a United States District Court vacated the United States Department of Agriculture (USDA) 2020 final rule on Genetically Engineered organisms (GE) organisms in December 2024, which forced Animal and Plant Health Inspection Service (APHIS) to restore older permitting, notification, and petition processes. Canada adds another review layer through its Plant with Novel Traits process, and United States Department of Agriculture (USDA) Foreign Agricultural Service reported 103 submissions and 261 field trials in 2024[2]Source: Danielson Erin and Alex Watters, “Biotechnology and Other New Production Technologies Annual,” USDA Foreign Agricultural Service, apps.fas.usda.gov. These parallel reviews lengthen commercialization timelines and reduce launch flexibility across the North America seed market.

Farm-Saved Seed Pressure in Pulses and Forage

Farm-saved seed continues to act as a structural constraint in certain segments of the North American seed market, particularly in pulses and forage crops. This challenge is most pronounced in the Canadian prairies and in lower-replacement categories, where growers have a reduced need for annual commercial seed purchases. Forage crops such as alfalfa, forage corn, and forage sorghum face greater competition from saved seed compared to premium row-crop programs. This dynamic limits pricing flexibility and slows the adoption of branded seeds in categories with lower intellectual property protections. Over time, this contributes to a more fragmented market in North America and reduces responsiveness to premium trait pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Sustain Structural Dominance, Transgenics Drive Margin

Hybrids are the largest segment, 81.7% of the North America seed market share in 2025, and also the fastest-growing segment, forecast to grow at a 6.6% CAGR through 2026 to 2031. Within transgenic hybrids, herbicide-tolerant lines continue to lead in spending, while insect-resistant and stacked-trait packages offer the highest premium potential in crops such as corn, soybean, canola, and cotton. Open-pollinated varieties and hybrid derivatives remain significant in forage, pulse, and specialty grains, where farm-saved seed retains commercial relevance. This division highlights the concentration of the North America seed industry in row crops, while lower-barrier categories exhibit a more diverse market structure.

In North America, the market for open-pollinated (OP) varieties and hybrid derivatives in seeds represents a significant segment of the broader seed industry, particularly for crops such as corn, soybean, vegetables, and specialty horticultural crops. Large commercial farms predominantly prefer hybrid seeds due to their productivity benefits, while OP varieties maintain niche demand in areas such as organic farming, local food systems, and specialty vegetable production. Hybrid derivatives are increasingly being developed with advanced traits, including drought tolerance, herbicide resistance, and enhanced oil or protein content, further solidifying their prominence in the North American seed market.

By Cultivation Mechanism: Protected Cultivation Accelerates Specialty Seed Premiums

Open-field cultivation is the largest segment, accounting for 99.7% of the North America seed market size in 2025. Greenhouse vegetable production is expanding near urban demand centers. Greenhouses, high tunnels, and vertical farms are increasingly purchasing coated, primed, and graft-compatible seeds with specialized disease resistance packages. While the North American seed market's supply base continues to rely on large-acreage row crops, value growth is accelerating in greenhouse and controlled-environment systems. This trend is drawing the attention of vegetable breeders who are focusing on dedicated greenhouse portfolios and enhanced disease-resistance platforms.

Protected cultivation is the fastest-growing segment, forecast to grow at a 7.6% CAGR through 2026 to 2031. Protected cultivation is gaining investment due to its ability to enable multiple crop cycles annually and mitigate the impact of climatic variability. Companies such as Rijk Zwaan, Enza Zaden, and Sakata Seeds have therefore kept dedicated North American research and commercial operations aligned with this shift. This positions the cultivation mechanism as one of the most distinct internal value divisions within the North American seed industry.

By Crop Type: Row Crops Anchor Market Volume While Vegetables Add Margin Depth

Row crops are the largest segment, representing 92.5% of the North America seed market share in 2025, and are the fastest-growing segment, forecast to grow at a 6.5% CAGR through 2026 to 2031. According to the United States Department of Agriculture, corn, soybeans, canola, cotton, and wheat form the commercial base of regional demand. The United States corn-planted area reached 95.2 million acres in 2025, underscoring the scale that supports the North American seed market. Oilseeds remain the second-largest value pool, and the United States Soybean Export Council projected that high-oleic soybean acreage would rise sharply by 2030/31.

Vegetables made significant market value in 2025, but contribute an outsized margin because hybrid pricing is much higher in disease-sensitive and protected systems. In North America, a significant share of vegetable production comes from protected cultivation systems, including greenhouses, high tunnels, hydroponics, and controlled-environment agriculture, as well as from disease-sensitive open-field crops that require intensive management. These systems predominantly use hybrid seed varieties, which, although more costly than open-pollinated alternatives, offer critical benefits such as greater yield stability, enhanced uniformity, and, most importantly, disease resistance and environmental resilience. These traits are particularly crucial in areas where pathogens, climate variability, or pest infestations can rapidly damage high-value crops.

Geography Analysis

The United States is the largest country, 77.0% of the North America seed market size in 2025. The country remains the core demand center of the North America seed market because it combines broad biotech adoption, large row-crop acreage, and a precision agriculture base that can monetize hybrid differentiation. According to the United States Department of Agriculture (USDA), in 2025, United States corn production reached a record 17.0 billion bushels and a record yield of 186 bushels per acre, which supports the case for continued investment in advanced genetics[3]Source: U.S. Department of Agriculture, National Agricultural Statistics Service, “Acreage,” U.S. Department of Agriculture, downloads.usda.library.cornell.edu. The United States is also the main growth market for identity-preserved and high-oleic soybeans as crush capacity rises and contract channels expand.

Canada is fastest-growing geography with a 6.9% CAGR through 2026 to 2031, supported by canola trait adoption, premium forage genetics, and a developed greenhouse vegetable sector. Canada also recorded 103 Plant with Novel Traits submissions and 261 field trials in 2024, indicating a healthy commercialization pipeline. These conditions keep Canada important to the North America seed market, even though it trails the United States in absolute terms. Pulse growers continue to utilize lower levels of certified seed. Nonetheless, export premiums for high-quality lentils and peas are driving gradual improvements.

Mexico offers growth opportunities in hybrid corn and greenhouse vegetables. Government seed-subsidy programs and the expansion of irrigation in regions such as Sinaloa and Guanajuato have facilitated the adoption of branded hybrids from companies like Syngenta and Corteva. However, a strong cultural preference for landrace maize among ejido farmers has limited growth rates. The extent to which infrastructure improvements and enhanced credit access are implemented will determine Mexico's ability to narrow the productivity gap with the United States during the forecast period.

Competitive Landscape

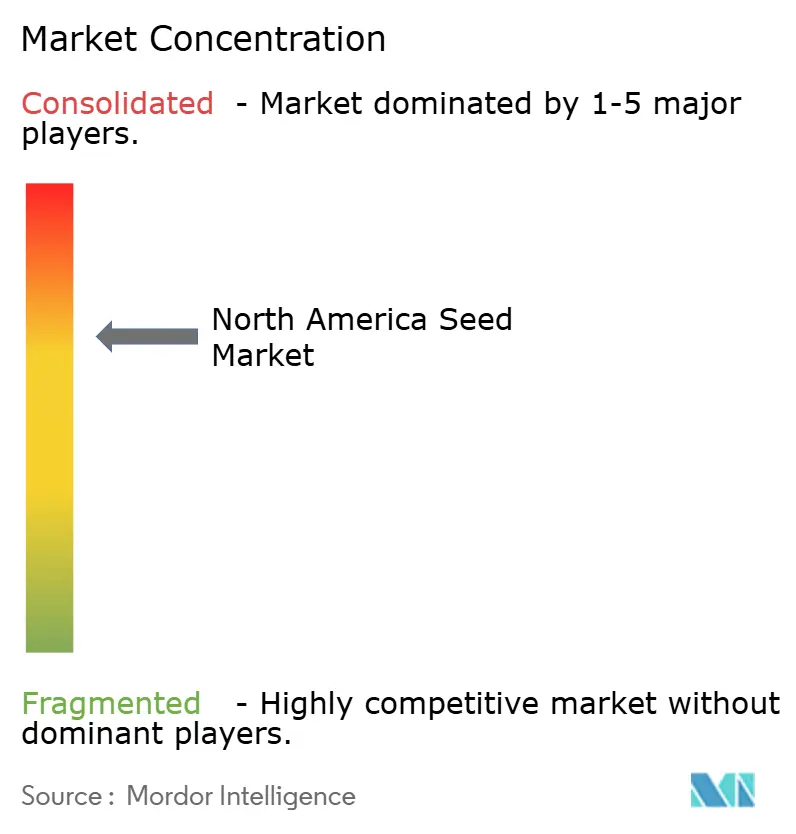

The North America seed market demonstrates moderate concentration, with the five largest companies projected to account for a significant share of revenue in 2025. Corteva Agriscience leads the market, driven by its Pioneer corn and soybean hybrids and a robust trait development pipeline. Bayer AG follows closely, supported by its Dekalb, Asgrow, and Deltapine brands. Syngenta Group holds a notable market share through its Golden Harvest and NK brands. BASF SE and Land O’Lakes round out the top tier, leaving room for regional breeders to compete.

BASF SE occupies a unique position in the market, operating across both soybean and vegetable seeds through its Xitavo and Nunhems brands. The company has further expanded its portfolio with InVigor Gold, a canola-quality Brassica juncea, enhancing its oilseed offerings. Additionally, there is an identified opportunity in biological seed-treatment bundling, where value-added coatings and inoculants remain underutilized by major players. Consequently, pricing dynamics in the North American seed market are increasingly influenced by genetic advancements and trait quality rather than shipment volumes alone.

Channel dynamics are evolving as dealer exclusivity limits shelf space for independent players. Smaller firms have raised concerns about these challenges but are also exploring alternative strategies, such as direct-to-grower e-commerce, which is gaining momentum in online seed sales. Established players continue to strengthen their positions through technological advancements in climate modeling and variable-rate seeding. Regional adaptability remains a key advantage for local breeders who develop hybrids tailored to specific microclimates.

North America Seed Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

Land O’Lakes Inc.

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bayer launched NewGold, a multi-crop seed brand emphasizing low-carbon intensity oilseed crops, including camelina and winter canola, to cater to the expanding renewable diesel and sustainable aviation fuel markets in North America. This initiative enhances Bayer's seed portfolio and highlights the increasing investment in specialized crop genetics, enabling farmers to diversify crop rotations and engage in biofuel value chains.

- August 2025: Syngenta Group and M.S. Technologies have unveiled soybean trait stack that adds tolerance to glyphosate, glufosinate, 2,4-D choline, and multiple HPPD inhibitors. Introductory seed volumes are planned for 2028, with broad United States commercial availability projected in 2029, pending regulatory approvals.

- March 2024: Syngenta Vegetable Seeds and Emerald Seed Company entered into an exclusive global licensing agreement, granting Syngenta access to Emerald’s elite hybrid and open-pollinated onion genetics. This collaboration strengthens Syngenta's portfolio and enables the company to provide specialized germplasm to a broader range of growers worldwide, including those in North America.

North America Seed Market Report Scope

A seed is a fertilized and matured ovule that contains an embryonic plant, stored nutrients, and a protective coat. It serves as the primary reproductive unit for planting. The North America seed market report is segmented by breeding technology (hybrids and open-pollinated varieties and hybrid derivatives), by cultivation mechanism (open field and protected cultivation), by crop type (row crops and vegetables), and by geography (Canada, Mexico, United States, and Rest of North America). The market forecasts are provided in terms of value (USD) and volume (Metric Tons).

By Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Other Traits | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

By Cultivation Mechanism

| Open Field |

| Protected Cultivation |

By Crop Type

| Row Crops | Fiber Crops | Cotton |

| Other Fiber Crops | ||

| Forage Crops | Alfalfa | |

| Forage Corn | ||

| Forage Sorghum | ||

| Other Forage Crops | ||

| Grains and Cereals | Corn | |

| Rice | ||

| Sorghum | ||

| Wheat | ||

| Other Grains and Cereals | ||

| Oilseeds | Canola, Rapeseed and Mustard | |

| Soybean | ||

| Sunflower | ||

| Other Oilseeds | ||

| Pulses | ||

| Vegetables | Brassicas | Cabbage |

| Cauliflower and Broccoli | ||

| Other Brassicas | ||

| Cucurbits | Cucumber and Gherkin | |

| Pumpkin and Squash | ||

| Other Cucurbits | ||

| Roots and Bulbs | Garlic | |

| Onion | ||

| Potato | ||

| Other Roots and Bulbs | ||

| Solanaceae | Chilli | |

| Eggplant | ||

| Tomato | ||

| Other Solanaceae | ||

| Unclassified Vegetables | Asparagus | |

| Lettuce | ||

| Okra | ||

| Peas | ||

| Spinach | ||

| Carrot | ||

| Other Unclassified Vegetables | ||

By Geography

| Canada |

| Mexico |

| United States |

| Rest of North America |

| By Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Other Traits | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| By Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| By Crop Type | Row Crops | Fiber Crops | Cotton |

| Other Fiber Crops | |||

| Forage Crops | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

| Grains and Cereals | Corn | ||

| Rice | |||

| Sorghum | |||

| Wheat | |||

| Other Grains and Cereals | |||

| Oilseeds | Canola, Rapeseed and Mustard | ||

| Soybean | |||

| Sunflower | |||

| Other Oilseeds | |||

| Pulses | |||

| Vegetables | Brassicas | Cabbage | |

| Cauliflower and Broccoli | |||

| Other Brassicas | |||

| Cucurbits | Cucumber and Gherkin | ||

| Pumpkin and Squash | |||

| Other Cucurbits | |||

| Roots and Bulbs | Garlic | ||

| Onion | |||

| Potato | |||

| Other Roots and Bulbs | |||

| Solanaceae | Chilli | ||

| Eggplant | |||

| Tomato | |||

| Other Solanaceae | |||

| Unclassified Vegetables | Asparagus | ||

| Lettuce | |||

| Okra | |||

| Peas | |||

| Spinach | |||

| Carrot | |||

| Other Unclassified Vegetables | |||

| By Geography | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms