Security Audits And Assessments Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

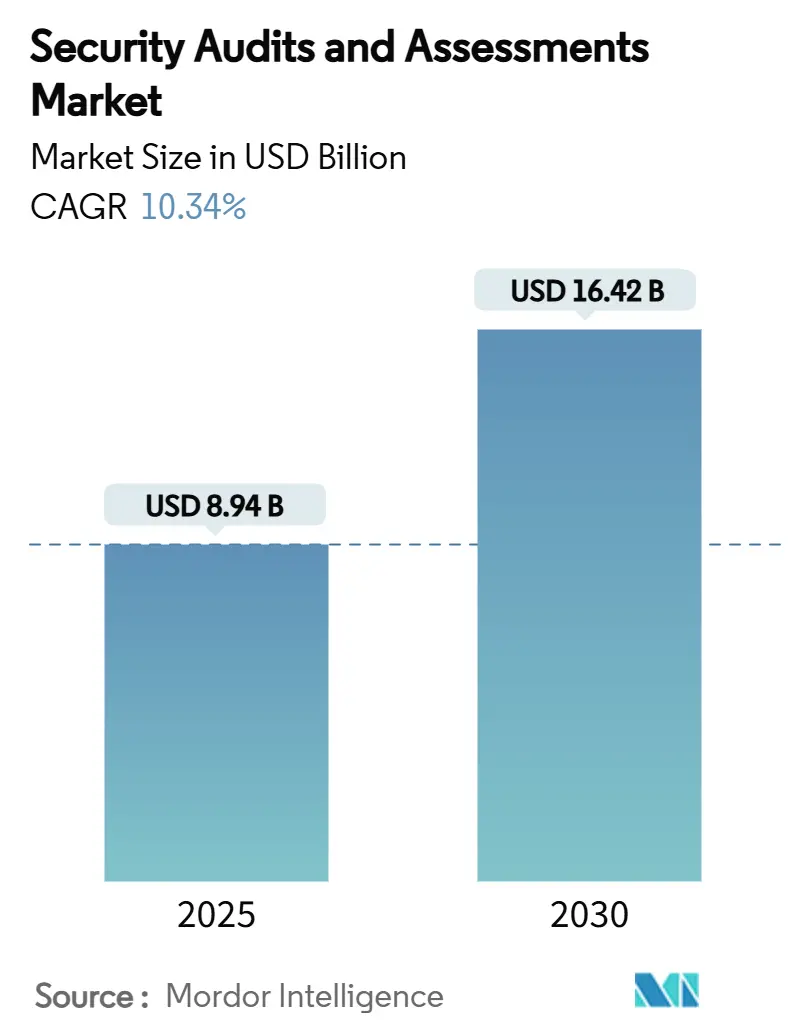

| Market Size (2025) | USD 8.94 Billion |

| Market Size (2030) | USD 16.42 Billion |

| Growth Rate (2025 - 2030) | 10.34% CAGR |

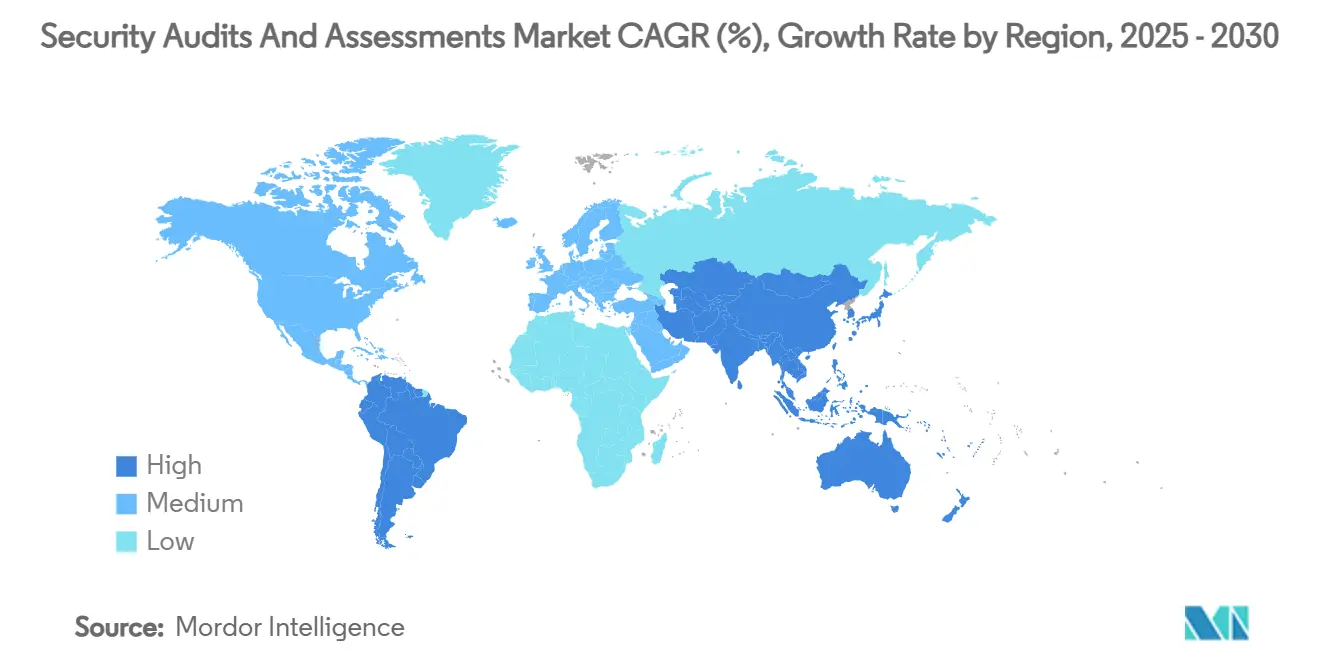

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Audits And Assessments Market Analysis by Mordor Intelligence

The security audits and assessments market reached USD 8.94 billion in 2025 and is forecast to expand to USD 16.42 billion by 2030, translating into a 10.34% CAGR; the market size projection reflects the sector’s shift from periodic compliance checks to continuous risk-based validation in response to escalating cyber threats and tightening global mandates.[1]European Union Agency for Cybersecurity, “Supporting NIS2 Implementation Through Actionable Guidance,” enisa.europa.eu Heightened breach costs, broader adoption of zero-trust architectures, and the rollout of supply-chain disclosure laws, such as SBOM, are accelerating demand for third-party security assessments, especially in cloud-native environments. Service providers are moving from project-based engagements toward automation-driven, managed offerings that deliver near real-time visibility, while clients increasingly view audits as an operational necessity rather than an annual compliance exercise. The extensive funding commitments announced by NATO members and national governments reinforce a multi-year growth runway, allowing the security audits and assessments market to remain resilient amid wider macro-economic uncertainty. The scarcity of certified auditors, particularly those specializing in AI security, cloud, and post-quantum cryptography, continues to inflate project fees while simultaneously spurring the uptake of automated validation platforms.

Key Report Takeaways

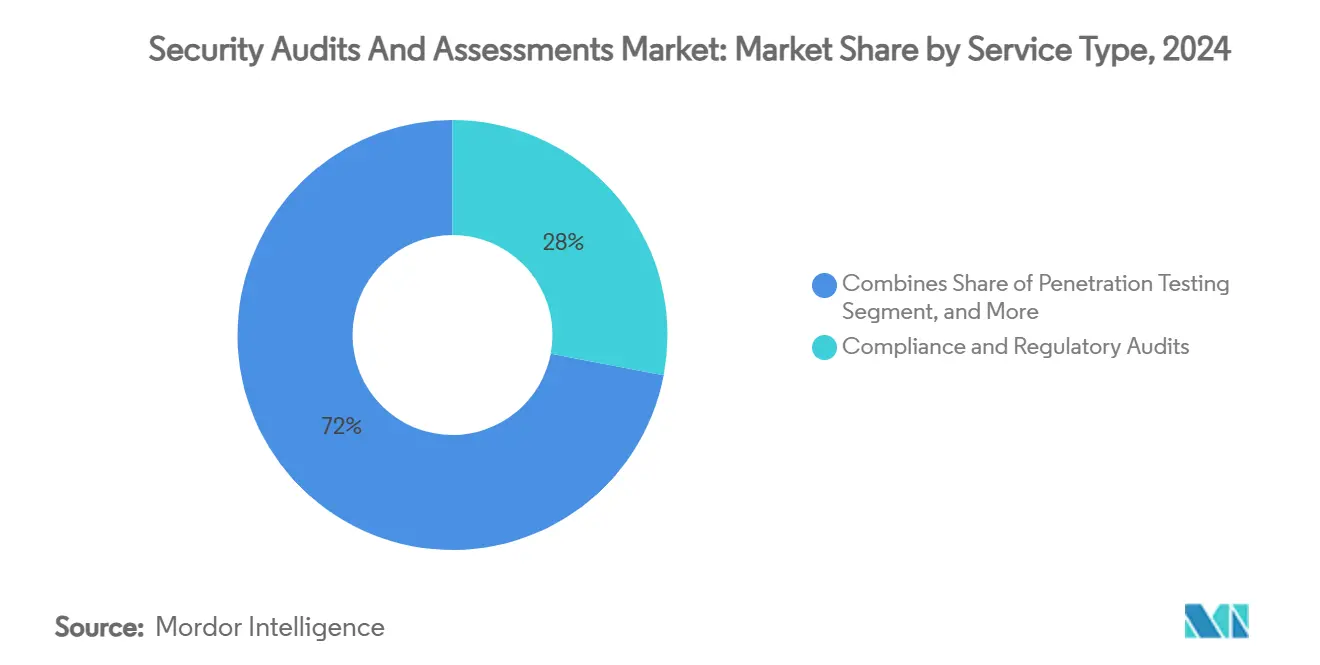

- By service type, compliance and regulatory audits held 28% of the security audits and assessments market share in 2024; cloud-security and DevSecOps assessments are expanding at an 18.40% CAGR through 2030.

- By organization size, large enterprises captured 65% revenue share in 2024 in the security audits and assessments market, but small and medium enterprises are projected to grow at a 14.20% CAGR through 2030.

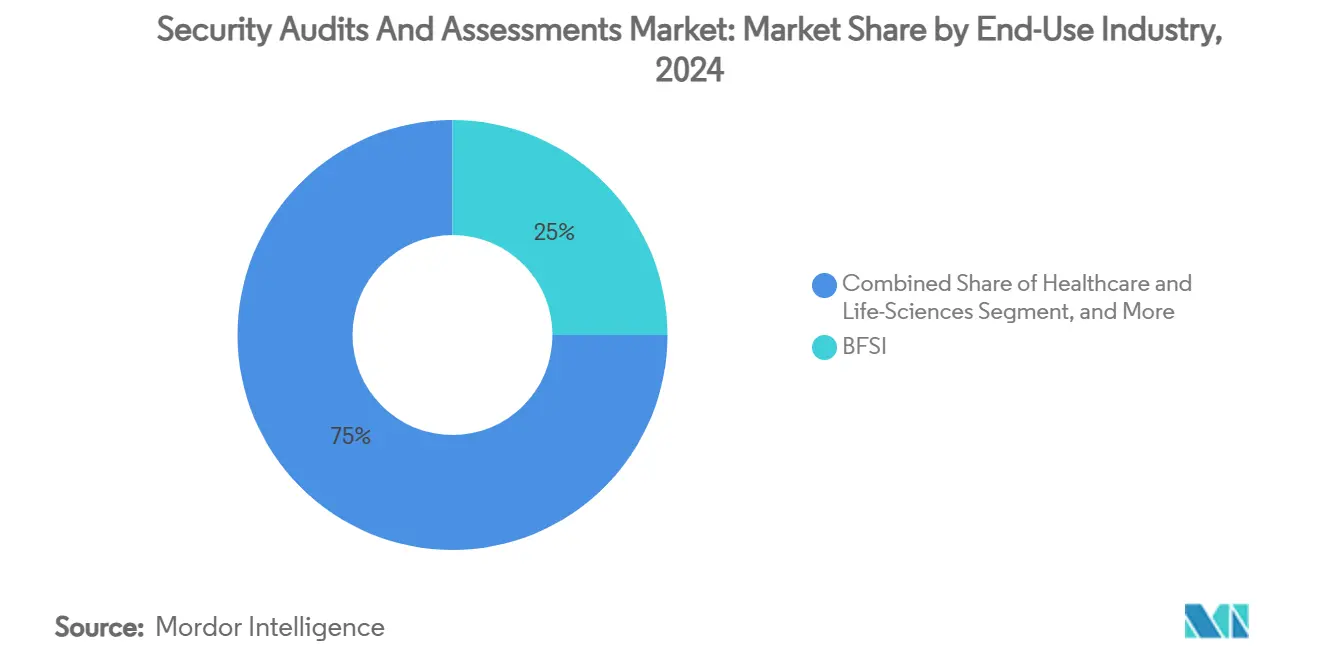

- By end-use industry, BFSI led with 25% of the security audits and assessments market share in 2024; healthcare and life sciences are forecast to expand at a 15.10% CAGR to 2030.

- By deployment mode, on-site project-based services controlled 55% of the security audits and assessments market size in 2024, yet remote managed services are growing at a 16.30% CAGR.

- By geography, North America accounted for 38% of the security audits and assessments market size in 2024, while the Asia-Pacific region is expected to advance at a 14.00% CAGR from 2024 to 2030.

Global Security Audits And Assessments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened frequency and cost of cyber-attacks | +2.80% | Global | Short term (≤ 2 years) |

| Expansion of zero-trust and continuous-compliance mandates | +2.10% | North America and EU | Medium term (2-4 years) |

| AI-driven vulnerability discovery tools raise audit demand | +1.90% | Global, with early gains in North America, Asia-Pacific | Medium term (2-4 years) |

| Supply-chain security disclosure requirements (SBOM, NIS2) | +1.70% | EU core, spill-over to North America | Short term (≤ 2 years) |

| Cloud-native adoption - need for cloud security assessments | +1.50% | Global | Long term (≥ 4 years) |

| Cyber-insurance underwriting standards tightening | +1.20% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Frequency and Cost of Cyber-Attacks

Average breach costs climbed to USD 4.88 million in 2024, with industrial incidents adding USD 830,000 over 2023 levels. Ransomware hit manufacturing hardest, accounting for 25.7% of incidents, prompting firms to assign 6-7% of IT spending to cyber controls. Retail breach costs rose 17.6%, intensifying demand for third-party penetration tests. Healthcare faced a 93% breach prevalence, pushing regulators toward mandatory incident-response audits. In Asia-Pacific, Chinese state-sponsored activity surged 150%, leading Singapore to deploy military resources for cyber defense, further elevating regional assessment spending.

Expansion of Zero-Trust and Continuous-Compliance Mandates

Federal zero-trust directives based on NIST SP 800-207 require agencies to validate identity, device, and application controls via regular audits. The EU’s NIS2 Directive extends mandatory risk assessments to 18 critical sectors, with non-compliance fines of EUR 10 million. NATO members have pledged 1.5% of GDP to cybersecurity by 2035, guaranteeing long-term funding for assessments. Organizations are shifting from severity-based to risk-based vulnerability management, fuelling demand for tailored audit frameworks. Integration of zero-trust with cloud workloads is creating new service lines focused on micro-segmentation validation.[2]National Institute of Standards and Technology, “NIST Guidance on Implementing a ZTA,” nist.gov

AI-Driven Vulnerability Discovery Tools Raise Audit Demand

The AI security tooling market is forecast to reach USD 133.8 billion by 2030, generating specialized audit needs to confirm model robustness and mitigate adversarial risk. Financial institutions deploying AI fraud analytics now commission algorithm-bias reviews, while manufacturers request audits of predictive maintenance models to block espionage. Automated security validation solutions grew from USD 334.3 million in 2023 to USD 824.7 million in 2028 as firms seek continuous posture checks without adding personnel. Regulators are drafting AI-specific security obligations, positioning assessment providers to capture new revenue streams in algorithmic transparency.

Supply-Chain Security Disclosure Requirements (SBOM, NIS2)

The U.S. Army began enforcing SBOM submissions in February 2025, mirroring EU Cyber Resilience Act demands for component visibility. PCI DSS 4.0 adds 64 requirements, including software inventory controls effective March 2025.[3]Cybeats, “PCI DSS 4.0 SBOMs – A 2025 Readiness Guide,” cybeats.com ENISA earmarked EUR 390 million for supply-chain resilience initiatives between 2025-2027, boosting assessment budgets. Eighty-nine percent of EU entities expect to hire additional security staff to oversee vendor risk programs. High-profile supply-chain breaches in Singapore highlight vulnerabilities in fourth-party relationships, propelling investment in SBOM automation and third-party audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of certified auditors inflating project costs | -1.80% | Global | Long term (≥ 4 years) |

| Tool sprawl and overlapping frameworks confuse buyers | -1.10% | North America and EU | Medium term (2-4 years) |

| Budget deferrals amid macro-economic uncertainty | -0.90% | Global | Short term (≤ 2 years) |

| Scope-creep and audit fatigue in highly regulated sectors | -0.70% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Certified Auditors Inflating Project Costs

Europe faces a 300,000-person cybersecurity talent gap, leaving 32% of firms unable to fill open roles, which drives consulting rates upward and stretches project timelines. Healthcare providers now commit 12-15% of IT budgets to security staff, double 2023 allocations. Automated validation vendors such as XM Cyber hold 26.9% revenue share in the segment, easing reliance on scarce specialists. Manufacturers direct up to 30% of cybersecurity budgets to training, yet post-quantum skills remain rare, creating premium opportunities for niche auditors. Regional managed service providers use local talent pools to deliver cost-effective offerings to SMEs.

Tool Sprawl and Overlapping Frameworks Confuse Buyers

Enterprises juggle ISO 27001, NIS2, CMMC, and sector-specific rules, fostering purchase duplication and coverage gaps. Healthcare organizations, balancing HIPAA with NIST updates, often employ dozens of overlapping point tools requiring rationalization audits. Integrated platforms like Qualys Enterprise TruRisk aim to consolidate tooling but still need independent validation to confirm efficacy, driving demand for third-party assessments. Acquisition activity, such as Palo Alto Networks’ purchase of QRadar SaaS assets, signals platform convergence yet obliges customers to audit migration success. Consulting firms offering framework-mapping services gain relevance as buyers seek roadmaps that reconcile diverging requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud-Security Assessments Drive Market Evolution

Cloud-security and DevSecOps assessments, growing at an 18.40% CAGR, are reshaping the security audits and assessments market as organizations modernize application stacks. Compliance and regulatory audits still commanded 28% of the security audits and assessments market share in 2024 because regulators require documented proof of controls. However, penetration testing is shifting toward continuous attack-path validation, and AI-enhanced vulnerability assessments now surface context-aware findings that demand fewer human hours. Risk advisory engagements increasingly focus on supply-chain exposure and zero-trust roadmap design, while demand for cloud-workload configuration reviews benefits from multi-cloud adoption trends. Providers package these services into subscription models that align with DevOps sprint cycles, pairing automated scans with quarterly human validation for high-risk systems.

Traditional annual audits are no longer sufficient for cloud-native architectures that change frequently; instead, customers expect real-time dashboards that integrate SBOM status, misconfiguration alerts, and compliance scores. Service lines covering Kubernetes hardening, identity and access management testing, and microsegmentation validation are rising fastest, especially in industries bound by data sovereignty rules. Managed detection and response partners extend assessments to runtime monitoring, giving clients a single pane for findings and remediation tasks. With regulators placing greater emphasis on continuous-compliance principles, cloud-security assessments have transitioned from being a specialized add-on to a foundational necessity. Consequently, security audits and assessments have taken center stage in discussions among buyers.

By Organization Size: SME Adoption Accelerates Through Managed Services

Large enterprises held 65% of global revenues in 2024, reflecting multi-region footprints and complex compliance responsibilities that necessitate comprehensive audit programs. They retain internal governance teams but outsource specialized tasks such as AI model testing, operational-technology assessments, and post-quantum readiness validation. Their contracts increasingly include outcome-based metrics, pushing vendors to deploy automation that guarantees consistent coverage across business units and accelerates reporting cycles.

Small and medium enterprises represent the fastest-expanding customer group at a 14.20% CAGR, driven by affordable, cloud-delivered offerings that eliminate upfront tooling costs. Many SMEs buy bundled packages that provide vulnerability scanning, policy mapping, and virtual CISO hours, allowing them to satisfy customer requirements without hiring full-time security staff. Regional providers tailor services to local regulations and language needs, while global vendors leverage partner channels to reach untapped segments. The democratization of assessment platforms thus broadens the addressable security audits and assessments market and reduces entry barriers for companies with fewer than 500 employees.

By End-Use Industry: Healthcare Leads Growth Amid Regulatory Pressure

BFSI maintained the largest revenue slice in 2024 at 25% because financial regulators mandate regular penetration testing and anti-fraud system audits. Yet healthcare shows the strongest momentum, expanding 15.10% annually as digital-health adoption brings sensitive data online and breach consequences intersect with patient safety. Hospitals commission audits of electronic medical record systems, IoT-enabled devices, and AI diagnostic platforms to demonstrate HIPAA and NIS2 alignment. Defense contractors follow closely, pressed by CMMC deadlines that require third-party attestation.

Manufacturing organizations, facing ransomware-induced downtime losses of USD 5.56 million per breach, increasingly audit operational-technology networks for segmentation efficacy and supply-chain resilience. Retailers reacted to headline incidents such as the Victoria’s Secret breach by hardening payment infrastructures and demanding audits of third-party service providers. Collectively, these dynamics diversify demand across the security audits and assessments industry without diluting the primacy of heavily regulated verticals.

By Deployment Mode: Remote Services Gain Traction Through Automation

On-site engagements retained 55% of 2024 revenues because critical infrastructure operators and high-classification environments still require physical presence for sensitive audits. Such projects encompass network walkthroughs, facility inspections, and stakeholder workshops that software cannot yet replace. They remain essential for segments like energy, defense, and healthcare where regulators expect direct evidence collection.

Remote and managed-service models are advancing at a 16.30% CAGR, buoyed by API-driven data collection, authenticated cloud scanners, and container-based testing agents. Automated validation tools feed centralized portals, enabling auditors to review results from anywhere and deliver remediation guidance asynchronously. Clients value predictable subscription fees and continuous monitoring over lump-sum project charges. Hybrid models are emerging where providers conduct annual on-site reviews supplemented by year-round remote validation, optimizing both cost and coverage. These shifts reinforce the scalability of the security audits and assessments market as labour constraints intensify.

Geography Analysis

North America generated 38% of 2024 revenue on the back of rigorous disclosure rules, a USD 12.7 billion federal cybersecurity budget, and strong vendor presence. United States organizations accelerated audits to meet SEC incident-reporting mandates and to prepare SBOM inventories for the February 2025 enforcement deadline. Canadian firms benefited from joint US-Canada threat-intelligence programs, while Mexican enterprises leveraged cross-border service contracts that bundle compliance and risk assessments. Market leadership is further anchored by NATO’s decision to earmark 1.5% of GDP for cybersecurity, assuring long-term public-sector spend on audits and critical-infrastructure validation projects.

Asia-Pacific is the fastest-growing region at a 14.00% CAGR, propelled by rising state-sponsored attacks and national capacity-building plans. Singapore’s unprecedented use of armed forces in cyberspace, plus CERT-In’s 9,708 audits completed in India during 2024, underscore the urgency of third-party assessments. Japan’s Digital Agency and South Korea’s K-Cyber strategy add regional tailwinds, while Chinese threat activity ironically boosts defensive budgets among neighbouring economies. The ASEAN Cybersecurity Cooperation Strategy harmonizes minimum assurance standards, creating multi-country opportunities for providers that can navigate diverse legal systems.

Europe’s outlook is shaped by the NIS2 Directive, EUR 390 million in Digital Europe Programme funding, and cross-border compliance complexities. Firms allocate 9% of IT budgets to security and expect staffing needs to rise sharply to meet deadlines. Germany and France invest heavily in critical-infrastructure audits, whereas Italy accelerates assessments to avoid EUR 10 million fines. Providers with pan-European delivery capabilities and deep regulatory knowledge gain competitive advantage. Meanwhile, the Middle East and Africa aim to surpass USD 3 billion in cybersecurity spend in 2025, translating into 16.6% growth for security services as governments push digital-economy agendas and adopt AI workloads.[4]Dark Reading, “Middle East, North Africa Security Spending to Top USD 3 Billion,” darkreading.com

Competitive Landscape

The security audits and assessments market displays moderate concentration. Deloitte leads with 30.7% of global security consulting revenue, leveraging a bench of 20,000 cyber specialists and ties to regulated industries. IBM combines consulting with technology platforms such as Guardium and QRadar to offer integrated assessments that span data, application, and network layers. Rapid7 generated USD 840 million in annualized recurring revenue in 2024, winning public-sector clients following progress toward FedRAMP certification for InsightGovCloud. Qualys grew 10% by merging vulnerability management, compliance, and cloud-security findings into its Enterprise TruRisk Platform, reducing the average audit preparation time by 40% for customers.

Palo Alto Networks absorbed IBM’s QRadar SaaS assets for USD 500 million, creating a joint SOC model that blends consulting reach with XSIAM analytics. Managed security service providers are diversifying into assessment work, leveraging automation to serve SME clients at scale. Niche firms specializing in AI security or post-quantum cryptography capture premium margins due to scarce expertise. Regional consultancies differentiate themselves through language fluency and proximity, addressing mid-market buyers who global giants often overlook. Overall, the security audits and assessments market balances incumbents’ breadth with challengers’ technology-first approaches.

Security Audits And Assessments Industry Leaders

International Business Machines Corporation (IBM Consulting)

Deloitte Touche Tohmatsu Ltd.

KPMG International Ltd.

Ernst & Young Global Ltd.

PricewaterhouseCoopers International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NATO allies pledged 1.5% of GDP for cybersecurity, securing future audit demand.

- May 2025: Victoria’s Secret breach triggered retailer focus on zero-trust and third-party risk reviews.

- March 2025: European Commission earmarked EUR 390 million for cybersecurity projects under Digital Europe Programme.

- February 2025: Rapid7 posted USD 840 million ARR and gained FedRAMP progress for InsightGovCloud.

Global Security Audits And Assessments Market Report Scope

| Compliance and Regulatory Audits |

| Penetration Testing |

| Vulnerability Assessment |

| Risk Assessment and Advisory |

| Cloud-Security / DevSecOps Assessment |

| Large Enterprises (Less than 1,000 Emp.) |

| Small and Medium Enterprises (More than 1,000 Emp.) |

| BFSI |

| Healthcare and Life-Sciences |

| Government and Defence |

| IT and Telecom |

| Manufacturing and Industrial |

| Retail and e-Commerce |

| On-site / Project-based |

| Remote / Managed-Service |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Service Type | Compliance and Regulatory Audits | ||

| Penetration Testing | |||

| Vulnerability Assessment | |||

| Risk Assessment and Advisory | |||

| Cloud-Security / DevSecOps Assessment | |||

| By Organisation Size | Large Enterprises (Less than 1,000 Emp.) | ||

| Small and Medium Enterprises (More than 1,000 Emp.) | |||

| By End-Use Industry | BFSI | ||

| Healthcare and Life-Sciences | |||

| Government and Defence | |||

| IT and Telecom | |||

| Manufacturing and Industrial | |||

| Retail and e-Commerce | |||

| By Deployment Mode | On-site / Project-based | ||

| Remote / Managed-Service | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the security audits and assessments market in 2030?

The market is expected to reach USD 16.42 billion by 2030, reflecting a 10.34% CAGR.

Which region is forecast to grow fastest in demand for security audits?

Asia-Pacific is projected to expand at a 14.00% CAGR through 2030, driven by rising state-sponsored threats and government investments.

How are supply-chain regulations such as SBOM influencing audit demand?

Mandatory SBOM disclosure laws in the United States and the EU are pushing organizations to commission detailed third-party assessments of software components and vendor practices.

Why do small and medium enterprises increasingly adopt managed security assessments?

Cloud-delivered, subscription-based services provide SMEs with affordable access to continuous audits without hiring in-house experts, supporting a 14.20% CAGR for this customer segment.

Which service category is growing fastest within security audits?

Cloud-security and DevSecOps assessments lead with an 18.40% CAGR as enterprises migrate workloads and embed security into software pipelines.

What is the main restraint limiting market expansion?

A global shortage of certified auditors inflates project costs and extends delivery timelines, shaving 1.8 percentage points off the forecast CAGR.

What drives demand for cloud forensics?

Ephemeral workloads and multicloud adoption require automated evidence capture that traditional on-prem tools cannot deliver.

Page last updated on: