Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

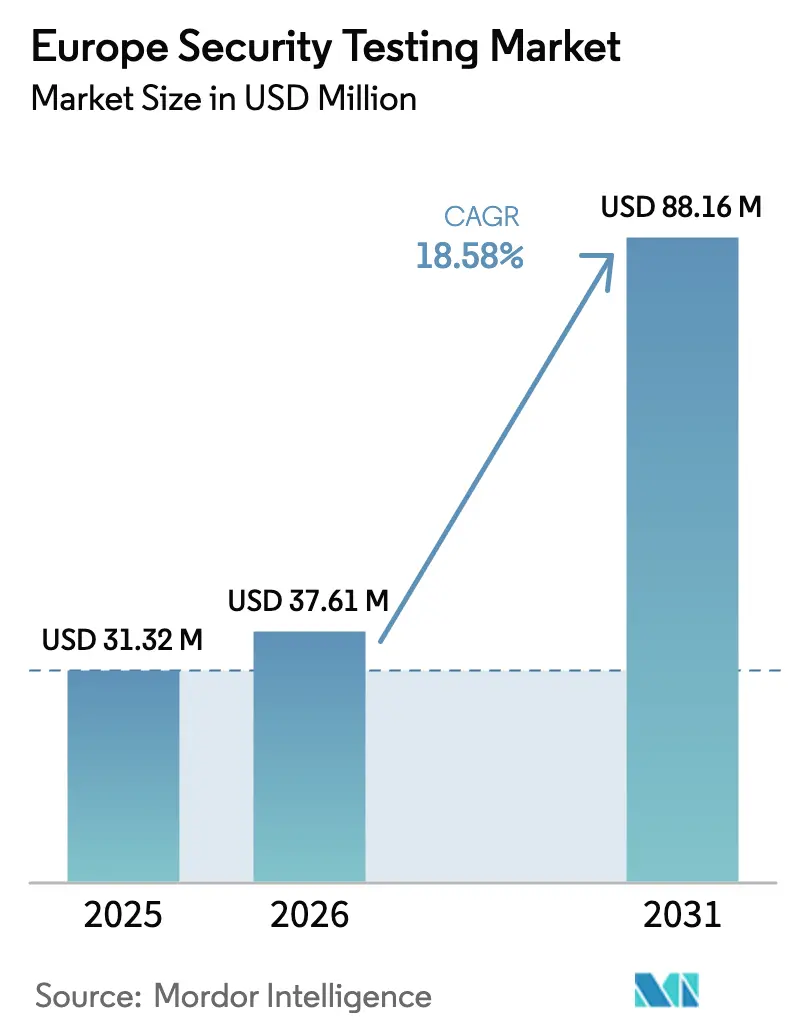

| Base Year Market Size (2025) | USD 31.32 Million |

| Market Size (2026) | USD 37.61 Million |

| Market Size (2031) | USD 88.16 Million |

| Growth Rate (2026 - 2031) | 18.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Security Testing Market Analysis by Mordor Intelligence

The Europe Security Testing Market size is projected to expand from USD 31.32 million in 2025 and USD 37.61 million in 2026 to USD 88.16 million by 2031, registering a CAGR of 18.58% between 2026 to 2031. Robust growth is underpinned by synchronized regulatory deadlines, a sharp rise in critical-infrastructure breaches, and the rapid spread of cloud-first development models. Germany’s Mittelstand factories, France’s public-sector digital-sovereignty programs, and the United Kingdom’s financial-services resilience agenda are shaping procurement priorities, while hybrid deployment architectures are becoming the default path to balance data-sovereignty needs with on-demand scalability. Vendor competition is intensifying as global consultancies, pure-play application security platforms, and local champions vie to offer bundled managed-testing subscriptions that address a widening skills gap. At the same time, artificial-intelligence analytics that suppress false positives are beginning to dictate buying decisions, especially among organizations fatigued by alert overload.

Key Report Takeaways

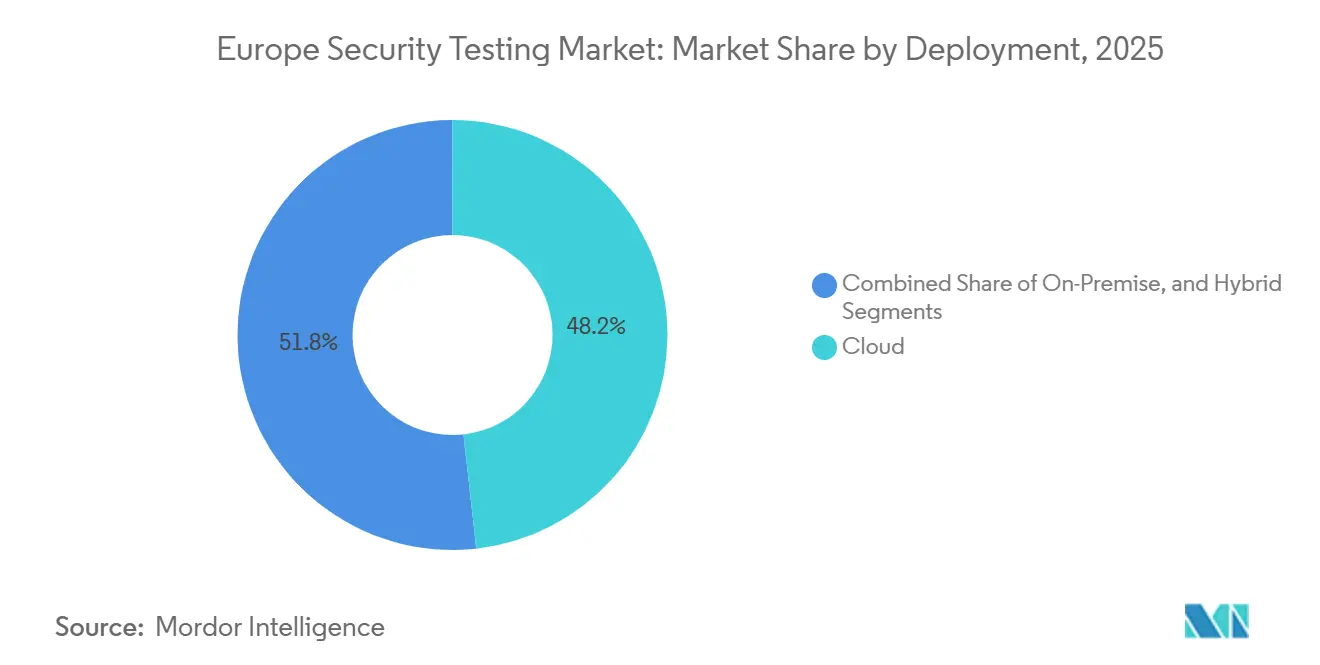

- By deployment, cloud solutions led with 48.23% of Europe security testing market share in 2025; hybrid models are advancing at a 18.73% CAGR through 2031.

- By type, application security testing accounted for 42.73% of the Europe security testing market size in 2025, while cloud application security testing is projected to expand at a 19.26% CAGR between 2026-2031.

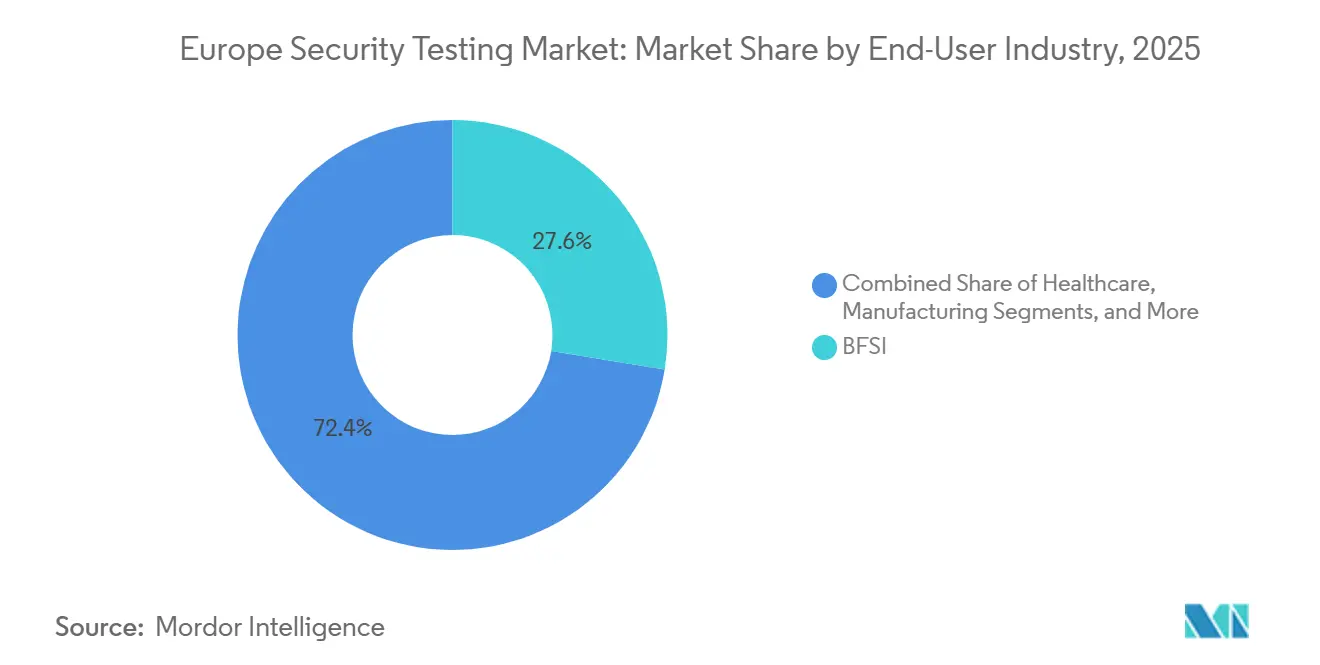

- By end-user industry, BFSI held 27.56% share of the Europe security testing market in 2025; manufacturing is forecast to grow fastest at 19.43% CAGR to 2031.

- By testing tool, penetration-testing frameworks captured 29.84% revenue share in 2025, whereas code-review platforms are expected to register a 20.06% CAGR to 2031.

- By country, Germany commanded 34.43% of 2025 revenue, but France is set to record the quickest growth at a 18.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Security Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail | +2.1% | Germany, Poland, France, pan-European energy and transport corridors | Short term (≤ 2 years) |

| Accelerated EU NIS2 and DORA Compliance Deadlines | +3.4% | EU-27 plus Norway, Iceland, Liechtenstein; strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Shift-Left DevSecOps Adoption in Software Supply-Chain | +1.8% | Global, with early gains in UK, Germany, Nordics | Medium term (2-4 years) |

| Industrial IoT Penetration in German Mittelstand Factories | +1.5% | Germany core, spillover to Austria, Czech Republic, Poland manufacturing hubs | Long term (≥ 4 years) |

| Mandatory Penetration-Testing Clauses in European Public-Sector Tenders | +1.7% | France, UK, Spain, Italy; emerging in Central and Eastern Europe | Medium term (2-4 years) |

| Quantum-Resistant Crypto Migration Pilots | +1.3% | EU-27, UK, Switzerland; led by financial services and government agencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

A 68% jump in serious incidents against European power and transport networks between 2024-2025 has moved continuous testing from a best practice to a board mandate.[1]European Union Agency for Cybersecurity, “NIS2 Directive,” enisa.europa.eu The 2024 ransomware disruption at Deutsche Bahn and the late-2024 DDoS attacks on Polish utilities exposed protocol weaknesses in operational-technology (OT) environments once thought to be insulated. Regulators now fine entities up to 2% of global turnover for failing to run quarterly vulnerability scans, prompting rail and grid operators to pre-book multi-year managed-testing contracts. Vendors able to decode Modbus, DNP3, and IEC 61850 traffic are winning deals because they offer actionable insights instead of generic advisories. In the short term, the scramble for OT specialists is tightening consulting supply, lifting project day rates and encouraging tool makers to embed industrial-protocol libraries directly into automated scanners.

Accelerated EU NIS2 and DORA Compliance Deadlines

NIS2 expanded the pool of regulated organizations from roughly 20,000 to 160,000 and DORA added heavy, scenario-based penetration-test obligations for 22,000 financial entities. Together, the statutes have created a steady pipeline of first-time buyers that previously relied on self-attestation. Early-enforcing states such as Germany and France already ask for test reports within 72 hours of critical findings, pushing enterprises toward SaaS platforms that can generate evidence artifacts on demand. Cloud providers and MSPs serving banks must also undergo audits, cascading compliance pressure through the supply chain. Over the medium term, this legal architecture institutionalizes security testing as a recurring operating expense, smoothing revenue visibility for vendors and raising the baseline demand floor across the continent.

Shift-Left DevSecOps Adoption in Software Supply-Chain

Static, dynamic, and composition analysis tools are shifting left into Git repositories as developers react to headline supply-chain intrusions. Fifty-eight percent of large European enterprises now scan code on every commit, up from 37% in 2022, and liability clauses in the 2024 Cyber Resilience Act are pushing the remainder to follow. Platforms that feed remediation tips into integrated development environments cut rework time and reduce security-team bottlenecks, making them attractive to agile squads under tight sprint cycles. Demand is most pronounced in United Kingdom fintechs and German automotive software units, where release cadences are daily or weekly. As artificial-intelligence coding assistants spread, real-time scan APIs are becoming table stakes, tilting the market toward vendors with developer-centric UX and generous free-tier entitlements.

Industrial IoT Penetration in German Mittelstand Factories

Two-thirds of midsize German manufacturers had at least one live Industrial IoT deployment by 2025, yet only a third had penetration-tested the associated OT networks.[2]VDMA, “Industry 4.0 Adoption in German Manufacturing,” vdma.org Because many programmable logic controllers are decades old, patch windows are rare, forcing companies to rely on compensating network controls whose effectiveness must be validated through testing. NIS2 now classifies critical component suppliers as essential entities, closing a long-standing enforcement gap. Over the long term, OT assessment capability will differentiate service providers, especially those who can bundle threat modeling with hands-on validation without halting production. Supply-chain pressure is already spilling into Austria, Czech Republic, and Poland as German OEMs impose contractual security clauses on tier-one and tier-two partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of CREST-Certified Security Testers | -1.9% | UK, Germany, Netherlands, Nordics | Short term (≤ 2 years) |

| Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening | -1.6% | Southern Europe (Italy, Spain, Portugal), Central and Eastern Europe | Short term (≤ 2 years) |

| Fragmented Data-Sovereignty Rules Slowing Cloud-Based Testing | -0.9% | France, Germany; emerging in Poland, Czech Republic | Medium term (2-4 years) |

| False-Positive Fatigue Reducing Test Frequency | -0.7% | Global, most acute in organizations with limited security-operations-center maturity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of CREST-Certified Security Testers

Europe needed at least 6,000 CREST-accredited professionals in 2025 but had only 4,200 on the rolls. Daily rates for senior testers rose 40% in two years, lengthening scheduling queues to as long as three months for regulated penetration tests. Some buyers have downgraded credential requirements to keep projects on track, eroding the standardization regulators intended. Tool vendors are exploiting the gap by touting continuous automated scanning as an interim substitute, but supervisors have yet to confirm whether such automation satisfies DORA’s threat-led scope. In the near term, the talent drought will remain a drag on Europe security testing market growth and will amplify wage inflation, especially in Germany and the Netherlands.

Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

Elevated European Central Bank rates curtailed small-business borrowing, pushing 42% of Southern European SMEs to cancel or delay digital projects in 2024.[3]European Investment Bank, “SME Access to Finance Survey 2024,” eib.org Cybersecurity has slipped down the capital-investment agenda for retailers, hospitality chains, and logistics brokers that operate on thin margins and face fewer explicit testing mandates. Many are stretching penetration-test cycles to 18-24 months and swapping licensed scanners for open-source tools despite higher false-positive loads. The restraint is short-lived because NIS2 fines and customer-driven assurance requests will ultimately force a catch-up cycle, yet in the interim it trims near-term opportunity in price-sensitive sub-regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Models Balance Compliance and Agility

Cloud platforms generated 48.23% of 2025 revenue, reflecting the appeal of pay-per-scan economics and zero appliance overhead in the Europe security testing market size. Demand stayed strong into 2026 as enterprises prioritized rapid scale-up for quarterly vulnerability sweeps. Hybrid approaches, however, show the highest 18.73% CAGR because regulated banks and hospitals keep sensitive data on-premise, routing only metadata to SaaS consoles for centralized policy enforcement. The arrangement satisfies national data-sovereignty statutes without sacrificing elastic compute, giving vendors with local datacenter footprints an edge.

On-premise appliances now serve a shrinking niche of defense contractors and air-gapped OT plants, but they remain non-negotiable where external connections are prohibited. Vendors are responding with containerized scanners shipped as virtual images that slot into existing private-cloud stacks, creating a stepping stone toward future hybrid conversions. Over the forecast window, improvements in confidential-computing chipsets and EU-level certification schemes are likely to narrow the perceived risk gap, nudging late adopters toward at least partial cloud orchestration.

By Type: Application Security Testing Dominates as Code Moves Center Stage

Application-level techniques represented 42.73% of 2025 turnover, confirming that exploitable code paths, not perimeter firewalls, now define enterprise exposure across the Europe security testing market. Within this bucket, cloud application security testing is accelerating at 19.26% CAGR because microservices, serverless functions, and ephemeral containers cannot be scanned by legacy network probes. Static analysis, dynamic analysis, and software composition analysis are routinely chained together in CI/CD pipelines, pushing scan counts into the thousands each month for large DevOps shops.

Mobile and web application testing remains relevant, particularly among digital-banking and e-commerce providers bound by PSD2 secure-communication clauses. Yet the deepest innovation capital is migrating to cloud-native runtime visibility, where interactive testing tools instrument code and correlate data-flow evidence to slash false positives. Vendor differentiation now stems from how seamlessly platforms slot into GitHub Actions, GitLab CI, and Bitbucket workflows, and from their ability to flag vulnerable open-source libraries before pull requests are merged.

By End-User Industry: BFSI Anchors Spending, Manufacturing Accelerates

Banks, insurers, and asset managers absorbed 27.56% of market spending in 2025 because DORA compels threat-led penetration tests every three years and places liability on boards for operational-resilience lapses. Institutions are standardizing on multi-year testing retainers that bundle red-team services, static code scanning, and continuous attack-surface management, cementing BFSI as the anchor tenant of the Europe security testing market share.

Manufacturing posts a brisk 19.43% CAGR as Industry 4.0 retrofits extend corporate LANs onto the shop floor, making programmable logic controllers reachable from the internet. Automotive suppliers in Germany and Italy are early movers, and subsidies for digital twins across Central Europe are widening the addressable base. Healthcare, government, and telecom show above-average growth, propelled by connected-device proliferation and explicit NIS2 essential-entity classifications, whereas retail and hospitality trail because of margin pressure and looser regulatory scrutiny.

By Testing Tool: Penetration Frameworks Lead, Code Review Gains Speed

Penetration-testing suites such as Metasploit and Burp Suite delivered 29.84% of 2025 revenue, reflecting their entrenchment in public-sector frameworks that cite CREST or equivalent credentials. Yet code-review engines, which underpin shift-left DevSecOps, are scaling faster at 20.06% CAGR. Enterprises appreciate the immediate developer feedback loop and the ability to block high-severity commits automatically, reducing remediation cost.

Web application scanners, API fuzzers, and OT-specific protocol testers round out the toolbox. Innovation focus is turning toward interactive and runtime agents that self-protect applications in production, a pattern already piloted by large online retailers ahead of the holiday shopping season. Vendors that unite static, dynamic, and runtime telemetry in one console are best positioned to cross-sell modules and raise account stickiness.

Geography Analysis

Germany accounted for 34.43% of 2025 spending after the Federal Office for Information Security mandated quarterly scans for rail, energy, and health operators. Local demand is also fueled by automotive OEMs forcing suppliers to demonstrate Europe security testing market compliance inside joint-venture plants. The United Kingdom remains a heavyweight, buoyed by London’s financial hub and the National Cyber Security Centre’s active-defense initiatives, even though local frameworks now diverge slightly from EU-wide standards post-Brexit.

France is on a 18.87% CAGR trajectory as the doctrine of digital sovereignty compels agencies to contract French-certified providers and mandates in-country cloud regions. The Nordics and the Netherlands display the highest per-capita cybersecurity spend, reflecting mature digital economies and cultural emphasis on privacy. Southern and Eastern Europe expand more slowly because SMEs face tighter credit conditions and often defer discretionary security budgets.

Data-sovereignty fragmentation remains the region’s structural friction point. SecNumCloud in France, C5 in Germany, and separate Dutch baseline rules force SaaS vendors to spin up local instances and pass multiple audits, increasing operating costs. The EU Cybersecurity Certification Framework intends to harmonize requirements over time, but practical mutual recognition is several years off, keeping hybrid deployment models in favor for the foreseeable future.

Competitive Landscape

Europe security testing market competition is moderate-to-high and fragmenting along capability lines. Global consultancies such as Accenture, IBM, and PwC offer integrated advisory, testing, and remediation, courting highly regulated sectors that seek single-throat-to-choke accountability. Pure-play application security vendors Synopsys, Veracode, Checkmarx, Rapid7 focus on developer tooling and automated coverage, while regional specialists like Orange Cyberdefense and NCC Group differentiate through language proximity and regulator familiarity.

Mergers and acquisitions are accelerating. Synopsys bought Cybellum to bolster embedded-device testing, and CrowdStrike folded Bionic’s application-posture analytics into its endpoint stack, signalling a swing toward full-lifecycle platforms. Financing rounds remain robust, exemplified by Checkmarx’s USD 300 million Series E, indicating investor confidence in multi-module product roadmaps. Subscription pricing, artificial-intelligence powered triage, and managed-service overlays are further blurring vendor categories.

White-space remains in mid-market managed testing, where firms with 250-2,000 employees need outcome-based packages that bundle tooling, analyst triage, and immediate remediation guidance. Operational-technology penetration remains underserved because protocol expertise is rare and on-premise test safety constraints are high. Open-source tool ecosystems led by OWASP ZAP and Nuclei continue to nibble at entry-level budgets, but enterprises typically layer commercial analytics over these engines to satisfy audit evidence and service-level agreement needs.

Europe Security Testing Industry Leaders

Accenture plc

Atos SE

Cisco Systems, Inc.

Core Security, LLC

CrowdStrike Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Synopsys opened a Munich research hub staffed by 150 engineers focusing on automotive and Industrial IoT security testing, aligning services with NIS2 OT mandates.

- December 2025: CrowdStrike completed its USD 350 million acquisition of Bionic, adding runtime application inventory and risk prioritization to the Falcon platform.

- November 2025: Orange Cyberdefense won a EUR 120 million (USD 129 million) five-year contract from France’s Ministry of the Interior to perform annual penetration tests across 450 agencies.

- October 2025: IBM introduced a Quantum-Safe Cryptography Assessment Service for European financial institutions, piloting engagements at Deutsche Bank and the European Central Bank.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe security testing market as all spending, expressed in US dollars, on software tools and professional or managed services whose primary purpose is to probe applications, networks, devices, and cloud workloads for security weaknesses and verify control effectiveness across European enterprises and public agencies.

Scope Exclusions: Vulnerability-management platforms that produce posture reports without executing live tests and generic quality-assurance services remain outside this boundary.

Segmentation Overview

- By Deployment

- On-Premise

- Cloud

- Hybrid

- By Type

- Network Security Testing

- VPN Testing

- Firewall Testing

- Other Service Types

- Application Security Testing

- Mobile Application Security Testing

- Web Application Security Testing

- Cloud Application Security Testing

- Enterprise Application Security Testing

- Network Security Testing

- By Testing Type

- SAST

- DAST

- IAST

- RASP

- By End-User Industry

- Government

- BFSI

- Healthcare

- Manufacturing

- IT and Telecom

- Retail

- Other End-User Industries

- By Testing Tool

- Web Application Testing Tool

- Code Review Tool

- Penetration Testing Tool

- Software Testing Tool

- Other Testing Tools

- By Country

- United Kingdom

- Germany

- France

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Cyber-risk officers, DevSecOps leads, and managed testing providers in the United Kingdom, Germany, France, the Nordics, and Eastern Europe shared contract values, cloud adoption ratios, and test-cycle frequencies.

Their inputs helped us cross-check secondary findings, close data gaps, and firm up our assumptions.

Desk Research

We began by mapping the regulatory spine using GDPR breach statistics, ENISA threat-landscape bulletins, and EU texts on NIS2 and DORA. Eurostat ICT spending tables, incident disclosures from the UK Information Commissioner, position papers from the European Cyber Security Organisation, and patent pulls through Questel added volume and technology insight. Company 10-Ks, investor decks, and curated news on Dow Jones Factiva supplied price points and roll-out timelines. This list is indicative only; many more open sources informed collection, validation, and clarification.

Market-Sizing & Forecasting

We first applied a top-down reconstruction that scales European IT-security expenditure with vertical-level testing intensity ratios. We then corroborated totals with selective bottom-up checks such as sampled average selling price multiplied by test volumes from channel interviews. Key variables fed into the model include:

count of DORA-regulated financial institutions,

share of workloads running in public cloud,

annual critical-infrastructure cyberattack incidents,

DevSecOps pipeline penetration across software teams,

mean GDPR penalty per breach,

average penetration-test frequency per 1,000 endpoints.

A multivariate regression blended with ARIMA error correction projects 2025-2030 results, while scenario analysis handles macro shocks. Where supplier roll-ups underrepresent small-firm spend, public-tender data interpolate the missing values.

Data Validation & Update Cycle

Mordor analysts run variance checks against quarterly earnings releases, Eurostat cyber breach tallies, and trade-association benchmarks.

Any anomaly wider than two standard deviations triggers senior review before sign-off.

Reports refresh every twelve months, and interim revisions follow material regulatory or M&A events.

A final sweep before delivery lets clients receive the latest view.

Why Our Europe Security Testing Baseline Commands Reliability

Published market values often diverge because firms draw different boundaries, apply unlike pricing curves, or update on separate cadences.

Key gap drivers for other publishers include limiting scope to application testing only, inflating totals by adding vulnerability management spend, relying on static 2023 price lists, or applying single-moment currency conversions. Mordor Intelligence refreshes annually, aligns variables with current regulations, and grounds prices in fresh interviews, which keeps our baseline steady and transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 31.32 B | Mordor Intelligence | - |

| USD 8.00 B | Regional Consultancy A | Omits network and cloud testing, few expert interviews |

| USD 2.98 B | Trade Journal B | Uses out-of-date ASPs, single-rate currency conversion |

The comparison shows that our disciplined scope, regulator-anchored variables, and continuous data maintenance deliver a balanced baseline that planners can reproduce and trust.

Key Questions Answered in the Report

How fast is security-testing spending growing in Europe?

Revenue in the Europe security testing market is projected to rise at a 18.58% CAGR between 2026-2031, reaching USD 17.62 billion by the end of the forecast window.

Which deployment model is gaining the most traction?

Hybrid deployment is expanding at 18.73% CAGR because it satisfies both data-sovereignty regulations and the need for elastic compute.

Why do banks account for the largest share of spending?

BFSI entities must run threat-led penetration tests every three years under DORA, driving sustained investment in multi-layer testing services.

What is the main talent constraint in Europe?

A 30% shortfall in CREST-certified testers is lengthening project lead times and inflating day rates across the region.

Which country is growing fastest?

France shows the highest forecast growth at a 18.87% CAGR, propelled by domestic-cloud mandates and public-sector testing clauses.

Page last updated on: