Cybersecurity Certifications Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

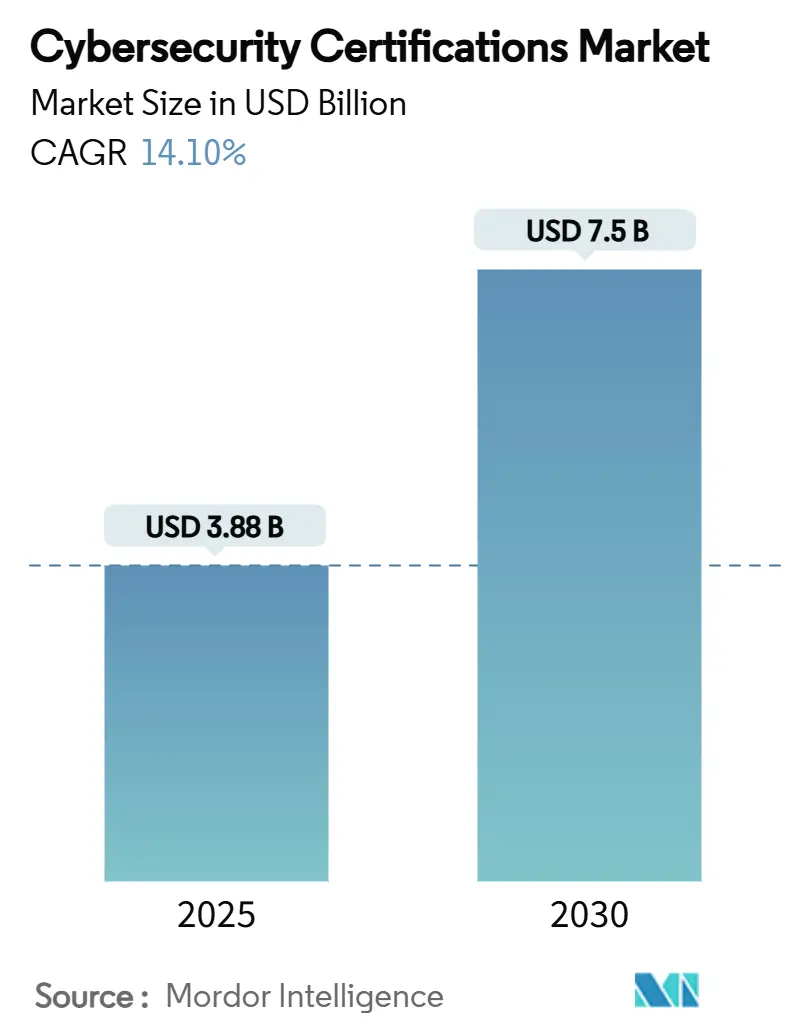

| Market Size (2025) | USD 3.88 Billion |

| Market Size (2030) | USD 7.5 Billion |

| Growth Rate (2025 - 2030) | 14.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity Certifications Market Analysis by Mordor Intelligence

The cybersecurity certifications market size stood at USD 3.88 billion in 2025 and is forecast to reach USD 7.50 billion by 2030, reflecting a 14.1% CAGR through the period. Growing breach costs, a workforce gap of 4.7 million unfilled roles, and tighter regulations keep demand for verified skills high. Governance-focused credentials, cloud-specific programs, and AI-related tracks now dominate enrollment patterns as employers link insurance discounts and compliance outcomes to documented staff expertise. Provider consolidation, especially private-equity-backed moves, is reshaping product strategy while affordable self-paced eLearning and MOOC formats widen global reach. North America retains spending leadership, yet Asia-Pacific delivers the fastest expansion on the back of state-funded vouchers and rapid digitalisation. [1]European Union Agency for Cybersecurity (ENISA), “NIS Investments 2024,” enisa.europa.eu

Key Report Takeaways

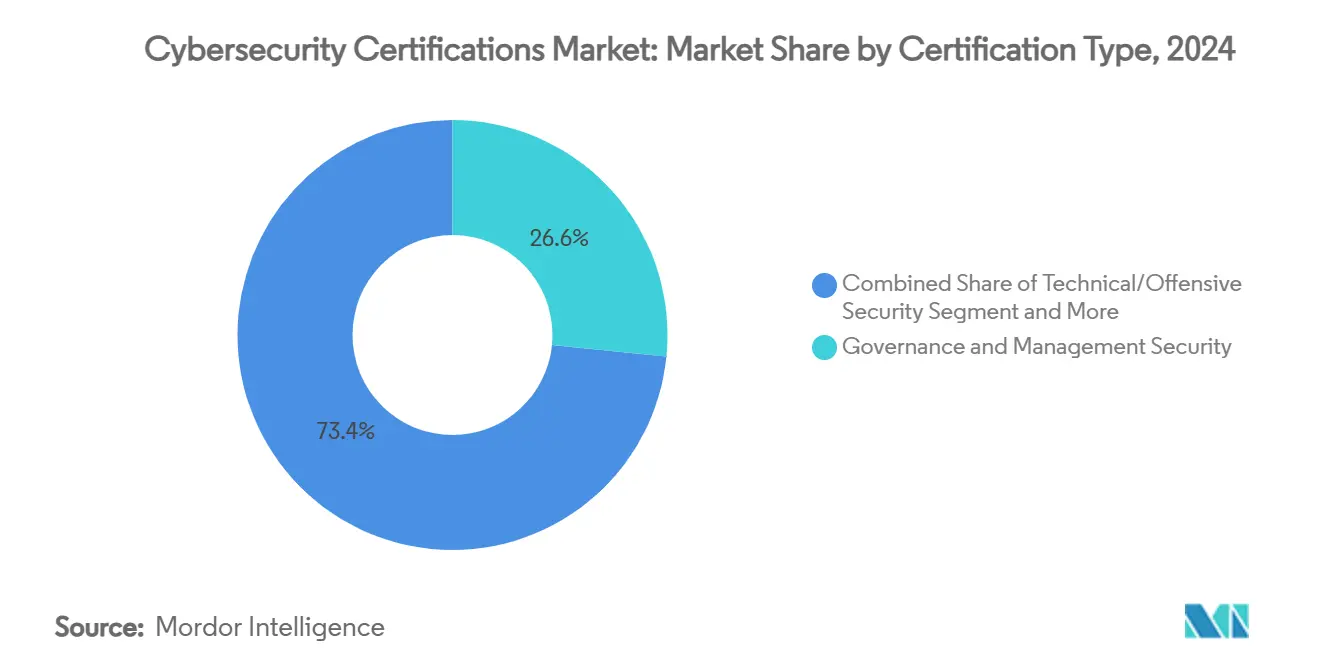

- By certification type, Governance and Management Security led with 26.6% revenue share in 2024 of the cybersecurity certifications market, whereas Cloud Security is projected to advance at a 15.3% CAGR to 2030.

- By delivery mode, self-paced eLearning held 33.3% of the cybersecurity certifications market share in 2024, while MOOCs recorded the highest projected CAGR at 15.2% through 2030.

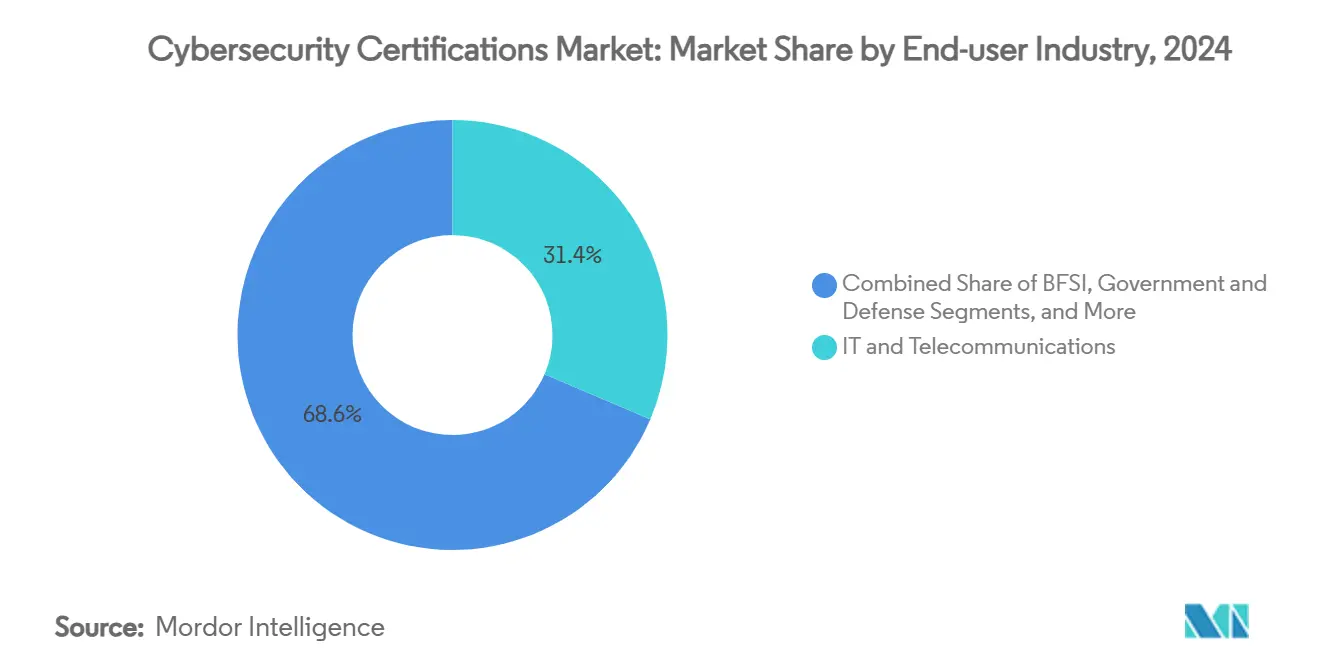

- By end-user industry, IT and Telecommunications accounted for a 31.4% share of the cybersecurity certifications market size in 2024, and Education and Training Providers are expanding at a 15.4% CAGR through 2030.

- By skill level, foundation programs captured a 40.1% share in 2024 of the cybersecurity certifications market; advanced-level tracks are rising fastest at a 15.9% CAGR to 2030.

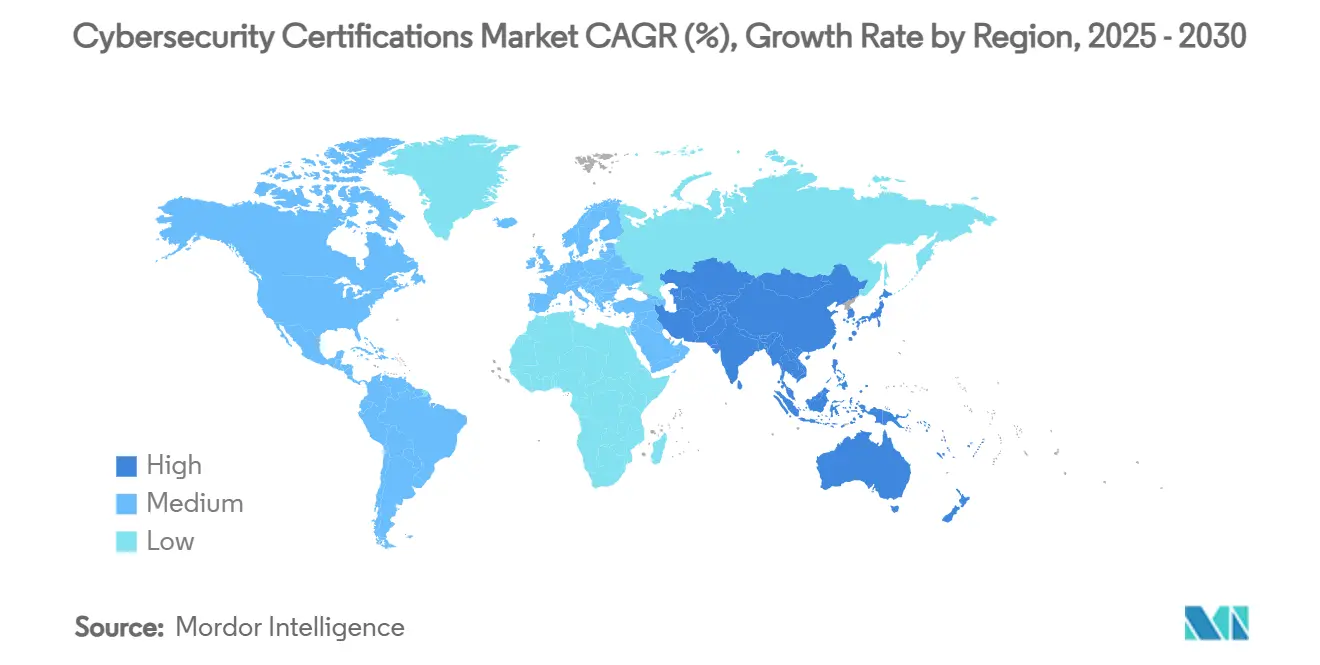

- By geography, North America held 38.3% of the cybersecurity certifications market share in 2024, whereas Asia-Pacific is forecast to post a 15.7% CAGR to 2030.

Global Cybersecurity Certifications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cyber-attack volume and breach costs | +3.2% | Global | Short term (≤ 2 years) |

| Expanding regulatory mandates (GDPR, NIS-2, etc.) | +2.8% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Global cybersecurity skills gap | +2.1% | Global, acute in APAC and North America | Long term (≥ 4 years) |

| Cloud/AI/IoT adoption spurs niche certifications | +1.9% | North America and APAC core, spill-over to Europe | Medium term (2-4 years) |

| Cyber-insurance underwriting tied to staff credentials | +1.4% | North America and Europe | Medium term (2-4 years) |

| Government-funded voucher programs in emerging markets | +0.8% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating cyber-attack volume and breach cost

Average breach expenses climbed to USD 4.88 million in 2025, and healthcare incidents almost doubled that level, forcing boards to fund skills that shorten dwell time and preserve insurability. [2]DeepStrike, “Cybersecurity Statistics 2025,” deepstrike.io Asia-Pacific absorbed 31% of all attacks in 2024, pushing enterprises to treat certified staff as the primary line of defence. With ransomware now striking more than 75% of organisations, demand is shifting toward incident-response and cloud-specific pathways that validate hands-on capabilities. Human error’s 95% contribution to breaches sustains interest in awareness-oriented credentials, while premium pricing for cloud security certificates mirrors the 82% share of breaches hitting hosted data.

Expanding regulatory mandates

The EU’s NIS-2 directive obliges essential-service operators to upgrade security staffing, with 89% anticipating additional headcount to remain compliant. Financial entities preparing for the Digital Operational Resilience Act face fixed incident-reporting windows that require auditors with ISO 27001 and ISO 27002 cross-coverage. Payment firms tackling PCI DSS 4.0 transition seek multi-factor-authentication expertise, lifting demand for niche payment-security exams. Similar rulebooks surface in the Asia-Pacific region, signalling a cascading wave of mandatory credentialing across supply chains.

Persistent global cybersecurity skills gap

Unfilled roles surpass 3.5 million and inflate salary offers, with certified U.S. practitioners earning an average of USD 147,138 in 2024, up 23% on 2021. The European Union alone lacks 274,000 professionals, prompting free entry-level study programmes that registered 24,000 enrollees within a year. Employers increasingly substitute degrees with certification-backed hiring, and alternative scholarships such as the Cyber Million initiative provide cost-free training to widen talent funnels.

Cloud/AI/IoT adoption creating niche tracks

Multi-cloud architectures and embedded AI reshape threat models, giving rise to credentials like the Trusted AI Safety Knowledge scheme launched in 2025. Industrial IoT risk drives uptake of ISA/IEC 62443 certificates among manufacturers connecting operational technology to IT networks. Ethical-hacking syllabi now fold in AI-assisted exploits, illustrating how syllabus agility must match fast-changing attacker methods. Big-ticket deals, such as Google’s USD 23 billion purchase of Wiz, underscore enterprise willingness to pay for cloud-security mastery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High exam and renewal costs for SMEs | -1.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Rapid technology shifts shorten certification shelf-life | -1.2% | Global, pronounced in tech-advanced regions | Medium term (2-4 years) |

| Rise of micro-badges challenges broad credentials | -0.9% | North America and Europe | Medium term (2-4 years) |

| Abundance of free online content dilutes perceived value | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High exam and renewal costs for SMEs

Fees remain prohibitive: a CISSP exam alone costs USD 749, and renewal adds recurring outlays, squeezing limited training budgets. CompTIA charges USD 75-150 for each three-year renewal, while EC-Council levies yearly continuing-education fees, multiplying the life-cycle cost. SMEs consequently postpone credentials or rely on uncertified talent, decelerating security maturity.

Rapid technology shifts shorten certification shelf-life

AI-driven tools, quantum-resistant cryptography, and monthly cloud-service releases erode the currency of static curricula. Professionals often chase multiple vendor-specific badges, pushing total study time and expenses upward. Certification bodies counter with shorter renewal cycles and modular micro-badges, yet the faster turnover raises total cost-of-ownership and confuses buyers about long-term relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Certification Type: Governance steers spend while cloud surges

Governance and Management Security credentials accounted for 26.6% of the cybersecurity certifications market size in 2024 as boards linked audit readiness and insurance premiums to documented oversight skills. Uptake remains strong among regulated industries that must evidence structured controls during external reviews. Market-standard tracks such as CISM and ISO 27001 Lead Auditor anchor executive awareness programmes and continue to influence cross-industry procurement patterns. Cloud Security paths, while smaller in absolute terms, grow at a 15.3% CAGR thanks to workload migration and the visibility of cloud breaches. They command premium exam pricing and often sit atop employer-funded learning lists, reflecting urgent asset-protection priorities.

Technical and Offensive Security certificates sustain momentum by integrating AI-enabled attack simulation within syllabi, a feature that keeps curricula relevant as adversaries automate reconnaissance. Entry-level Core Security credentials maintain broad appeal for career changers and remain mandated for certain government roles. Industrial-IoT, Audit and Compliance, and Privacy tracks round out the portfolio, each benefitting from targeted regulations that compel sector-specific expertise. The diversity within the segment positions vendors to upsell learners from foundation badges to layer-specific specialisations, widening lifetime customer value across the cybersecurity certifications market.

By Delivery Mode: Flexible eLearning commands share, MOOCs accelerate access

Self-paced eLearning captured 33.3% of the cybersecurity certifications market share in 2024, mirroring employers' lean-in to asynchronous study that minimizes downtime. The format’s modular design suits incremental learning goals and eases global roll-out across distributed teams. Providers enhance value with AI-guided revision tools that raise pass rates and shorten preparation time.

MOOCs are scaling fastest at a 15.2% CAGR, propelled by university-vendor alliances that bundle professional certificates with academic credit. [3]Coursera, “Google Cloud Cybersecurity Professional Certificate,” coursera.org Instructor-led Virtual classes hold mid-tier appeal, balancing interactive depth with travel-free convenience. Immersive cyber ranges deliver the highest engagement for specialist tracks such as Red Teaming, with vendors like Thales simulating sector-specific scenarios from banking to aerospace. Classroom and bespoke on-site formats persist for hardware-intensive courses or classified environments but cede volume to digital alternatives as bandwidth and VR tools improve.

By End-user Industry: IT maintains lead, education races ahead

IT and Telecommunications held 31.4% of the cybersecurity certifications market size in 2024, reflecting its dual identity as breach target and security service provider. Spending remains recurrent as managed-service firms must keep consultants certified to meet client SLAs.

Education and Training Providers show the briskest rise at a 15.4% CAGR, becoming both consumer and supplier of credentials through bootcamps, degree integrations, and scholarship programmes. BFSI entities mandate payment-security and resilience badges to guard high-value data pipelines. Government and Defence stay active through stipulations such as DoD 8570, while Healthcare requests HIPAA-aligned tracks to curb record-set breach costs. Manufacturing leans toward ISA/IEC 62443 to protect converged OT/IT estates, and energy utilities favour NERC CIP courses to fortify grid assets.

By Skill Level: Foundation dominates volume, advanced drives value

Foundation courses amassed a 40.1% share in 2024, fuelled by free-to-low-cost programmes that funnel newcomers into the profession. They address entry-level scarcity and offer an on-ramp for vocational switchers without computing backgrounds.

Advanced-level tracks expand fastest at 15.9% CAGR and increasingly emphasise cloud-native defence, AI governance, and zero-trust architecture. Employers cite these badges when assigning project leadership or calculating insurance risk, elevating their compensation premiums. Intermediate certificates bridge the gap with lab-heavy curricula, while expert-tier designations remain niche but lucrative amid limited instructor capacity. Modular micro-credentials allow professionals to maintain currency between major exam cycles, sustaining engagement and upsell opportunities across the cybersecurity certifications market.

Geography Analysis

North America controlled 38.3% of the cybersecurity certifications market share in 2024, underpinned by strict compliance frameworks and abundant corporate budgets. Federal grants and programmes like the White House workforce initiative subsidise training pathways that funnel candidates into high-paying roles. Universities partner with cloud giants to issue no-cost certificates for veterans, bolstering labour supply and corporate diversity targets. Cyber-insurance carriers increasingly link premium discounts to credential counts, reinforcing virtuous cycles of learning spend.

Asia-Pacific delivers the highest regional CAGR at 15.7%, buoyed by state-funded vouchers, growing cyber-insurance adoption, and 31% of global attack volume. India’s policy incentives for AI-oriented skills, Singapore’s SkillsFuture credits, and China’s critical-infrastructure law collectively multiply enrolments. Emerging economies such as Thailand and Vietnam chase digital-banking rollout timelines, triggering demand for both foundation and cloud-security certificates. Multinational firms localise exam centres and vernacular courseware to capture this surge.

Europe stays regulation-led: NIS-2 and the Digital Operational Resilience Act oblige essential service operators and financial entities to verify staff competence, spurring steady uptake of governance and audit tracks. National initiatives like the UK Cyber Local projects fund regional hubs that blend community development with targeted skills pipelines. South America, the Middle East, and Africa represent nascent but strategic frontiers where World Bank and ITU programmes channel USD 250 million into cyber-capacity building, seeding future demand for recognised credentials.

Competitive Landscape

Private equity reshapes the sector. The 2024 sale of CompTIA to H.I.G. Capital and Thoma Bravo turn a long-standing non-profit into a for-profit vehicle positioned to accelerate platform investment and global marketing. [4]MSSP Alert, “CompTIA Sold to Private Equity,” msspalert.com Similar capital inflows surfaced when Leeds Equity Partners bought OffSec, recognising the premium commanded by lab-centric, hands-on certifications. Acquisition logic centres on scale, curriculum refresh speed, and the ability to cross-sell continuous-learning subscriptions.

Partnership strategy has become a key differentiator. ISC2 aligned with IBM and the Linux Foundation to embed secure-coding competencies in open-source supply chains. SANS Institute’s joint offering with Microsoft boosts cloud-security coverage while its GEIR badge targets leadership skills often missing from purely technical programmes. Cloud Security Alliance collaborates with Northeastern University to pioneer AI-safety certification, capturing first-mover advantage in a rapidly emerging risk domain.

Technology adoption in training products is rising. Vendors deploy AI tutors that personalise study plans, predictive analytics that flag drop-out risk, and VR-based cyber ranges that replicate real-world breach dynamics. Micro-badges issued by Palo Alto Networks record discrete competencies, challenging traditional multi-year certificates by offering smaller, stackable proofs of skill. The combined market share of the top five vendors sits near 45%, signalling a moderately concentrated arena yet still open to niche specialists that address sector-specific or regional compliance needs.

Cybersecurity Certifications Industry Leaders

International Information System Security Certification Consortium (ISC)²

Computing Technology Industry Association (CompTIA)

International Council of E-Commerce Consultants (EC-Council)

Information Systems Audit and Control Association (ISACA)

Global Information Assurance Certification (GIAC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: LevelBlue acquired Trustwave to form the largest independent MSSP, blending AI-enhanced detection with FedRAMP-approved services.

- April 2025: Google finalised its USD 23 billion purchase of Wiz, bolstering multi-cloud security capacity.

- February 2025: SANS Institute launched GEIR Certification aimed at bridging tactical expertise and executive decision-making.

- January 2025: Quorum Cyber bought Kivu Consulting, adding 24/7 incident-response coverage across North America and the UK.

- November 2024: Thoma Bravo and H.I.G. Capital agreed to acquire CompTIA’s certification portfolio, shifting it to a growth-focused corporate structure.

Global Cybersecurity Certifications Market Report Scope

| Governance and Management Security (e.g., CISSP, CISM) |

| Technical/Offensive Security (e.g., OSCP, CEH, GPEN) |

| Cloud Security (e.g., CCSP, CCSK, AWS Security Specialty) |

| Audit and Compliance (e.g., CISA, ISO/IEC 27001 Lead Auditor) |

| Privacy and Data Protection (e.g., CIPP, CIPM, GDPR-P) |

| Entry-level Core Security (e.g., CompTIA Security+, SSCP) |

| Industrial and IoT Security (e.g., ISA/IEC 62443, GICSP) |

| Self-paced eLearning |

| Instructor-led Virtual (Live Online) |

| Instructor-led Classroom (Physical) |

| Corporate On-site/Bespoke Cohort |

| Immersive Virtual Labs/Cyber-Ranges |

| Massive Open Online Courses (MOOCs) |

| IT and Telecommunications |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Retail and E-commerce |

| Energy and Utilities |

| Education and Training Providers |

| Other End-user Industries |

| Foundation (Entry-level) |

| Intermediate (Practitioner) |

| Advanced (Professional) |

| Expert/Specialist (Master-level) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Certification Type | Governance and Management Security (e.g., CISSP, CISM) | ||

| Technical/Offensive Security (e.g., OSCP, CEH, GPEN) | |||

| Cloud Security (e.g., CCSP, CCSK, AWS Security Specialty) | |||

| Audit and Compliance (e.g., CISA, ISO/IEC 27001 Lead Auditor) | |||

| Privacy and Data Protection (e.g., CIPP, CIPM, GDPR-P) | |||

| Entry-level Core Security (e.g., CompTIA Security+, SSCP) | |||

| Industrial and IoT Security (e.g., ISA/IEC 62443, GICSP) | |||

| By Delivery Mode | Self-paced eLearning | ||

| Instructor-led Virtual (Live Online) | |||

| Instructor-led Classroom (Physical) | |||

| Corporate On-site/Bespoke Cohort | |||

| Immersive Virtual Labs/Cyber-Ranges | |||

| Massive Open Online Courses (MOOCs) | |||

| By End-user Industry | IT and Telecommunications | ||

| BFSI | |||

| Government and Defense | |||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Retail and E-commerce | |||

| Energy and Utilities | |||

| Education and Training Providers | |||

| Other End-user Industries | |||

| By Skill Level | Foundation (Entry-level) | ||

| Intermediate (Practitioner) | |||

| Advanced (Professional) | |||

| Expert/Specialist (Master-level) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the cybersecurity certifications market by 2030?

The cybersecurity certifications market is projected to reach USD 7.50 billion by 2030, up from USD 3.88 billion in 2025.

Which certification category is growing fastest?

Cloud Security credentials record the highest growth, advancing at a 15.3% CAGR through 2030.

Which delivery mode currently captures the largest market share?

Self-paced eLearning leads with 33.3% share as of 2024.

Why is Asia-Pacific the fastest-growing region?

Rapid digitalisation, government-funded vouchers, and a high incidence of cyberattacks propel Asia-Pacific at a 15.7% regional CAGR.

How do regulations influence certification demand?

Mandates such as the EU’s NIS-2 and the Digital Operational Resilience Act compel firms to verify staff skills, directly boosting certification uptake.

What challenge do small businesses face in adopting certifications?

High exam and renewal fees combined with limited budgets often delay SME participation in formal credential programmes.

Page last updated on: