Market Overview

| Study Period | 2020 - 2031 |

|---|---|

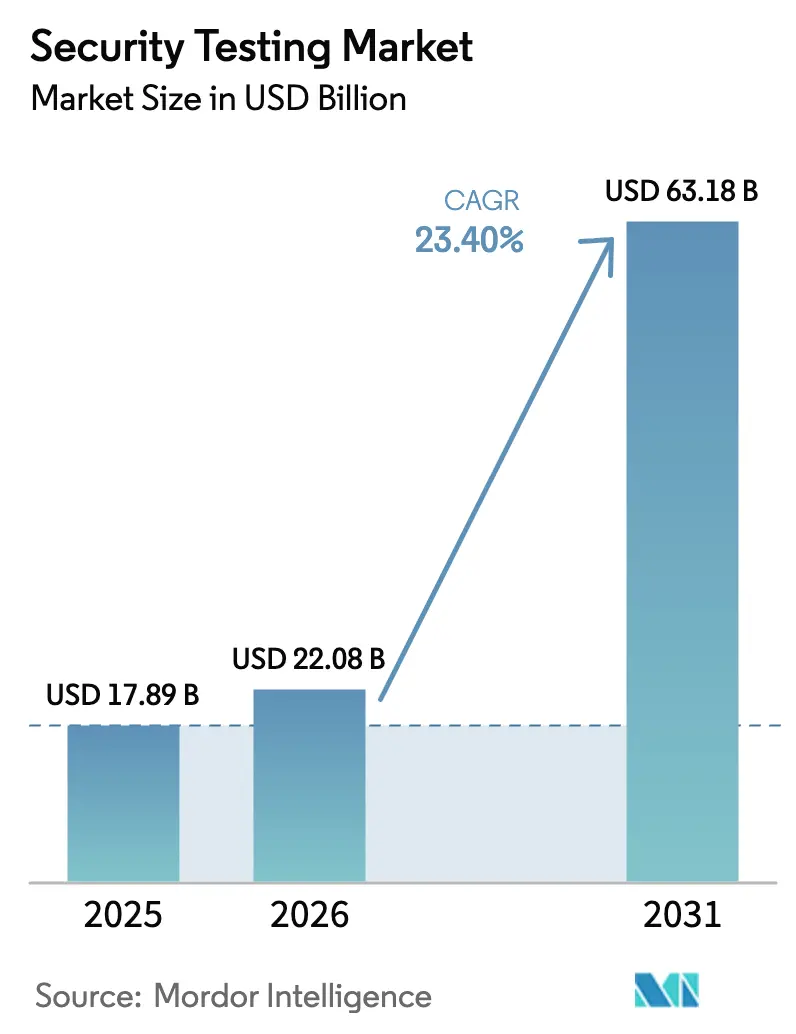

| Market Size (2026) | USD 22.08 Billion |

| Market Size (2031) | USD 63.18 Billion |

| Growth Rate (2026 - 2031) | 23.40% CAGR |

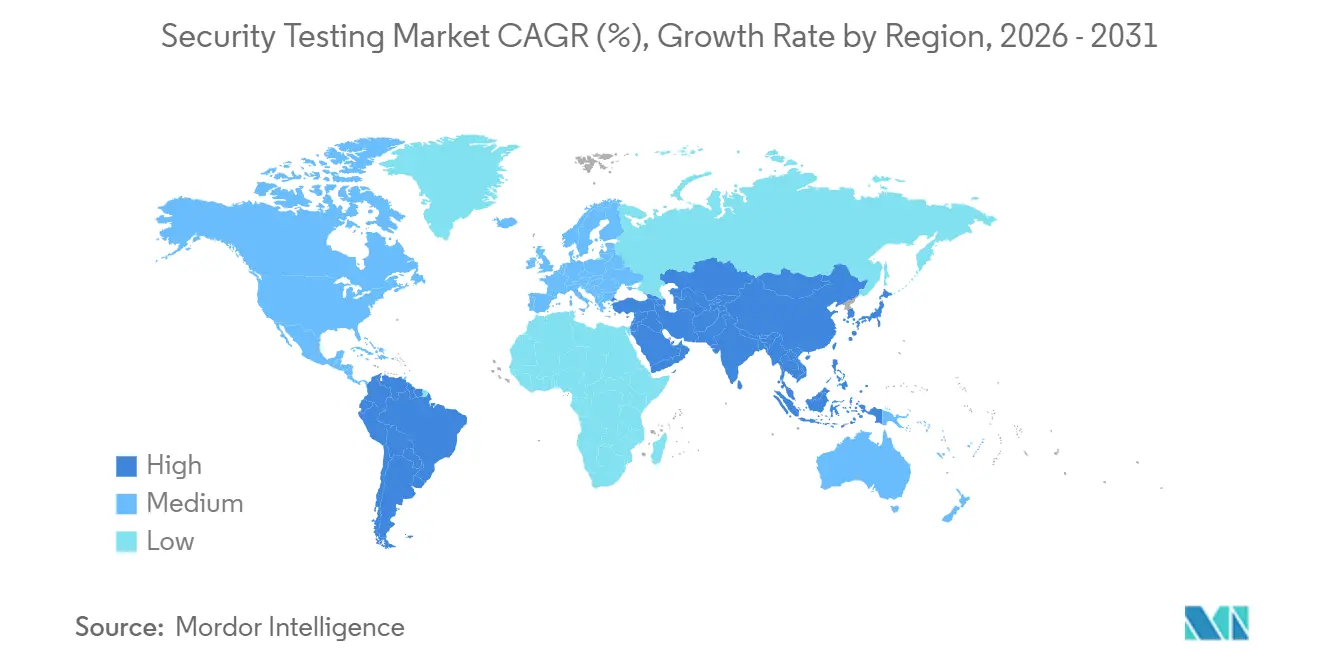

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Security Testing Market Analysis by Mordor Intelligence

The security testing market size is USD 22.08 billion in 2026 and is projected to reach USD 63.18 billion by 2031, registering a 23.40% CAGR over the forecast period. Demand accelerates as mandatory software bill of materials disclosure under United States Executive Order 14028 and the European Union Cyber Resilience Act compels continuous validation of software supply chains, while AI-generated code introduces hidden vulnerabilities that slip past traditional scanners. Cloud platforms, which integrate directly with continuous-integration pipelines, account for most new deployments and are reinforced by DevSecOps mandates that push testing earlier in the lifecycle. Automated techniques dominate because machine-learning models now filter out false positives that once fatigued security analysts. Regionally, North America leads on account of strict breach-notification rules and automotive cybersecurity regulations, but Asia-Pacific is expanding the fastest owing to sovereign-cloud policies in China and India that require local penetration testing. Competitive intensity rises as hyperscalers embed native testing capabilities, established vendors acquire niche tool makers, and crowdsourced platforms mobilize global researcher communities.

Key Report Takeaways

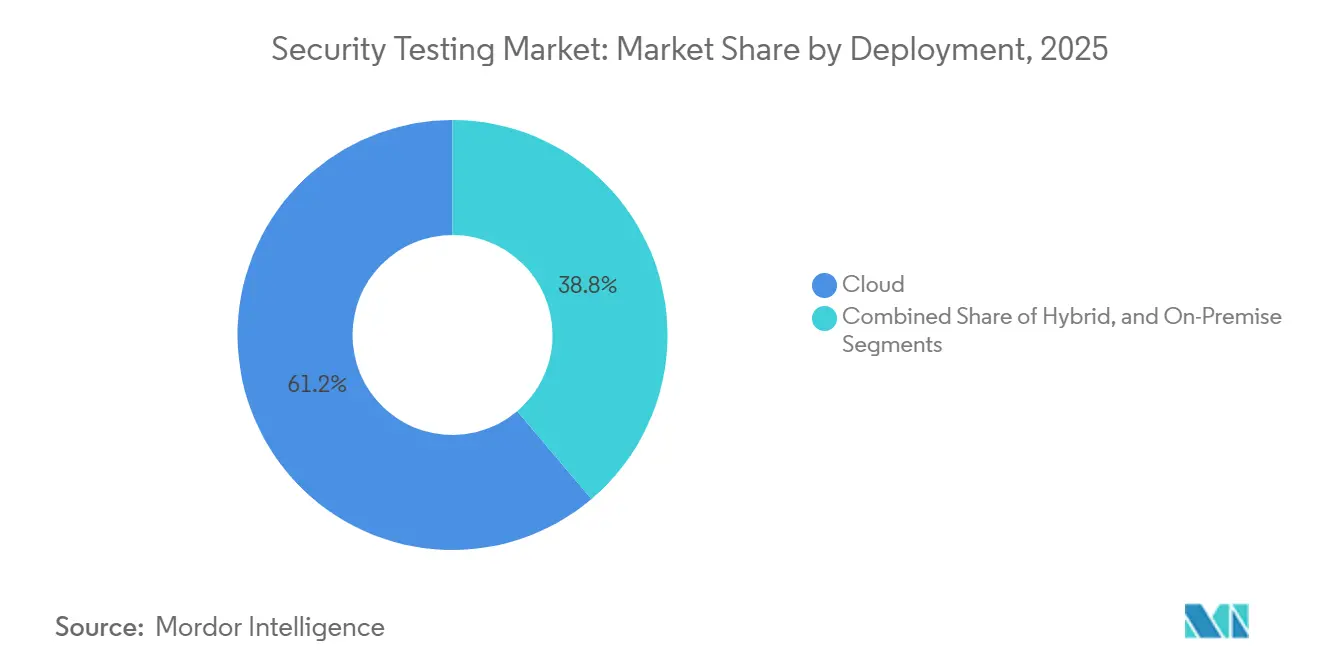

- By deployment, cloud platforms held 61.20% of security testing market share in 2025, while hybrid models are forecast to grow at 22.40% CAGR from 2026 to 2031.

- By type, network security testing led with a 37.44% share in 2025, whereas application security testing is set to expand at a 21.80% CAGR through 2031.

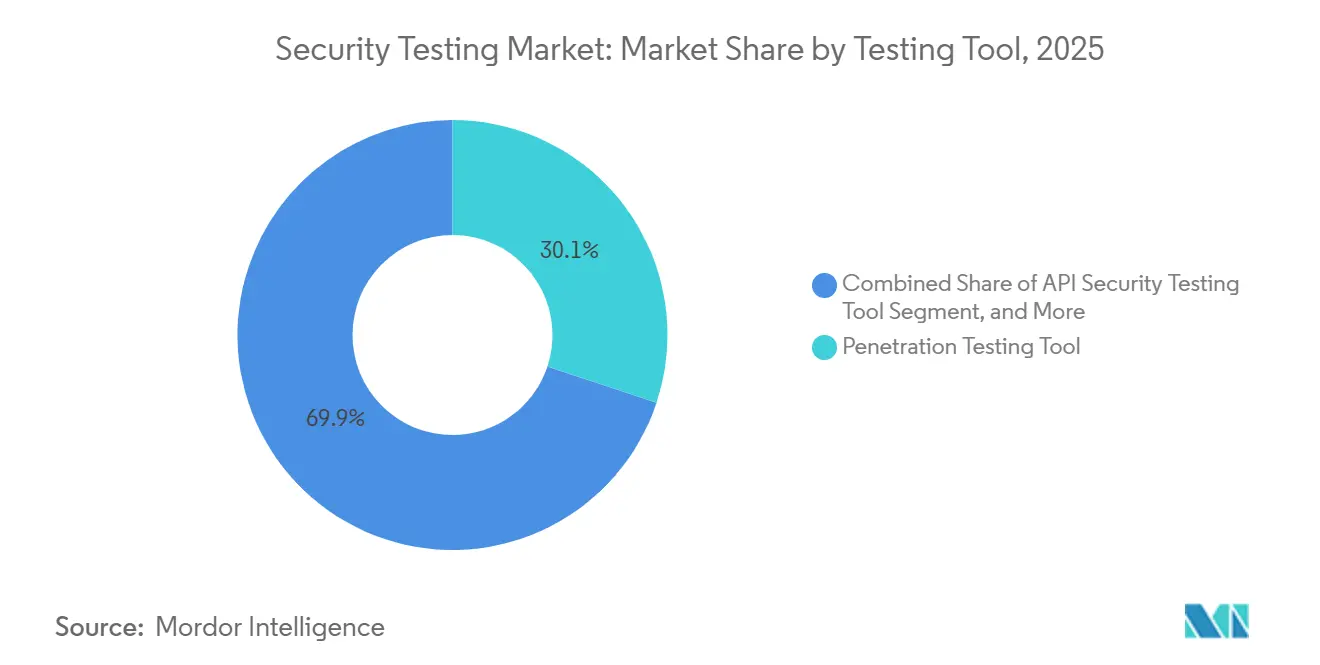

- By testing tool, penetration-testing frameworks commanded 30.11% share in 2025, but API security tools are projected to climb at a 24.30% CAGR to 2031.

- By organization size, large enterprises accounted for 56.87% share in 2025, yet small and medium enterprises are expected to advance at a 20.70% CAGR between 2026 and 2031.

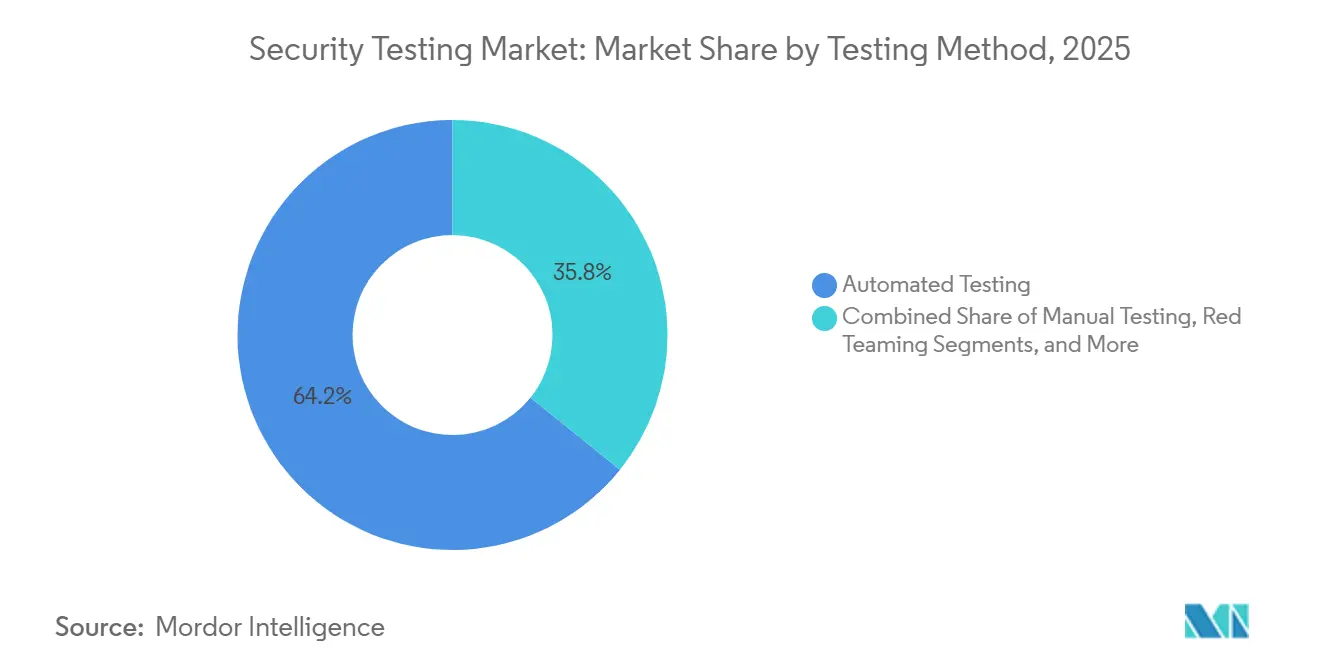

- By testing method, automated techniques accounted for a 64.22% share in 2025 and are anticipated to register the highest CAGR of 23.60% from 2026 to 2031.

- By end-user industry, banking, financial services, and insurance led with 26.54% revenue share in 2025, while healthcare is poised to grow at a 24.90% CAGR through 2031.

- By geography, North America dominated with a 35.40% share in 2025, whereas Asia-Pacific is forecast to register the highest regional CAGR at 22.30% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Security Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Sophistication of Cyber-Attacks | +5.2% | Global, with acute concentration in North America, Europe, and Asia-Pacific financial hubs | Short term (≤ 2 years) |

| Stringent Global Data-Protection Regulations | +4.8% | Europe (GDPR), North America (CCPA, state laws), Asia-Pacific (China PIPL, India DPDPA) | Medium term (2-4 years) |

| Rapid Cloud Migration and DevSecOps Adoption | +6.1% | Global, led by North America and Europe, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Remote and Hybrid Workforces | +3.4% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) |

| Mandatory SBOM Compliance (EO 14028, EU CRA) | +4.3% | North America (federal procurement), Europe (product certification), spillover to Asia-Pacific exporters | Long term (≥ 4 years) |

| Automotive UNECE R155 Security Mandates | +2.7% | Europe, Asia-Pacific (Japan, South Korea), North America (voluntary adoption) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication of Cyber-Attacks

Ransomware groups shifted to double-extortion tactics, encrypting data and threatening disclosure, which forces organizations to move from annual audits to continuous penetration testing. A 73% rise in attacks on critical infrastructure in 2024 highlighted zero-day exploitation before patches arrive. Supply-chain compromises that insert malicious code into upstream libraries elevate the need for software composition analysis. Financial institutions now demand third-party validation for every integration because a single compromised API can propagate across interconnected banking networks. Nation-state actors remain resident inside networks for months, prompting enterprises to run red-team exercises that mimic long-dwell adversaries.

Rapid Cloud Migration and DevSecOps Adoption

By late-2025, 68% of enterprise workloads ran on public or hybrid clouds, yet misconfigured storage buckets exposed more than 2 billion records, underscoring the mismatch between migration velocity and security maturity. DevSecOps embeds scanning within each code commit, trimming remediation costs by about 85% compared with post-production fixes. Native policy engines inside container platforms block deployments that fail security gates, making automated testing a prerequisite rather than an option. Serverless functions need specialized assessments because they spin up briefly and lack persistent hosts. Multi-cloud adoption complicates enforcement, so unified dashboards that normalize findings across providers gain traction.

Stringent Global Data-Protection Regulations

GDPR fines reached EUR 4.1 billion (USD 4.6 billion) across 2024-2025, with most penalties citing inadequate technical safeguards.[1]European Data Protection Board. "EDPB Homepage." Accessed January 13, 2026. California’s 2025 CCPA amendments introduced mandatory audits for firms processing over 100,000 consumer records, widening the compliance net.[2]State of California Department of Justice. "California Consumer Privacy Act (CCPA)." Accessed January 13, 2026. China’s Personal Information Protection Law orders annual third-party assessments, forcing multinationals to retain domestic testers. India’s Digital Personal Data Protection Act embeds security-by-design obligations that push testing earlier. ISO 27001 certification, now a prerequisite in more than 50 public-sector procurement programs, formalizes security testing as evidence of due diligence.

Mandatory SBOM Compliance

United States suppliers to federal agencies must deliver machine-readable SBOMs that automated scanners compare against the National Vulnerability Database. The EU Cyber Resilience Act extends similar rules to all products with digital elements, effectively globalizing component disclosure. Open-source code comprises up to 90% of modern applications, so continuous monitoring of dependency health is imperative. Build-time SBOM generators automate inventories, yet human verification still uncovers obfuscated or dynamically loaded libraries that automated tools miss. Vendors anticipate a compliance baseline whereby every software release ships with an accompanying SBOM and vulnerability-free attestation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Cybersecurity Professionals | -3.8% | Global, acute in developed markets | Medium term (2-4 years) |

| High Cost of Comprehensive Security Testing | -2.9% | Global, heavier on SMEs | Short term (≤ 2 years) |

| AI-Generated Code Creating Hidden Vulnerabilities | -1.6% | Global software-intensive sectors | Short term (≤ 2 years) |

| Alert Fatigue from False Positives | -1.4% | Global, where SOC maturity is low | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Cybersecurity Professionals

A worldwide deficit of 4 million practitioners in 2025 left demand for testing specialists outstripping supply by 3.5-to-1 in North America and Europe. Universities produce fewer than 50,000 graduates annually with relevant credentials, barely covering retirements. Rising salaries price smaller firms out of the labor market, steering them toward managed services. Certification pathways that require multi-year experience elongate lead times for new entrants. Companies deploy orchestration and automated response tools to compensate, yet those platforms themselves require skilled operators.

High Cost of Comprehensive Security Testing

Full-spectrum testing can consume 15-25% of an application development budget, discouraging smaller organizations from rigorous programs. Per-scan pricing scales linearly with codebase size, while one-off penetration engagements can cost up to USD 200,000 per application. Jurisdictions such as China restrict source-code transfer abroad, obliging on-premise deployments that carry higher total cost of ownership. Open-source tools reduce license fees but shift expenses to in-house labor. As a result, many firms limit testing frequency to annual cycles despite threats that evolve weekly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Platforms Dominate Amid Hybrid Adoption

Cloud deployment accounted for a 61.20% security testing market share in 2025. Elastic scalability and native integrations with CI/CD pipelines allow teams to trigger scans on every commit, cutting detection lags from weeks to minutes. The segment is expected to grow at a 22.40% CAGR through 2031, propelled by serverless and container workloads that depend on cloud-native tooling. On-premise installations remain vital in defense and critical-infrastructure settings where air-gapped networks prohibit internet connectivity. Hybrid strategies emerge as a compromise, running static analysis in the cloud while performing dynamic scans inside sovereign datacenters. Multi-cloud adoption intensifies complexity because each provider offers proprietary controls, so organizations prefer vendor-neutral dashboards that unify results. Regulatory schemes such as FedRAMP require the testing platform itself to hold certification, narrowing the vendor pool and concentrating demand with established players. Consequently, the security testing market size for cloud deployment is set to outpace on-premise spending, though hybrid architectures will persist where sovereignty or latency matters.

Hybrid adoption also benefits vendors that package portable scanners capable of operating online or offline. These tools fetch vulnerability signatures when internet access is available, then execute behind the firewall. Such flexibility appeals to financial institutions that run sensitive workloads on private clouds yet develop new services in public clouds. Over time, cloud platforms will embed more native testing features, further eroding demand for standalone on-premise appliances. However, industries with strict export-control or classified-data requirements will continue procuring self-hosted solutions, ensuring a residual but stable revenue stream for legacy models.

By Type: Application Testing Outpaces Traditional Network Validation

Network testing led with a 37.44% share in 2025, but the application segment is anticipated to rise at a 21.80% CAGR to 2031. Modern microservices and API-first designs expand attack surfaces beyond perimeter firewalls, so organizations shift funding toward code-centric assessments. Static and dynamic techniques converge in interactive platforms that observe runtime behavior and pinpoint vulnerable paths with fewer false positives. Mobile and web apps drive volume because consumer-facing services collect personal data and must demonstrate compliance with privacy mandates. The security testing market size attributed to application assessments is therefore climbing faster than for network tools.

Meanwhile, runtime application self-protection installs instrumentation inside production workloads to block exploits in real time. Adoption remains low outside high-value assets owing to performance overhead, yet interest is growing where downtime costs eclipses hardware expenses. Device testing for embedded firmware rose after regulators required pre-market validation of medical and automotive software. Social-engineering simulations also gain ground; cyber-insurance carriers now ask policyholders to prove employee resilience to phishing. Taken together, these trends signal a structural pivot toward application-level scrutiny that perimeter-centric strategies cannot deliver.

By Testing Tool: API Solutions Register the Fastest Growth

Penetration frameworks held 30.11% share in 2025, reflecting their long tenure as staple tools. However, API security tools are forecast to post a 24.30% CAGR through 2031 as enterprises expose hundreds of endpoints per application. Continuous discovery crawlers map live APIs, while fuzzers inject malformed traffic to uncover latent flaws that static schemas miss. The security testing market share for API-centric tools will therefore swell as digital transformation drives microservices adoption.

Web-application scanners evolve from scheduled sweeps to event-driven triggers that fire on every code merge. Code-review engines now incorporate machine-learning models trained on labeled vulnerability datasets, slicing false positives by double-digit percentages. Container and infrastructure-as-code scanners join the toolbox, seeking misconfigurations and leaked credentials before deployment. Vendors differentiate by bundling analytics dashboards that prioritize remediation based on exploitability and business impact, helping teams focus scarce labor on top-risk items. Consolidation accelerates as full-suite providers acquire niche API startups, giving buyers an integrated option that simplifies procurement.

By Organization Size: SMEs Rely on Managed Services for Coverage

Large enterprises controlled 56.87% of spending in 2025, yet small and medium enterprises show the highest growth at a 20.70% CAGR from 2026 to 2031. Subscription-based managed security testing delivers continuous coverage without capital outlay, aligning well with limited in-house expertise. Cyber-insurance renewals increasingly require evidence of vulnerability scans, further encouraging uptake. The security testing market size among SMEs is thus set to expand faster than budgets in the large-enterprise segment.

Nevertheless, Fortune-500 firms pivot from yearly assessments to continuous testing embedded inside development pipelines. They integrate automated gates that block code merges with critical flaws, transforming security from an operational add-on into a development-time constraint. SMEs face disproportionate breach consequences, single ransomware events can consume up to 30% of annual revenue, so proactive testing becomes a cost-avoidance strategy. Managed providers court this tier with turnkey dashboards that translate technical findings into business-risk language, reducing interpretation burden.

By Testing Method: Automation Becomes the Default While Human Insight Remains Critical

Automated techniques accounted for 64.22% share in 2025 and are projected to rise at a 23.60% CAGR. Machine-learning classifiers now rank findings by exploit likelihood and asset criticality, cutting manual triage volumes. Continuous integration systems embed security gates that deny merges when severity thresholds are exceeded, enforcing policy without human intervention. The security testing industry still values manual expertise for business-logic flaws and privilege-escalation chains that automated engines struggle to model.

Red-team engagements simulate advanced persistent threats over weeks or months, offering insights into detection and response readiness that tool-driven testing cannot provide. Continuous testing as a service, in which providers monitor code repositories and runtime telemetry, emerges as a hybrid that blends automation with expert oversight. As tools mature, the pendulum swings toward human-in-the-loop models where analysts validate machine output, ensuring both scale and contextual accuracy.

By End-User Industry: Healthcare Emerges as the Fastest Expanding Vertical

Banking, financial services and insurance captured 26.54% revenue share in 2025 thanks to stringent PCI DSS 4.0 rules that stipulate quarterly scans and annual penetration tests. Healthcare is forecast to record a 24.90% CAGR through 2031 as ransomware attacks on electronic health records compel hospitals to validate security controls before device deployment. The security testing market size linked to healthcare thus grows faster than any other vertical.

Manufacturing invests in operational-technology assessments because industrial control systems, once isolated, now connect to corporate networks for predictive maintenance. Automotive firms build dedicated cyber-labs to comply with UNECE R155, running embedded, wireless and backend cloud tests across the vehicle lifecycle. Retailers upgrade testing around e-commerce platforms after high-profile payment breaches. Energy utilities audit smart-grid components to avoid cascading outages. These sectoral nuances confirm that compliance mandates plus public breach fallout drive industry-specific adoption tracks.

Geography Analysis

North America held a 35.40% security testing market share in 2025, underpinned by enforced breach-notification laws and early DevSecOps uptake. Executive Order 14028 requires all federal suppliers to document testing and produce SBOMs, a stipulation that ripples into commercial procurement. Financial regulators in New York and California prescribe precise testing cadences, elevating baseline demand. Automotive producers voluntarily align with UNECE R155 to maintain export eligibility, further inflating testing volumes. Although the region benefits from a dense ecosystem of tool vendors and managed service providers, the talent shortfall constrains capacity expansion.

Asia-Pacific is projected to grow at a 22.30% CAGR from 2026 to 2031, the fastest among major regions. Sovereign-cloud initiatives in China and India stipulate localization of testing data, spawning domestic providers and driving multinational firms to adopt hybrid architectures. China’s cybersecurity regime requires annual assessments by accredited labs, while India’s 2024 data-protection law embeds security-by-design into development processes. Japan spearheads automotive cybersecurity testing for connected vehicles and shares expertise with South Korea. Southeast Asian nations launch capacity-building programs, but limited local expertise keeps managed-service penetration modest among small businesses.

Europe maintains momentum thanks to GDPR, which levied EUR 4.1 billion in fines for inadequate safeguards during 2024-2025. The Cyber Resilience Act widens mandatory testing to consumer electronics, forcing every vendor of digital products to validate security features before market launch. South America grows moderately as Brazil’s LGPD mirrors GDPR, yet economic volatility caps spending. The Middle East invests in national cybersecurity centers, and Saudi Arabia mandates testing for critical infrastructure as part of Vision 2030. Africa remains nascent, though South Africa and Nigeria introduce baseline requirements that gradually lift adoption. Collectively, these regional narratives confirm that regulation plus digital transformation shape the demand curve, while workforce availability modulates practical execution pace.

Regulatory Landscape

Regulation increasingly ties security testing to auditable evidence across both organizational controls and product security. In the European Union, the Cyber Resilience Act (Regulation (EU) 2024/2847) entered into force in December 2024 and introduces incident and actively exploited vulnerability reporting obligations starting September 11, 2026, with reporting routed to ENISA and relevant national CSIRTs via ENISA's Single Reporting Platform. These requirements raise the bar for continuous vulnerability management and verification testing for products with digital elements, even ahead of the CRA's broader compliance milestone for products placed on the EU market (December 11, 2027).

Standards and frameworks are also being updated in ways that reinforce structured testing and governance. NIST released Cybersecurity Framework 2.0 quick-start guidance (including SP 1308) in 2026, supporting tighter linkage between testing outcomes and enterprise risk management and workforce practices. ISO updated the ISMS standards family with ISO/IEC 27000:2026 (July 2026). Along with ongoing spillover from supply-chain disclosure requirements such as United States Executive Order 14028 and sector rules such as UNECE R155 for automotive cybersecurity, these anchors push buyers toward repeatable test evidence, documented remediation workflows, and vendor proof of secure development and vulnerability handling.

Value Chain Analysis

The security testing value chain runs from tool and content inputs (vulnerability intelligence, signatures, and rule packs; open-source libraries and dependency metadata used for SCA) to platform development covering SAST, DAST, IAST, RASP, penetration testing frameworks, API testing, and exposure validation. Delivery then occurs through direct enterprise sales, cloud marketplaces, and managed services. Implementation layers commonly include CI/CD and developer tooling integrations, policy and workflow configuration such as severity gating, ticketing, and risk scoring, plus advisory services for program design, red teaming, and compliance evidence packaging. Cloud-first distribution and CI/CD embedding increasingly elevate hyperscalers and platform ecosystems as channels, while regulated buyers still maintain self-hosted or hybrid deployments to meet sovereignty and data-transfer constraints.

Downstream, enterprises operationalize findings through remediation in code repositories and configuration management, followed by retesting to create auditable trails for regulators and insurers. Third-party risk management and supply-chain assurance remain key demand drivers, including vendor risk assessments, security audits, and continuous monitoring of network components by telecom operators and other critical infrastructure buyers. In media and entertainment, vendor onboarding often requires Trusted Partner Network (TPN) assessments that incorporate penetration testing for internet-facing systems, cloud workflows, and data centers. The chain is constrained by the cybersecurity talent gap, which increases reliance on automation and external experts, and by localization requirements in some jurisdictions that affect where scanning data and artifacts can be processed and stored.

Competitive Landscape

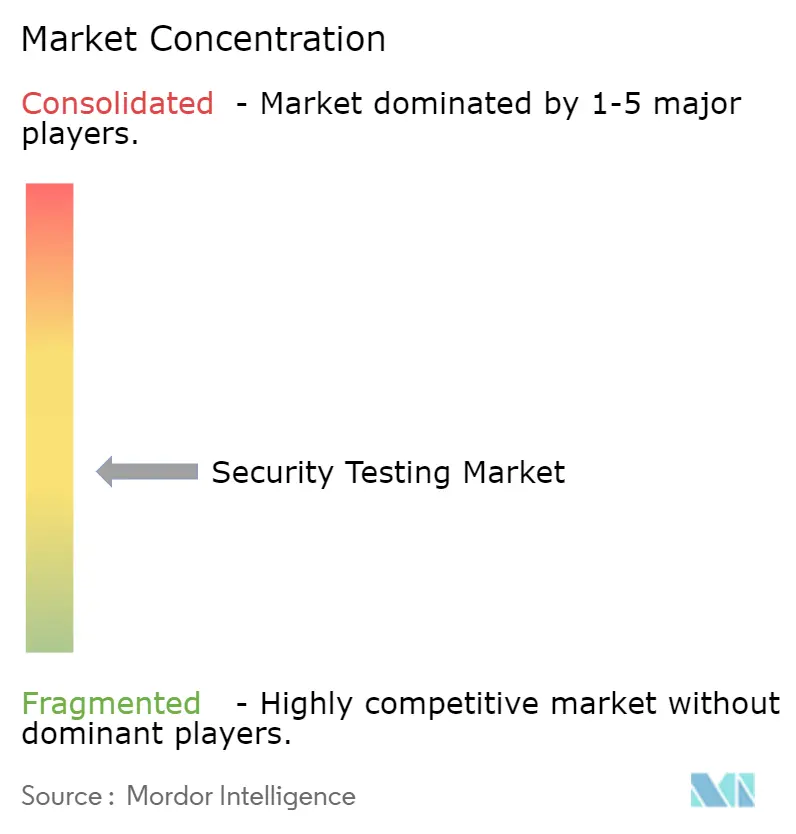

The security testing market exhibits moderate fragmentation as enterprise software giants, cloud providers and niche startups vie for wallet share. IBM, Synopsys and OpenText ship integrated suites that span static analysis to runtime protection. Hyperscalers embed native scanners into cloud build pipelines, capturing DevSecOps workflows at the source. Crowdsourced penetration platforms such as HackerOne mobilize global researcher networks, offsetting the 4 million-person talent shortfall. Managed service providers combine continuous testing with incident response, giving small and medium enterprises turnkey coverage.

Acquisition activity accelerates as full-suite vendors scoop up API and container-security specialists to close portfolio gaps. Cisco’s 2025 purchase of an OT-testing firm exemplifies moves into industrial segments. White-space persists in operational-technology environments with resource-constrained devices that cannot host runtime agents, and in automotive over-the-air update validation where UNECE R155 enforces narrow testing windows. Artificial-intelligence-powered prioritization engines emerge as differentiators, though adversaries simultaneously weaponize AI to craft polymorphic exploits.[3]United Nations Economic Commission for Europe. "UN Regulation No. 155 - Cyber Security and Cyber Security Management System." Accessed January 13, 2026. Open-source tools remain popular for cost reasons but require skilled operators, sustaining a premium tier for commercial platforms that bundle analytics and workflow automation.

The outlook suggests rising consolidation among mid-tier vendors, continued platformization by hyperscalers and sustained demand for specialist expertise in niche verticals such as industrial control systems and medical devices.

Security Testing Industry Leaders

-

Core Security Technologies Inc

-

Offensive Security LLC

-

Applause App Quality Inc

-

IBM Corporation

-

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clear whitespace is forming around operationalizing AI-assisted and agentic testing in day-to-day engineering workflows, particularly where skills shortages and alert fatigue constrain manual throughput. In April 2026, Anthropic launched Project Glasswing, with participants including Amazon Web Services, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorganChase, Linux Foundation, Microsoft, NVIDIA, and Palo Alto Networks, to apply AI vulnerability detection tools to critical software. The program reinforces vendor and buyer focus on continuous, automated validation rather than point-in-time assessments. This supports platforms that can translate AI findings into developer-ready fixes, integrate with CI/CD gates, and provide traceable evidence for governance needs.

Compliance and third-party assurance continue to shape where security testing spend concentrates and how it is procured. NIST published CSF 2.0 quick-start guidance (SP 1308) in March 2026 to connect cybersecurity activities with enterprise risk management and workforce practices, supporting demand for measurement, reporting, and repeatable test evidence. At the same time, DORA (effective January 2025) and NIS2-related vulnerability handling and regular testing duties in Europe drive regulated entities and suppliers toward structured testing programs. Sector assurance schemes also open commercial lanes: the Trusted Partner Network released its STAR Report in April 2026 based on assessment data, highlighting elevated alerts tied to credential-based attacks and un-remediated vulnerabilities, which increases the need for continuous testing, credential exposure checks, and vendor remediation validation across entertainment supply chains. Vendors that package data-residency controls, auditable reporting, and third-party-ready attestation alongside automated testing can win procurement tied to these governance and supply-chain requirements.

Recent Industry Developments

- July 2026: Picus Security launched the Picus Autonomous Exposure Validation Platform, combining breach and attack simulation, autonomous penetration testing, and exposure validation in one offering. The release reflects a shift toward continuous, automated validation that goes beyond vulnerability discovery and into verifying exploitability and control effectiveness.

- June 2026: Aikido Security acquired Root, an agentic platform focused on researching, patching, and testing open source dependencies and container images. The deal strengthens software supply chain testing capabilities by linking dependency intelligence with actionable remediation and retesting workflows.

- May 2026: Accenture Ventures announced an investment in XBOW, positioned as an autonomous cybersecurity testing platform, to integrate with Accenture's Cyber.AI solution. The development signals services-led scaling of autonomous testing into enterprise programs that already rely on managed delivery and standardized governance reporting.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the security testing market is defined as the revenue earned from services and tools used to find security weaknesses in applications, networks, devices, and related digital environments, and then document the results for remediation and compliance.

Scope exclusions: Hardware-only security products, general IT testing that is not security-focused, and pure incident response work done after a breach are excluded unless sold as part of a security testing engagement.

Segmentation Overview

-

By Deployment

- On-Premise

- Cloud

- Hybrid

-

By Type

-

Network Security Testing

- VPN Testing

- Firewall Testing

- Other Network Testing Types

-

By Application Security Testing

- Mobile Application Security Testing

- Web Application Security Testing

- Cloud Application Security Testing

- Enterprise Application Security Testing

- SAST

- DAST

- IAST

- RASP

- Device Security Testing

- Social Engineering Testing

-

Network Security Testing

-

By Testing Tool

- Web Application Testing Tool

- Code Review Tool

- Penetration Testing Tool

- Software Testing Tool

- API Security Testing Tool

- Other Testing Tools

-

By Organization Size

- Large Enterprises

- Small and Medium Enterprises

-

By Testing Method

- Automated Testing

- Manual Testing

- Continuous Testing as a Service

- Red Teaming

-

By End-User Industry

- Government

- BFSI

- Healthcare

- Manufacturing

- IT and Telecom

- Retail

- Automotive

- Energy and Utilities

- Other End-User Industries

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to build the demand context and to keep assumptions tied to real-world indicators. We referenced public sources such as cybersecurity breach and incident reporting digests, guidance and publications from bodies like NIST, security and privacy regulations and enforcement notes, and national statistics portals that help track digital adoption, cloud use, and enterprise IT activity.

We also reviewed annual reports and investor presentations of relevant service-led and software-led suppliers, along with reputable press coverage and association websites that publish market signals like certification trends and workforce demand. For numeric backstops, we selectively used paid subscriptions for company financial intelligence, patent databases, and news and financials, mainly to cross-check revenue mix, acquisition impacts, and product launch timing. The sources named here are illustrative only, and many other references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was used to pressure-test scope boundaries and pricing, and to confirm how buying behavior is shifting across cloud, hybrid, and on-premise environments. We spoke with a mix of suppliers, channel partners, and enterprise security and risk stakeholders across APAC, EMEA, and the Americas, then used follow-up checks to close gaps on tool adoption, delivery models, and renewal patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 21% | Managers: 45% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build, where enterprise IT and cybersecurity spend signals are reconstructed by region and then filtered using security testing penetration by workload type (application, network, device, and social engineering) and delivery model (cloud, hybrid, on-premise). Once that demand spine is in place, the totals are corroborated with selective bottom-up checks, such as sampled vendor revenue splits, channel feedback, and modeled average contract value times estimated active customer counts, and then the model adjusts outliers.

Inputs used in the model include testing-method mix shifts (automated, manual, continuous, red teaming), cloud migration pace, regulatory and audit intensity for major verticals, typical testing frequency aligned to release cycles, and pricing movement for tools and services. When data is sparse for smaller regions or niche tool types, gaps are handled through proxy ratios anchored to similar end-user profiles, and those proxies are validated through interviews before being included.

For forecasting, we primarily use scenario analysis supported by a small set of measurable drivers, such as breach frequency headlines, cloud workload growth, and compliance-driven assessment cycles, and these are tuned using expert consensus from primary discussions. Where a driver is volatile, a conservative and an aggressive case are run first, and the final path is selected after assumptions are rechecked with regional practitioners.

Data Validation & Update Cycle

Model outputs are checked against independent signals like supplier revenue direction, hiring and certification momentum, and the observed shift toward continuous testing in DevSecOps-aligned programs, then variance is investigated before sign-off. If a segment shows an unusual jump, the assumptions on penetration, pricing, or delivery mix are revisited, and selected experts are re-contacted to confirm whether the change is real or timing-related.

A second analyst review is completed to verify calculations, year alignment, and currency conversions, and to ensure inclusions and exclusions are applied consistently across regions and end-user industries. Reports are refreshed annually, with interim updates when major events materially change spending patterns, and a final freshness pass is performed close to delivery so clients receive the latest updated view.

Mordor Intelligence's Global Security Testing Market Market Size Compared With Other Published Estimates

Published market sizes for security testing can look far apart even when they use similar labels, because the boundaries of what counts as testing revenue are not consistent. Differences usually come from what is bundled in (for example, compliance audit work or managed services), how hybrid delivery is treated, and whether the time series is anchored to a clear base year.

Breach activity trends, cloud workload growth signals, and vendor revenue mix checks are the guardrails that keep Mordor Intelligence's estimate tied to the security testing activities defined in this study, instead of drifting into adjacent security operations or broader managed security bundles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 22.08 B (2026) | |

| Industry Research Group A | USD 14.67 B (2024) | Uses an earlier base year and a different time cut of demand drivers, and the included revenue boundary may treat parts of testing as embedded within broader security software and service lines, which can compress the standalone testing total. |

| Advisory Publisher B | USD 13.00 B (2024) | The scope appears to fold in items like compliance and audit testing and some managed security testing constructs, and without a clearly matched base-year alignment, the resulting figure is not directly comparable to a pure testing-revenue definition. |

The spread in the table mainly comes from year alignment and what each publisher counts as security testing versus adjacent security work sold under broader programs. By keeping the scope tied to defined testing types and validating the model through observable demand signals and interview-based checks, our estimate stays traceable to repeatable inputs that can be reviewed and updated consistently.

Key Questions Answered in the Report

How large is the security testing market in 2026 and how fast is it growing?

The security testing market size is USD 22.08 billion in 2026 and is projected to advance at a 23.40% CAGR through 2031.

Which deployment model commands the highest share?

Cloud platforms lead with 61.20% security testing market share in 2025 due to their seamless integration with DevSecOps workflows.

Which region is expanding the quickest?

Asia-Pacific is forecast to post a 22.30% CAGR from 2026 to 2031, driven by sovereign-cloud mandates and local compliance requirements.

What segment shows the fastest tool-level growth?

API security testing tools are expected to grow at a 24.30% CAGR, the highest among all testing-tool categories through 2031.

Why is healthcare demand accelerating?

Heightened ransomware attacks on electronic health records and new FDA device-security guidance are pushing hospitals to adopt pre-deployment testing, propelling a 24.90% CAGR in healthcare spending.

How does the skilled-labor shortage affect adoption?

A gap of 4 million cybersecurity professionals globally elevates reliance on managed services and automation to keep testing programs sustainable.

Page last updated on: