Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Security Assertion Markup Language Authentication Market is Segmented by Offerings (Solution, Services), Deployment Mode (Cloud, On-Premise, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Vertical (BFSI, Government and Defense, Healthcare and Life Sciences, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

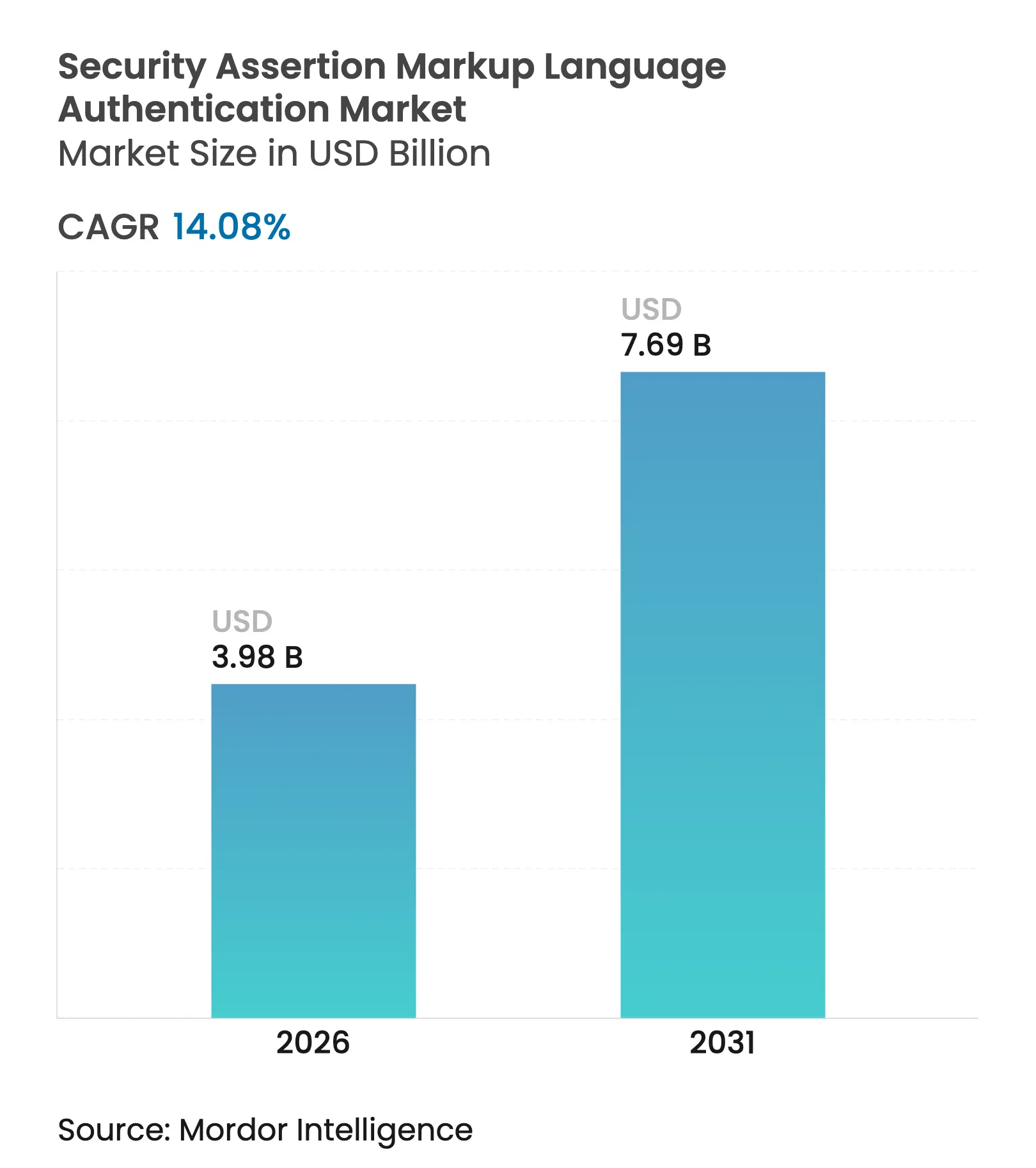

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 7.69 Billion |

| Growth Rate (2026 - 2031) | 14.08 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Security Assertion Markup Language authentication market size was valued at USD 3.49 billion in 2025 and estimated to grow from USD 3.98 billion in 2026 to reach USD 7.69 billion by 2031, at a CAGR of 14.08% during the forecast period (2026-2031). Rapid zero-trust adoption, tightening global regulations, and multi-cloud proliferation are reinforcing the protocol’s position as the de facto engine for cross-domain single sign-on. Cloud deployment now accounts for 68.25% of implementations, indicating a decisive shift toward SaaS-based identity services. North America led in 2024 with a 38% share after the Department of Homeland Security formalised SAML in its Zero Trust Implementation Strategy.[1]Department of Homeland Security, “Zero Trust Implementation Strategy,” dhs.govAsia is expanding fastest on the back of large-scale digital government projects and the roll-out of electronic identity wallets. Growth prospects are further strengthened by AI-enabled anomaly detection that delivers more than 90% accuracy against assertion forgery attacks, positioning SAML as an adaptive security control rather than a static authentication layer. At the same time, the emergence of OIDC and FIDO2 is reallocating vendor R&D spending and heightening competitive tension.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Zero-Trust adoption in regulated US industries propelling SAML federation Zero-Trust adoption in regulated US industries propelling SAML federation | +3.2% | North America, spillover to Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+3.2% | Geographic Relevance:North America, spillover to Europe | Impact Timeline:Medium term (2-4 years) |

Regulatory mandates (US ICAM 2.0, EU eIDAS 2) requiring standards-based SSO Regulatory mandates (US ICAM 2.0, EU eIDAS 2) requiring standards-based SSO | +2.8% | North America, Europe | Short term (≤ 2 years) | |||

Cloud migration surge in BFSI necessitating legacy-to-SaaS interoperability Cloud migration surge in BFSI necessitating legacy-to-SaaS interoperability | +2.5% | Global, emphasis on North America and Europe | Medium term (2-4 years) | |||

Embedded SAML connectors in leading SaaS suites accelerating down-stream adoption Embedded SAML connectors in leading SaaS suites accelerating down-stream adoption | +1.9% | Global | Short term (≤ 2 years) | |||

Cyber-insurance underwriting mandates for SAML/SSO compliance Cyber-insurance underwriting mandates for SAML/SSO compliance | +1.7% | North America, Europe | Medium term (2-4 years) | |||

Edge-OT device on-boarding in utilities via SAML-secured SCADA gateways Edge-OT device on-boarding in utilities via SAML-secured SCADA gateways | +1.1% | North America, Europe | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Zero-trust adoption in regulated US industries propelling SAML federation

Zero-trust has moved from concept to implementation, with 81% of enterprises reporting active roll-outs in 2025. The Department of Homeland Security positions SAML as a foundational element for continuous verification. Organisations now prioritise identity management budgets, driving demand for AI-backed assertion validation that operates in real time. Behaviour analytics fused with SAML reduces attack dwell time and mitigates lateral movement risks

Regulatory mandates (US ICAM 2.0, EU eIDAS 2) requiring standards-based SSO

Multi-jurisdictional businesses face a compliance imperative to adopt interoperable authentication. The EU Digital Identity Regulation obliges organisations to deliver digital wallets by 2026, effectively hard-coding SAML into procurement criteria. US federal agencies maintain SAML support for cross-domain needs even while piloting FIDO2, signalling a dual-stack future. Global corporations pre-empt region-specific mandates by standardising on SAML to simplify audits and lower remediation costs.

Cloud migration surge in BFSI necessitating legacy-to-SaaS interoperability

Financial institutions transferring core workloads to cloud platforms leverage SAML as a security bridge to legacy host systems. Harmonised identity planes shorten migration timelines and avoid wholesale directory changes. Sweden’s fintech reforms under PSD3 underscore the need for strong, cross-domain authentication that preserves existing risk controls while enabling open banking APIs. [2]Kommerskollegium, “The Swedish Market for Financial Technology,” kommerskollegium.se

Embedded SAML connectors in leading SaaS suites accelerating downstream adoption

Native connectors in Salesforce, Microsoft 365 and ServiceNow convert SAML enablement from custom coding to simple configuration. The transition by Salesforce to multiple-configuration SAML in Spring ’25 allows a single tenant to accept assertions from distinct identity providers, unlocking use cases such as partner access and M&A IT integration.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Emerging token standards (OIDC, FIDO2) diluting vendor R&D for SAML Emerging token standards (OIDC, FIDO2) diluting vendor R&D for SAML | -1.8% | Global, emphasis on North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global, emphasis on North America | Impact Timeline:Medium term (2-4 years) |

Mobile-latency concerns driving digital-native firms toward alternatives Mobile-latency concerns driving digital-native firms toward alternatives | -1.2% | Global | Short term (≤ 2 years) | |||

High integration cost for legacy ERP in APAC SMB segment High integration cost for legacy ERP in APAC SMB segment | -0.9% | Asia, emphasis on ASEAN and India | Medium term (2-4 years) | |||

Shortage of deep SAML assertion debugging talent increasing TCO Shortage of deep SAML assertion debugging talent increasing TCO | -0.7% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Emerging token standards (OIDC, FIDO2) diluting vendor R&D for SAML

Vendors are reallocating engineering budgets toward lighter protocols optimised for mobile and API traffic. SAP’s plan to phase out SAML for user-interactive log-ins within its Business Technology Platform exemplifies the pivot. Feature velocity for SAML enhancements is slowing just as enterprises request adaptive and continuous authentication, introducing a capability gap.

Mobile latency concerns driving digital-native firms toward alternatives

XML payload size, extra redirects and browser dependency hinder SAML in bandwidth-constrained scenarios. Digital-native businesses running mobile-only channels gravitate to JWT-based OIDC flows that improve page-load metrics and reduce session drop-off. This bifurcation forces dual-protocol estates, increasing operational complexity and skill requirements.

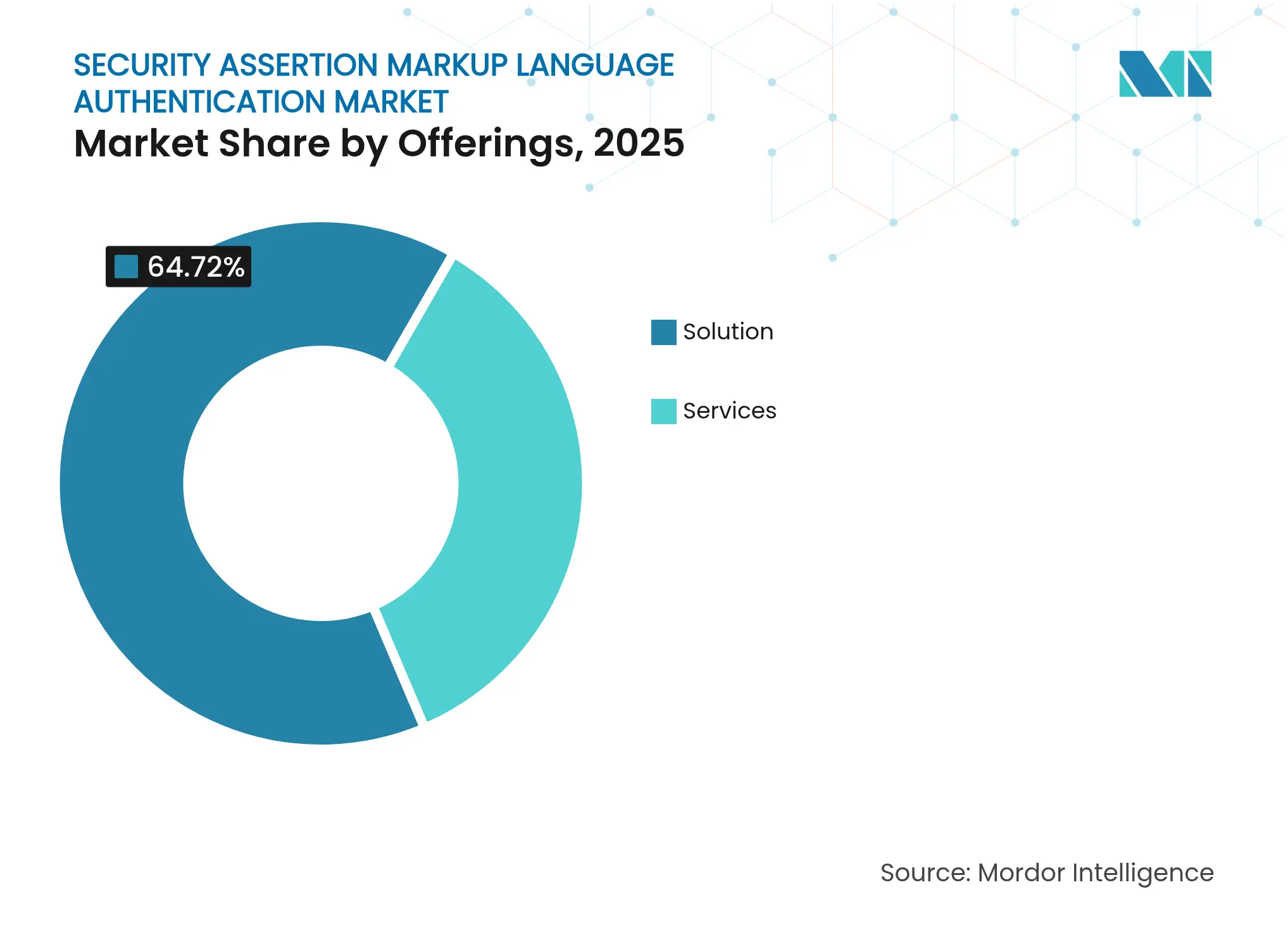

By Offerings: Services’ growth overtakes solutions

The solution segment generated 64.72% of 2025 revenues, anchored by federation servers and identity provider software that underpin enterprise SSO. Many deployments now layer Cloud Access Security Brokers to retrofit SAML onto SaaS apps lacking native support. Professional services are escalating due to scarce in-house skills, with managed offerings providing 24/7 oversight and rapid incident containment.

Services are forecast to expand at 15.78% CAGR, outpacing overall Security Assertion Markup Language authentication market growth. Advisory partners deliver threat-model reviews and optimisation sprints, while training programmes close knowledge gaps in assertion debugging. This demand uptick positions the services segment as a key driver of incremental revenue for platform vendors.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Hybrid bridges legacy and cloud

Cloud held a 67.60% share in 2025 as new adopters opted for SaaS identity providers that avoid capital expenditure. Multi-tenant architectures accelerate provisioning, and elastic scale aligns with variable sign-on peaks such as seasonal retail promotions.

Hybrid deployments are projected to grow at 14.94% CAGR. Financial institutions pursue phased migrations, using SAML to connect on-prem host systems to new cloud-native apps. This model preserves data sovereignty mandates and mitigates migration risk. On-premise estates remain relevant in jurisdictions where public cloud residency clauses restrict external hosting of identity data.

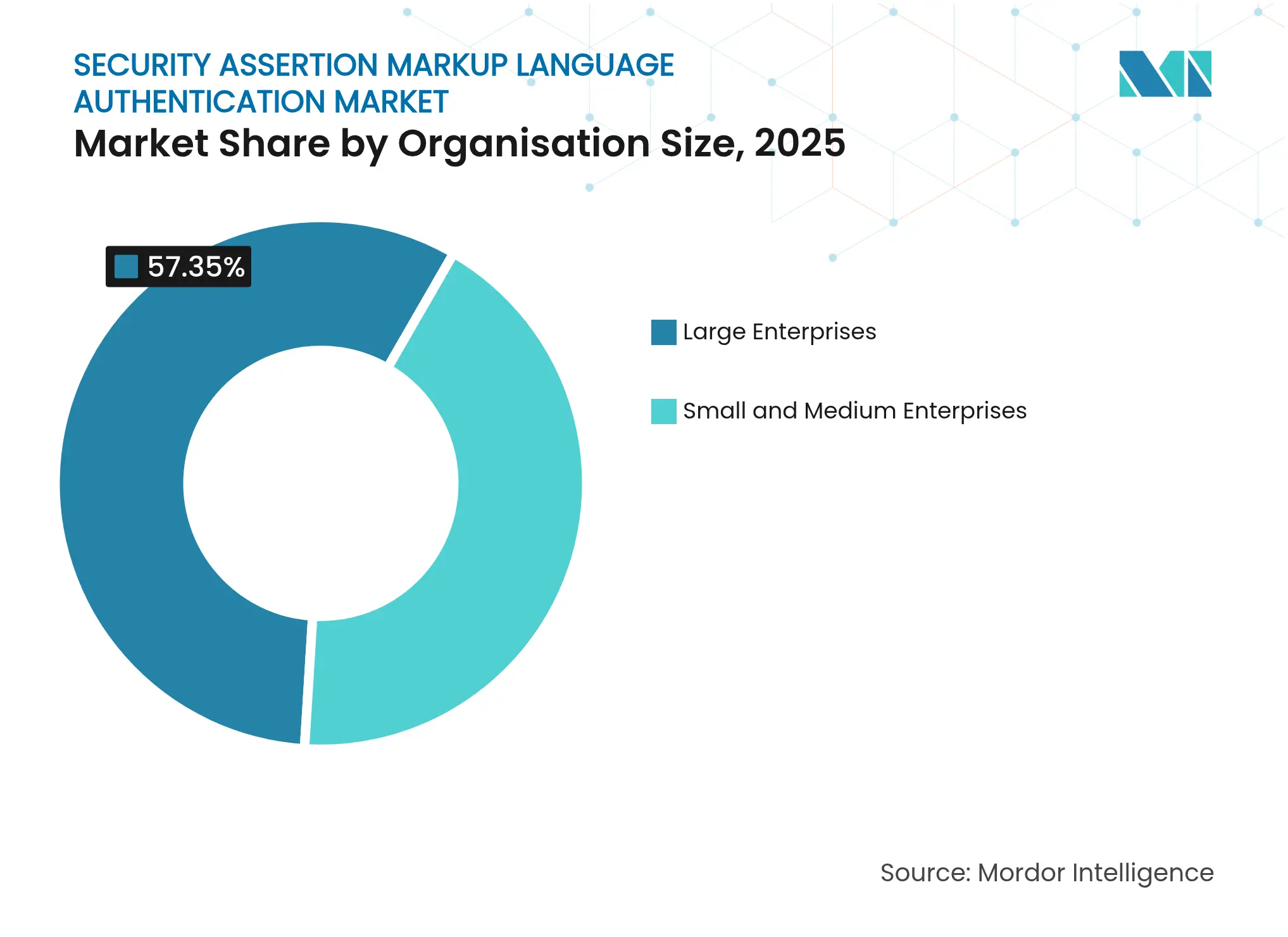

By Organisation Size: SME adoption accelerates

Large enterprises commanded 57.35% of the Security Assertion Markup Language authentication market share in 2025, capitalising on the productivity lift from eliminating password log-ins across vast application portfolios. They also face sophisticated attack vectors, making advanced assertion analytics crucial.

SMEs are predicted to expand at 15.85% CAGR. Turnkey SaaS bundles remove upfront complexity, and cyber-insurance carriers increasingly condition policy issuance on standards-based SSO. The “authentication-as-code” pattern embeds SAML policy in CI/CD pipelines, aligning with lean DevSecOps teams and shortening release cycles.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Healthcare surges ahead

BFSI accounted for 24.60% of 2025 revenue, relying on SAML to unify customer and employee access across retail banking, wealth management and trading platforms. CIAM integrations reduce onboarding abandonment and sustain security posture.

Healthcare & life sciences will grow at 16.72% CAGR as electronic records gain ubiquity. Practitioners need seamless cross-domain access, and patient privacy statutes mandate fine-grained control. AI-enhanced assertion inspection detects forgery attempts with over 90% accuracy, mitigating risks to sensitive data. Government & defence, IT & telecom and retail continue to invest, each driven by sector-specific compliance and user-experience demands.

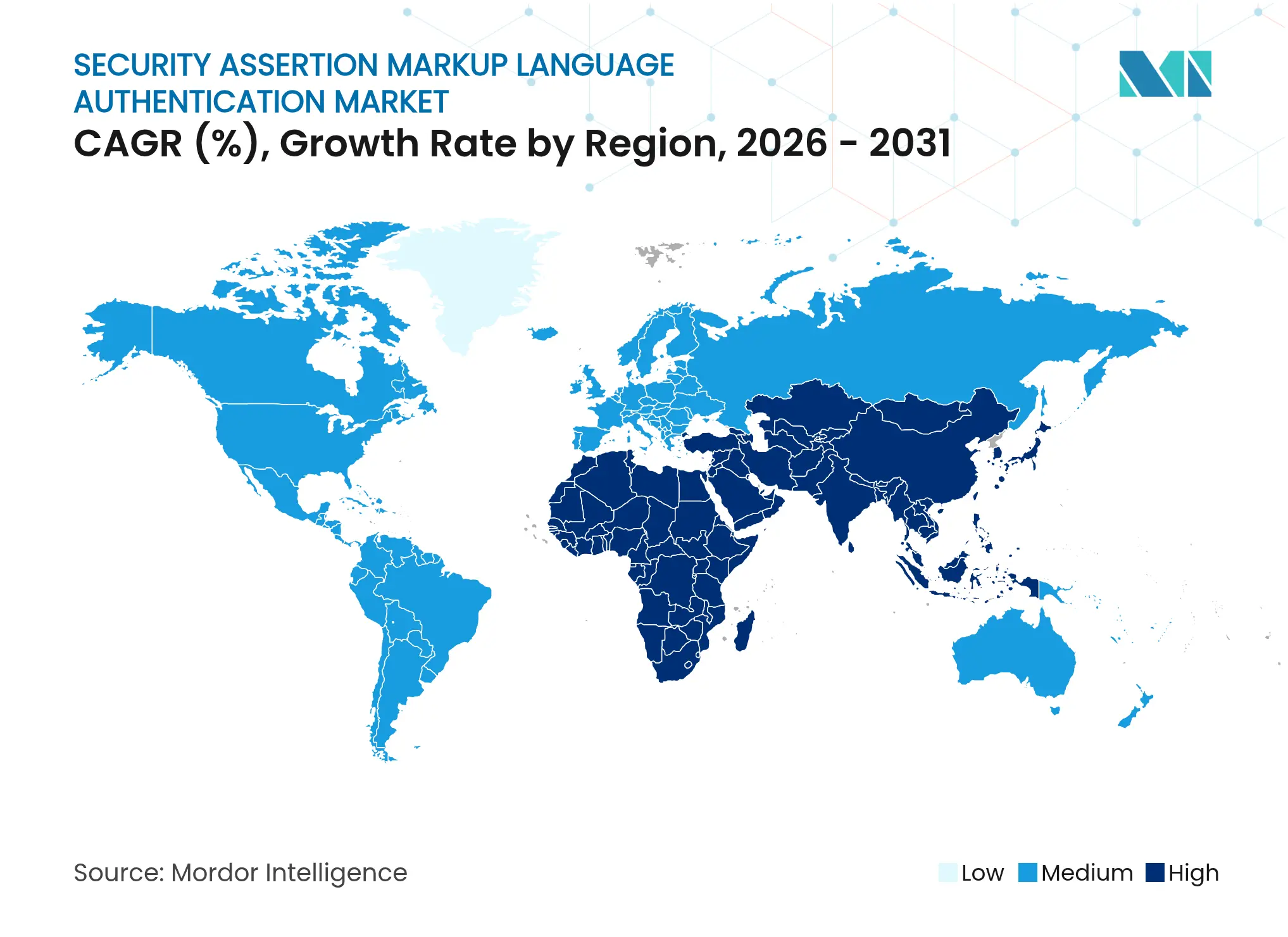

North America held 37.62% of the Security Assertion Markup Language authentication market revenue in 2025. United States directives on zero-trust and cloud modernisation place SAML at the centre of strategic roadmaps. Canada and Mexico follow, propelled by cross-border data-protection harmonisation.

Asia is projected to post a 15.65% CAGR, the fastest worldwide. Japan exhibits mature financial-sector uptake, China scales adoption through digital public-service portals, and India’s public-cloud boom drives hybrid SAML roll-outs. The APEC Committee stresses standards-based security for cross-border invoicing, reinforcing protocol relevance. Emerging ASEAN markets leverage donor-funded cybersecurity frameworks to accelerate adoption.

Europe maintains steady expansion under the EU Digital Identity Regulation. Germany, France, and the United Kingdom spearhead uptake, aligned to GDPR and forthcoming eIDAS 2 wallets. In the Middle East, GCC states launch digital-government mega programmes that rely on SAML gateways to secure citizen services. South Africa leads Africa, and Brazil anchors South America in BFSI-centric deployments.

Market Concentration

The market shows moderate concentration. Microsoft, Okta, and Ping Identity combine identity, access, and governance on converged platforms, while a long tail of specialists delivers vertical or regional depth. Ping Identity recorded 31% ARR growth in 2024, reaching USD 800 million as cloud subscriptions surpassed perpetual licences.

Competition now hinges on AI integration. Vendors embed machine-learning models to analyse session telemetry and flag anomalous assertions in real time. Partnerships with threat-intel feeds enrich risk scores that invoke step-up authentication. This pivot from static SSO to adaptive trust elevates switching costs and defends price premiums.

Platform consolidation is evident: IAM suites now bundle MFA, identity governance, and API security, positioning SAML as one module in a broader portfolio. New entrants differentiate with developer-centric SDKs, domain-specific compliance packs, and low-code orchestration. These disruptors often target underserved mid-market clusters where legacy tooling is cost-prohibitive.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The study of security assertion markup language (SAML) authentication market has considered varied offerings from the companies of both cloud as well as on-premise deployment for a wide range of industry verticals across the world. In SAML authentication a service provider (SP) redirects an access-requesting user/client to a trusted identity provider (IdP) in order for them to authenticate it. Once it is authenticated, the IdP provides SP a SAML assertion that they can use to provide the user access to their service.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.