Advanced Authentication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

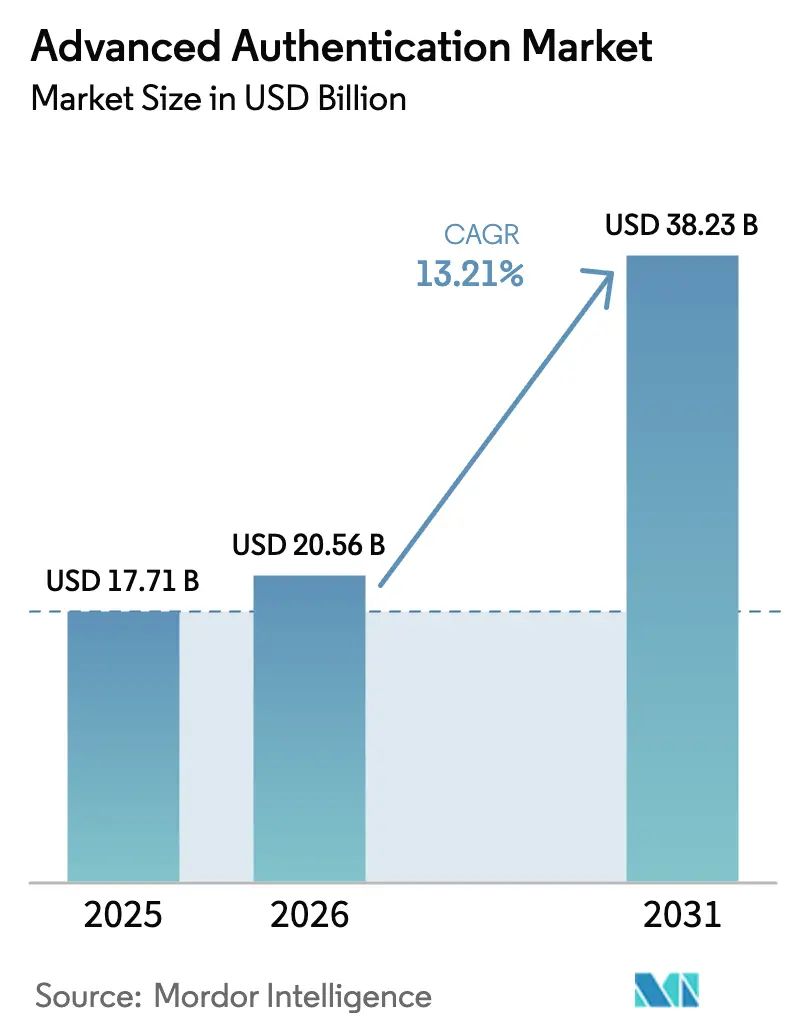

| Market Size (2026) | USD 20.56 Billion |

| Market Size (2031) | USD 38.23 Billion |

| Growth Rate (2026 - 2031) | 13.21% CAGR |

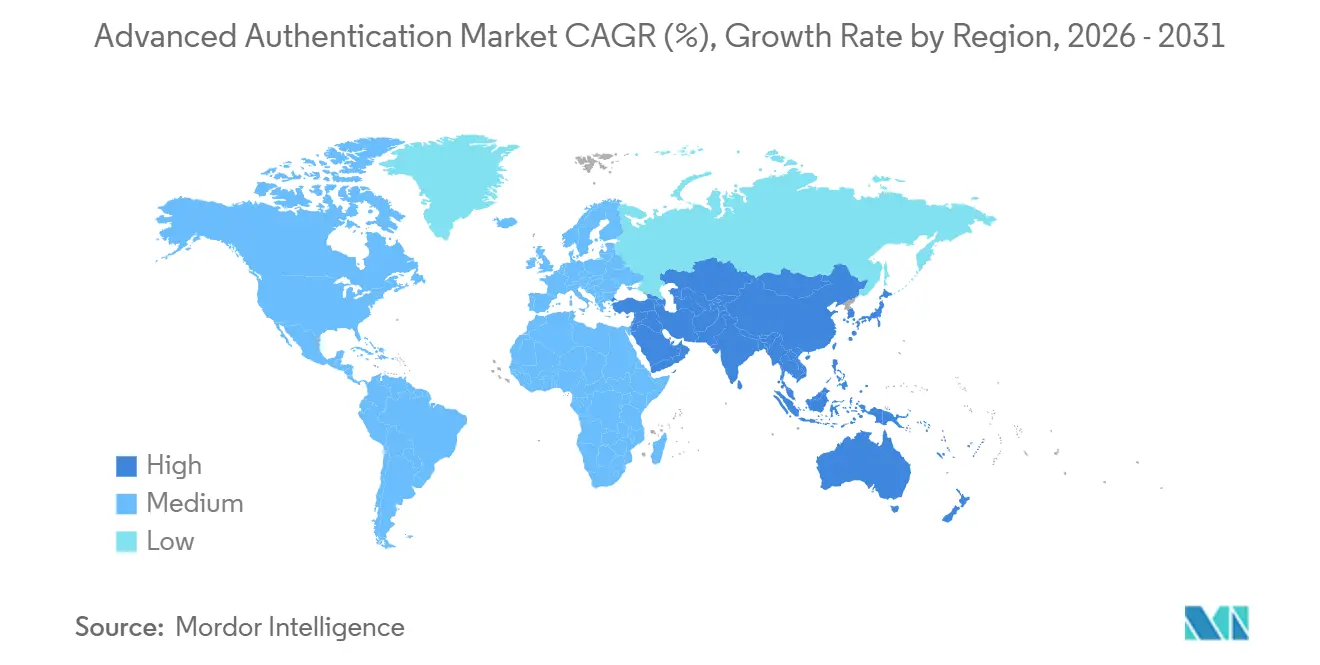

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Authentication Market Analysis by Mordor Intelligence

The Advanced Authentication Market size is expected to increase from USD 17.71 billion in 2025 to USD 20.56 billion in 2026 and reach USD 38.23 billion by 2031, growing at a CAGR of 13.21% over 2026-2031. Identity-centric security design, zero-trust mandates, and accelerated cloud migration continue to displace perimeter controls, reallocating cyber budgets toward authentication platforms that embed risk signals into every session. Cloud deployment led with 64.33% share in 2025 as identity-as-a-service vendors bundled passwordless, biometric, and risk-based verification into application programming interfaces that developers can invoke on demand. Biometrics accounted for 55.72% of authentication method revenue in 2025, yet behavioral analytics is expanding fastest at 14.47% because passive keystroke and navigation monitoring reduce user friction. Continuous and adaptive authentication is growing by 14.09% as financial regulations now require risk-responsive verification for high-value transactions. Competitive dynamics are shifting as hyperscalers such as Microsoft and Google bundle passkeys into broader cloud plans, compressing standalone vendor margins.

Key Report Takeaways

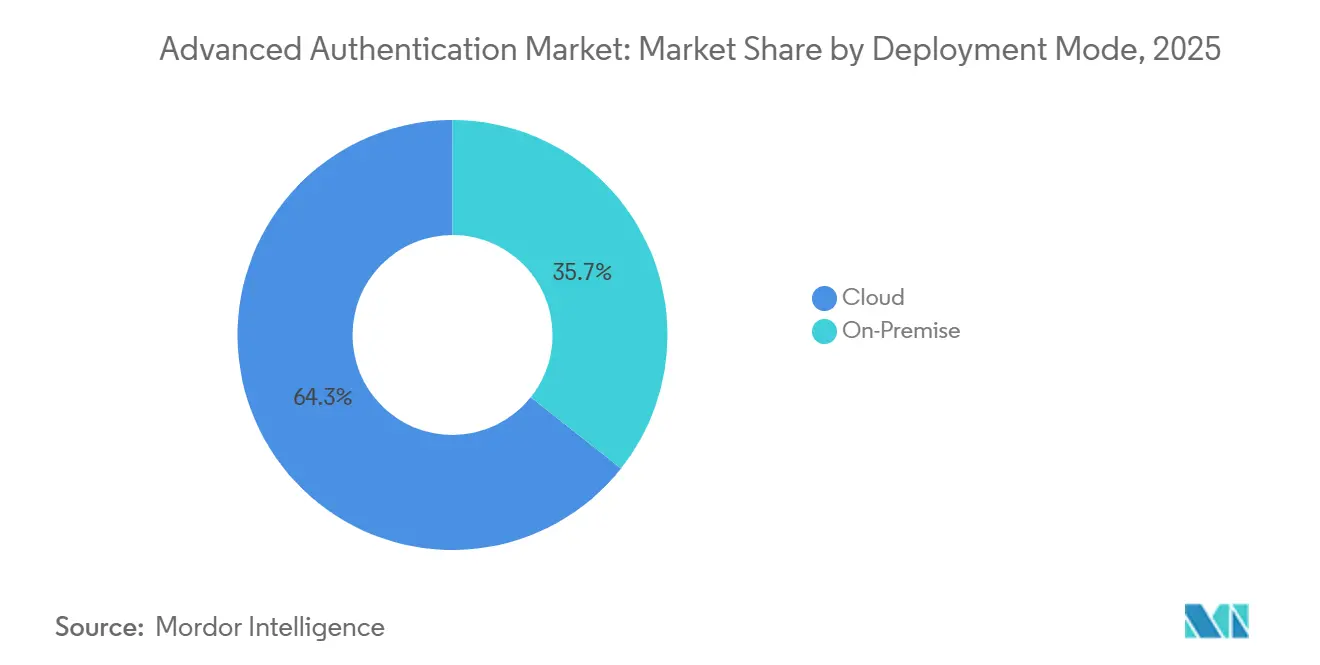

- By deployment mode, cloud accounted for 64.33% of the advanced authentication market share in 2025, while the segment itself is forecast to grow at a 13.87% CAGR through 2031.

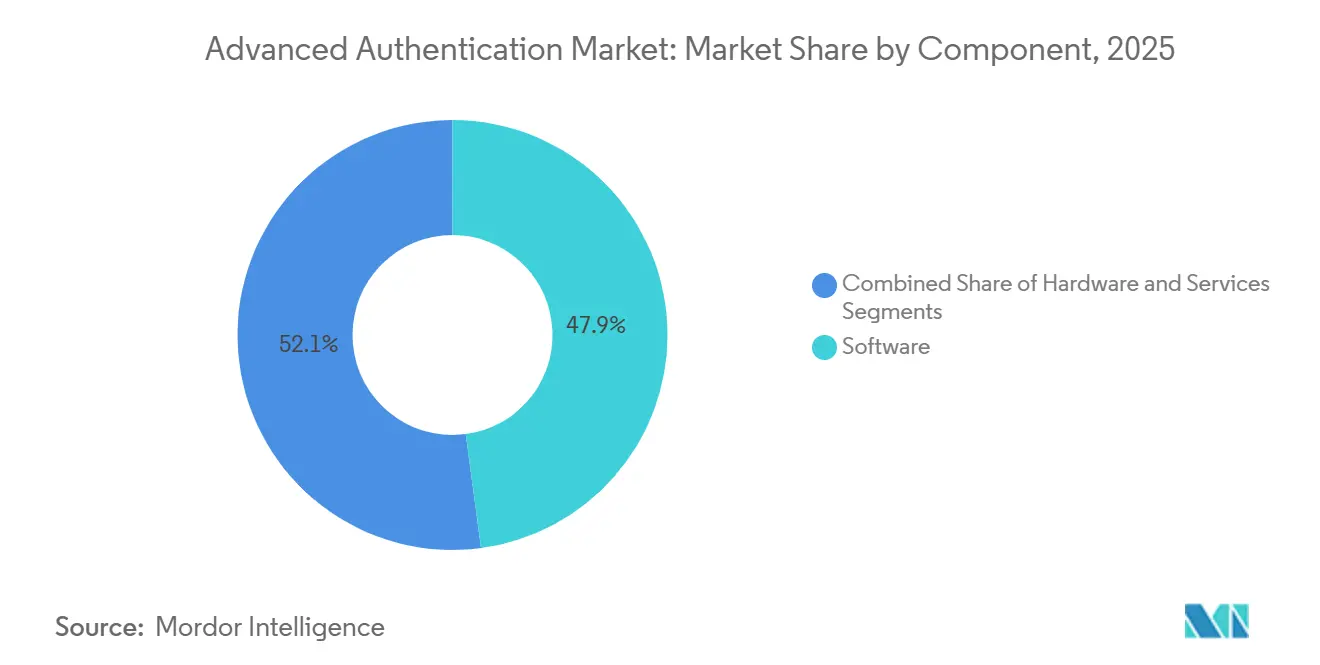

- By component, software accounted for 47.89% of revenue in 2025, and services are projected to register the highest 13.83% CAGR through 2031.

- By authentication method, biometrics led with 55.72% share in 2025; behavioral analytics is expected to expand at a 14.47% CAGR to 2031.

- By authentication model, multi-factor authentication commanded a 43.48% share in 2025, whereas continuous and adaptive authentication is advancing at a 14.09% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance accounted for 29.47% of revenue in 2025, while healthcare and life sciences are projected to post the fastest 15.07% CAGR through 2031.

- By geography, North America accounted for 38.91% of revenue in 2025, and Asia-Pacific is poised to record the highest 14.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Authentication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Cloud Adoption Driving Zero-Trust Architectures | +2.8% | Global, North America and Europe concentration | Medium term (2-4 years) |

| Rising Security Breach Costs and Cyber-Insurance Premiums | +2.3% | Global, pronounced in North America and BFSI hubs | Short term (≤ 2 years) |

| Accelerated Remote Workforce After 2025 | +1.9% | Global, notably North America, Europe, urban Asia-Pac | Medium term (2-4 years) |

| Mandatory Multi-Factor Authentication Compliance in Regulated Sectors | +2.6% | North America, Europe, Asia-Pacific financial and health | Short term (≤ 2 years) |

| Device-Embedded Hardware Roots of Trust in Consumer Electronics | +1.7% | Global, led by Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Quantum-Resistant Cryptography Investments by Governments | +1.2% | North America, Europe, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Cloud Adoption Driving Zero-Trust Architectures

Enterprises shifting workloads into public clouds discovered that traditional network perimeter defenses no longer apply, so identity verification became the primary control point. The U.S. Cybersecurity and Infrastructure Security Agency issued a zero-trust maturity model in 2024, positioning phishing-resistant credentials and continuous validation as foundational pillars.[1]Cybersecurity and Infrastructure Security Agency, “Zero Trust Maturity Model,” cisa.gov Cloud providers expose authentication through gateways that trigger step-up challenges whenever sensitive resources are requested, trimming lateral movement in breaches by 70% according to Microsoft’s 2025 Digital Defense Report. Multi-tenant software-as-a-service applications further amplify demand, as each tenant requires granular, policy-driven authentication without bespoke configuration. Integration between authentication platforms and cloud access security brokers is becoming mainstream, creating a unified view of user context across identity and network layers. As a result, purchase decisions increasingly favor vendors that can embed risk signals directly into cloud application workflows rather than rely on separate on-premise gateways.

Rising Security Breach Costs and Cyber-Insurance Premiums

The average data breach cost hit USD 4.88 million in 2024, with compromised credentials implicated in 16% of incidents.[2]IBM, “Cost of a Data Breach Report 2024,” ibm.com Cyber-insurance underwriters reacted by mandating multi-factor authentication on privileged and remote accounts before issuing or renewing policies, transforming authentication from an optional enhancement into a prerequisite for coverage. Enterprises now weigh authentication investments against potential premium surcharges and regulatory fines, the latter totaling EUR 1.6 billion (USD 1.7 billion) under the General Data Protection Regulation in 2024. The financial calculus is clear: failing to modernize authentication not only elevates breach risk but also drives direct cost increases. Consequently, mid-market organizations that once delayed upgrades due to budget limitations are accelerating adoption to maintain insurability and compliance.

Accelerated Remote Workforce After 2025

Hybrid work stabilized post-pandemic, with 42% of the U.S. labor force remaining fully or partly remote in 2025.[3]Bureau of Labor Statistics, “American Time Use Survey,” bls.gov Remote access strips away location-based trust, obliging authentication systems to verify device posture, network provenance, and behavioral consistency before granting entry. Identity-as-a-service platforms integrated endpoint telemetry so that logins from unmanaged devices or unfamiliar geolocations are denied or escalated. Employees also expect frictionless mobile authentication, approving requests on biometric-enabled smartphones rather than juggling hardware tokens, a preference especially strong in Asia-Pacific, where smartphone penetration tops 80% in major cities. These usability expectations amplify demand for adaptive, context-aware verification that balances security with productivity.

Mandatory Multi-Factor Authentication Compliance in Regulated Sectors

Regulations evolved from recommendations to directives. The European Union’s Digital Operational Resilience Act, effective January 2025, obliges financial entities to implement adaptive authentication that tightens verification as transaction risk rises. U.S. health regulators clarified in 2024 that multi-factor authentication is effectively mandatory under the Health Insurance Portability and Accountability Act for entities lacking equivalent safeguards. Japan’s privacy amendments demanded strong authentication for operators handling sensitive biometric data. Compressed timelines leave little room for in-house development, so organizations favor cloud platforms with pre-built regulatory templates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upgrade and Token Replacement Costs | -1.4% | Global, acute in cost-sensitive mid-market and emerging economies | Short term (≤ 2 years) |

| Interoperability Gaps Across Legacy Infrastructure | -1.1% | North America and Europe mature enterprises | Medium term (2-4 years) |

| User Friction Leading to Authentication Fatigue | -0.8% | Global, consumer-facing applications | Short term (≤ 2 years) |

| Shortage of Skilled IAM Professionals | -0.9% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upgrade and Token Replacement Costs

Replacing legacy one-time-password tokens with modern credentials can cost USD 50–100 per user when procurement, enrollment, and support are factored in. Migration often requires consulting engagements priced at around USD 200,000 for mid-sized deployments, putting pressure on budgets in cost-sensitive sectors. Survey data from the Identity Defined Security Alliance showed that 38% of enterprises cited cost as the main barrier to adoption, despite recognizing breach risks. Subscription cloud services offset some capital outlay, yet the initial transition still weighs on short-term budgets, particularly in emerging economies where IT spend is tightly constrained.

Interoperability Gaps Across Legacy Infrastructure

Many enterprises run a patchwork of cloud applications, on-premise enterprise resource planning suites, and decades-old mainframes. Modern protocols such as FIDO2, OpenID Connect, and Security Assertion Markup Language 2.0 demand application-level support that legacy systems often lack. Middleware gateways translate tokens but add latency and single points of failure, diluting expected reliability gains. Regulated industries face the sharpest pain; core banking platforms coded in COBOL cannot natively consume modern assertions, forcing the use of custom adapters that require scarce mainframe expertise. These technical hurdles routinely extend project timelines and inflate integration budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Momentum Outpaces Software and Hardware

Services revenue within the advanced authentication market is projected to expand at 13.83% annually through 2031, reflecting buyers’ preference for outsourced policy design, integration, and 24/7 monitoring that relieve internal teams of the complexity. Software still accounted for 47.89% of 2025 revenue because cloud identity suites embed authentication, governance, and analytics into a single console. Hardware, including smart-card readers and biometric scanners, remains essential for air-gapped defense and critical infrastructure, yet its growth lags as passwordless mobile credentials proliferate. Hospitals illustrate the pivot toward services: consultants map intricate clinical roles to least-privilege access rules, then run managed operations that guarantee audit-ready reporting. As enterprises mature, they see incremental value in continuous optimization rather than in the initial technology license, shifting wallet share to managed security service providers.

This tilt underscores how the advanced authentication market share for value-added services will keep widening. Cloud vendors encourage the shift by offering modular subscriptions that bundle support hours, compliance templates, and orchestration playbooks, blurring the line between product and service. Systems integrators also package authentication with broader zero-trust rollouts, further accelerating demand for services. Meanwhile, hardware refreshes stay cyclical and narrowly scoped, sustaining but not expanding their portion of total spend. The competitive edge, therefore, lies in domain expertise and outcome-based contracts rather than point features.

By Authentication Method: Behavioral Analytics Accelerates Past Biometrics

Biometrics accounted for 55.72% of 2025 revenue, yet growth is decelerating as regional privacy constraints and market saturation curb new deployments. Behavioral analytics adds momentum, recording the fastest 14.47% CAGR, as passive keystroke, mouse movement, and navigation analysis authenticate users continuously without interrupting workflow. Banks integrate behavioral risk scores into fraud engines, preventing account takeover in real time and improving customer retention. Fingerprint sensors remain ubiquitous on smartphones, but gloves, moisture, and ambient light reduce accuracy in industrial and healthcare settings, prompting interest in multimodal or behavioral options. Facial recognition divides markets, enjoying favorable regulation in parts of the Asia-Pacific while meeting resistance under Europe’s General Data Protection Regulation.

Behavioral analytics, therefore, captures a growing share of the advanced authentication market as enterprises seek frictionless security that minimizes helpdesk calls. Vendors differentiate through proprietary machine-learning models that quickly personalize baselines and adapt to subtle user shifts, enhancing both security and the user experience. As adoption climbs, pricing pressure on commodity biometric hardware intensifies, nudging suppliers to bundle analytics and orchestration services. The long-term trajectory suggests coexistence, with biometrics anchoring high-assurance use cases and behavior filling continuous verification gaps.

By Authentication Model: Continuous Verification Displaces Periodic Challenges

Multi-factor authentication still led with a 43.48% share in 2025, primarily because compliance frameworks treat it as the baseline safeguard. Continuous and adaptive authentication, however, is advancing at a 14.09% CAGR as organizations close the exposure window left by one-time or session-start challenges. Continuous models reassess identity whenever context or behavior shifts, stepping up verification only when risk rises, thereby protecting sensitive assets without imposing blanket friction. European financial firms embraced the approach to satisfy the Digital Operational Resilience Act's rules, which bind authentication strength to transaction risk, and U.S. tech companies use it to thwart lateral-movement attacks.

Because continuous engines ingest signals from devices, networks, and user behavior, they demand robust analytics and orchestration layers. Vendors compete on how granularly they can tune policies down to individual application actions or data fields without manual scripting. The advanced authentication market share for continuous models will therefore expand as passwordless passkeys replace static passwords and as regulators codify real-time risk evaluation. Organizations that deploy adaptive logic report measurable drops in account-takeover incidents and helpdesk load, reinforcing the economic case for migration.

By Deployment Mode: Cloud Consolidates Its Lead

Cloud deployment held a 64.33% share in 2025 and is expected to grow at 13.87% through 2031, mirroring enterprises’ broader migration to software-as-a-service. Identity-as-a-service platforms ship with thousands of pre-built connectors, reducing rollout timelines and minimizing the need for custom code. Consumption-based pricing aligns spend with active users, making advanced features accessible to mid-market firms. On-premise implementations remain for defense, critical infrastructure, and jurisdictions requiring local credential storage, yet many of these organizations pilot hybrid control planes that process policy in the cloud while keeping keys on site.

Hyperscalers reinforce cloud dominance by bundling passwordless passkeys, risk scoring, and compliance templates into baseline subscriptions, compressing marginal cost to near zero and pressuring standalone appliance vendors. The advanced authentication market for cloud services, therefore, grows faster than the overall category. Even conservative sectors adopt micro-segmented pilots, gradually expanding coverage as audit cycles validate controls. Meanwhile, appliance refresh budgets flatten, and pure-play on-prem solutions pivot toward managed or hybrid offerings to remain relevant.

By End-User Industry: Healthcare Surges While BFSI Retains Scale

Banking, financial services, and insurance accounted for 29.47% of 2025 revenue, driven by stringent know-your-customer mandates and the high cost of account takeover. Healthcare and life sciences, however, are poised to record the fastest CAGR of 15.07% to 2031. Hospitals integrate biometric single sign-on and proximity cards so clinicians can instantly retrieve patient data without sharing passwords, aligning with Health Insurance Portability and Accountability Act audit requirements. Government and defense agencies continue to rely on Common Access Card hardware credentials, sustaining token demand despite a wider market pivot toward mobile passkeys.

Retail and eCommerce firms deploy adaptive authentication to reduce payment fraud by leveraging behavioral analytics to distinguish legitimate shoppers from bots. Energy utilities face unique challenges in integrating authentication into industrial control systems, where legacy protocols complicate risk-based checks. Across industries, the advanced authentication market share shifts toward sectors balancing high compliance pressure with complex user workflows. Healthcare’s rise underscores how security spending accelerates when data sensitivity meets operational urgency, cementing its place as the growth pace-setter over the forecast horizon.

Geography Analysis

North America contributed 38.91% of 2025 revenue as early zero-trust initiatives rippled from federal agencies to commercial enterprises. The Office of Management and Budget memorandum M-22-09 required government entities to deploy phishing-resistant authentication, and state and local administrations soon mirrored federal procurement practices. Canada updated its privacy law in 2024, introducing punitive breach fines that boosted enterprise investment in multi-factor and passwordless solutions. Although Mexico’s fintech regulations accelerated adoption in banking, budget constraints slowed rollouts in other sectors despite rising breach activity.

Europe maintains a meaningful presence as the General Data Protection Regulation’s accountability principle obliges the implementation of demonstrable technical controls, and the Digital Operational Resilience Act explicitly prescribes adaptive authentication for financial services. Germany’s technical guidelines for critical infrastructure and the United Kingdom’s push toward passwordless verification further anchor demand. Russia enforces local-server requirements for credential storage, complicating multinationals' cloud adoption.

Asia-Pacific is projected to grow at 14.24% through 2031, the highest regional rate. China’s Cybersecurity Law amendments mandate multi-factor authentication for critical information infrastructure operators, while India’s Aadhaar program processes over 2 billion biometric verifications monthly, normalizing passwordless login across public and private sectors. Japan’s privacy amendments and South Korea’s financial guidelines intensify local compliance requirements, driving enterprises toward adaptive solutions. Australia’s Essential Eight framework upgraded multi-factor authentication from recommended to mandatory, influencing government and critical-infrastructure spending.

The Middle East and Africa show uneven adoption. The United Arab Emirates imposed authentication standards for government portals, while Saudi Arabia’s Essential Cybersecurity Controls require multi-factor authentication in critical sectors. South Africa enforces reasonable security measures under the Protection of Personal Information Act, yet implementation varies across industries. South America centers on Brazil, where open banking regulations mandate strong customer authentication, while other economies lag due to fiscal headwinds.

Regulatory Landscape

Advanced authentication is increasingly shaped by prescriptive, high-assurance identity rules and standards that push phishing-resistant factors, verified onboarding, and stronger biometric governance. In the United States, NIST finalized SP 800-63B-4 in May 2025, tightening requirements around authenticator strength and lifecycle controls for federal digital identity implementations and influencing regulated-sector procurement beyond government. In Europe, financial-sector authentication requirements are reinforced by the Digital Operational Resilience Act (effective January 2025), while eIDAS-related implementation work is steering providers toward interoperable wallet onboarding.

In April 2026, the European Commission adopted Implementing Regulation (EU) 2026/798 (7 April 2026), setting reference standards for remote onboarding to European Digital Identity Wallets at assurance level high. This raises demand for liveness detection, biometric binding, and secure identity proofing workflows embedded into authentication platforms. Biometric and AI-enabled authentication is also subject to tighter governance under the EU Artificial Intelligence Act (Regulation (EU) 2024/1689), with full application cited for August 2026, increasing compliance pressure on vendors offering facial recognition and AI-driven verification in Europe. In Germany, Federal Office for Information Security (BSI) technical guidance such as BSI TR-03135 continues to anchor implementation expectations for identity proofing and authentication in high-assurance use cases.

Value Chain Analysis

The value chain covers component suppliers (secure elements, sensors, and token hardware), protocol and standards ecosystems (FIDO Alliance specifications and metadata services), platform vendors (identity-as-a-service, MFA, and risk engines), and deployment partners (systems integrators and managed security service providers) that implement policy, connectors, and monitoring across hybrid estates. Upstream, hardware roots of trust and device-bound credentials support passkeys, biometrics, and mobile smart credentials, while cloud identity platforms package authentication APIs, orchestration, and analytics for application teams and line-of-business owners.

Standards bodies increasingly set the cadence for interoperability and downstream productization. In January 2026, the FIDO Alliance published FIDO Metadata Service v3.1.1 as a Proposed Standard, and in February 2026 published CTAP v2.3 as a Proposed Standard, tightening the integration loop between authenticators, servers, and relying parties. Downstream, identity programs are expanding beyond login to wallet and verifiable credential ecosystems, highlighted by the FIDO Alliance digital credentials initiative launched in December 2025 with initial deliverables planned for 2026. Adjacent supply-chain moves, such as SEALSQ and GlobalFoundries aligning in July 2026 on trusted supply, also point to the dependency of advanced authentication outcomes on assured semiconductor and secure-component provenance.

Competitive Landscape

The advanced authentication market is moderately concentrated: the top five vendors captured roughly 35% of global revenue in 2025. Microsoft, Google, and Okta dominate identity-as-a-service by leveraging existing cloud subscriptions to distribute passkeys at minimal incremental cost, compressing margins for standalone challengers. Thales and IDEMIA lead the hardware segments, benefiting from Common Criteria certification, which remains mandatory for defense and critical infrastructure procurement. Behavioral analytics specialists such as BioCatch and Transmit Security exploit gaps in fraud detection and orchestration by integrating continuous signals into legacy banking stacks.

Standards bodies level the playing field. FIDO Alliance certification commoditizes baseline protocol implementation, pushing vendors to compete on user experience, breadth of integrations, and value-added governance tools. Patent filings underscore strategic direction: Yubico added 12 patents in 2024 for tamper-resistant hardware tokens, while Microsoft focuses on continuous risk-scoring algorithms. Private-equity-led consolidation persists, with Thoma Bravo aggregating identity vendors to achieve scale synergies. Regional incumbents NEC and Fujitsu leverage domestic trust and data-residency compliance to defend share in Japan and South Korea, illustrating how local regulation shapes supplier preference.

Hyperscalers are integrating passwordless authentication into their cloud services. As this trend unfolds, the focus of differentiation is moving towards policy orchestration, specialization in specific verticals, and the use of risk analytics. Vendors that can streamline user experiences across hybrid environments, all while adhering to varied regulations, are poised to surpass competitors who depend only on traditional credential technologies. This shift highlights the growing importance of offering comprehensive solutions that address both security and usability challenges, ensuring seamless operations for businesses navigating complex regulatory landscapes.

Advanced Authentication Industry Leaders

Thales S.A.

NEC Corporation

Broadcom Inc.

Fujitsu Limited

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is the replacement of SMS one-time passwords with phishing-resistant, context-rich verification in regulated and high-fraud journeys. NIST SP 800-63B-4 (finalized May 2025) raises the bar for phishing-resistant authentication at AAL2, pushing buyers toward FIDO2/passkeys and device-bound authenticators instead of shared secrets and OTPs. At the same time, the EU trajectory toward digital identity wallets, including eIDAS 2.0 requirements for Member States to offer an EU Digital Identity Wallet by end-2026 and the Commission Implementing Regulation (EU) 2026/798 on high-assurance remote onboarding (April 2026), expands demand for wallet-ready authentication, remote identity proofing, and step-up verification that can be embedded into onboarding and transaction flows.

Another whitespace area sits at the intersection of authentication and AI-driven abuse, where multimodal biometrics, liveness checks, behavioral analytics, and network signals are being combined to address deepfakes and automated injection attacks. In April 2026, the FIDO Alliance formed an Agentic Authentication Technical Working Group to standardize secure AI agent interactions and delegation, which creates near-term buildout needs for non-human identity, delegated authorization, and policy orchestration alongside human authentication. Telecom-led network intelligence is also being productized through API exposure, enabling silent, network-based verification as an alternative to SMS OTP for consumer and enterprise applications and encouraging orchestration vendors to integrate telco signals with risk-based authentication and continuous/adaptive models in BFSI and healthcare workflows.

Recent Industry Developments

- June 2026: Thales announced that Availity migrated its healthcare identity infrastructure to the Thales OneWelcome Identity Platform, supported by Identity Fusion. The update strengthens enterprise identity controls for a major US healthcare ecosystem and increases demand for cloud-ready authentication and access governance that can handle complex, regulated user populations.

- April 2025: NEC introduced an Identity Cloud Service positioned for scalable identity verification. The release underscores continued productization of cloud-native identity proofing and authentication services as buyers prioritize faster deployment, pre-built connectors, and policy templates across regions.

- June 2024: Thales introduced Passwordless 360, positioning it as a complete enterprise passwordless capability. This added competitive pressure around passkeys and passwordless rollout tooling, encouraging broader lifecycle management and orchestration features rather than standalone authenticators.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the advanced authentication market is defined as spending on stronger user and device verification used to access apps, networks, and transactions, beyond a basic password. It includes solution and service revenue tied to technologies like biometrics, smart cards, and multi-factor and risk-based authentication.

Scope exclusions: We exclude general identity governance, broad cybersecurity bundles that do not break out authentication, and pure legacy password management without an advanced factor.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Authentication Method

- Smart Cards

- Biometrics

- Fingerprint Recognition

- Iris and Retina Recognition

- Facial Recognition

- Voice Recognition

- Mobile Smart Credentials

- Tokens

- User-based Public Key Infrastructure

- Behavioral Analytics

- By Authentication Model

- Two-Factor Authentication (2FA)

- Multi-Factor Authentication (MFA)

- Continuous and Adaptive Authentication

- Risk-Based Authentication

- By Deployment Mode

- On-Premise

- Cloud

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Government (Civil)

- Defense

- IT and Telecom

- Retail and eCommerce

- Energy and Utilities

- Transportation and Logistics

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public standards and policy direction because they shape what strong authentication means in real procurement. Sources such as NIST Digital Identity Guidelines, ISO and IEC authentication-related standards, and ENISA publications help us map method definitions and minimum assurance expectations.

To anchor the model in real adoption signals, we also refer to sources such as U.S. SEC filings and annual reports, official government cyber guidance, relevant central bank and financial regulator security circulars, and peer-reviewed security journals for trends like passwordless and behavioral analytics. In addition, patent databases and paid company financials and intelligence subscriptions are used to sanity check product exposure, service mix, and recent launches. These references are illustrative, and many other public and paid sources were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focuses on practitioners who buy, implement, or support authentication programs, including enterprise security owners, IAM teams, channel partners, and solution architects. Inputs from North America, Europe, Asia Pacific, the Middle East and Africa, and South America were used to confirm deployment mix, service attach rates, and realistic timing for passwordless rollouts. Findings were then used to close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 46% |

| Mid tier: 49% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 16% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing uses a top-down and bottom-up approach, starting from the enterprise security spend pool and then reconstructing the addressable slice using adoption and deployment indicators for advanced authentication. Where the story needed to be more concrete, totals were corroborated with selective bottom-up approximations built from sampled vendor revenue cues, channel feedback, and typical price per user or per transaction multiplied by plausible user counts.

Key inputs used in the model include the share of cloud versus on-premises deployments, the revenue split across hardware, software, and services, the method mix between biometrics, smart cards, and other mechanisms, and the pace of MFA and passwordless enablement in regulated industries. We also track program-level drivers such as remote workforce access patterns, mobile app sign-in growth, and tightening identity assurance guidance, which then influences renewal cycles and new project starts.

For forecasting, scenario analysis is applied to the core variables, and assumed ranges are checked with expert feedback so adoption curves do not shift unrealistically. When bottom-up signals were incomplete in smaller countries or niche use cases, gaps were handled using regional ratios and penetration proxies that were validated again during follow-up calls.

Data Validation & Update Cycle

Validation happens through several passes where model outputs are compared against independent signals such as method shares, cloud adoption share, and the observed direction of services growth. Any large variance triggers a deeper review of assumptions, followed by re-checking unit economics and the implied user or device counts before final sign-off.

Reports are refreshed every year, and interim updates are made when major policy shifts, security incidents, or pricing changes materially move demand. Right before delivery, a final sweep is completed so the figures reflect the latest public updates and any newly confirmed primary feedback.

Mordor Intelligence's Advanced Authentication Market Size Compared With Other Published Estimates

It is normal to see different market sizes for advanced authentication because publishers select different product boundaries, base years, and conversion assumptions, and those choices ripple through the final number. Differences also show up when some studies report only platform software, and others include hardware, integration, and managed services.

Some published estimates appear to narrow the definition to a smaller slice, such as a limited set of methods or only one delivery layer, which pulls the value down. Other estimates use a wider security scope and then count adjacent identity spending. For Mordor Intelligence, the total is built only from authentication-related hardware, software, and services that directly support verification events (and not broader identity governance or general security tools).

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.71 B (2025) | |

| Global Publisher A | USD 26.20 B (2024) | Uses a different base year and often captures a broader set of authentication method categories at a global rollup, which can also reflect different currency timing and pricing progression assumptions. |

| Industry Publisher B | USD 5.48 B (2025) | Likely reflects a narrower counted scope, such as focusing on a limited solution subset or excluding parts of hardware and services, which reduces the captured spend compared with a full component view. |

The spread is mainly explained by what gets counted as authentication spend, the base year chosen for the starting value, and how the method and service mix is treated. By keeping the calculation tied to observable mix splits and adoption signals, and then re-checking those with interview feedback, we arrive at a number that is easier to trace and repeat across regions and years.

Key Questions Answered in the Report

How big is the advanced authentication market in 2026?

The advanced authentication market size reached USD 20.56 billion in 2026, reflecting widespread adoption of identity-centric security.

Which segment is growing fastest within authentication methods?

Behavioral analytics leads growth with a 14.47% CAGR through 2031 because passive monitoring authenticates users without interrupting sessions.

Why is healthcare adoption accelerating?

Healthcare shows a 15.07% CAGR through 2031 as hospitals integrate biometric and single sign-on tools to comply with HIPAA while preserving clinician workflow.

What drives cloud deployment dominance?

Cloud holds 64.33% share in 2025 because identity-as-a-service platforms offer pre-built connectors, lower upkeep, and consumption-based pricing.

How do regulations influence Asia-Pacific growth?

China’s Cybersecurity Law and India’s Aadhaar ecosystem mandate multi-factor or biometric verification, pushing Asia-Pacific toward a 14.24% CAGR through 2031.

What is the key barrier to modernization?

High token replacement and integration costs, sometimes USD 50–100 per user, remain the primary restraint for budget-constrained organizations.

Page last updated on: