Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.75 Billion |

| Market Size (2031) | USD 46.39 Billion |

| Growth Rate (2026 - 2031) | 10.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Security Market Analysis by Mordor Intelligence

The security market size was valued at USD 26.13 billion in 2025 and estimated to grow from USD 28.75 billion in 2026 to reach USD 46.39 billion by 2031, at a CAGR of 10.04% during the forecast period (2026-2031). Heightened executive-level focus on Zero-Trust architecture, the fusion of physical and cyber defenses, and rapid adoption of AI-enabled analytics anchor the growth trajectory. Enterprises are redesigning protection strategies around identity, continuous verification, and real-time situational awareness, retiring siloed controls that once divided guards, cameras, and firewalls. Spending also follows the expanding threat surface created by 5G networks, critical infrastructure digitization, and climate-resilient perimeter projects. Meanwhile, semiconductor shortages and data-residency rules add cost pressures that favor vendors able to deliver flexible deployment models and credible compliance reporting. As a result, the security market now rewards platforms that converge hardware, software, and managed services into one consistent risk-management fabric.

Key Report Takeaways

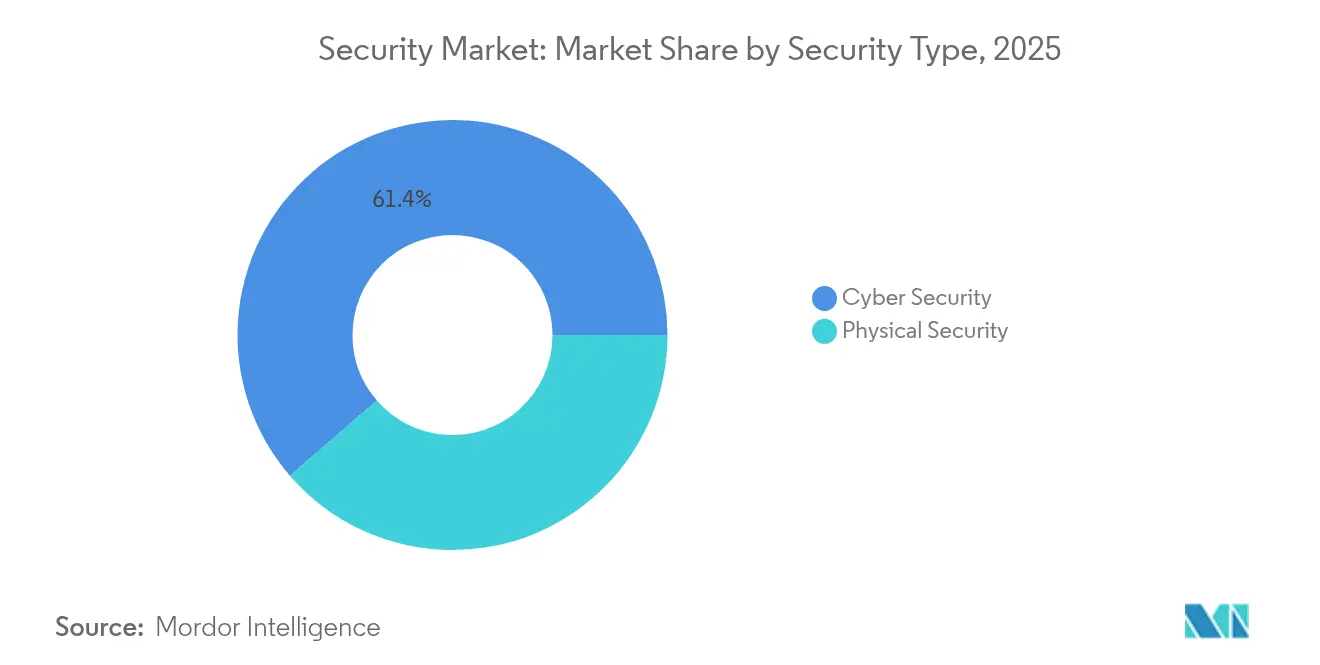

- By security type, Cyber Security held 61.35% of security market share in 2025, while Cloud Security is projected to expand at an 11.33% CAGR through 2031.

- By end-user vertical, Government & Public Sector commanded 24.58% revenue share of the security market in 2025; Healthcare is set to grow fastest at 10.26% CAGR to 2031.

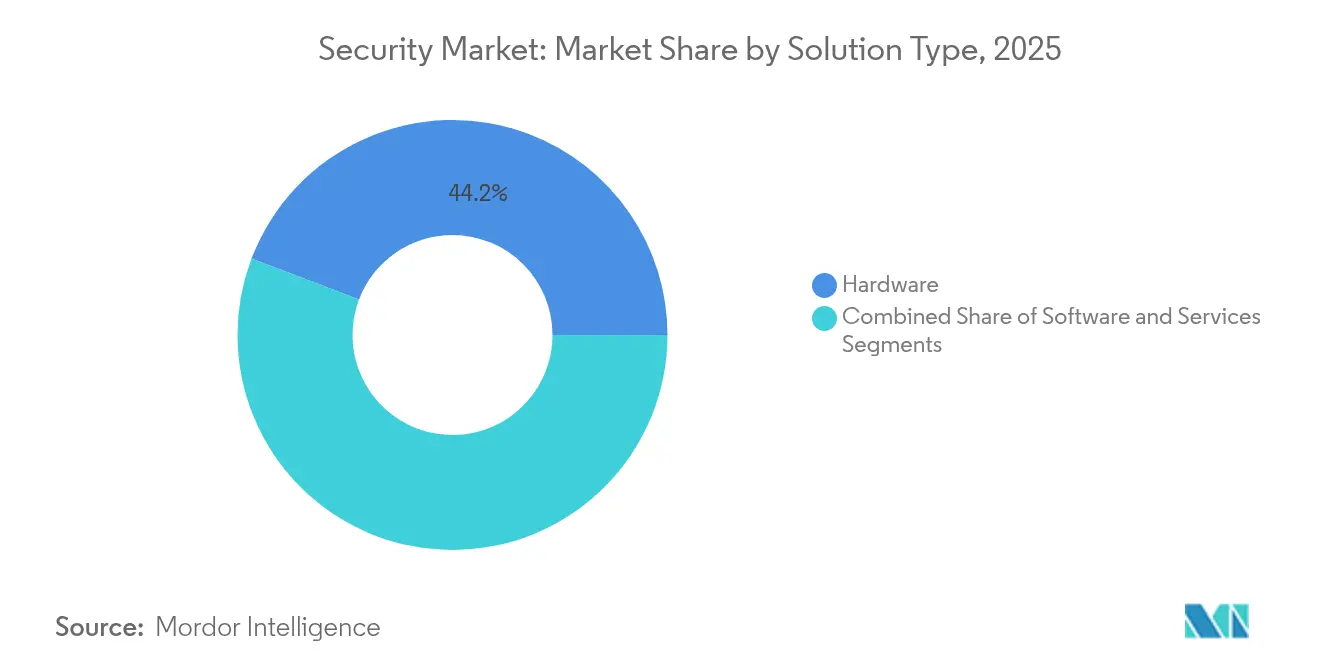

- By solution type, Hardware accounted for 44.22% share of the security market size in 2025, while Services are advancing at an 10.78% CAGR through 2031.

- By deployment type, On-premise models retained 70.12% share of the security market size in 2025; Cloud-based deployments show the highest growth at 11.02% CAGR through 2031.

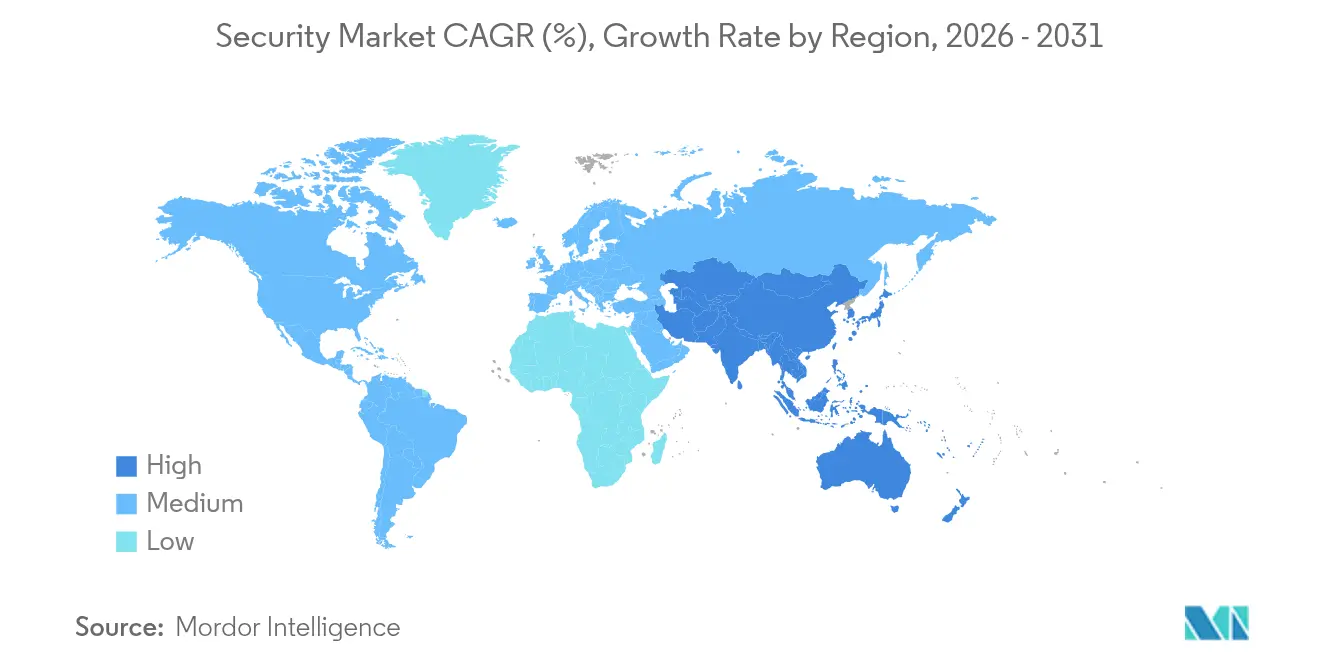

- By geography, North America led with 37.58% of security market share in 2025; Asia-Pacific is projected to record a 10.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convergence of physical and cyber-security platforms | +2.1% | North America and Europe | Medium term (2–4 years) |

| AI-enabled video analytics reducing false alarms | +1.8% | North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| National Zero-Trust mandates | +2.3% | North America, spillover to allies | Short term (≤ 2 years) |

| Rapid 5G roll-out exposing new attack surfaces | +1.4% | Asia-Pacific core, global implications | Medium term (2–4 years) |

| Climate-resilient perimeter projects | +0.9% | Coastal Europe and US East Coast | Long term (≥ 4 years) |

| Insurance requirements for verified intrusion detection | +1.2% | Developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Convergence of Physical and Cyber-Security Platforms in Critical Infrastructure

Unified security operations centers integrate badge-reader logs, video feeds, and network telemetry to spot cross-domain threat patterns, a capability highlighted by CISA’s 2022 guidance that converged programs detect incidents 34% faster than isolated teams.[1]CISA "U.S. Cybersecurity and Infrastructure Security Agency. "Executive Order on Improving the Nation's Cybersecurity,"cisa.gov Energy utilities now map physical access to NERC CIP-mandated network zones, producing audit trails that simplify regulatory reporting. Sandia National Laboratories projects that blended cyber-physical attacks will represent 40% of critical-infrastructure breaches by 2027, accelerating demand for platforms that correlate sensor data across both domains.

AI-Enabled Video Analytics Reducing False Alarms and Guard Costs

Edge cameras running deep-learning models filter out harmless motion, trimming false alarm rates by up to 70% and enabling clients to cut guard hours by 25–40% without sacrificing vigilance.[2]PhilArchive, "AI-Based Intelligent Video Surveillance System,"philarchive.org GardaWorld’s acquisition of Stealth Monitoring merged eight monitoring centers and 2,000 analysts into an AI-driven network that shifts spending from routine patrols to predictive analysis. Digital-twin overlays further enhance situational awareness by simulating risk scenarios before an incident materializes.

National Zero-Trust Mandates Accelerating Secure Access Investments

Executive Order 14028 compels U.S. federal agencies to adopt phishing-resistant authentication, encrypt DNS and HTTP traffic, and baseline endpoint health before FY 2024, a timetable captured in DHS’s implementation roadmap.[3]U.S. DHS, "Zero Trust Implementation Strategy,"dhs.gov Private contractors mirror these requirements to remain eligible for government contracts. CISA reports that 76% of agencies using shared Zero-Trust services improved mean time to detect by at least 20% in 2024.

Rapid 5G Roll-out Exposing New Attack Surfaces in Asia

Standalone 5G introduces service-based architectures that inherit 4G vulnerabilities while adding pathways such as GTP-U tunnels. SecurityGen documents packet reflection flaws that enable denial-of-service and session hijacking in private 5G deployments. Trend Micro notes that misconfigured slicing lets external actors pivot into IoT and OT networks, expanding the threat surface.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-residency laws complicating global SOCs | −1.6% | EU, global multinationals | Medium term (2–4 years) |

| Semiconductor supply constraints | −1.3% | Worldwide, acute in APAC | Short term (≤ 2 years) |

| High CapEx for multi-sensor perimeters | −0.8% | Africa & Latin America | Long term (≥ 4 years) |

| Talent shortage inflating service prices | −1.1% | APAC & North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data-Residency Laws Complicating Global SOC Deployments

The Schrems II ruling invalidated the EU–US Privacy Shield, forcing security operations centers to segregate personal data by region or adopt expensive supplemental measures such as client-side encryption and pseudonymization. Operators juggling GDPR, China’s PIPL, and emerging Indian statutes face fragmented logging and longer analytic cycles, undermining threat-intel sharing. AWS argues that localization does little to stop remote exploits, yet enterprises still incur extra infrastructure and legal costs.

Semiconductor Supply Constraints Delaying Edge Hardware Upgrades

Hurricane Helene suspended Spruce Pine’s ultra-pure quartz output for four weeks in 2024, disrupting the single most critical feedstock for lithography optics and delaying camera-sensor production by several quarters. Ongoing export restrictions on AI chips plus China’s curbs on gallium exports widen lead times for perimeter-device replacements, prompting integrators to prioritize software-defined conversions over hardware refreshes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Type: Cyber Dominance Meets Cloud Acceleration

Cyber Security contributed 61.35% to the security market in 2025, supported by intensified ransomware activity and state-sponsored espionage. Within this umbrella, network and endpoint controls remain foundational, yet Cloud Security is on course for an 11.33% CAGR, reflecting the pivot toward identity-centric architectures as workloads shift to SaaS and IaaS. The security market size for Cloud Security is projected to expand from USD 6.6 billion in 2025 to USD 12.55 billion by 2031. Physical Security persists in high-risk facilities, and the growing overlap between badge management and SIEM data feeds energizes hybrid solutions. AI-powered analytics that fuse camera output with network metadata now headline most vendor roadmaps, reinforcing convergence momentum.

Network hardening and micro-segmentation underpin Zero-Trust deployments across defense and aerospace, while application-security tooling scales in response to software-supply-chain attacks. Information-security suites combine data discovery, classification, and rights management for compliance reporting under GDPR and HIPAA. On the physical side, video-surveillance shipments integrate on-edge AI chips that filter scenes before streaming, cutting bandwidth by up to 60%. Perimeter-security roll-outs along new coastal protection structures illustrate how physical devices must now link directly with SOC dashboards for unified incident response.

By End-User Vertical: Government Leadership Amid Healthcare Surge

Government & Public Sector retained 24.58% of the security market in 2025 as agencies raced to hit Zero-Trust milestones stipulated by Executive Order 14028. The security market size for the segment reached USD 6.42 billion in 2025 and is forecast to exceed USD 11.28 billion by 2031. Healthcare, however, is advancing at a 10.26% CAGR, spurred by 725 major breaches reported in 2023 and an every-7-minute attack cadence. Hospitals now allocate up to 15% of IT budgets to cybersecurity—an increase that sustains double-digit demand for network detection and medical-device visibility platforms.

Commercial enterprises maintain sizable allocations for protecting distributed workforces and intellectual property. Critical infrastructure operators (utilities, airports, ports) co-fund integrated command centers that blend SCADA telemetry with physical access data. Education boards, spurred by student data leaks, elevate endpoint monitoring coverage, while residential buyers steadily adopt smart lock and doorbell camera packages bundled with cloud recording services.

By Solution Type: Hardware Foundation Supports Services Growth

Hardware captured 44.22% of security market share in 2025, reflecting the continued need for cameras, badge readers, firewalls, and dedicated appliances to anchor foundational controls. Services, though, are tracking an 10.78% CAGR as enterprises outsource Tier-1 monitoring, incident response, and compliance management. The security market size for Services is expected to rise from USD 9.07 billion in 2025 to USD 16.72 billion by 2031. Software advances center on orchestration and AI-based correlation engines that improve analyst productivity and close coverage gaps created by unfilled headcount.

Pandemic-era chip delays amplified interest in virtualized firewalls that run on commodity x86, stretching existing hardware while clients await refreshed silicon. Meanwhile, vendors package consulting, threat-hunting, and 24×7 SOC access into subscription bundles that align cost with risk exposure. The Services upswing gains further tailwind as cyber-insurance underwriters demand documented playbooks and third-party attestations.

By Deployment Type: On-Premise Stability Amid Cloud Transition

On-premise deployments represented 70.12% of security market size in 2025, reflecting entrenched data-sovereignty norms among defense, finance, and healthcare operators. Cloud-based alternatives, however, are accelerating at 11.02% CAGR thanks to scalable consumption, automatic patching, and API-level integration. Hybrid blueprints dominate mature enterprises: high-sensitivity workloads stay on-site, while less critical logs and analytical processes shift to SaaS.

Regulatory debates after Schrems II push multinationals toward regional data hubs, spurring providers to launch “sovereign cloud” zones certified for local compliance. Vendors responding with containerized security stacks allow clients to redeploy the same codebase across bare metal, private cloud, and hyperscale regions, smoothing migration without rewriting policy sets.

Geography Analysis

North America held 37.58% of security market share in 2025 on the back of USD 9.8 billion federal cybersecurity allocations and large-scale coastal resilience projects like the Charleston Peninsula wall that embed multi-sensor monitoring grids. U.S. agencies drive volume for identity-centric controls, while private contractors adopt the same frameworks to preserve procurement eligibility. Canada’s critical infrastructure plan earmarks expanded perimeter-intrusion systems for pipelines and ports, and Mexico’s nearshoring surge lifts demand for factory and warehouse surveillance.

Asia-Pacific is expected to register the fastest 10.56% CAGR through 2031, propelled by aggressive 5G roll-outs and dedicated private-network pilots across manufacturing and logistics hubs. China’s “Eastern Data, Western Compute” initiative triggers new SOC builds in interior provinces, while Japan’s XDR market reached JPY 3.7 billion (USD 25.2 million) in 2024 with Secureworks holding 48.6% share. India’s USD 130.27 million coastal resilience program integrates smart fence sensors and drone-detection radars to protect critical ecosystems. ASEAN countries prioritize smart-city command centers, and Australia advances mandatory critical-infrastructure cyber-resilience testing.

Competitive Landscape

The security market exhibits moderate fragmentation, yet consolidation is accelerating as vendors race to assemble end-to-end ecosystems. GardaWorld’s USD 60 million acquisition of OnSolve adds crisis-communication software to its Crisis24 intelligence network, packaging risk awareness, physical response, and digital monitoring into one subscription. Earlier, the firm absorbed Stealth Monitoring to embed AI analytics across eight command centers, positioning for outcome-based guard services. Allied Universal’s 24 acquisitions since 2022 and planned 2026 IPO underscore the scale premium now rewarded in high-volume guarding blended with tech enablement.

Technology players extend scope via targeted buys. Palo Alto Networks moved into model-security tooling by acquiring Protect AI, recognizing that AI workloads need bespoke defenses. Axon’s purchase of Dedrone injects drone-detection analytics into public-safety suites, preparing agencies for emerging aerial threats. White-space opportunities remain around climate-adaptive security, managed OT-security services, and compliance automation—segments where nimble specialists can carve niche positions before incumbents bundle similar features.

Supply-chain volatility elevates firms with diversified sourcing or inventory buffers. Semiconductor shortages limit smaller camera vendors’ ability to meet lead-time commitments, whereas large integrators pre-purchase wafers and reflow lines to maintain delivery continuity. Talent scarcity further tilts the field toward providers with global SOC footprints and automation investments that reduce analyst-to-device ratios.

Security Industry Leaders

-

Verkada Inc.

-

Honeywell International Inc.

-

Genetec Inc.

-

HID Global Corporation

-

Palo Alto Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GardaWorld completed acquisition of OnSolve, merging critical-event management with Crisis24 to deliver AI-driven risk-management services across 132,000 professionals.

- January 2025: Executive Order 14144 tightened Zero-Trust mandates, adding phishing-resistant authentication and third-party risk controls for federal agencies.

- December 2024: Allied Universal acquired Unified Command, deepening event-safety analytics ahead of its 2026 IPO.

- November 2024: GardaWorld finalized the Stealth Monitoring deal, integrating eight monitoring centers into its ECAMSECURE platform for proactive threat prevention.

Global Security Market Report Scope

The global security market encompasses a wide range of solutions designed to protect physical and digital assets. It includes physical security systems like access control, video surveillance, and intrusion detection, as well as cybersecurity measures such as network protection, endpoint security, and cloud security. The market serves various sectors, including government, commercial, industrial, residential, and critical infrastructure. Key technologies driving the market include AI, IoT, and biometrics,

The study tracks the revenue generated from the sale of security products and services by various manufacturers and service providers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The security market is segmented by security type (physical security[access control, video surveillance, intrusion detection, and perimeter security], cyber security [network security, endpoint security, application security, cloud security, and information security]), end-user vertical (government and public sector, commercial, industrial, residential, healthcare, education, and critical infrastructure), solution type (hardware, software, and services), deployment type (on-premise and cloud-based), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Physical Security | Access Control |

| Video Surveillance | |

| Intrusion Detection | |

| Perimeter Security | |

| Cyber Security | Network Security |

| Endpoint Security | |

| Application Security | |

| Cloud Security | |

| Information Security |

| Government and Public Sector |

| Commercial |

| Industrial |

| Residential |

| Healthcare |

| Education |

| Critical Infrastructure |

| Hardware |

| Software |

| Services |

| On-premise |

| Cloud-based |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Security Type | Physical Security | Access Control | |

| Video Surveillance | |||

| Intrusion Detection | |||

| Perimeter Security | |||

| Cyber Security | Network Security | ||

| Endpoint Security | |||

| Application Security | |||

| Cloud Security | |||

| Information Security | |||

| By End-user Vertical | Government and Public Sector | ||

| Commercial | |||

| Industrial | |||

| Residential | |||

| Healthcare | |||

| Education | |||

| Critical Infrastructure | |||

| By Solution Type | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Type | On-premise | ||

| Cloud-based | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the security market?

The security market generated USD 28.75 billion in 2026 and is projected to reach USD 46.39 billion by 2031.

Which segment is growing fastest within the security market?

Cloud Security is expanding at an 11.33% CAGR as organizations migrate to identity-centric architectures.

Why does North America lead the security market?

Federal Zero-Trust mandates, sizable cybersecurity budgets, and climate-resilient infrastructure projects underpin North America’s 37.58% share.

How are semiconductor shortages affecting security deployments?

Supply constraints delay camera and sensor upgrades, prompting buyers to favor software-defined solutions until new hardware becomes available.

Page last updated on: