Risk-based Authentication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

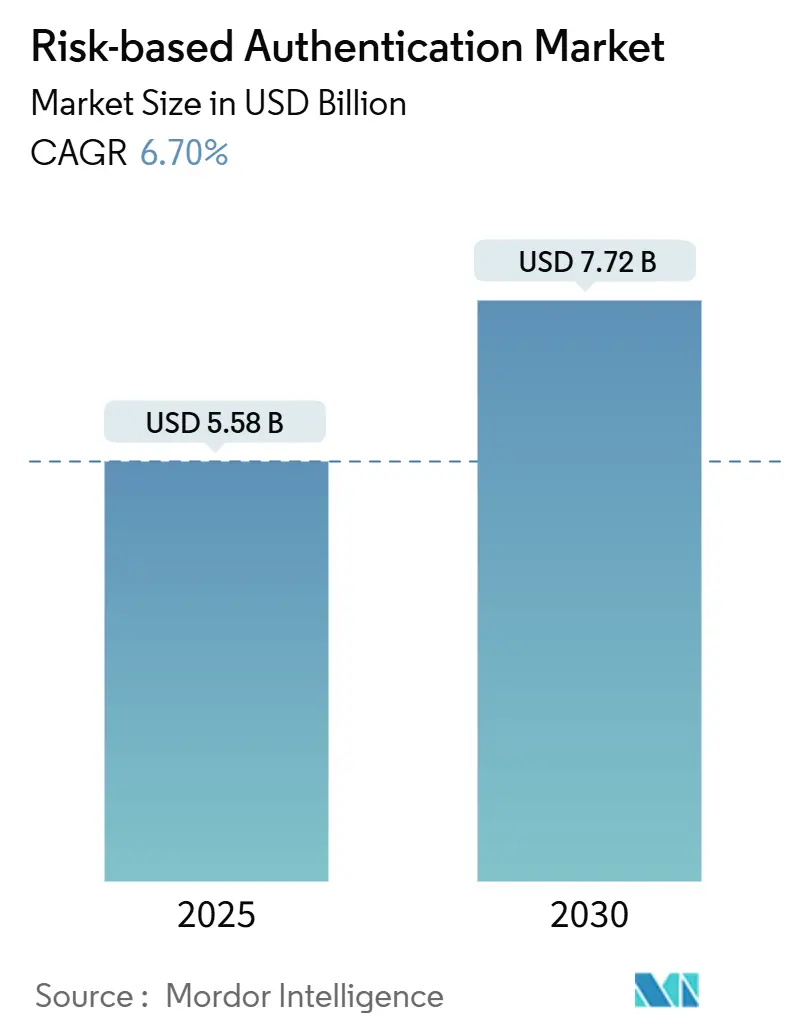

| Market Size (2025) | USD 5.58 Billion |

| Market Size (2030) | USD 7.72 Billion |

| Growth Rate (2025 - 2030) | 6.70% CAGR |

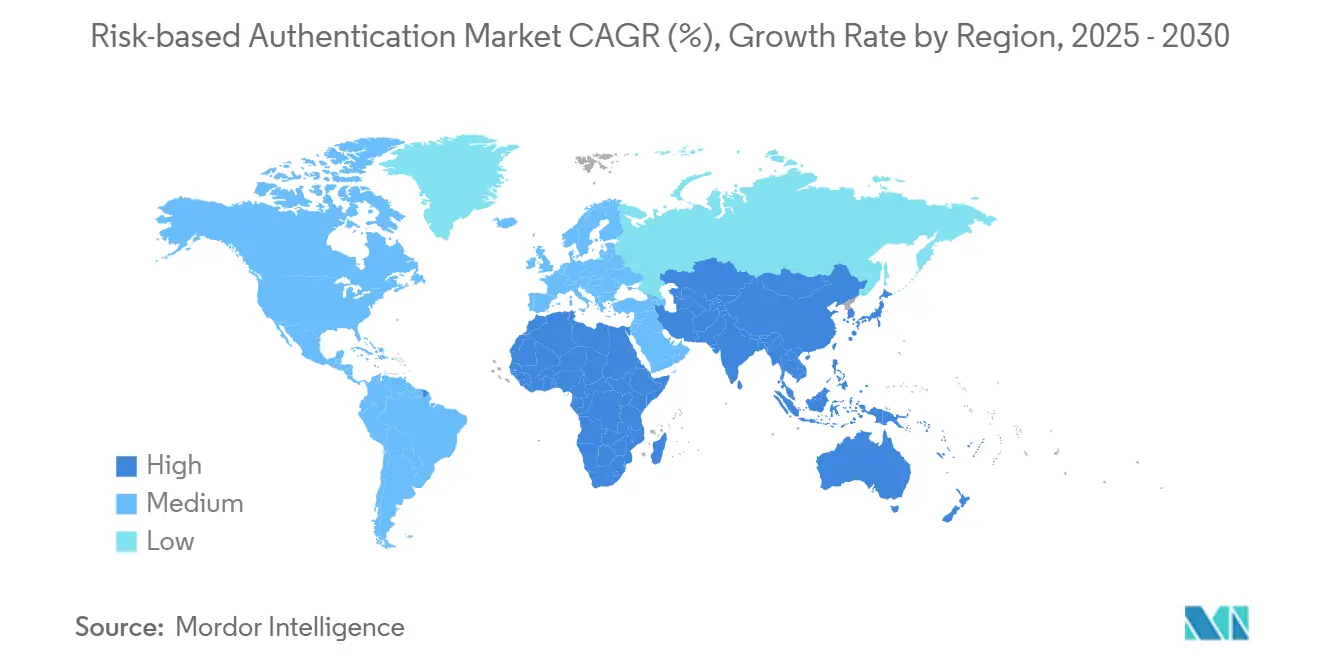

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

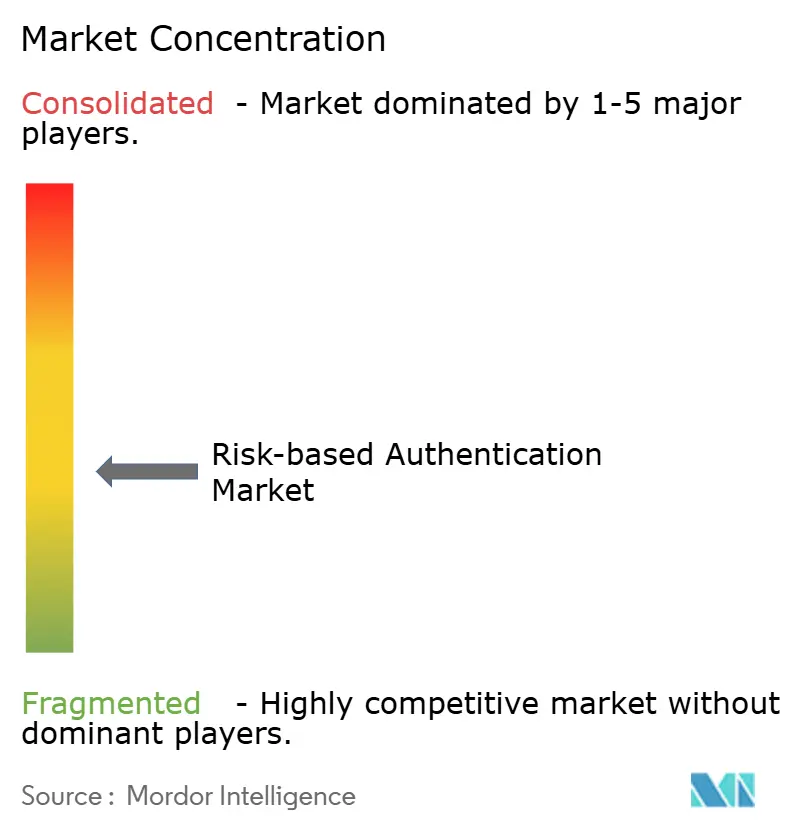

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Risk-based Authentication Market Analysis by Mordor Intelligence

The risk based authentication market size is valued at USD 5.58 billion in 2025 and is forecast to reach USD 7.72 billion by 2030, advancing at a 6.70% CAGR during the period. Heightened cyber attacks, stricter regulatory mandates for strong customer authentication, and the mainstreaming of zero trust architectures collectively propel growth. Cloud delivery models dominate because they scale globally and embed continuous risk evaluation without large capital outlays. Artificial intelligence amplifies adoption by enabling real-time behavioral scoring that lowers false positives and minimizes user friction. Vendors also benefit from surging demand for explainable AI, as regulators intensify scrutiny over algorithmic fairness in authentication decisions.

Key Report Takeaways

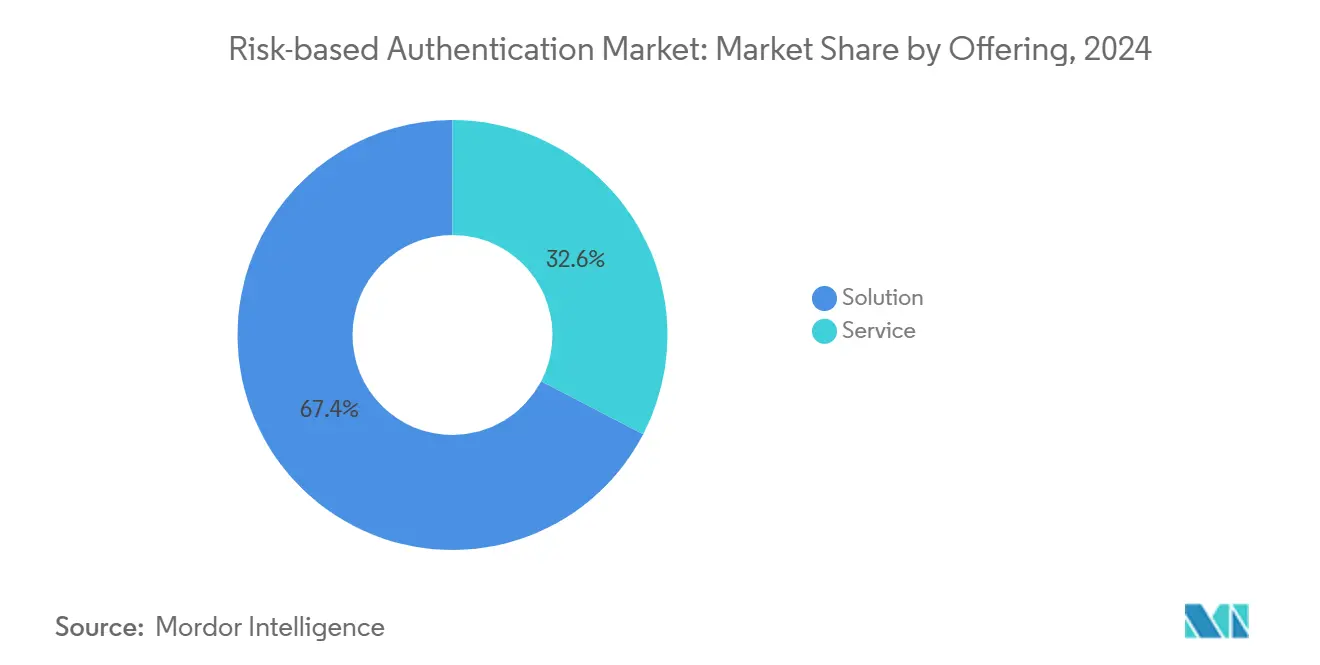

- By deployment, cloud solutions held 71.22% of the risk based authentication market share in 2024, while the on-premise option is projected to rise at only 2.1% CAGR to 2030.

- By offering, services recorded the fastest 8.11% CAGR; solutions retained 67.36% revenue share of the risk based authentication market in 2024.

- By authentication method, multi-factor and composite techniques led with 42.89% revenue share in 2024, whereas adaptive behavioral authentication is set to grow at 6.93% CAGR through 2030.

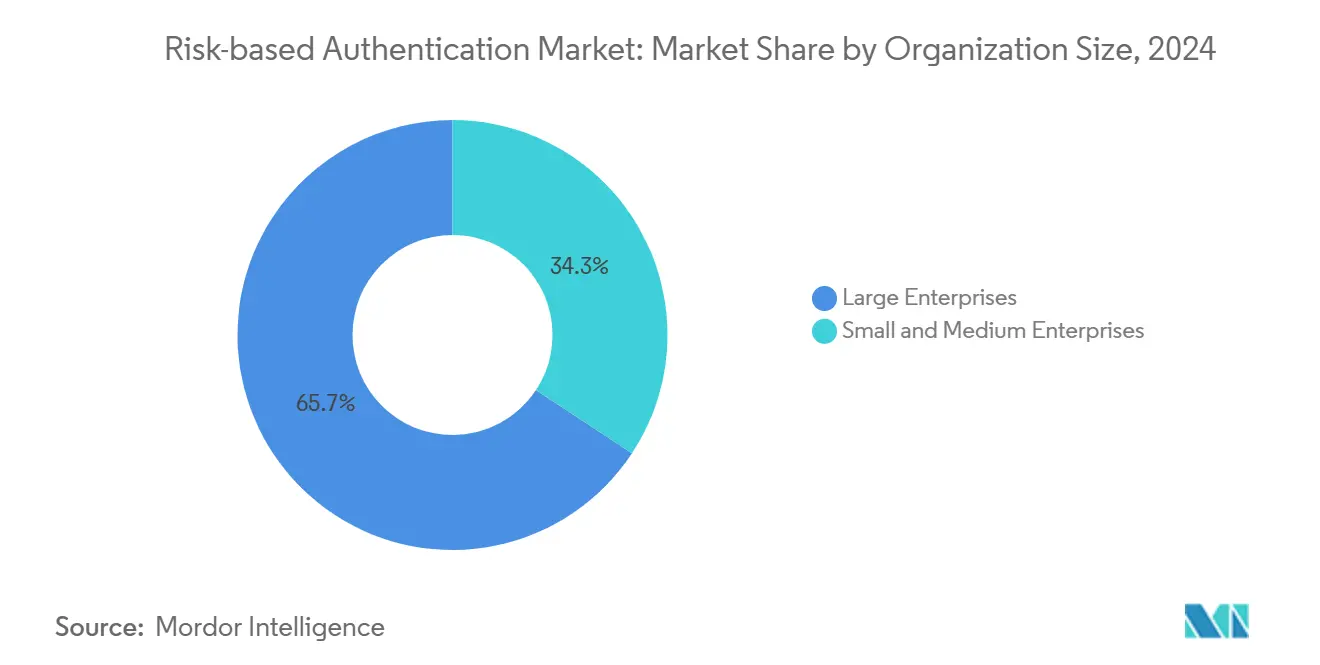

- By organization size, large enterprises accounted for 65.73% of the risk based authentication market share in 2024; small and medium enterprises are expanding at 8.19% CAGR through 2030.

- By end-user vertical, banking and financial services captured 29.71% revenue share in 2024, but healthcare is projected to progress at 6.86% CAGR up to 2030.

- By geography, North America dominated with 35.44% revenue share in 2024, whereas Asia-Pacific is poised for the highest 6.97% CAGR during the forecast horizon.

Global Risk-based Authentication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing data breaches across end-user verticals | +1.2% | North America, Europe | Medium term (2-4 years) |

| Adoption of BYOD policies | +0.8% | Asia-Pacific, North America | Short term (≤2 years) |

| Regulatory mandates for strong customer authentication | +0.9% | Europe, North America, Asia-Pacific | Long term (≥4 years) |

| Integration of behavioral biometrics | +1.1% | Global | Medium term (2-4 years) |

| Passwordless initiatives within zero trust | +1.0% | North America, Europe | Medium term (2-4 years) |

| Expansion of open banking APIs | +0.7% | Europe, Asia-Pacific, Americas | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Data Breaches Across Key Verticals

Frequent credential theft and account takeover attacks motivate enterprises to deploy adaptive checks that inspect behavioral anomalies before granting access. In 2024, 90% of successful cyber incidents originated from compromised credentials.[1]“Zero Trust Maturity Model,” Cybersecurity and Infrastructure Security Agency, cisa.gov Financial firms accelerate investment after several breaches highlighted gaps in static two-factor controls. Healthcare providers add continuous risk scoring to protect patient records while maintaining clinical workflow speed under HIPAA requirements. Insurance carriers leverage risk based authentication data to enrich underwriting decisions and cyber risk policies.

Adoption of BYOD Policies Among Enterprises

Remote work norms cause millions of unmanaged smartphones and laptops to interface with corporate resources. Updated NIST guidelines urge decision-makers to weigh device health and network context as part of every login.[2]“Digital Identity Guidelines: Authentication and Lifecycle Management,” National Institute of Standards and Technology, nist.gov Small businesses in Asia-Pacific favor cloud-native authenticators that auto-adjust challenges based on device trust, cutting back on hardware spending. U.S. employers see productivity gains when personal devices can access resources friction-free yet under continuous monitoring.

Surge in Regulatory Mandates for Strong Customer Authentication

Europe’s Payment Services Directive 2 set a global precedent by obliging financial institutions to apply step-up authentication when transaction risk surpasses predefined thresholds.[3]“Guidelines on Strong Customer Authentication and Common and Secure Communication,” European Banking Authority, eba.europa.eu Similar principles appear in Singapore and Canada, broadening the regulatory perimeter. HIPAA guidance likewise stresses context-aware access proportional to information sensitivity, spurring hospital demand. Providers with explainable AI and detailed audit logs meet auditors’ transparency requirements more readily than rule-driven legacy products.

Integration of Behavioral Biometrics Enhancing Accuracy

Machine learning now profiles keystroke cadence, finger pressure, and touchscreen gestures to detect impostors even when legitimate credentials are present. The FFIEC specifically endorsed behavioral analytics as a best practice in August 2024. Early adopters in banking report lower fraud losses without raising abandonment rates. Hospitals integrate silent behavioral checks to keep clinicians signed in during emergencies yet block anomalous access attempts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation costs for SMEs | -0.6% | Global, especially emerging markets | Short term (≤2 years) |

| Algorithmic bias concerns triggering regulatory scrutiny | -0.4% | North America and Europe | Long term (≥4 years) |

| Limited interoperability standards across heterogeneous identity platforms | -0.5% | Global, pronounced in large multi-vendor enterprises | Medium term (2-4 years) |

| Skills gap in configuring and integrating adaptive authentication solutions | -0.3% | Global, acute in small and medium enterprises | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs for SMEs

Two-thirds of small businesses cite budget limitations as the top barrier to deploying advanced authenticators. Even when cloud models trim capital outlays, many owners lack cyber expertise to configure scoring rules or integrate APIs. Managed service providers step in with turnkey bundles that convert hefty licensing fees into monthly operating expenses. Vendors that package pre-tuned policies and wizard-based setup gain traction among cost-sensitive clinics and boutiques.

Algorithmic Bias Concerns Triggering Regulatory Scrutiny

Regulators warn that machine learning evaluations may inadvertently disadvantage protected classes. The U.S. Federal Trade Commission issued guidance demanding proof of fairness and redress mechanisms in authentication workflows. Proposed EU AI legislation classifies certain identity checks as high-risk, imposing documentation duties on vendors. Enterprises therefore prioritize platforms that supply bias testing dashboards and explainable scores without compromising detection rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum

Services represented USD 1.83 billion of the risk based authentication market size in 2025, and their 8.11% CAGR outpaces software growth. Organizations prefer subscription-based consulting, integration, and managed detection because those packages shortcut deployment and compliance tasks. Solution licenses retained 67.36% revenue share in 2024, yet the widening growth gap signals an enduring pivot toward authentication-as-a-service. Within services, regulation-driven advisory is booming as banks fine-tune PSD2 controls while hospitals realign identity policies with HIPAA deadlines.

The shift compels traditional software publishers to embed monitoring and help-desk functions to stay competitive. Security service providers cross-sell risk based authentication market offerings alongside broader identity suites, buoyed by client demand for single-pane reporting. Customers gravitate toward vendors that include continuous tuning of behavioral models, periodic bias audits, and SLA-backed uptime guarantees.

By Deployment: Cloud Dominates Transformation

Cloud implementations contributed 71.22% of the risk based authentication market size in 2025 and are projected to grow at 8.23% CAGR to 2030. Enterprises value instant scalability and geographic redundancy, key for zero trust programs that must validate every session irrespective of user location. On-premise options persist within public sector and air-gapped environments but face slower refresh cycles and higher maintenance overhead.

Multi-cloud trends boost demand for identity services that run uniformly across AWS, Azure, and private Kubernetes clusters. Vendors answer by decoupling policy engines from specific infrastructures and by offering data residency controls to address sovereignty regulations. Early adopters report quicker feature rollout and 30% lower total cost when migrating from appliance-centric designs to SaaS authenticators, underscoring the cloud’s sustained edge.

By Authentication Method: Adaptive Intelligence Gains Ground

Multi-factor and composite schemes maintained 42.89% revenue share of the risk based authentication market in 2024 thanks to long-standing compliance recognition. Yet adaptive behavioral authentication is forecast to grow at 6.93% CAGR, reflecting a move from static credentials toward invisible, context-aware checks. Password-only logins steadily decline as phishing exploits highlight their fragility.

Vendors are blending device telemetry, location, and micro-behavioral cues to decide whether step-up factors are necessary, thereby cutting average login time by up to 40% compared to blanket MFA. Possession-based tokens stay relevant in defense and critical infrastructure, whereas continuous behavioral biometrics appeal to consumer finance apps eager to keep checkout flows below 15 seconds.

By Organization Size: SME Uptake Accelerates

Large enterprises controlled 65.73% revenue share in 2024, driven by extensive IT budgets and stricter audit regimes. However, the small and medium enterprise segment is poised to add the greatest absolute user count, expanding at 8.19% CAGR. Simplified SaaS dashboards, pay-as-you-grow tiers, and low-code connectors allow resource-constrained teams to adopt policies once reserved for Fortune 500 firms.

Industry alliances provide templated rulesets for retail, clinics, and legal practices, thereby abstracting algorithm tuning complexities. As MSPs bundle authentication with email security and endpoint monitoring, SMEs gain an integrated defense posture without staffing a full-time security analyst.

By End-user Vertical: Healthcare Surges

Banking retained 29.71% revenue share of the risk based authentication market size in 2024 because PSD2, AML, and fraud-loss pressures justify sizable investments. Strong customer authentication remains table stakes for new digital banking entrants competing on trust and UX. Healthcare, however, will clock 6.86% CAGR through 2030 as electronic health record portals, telemedicine, and connected devices multiply access points.

Clinicians require low-friction sign-ins during emergencies, prompting adoption of silent behavioral checks paired with smart badges. Pharmacies embed risk scoring into prescription authorization to detect diversion attempts. Regulators now audit hospitals for evidence that access controls adapt to data sensitivity, propelling continuous authentication into operating theaters and intensive care units.

Geography Analysis

North America generated 35.44% of global revenue in 2024, underpinned by stringent NIST frameworks and early zero trust rollouts. The United States federal push for identity modernization fuels purchases across defense, energy, and civilian agencies. Canada’s financial institutions follow suit to align with AML and consumer-protection statutes. Venture funding remains abundant, enabling start-ups to pilot behavioral AI models that overhaul legacy MFA.

Asia-Pacific is set to deliver a 6.97% CAGR, the strongest worldwide. Government roadmaps such as Singapore’s Model AI Governance Framework require algorithm transparency, encouraging adoption of vendors that expose bias dashboards. India’s digital identity stack and Australia’s open banking program jointly create outsized authentication volumes. Japan’s cashless push and South Korea’s digital banking contests further enlarge addressable demand for frictionless yet explainable risk scoring.

Europe maintains steady expansion anchored in PSD2’s compulsory step-up verification. The European Banking Authority’s technical standards sharpen financial sector procurement criteria, while GDPR influences every vertical to add contextual permissioning and data minimization. Enterprises across Germany and France favor platforms with on-premise fail-over to satisfy sovereignty clauses. Emerging deployments in the Middle East and Africa and South America mirror European frameworks as governments digitize public services and push inclusive financial agendas.

Competitive Landscape

The risk based authentication market features moderate fragmentation: legacy identity suites, behavioral analytics pure-plays, and born-in-cloud platforms vie for wallet share. RSA Security, IBM, and Microsoft bolster suites via acquisitions that inject AI signal processing. Okta’s merger with Auth0 exemplifies platform consolidation aimed at covering both workforce and customer identities.

Specialists such as BioCatch and BehavioSec differentiate through patented gesture and touch models that spot impostors within 300 milliseconds. Cloud-first entrants provide pre-packaged connectors for SaaS apps, appealing to mid-market buyers. Hardware token makers pivot toward FIDO2 passwordless keys, while API-driven platforms open marketplaces so third parties can embed industry-specific risk signals.

Partnerships with payment processors and EHR vendors grant incumbents sticky integration points that newcomers must dislodge. Interoperability alliances under the FIDO Alliance and OpenID Foundation gain strategic importance as buyers demand unified policies across heterogeneous estates. Pricing wars concentrate in the SME segment, spurring vendors to release freemium tiers that seed future upsells to adaptive AI modules.

Risk-based Authentication Industry Leaders

RSA Security LLC

IBM Corporation

Broadcom Inc.

Micro Focus International plc

Okta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft introduced Entra ID Protection enhancements that analyze behavioral deviations across Microsoft 365 and issue inline risk scores.

- September 2025: Okta finalized a USD 6.5 billion acquisition of Auth0, merging workforce and customer identity platforms into a unified codebase.

- August 2025: IBM Security launched Watson for Cyber Security Authentication, applying natural language processing to contextual risk signals for login decisions.

- July 2025: RSA Security partnered with Amazon Web Services to embed its risk scoring algorithms into AWS Identity and Access Management.

Global Risk-based Authentication Market Report Scope

The scope of the current publication of the risk-based authentication market includes revenue generated by different solutions and services which offer Risk-based authentications.

Risk-based authentication (RBA) is a non-static authentication system that takes into account the profile of the user that is requesting to access the system in order to determine the risk profile associated with that transaction. These systems evaluate the credentials when a person attempts to access an application, database, or any other secure resource.

The scope of the study also covers the trends, revenue, and forecasts for different end-user verticals such as banking and financial services, retail, IT, and telecommunications, among others.

The revenue generated through standalone Multi-factor authentication and other authentication solutions and services is not considered as part of the study.

| Solution |

| Service |

| On-premise |

| Cloud |

| Knowledge-based Authentication |

| Possession-based Authentication |

| Inherence-based/Biometrics |

| Adaptive Behavioral Authentication |

| Multi-factor/Composite Methods |

| Large Enterprises |

| Small and Medium Enterprises |

| Banking and Financial Services |

| Retail |

| IT and Telecommunication |

| Government |

| Healthcare |

| Other End-user Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Offering | Solution | ||

| Service | |||

| By Deployment | On-premise | ||

| Cloud | |||

| By Authentication Method | Knowledge-based Authentication | ||

| Possession-based Authentication | |||

| Inherence-based/Biometrics | |||

| Adaptive Behavioral Authentication | |||

| Multi-factor/Composite Methods | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Vertical | Banking and Financial Services | ||

| Retail | |||

| IT and Telecommunication | |||

| Government | |||

| Healthcare | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the risk based authentication market in 2030?

It is expected to reach USD 7.72 billion, reflecting a 6.70% CAGR from 2025.

Which deployment mode leads adoption of risk based authentication?

Cloud-based delivery commanded 71.22% revenue share in 2024 and continues to expand fastest.

Why are healthcare organizations accelerating adoption of adaptive authentication?

HIPAA compliance and the need for seamless clinical workflows drive a 6.86% CAGR in healthcare deployments.

How do regulatory mandates influence authentication investments in banking?

PSD2 and similar rules require transaction-level risk assessment, sustaining banking’s 29.71% revenue share.

What main challenge do small businesses face when implementing risk based authentication?

Upfront and ongoing costs remain the leading barrier, cited by 67% of SMEs in SBA research.

Which region is set to grow fastest through 2030?

Asia-Pacific, supported by digital transformation programs and evolving AI governance, will grow at 6.97% CAGR.

Page last updated on: