Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Passive Authentication Market Report is Segmented by Component (Solutions, Services), Authentication Technology (Behavioral Biometrics, Face and Gesture Recognition and More), Deployment Mode (Cloud, On-Premises), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Retail and E-Commerce, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

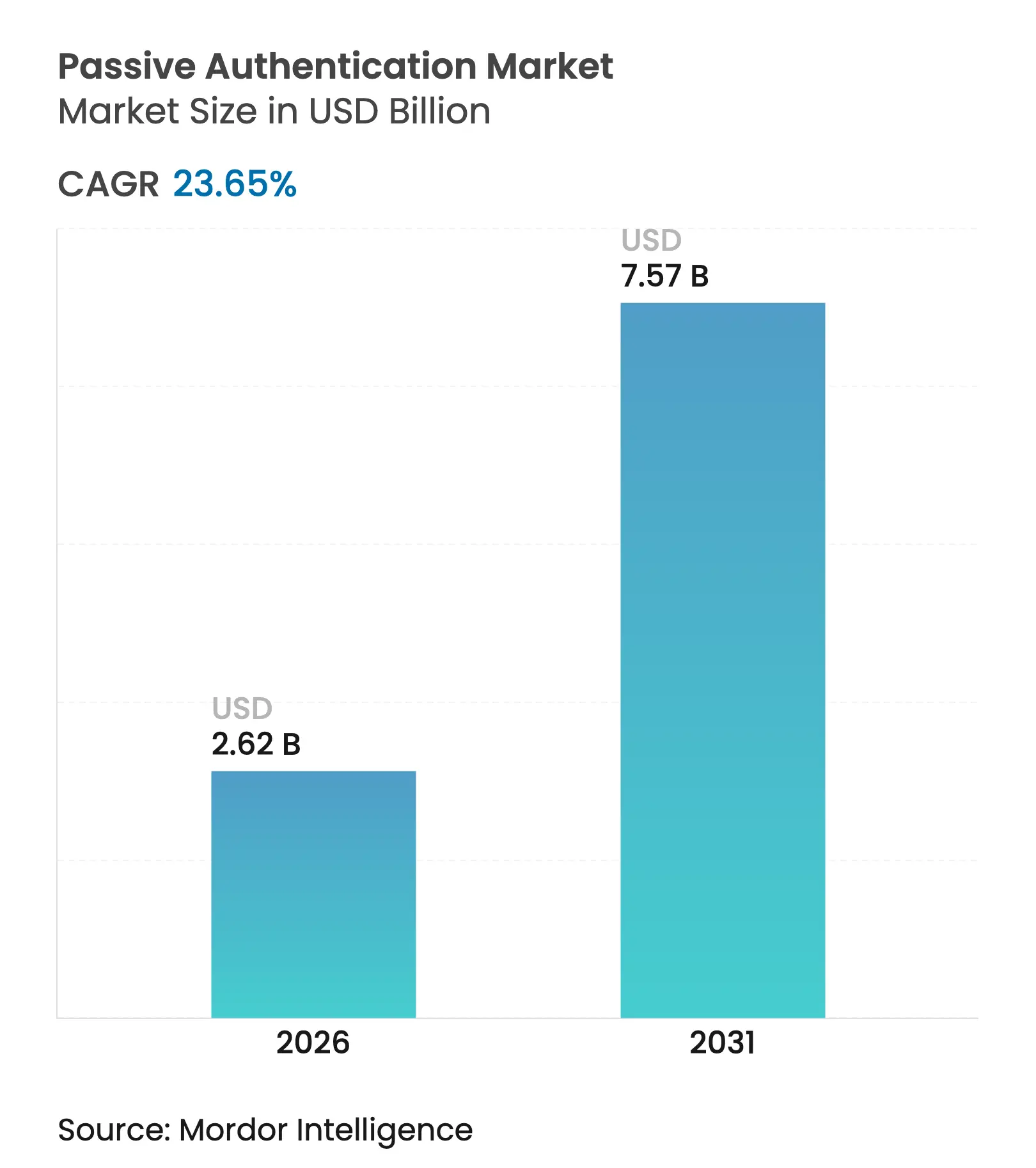

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 7.57 Billion |

| Growth Rate (2026 - 2031) | 23.65 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Passive Authentication Market size was valued at USD 2.12 billion in 2025 and estimated to grow from USD 2.62 billion in 2026 to reach USD 7.57 billion by 2031, at a CAGR of 23.65% during the forecast period (2026-2031). Demand escalates as enterprises confront AI-generated identity fraud, integrate biometric factors into payment journeys, and expand zero-trust programs. Regulatory mandates such as Europe’s PSD2 Strong Customer Authentication (SCA) and Asia’s emerging biometric requirements push behavioral and multi-modal techniques into mainstream deployment. Cloud delivery remains the preferred model thanks to rapid scalability and API-first integration, while managed services gain traction among resource-constrained SMEs. Competitive intensity rises as established identity vendors acquire behavioral specialists and as API-centric start-ups pursue vertical-specific offerings.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

AI-driven

deepfake fraud escalation

AI-driven

deepfake fraud escalation

| +6.2% | Global, with concentration in North America & Europe | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:+6.2% | Geographic Relevance:

Global,

with concentration in North America & Europe

| Impact Timeline:

Short

term (≤ 2 years)

|

Digital

banking boom in emerging Asia

Digital

banking boom in emerging Asia

| +5.8% | Asia Pacific core, spill-over to MEA | Medium term (2-4 years) | |||

PSD2

SCA mandate

PSD2

SCA mandate

| +4.1% | Europe, with regulatory influence in UK & Canada | Medium term (2-4 years) | |||

API-First

Embedded-Finance Platforms Demanding Invisible Authentication

API-First

Embedded-Finance Platforms Demanding Invisible Authentication

| +4.2% | Global, with fintech concentration in North America & Europe | Long term (≥ 4 years) | |||

Surge

in call-center account-takeover attacks

Surge

in call-center account-takeover attacks

| +3.7% | Global, with early adoption in North America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

AI-driven deepfake fraud escalation

Financial institutions are experiencing synthetic-identity attacks that compromise voice verification channels, prompting rapid adoption of multi-modal passive checks that combine device, behavioral, and location signals to neutralize cloned audio and video. BioCatch reports that 91% of fraud executives are re-evaluating voice-based methods as criminals weaponize generative AI.[1]BioCatch, “BioCatch Releases Inaugural Annual Report on AI’s Impact on Digital Fraud and Financial Crime,” biocatch.com

Digital banking boom in emerging Asia

Mobile-first banks and e-wallet operators need invisible security layers that preserve user experience at scale. Regional mandates for biometric log-ons and cross-border payment frameworks such as Project Nexus create fertile ground for passive risk-scoring engines that operate across borders without additional friction.[2]Jumio, “The Key to Digital Payment Compliance in Asia Pacific,” jumio.com

PSD2 SCA mandate

European regulators now recognize biometric traits including behavioral patterns as valid inherence factors. Banks therefore deploy continuous keystroke and cursor-movement analytics to satisfy the “dynamic linking” requirement without forcing additional steps on users.[3]European Banking Authority, “Regulatory Technical Standards on Strong Customer Authentication and Secure Communication,” eba.europa.eu

Surge in call-center account-takeover attacks

Voice spoofing in telephone banking and telecom support channels increases operational losses. Pindrop’s liveness-analysis platform spots synthetic speech modulations, allowing carriers and banks to confirm caller legitimacy in the background.[4]Pindrop, “Pindrop Secures $100 Million Financing to Accelerate Fraud and Deepfake Detection Technologies,” pindrop.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

GDPR /

CCPA limits on behavioral data collection

GDPR /

CCPA limits on behavioral data collection

| -2.8% | Europe & California, with global privacy spillover | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-2.8%

| Geographic Relevance:

Europe

& California, with global privacy spillover

| Impact Timeline:

Long

term (≥ 4 years)

|

Algorithmic

bias and model drift

Algorithmic

bias and model drift

| -1.9% | Global, with higher impact in diverse demographic markets | Medium term (2-4 years) | |||

Legacy

IAM Integration Complexity Slowing Enterprise Roll-outs

Legacy

IAM Integration Complexity Slowing Enterprise Roll-outs

| -1.5% | Global, with higher impact in North America & Europe | Medium term (2-4 years) | |||

Regulatory

Skepticism Over "Invisible" Authentication Transparency

Regulatory

Skepticism Over "Invisible" Authentication Transparency

| -1.2% | Global, with concentration in highly regulated markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

GDPR / CCPA limits on behavioral data collection

Data-minimization rules restrict continuous profiling, compelling providers to adopt privacy-preserving techniques such as differential privacy and federated learning. These architectures reduce exposure to consent risk but increase computational overhead.

Algorithmic bias and model drift

Authentication accuracy can erode when training data lack demographic diversity. Scientific studies confirm variance in keystroke dynamics across age and cultural cohorts, pressuring vendors to deploy bias-detection frameworks and continuous model retraining.

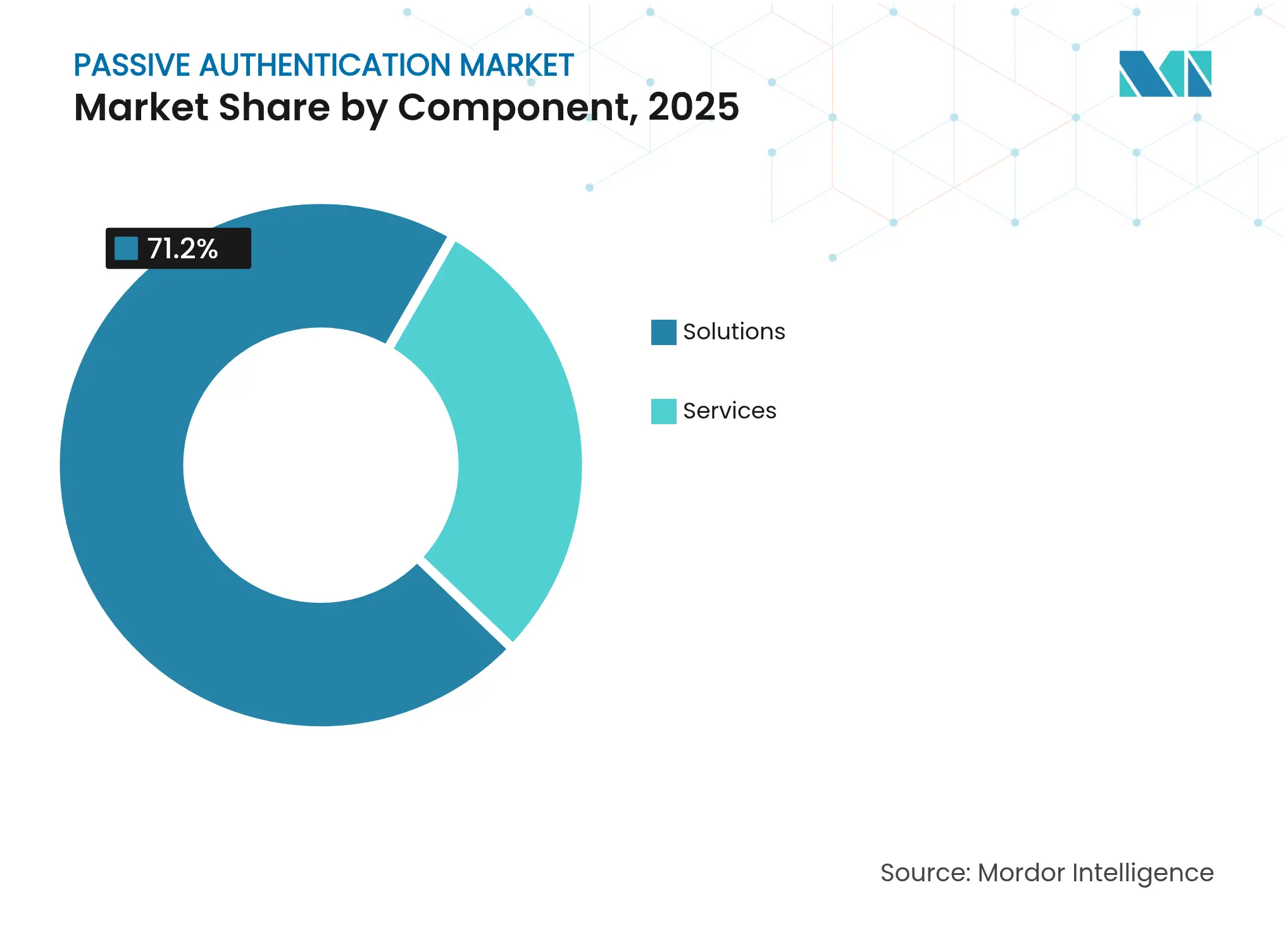

By Component: Services Expand as Integration Grows Complex

The services segment, while smaller, is projected to rise at a 24.45% CAGR through 2031 as organizations seek custom integrations, behavioral-model tuning, and 24/7 monitoring. Firms outsource algorithm maintenance and compliance reporting to managed-security providers that blend SOC operations with biometric expertise. Platform vendors respond by launching partner ecosystems, allowing consultancies to embed domain-specific dashboards inside broader risk-management suites.

Solutions remain the headline revenue engine, reflecting 71.20% of the passive authentication market in 2025. Product roadmaps emphasize low-code configuration and developer-friendly APIs that accelerate proof-of-concept rollouts. As multi-modal functions mature, vendors bundle behavioral, device, and document verification modules into a unified orchestration layer, shrinking the time from pilots to enterprise-wide deployment.

Note: Segment shares of all individual segments available upon report purchase

By Authentication Technology: Multi-Modal Fusion Overtakes Single-Factor Tactics

Behavioral biometrics retained 37.40% share in 2025 by exploiting continuous user-interaction signals to generate contextual risk scores. Advances in gait, gesture, and micro-emotion analytics expand coverage to mobile and wearable endpoints. The passive authentication market size for behavioral techniques is expected to rise steadily as enterprises embed keyboard, mouse, and touchscreen data into fraud engines.

Multi-modal authentication is the fastest-growing cohort at a 24.95% CAGR. Banks, hospitals, and airlines combine voice, face, and device telemetry within a single decision framework to counter deepfake threats. Vendors apply score-level fusion logic illustrated by patented multimodal decision algorithms to balance false positives against usability targets, enabling step-up challenges only when anomalies emerge.

By Deployment Mode: Cloud Leads as Zero-Trust Initiatives Mature

Cloud deployments captured 67.10% of the passive authentication market share in 2025 and sustain a 21.55% CAGR through 2031. Enterprises cite infrastructure-light rollouts, elastic capacity, and immediate access to threat-intelligence updates as primary reasons for cloud preference. Continuous integration pipelines let security teams refine behavioral models weekly without costly hardware refreshes.

On-premises installations persist in defense, government, and tightly regulated healthcare environments where data residency is non-negotiable. Hybrid and edge architectures gain popularity, placing inference engines at branch locations or mobile devices while reserving model-training tasks for centralized clouds. This topology reduces latency and ensures resilience when connectivity dips.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

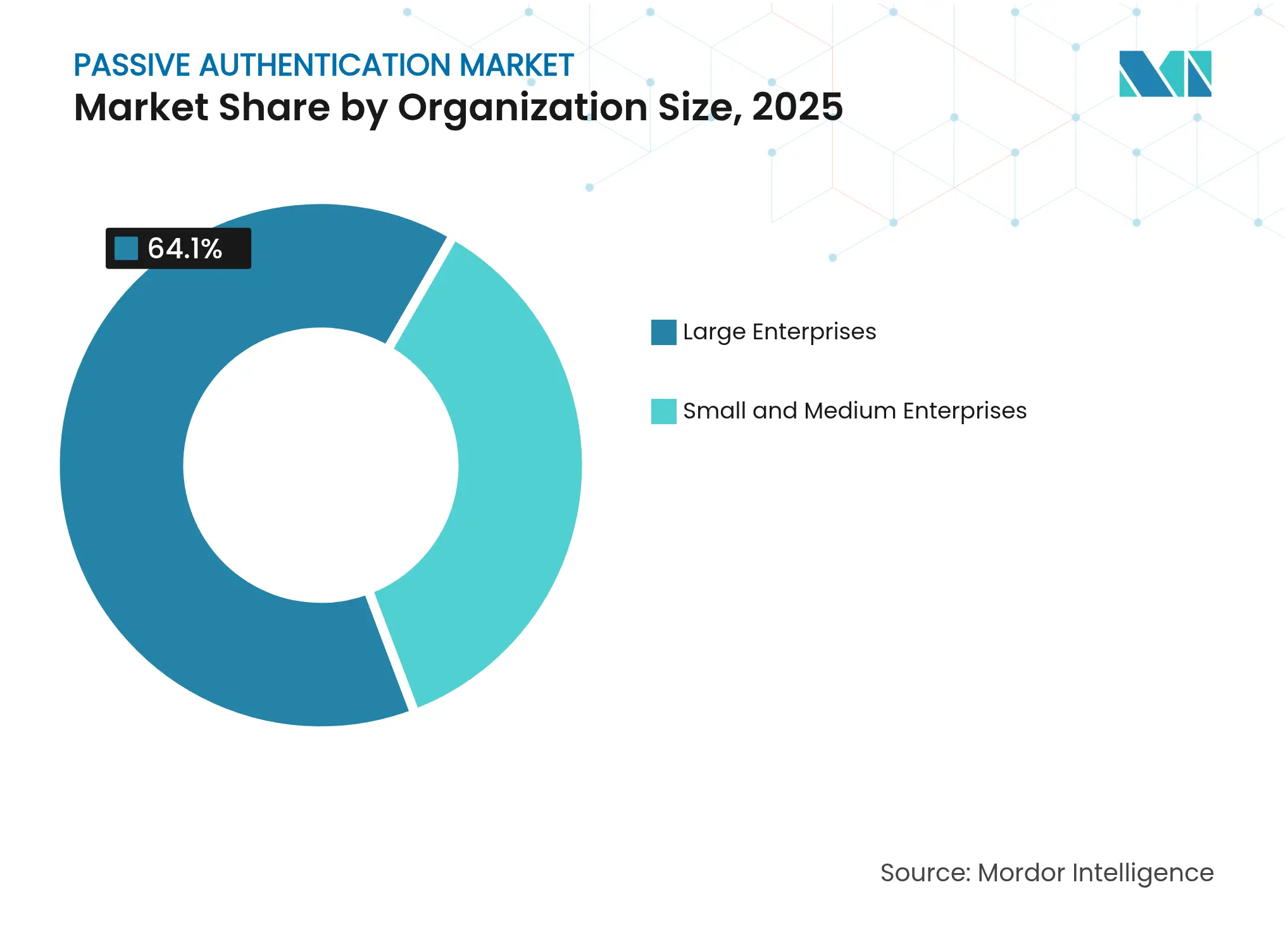

By Organization Size: SME Uptake Accelerates via Managed Services

Large enterprises commanded 64.10% of 2025 revenue thanks to sizeable fraud budgets, yet SMEs are registering a 25.75% CAGR as cost-effective SaaS subscriptions lower barriers to entry. Managed authentication services wrap identity orchestration, behavioral-model calibration, and compliance reporting into monthly fees that align with SME cash-flow cycles.

API-first vendors now market “plug-and-trust” kits that clients integrate within hours, bypassing protracted procurement cycles and heavy professional-service bills. As fintechs embed payment capabilities into small-business software, passive checks execute behind the scenes, delivering enterprise-grade security without local infrastructure.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare Emerges as Growth Leader

BFSI retained 41.30% of 2025 revenue because regulatory scrutiny and high fraud exposure make advanced authentication non-negotiable. Continuous behavioral monitoring detects session anomalies, blocking mule accounts and synthetic identities in real time.

Healthcare and life sciences exhibit the fastest growth at a 23.95% CAGR. Telemedicine platforms and electronic health-record portals must validate patient identities without hampering clinical workflows. Palm-vein and gait analytics perform seamlessly in gloves, masks, or wheelchairs, satisfying hospital security and inclusion requirements. Retail and e-commerce operators deploy behavior-based trust scores to suppress cart abandonment while throttling bot traffic. Telecommunications firms leverage voice fingerprints in call centers to shorten interactive-voice-response (IVR) menus and cut average handle time.

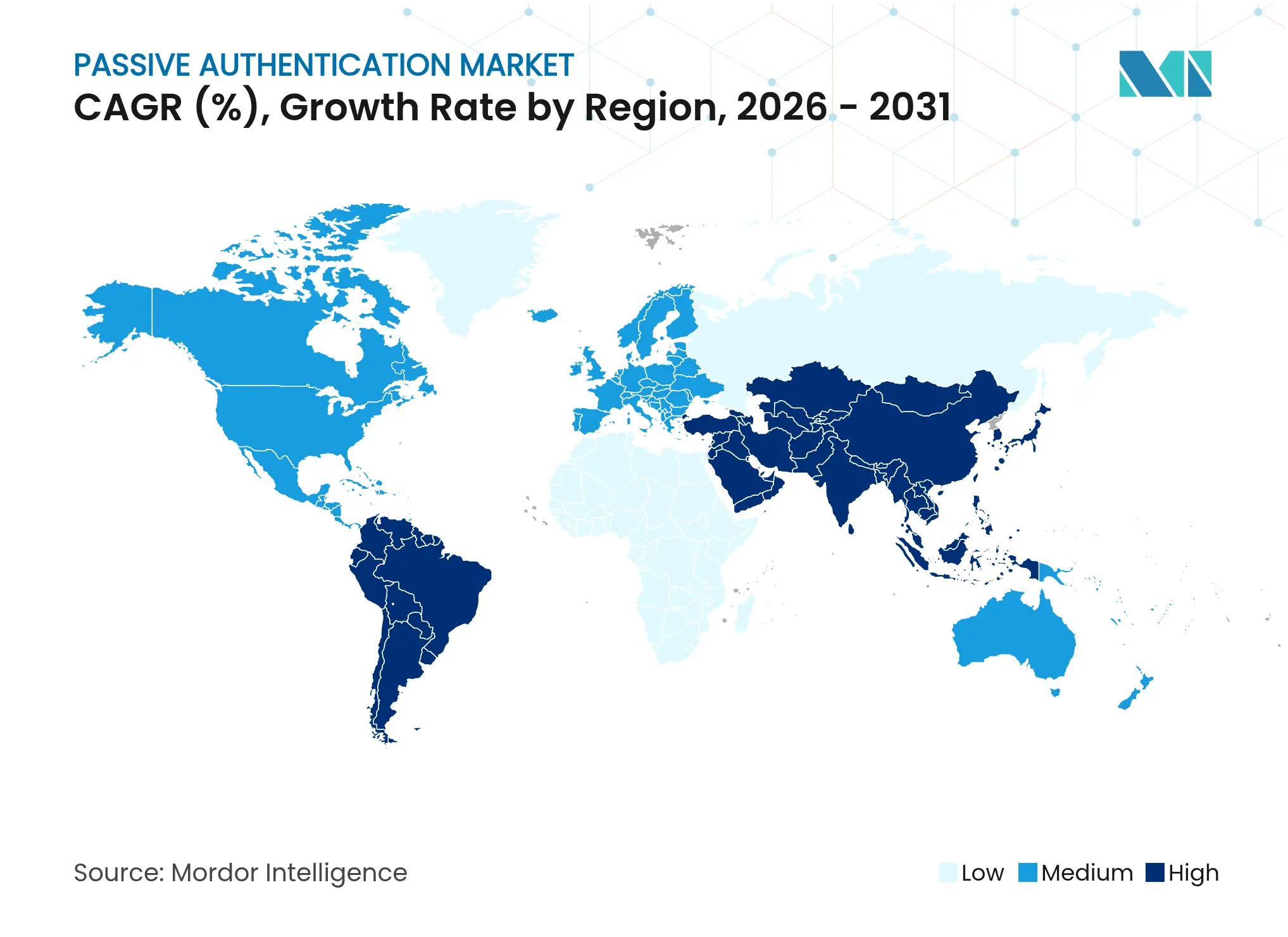

North America, holding 39.40% of 2025 revenue, benefits from mature cyber budgets and an active regulatory discourse. The Federal Reserve urges stronger defenses against AI-enabled identity fraud, and U.S. firms collectively invest in patent portfolios that anchor best-practice frameworks for global adoption. Canada harmonizes privacy rules with Europe, creating cross-border authentication corridors. Continued healthcare digitization further elevates demand for secure yet friction-free identity assurance.

Asia-Pacific is the fastest-growing region, projected at a 24.05% CAGR. Biometric mandates across Indonesia, Vietnam, and Singapore position passive checks as standard practice for account opening and payments. China and India contribute scale by embedding device and behavioral analytics into super-apps, while Japanese and South Korean enterprises adopt multi-modal fusions for factory and retail automation. Regional payment-network initiatives require portable identity proofs, promoting standards convergence across borders.

Europe maintains steady momentum under PSD2 SCA. Banks leverage behavioral analytics to satisfy inherence factors and to enable seamless “dynamic linking” of high-risk transactions. Nordic states integrate passive authentication into national e-ID schemes, and Germany and France push enterprise use cases in manufacturing and automotive. The United Kingdom experiments with sandbox regulation, giving fintechs latitude to pilot privacy-preserving federated-learning models. Across the Middle East and Africa, smart-city and financial-inclusion programs catalyze pilot deployments that blend face, fingerprint, and device telemetry to authenticate citizens at point of service.

Market Concentration

The passive authentication market shows moderate fragmentation. Top platforms combine patents in behavioral analytics, device intelligence, and liveness detection to reinforce product moats. Leading vendors partner with system integrators to deliver sector-focused blueprints, for example, voice-centric packages for telecoms or palm-vein kits for hospitals.

API-centric challengers differentiate through lightweight SDKs and transparent usage-based pricing. Their go-to-market strategy stresses rapid developer adoption, aligning with fintech and SaaS ecosystems that favor low-code integration. Strategic funding rounds, such as Pindrop’s USD 100 million capital injection to expand deepfake detection capabilities, underline investor confidence in AI-driven behavioral defense.

M&A momentum is evident as identity incumbents acquire niche biometrics firms to gain proprietary algorithms and expand into new verticals. Patent US20090171623A1 on multimodal fusion logic illustrates the technical hurdles newcomers face when building state-of-the-art score-combination engines. Market participants increasingly tout privacy-preserving AI as a differentiator, balancing compliance with performance in regions governed by stringent data-protection laws.

*Disclaimer: Major Players sorted in no particular order

1. Table of Contents

2. INTRODUCTION

3. RESEARCH METHODOLOGY

4. EXECUTIVE SUMMARY

5. MARKET LANDSCAPE

6. MARKET SIZE AND GROWTH FORECASTS (VALUE)

7. COMPETITIVE LANDSCAPE

8. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A passive Authentication is a form of authentication in which the user's identity is checked and confirmed without requiring specific additional actions for authentication. Instead, the user's activity, properties, or other observable data are gathered and analyzed for evidence of identity without further intervention from, or work by, the user. Passive authentication is, in essence, frictionless.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.