Mobile Devices User Authentication Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

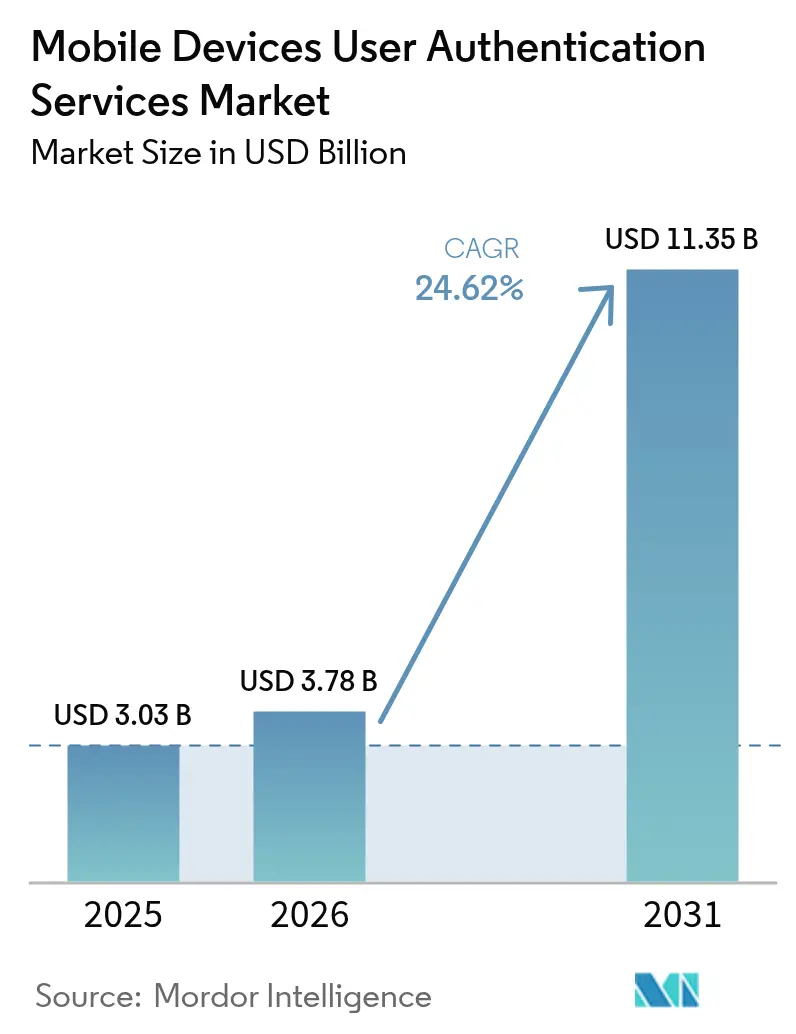

| Market Size (2026) | USD 3.78 Billion |

| Market Size (2031) | USD 11.35 Billion |

| Growth Rate (2026 - 2031) | 24.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Devices User Authentication Services Market Analysis by Mordor Intelligence

The mobile devices user authentication services market size is expected to grow from USD 3.03 billion in 2025 to USD 3.78 billion in 2026 and is forecast to reach USD 11.35 billion by 2031 at 24.62% CAGR over 2026-2031. Structural demand is shifting from passwords toward phishing-resistant verification, reflected in the 550% jump in passkey roll-outs during 2024 and the 26% CAGR expected for passwordless platforms between 2025-2030. Heightened regulatory scrutiny—ranging from Europe’s Strong Customer Authentication (SCA) rules to the U.S. Department of Defense Zero Trust Roadmap—is catalyzing multi-factor deployments that satisfy regional compliance needs while raising the performance bar for vendors.[1]U.S. Department of the Air Force, “DAF Enterprise Zero Trust Roadmap,” dafcio.af.mil Competitive strategies now center on ecosystem integration: platform leaders push broad identity fabrics while specialists capture growth pockets in hardware keys, behavioral analytics, and carrier APIs. Against this backdrop, enterprises recognise the economic upside of passwordless authentication, with JumpCloud reporting that device-level biometrics reduce credential management overhead and breach costs in equal measure.

Key Report Takeaways

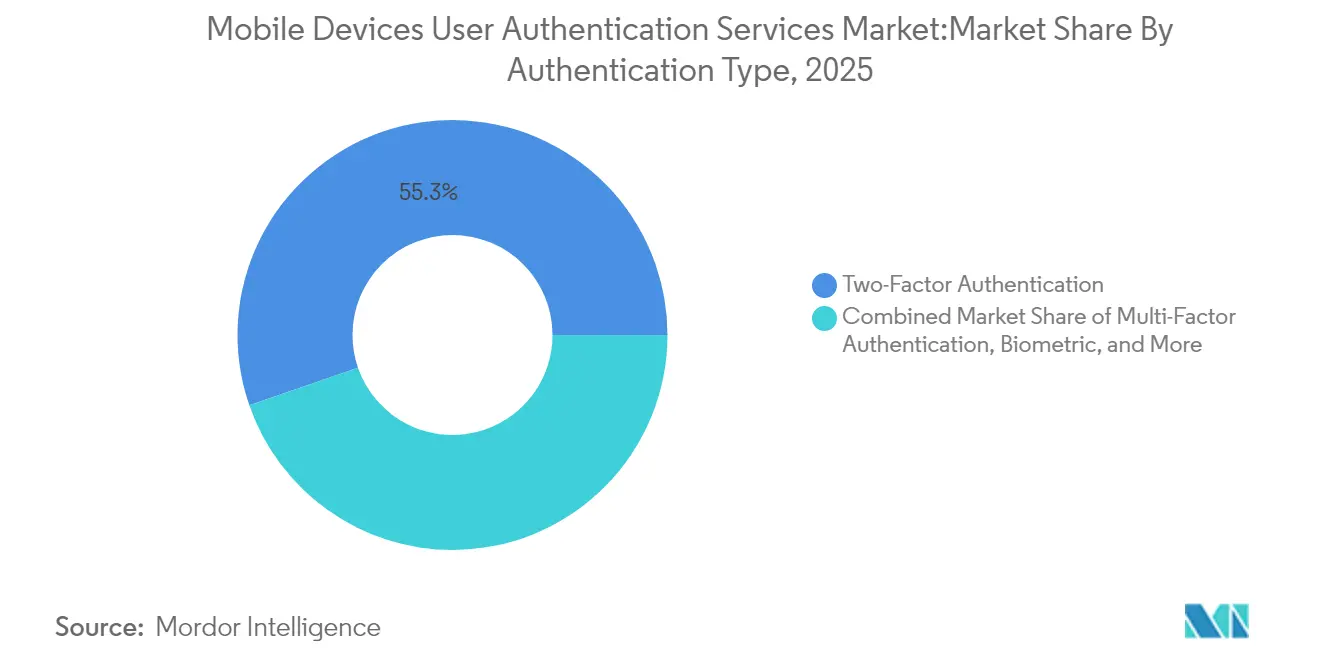

- By authentication type, Two-Factor/MFA held 55.30% of the mobile devices user authentication services market share in 2025, while Passwordless Authentication is projected to grow at a 25.20% CAGR through 2031.

- By deployment mode, cloud-based Authentication-as-a-Service commanded 59.10% share in 2025; hybrid edge + cloud models are set to advance at 22.10% CAGR to 2031.

- By authentication channel, SMS OTP accounted for 44.20% of the mobile devices user authentication services market size in 2025, whereas push notification authentication is forecast to rise at 23.20% CAGR to 2031.

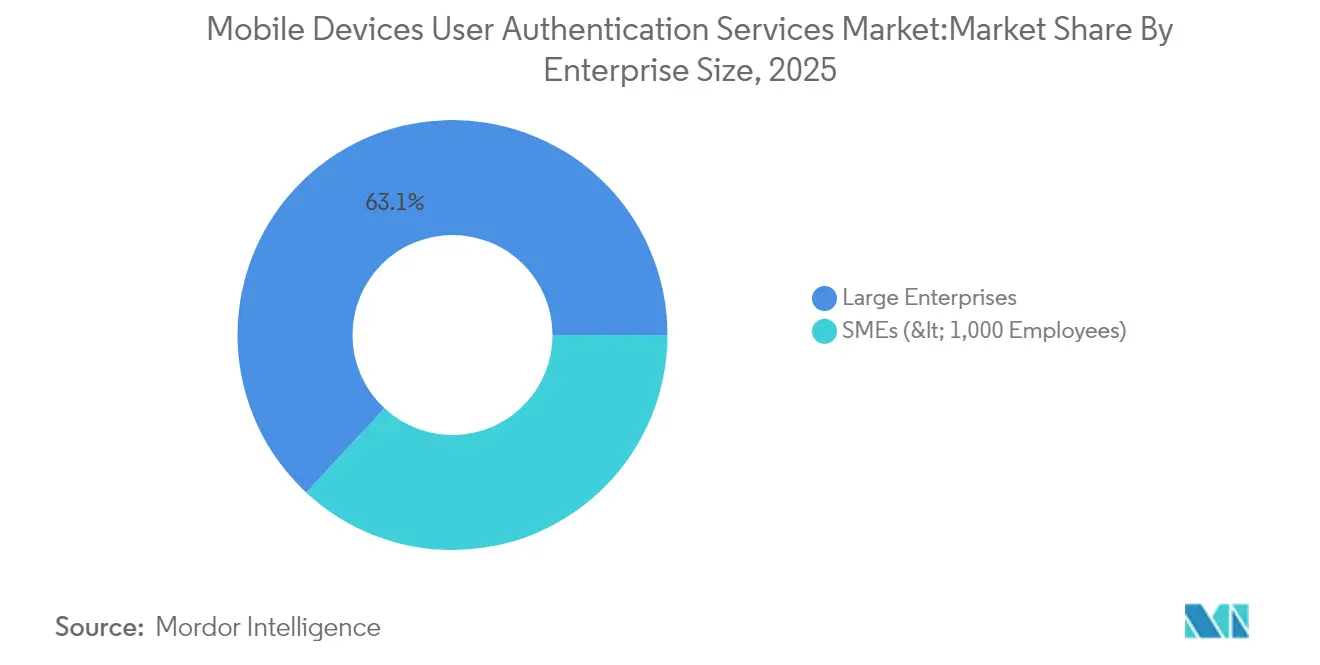

- By enterprise size, large enterprises contributed 63.10% revenue share in 2025, but the SME segment is expected to accelerate at 23.70% CAGR during 2026-2031.

- By end-user vertical, the BFSI sector led with 33.05% share in 2025; healthcare and life sciences is anticipated to register the fastest expansion at 24.90% CAGR through 2031.

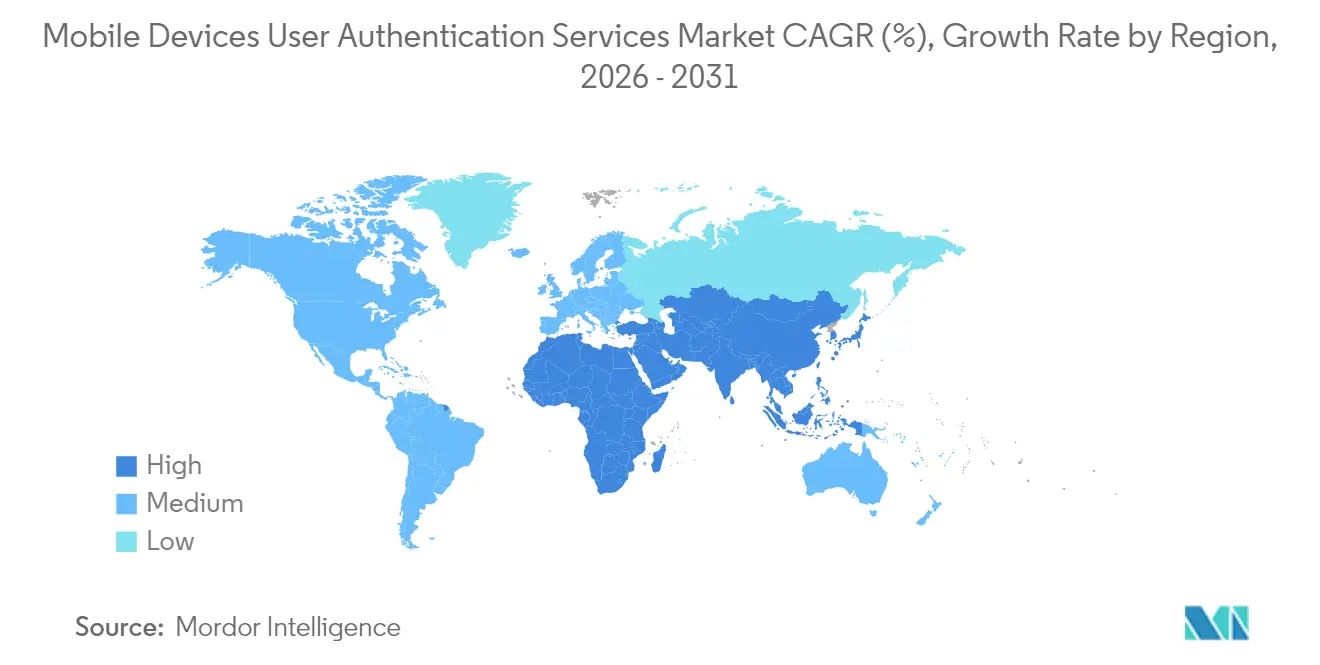

- By geography, North America maintained 37.40% share in 2025, yet Asia is projected to climb at 27.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Devices User Authentication Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of passwordless and WebAuthn standards | +5.8% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Surge in FinTech and mobile banking (SCA compliance) | +4.7% | Europe, North America, rising in Asia | Short term (≤ 2 years) |

| Mid-range smartphone biometric hardware penetration | +4.2% | Asia (China, India, ASEAN-5) | Medium term (2-4 years) |

| Enterprise zero-trust security architecture | +4.9% | North America, Europe, advanced Asian economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption of Passwordless and WebAuthn Standards Across Mobile-First Enterprises

Seventy percent of organisations either plan to adopt or have already introduced passwordless authentication, illustrating how WebAuthn shifts the security baseline. Native support from platform incumbents such as Microsoft Entra ID embeds passkey functionality directly into device hardware, eradicating shared-secret risk while simplifying user journeys. Consumer familiarity with passkeys rose to 57% in 2025, up from 39% three years earlier, signalling readiness for large-scale transition.[2]JumpCloud, “Passwordless Authentication Adoption Trends in 2025,” jumpcloud.comMomentum will intensify as banks, airlines and travel portals adopt FIDO-compliant flows in 2025, confirming passwordless as a mainstream control for high-value mobile transactions. Vendors able to orchestrate cross-platform credential mobility stand to win disproportionate share in the mobile devices user authentication services market.

Surge in FinTech and Mobile Banking (SCA Compliance) Driving MFA Roll-outs

European Banking Authority guidance ruling out device-unlock biometrics as a standalone SCA accelerates multi-factor adoption, forcing issuers to build layered verification that combines biometrics, possession factors, and dynamic risk checks. The expected PSD3 proposal will further prohibit mobile-only flows, prompting banks to embed out-of-band authenticators. Spillover into adjacent digital commerce is material; e-commerce, ride-hailing, and gig-work platforms adopt banking-grade controls to satisfy consumer trust and regulatory parity. These converging demands underpin double-digit growth in the mobile devices user authentication services market across financial and quasi-financial ecosystems.

Mid-Range Smartphone Biometric Hardware Penetration in Asia

Component cost declines enable fingerprint sensors and 3-D face cameras to reach mid-tier handsets, unlocking software-based FIDO authenticators for hundreds of millions of users. Chinese OEMs now bundle multimodal perception chips, lifting AI-digitalisation system revenue at players such as Beijing Yunji Technology at 64.6% CAGR since 2020.[3]Beijing Yunji Technology, “Prospectus,” hkexnews.hkIndia’s Aadhaar-linked digital identity journey and fast-rising UPI payments reinforce demand for frictionless authentication at scale. As biometric coverage climbs, service providers can decommission SMS OTP fallback, lowering cost while improving completion rates. The result is a structural tailwind that positions Asia as the single largest incremental revenue pool for the mobile devices user authentication services market by 2030.

Enterprise Zero-Trust Security Architecture Accelerating Mobile Authenticator Adoption

More than 60% of enterprises are replacing perimeter VPNs with zero-trust network access, a shift that elevates continuous identity verification as the first line of defence. Yet Enterprise Management Associates finds that only 43% explicitly address lateral movement, creating gaps that attackers exploit. Mobile authenticators close this gap by validating session integrity every time a user accesses micro-segmented resources. The U.S. Defense Department’s FY27 deadline for phishing-resistant authentication sets a template that commercial enterprises are already mirroring, cementing market acceleration in North America and cascading to partners worldwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SMS OTP latency & failure in carrier-fragmented regions | −2.3% | South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| Biometric data privacy concerns under GDPR | −1.8% | Europe with global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SMS OTP Latency and Failure in Carrier-Fragmented Regions

Global spend on SMS OTP exceeds USD 1.6 billion even though delivery rates fall below enterprise thresholds in multi-operator markets, triggering cart abandonment and failed logins. Regulators in Singapore, India and the United States aim to retire SMS OTP by 2025, amplifying urgency for alternatives. NIST now discourages SMS as a secure factor, while leading exchanges such as Coinbase confirm that 95% of account takeovers leveraged SIM-swap attacks. Transition costs may temporarily restrain small businesses, but declining push notification and passkey expenses neutralise the barrier over time.

Biometric Data Privacy Concerns under GDPR

GDPR categorises biometric identifiers as sensitive personal information, compelling explicit consent, and robust safeguards. Divergent definitions in ASEAN jurisdictions complicate cross-border implementations and raise compliance overhead. Smaller vendors face disproportionate legal costs, slowing innovation. Market leaders counteract by adopting on-device biometric matching that prevents server-side storage, alleviating privacy risk and regulatory exposure. Harmonised frameworks, if adopted, could free latent demand and lift the mobile devices user authentication services market trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Authentication Type: Passwordless eclipsing legacy methods

MFA dominated revenue with 55.30% in 2025, reflecting early defences against credential theft. Passwordless now sets the growth pace at 25.20% CAGR, powered by platform-level FIDO support and rising passkey familiarity. The mobile devices user authentication services market size for passwordless flows is projected to reach USD 4.62 billion by 2031, nearly doubling its 2025 base. Hardware security keys, while niche, address high-assurance needs in telecom and defence, expanding at double-digit rates as unit economics improve. Behavioural and passive authentication add continuous verification, reducing user prompts and aligning with zero-trust mandates. Vendors marrying hardware keys with invisible behavioural layers are well-positioned to capture enterprise up-sell budgets.

Fingerprints, facial recognition, and voice match account for the bulk of biometric adoption, yet behaviour-centric models grow faster by embedding in existing mobile SDKs. Number matching and device reputation analytics reduce MFA fatigue, closing an exploit path that attackers manipulate. The combination of these trends repositions the mobile devices user authentication services market as an enabler of seamless digital experience rather than a checkpoint, strengthening the business case for board-level investment

By Deployment Mode: Hybrid models gaining strategic relevance

Cloud Authentication-as-a-Service delivered 59.10% revenue in 2025, driven by rapid SaaS roll-outs and elastic scaling advantages. The hybrid edge-plus-cloud option grows at 22.10% CAGR as regulated industries safeguard data residency while using cloud identity innovation. Organisations deploying Microsoft’s hybrid Kerberos trust model demonstrate latency reductions and policy coherence when authenticating local Windows Hello credentials through both on-premises directory and cloud endpoint. The mobile devices user authentication services market share for on-premise architectures will slide below 14.75% by 2031, yet it persists wherever sovereign data mandates remain strict.

Hybrid adoption follows migration waves: firms lift simple web workloads first, then layer cloud-native FIDO brokers, leaving heritage mainframe authentications on-site until retirement. This staged transition sustains multi-year service revenue for integrators and lengthens average contract duration. Vendors offering policy-driven orchestration across trust planes achieve stickier relationships while minimising rip-and-replace risk for clients.

By Authentication Channel: Push notifications displacing SMS OTP

SMS OTP still delivered 44.20% of 2025 transactions due to ubiquity, but faces a precipitous decline as enterprises cut exposure to SIM-swap fraud. Push authentication expands at 23.20% CAGR thanks to encrypted in-app prompts that require device possession and informed consent. Enterprises incorporate number matching, geo data, and transaction context to blunt MFA fatigue attacks. In-app biometric APIs, once reserved for premium banking apps, now proliferate across retail, gaming, and telehealth.

SIM-based silent network authentication gains momentum in Africa and Latin America, exploiting carrier APIs to verify device legitimacy without user input. Cost advantages over SMS reach 90%, according to Authsignal case studies, freeing budget to invest in higher-assurance factors. Email OTP and magic links remain contingencies for account recovery rather than primary channels, ensuring that the overall traffic mix tilts strongly toward app-centric methods by 2031.

By Enterprise Size: SMEs closing the security gap

Large enterprises captured 63.10% of 2025 revenue based on compliance budgets and complex user estates. Yet SMEs deliver 23.70% CAGR, benefiting from subscription pricing and turnkey deployment. JumpCloud notes that 68% of SME devices still lack biometric capability, signalling runway for vendor growth once mid-range hardware standardises sensors. The mobile devices user authentication services industry has responded with pay-as-you-grow models and low-code integration kits.

BYOD prevalence—90% of employees mix personal and work devices—pushes SMEs to fortify identity layers or risk data leakage. Cloud-native MFA tools reduce operational drag and password reset tickets, translating into tangible ROI that boards can quantify. Consequently, the adoption curve in smaller firms steepens, shrinking the historical security capability gap between enterprise tiers.

By End-User Vertical: Healthcare outpacing traditional leaders

BFSI retained 33.05% revenue in 2025, supported by PSD2, PCI-DSS, and FedNow pressure to harden payment verification. Healthcare and life sciences now outpace all other sectors at 24.90% CAGR as digitised health records and telemedicine expand risk surfaces. The proposed June 2024 HIPAA Security Rule update mandates multi-factor authentication for electronic protected health information, reinforcing the vertical’s technology urgency.

Government agencies embed FIDO2 into citizen portals, while manufacturing scales device-level authentication for industrial IoT. Higher education shows strategic shifts, illustrated by Harvard’s forthcoming switch from Duo to Okta to modernise identity workflows. Each vertical’s unique compliance trigger points foster specialised offerings, deepening segmentation, and giving mid-sized providers scope to differentiate.

Geography Analysis

North America generated 37.40% of 2025 sectoral revenue, anchored by regulatory catalysts like the Cybersecurity and Infrastructure Security Agency Zero Trust Maturity Model that champions continuous verification. Half of U.S. enterprises have already deployed some form of passwordless authentication, creating a reference base that accelerates late-mover adoption. Vendor presence is dense, with Microsoft, Okta, and Yubico shaping standards while niche players pioneer behaviour analytics. Public-sector contracts, notably the Department of Defense FY27 mandate, provide long-term volume visibility and drive spill-over purchases in adjacent civilian agencies. The mobile devices user authentication services market, therefore, remains highly competitive yet expandable as zero-trust programmes scale.

Asia is the fastest-growing theatre at 27.90% CAGR through 2031, propelled by smartphone ubiquity and government digital identity schemes. Chinese OEM integration of advanced biometric sensors combined with India’s Aadhaar-linked payments ecosystem creates massive authentication throughput. ASEAN-5 markets add incremental momentum via e-government and digital banking roll-outs, even though data privacy legislation is still maturing, injecting both growth and complexity. Carrier-backed SIM authentication APIs fill infrastructure gaps in low-bandwidth geographies, enlarging the addressable demand for the mobile devices user authentication services market while embedding telecom groups deeper into the value chain.

Europe balances strict GDPR compliance with rapid SCA uptake. The European Banking Authority’s clarification on digital wallets elevates multi-factor requirements across commerce and sets a playbook that other verticals can emulate. Anticipated PSD3 rules will forbid mobile-only flows, favouring vendors with orchestration engines capable of dynamic factor step-ups. Northern Europe demonstrates highest penetration due to early digital identity schemes, while the United Kingdom, Germany and France post robust growth as Open Banking and eID frameworks mature. Cross-border harmonisation under the forthcoming EU Digital Identity Wallet will unlock new use cases, maintaining Europe as a lucrative yet compliance-heavy segment of the mobile devices user authentication services market.

Regulatory Landscape

Regulation and standards are tightening around phishing-resistant, privacy-preserving authentication, which is accelerating the move away from SMS OTP and standalone biometrics for high-risk mobile transactions. In the United States, NIST SP 800-157 Rev. 1 (November 2024) broadened guidance for Derived PIV Credentials across form factors used by federal staff and contractors, and NIST SP 800-63B-4 (August 2025) formalized updated authenticator management requirements, including support for syncable authenticators and clearer expectations across assurance levels that affect federal and regulated-sector procurement.

Across Europe and Asia, policy and interpretations are reducing ambiguity for passkeys and on-device biometrics while raising the compliance bar for payment and identity journeys. The FIDO Alliance engaged the European Commission DG FISMA in April 2025 to align PSD2/PSR Strong Customer Authentication rules with passkey-based approaches, and South Korea's Personal Information Protection Commission (KPIPC) issued an interpretation in November 2025 that FIDO authentication using on-device biometrics does not require separate consent when biometric data stays on the device, lowering friction for regulated mobile sign-in designs. The United Kingdom government also continues to shape enterprise mobile controls through its cyber security policy guidance on mobile device management (April 2024), reinforcing governance requirements that feed into mobile identity and access implementations.

Value Chain Analysis

The value chain runs from device-rooted security to cloud policy and monitoring. Upstream, silicon and device OEM capabilities such as secure enclaves, trusted execution, and camera and fingerprint modules support hardware-backed key storage that underpins passkeys and device binding, while OS platforms (Android and iOS) expose biometric and key management APIs used by authenticator apps and embedded SDKs.

Midstream, authentication service providers deliver Authentication-as-a-Service, risk engines, and orchestration across MFA, push, passkeys (WebAuthn/FIDO2), and recovery flows. Biometric and behavioral SDK developers supply signal capture and matching components that get integrated into mobile applications. Standards and telecom infrastructure also play a direct role in interoperability and delivery performance. The FIDO Alliance strengthened certification and interoperability scaffolding with Authenticator Metadata Requirements v1.6 (March 2025) and advanced server-side requirements aligned to WebAuthn Level 3 and CTAP 2.3 (February 2026), which supports cross-platform deployments and reduces vendor lock-in risk for enterprises. Downstream, mobile network operators and aggregators provide SMS and emerging silent authentication and subscriber validation capabilities, but they also carry growing security obligations. ITU-T X.1456 (April 2025) adds security guidance for digital financial services, including IMSI validation gateways, and telecom cyber-security rules in markets such as India elevate reporting and network-security expectations, reinforcing carriers as fraud-control nodes while highlighting bottlenecks around signaling security and regional compliance variation.

Competitive Landscape

The mobile devices user authentication services market is moderately concentrated: the top five providers control 45-50% revenue, allowing smaller innovators to carve profitable niches. Platform leaders such as Microsoft and Okta pursue horizontal scale via ecosystem partnerships, embedding identity into productivity suites and cloud platforms. Thales differentiates with a full-stack approach, bundling payment card security and mobile SIM OTA management alongside passwordless 360° launches that emphasise responsible biometrics.

Yubico exemplifies high-growth specialisation, posting 40% CAGR since 2020 by focusing on hardware keys that meet phishing-resistant mandates; a 200,000-unit deployment at T-Mobile validates scalability. Fingerprint Cards AB pairs with Egis Technology to integrate sensors into mass-market devices, securing supply-chain relevance. Carriers such as Millicom target Latin America through a USD 440 million M&A designed to control authentication APIs in bandwidth-constrained environments.

White-space remains in behavioural biometrics, risk-based orchestration, and compliance-as-code. Vendors investing in AI models that continuously learn user context can trim false positives, preserving user experience while tightening security. Hardware-software convergence also accelerates; Swissbit’s combined FIDO and physical access key illustrates product-led expansion into OT environments. As passwordless adoption scales, solution integrability and developer experience will dictate share migration among incumbents and challengers.

Mobile Devices User Authentication Services Industry Leaders

Symantec Corporation

Broadcom Inc. (CA Technologies)

Cisco Systems Inc. (Duo Security)

Microsoft Corporation

Okta Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulator-led retirement of low-assurance factors is creating near-term whitespace for alternatives that keep strong security while reducing friction in mobile authentication. The Central Bank of the UAE set a March 2026 deadline under its 3057 directive to phase out SMS and email OTP for financial transactions, directing banks toward biometrics, FIDO2 cryptographic passkeys, and secure in-app approvals. This expands demand for push-based approvals, device-bound cryptographic authenticators, and step-up orchestration that can be demonstrated in audits.

A parallel opportunity is Europe-based expansion of wallet identity journeys. The European Commission adopted Implementing Regulation (EU) 2026/798 (April 2026), defining standards for remote onboarding to European Digital Identity Wallets at substantial and high assurance, which supports integration demand for mobile authentication services able to back wallet enrollment, re-authentication, and transaction signing while meeting privacy and assurance requirements. Beyond regulatory replacement, infrastructure modernization is also a key lever for scaling passkeys in enterprise settings. NIST SP 800-63B-4 (August 2025) offers a clearer reference point for phishing-resistant MFA in US government-aligned ecosystems, while FIDO technical work in 2026 (server requirements aligned to WebAuthn Level 3 and CTAP 2.3) supports interoperable deployments across apps, browsers, and managed and unmanaged devices. Vendors that package mobile device binding (hardware-backed key pairs in Secure Enclave or Android Keystore), factor orchestration across push, passkeys, and recovery, and compliance evidence for auditors can capture spend as enterprises replace SMS OTP flows and extend passwordless coverage beyond early adopter workforces into customer authentication and regulated transaction use cases.

Recent Industry Developments

- July 2026: Microsoft announced that passkeys became the default sign-in experience in Microsoft Entra ID. This pushes large enterprise tenants toward phishing-resistant authentication at the identity-provider layer, increasing demand for passkey readiness across mobile apps, helpdesk processes, and account recovery flows.

- May 2026: Cisco (Duo) introduced mobile inline authentication for mobile access devices to replace Verified Duo Push. The change concentrates more of the authentication journey inside the mobile flow, supporting lower-friction approvals while tightening control over device-bound context signals used for risk decisions.

- November 2024: NIST published SP 800-157 Revision 1, expanding guidance for Derived PIV Credentials across additional form factors for federal employees and contractors. This update reinforces federal alignment toward stronger, portable credentials and supports downstream adoption of higher-assurance mobile authentication implementations in government-adjacent supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from services and software that confirm a user's identity on mobile endpoints, mainly smartphones, tablets, and wearables, through methods like passwords, one-time passcodes, device-based checks, biometrics, and behavior-based signals.

Scope exclusions: It excludes pure hardware tokens, stand-alone mobile device management tools, and broad identity proofing platforms that are not centered on mobile user authentication.

Segmentation Overview

- By Authentication Type

- Passwords and PINs

- Two-Factor Authentication

- Multi-Factor Authentication

- Biometric Authentication

- Behavioral and Passive Authentication

- Risk-Based / Contextual Authentication

- Soft Tokens and Authenticator Apps

- Hardware Security Keys / FIDO Tokens

- By Deployment Mode

- Cloud-Based Authentication as-a-Service

- On-Premise

- Hybrid (Edge + Cloud)

- By Authentication Channel

- SMS OTP

- Push Notification

- In-App Biometric API

- SIM / Silent Mobile Network Authentication

- Email OTP / Magic Link

- By Enterprise Size

- SMEs (< 1,000 Employees)

- Large Enterprises

- By End-user Vertical

- BFSI

- Consumer Electronics and E-Commerce

- Government and Public Sector

- Telecommunications and IT Services

- Healthcare and Life Sciences

- Manufacturing and Industrial IoT

- Education and eLearning

- Travel and Hospitality

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Nordics

- Sweden

- Norway

- Finland

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Nordics

- APAC

- China

- India

- Japan

- South Korea

- ASEAN-5

- Australia

- New Zealand

- Rest of APAC

- Middle East

- GCC

- Saudi Arabia

- UAE

- Turkey

- Israel

- Rest of Middle East

- GCC

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, select measurable demand signals, and form realistic price and adoption assumptions before we spoke to industry participants. We referred to public sources such as NIST digital identity guidance, ENISA publications, Federal Trade Commission identity theft resources, and authentication related standards and regulatory notes that shape adoption behavior.

We also reviewed supporting evidence from sources such as US SEC filings and annual reports, investor presentations, patent databases, and reputable press coverage on passkeys, MFA rollouts, and mobile security programs. When needed, paid subscriptions were used for structured company financials and news tracking, along with patent lookups, which helps keep vendor coverage consistent across regions. These sources are illustrative and not exhaustive, since many other public documents were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with a mix of authentication service providers, mobile security solution teams, channel partners, and enterprise buyers deploying mobile-first authentication for workforce and customer logins. We used these discussions to confirm what is counted as mobile authentication revenue, to refine pricing behavior (subscription, license, and API usage charging), and to pressure-test regional adoption patterns across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 42% |

| Mid tier: 57% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 18% | Managers: 57% | Americas: 24% |

Market-Sizing & Forecasting

For sizing, a top-down build was used where mobile device installed base trends and digital account activity are translated into an addressable authentication demand pool, then filtered through adoption rates for MFA and passwordless flows. The math stays practical by tying it to variables that can be tracked each year, and then we corroborate the result with selective bottom-up checks using sampled vendor revenue splits, channel feedback, and sampled price per user or price per authentication event applied to plausible volumes.

Key inputs used in the model include smartphone and wearable penetration, the share of active users and employees using protected apps, multi-factor enrollment rates, the shift toward phishing-resistant methods like passkeys, and average price progression for subscription and API-based charging. Where bottom-up views were incomplete in smaller regions or niche industries, gaps were handled by applying validated proxy ratios, such as mobile-first share of total authentication deployments, followed by consistency checks against observed enterprise rollout patterns.

Forecasting was done using scenario analysis supported by trend indicators and expert consensus. Adoption can change quickly after policy changes, major breach events, or platform-level updates to authentication defaults, so growth paths were adjusted by region using differences in compliance pressure, digital banking usage, and enterprise cloud migration timing.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, such as regional enterprise security spending direction, mobile login volume growth patterns, and reported mix shifts toward MFA and passwordless deployments. Outliers are investigated through variance checks on adoption, pricing, and implied revenue per user, then reviewed in a multi-step analyst process before final sign-off.

The study is refreshed annually, and interim updates are triggered when there are material changes such as major regulatory moves, large authentication standard shifts, or notable changes in mobile platform authentication behavior. Before delivery, a final review pass is completed so the numbers reflect the latest available public updates and field feedback.

Mordor Intelligence's Mobile Devices User Authentication Services Market Size Compared With Other Published Estimates

Published market sizes for mobile authentication often look far apart because the boundaries are not the same, even when the wording sounds similar. Differences usually come from what gets counted as a service, whether the scope is mobile-only versus broader IAM, and how pricing and adoption are projected year to year.

The table shows a wide spread mainly because some estimates fold in adjacent security categories or hardware-tied authentication sales, while others assume a slower price decline or a different mix of subscription versus usage-based charges. Currency conversion timing, the base year chosen, and how often assumptions are refreshed can also move the number up or down even when the underlying adoption story is consistent.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.03 B (2025) | |

| Industry Research Publisher A | USD 18.70 B (2025) | This figure appears to use a wider umbrella that likely includes broader identity and access management spend beyond mobile endpoints, and may also bundle adjacent device security or identity platforms, which expands the counted revenue pool. |

| Research Platform B | USD 3.84 B (2025) | This estimate is closer, but it does not clearly state exclusions, and it may include additional identity proofing or non-mobile authentication services in some parts of the definition, which can lift the base-year total. |

The table points to scope as the main gap driver. In Mordor Intelligence's model, revenue is counted only when it is tied to user authentication on mobile endpoints and priced as subscription, license, or API usage, with pure hardware tokens and stand-alone MDM kept out. When the same market is widened to include broader identity stacks or adjacent security categories, the 2025 number naturally moves higher, even if growth expectations are similar.

Key Questions Answered in the Report

What is the current size of the mobile devices user authentication services market?

The market is valued at USD 3.78 billion in 2026 and is forecast to reach USD 11.35 billion by 2031.

How fast is the market expected to grow?

The sector is projected to expand at a 24.62% CAGR during 2026-2031, driven by passwordless adoption, zero-trust programs and stricter regulations.

Which authentication method shows the strongest growth momentum?

Passwordless authentication is advancing at a 25.20% CAGR and is supported by rising passkey familiarity and native WebAuthn support in major operating systems.

Which region will post the highest growth rate through 2031?

Asia leads with a 27.90% CAGR, fueled by biometric hardware in mid-range smartphones and government-backed digital identity initiatives.

Why are enterprises phasing out SMS OTP?

SIM-swap fraud and low delivery rates prompt organisations to switch to push notifications, passkeys and carrier APIs, reducing authentication costs by as much as 90%.

What deployment model are regulated industries adopting most quickly?

Hybrid edge-plus-cloud architectures are growing at 22.10% CAGR because they balance data-sovereignty requirements with cloud agility and reduced latency.

Page last updated on: